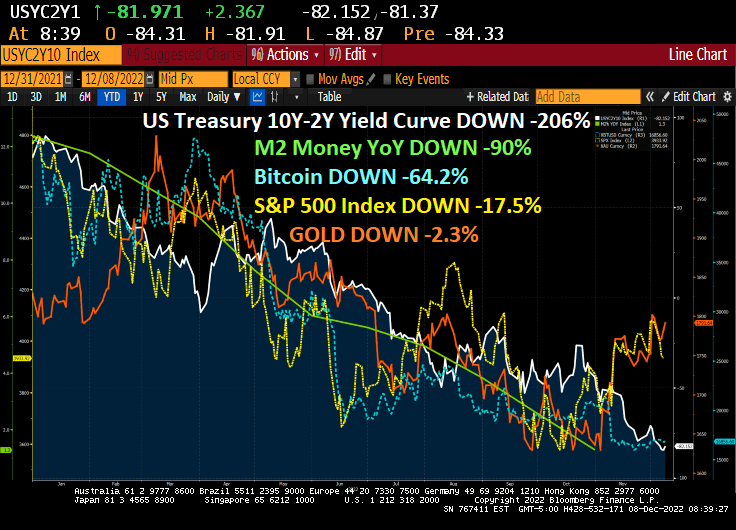

Apparently, despite the denials from the Biden Administration, someone at Bureau of Labor Statistics or someone in Congress or the Federal Reserve or the Biden Admininstration itself likely tipped the wink on the soft CPI report on Tuesday.

Treasuries were well on the front-foot in the lead up to the below-estimate November CPO print, as a surge of buying took place seconds before the official 8:30 am New York release time. Over a 60 second period before the data, 13,518 March 10-year futures traded as the contract moved from 114-04+ up to 114-22. Gains were then extended up to 115-11 session highs once the data was released.

On the equity side, stock futures suddenly spiked more than 1%. Trading in Treasury futures surged, pushing benchmark yields lower by about 4 basis points. Those are major moves in such a short period of time — bigger than full-session swings on some days. And they should get scrutinized by regulators, long-time market observers say, even if a leak is only one of several possible explanations for why traders suddenly started buying right before the report was published.

Remember that current Treasury Secretary Janet Yellen was accused of leaking information to a NY hedge fund ahead of the Fed Open Market Committee meeting? And then we have the Wolf of Wall Street.

I wonder if the REAL Wolf of Wall Street did this?

You must be logged in to post a comment.