Under Bidenomics, with its high inflation rate and crushing negative wage growth, consumers are draining their savings and living on a prayer …. and consumer credit to cope.

What is worriesome in the transition rates (like current to 90-days delinquent) Credit cards (blue) and auto loans (red).

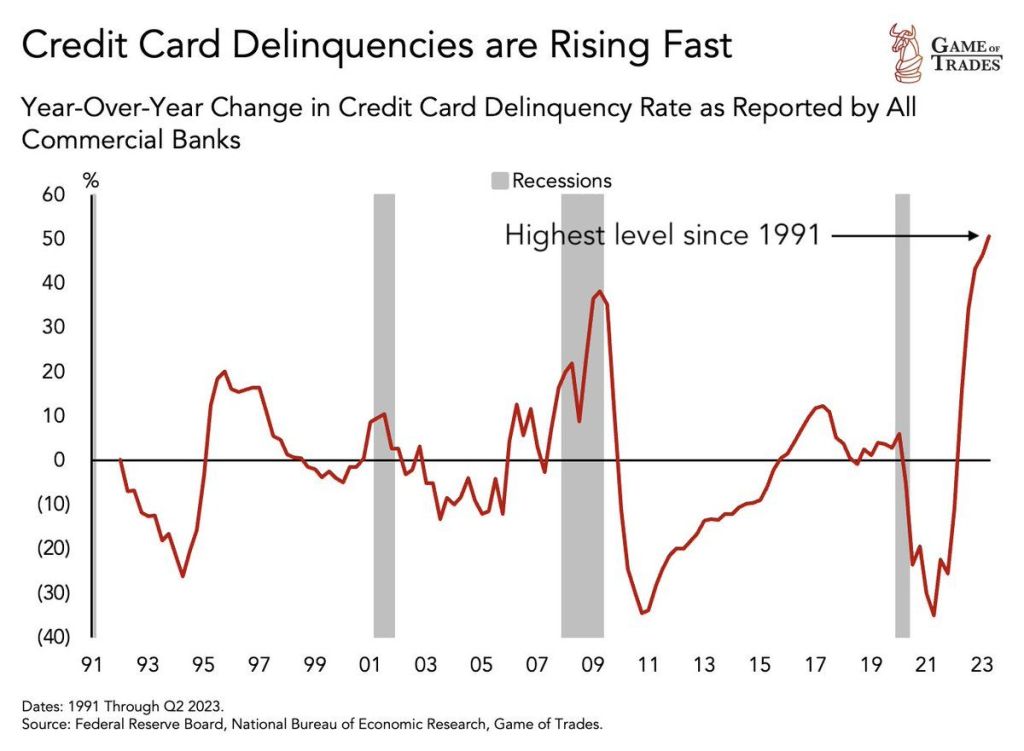

A closer look at credit card delinquency rates on a year-over-year (YoY) basis, showing the fastest growth in delinquencies since the Covid economic lockdowns.

Then we have commercial real estate delinquencies are now the highest the have been since 2013.

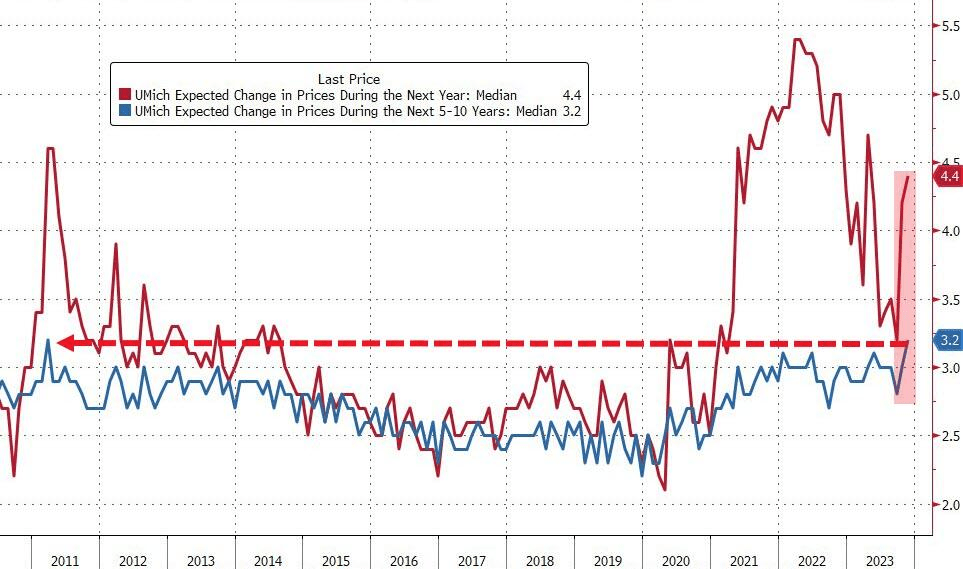

Meanwhile, University of Michigan consumer sentiment about inflation spiked to 4.4%. That is the highest medium-term inflation expectation since 2011.

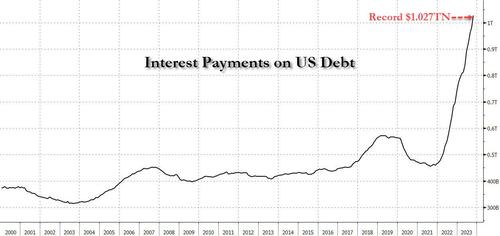

$1.027 trillion in interest is calculated by multiplying the average interest rate on marketable US Treasury debt (which according to the Treasury is 3.096% as of Oct 31) by the $26.003 trillion in marketable US debt (as of Oct 31) which nets off to $805 billion, and adding to this non-marketable debt interest (which as of Oct 31 was 2.884% multiplied by the amount of non-marketable debt which is $7.696 trillion) and which in turn is an additional $222 billion in interest. Add across and you get $1.027 trillion.

Naturally, this calculation of estimated real-time interest costs – which is entirely based on Treasury data – is different than what the Treasury actually paid. Interest costs in the fiscal year that ended Sept. 30 ultimately totaled $879.3 billion, up from $717.6 billion the previous year and about 14% of total outlays, however that number is merely lagging what the pro forma print currently is, and will inevitably catch up to it, and then lag on the other side even as pro forma interest payment start dropping (once interest rates plunge after the next QE/YCC is launched).

Fans of exponential functions, we got you covered: the unprecedented surge in both interest rates and interest expense in the past two years means that total US interest has doubled since April 2022 and that’s with the inherent lag in interest catch up – as a reminder, the vast majority of 5, 7, 10 and 30 year debt is still locked in at much lower interest rates, and as such, rates will continue to rise as all of the existing debt rolls into much higher rates over the coming years.

Looking ahead, the staggering surge in both yields and total long-term Treasuries in recent months confirms the government will continue to face an escalating interest bill. As a reminder, we were the first to point out that it took just one month after US federal debt first rose above $33 trillion for the first time, to spike by another $600 billion.

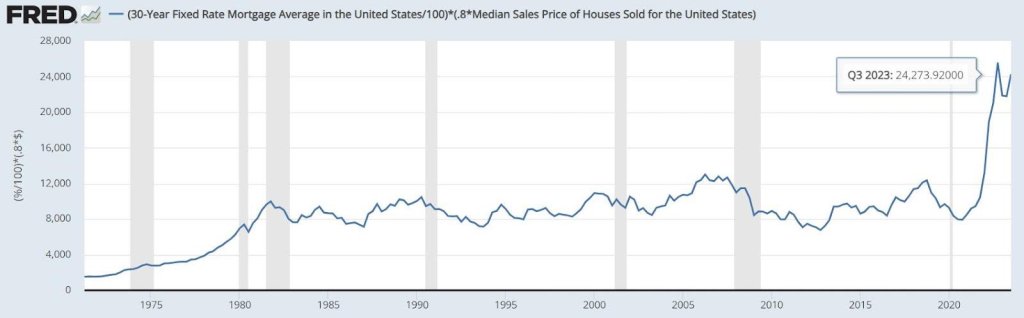

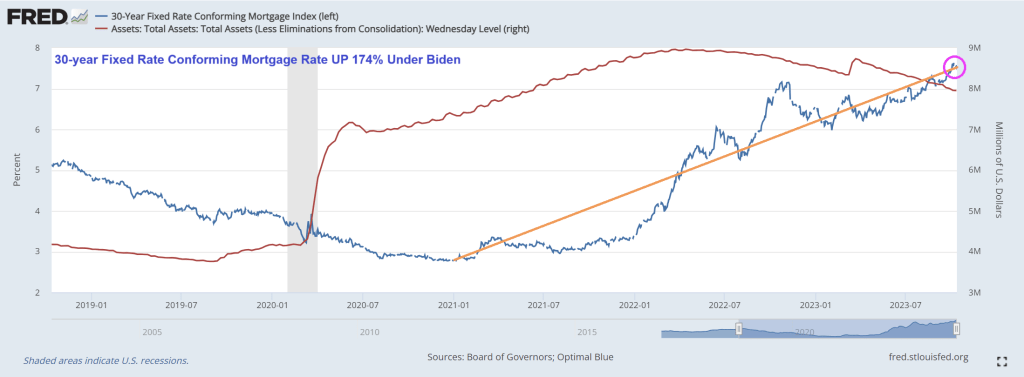

On the personal finance side, annual Interest payments on a 30-year, fixed-rate mortgage before Biden was $8,500, but after Biden it almost tripled to $24,300! That means that annual mortgage interest rose 186% under Biden.

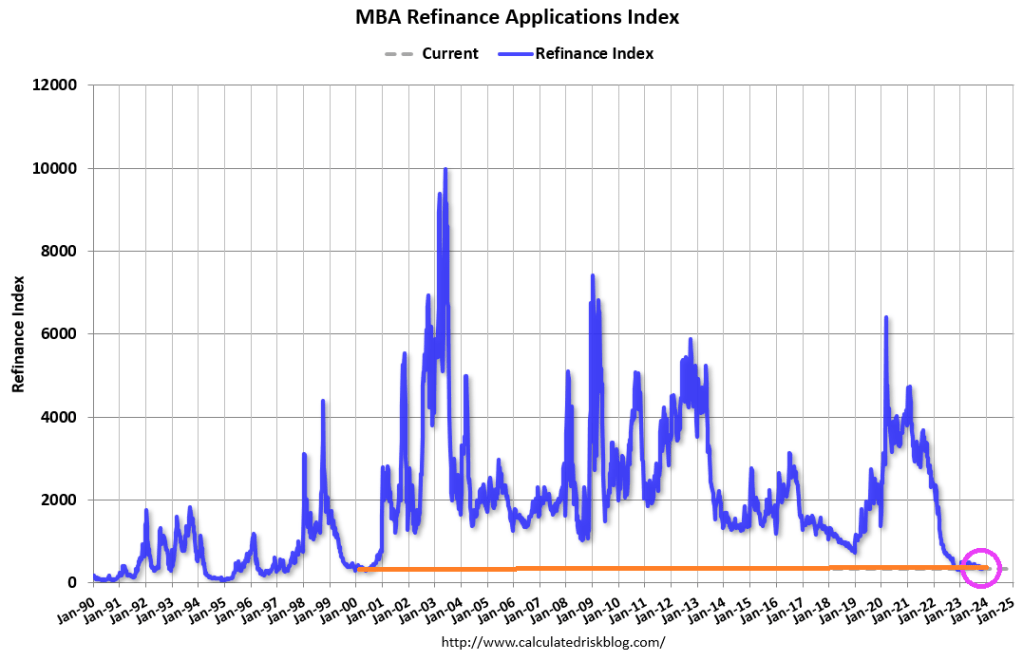

US inflation is lower than it was a year ago (cheers from The View CNN and MSNBC cheerleaders), but inflation remains stubborning above The Fed’s 2% target rate and will likely remain above 2% for the nexf few years. So mortgage demand is much like inflation … mortgage demand increased in the latest week but generally is very low compared to last year.

Mortgage applications increased 2.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 3, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 1 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 7 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 20 percent lower than the same week one year ago.

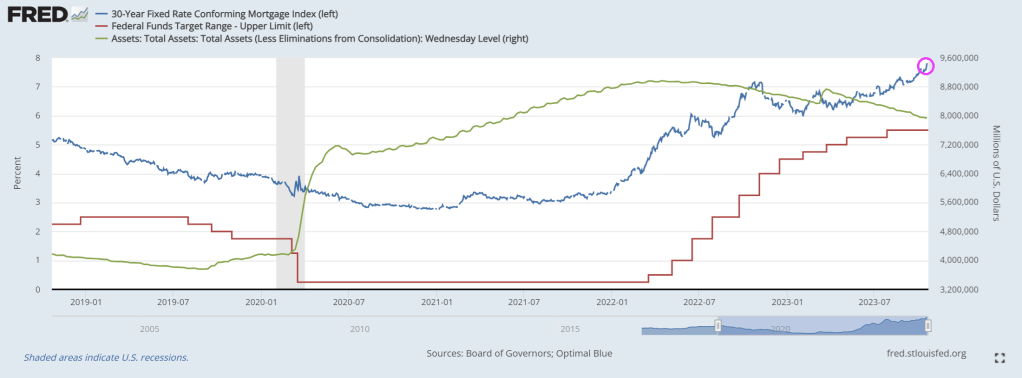

The 30-year fixed mortgage rate dropped by 25 basis points to 7.61 percent, the largest single week decline since July 2022. But, mortgage rates are up 169% under Biden and Bidenomics.

Bidenomics is a windfall for the donor class (high rate of return on campaign contributions) while the middle class gets beaten to a pulp. Waiting for Biden to lean over and creepily whisper “It’s working!” Even though it is clearly not working, at least for the middle class.

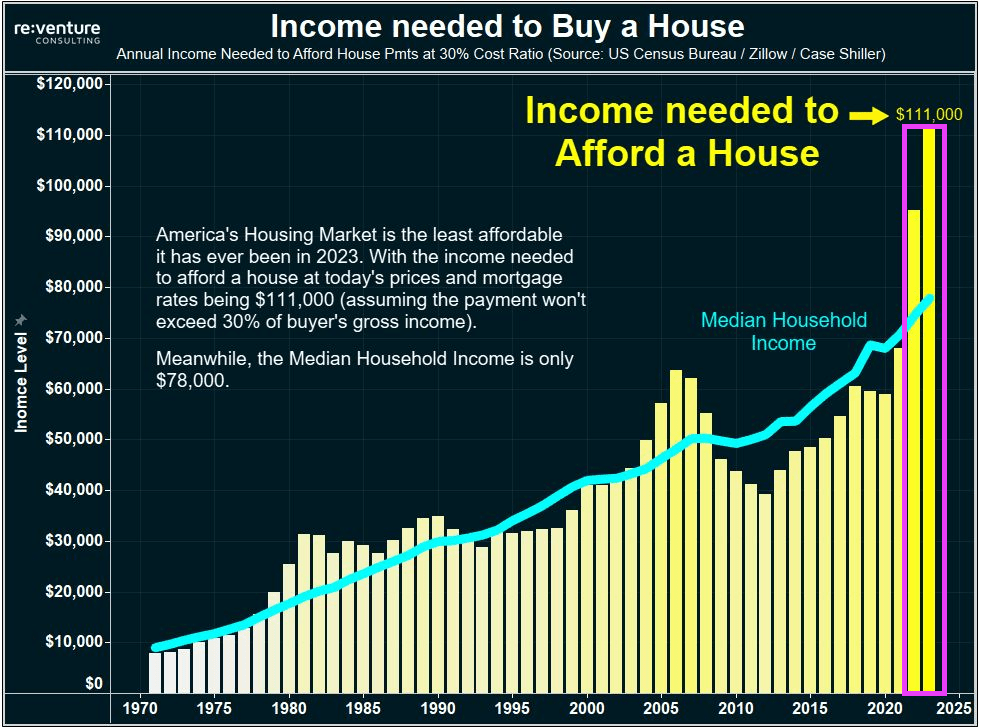

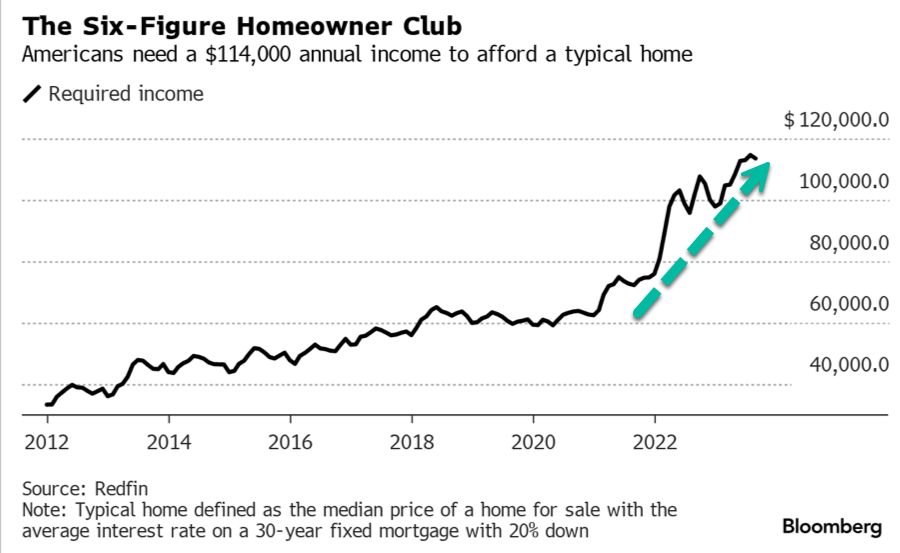

Evidence that Bidenomics is not working and destructive? Try the surging income needed to buy a house under Biden. Home prices are rising faster than median household income. As in $111,000 income needed to buy a house, while median household income is only $78,000. So, housing is simply unaffordable under Bidenomics. The Biden era is outlined in pink.

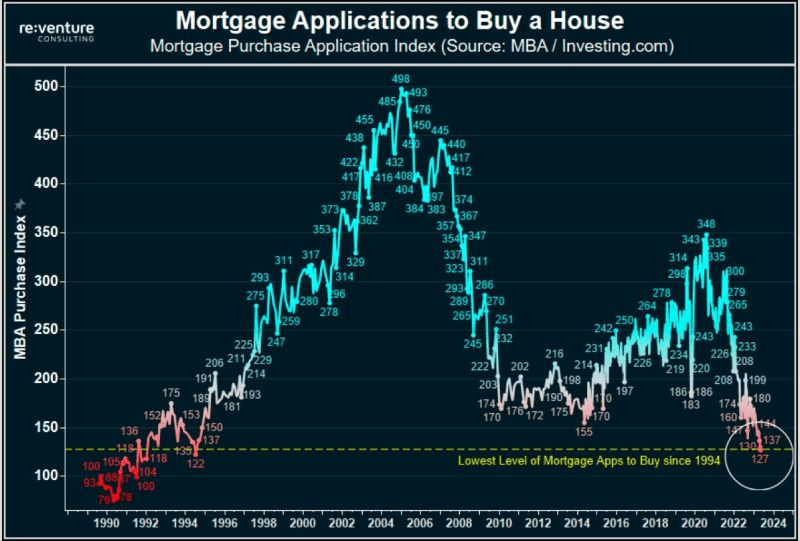

Mortgage purchase applications have collapsed to 1994 levels.

Meanwhile, stressed households are seeing credit card delinquencies at the highest level since 1991.

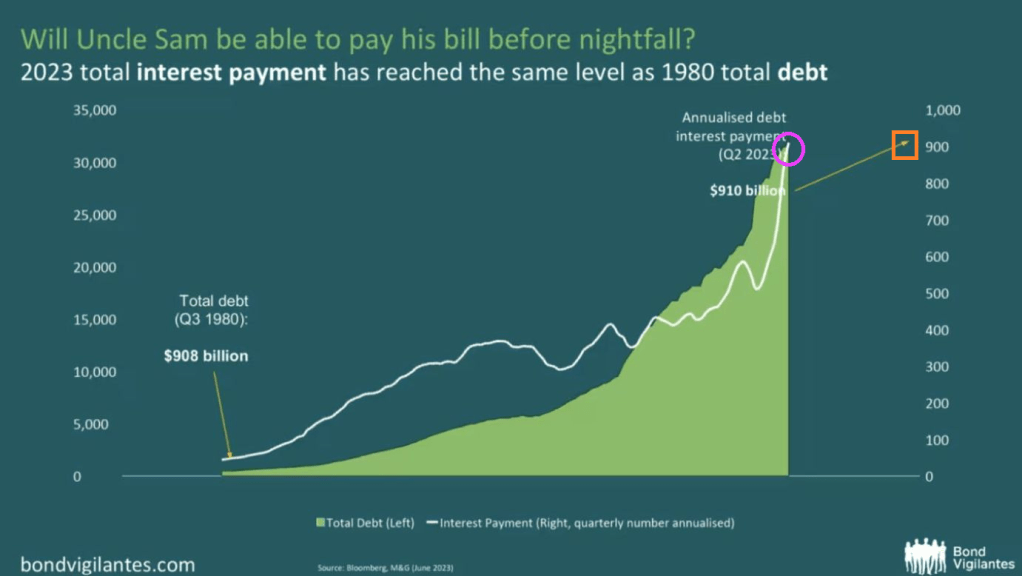

And thanks to Uncle Spam (given how Uncle Sam is destroying the middle class it is now Uncle Spam), 2023 interest payments are the same as the total debt from 1980! Spam, which the Federal government has devolved into, is very high in fat, calories and sodium and low in important nutrients, such as protein, vitamins and minerals.

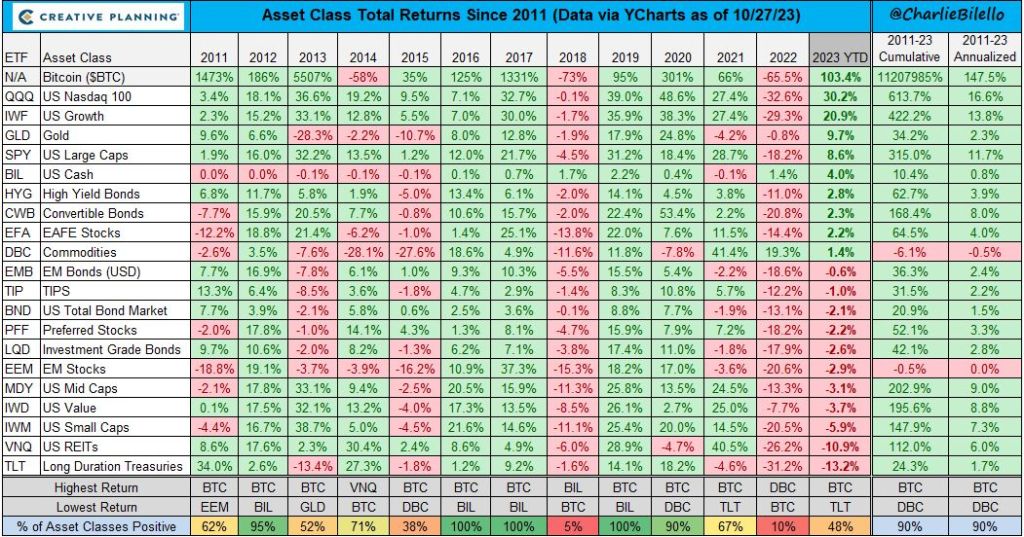

2022 was a bad year for investments under Bidenomics. 2023 year to date is showing huge gains for Bitcoin, the NASDAQ and gold. Bringing up the rear are long duration Treasuries and REITs (real estate investment trusts), both earning negative returns thus far of less than -10%.

Bidenomics has been a massive windfall for the top 1% of households in terms of wealth due to the emphasis on green energy transformation. But for the 99%, Bidenomics has been a disaster (unless you consider low-paying job creation a victory).

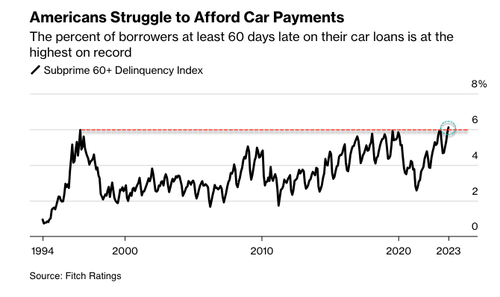

The auto sector, considered a leading economic indicator, pinpoints the arrival of the crushing auto loan crisis and even the possibility of the onset of the next recession. In late January, we Fitch revealed tat consumers are falling behind on auto payments – the most since the peak of the Great Financial Crisis. Fast forward nine months later, to September, that rate just hit the highest level in nearly three decades.

And with interest rates rising the fastest in history,

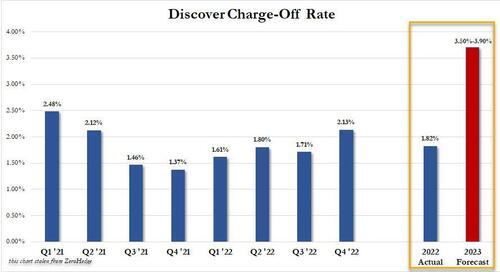

And Discover projected charge off rate for 2023 would more than double from its current 1.82% to as much as 3.90%!

In what could be the early innings of the auto loan crisis, something we called a “perfect storm” earlier this year, Bloomberg cites new Fitch data:

The percent of subprime auto borrowers at least 60 days past due on their loans rose to 6.11% in September, the highest in data going back to 1994, according to Fitch Ratings.

Source: Bloomberg

“The subprime borrower is getting squeezed,” said Margaret Rowe, senior director with Fitch.

Rowe said, “They can often be a first line of where we start to see the negative effects of macroeconomic headwinds.”

What has been widely known is the consumer has been funding car purchases with even more debt to afford record-high prices, with many monthly payments exceeding $1,000. Factor in the Federal Reserve’s most aggressive interest rate hiking cycle in a generation, elevated inflation, and the restarting of the federal student loan payments, tens of millions of consumers are under immense pressure this fall.

An endless stream of retailers, such as Walmart, Nordstrom, Macy’s, and Kohl’s – all of whom have recently warned about a consumer slowdown. Banks have also raised concerns, such as Morgan Stanley’s Mike Wilson, who believes the consumer is ‘falling off a cliff.’ And the latest high-frequency data from Barclays shows card spending has taken another leg down.

As delinquencies rise, Cox Automotive forecasts that 1.5 million vehicles will be seized this year, up from 1.2 million in 2022. That’s still below pre-pandemic levels, but the numbers could soar if a recession materializes in 2024.

Bloomberg cited Bankrate data that shows consumers with excellent credit can lock in an average interest rate of around 5.07% for a new car and 7.09% for a used vehicle. Those with bad credit should expect a new car rate of 14.18% and 21.38% for a used car.

The perfect storm we described earlier this year is unfolding.

At least residential mortgage delinquency rates remain low. With elevated home prices, the incentive to default on a loan is limited.

So The Perfect Storm hasn’t hit residential real estate … yet. But with households needing $114,000 in annual income to afford a typical home …

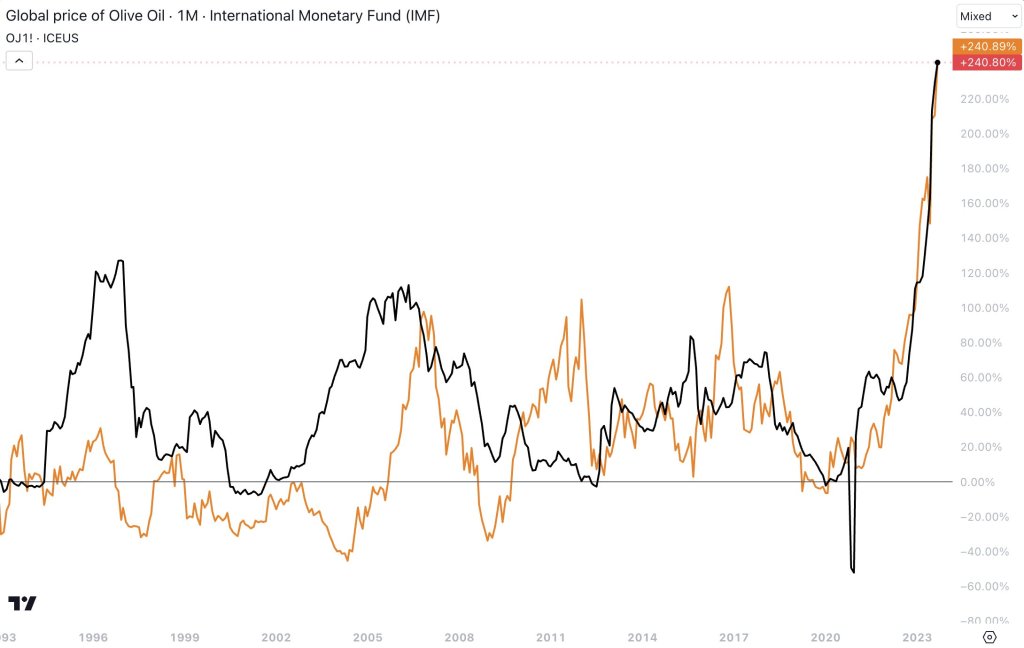

But at least home prices aren’t rising as fast as olive oil and orange juice!! Wow, that excesssive stimulypto by The Fed and Federal government is really screwing things up in the economy.

Biden is like George Clooney in “The Perfect Storm” sending the US out into stormy, violent seas while obessing about Ukraine and protecting Iran/Hamas.

Well, the San Francisco 49ers are playing the Cleveland Browns today with the Browns missing injured RB Nick Chubb and QB Deshaun Watson, replacing them with QB Dorian Thompson-Robinson (aka, Do Not Resuscitate or DNR) and RB Jerome “Exploding Pinto” Ford. ESPN gives the Browns a 26% chance of winning. I am amazed it is that high!

But back to economic news!

Gold is soaring due to the instability in the Middle East (Iran/Hamas/Hezbollah attacks on Israel). Let’s see if Israel continues it assault on Gaza or not.

Janet Yellen, Biden’s Treasury apparatchik, was at the IMF/World Bank meetings in Marrakesh (yes, former students are expecting me to like Crosby, Stills and Nash “Marrakesh Express” but I detest CS&N). Instead, here is Them with Here Comes The Night which is more fitting about risks in the global economy.

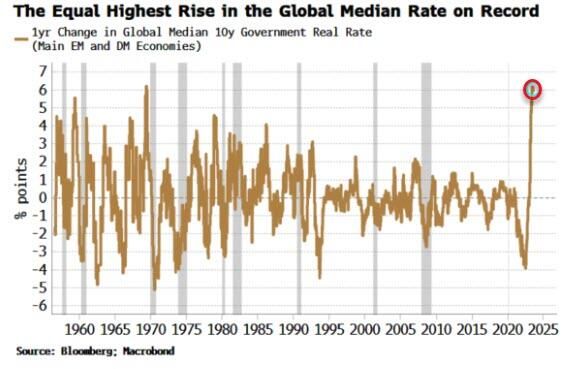

The heavy debt burdens of advanced economies — from the United States to China and Italy — was a recurrent theme in the meetings, which came after financial markets in recent weeks pushed U.S. bond yields higher. Italian central bank governor Ignazio Visco said there was an impression markets were “reevaluating the term premium” as investors become more nervous about holding longer-term debt.

JPMorgan chair of global research Joyce Chang put it another way. “The bond vigilantes are back, and the Great Moderation is over,” she told a panel of the two-decade era of relative economic calm before the 2008/09 financial crisis.

The Federal Reserve still hasn’t shrunk their massive balance sheet and removed the Covid stimulus. Call it lack of Fed retreat.

And mortgage rates continue to rise, up 174% under Stumblin’ Joe Biden despite The Fed not really shrinking their balance sheet.

I may be the only person in the US cheering for House Republicans being at an impasse over House Speaker. Why? Congress can’t approve massive spending bills with out a Speaker! Less spending, less inflation! There fixed inflation without The Fed.

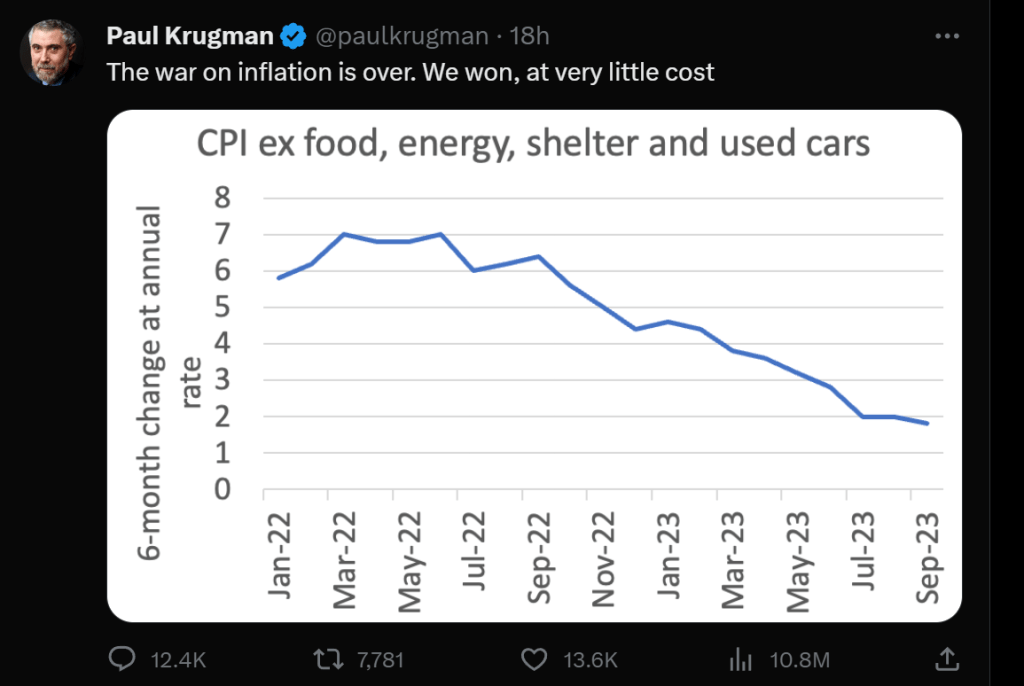

Paul Krugman, Nobel Laureate in economics and media celebrity, made a terrible claim yesterday when he pronounced that “The war on inflation is over. We won, at very little cost.” Krugman’s proclamation was trumpeted by The View’s Joy Behar Joy who claimed that everything is going great in the country! The economy is “booming” and people are having an “easier time” putting bread on the table. Huh? Easier than a month ago maybe, but not easier since 2021 under Bidenomics.

Hmm. Suppose that during World War II the Germans had stopped after they invaded and captured Paris on June 14, 1940. The war could have been over, but France was lost to Germany amidst thousands of dead and loss of property. That is not a victory, but a crushing defeat.

Just like my Paris example, Krugman’s claim the war on inflation is over and we won AT VERY LITTLE COST was grossly misleading and a big kerplunk (thud). Why? For one, the average American family is $7,400 POOR than in January 2021 when Biden became President. So, it looks like we know the cost of inflation and it was steep, not “very little cost.” Well, very little cost to elitist millionaires like Krugman.

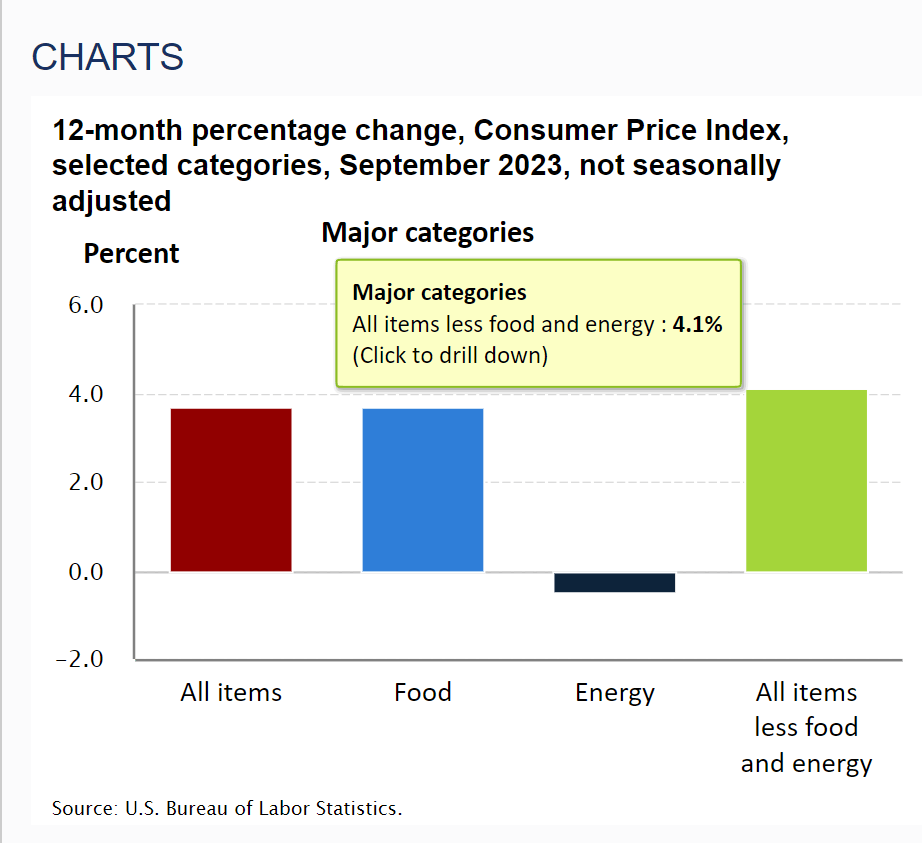

Krugman loves the recent inflation report from the BLS. Specifically, the 12-month change in the Consumer Price Index Less Food And Energy for September was 4.1%. Krugman focuses on the recent 6-month change being less than 2%. In Krugman’s mind, this is victory … core inflation has been tamed and inflation is at The Fed’s target rate of 2%.

But before Krugman pops the champagne cap on the 1959 Dom Perignon for $42,350 (while the rest of us are drinking E&J Gallo’s Thunderbird), bear in mind that he is referring to the RATE OF GROWTH in prices, not the highly elevated levels of prices. Victory against inflation would be if prices returned to December 2020 levels.

I pointed out yesterday that “real” wages contracted 0.1% YoY (after 3 months positive) in September. It is important to note that real wage growth was negative from 2021 until 3 months ago, but has gone negative yet again. Victory??

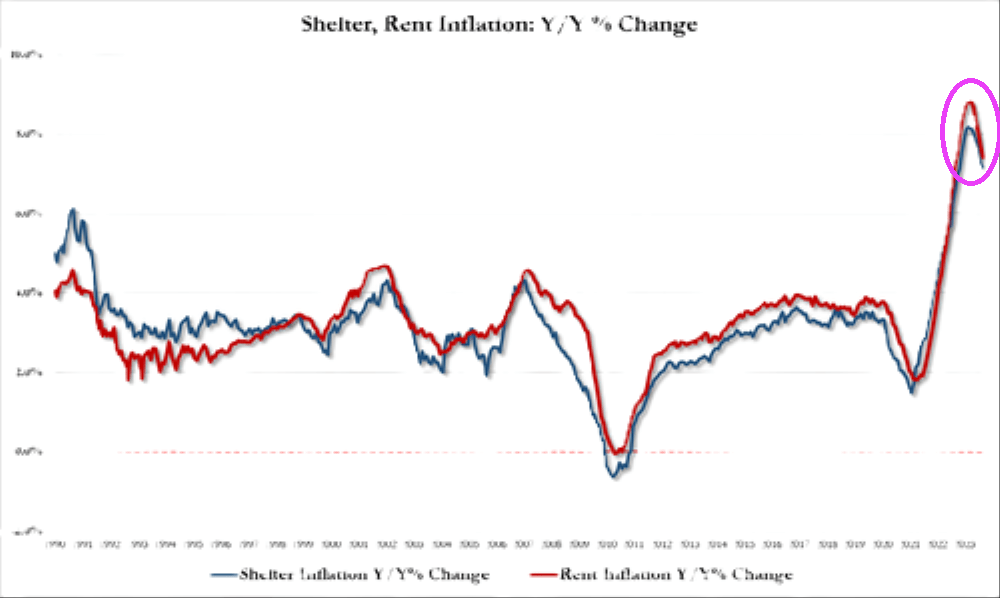

Krugman prefers core inflation, removing food, housing and energy. You know, the three things most Americans actually care about. Take shelter (or rent of residence) where rent is growing at a sizzling 7.1% YoY.

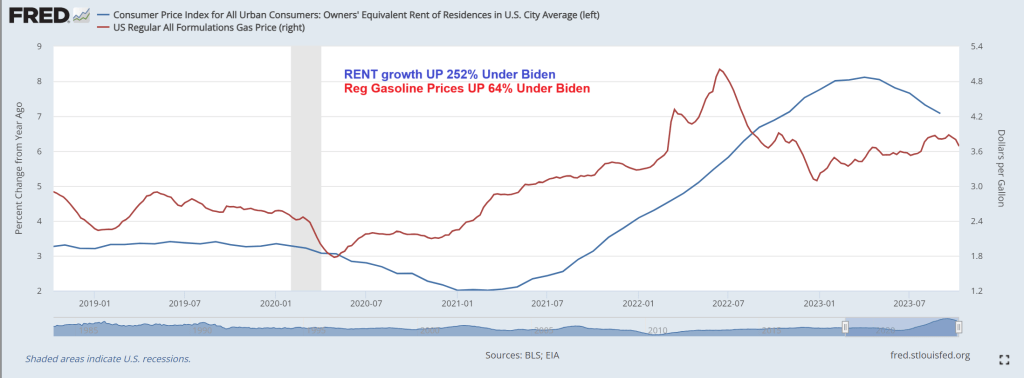

Under Biden and Congress’ reckless spending splurges (and inane Federal energy policies), regular gasoline prices are up 64%. Growth in rent of residence has grown 252%! So, Professor Krugman, Americans are far worse off than before Biden was President.

If prices return to December 2020 (or pre-Covid levels), I will declare a victory. But for right now, symbollically, the German army is occupying France and Paris with horrible suffering for the French people. In other words, Americans are still far worse off under Biden even though inflation is finally slowing.ew

Speaking of France and World War II, maybe we should consider Joe Biden as today’s Pierre Laval, leader of Vichy France since Biden seems more concerned with pleasing Klaus Schwab and The World Economic Forum than America’s middle class and low wage worker (like Laval was concerned with that German leader Adolf Hitler thought).

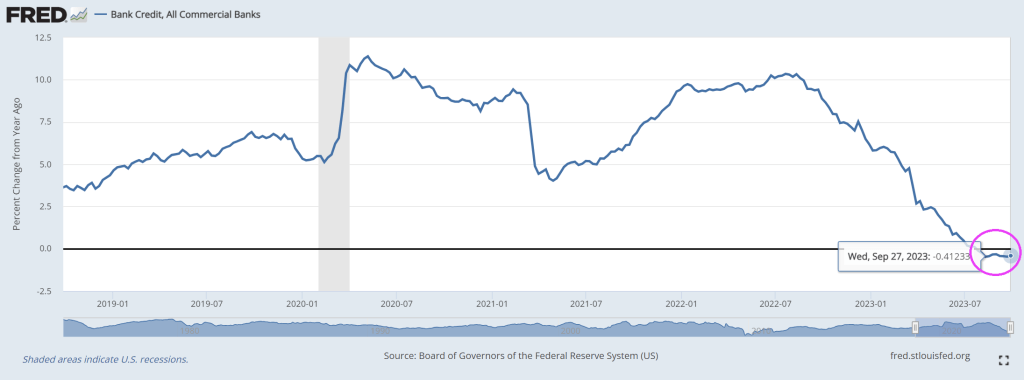

Bidenomics is failing catestropically. Example? As interest rates rise to fight Biden’s Federal spending splurges, bank credit growth slowed to -0.41% YoY for the 10th straight week of negative credit growth.

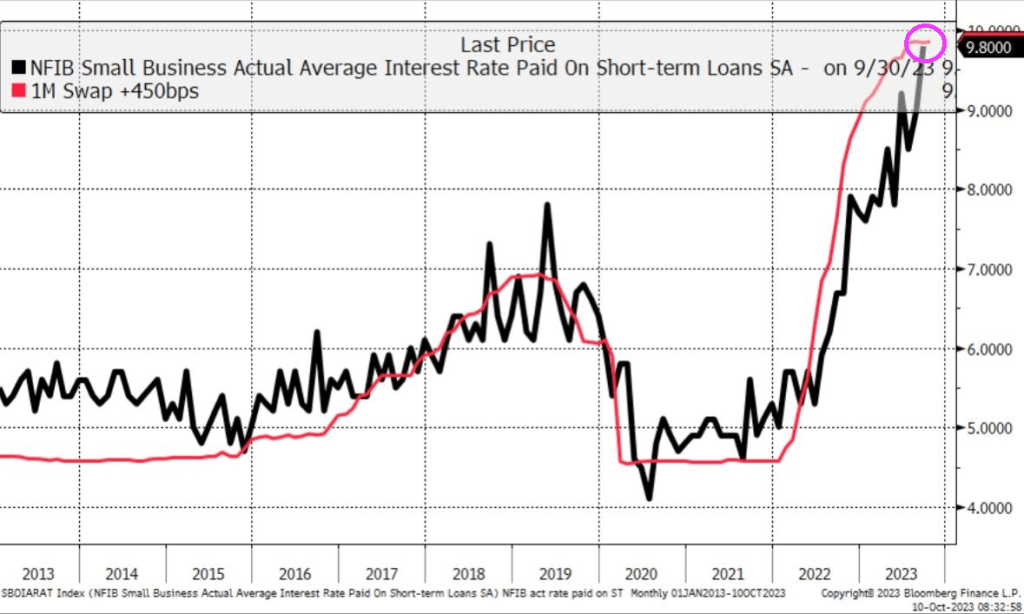

While interest paid on short-term loans almost 10%!!

“Jimmy, watch me tank the economy even worse than you did!”

Former Fed Chair Janet Yellen, notorious for leaving rates too low for too long (TLTL) and then suddely raising them after Donald Trump was elected President, wants rates lower again for much longer. Make rates great again (MRGA?).

YELLEN SAYS DEBT SERVICE COSTS WILL BE 1% OF GDP FOR THE NEXT DECADE. – Reuters

Her statement implies that the economy will be strong and the government will run budget surpluses, or interest rates will be near zero for the next ten years.

Instead of guessing what she is pondering, we do some math and arrive at the only possible answer.

The Government Can’t Afford Today’s Interest Rates

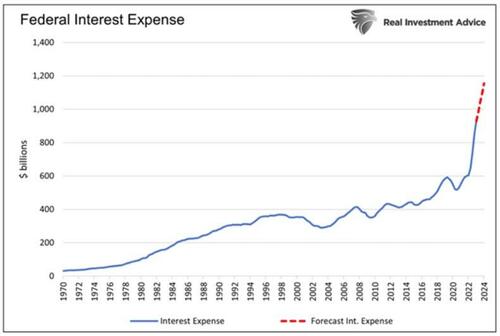

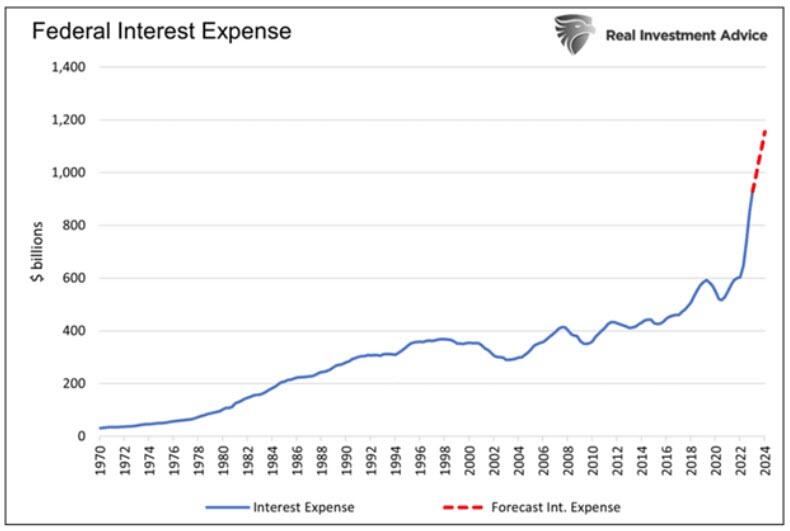

Before walking through various scenarios to figure out what Yellen may be implying, it’s helpful to provide background on what drives her mindset. In our article The Government Can’t Afford Higher For Longer, Much Longer, we shared the following graph and commentary:

Total federal interest expenses should rise by approximately $226 billion over the next twelve months to over $1.15 trillion. For context, from the second quarter of 2010 to the end of 2021, when interest rates were near zero, the interest expense rose by $240 billion in aggregate. More stunningly, the interest expense has increased more in the last three years than in the fifty years prior.

The graph above is just the tip of the fiscal iceberg. Every month, lower-interest-rate debt matures and will be replaced with higher-cost debt.

Higher interest rates are an additional funding burden for the federal government. Janet Yellen surely understands the damaging situation and grasps that higher interest rates are not feasible given current debt levels.

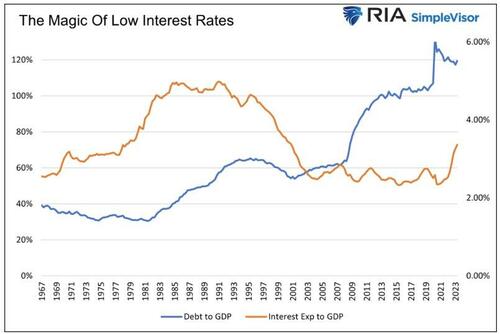

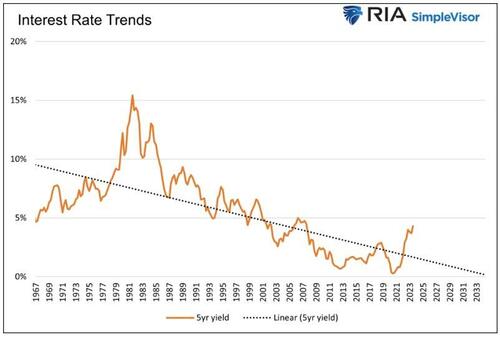

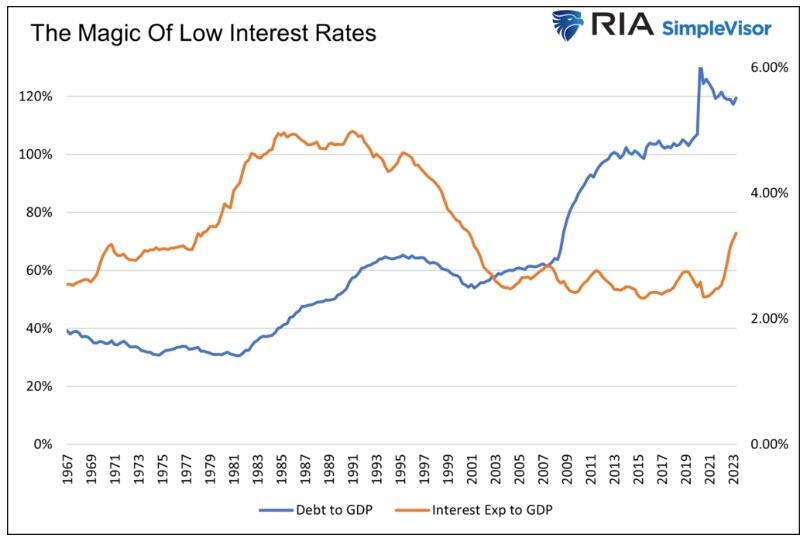

Low-Interest Rates Make Debt Manageable

The government’s debt-to-GDP ratio has climbed three-fold since 1966. Yet, until very recently, the ratio of the federal interest expense to GDP was at its lowest level since 1966.

While the amount of debt rose sharply, its cost was offset by rapidly falling interest rates. As a result, higher debt levels were very manageable.

If $1 trillion of debt with a 4% coupon matures, and the Treasury replaces it with $2 trillion at a 2% coupon, the interest expense doesn’t change despite doubling the debt. While a simplified example, that is essentially what has occurred for the last 30 years.

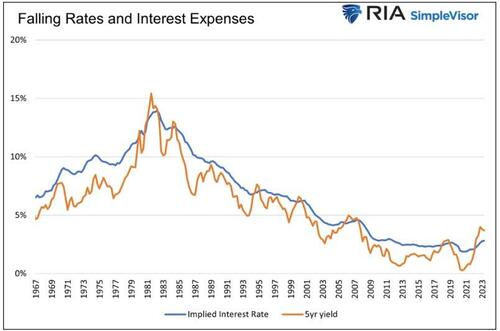

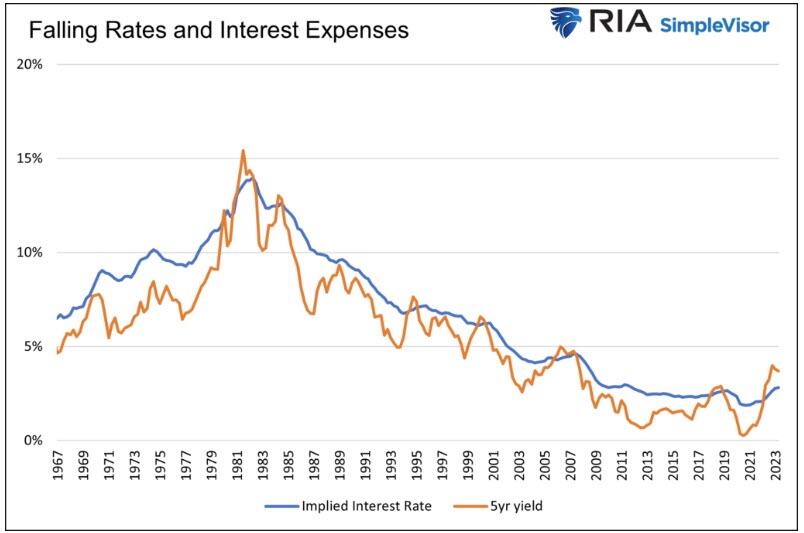

The following graph compares the 5-year U.S. Treasury note and the implied cost of funding the government’s debt.

In time, as lower interest rate debt is replaced with higher interest rate debt, the benefits of lower rates work in reverse.

“Debt Service Costs At 1%” – Is It Possible?

We return to Janet Yellen’s message and discuss why she is likely correct.

Balanced Budgets and Unicorns

In the five years leading up to the pandemic, nominal GDP grew at 5.03% annually. Let’s optimistically assume growth continues at 5% consistently for the next ten years. Now, let’s tack on an even bolder presumption: the government balances its budget every year for the next ten years. Thus, the amount of outstanding debt will remain constant. For context, in the last 57 years, there has only been one year in which the amount of debt has not increased.

In such a far-fetched scenario, the debt-to-GDP ratio would drop considerably to 70%. However, interest costs would equal 2% of GDP. Such is much better than the current 3.36% but double Janet Yellen’s 1% objective.

Budget surpluses for the next ten years would lower interest expenses even more and possibly get the interest expense to GDP ratio to 1%. However, the odds of a unicorn spraying rainbows across the sky and the government running a surplus are the same: zero percent.

Consequently, we exclude surpluses as a viable way to reduce the interest expense to a more manageable level.

Budget Deficits And The Magic Of Low-Interest Rates

Balanced budgets or surpluses are unrealistic, given the political and fiscal trends. Further, the economy relies heavily on government spending. While fiscal prudence would be good in the long run, the short-run effect would be a recession.

Instead of using pipe dreams as scenarios, let’s get realistic. The more likely, albeit still optimistic, scenario involves the debt and GDP growing at the same rate. Let’s also assume interest rates remain at current levels. In this exercise, we assume an average borrowing cost of 4.75%, which is a little below the current weighted average funding cost for the government. Under this “realistic” picture, interest expense would climb to 5.6% of GDP.

The only logical variable in the equation that can make Janet Yellen correct is the future interest rate.

To arrive at Yellen’s 1% figure, assuming debt grows at the rate of GDP, interest rates must be much lower.

In time, a weighted average interest rate of 0.85% would put the nation’s interest expense at 1% of GDP.

When Janet Yellen tells us the debt cost to GDP ratio will be 1% over the next ten years, she is really saying interest rates will be below 1% for the next ten years.

Therefore, Janet Yellen must believe that the recent spike in inflation and yields is an anomaly. If the pre-pandemic economic and interest rate trends resume, she will be correct.

Summary

Part of Janet Yellen’s job is to exude confidence to its investors. In this case, it means telling the public that the current jump in interest expenses will not last. While she would probably prefer to be straightforward and say interest rates will be much lower, she must also be sympathetic to the Fed’s job of getting inflation down. Therefore, to walk the party line, she must speak in code, so to speak.

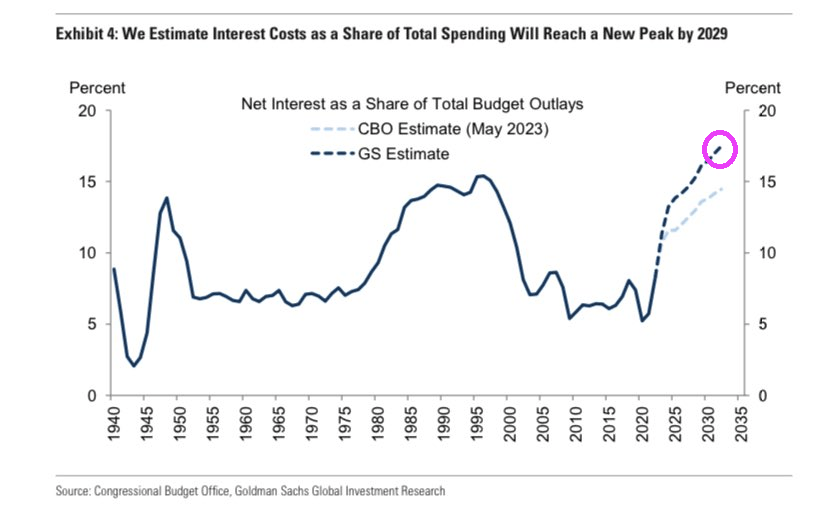

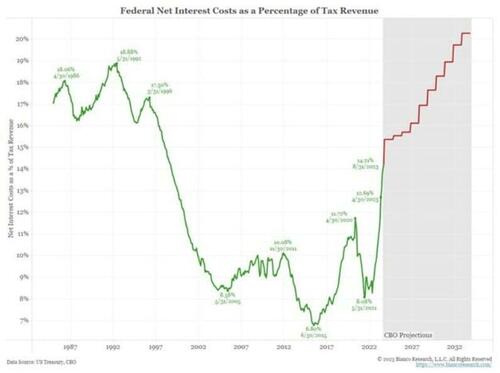

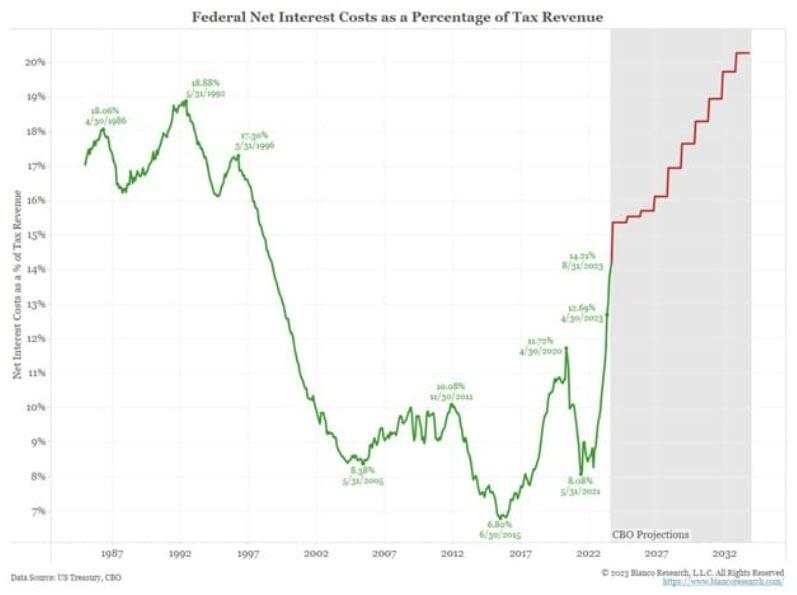

Whether you agree with Yellen’s projection or not, the following CBO graph projecting interest costs as a percentage of tax revenues, courtesy of Bianco Research, highlights that the government has no choice but lower for longer interest rates. The current level of interest rates will bankrupt the nation.

This makes sense. Two global elitists who look down with disdain and want to reprogram MAGA voters. Can we reprogram the MRGA types into letting rates float to market.

Joe Biden, who has always been a compulsive liar but at least sounded cognicent, is now babbling and whispering that Bidenomics works. But for who?

Clearly not for first time homebuyers or people looking to move. Bankrate’s 30-year mortgage rate is up to almost 8%, the highest since July 2000 and Willy Slick Clinton. That is a 176% increase in mortgage rates under the most inept “Economic Sheriff” in history.

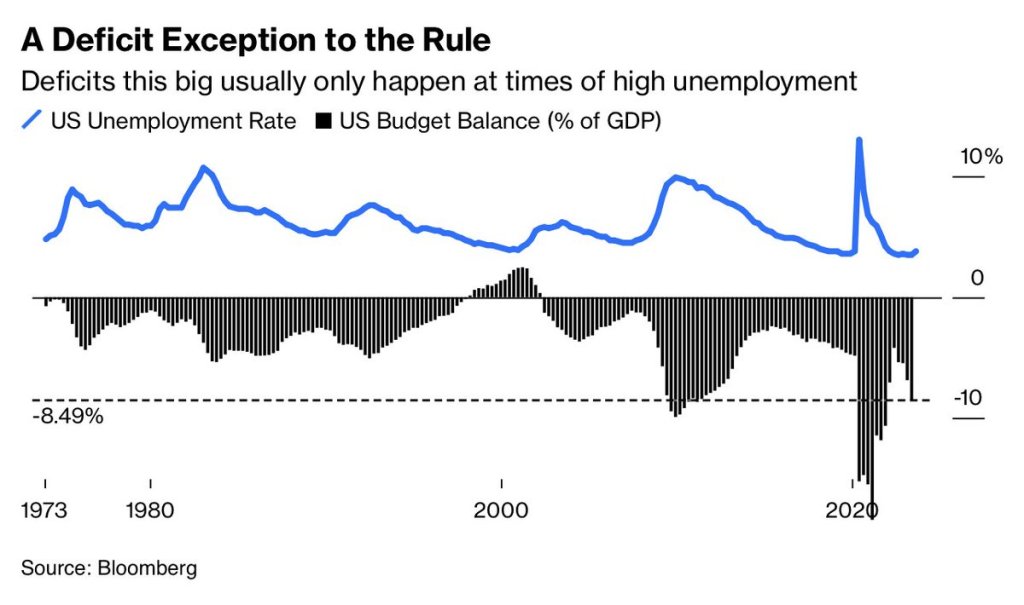

Deficits? Deficits (which Biden makes outlandish claims) are usually only this big at times of HIGH unemployment and recessions. So, are the staggering deficits under Biden a precursor to a hard landing (recession)? Don’t listen to what Biden or KJP say!!!

Biden’s outlandish claims that he single handedly reduced the deficit by the most in history is, well, typical Biden bloviating. Actually, tax receipts soared after Covid lockdowns ended. Period. Now that stimulus is wearing out, deficits are climbing again.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.