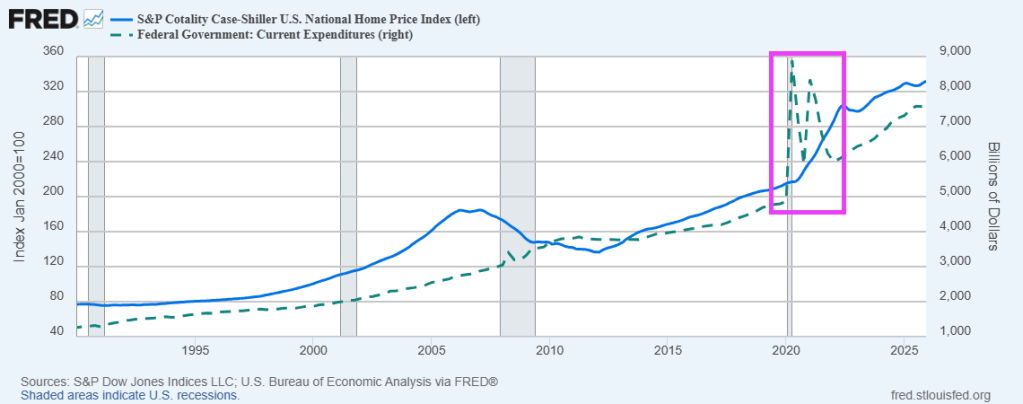

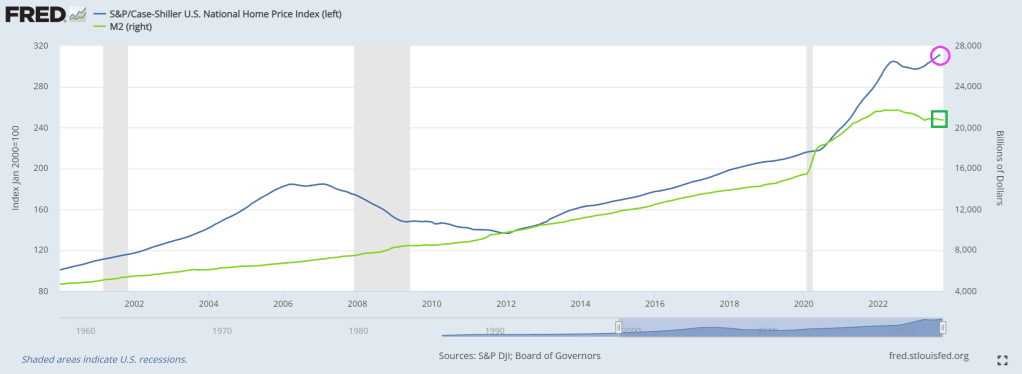

We are seeing the aftermath of the Federal government’s fiscal response to the Covid outbreak of 2020. Home prices exploded following The Federal government’s spending spree. The end result? US housing is simply unaffordable for millions of households.

Not really surprising given the soaring home prices following the Covid Federal spending spree.

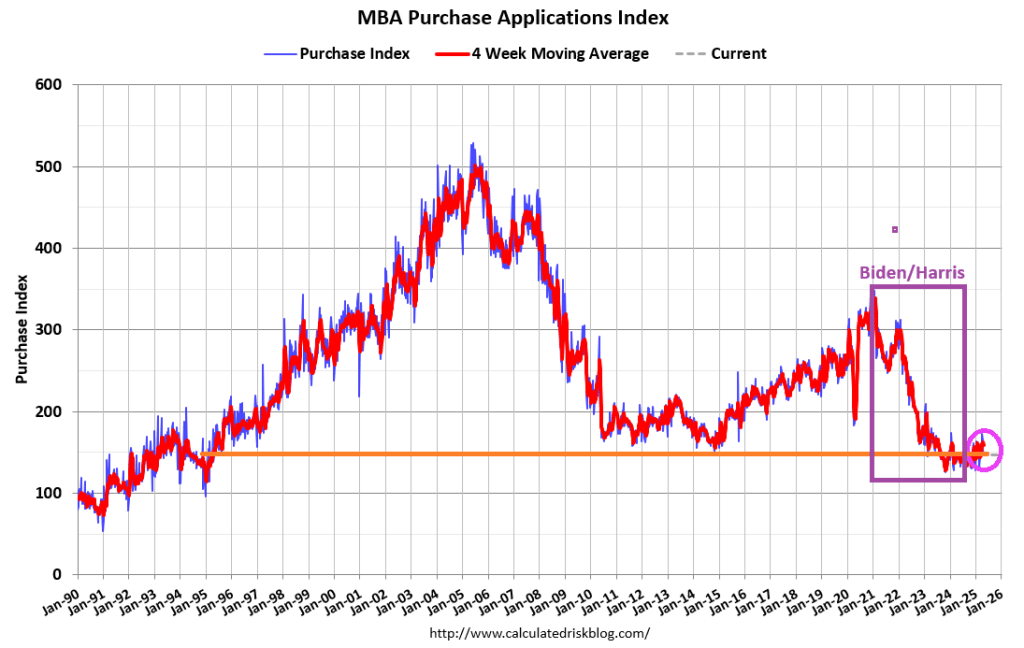

Mortgage applications decreased 4.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 25, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 3 percent higher than the same week one year ago.

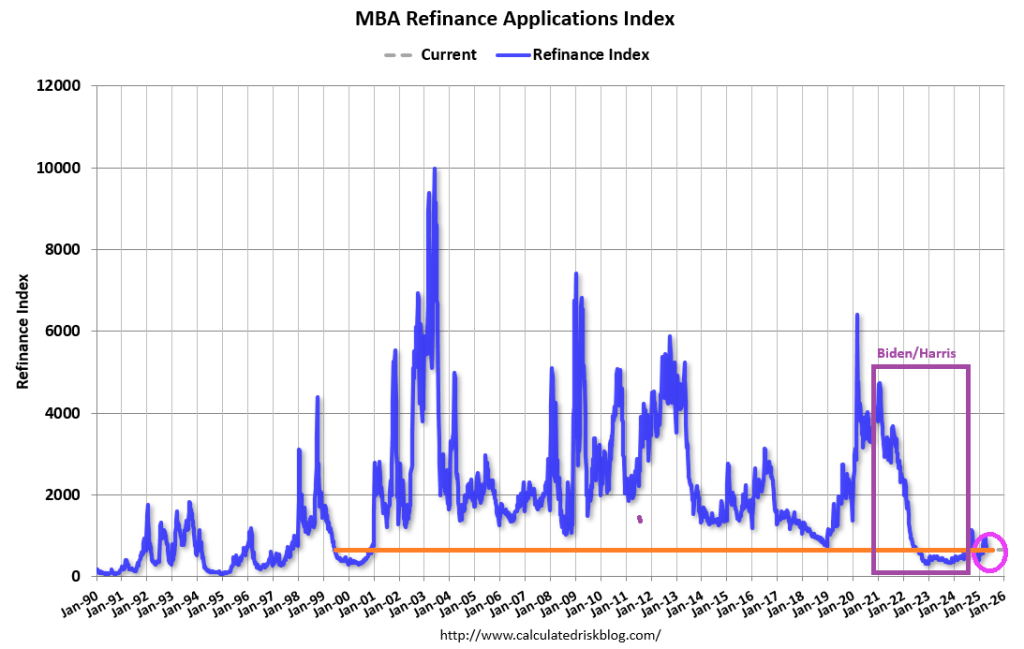

The Refinance Index decreased 4 percent from the previous week and was 42 percent higher than the same week one year ago.

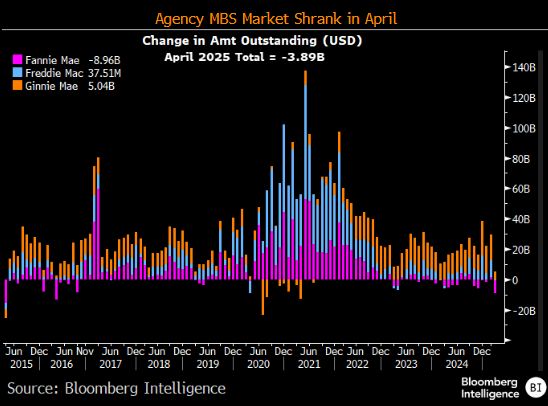

The Agency MBS market shrank in April.

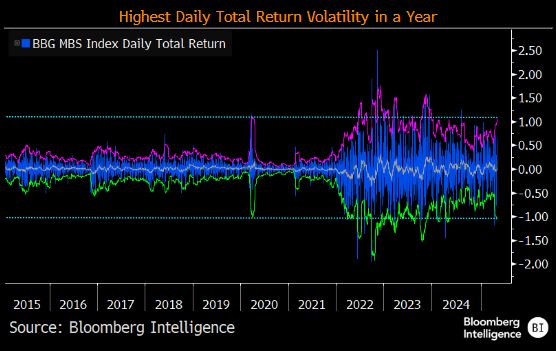

And MBS daily returns have the highest return volatility.

Joe Biden could barely eat his dinner at the White House Correspondents’ Dinner. And we think he is calling the shots in The White House?? Oh well. Perhaps it is Treasury Secretary Janet Yellen or Klaus Schwab of the World Economic Forum.

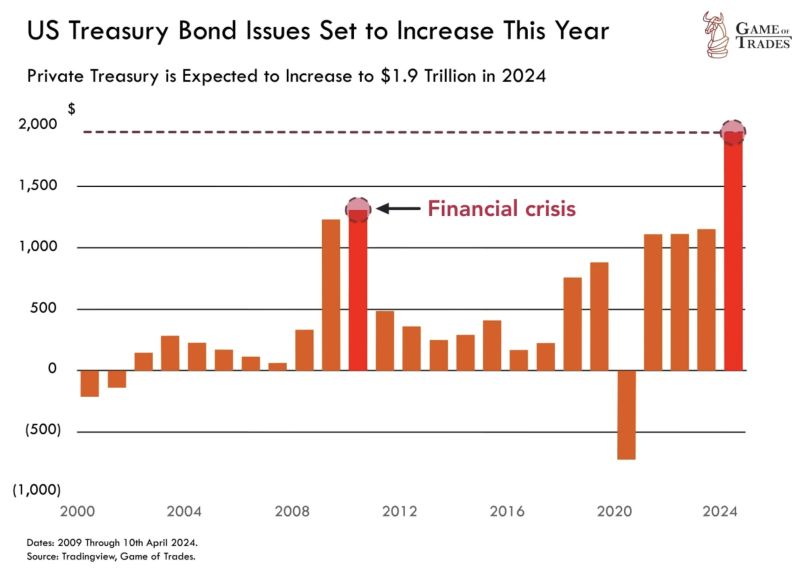

In any case, Treasury bond issuance in 2024 is expected to hit $1.9 TRILLION. Surpassing levels seen even during the 2008 financial crisis.

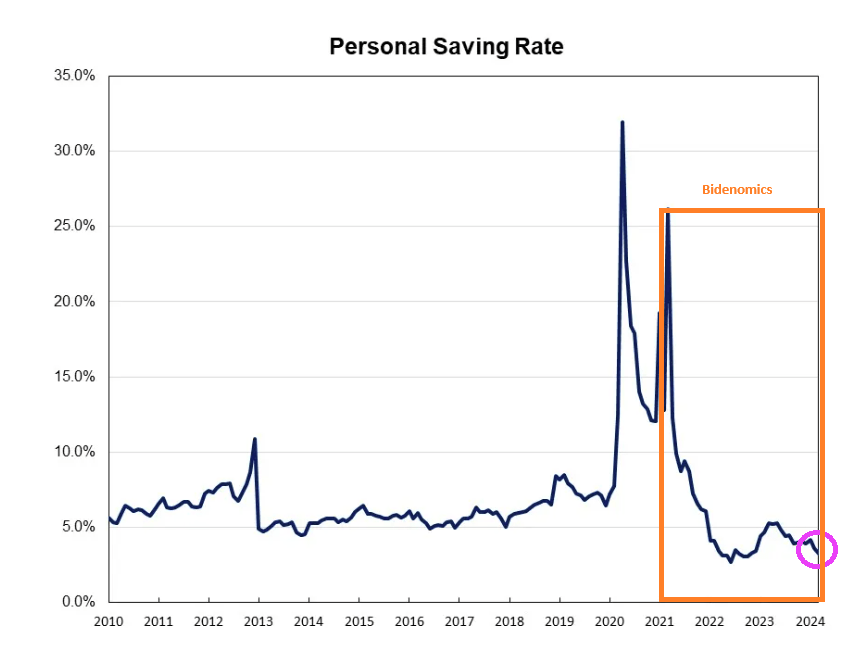

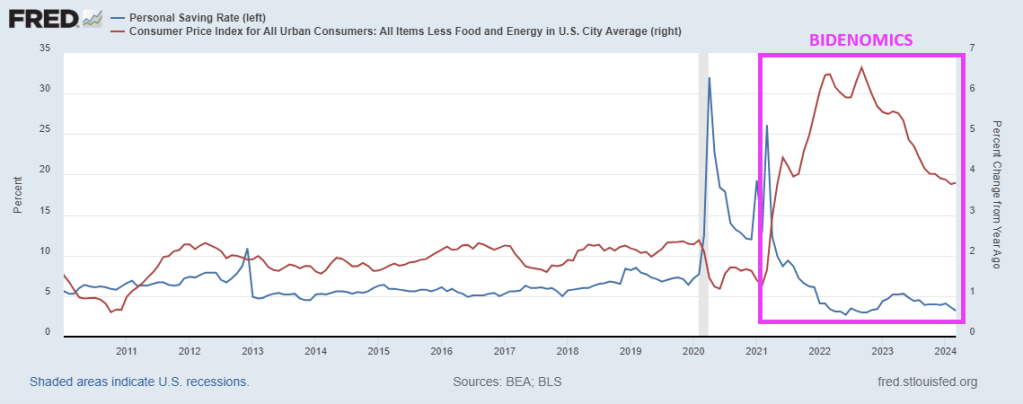

And with inflation, the US personal saving rate is near the lowest level since Obama (2010).

And with the core inflation rate still higher than anytime since 2010, households are paying more for … everything depleting their savings.

With Biden and Congress spending like drunken sailors on shore leave, and no end in sight, this will eventually explode. Ukraine, foreign aid, no border security, virtually no money for Maui fire, E. Palestine Ohio is still a wreck, etc. They always have money for someone else. And if Trump is elected in November, watch CNN and MSNBC and Biden/Congress blame Trump.

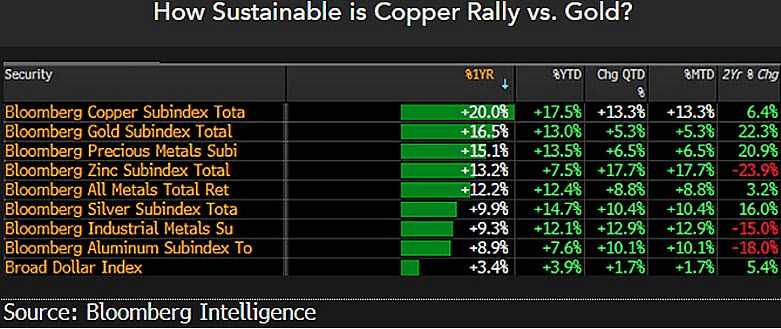

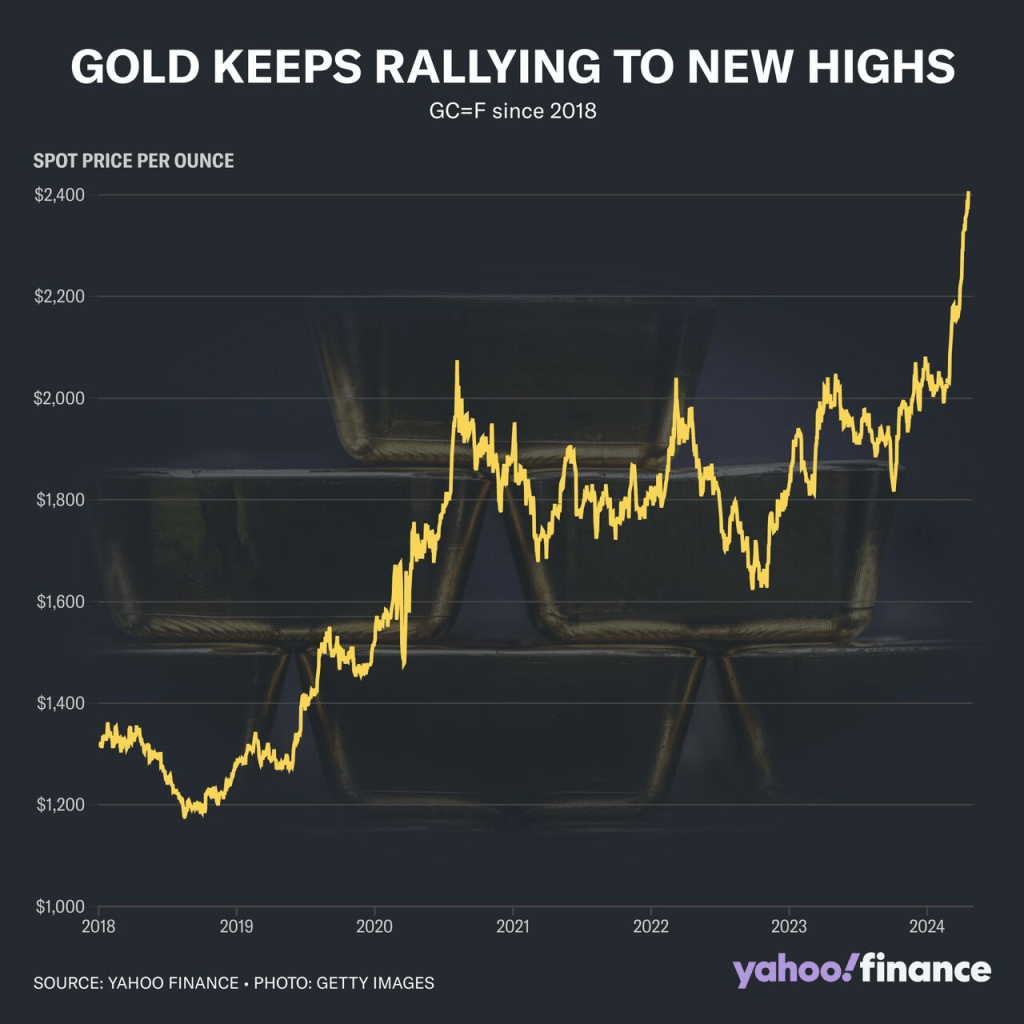

Commodities are a way to protect yourself against the government and their insane spending and debt.

My point? Gold keeps rising!

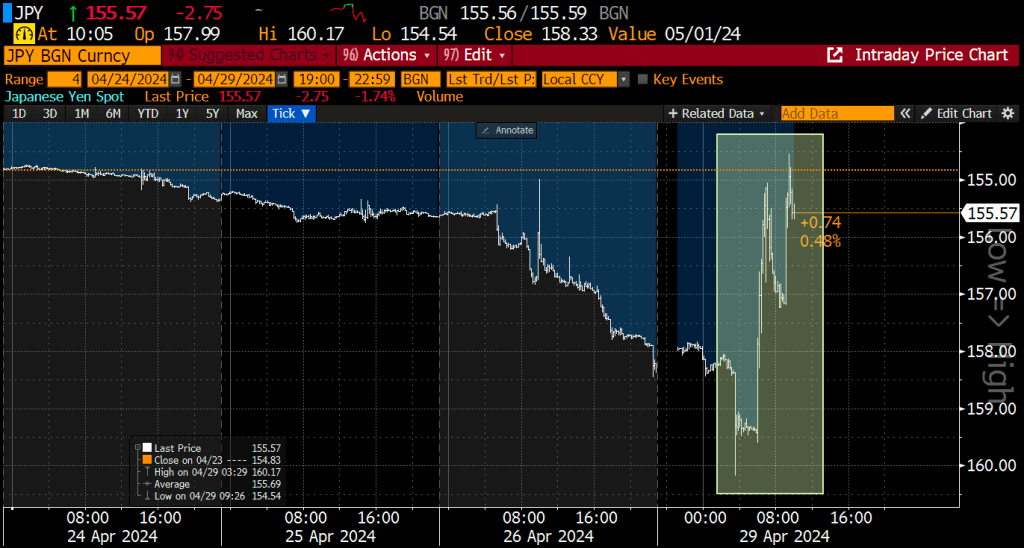

The leading foreign holder of US debt is Japan, which is following the insane path as the US and resembles a banana republic.

Former Fed chair under Obama and current Treasury Secretary Janet Yellen under Biden is Doctor Wonderful. NOT!!

I don’t know what Biden thinks is so funny. Maybe it is because House “Majority” Leader Mike Johnson (RINO-LA) gave Biden and Schumer everything they wanted (Ukraine, Israel funding but nada for security our borders). Life is good when you are stupid and mean-spiritied like Joe Biden!

Biden is so vain: capped teeth, hair plugs, constant tan, face lifts, etc.

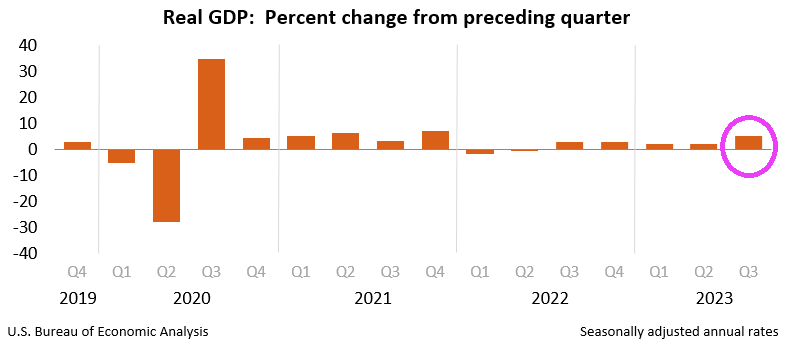

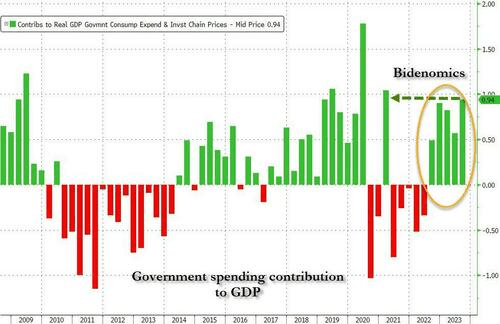

As expected, Q3 Real GDP was revised upwards to 5.2% annualized. Of course, this shatters JKP’s talking points that Biden inherited a train wreck of an economy from Trump. Q3 2020 Real GDP grew at over 30%.

And on a year-over-year (YoY) basis, US real GDP grew at 3.0% in Q3. Unfortunately, real hourly compensation grew at a measly 0.6% YoY.

Meanwhile, home prices have hit an all-time high. Too bad real wages are so low.

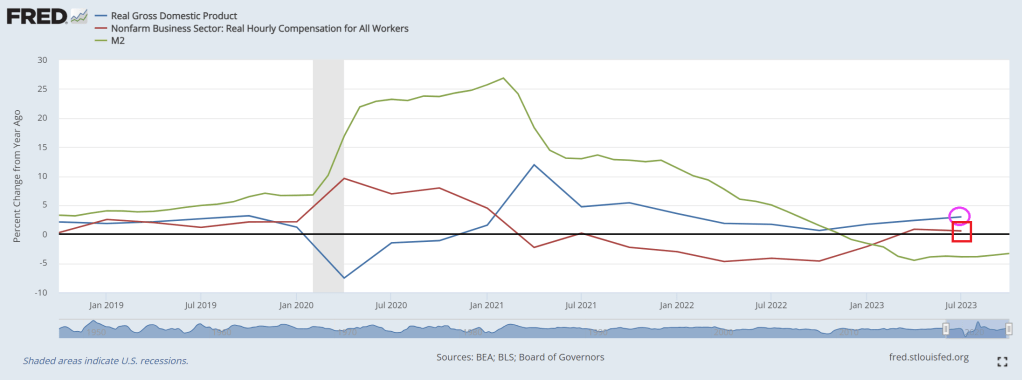

Why is growth so strong? One factor has been government spending which grew an unsustainably 4.7% in real terms over the last year. Outside the pandemic, this is one of the fastest rates in decades and works at a cross purpose with monetary policy objectives.

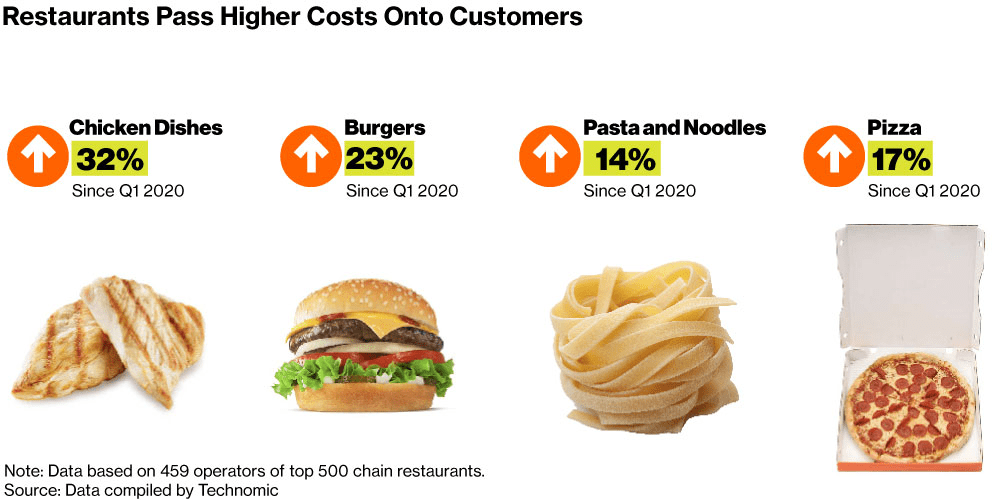

Despite Biden/KJP’s ridiculous lies about about this Thanksgiving being the 4th “cheapest” in history, inflation while cooling is still way up under Biden. In fact, food prices are up 25% since 2020.

Since 2020, US groceries are up 25%, used cars climbed 35% and rents roughly 20%. In 2020, a survey showed a 4-person household spent an average of $238.32 in a week on food at home. A similar survey in 2023 showed that figure had jumped 32% to $315.22.

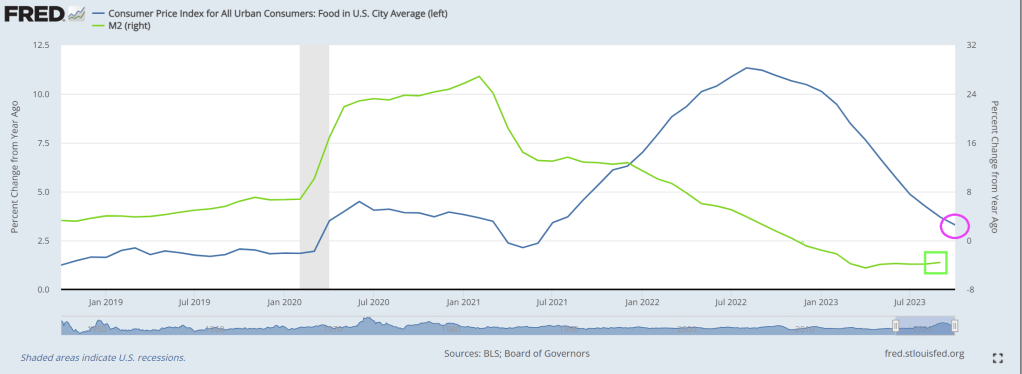

Notice that food CPI peaked at 11.33% in August 2022 and has been declining since as M2 Money growth dies.

Of course, Biden blames high prices on … anyone but himself and big spending Congress. “Biden admits prices ‘too high’ but blames sellers for 18% inflation.” Sure Joe, the big spending bills you championed as part of Bidenomics that helped surge M2 Money supply (green line) has nothing to do with price increases, just the evil private sector.

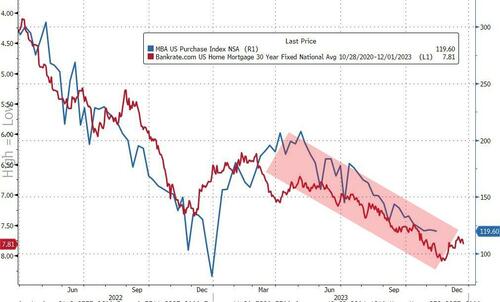

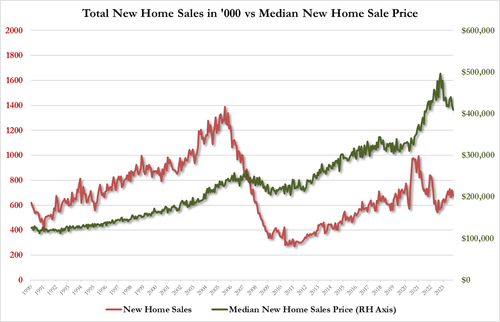

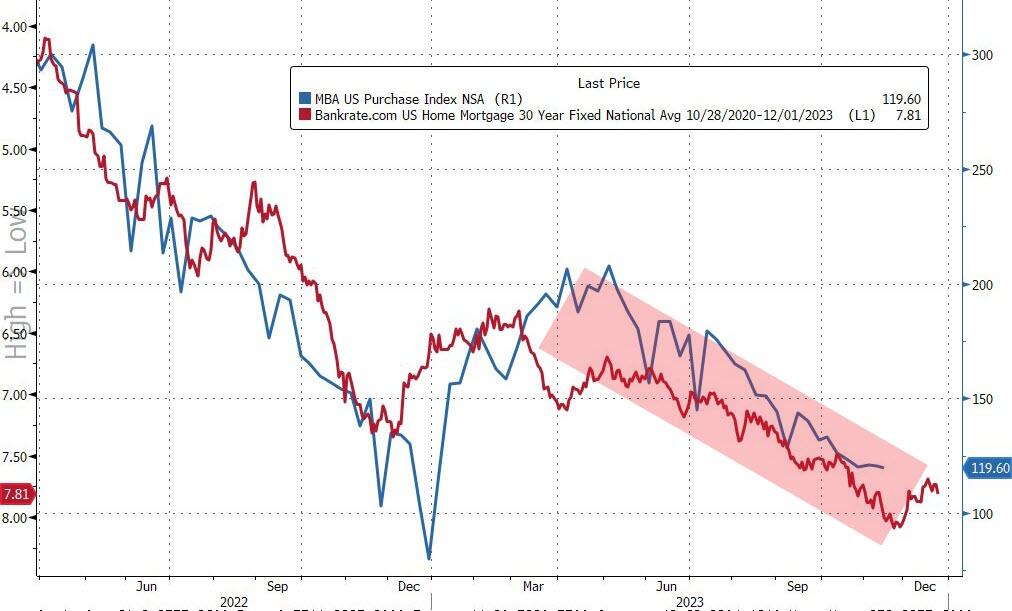

As a reminder, The Mortgage Bankers Association’s index of home-purchase applications tumbled to 120 – the lowest level since 1995 – as mortgage rates hit 8% for the first time in 23 years in October.

Source: Bloomberg

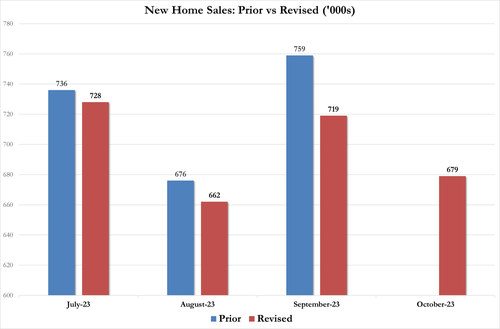

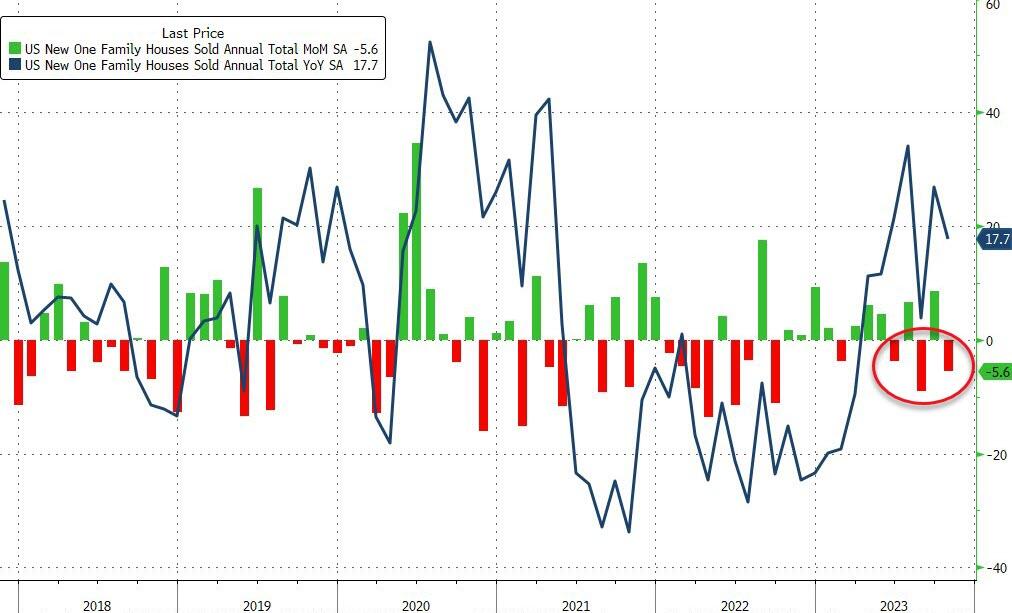

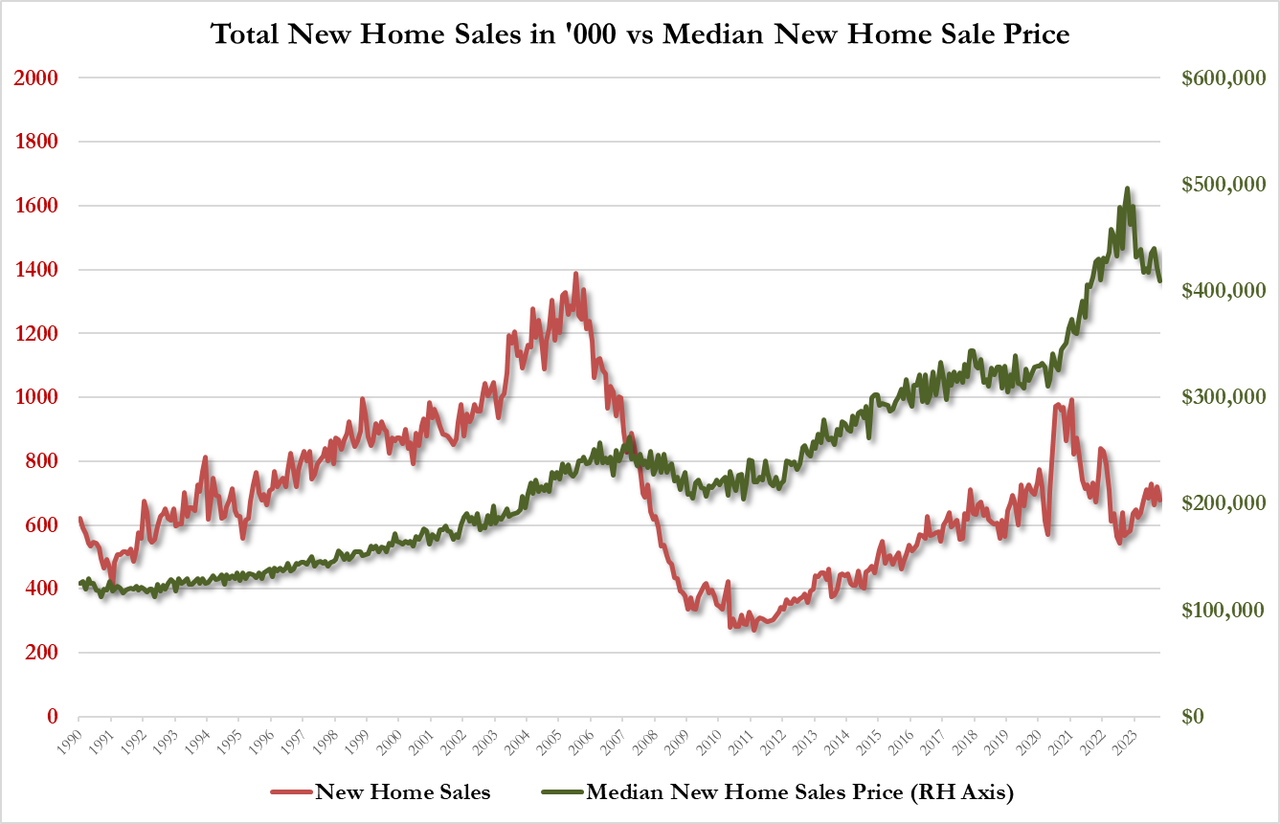

So, it should be no surprise that new home sales were even worse than expected, plunging 5.6% MoM (and making it even worse, the 12.3% MoM jump in Sept was revised down to +8.6%)…

Source: Bloomberg

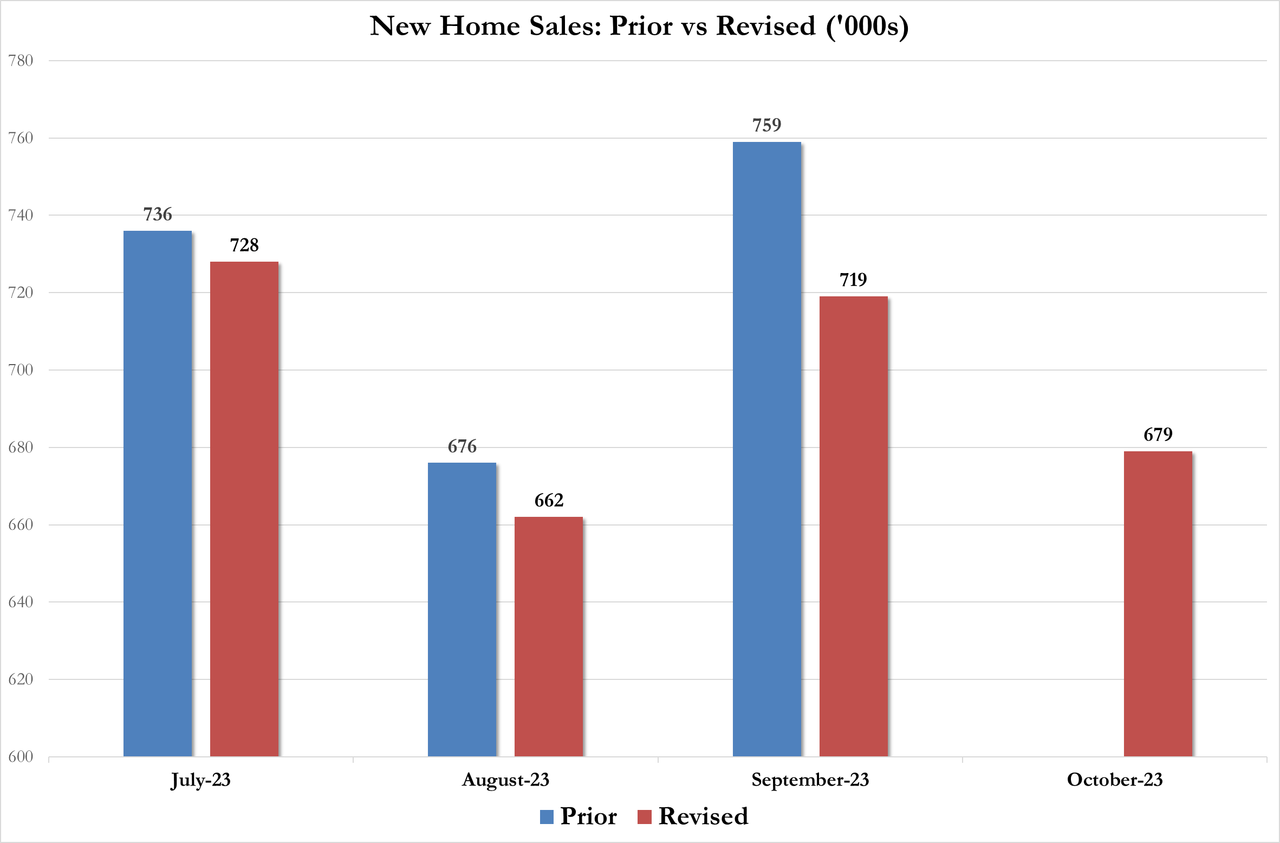

The trend of downward revisions continues…

The New Home Sales SAAR of 679k is flat from April (that was below all economists’ forecasts)…

Source: Bloomberg

It appears the homebuilders finally hit their wall eating the gap between these two lines was just not sustainable…

Source: Bloomberg

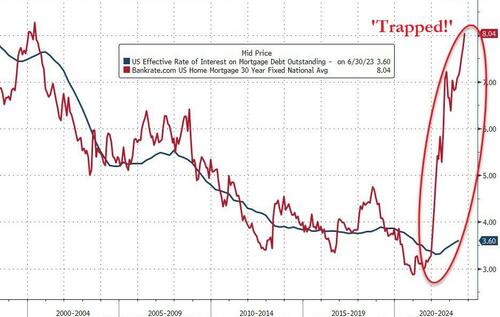

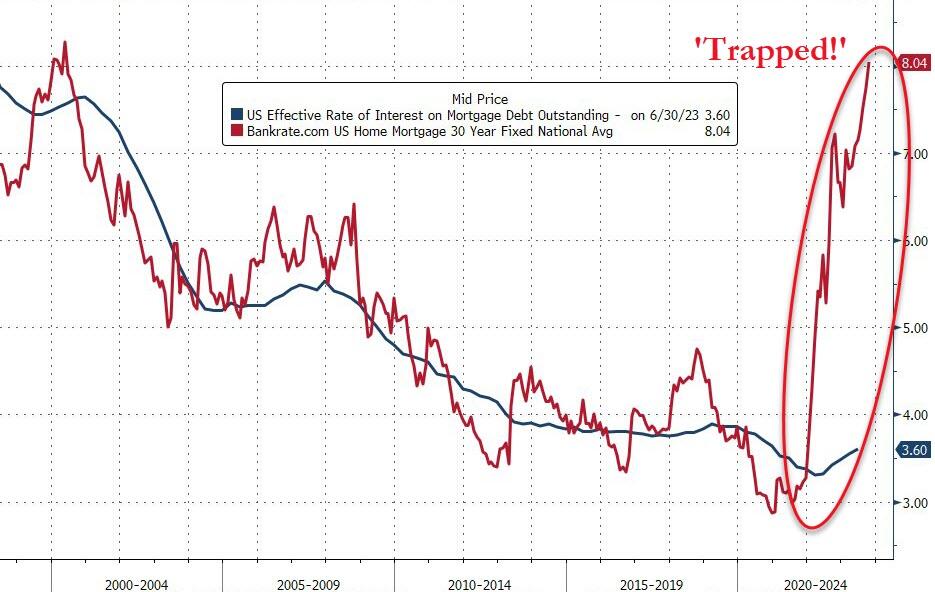

And as we noted previously, homebuilders can’t be filling this gap either – between the current 30Y mortgage rate and the effective rates that borrowers are currently paying on their home loans – (i.e. subsidizing new home sales) forever…

Source: Bloomberg

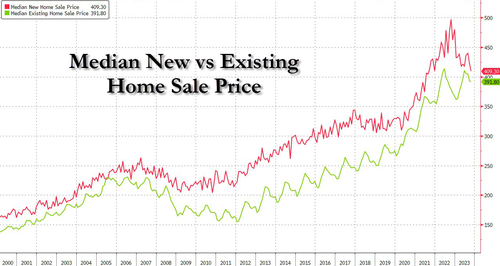

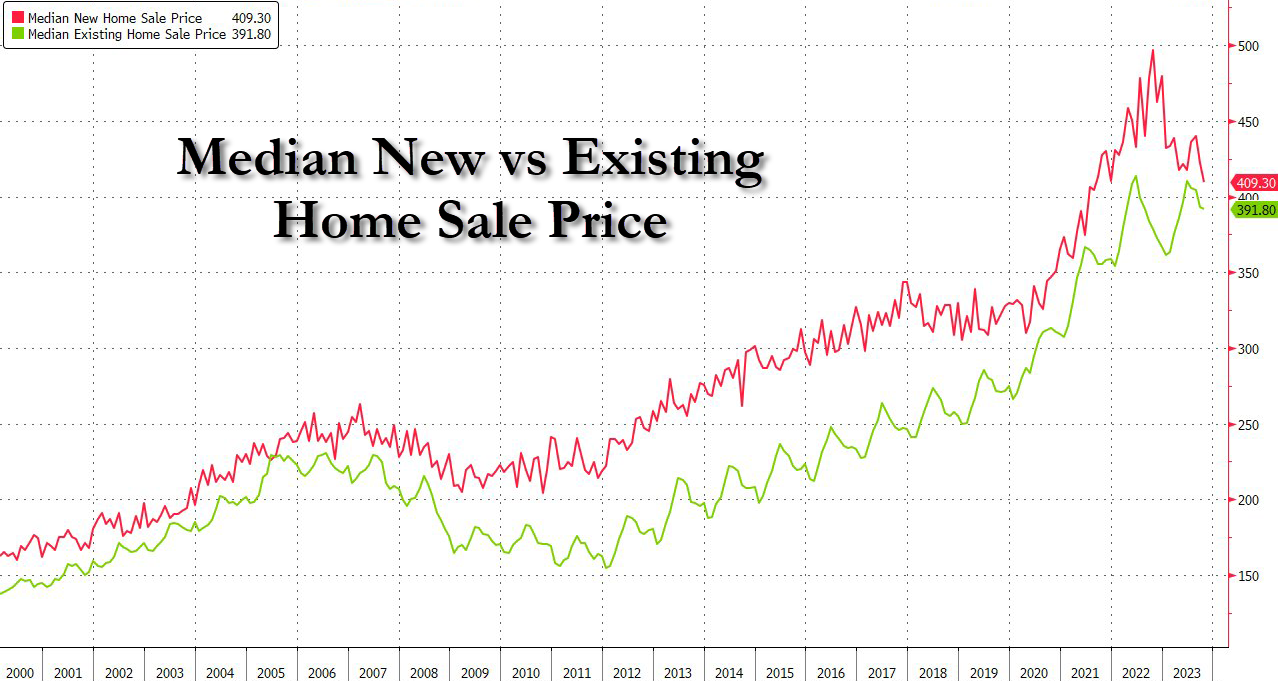

The median new home price fell 17.6% y/y to $409,300; average selling price at $487,000

That is the lowest median price since Aug 2021, catching back down to existing home prices…

Source: Bloomberg

Is Powell winning his war on affordability? Or crushing the middle class’s main source of wealth? Or is it Hammer Time??

The World Economic Forum (WEF) is a leading pusher of the ESG drug, pushed by the elite class intending to control the world. Unfortunately, numerous American politicians and influencers have attended the Davos meetings and have openly praised the WEF and its leader Klaus Schwab.

ESG investing, or sustainable responsible investing (SRI), uses this information about a company to inform investment decisions that prioritize all stakeholders.

Here’s how the Forum’s partners are leading the switch to stakeholder capitalism.

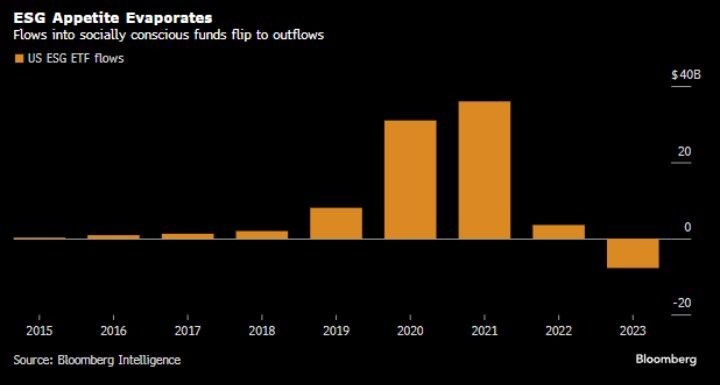

But all is not well with WEF’s ESG drug distribution. In fact, ESG flows into socially consious funds were a big thing during Covid (2020) and the first year of Biden’s Reign of Error. But ESG flows slowed sharply in 2022 and seeing net outflows in 2023.

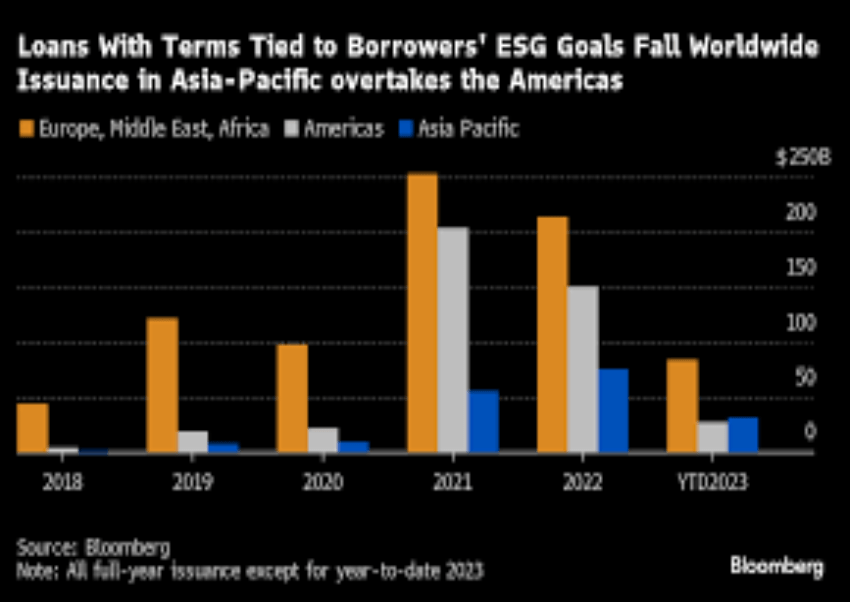

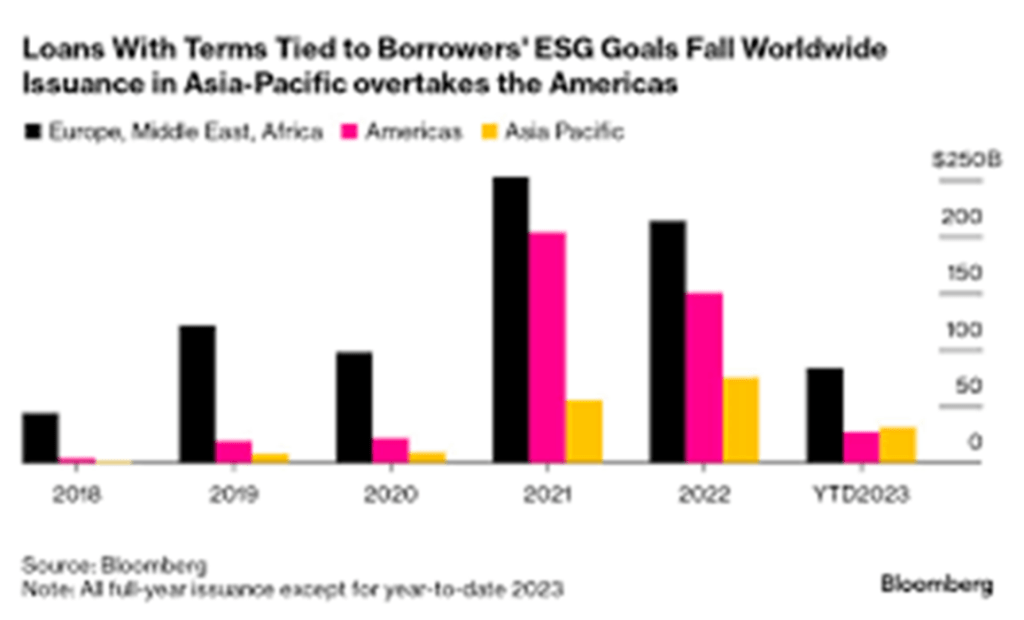

US borrowers are retreating en masse from the world’s second-biggest ESG debt class.

The $1.5 trillion market for sustainability-linked loans, in which borrowing is tied to environmental, social or governance goals, has seen an overall slowdown in volumes this year as both interest rates and greenwashing fears rise. But nowhere has the decline been as precipitous as in the US, where the number of new sustainability-linked loans is down 80% from a year earlier.

But ESG is still relatively popular in Europe, Middle East and Africa (orange). But taste for ESG is waning around the globe. But the selection of Biden as President in the US marked a surge in ESG -tied loans in 2021 and 2022 (not to mention the insane levels of spending out of Biden and Congress, much tied to the sustainability, green energy fantasy.

Loans with terms tied to borrower’s ESG goals have fallen worldwide.

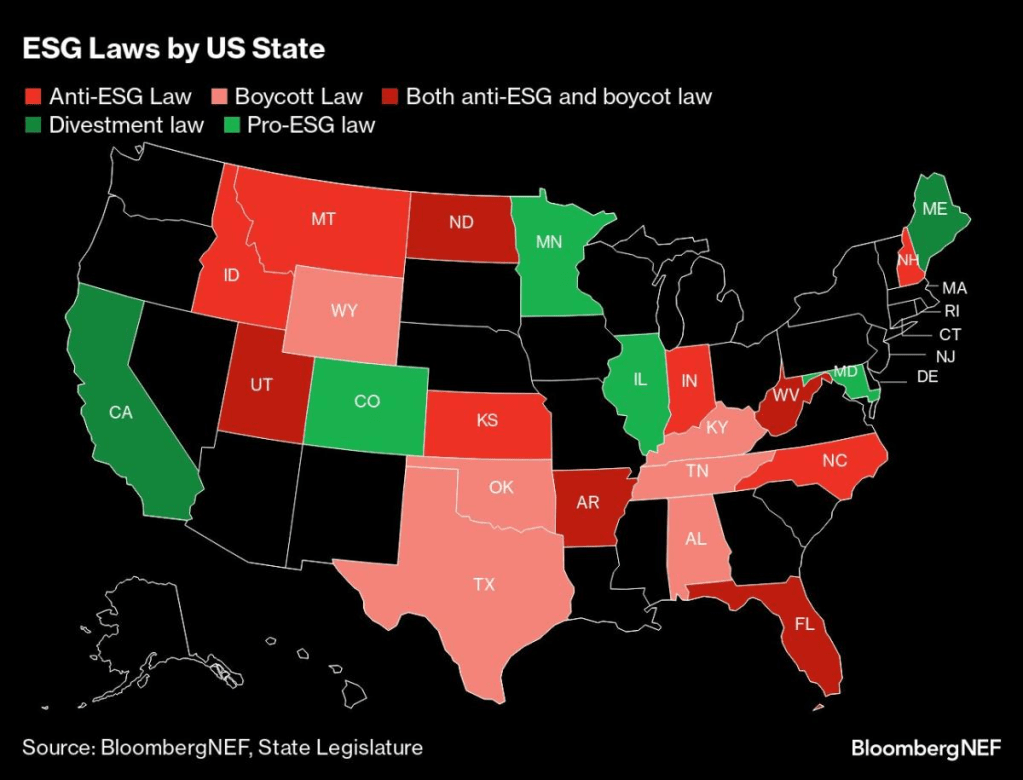

Several states (largely blue states like California, Minnesota, Illinois, and Colorado have pro-ESG laws) while several states have anti-ESG laws (largely red states like Montana, Idaho, North Dakota, Kansas, Utah, Indiana, Arkansas, Florida, and West Virginia).

And of course, global warning may not be as dire as John Kerry and Greta Thunberg say.

WEF’s Klaus Schwab about to get sniffed by his 80-year old puppet, Joe Biden. In fact, Biden is singing “I’m your puppet.”

Here is Hunter Biden welcoming the Green Energy fairy and all the trillions in misallocated spending it brings.

Even eating breakfast under Bidenomics is more expensive. Particularly if you like orange juice like I do. To save money, I am probably going to have to switch to nasty-tasting Tang.

Food CPI is up 3.69% year-over-year. The rate of growth in food prices is slowing. But do I trust BLS data on CPI? Of course not.

Orange juice prices are up 47% under Biden.

And we see that REAL GDP is growing at a slower rate than nominal GDP.

Speaking of Bidenomics, here is an interesting Zero Hedge story on “The Biden-Du Pont Nexus: From A Prestigious Golf Club To A Controversial Child Rape Plea Deal.” What is it with Delaware elites having sex with their children?? And why is NY AG Letitia James prosecuting Donald Trump when there has been no crime while she let’s Epstein’s clients who flew to have sex with minors (used to be illegal) off the hook?

But I feel good! After my breakfast of … Scotch Broth. OJ is just too expensive.

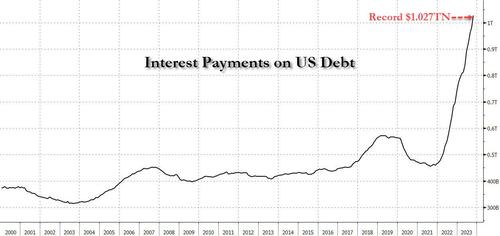

$1.027 trillion in interest is calculated by multiplying the average interest rate on marketable US Treasury debt (which according to the Treasury is 3.096% as of Oct 31) by the $26.003 trillion in marketable US debt (as of Oct 31) which nets off to $805 billion, and adding to this non-marketable debt interest (which as of Oct 31 was 2.884% multiplied by the amount of non-marketable debt which is $7.696 trillion) and which in turn is an additional $222 billion in interest. Add across and you get $1.027 trillion.

Naturally, this calculation of estimated real-time interest costs – which is entirely based on Treasury data – is different than what the Treasury actually paid. Interest costs in the fiscal year that ended Sept. 30 ultimately totaled $879.3 billion, up from $717.6 billion the previous year and about 14% of total outlays, however that number is merely lagging what the pro forma print currently is, and will inevitably catch up to it, and then lag on the other side even as pro forma interest payment start dropping (once interest rates plunge after the next QE/YCC is launched).

Fans of exponential functions, we got you covered: the unprecedented surge in both interest rates and interest expense in the past two years means that total US interest has doubled since April 2022 and that’s with the inherent lag in interest catch up – as a reminder, the vast majority of 5, 7, 10 and 30 year debt is still locked in at much lower interest rates, and as such, rates will continue to rise as all of the existing debt rolls into much higher rates over the coming years.

Looking ahead, the staggering surge in both yields and total long-term Treasuries in recent months confirms the government will continue to face an escalating interest bill. As a reminder, we were the first to point out that it took just one month after US federal debt first rose above $33 trillion for the first time, to spike by another $600 billion.

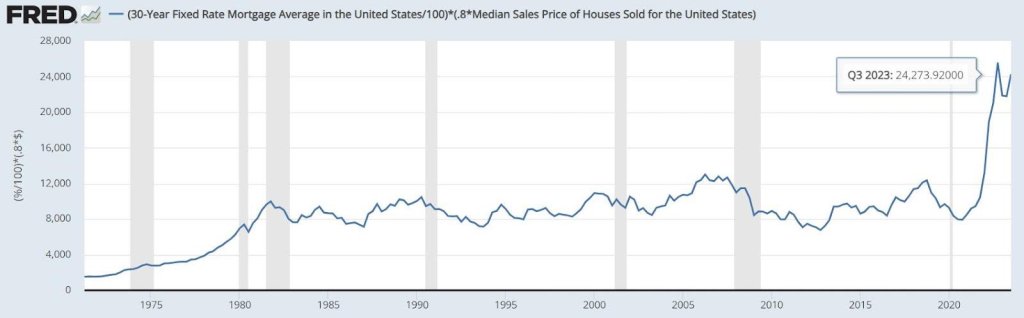

On the personal finance side, annual Interest payments on a 30-year, fixed-rate mortgage before Biden was $8,500, but after Biden it almost tripled to $24,300! That means that annual mortgage interest rose 186% under Biden.

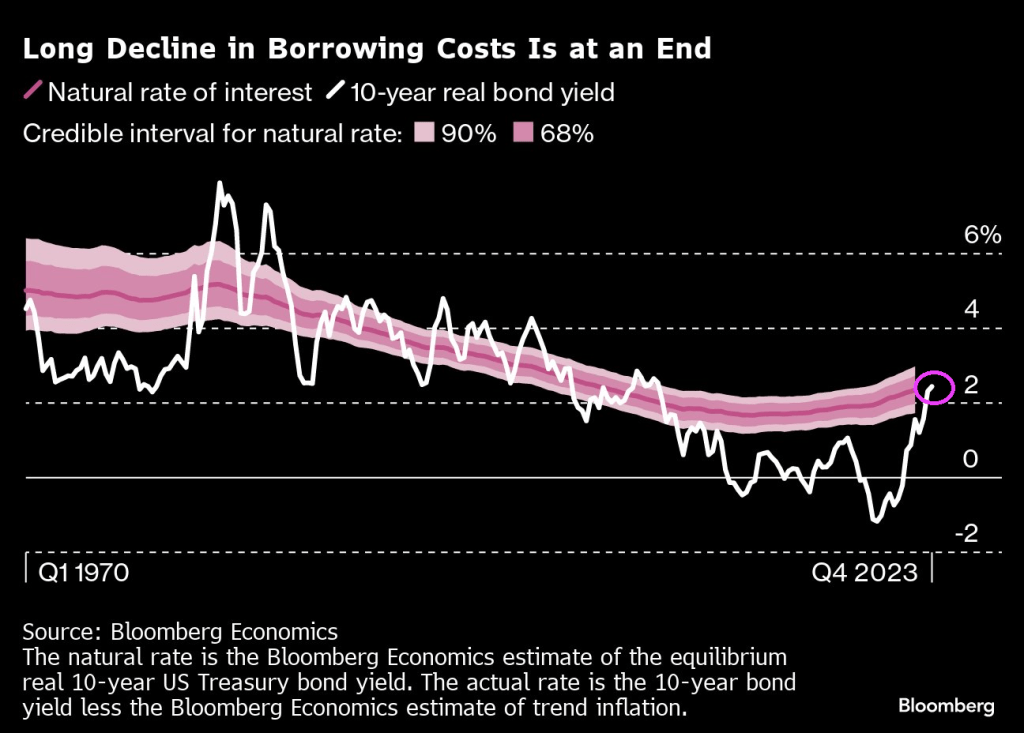

But on the middle class front, we can see “cheap rates” are a thing of the past as markets have to deal with Biden’s inflation problem and Fed rate hikes.

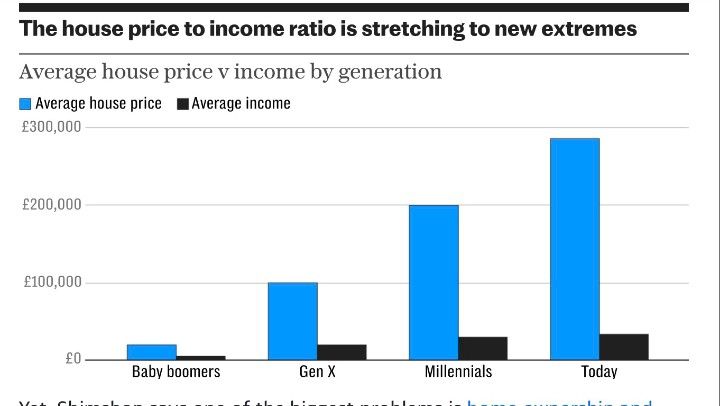

And with rising home prices under Biden, the house price to income ratio is out of control and causing pain for the middle class.

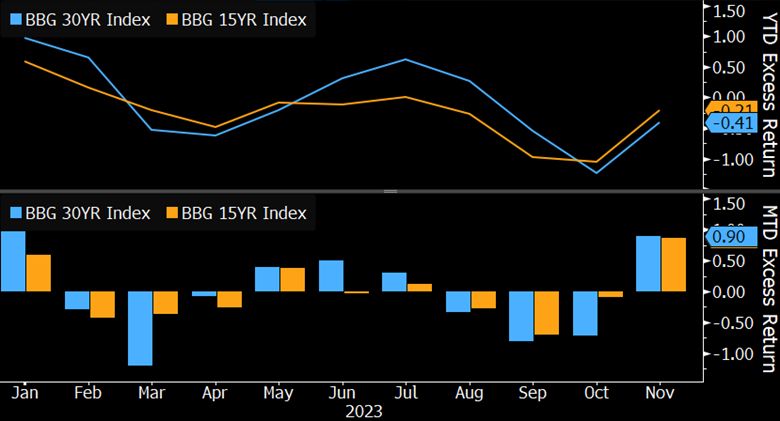

On the MBS front, we see negative returns.

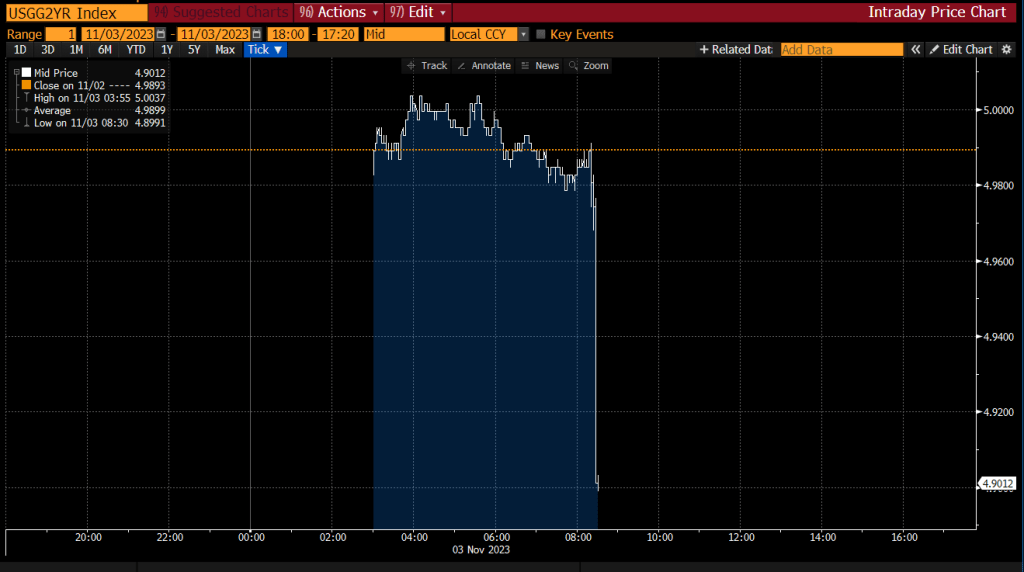

The 2-year Treasury yield is dropping faster than Biden’s polling numbers.

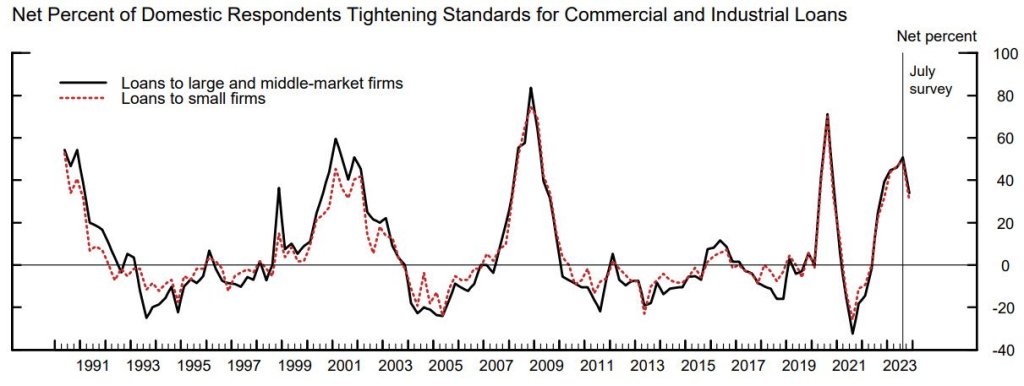

On the credit side, more lenders are tightening standards for C&I loans.

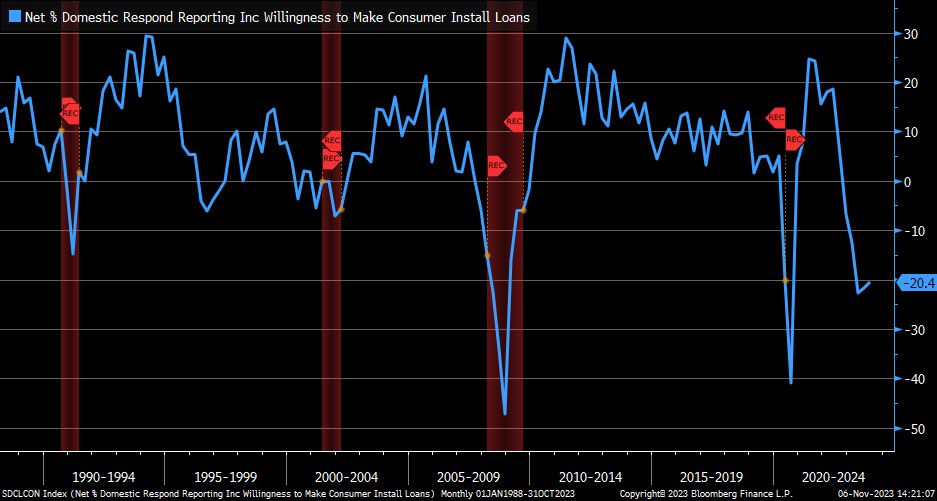

And banks remained restrictive in their willingness (or lack thereof) to make consumer loans, but there was a marginal improvement from prior release.

On the global front, Maersk announces plans to cut at least 10,000 jobs due to weakening global trade.

Here is a picture of Hinky Dink (Joe Biden) and Bathhouse Barry Soetoro. I mean Bathhouse John Coughlin, the Lords of the Levee.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.