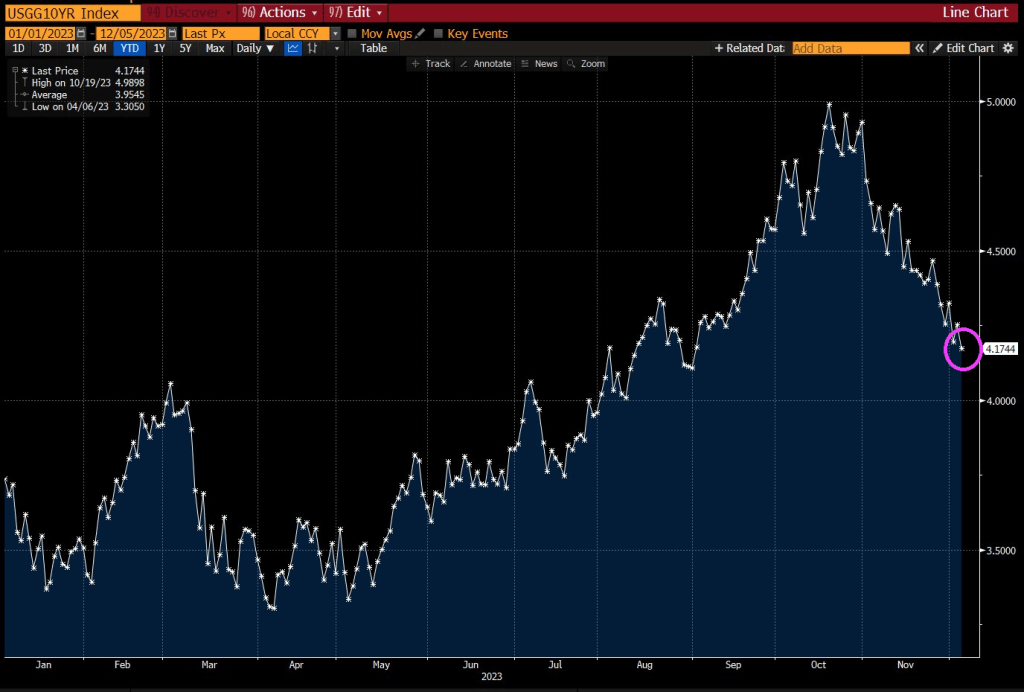

Fed money printing is simply irresistable. Particularly when the US economy seems so addicted to Fed money printing.

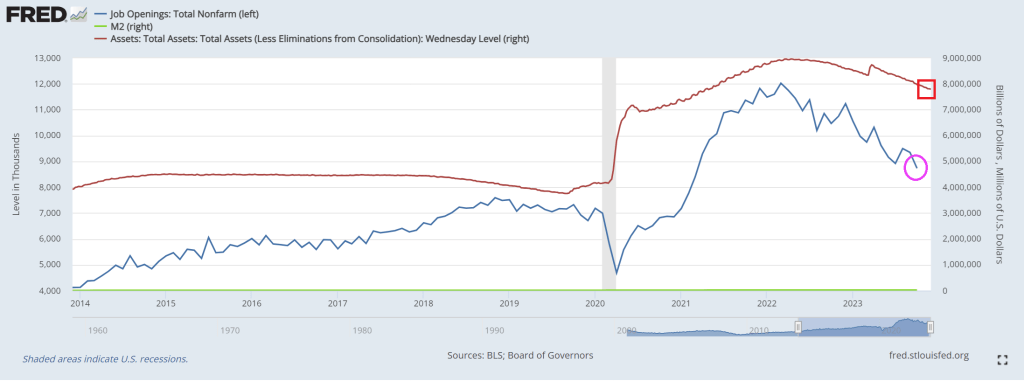

The number of job openings decreased to 8.7 million on the last business day of October, the U.S. Bureau of Labor Statistics reported today. Over the month, the number of hires and total separations changed little at 5.9 million and 5.6 million, respectively. Within separations, quits (3.6 million) and layoffs and discharges (1.6 million) changed little. This release includes estimates of the number and rate of job openings, hires, and separations for the total nonfarm sector, by industry, and by establishment size class.

But if we look at job openings plotted against The Fed’s balance sheet, we see an ugly relationship. Job openings rose under Biden in 2021 and 2022 … as The Fed continued buying assets. Then, like magic, The Fed started shrinking their balance sheet and US job openings began to shrink.

Money printing is simply irresistable! Its like Brawndo from the film “Idiocracy.”

You might as well face it, markets are “addicted to gov.” Government monetary interference, that is. Government money printing and massive Federal spending.

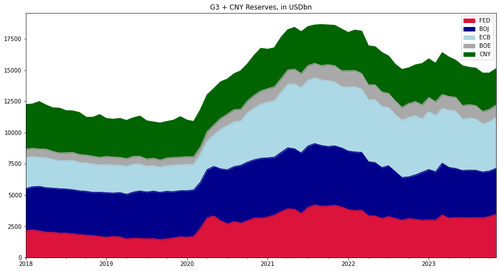

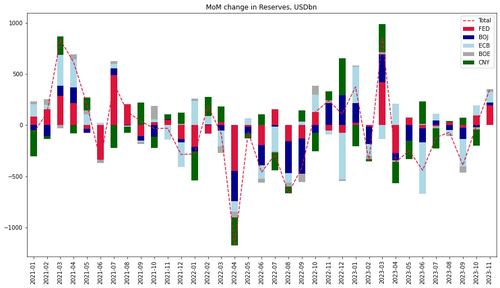

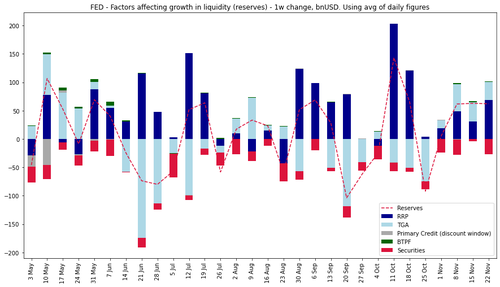

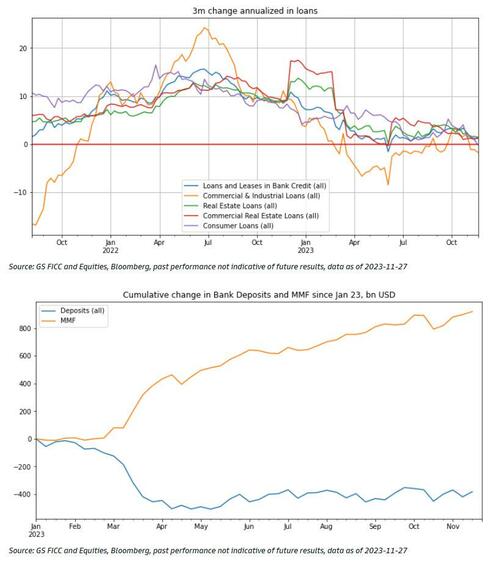

According to Goldman calculations, $350BN of liquidity (in USD terms) was added in November from the G4 central banks + the PBOC was nothing short of a fire hose.

In fact, this was the third largest monthly increase this year after January and March 2023.

The US addition of $60bn for a third consecutive week plus weaker dollar are the main drivers.

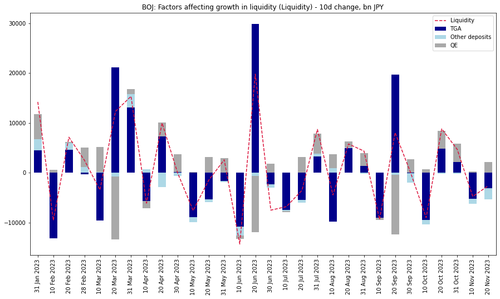

While the BoJ keeps adding liquidity via bond purchases, increases in the TGA balances in the past 20 days have net drained Yen liquidity.

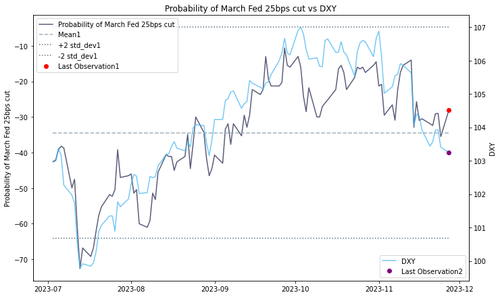

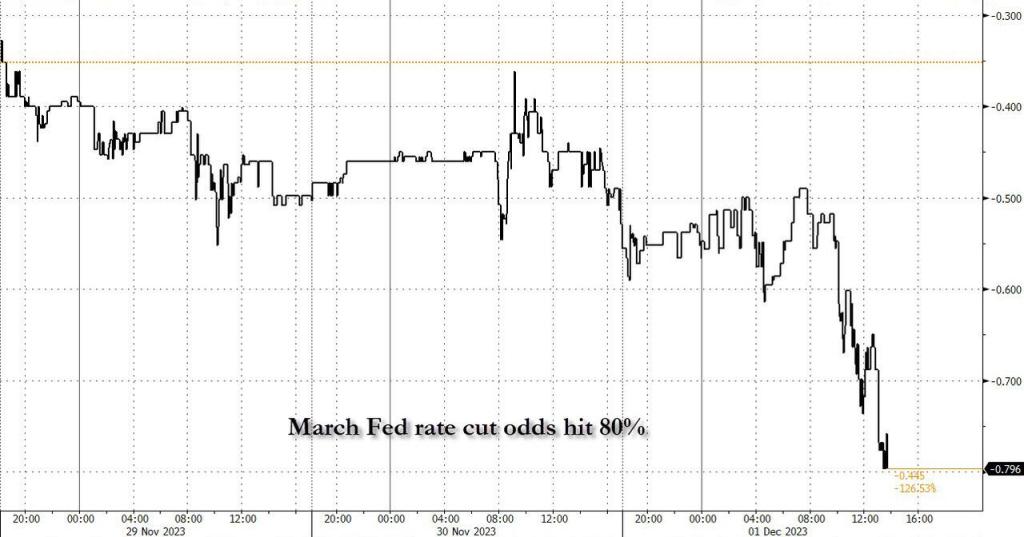

Looking forward over the year end and at the start of 2024, Goldman thinks that the US can keep adding liquidity via high bill issuance and RRP withdrawal over the next couple of months (something we discussed last month in “How Treasury Averted A Bond Market “Earthquake” In The Last Second: What Everyone Missed In The TBAC’s Remarkable Refunding Presentation“), while the dollar contribution to benign liquidity conditions could face some headwinds due to the risk of pricing out of some of the March Fed cuts as a result of the strong positive FCI impulse in November.

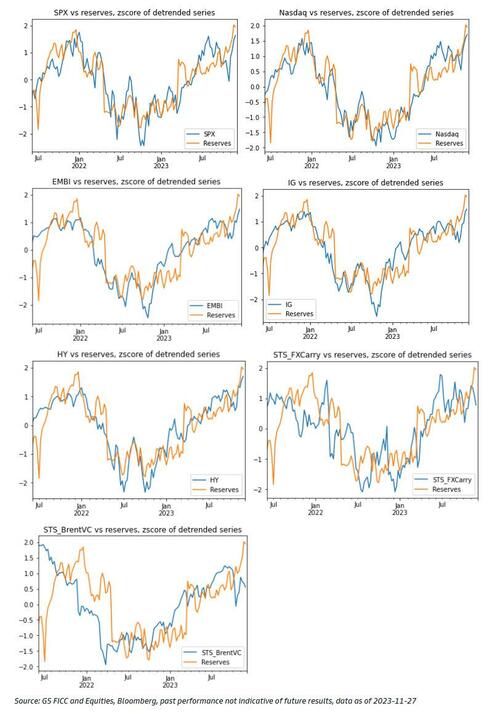

Goldman’s one-factor model for risky assets based on the liquidity cycle suggests that US IG and EM hard currency debt are cheap and the bank’s STS FX carry and Brent Vol Carry indices have under-performed the benign liquidity environment and may catch up the next two months.

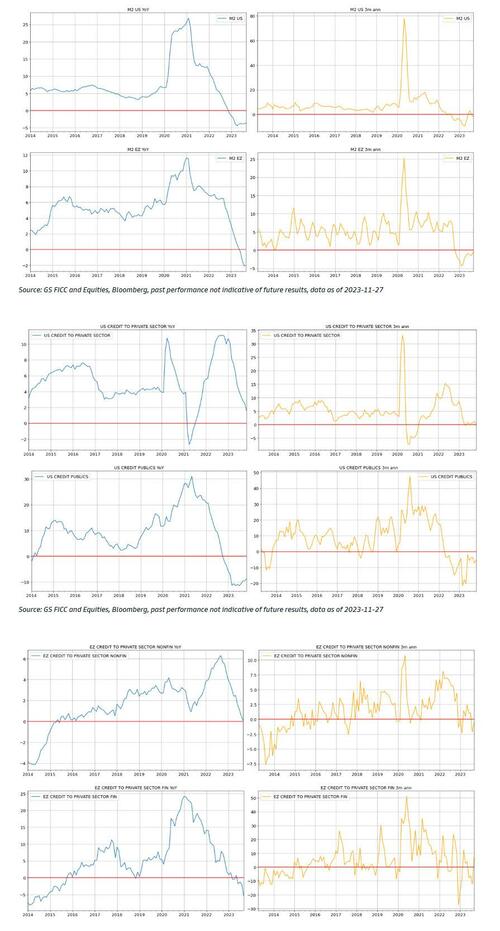

The US and Eurozone money supply and lending growth indicators remain weak, implying extended downside bias in domestic demand and inflation in H1-2024 (i.e., higher likelihood for easing absent a reflationary shock out of China or a supply-driven commodity price surge).

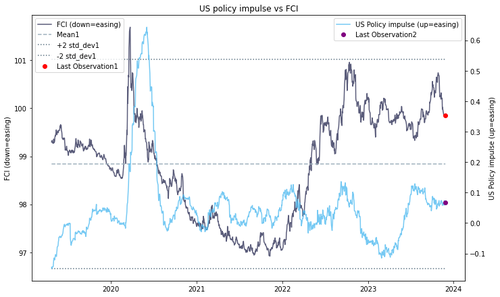

Finally, The US policy impulse (comprising of liquidity, fiscal stance, as well as nominal and real forward rates) has moved sideways in October and November after some renewed tightening in September. The GS FCI index eased nearly -100 basis points (-1.4z) in November.

Doctor, doctor (Yellen), we got a bad case of distortionomics (where the 1% wins and the 99% fall behind). After all, under Dr. Yellen as our Treasury Secretary, we are suffering from massive fiscal inferno with wild government spending. I would use “Government Gone Wild!” but the thought of Yellen … well, never mind.

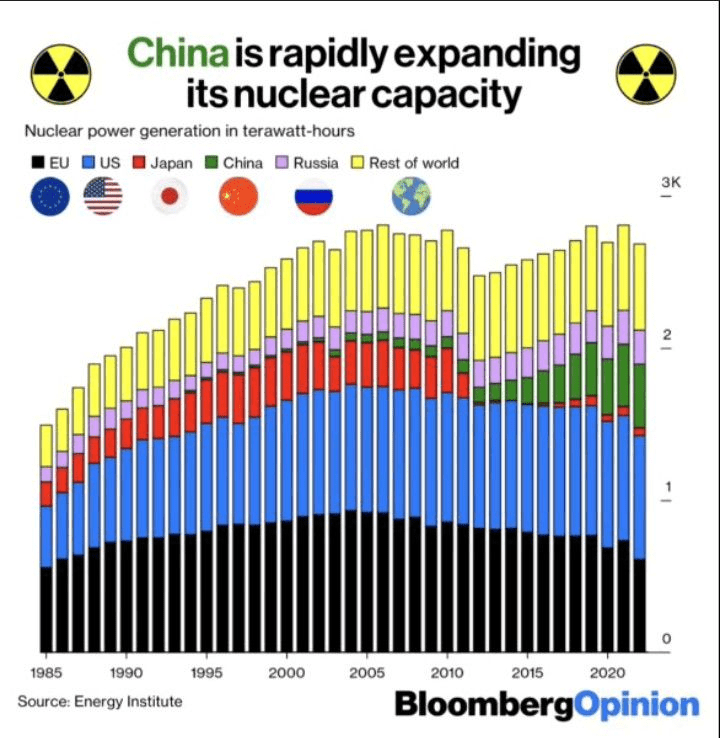

Meanwhile, while John Kerry pushes for ending ALL coal powered plants (good luck charging the thousands of EV charging stations on wind/solar power!), China is building NUCLEAR plants. While US green wimps (Kerry comes to mind) whine whenever nuclear plants are mentioned for the US.

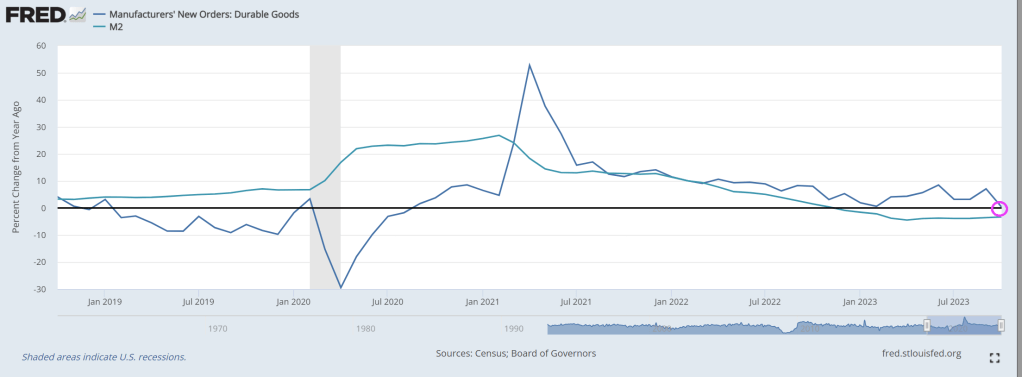

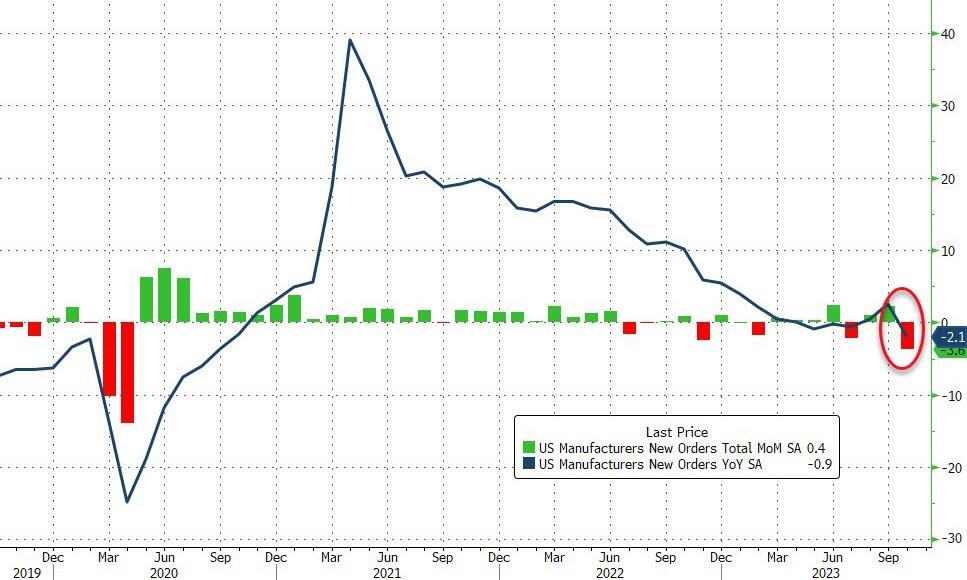

Factory orders tumbled even more than expected, down 3.6% MoM – the biggest drop since the COVID lockdowns (April 2020). September was also revised lower (making October’s decline even worse) from +2.8% MoM to +2.3% MoM…

Source: Bloomberg

The big monthly decline and revisions dragged orders down 2.1% YoY (the biggest drop since Sept 2020).

Core factory orders also dropped (-1.2% Mom), leaving them down 2.2% YoY – the eight month in a row of annual declines…

Source: Bloomberg

The final Durable Goods Orders data for October confirmed the preliminary print plunge down 5.4% MoM.

Finally, we note that it could have been a lot worse as Defense spending shot up 24.7% MoM (as non-defense dropped 15.8% MoM0…

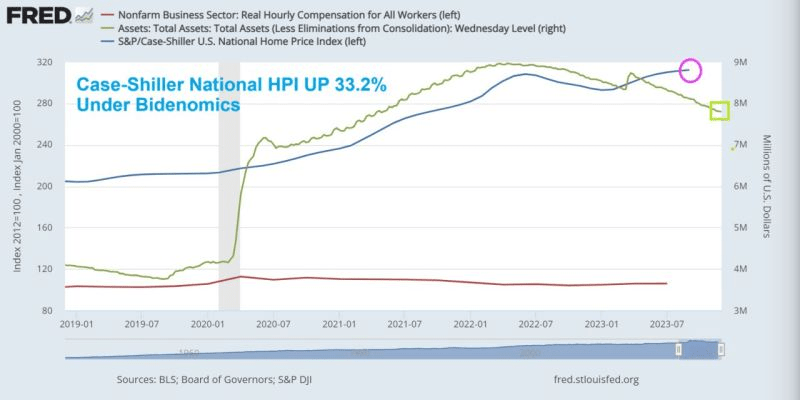

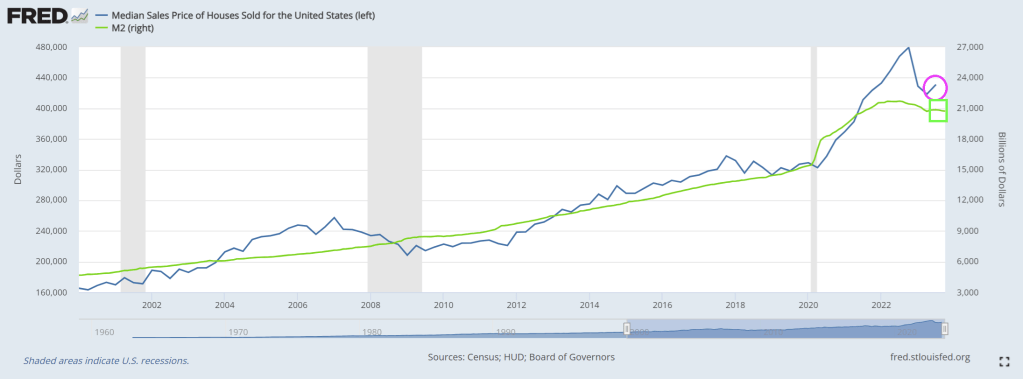

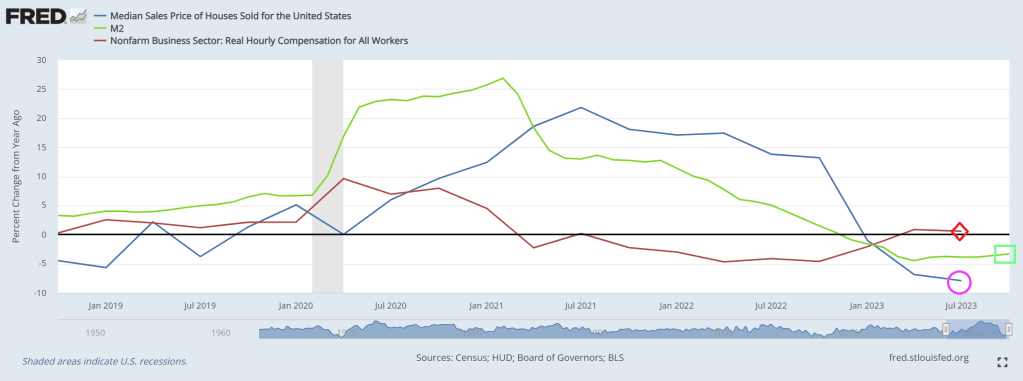

While the Case-Shiller National home price index is rising again, it has been slowing since March 2022. This is happening as “the honey pot” (aka, M2 Money printing) growth is now negative. While real hourly compensation growth is slightly, the average rate of growth since April 1, 2021, is -2.1%. (Not exactly what Biden wants to broadcast as a feature of Bidenomics).

According to a recent report from Point2 Homes, many recently bought homes, particularly in the hottest regions, are deep in the red. On average, single-family homeowners have been shedding $223 in property value every day since they bought their homes last year.

Condo owners are faring even worse, losing up to $336 a day in San Francisco, or a stunning $122,500 a year.

“This double-blow market means that the most newly minted owners were first hit by the highest home prices in history, only to be cut off from building wealth by the current falling prices,” analysts wrote.

Some major markets are seeing massive net losses

Single-family homes in 16 cities examined in the analysis have faced price declines of over $10,000 over the past year.

Memphis saw the most significant single-family price plunge, as well as the second-largest decline in condo prices, which analysts say could be due to rising inventory in the city.

Condo prices in 37 cities are also weakening, including in New York and Oakland.

So, what does this mean for homeowners? Folks who shelled out plenty of cash last year to secure their deals are now grappling with depreciating property values, which means it’s harder to build equity.

And if they want to sell in today’s market, they risk reaping less for their homes than what they paid for them. Zillow reports new buyers won’t sell at a profit until they’ve spent over a decade in their homes.

In another report from Redfin, analysts estimated that more than 3% of homes sold at a loss between August to October this year. The median amount was recorded at around $40,000, although some properties lost up to six figures on the sale.

Again, San Francisco sellers reported the biggest losses, with 1 in 7 homeowners losing money on their sales. And Memphis TN leads in percentage loss at -17.1%!

There are a couple of factors that could be contributing to the Golden City’s housing woes, including the rise of remote work coupled with tech layoffs pushing residents to relocate to other areas.

“There are buyers out there, but they’re a lot more cautious and picky than they were when mortgage rates were low,” Redfin Premier real estate agent Andrea Chopp said in September.

“The Bay Area housing market was unsustainable before, so this correction is probably healthy, but the unfortunate thing is prices remain unaffordable for a lot of people—especially with rates now above 7%,” she said.

97% of sellers are in the money, though

It’s not all doom and gloom for sellers—at least not for those who’ve been residing in their homes for a long time and bought when prices were much lower than they are today.

In many markets, sellers have been reluctant to let go of their low mortgage rates and apply for a home loan at a much higher rate, and that’s keeping inventory tight and prices high.

In the three months ending July 31, 97% of sellers across the country sold for a profit, with the typical home selling 78.4%, or $203,232, more than the seller bought it for, says Redfin.

And while San Francisco has been reporting more losses than usual, the median homeowner is still reaping $625,500 more on their home sale compared to the original purchase price.

The Godfather of San Francisco property losses, California Governor Gavin Newsom.

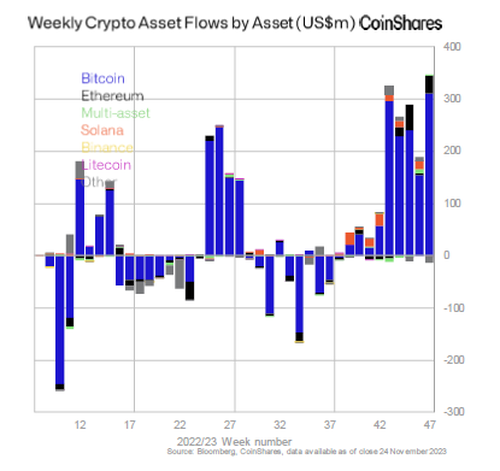

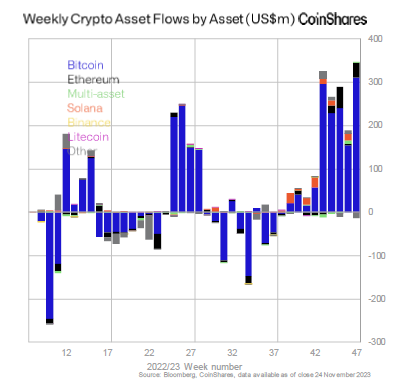

Joe Biden has a new name: the crypt keeper. As in the person through his economic screw-ups is causing a massive inflow to cryptos.

Anticipation of an eventual US spot Bitcoin ETF – which Bloomberg’s analysts assign a 90% probability of being approved by the SEC in January.

as well as surging prices, have helped to spur inflows into digital-asset investment products for a ninth consecutive week, the largest run since the crypto bull market in late 2021.

According to a recent report from CoinShares, these products which include trusts and exchange-traded products, saw inflows of $346 million last week, with Canada and Germany contributing to 87% of the total. Only $30 million came from the US, a sign of continued low participation from the country, the asset-management firm said. Of course, that will change as soon as investors start seeing double digit percentage weekly gains, and reallocating their money into crypto in droves, just like they did in 2020 and 2021.

Since early October, the crypto market has surged as traditional asset managers like BlackRock prepared for spot Bitcoin ETFs, potentially bringing in many more investors into the asset and resulting in inflows of tens of billions in fresh capital.

“The combination of price rises and inflows have now pushed up total assets under management to $45.3 billion, the highest in over one and half years,” the report said.

Bitcoin products raked in $312 million last week, pushing inflows to over $1.5 billion since the start of the year. Ether products saw $34 million in inflows last week, almost negating outflows all of 2023.

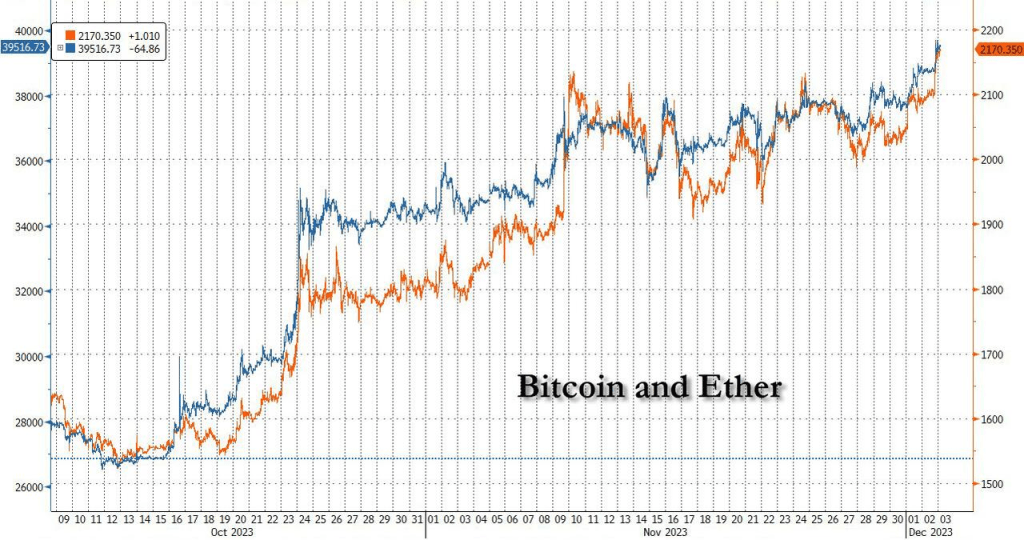

Amid the surging inflows, and amid expectations for imminent ETF approval by the SEC and a surge in March rate cuts odds, bitcoin and ethereum have continued their furious ascent, with the former now trading just shy of $40.

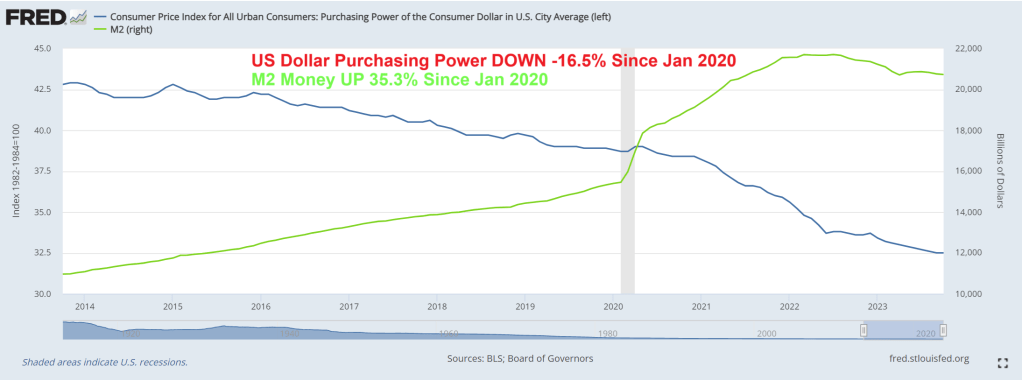

Since Covid and the idiotic government and school shutdowns of 2020, the purchasing power of the US Dollar has fallen -16.5% as M2 Money grew 35.3%. Keep on printing?

I suppose Biden’s biography can be called “Tales From The Crypt(o)”.

It came after the Munich freezeout where the private jets of global elites were snowed-in. But apparently most made it to Dubai for COP28. Or more apt, the Cop-out meeting where the global elites meet eating caviar and guzzling champagne and telling us to die off, eat bugs and drive idiotic EVs that most Americans can’t afford. (A $100,000 Ford F-150 Lightning??)

But at least we can hear England’s royalty, King Charles, bloviate about the weather. Along with American royalty, VP Kamala Harris and Climate Envoy John Kerry who committed the US to closing down out coal burning plants.

King Charles is no friend of general humanity. Speaking at COP28, he said: “The Earth does not belong to us, we belong to the Earth.” As with many know-your-place elitists, he appears to abhor the impacts that humans have on the planet. He exhibits, sadly on a world stage, a snobbish distain for capitalism – what used to be dismissed in British aristocratic circles as ‘trade’. This capitalist trend over the last 200 years has harnessed the power of natural hydrocarbons to raise billions to a standard of living and health unimaginable to previous generations. In 2009, Charles said we can no longer afford consumerism and the “age of convenience” was over.

Not for the new British King, it need hardly be observed. He lives a life of pampered indulgence where no expense is spared to ensure his every comfort. On his accession to the throne, he added considerably to his Palace Portfolio. To spread his malevolent Net Zero fantasies, he has a fleet of cars, private planes and even a personal train at his command. He uses these to call for “transformational action” to be taken to save the planet. In his COP28 speech, he called for the restoration of nature, the need for sustainable agriculture, and co-operationbetween the public and private sectors.

Few calls could be more political in tone. The restoration of nature and sustainable agriculture is shorthand for largely meat-free diets and massive reductions in nitrogen fertiliser. The latter, in particular, will lead to worldwide famine. COP28 seems set to announce new food and agriculture restrictions using the tactic of demonising methane, a gas emitted by animals and humans that is barely measurable in the atmosphere due to a very short lifecycle. Whenever the subject of ‘co-operation’ between public and private sectors is raised, there is an immediate dash to count the spoons, since it can only signal a large transfer of cash from productive industries to unproductive and inferior green operations.

At one point in his COP speech, King Charles veered into sandwich-board territory claiming that “we are seeing alarming tipping points being reached”. There was no evidence presented to justify this claim, often made by climate extremists using modelled data. In fact, he didn’t even refer to any actual ‘tipping’ event that has been reached. Many scientists have concluded that bad, or extreme, weather events are no worse than in the immediate past. Many categories of natural disasters such as floods, droughts and ecosystem productivity “show no clear positive trend of extreme events”, note a group of four Italian scientists. They argue that the data shows there is no “climate emergency”.

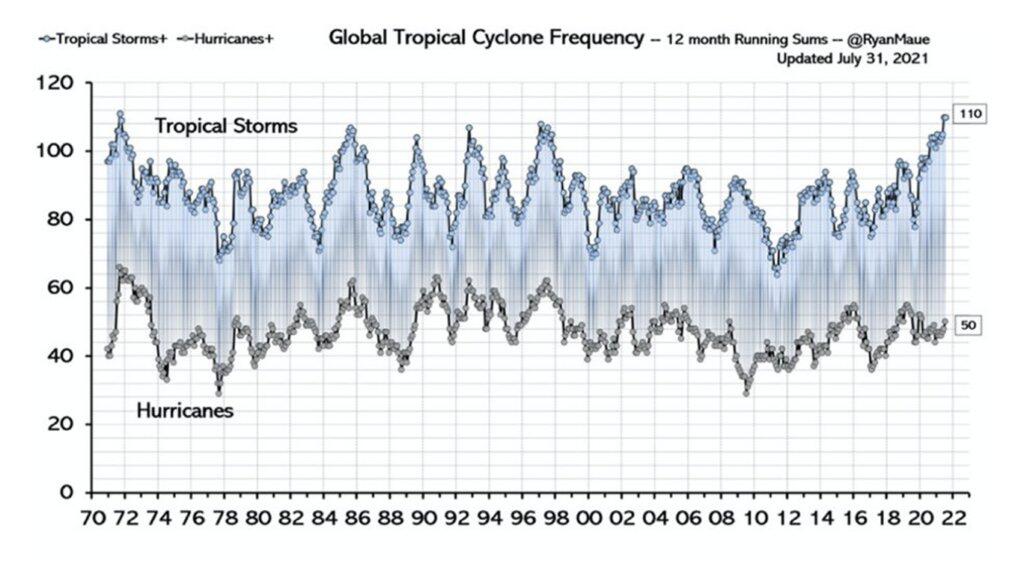

None of these facts seem to matter to a political King, who, like a stuck Guardian record, keeps on pressing on with made-up emotional stories of impending climate Armageddon. At one point he referred to repeated cyclones battering vulnerable islands, something that cyclones have always done.

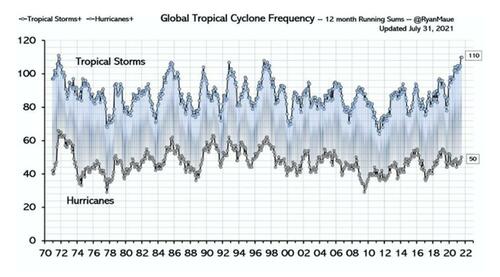

The King can always cherry-pick individual storms but there is plenty of evidence to show that hurricane and cyclone frequency, along with intensity, has changed little over the recent historical record, as the above graph shows. And The King demands that global taxpayers pay $5 trillion annually to prevent “climate catestrophy.” Easy for the billionaire King to say such nonsense.

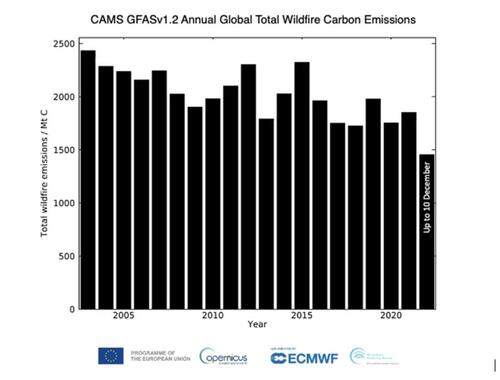

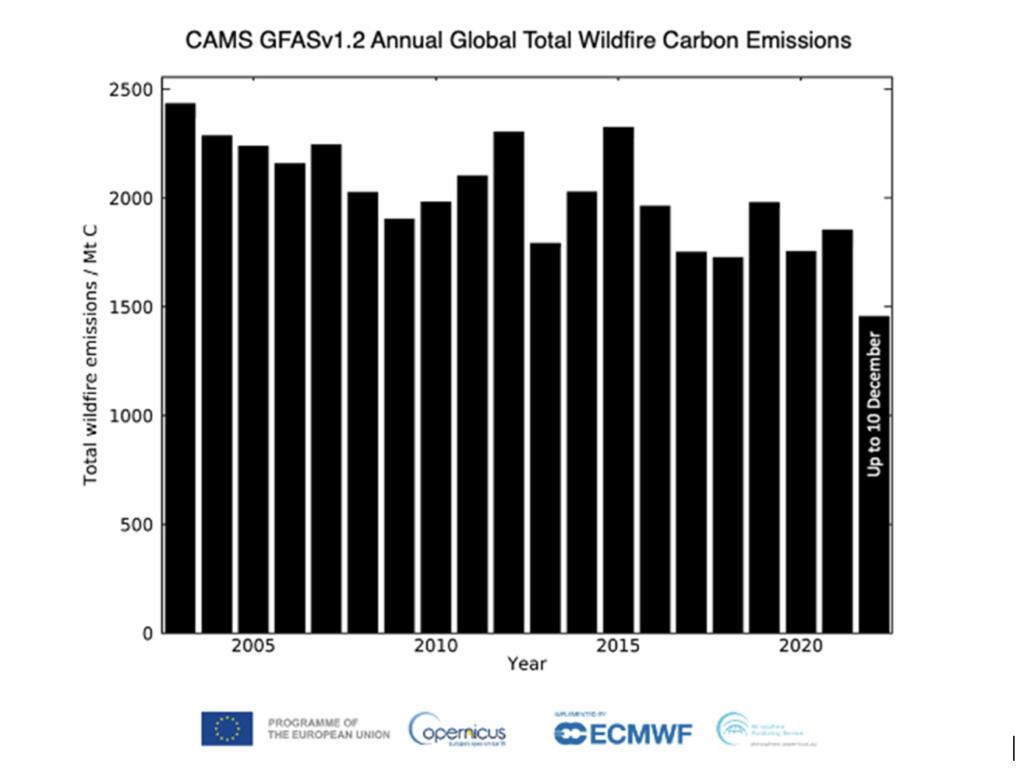

Wildfires are a bit of a dud when it comes to whipping up climate hysteria, not least because the UN Intergovernmental Panel on Climate Change notes that most conflagrations are started by humans. “Human activities have become the dominant driver,” it observes. But when there is political Net Zero work to be done, the King is only too happy to overlook the evidence. In common with many other countries this year, Canada experienced its worst wildfires for a century, he said.

Despite all the human involvement, the above graph shows the gradual decline of global emissions from wildfires over recent decades. In fact, wildfires are almost impossible to pin on any changes on climate since so many other factors, such as arson and land management, are in play.

Net Zero is rapidly becoming the dominant political issue of the age. Its obvious collectivist nature gathers support from mostly sectional interests in society. It has no significant grassroots support, since it aims to restrict human lifestyles and wealth on a scale never attempted before in history. It is awash with junk science, fake statistics and computer models. Like the models that said that the earth only has 10 years left, despite current global temperatures being cooler today than much of history.

The late Queen, in her infinite wisdom, never went anywhere near it. But I wonder if “Climate Queen” Greta Thunberg will be speaking? After all, I am dying to hear high school dropout and climate crazy Greta lecture me with her patented “How dare you!”

When John Kerry testified in Congress, he was asked if he owned his own private jet. Being a life-long career politician, Kerry gave a half truth. “No I do not own a private jet.” But his wife does (remember Theresa Kerry was formerly married to Republican Senator John Heinz (of Heinz pickles and ketchup fame).

Hey John, how are we going to power all those EV charging stations without coal? And The Left’s ludicrous fear of nuclear energy. Wind farms (aka, eagle killers)? Offshore wind farms (whale killers)? Solar farms? With panels made in China??

While members of the Biden Administration party at DC nightclubs, the rest of America are drinking Carlo Rossi wine (a favorite of mine in high school!) and eating Spam.

While hourly pay has increased, inflation has outpaced it.

Spending on basic survival needs like food, transportation, housing, and energy has increased, with households in the Mountain West facing the highest rates of inflation.

“We choose January 2021 as the base month because it was the last time inflation was within recent historical norms,” the report reads.

“Due to a combination of higher inflation rates and higher average household spending, inflation is imposing the highest monthly costs on families in the states of Colorado, Utah, and Arizona,” the report adds.

Families in Colorado and Washington, DC, are experiencing inflation costs higher than the national average.

Things are even worse in 2023 regarding inflation ravaging worker’s income. Over 60% of Americans reported that their wages were lagging well behind inflation.

Since January 2021, US purchasing power of the US Dollar is down a whopping -15.4% under Biden.

And home prices are up 33.2% under Biden, much of it due to The Feral Reserve money printing to fund Biden’s folicy initiatives. (I saw Biden claim he wrote the Inflation Reduction Act … the one thing we know is House legislation is written by an army of Congressional staffers, not El Presidente).

Home prices up 33.2% and purchasing power of US Dollar down -15.4% under Biden.

And like magic, Biden made $11,400 disappear from household income to pay for Bidenomics.

Median home prices are up a whopping 20% under Biden and his signature Bidenomics, growing the economy from the inside-out (?) instead of top-down. Excuse me Joe, Bidenomics is pure top-down Soviet-style economic planning. Markets be damned! The end result? Housing is far more expensive under Biden as are down payments.

If we look at year-over-year (YoY), we can see the burst of Covid-related spending and M2 Money growth (green line) that surged in 2020/2021. And rising home prices followed shortly thereafter. But as M2 Money growth slows, median home price growth declined into negative growth. The only factor that is positive is real hourly compensation (red line). But that is barely above 0%.

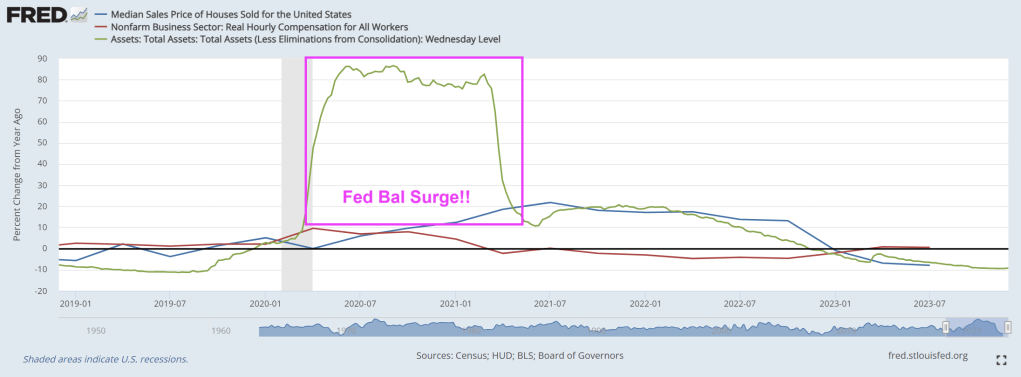

If we look at The Fed’s balance sheet surge (much like a storm surge), you can see the 2020/2021 overreaction to Covid and the various government shutdowns (along with school shutdowns).

The problem is that The Fed is shrinking their balance sheet like Biden shuffles. Maybe The Fed is following Biden’s lead: slow walking, incoherent messaging. And with the Fed storm surge of 2020/2021, Case-Shiller national home price index is up 33.2% under Bidenomics. Good luck with that down payment if you are renting and want to become a homeowner.

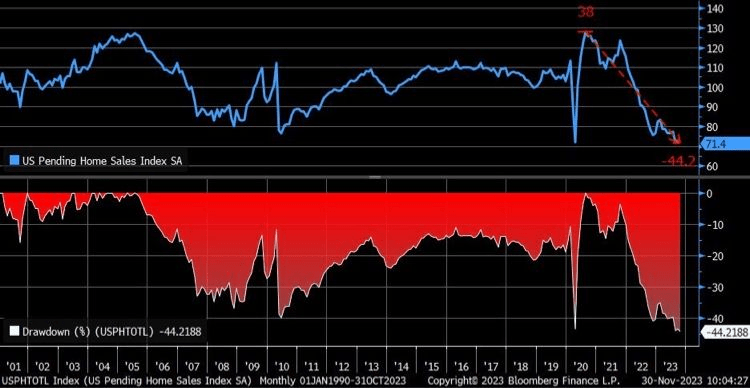

Pending home sales crash is showing why government usually fails to deliver sensible outcomes.

After all, Biden (and his overlord Obama) are truly addicted to gov solutions. Which means they are doomed to fail, as most government policies do.

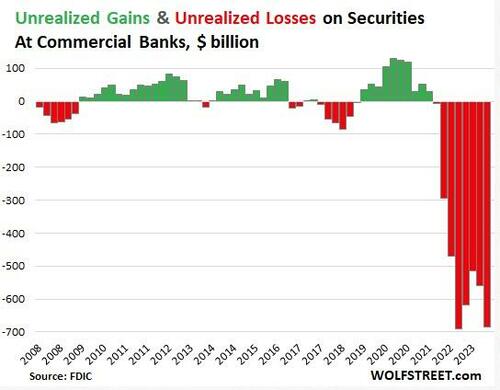

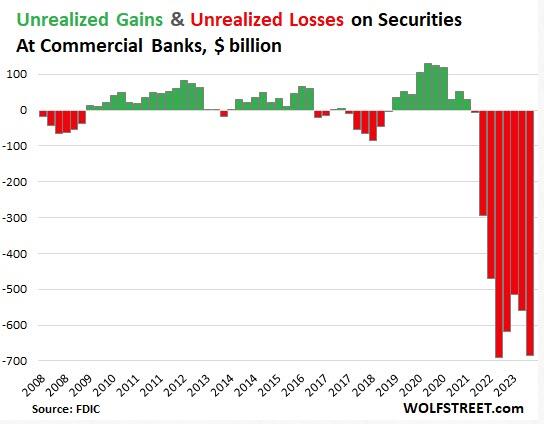

Unrealized losses on securities held by US banks exploded by 22% in the third quarter.

Of course, unrealized losses don’t really matter — until they do.

This is yet more evidence that the financial crisis that kicked off last March continues to bubble under the surface.

Unrealized losses, primarily on US Treasuries and mortgage-backed securities rose by $126 billion in Q3 and now total $684 billion, according to the FDIC’s quarterly bank data release.

Current unrealized losses are only slightly below the record set in the third quarter of 2022. This reflects the fact that the FDIC took over three failed banks earlier his year and ate their unrealized losses when it sold the banks’ assets, thus wiping them from the books.

Unrealized looses on securities are divided between two accounting methods.

Unrealized losses on held-to-maturity (HTM) securities jumped by $81 billion to $391 billion.

Unrealized losses on available-for-sale (AFS) securities jumped by $45 billion to $293 billion.

It’s important to understand these are only paper losses. Ostensibly, the banks will hold these bonds until maturity and then will be paid their face value. If it plays out this way, there won’t be any real losses.

The problem is that these unrealized losses drastically decrease a bank’s liquidity. If it has to sell bonds in order to raise capital, the bank will experience significant losses. This is exactly what took down Silicon Valley Bank last March.

Here’s what happened.

SVB sold a large portion of its bond portfolio at a $1.8 billion loss. At the time, SVB CEO Greg Becke said the bank made the sale “because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients.”

The bank bought the bonds when interest rates were low. As a result, the $21 billion available for sale (AVS) bond portfolio was not yielding above cash burn. Meanwhile, rising interest rates caused the value of the portfolio to fall significantly. The plan was to sell the longer-term, lower-interest-rate bonds and reinvest the money into shorter-duration bonds with a higher yield. Instead, the sale dented the bank’s balance sheet and caused worried depositors to pull funds out of the bank.

WolfStreet explained more generally how these “irrelevant” unrealized losses can suddenly become relevant.

Banks, via a quirk in bank regulations, don’t have to mark these securities to market value, but can carry them at purchase price. The difference between market value and purchase price is the ‘unrealized gain or loss’ that the bank must disclose in its quarterly financial filings, so that we the depositors can see them and get spooked by them and yank our money out, us billionaires and centimillionaires first, on the two fundamental principles of investing: 1, he who panics first, panics best; and 2, after us the deluge.”

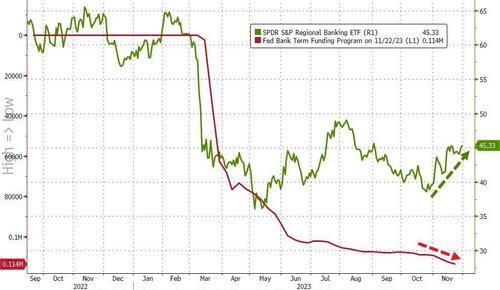

The Federal Reserve set up a bailout program to allow banks to deal with this problem. Instead of selling bonds at a loss, cash-strapped banks can go to the Fed’s Bank Term Funding Program (BTFP) and borrow against them “at par” (face value). This allows banks to use these undervalued assets to raise cash (at least temporarily) without realizing big losses on their balance sheets.

As unrealized losses rise, banks continue to tap into this bailout program more than nine months after the crisis kicked off.

In effect, the Fed managed to paper over the financial crisis with this bailout program.

It basically slapped a bandaid on it. But it has not addressed the underlying issue – the impact of rising interest rates on an economy and financial system addicted to easy money.

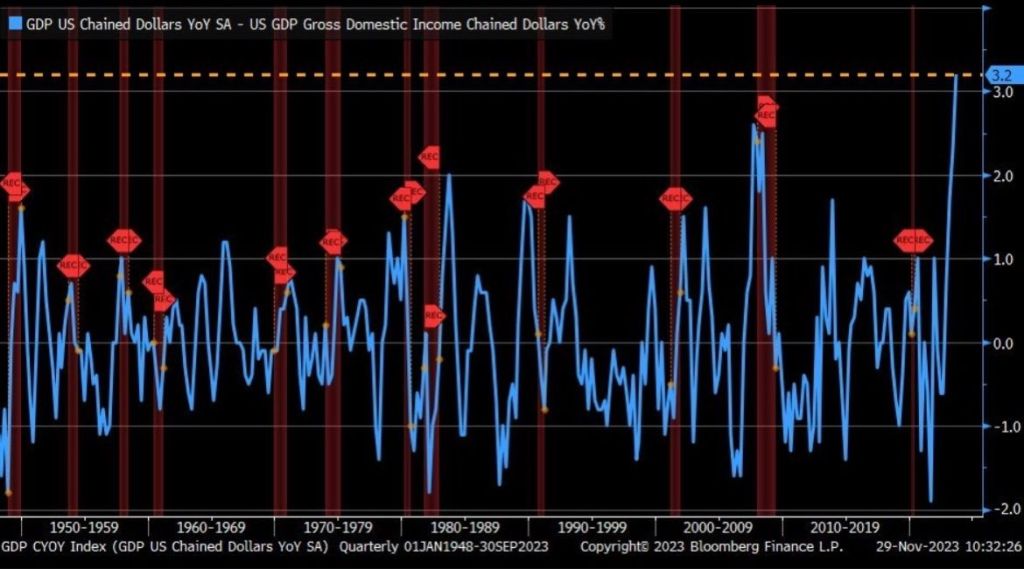

Remember, the US is on the cusp of a REAL recession, thank to Bidenomics.

The spread between real GDP and real Gross Domestic Income (GDI) just hit an all-time high. Even higher than The Great Recession of 2009.

Might as well have AC/DC’s Angus Young as US Treasury Secretary instead of tone-deaf Janet Yellen.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.