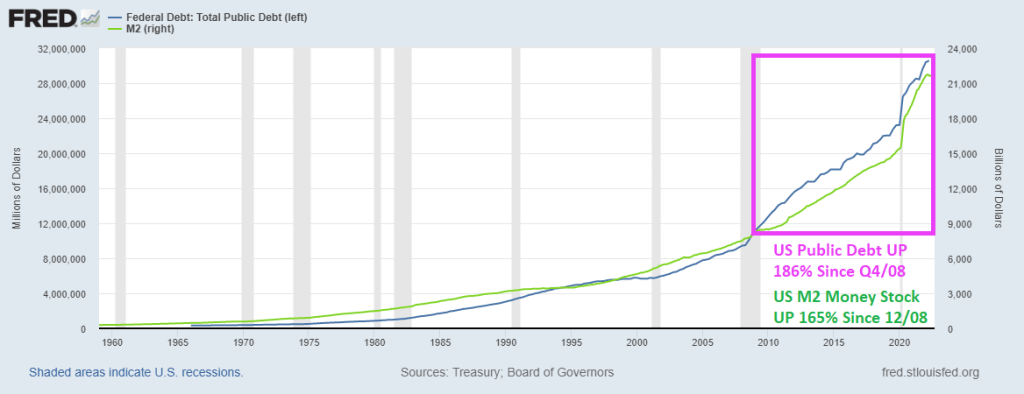

Ever since the financial crisis of 2008 and the election of President Obama and a Democrat Congressional sweep, the US has embraced Modern Monetary Theory (MMT or borrow, print and spend without consequence). And between the financial crisis and the Covid crisis of 2008, we have seen an increase in US public debt from $10.7 trillion in Q4 2008 to a staggering $30.6 trillion as of Q2 2022. That is a staggering increase of 186% in only 14 years.

How about US Money stock? M2 Money stock has grown by 162.5% since the beginning of 2009 and the “Blue Wave” of 2008. And nothing has been the same.

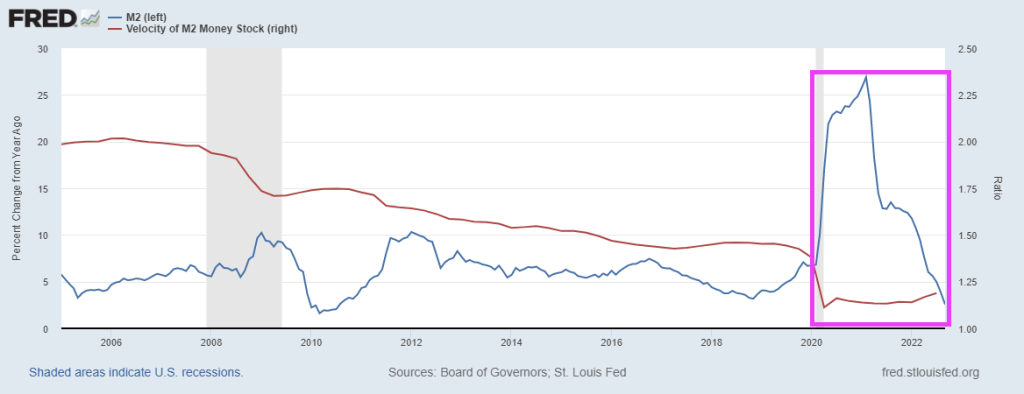

The Covid outbreak in early 2020, we saw Fed money printing that has never seen before … or since. But one thing is for sure, M2 Money Velocity (GDP/M2) is near all-time lows.

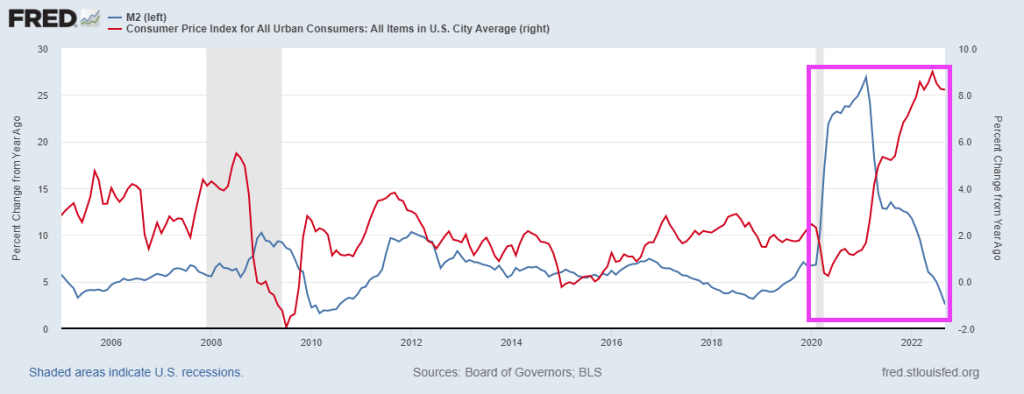

Then we have headline US inflation as a function of M2 Money growth YoY.

To paraphrase Alexander Dayne from Galaxy Quest, “They broke the financial system, they broke the bloody financial system!”

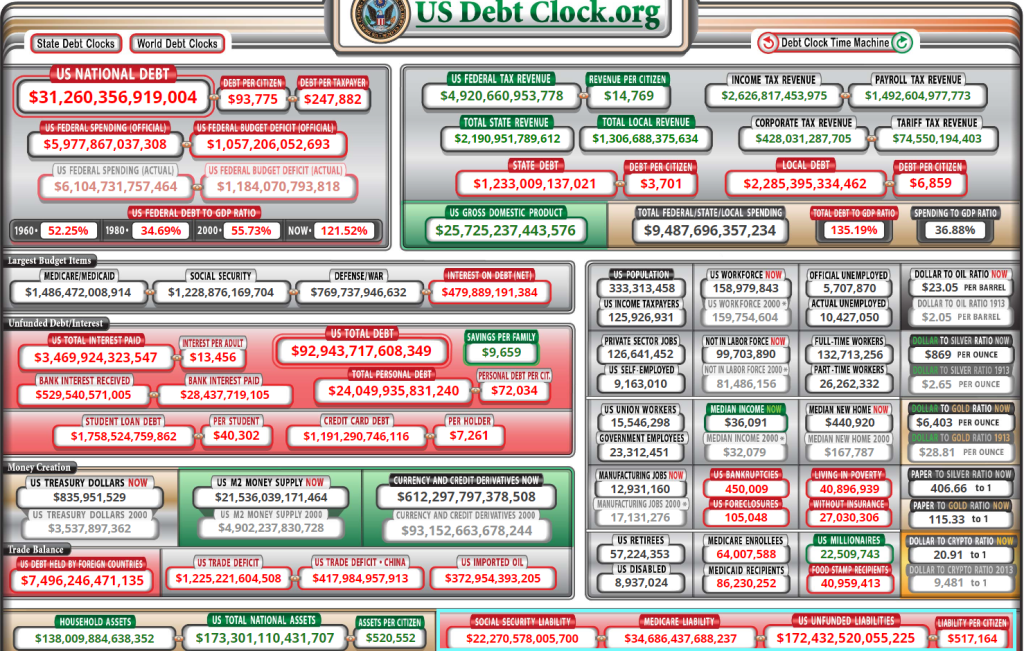

And it is the midterm election “silly season” where no politician will discuss the complete and utter mess they have made. According to US Debt Clock, US national debt is already up to $31.26 trillion (OMG!), but the REALLY scary number that not a single politician will address is UNFUNDED LIABILITIES OF $172.4 TRILLION.

Can we go back to the gold standard? Or silver standard? Or ANY standard for that matter??

Instead, we have porous borders and patently UNSOUND money, thanks to MMT.

You must be logged in to post a comment.