First, The Fed’s discount window soared to its highest level since … you guessed it … the previous financial crisis of 2008/2009.

Second, the 10-year Treasury yield declined -16 basis points this morning as investors flee to safety.

Bankrate’s 3-year mortgage rate rose to 7%, but with today’s decline in the 10-year Treasury yield we should see mortgage rates declining.

Yes, much of the blame belongs to The Fed’s leadership (Bernanke, Yellen, Powell) for leaving rates too low for too long, then suddenly try to lower inflation by raising rates. Now we have The Fed’s balance sheet INCREASING again as the use of The Fed’s discount window soars to highest level since Lehman Bros fiasco.

Cry for Argentina! Their central bank boosted its benchmark Leliq rate by 300 basis points to 78%. The monetary authority’s board considered the increase in response to accelerating inflation and after leaving the key rate unchanged for several months.

Of course, the US Federal Reserve is going in the opposite direction to combat the US banking crisis created by inflation and Yellen’s “Too low for too long” Fed policies.

I am beginning to wonder in Treasury Secretary Janet Yellen and Chicago Mayor Lori Lightfoot are the same person. Both complete Statist screw-ups.

So, the Biden Administration made a horrible error by guaranteeing deposits at Silicon Valley Bank for deposits over $250,000. Essentially, Biden bailed out big tech that kept their deposits at SVB.

But what triggered the run on SVB and other banks? Simple. Biden and Congress spent like drunken sailors with Covid and The Federal Reserve went nuts printing money. Viola! We got inflation. But with inflation came The Fed’s attempt to get inflation back to its 2% target (difficult since Biden/Congress refuse to return spending to pre-Covid levels). But as interest rates rise, duration (weighted average life of MBS) rose dramatically meaning that risk increased. But banks like SVP ignored the risk, or didn’t hedge, or were spending time worrying about non-bank related issues.

So, what happened? Banks are holding Treasuries and MBS (orange line) that are getting clobbered with rate hikes (yellow line).

Talk about volatility. Today, the 2-year Treasury yield is up over 20 basis points as bond volatility hits levels last seen in 2008, just prior to the subprime credit crisis.

So, Biden’s bailout of SVP depositors stopped the deposit run for the moment. But if The Fed keeps hiking rates, banks are going to be hurting worse and worse. They could rebalance their portfolios and/or hedge. But with Uncle Spam (Biden) at the helm, bailouts are always on the table.

Now that The Fed-induced-banking crisis has cooled … for the moment … I can focus on that mysterious positive homebuilder sentiment release from yesterday.

The sentiment was driven by 5+ unit (multifamily) starts which were up 24% in February, which 1-unit (single-family detached) starts were up only 1.10%. 23 consecutive months of NEGATIVE real wage growth and still ultra-high home prices begat lots of multifamily housing starts.

The problem for Americans is the real weekly wage growth has been negative for 23 consecutive weeks while home prices remain high, particularly after the Covid bailout by The Fed.

Apparently, the NEO financial crisis (not the subprime, but The Fed’s “too low for too long” crisis) is still with us.

Credit Suisse Group AG’s top shareholder, whose stake has lost more than one-third of its value in three months, ruled out investing any more in the troubled Swiss bank as a bigger holding would bring additional regulatory hurdles.

“The answer is absolutely not, for many reasons outside the simplest reason, which is regulatory and statutory,” Saudi National Bank Chairman Ammar Al Khudairy said in an interview with Bloomberg TV on Wednesday. That was in response to a question on whether the bank was open to further injections if there was another call for additional liquidity.

Credit Suisse says it has identified material weaknesses in its internal control over financial reporting as of December 31, 2022 and 2021, according to the annual report.

The material weaknesses relate to the failure to design and maintain an effective risk assessment to identify and analyze the risk of material misstatements in its financial statements and the failure to design and maintain effective monitoring activities relating to: – Providing sufficient management oversight over the internal control evaluation process to support the Group’s internal control objectives – Involving appropriate and sufficient management resources to support the risk assessment and monitoring objectives Assessing and communicating the severity of deficiencies in a timely manner to those parties responsible for taking corrective action

And it could simply be that Credit Suisse was caught in the Central Bank “Bear Trap” where banks get clobbered as interest rates rise.

Credit Suisse’s CDS (credit default swap) is soaring!

And on the “it ain’t over till its over” news from Credit Suisse, the US Treasury 2-year yield plunged -40.4 basis points.

And the US Treasury 10-year yield plunged -24.8 basis points.

The official logo of the Federal Reserve should be Munch’s The Scream.

Well, the banking fiasco CREATED BY THE FEDERAL RESERVE is still with us. Why? Because the FDIC guaranteed deposits above $250,000 for the first time in history, bailing out millionaires/billionaires. I call this Crony Socialism (but I repeat myself).

Congress doesn’t understand banking, only how to spend money.

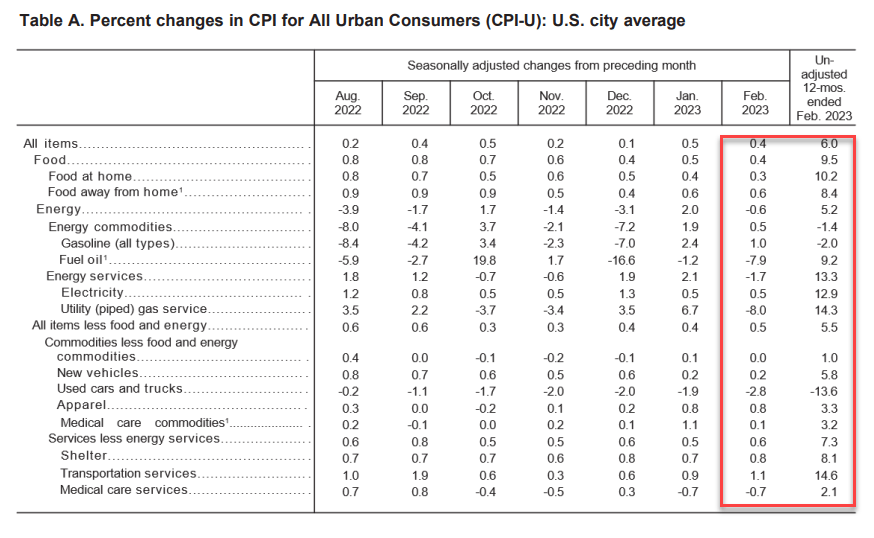

While headline inflation (CPI) came in a 6% (considerably higher than The Fed’s 2% target), core inflation came in at 5.5% year-over-year (YoY), which was expected.

The truly nasty number is today’s inflation report is that weekly earnings YoY remained the same at a terrible -1.9%. Meaning that inflation is higher than nominal wage growth. This is the 23rd straight month of negative real weekly earnings. Well done, Fed and Biden!

Food is up 10.2% YoY. Electricity up 12.9%, shelter up 8.1%.

On the news, the US Treasury 2-year yield rose 34.3 basis points.

Somehow I doubt that Biden’s press secretary will tout 23 straight months of negative weekly earnings growth as one of Biden’s economic accomplishments.

You must be logged in to post a comment.