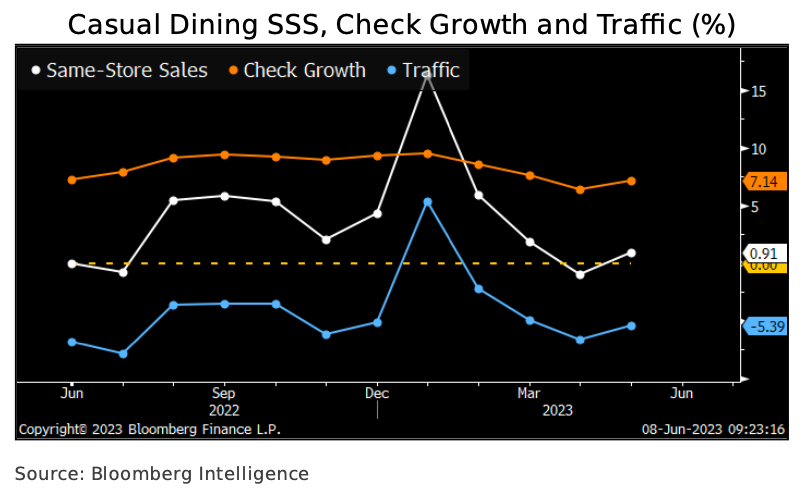

Bloomberg Intelligence’s Michael Halen penned a new note titled “2H Restaurant Sales: Inflation Killing Appetites.” It outlines, “Consumer spending finally buckles under more than two years of inflation and price hikes,” and the likely result is a trade-down of casual-dining chains like Brinker and Cheesecake Factory for quick-service chains like McDonald’s and Wendy’s.

The trade-down, which could start as early as this summer, is expected to dent consumer spending in restaurants such as Cheesecake Factory, Texas Roadhouse, and at brands operated by Brinker and Darden, Halen said.

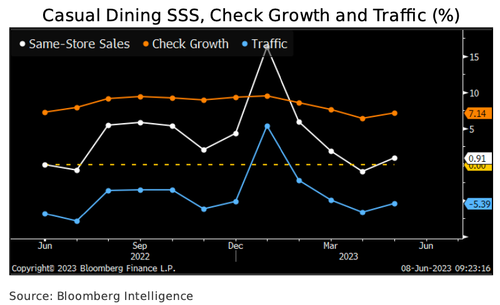

Casual-dining industry same-store sales rose just 0.9% in May, according to Black Box Intelligence, as traffic dropped 5.4%. We expect cash-strapped low- and middle-income diners to cut restaurant visits and checks through year-end due to more than two years of real income declines and ballooning credit-card balances.

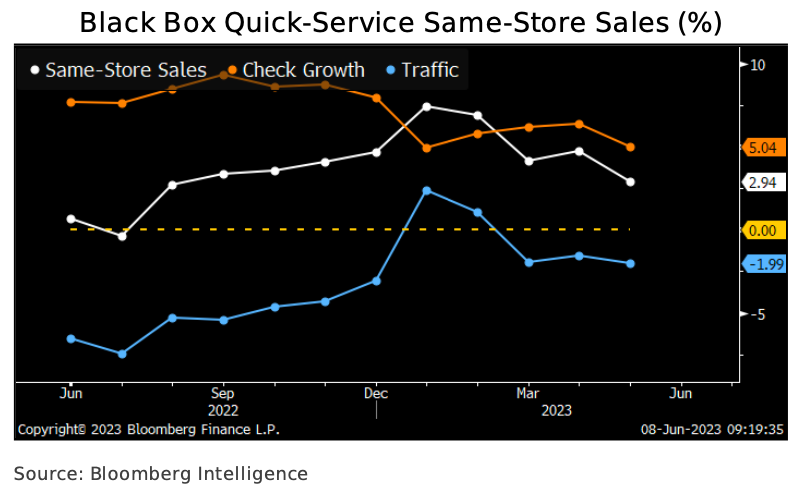

Halen provides more details about quick-service restaurants to fare better than causal-dining ones as “consumer spending finally buckles.”

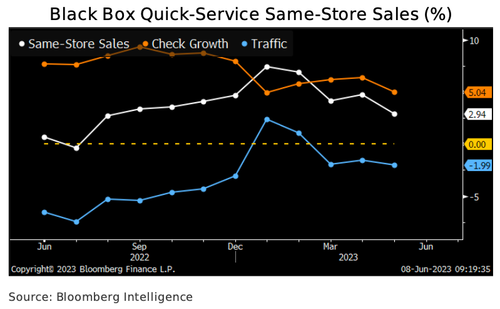

Quick-service restaurants’ same-store sales could moderate with consumer spending in 2H but should fare better than their full-service competitors. Results rose 2.9% in May, according to Black Box data, as a 5% average-check increase was partly offset by a 2% guest-count decline. Check- driven comp-store sales gains are unsustainable, and we think inflation and menu price hikes will motivate low- and middle-income diners to reduce restaurant visits and manage their spending in 2H. On Domino’s 1Q earnings call, management said lower-income consumers shifted delivery occasions to cooking at home. Still, a trade-down from full-service dining due to cheaper price points may cushion the blow.

McDonald’s, Burger King, Wendy’s, and Jack in the Box are among the quick-service chains in Black Box’s index.

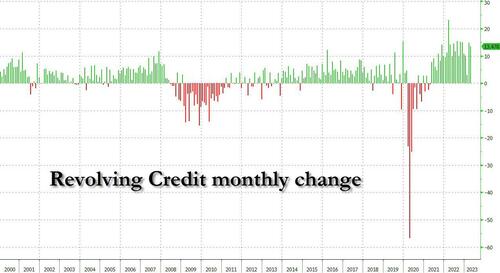

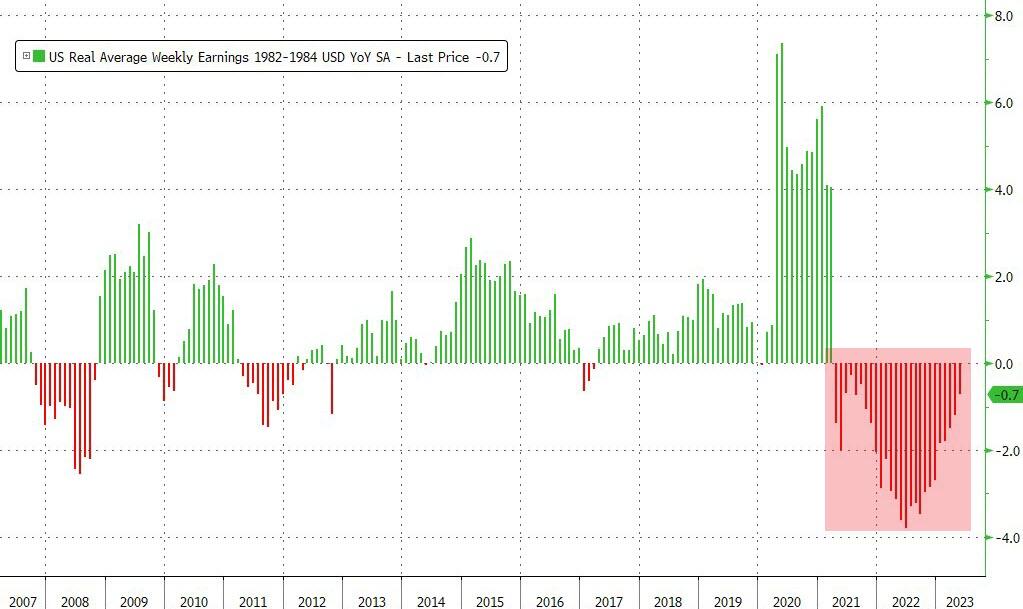

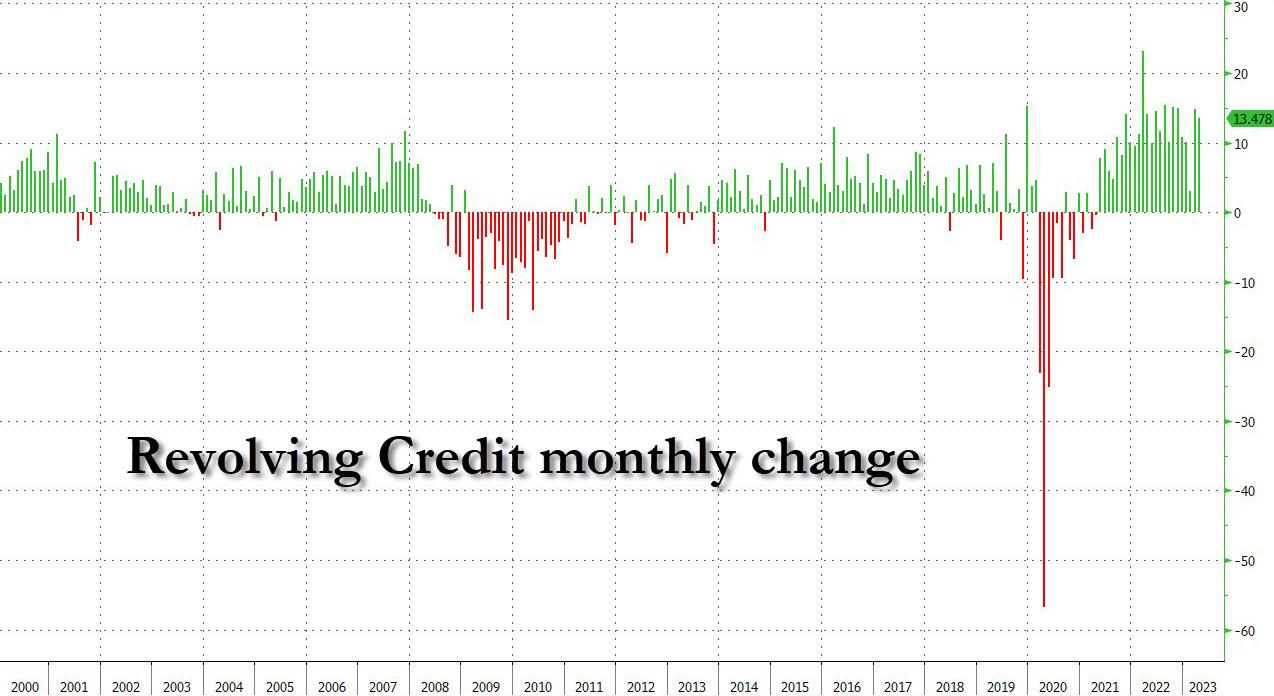

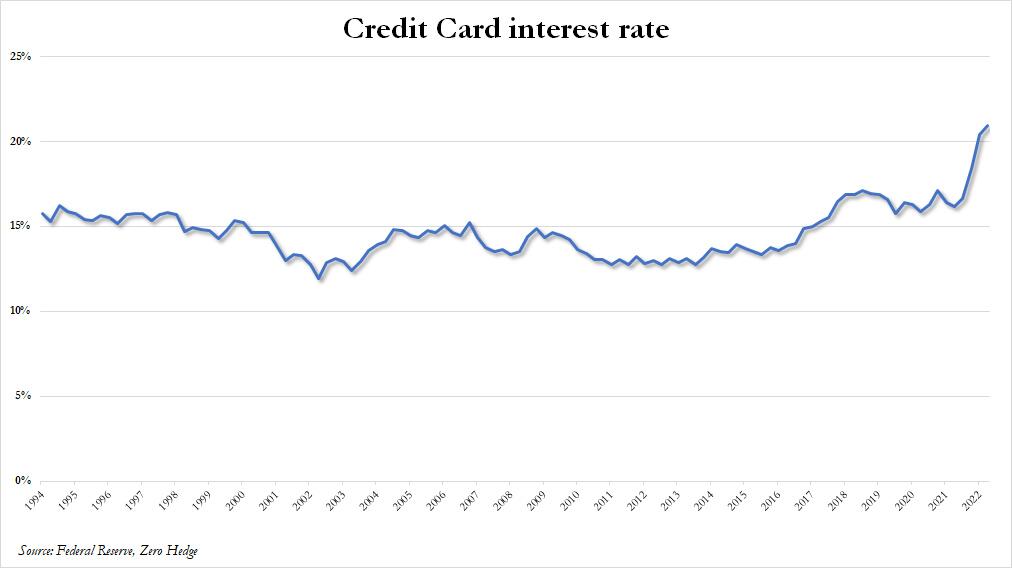

The latest inflation data shows consumers have endured the 26th straight month of negative real wage growth. What this means is that inflation is outpacing wage gains. And bad news for household finances, hence why many have resorted to record credit card usage.

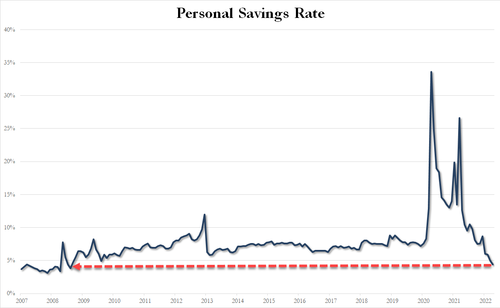

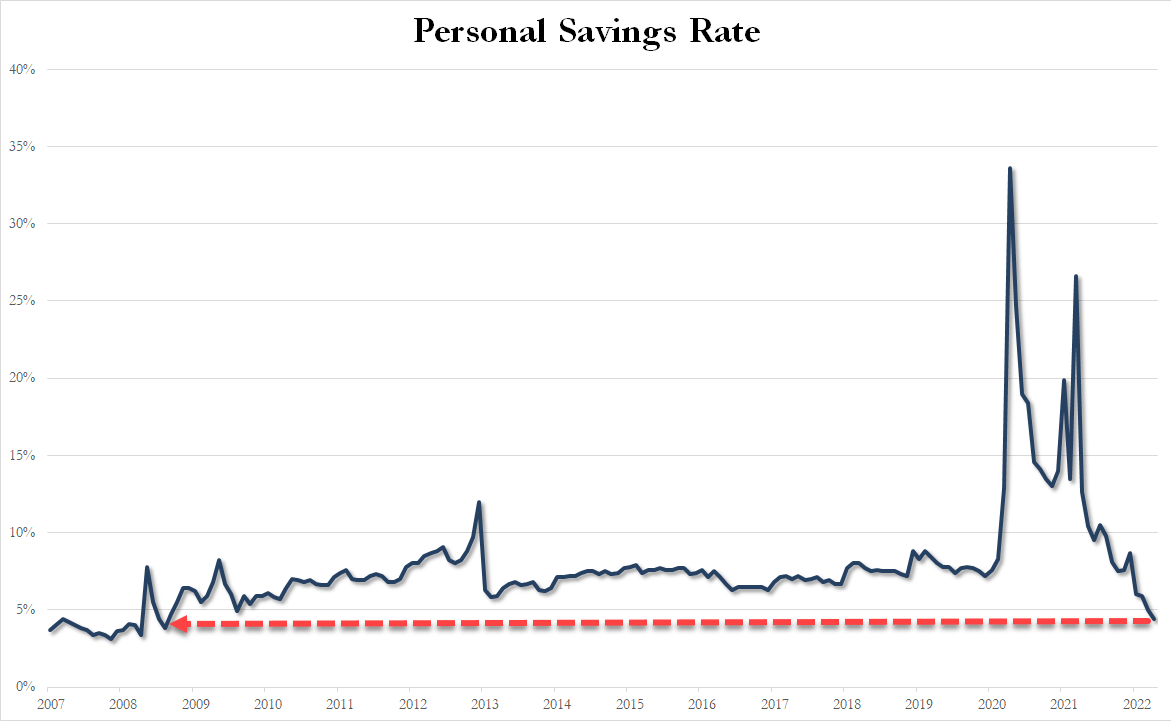

And the personal savings rate has collapsed to just 4.4%, its lowest level since Sept. 2008 (the dark days of Lehman). And why is this? To afford shelter, gas, and food, consumers are drawing from emergency funds due to the worst inflation storm in a generation.

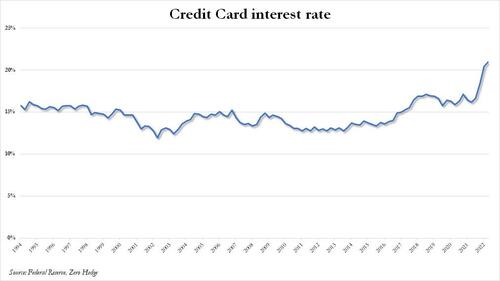

As revolving consumer credit has exploded higher and the last two months have seen a near-record increase…

… even as the interest rate on credit cards has jumped to the highest on record.

With record credit card debt load and highest interest payments in years, plus depleted savings, oh yeah, and we forgot, the restart of student loan payments later this year, this all may signal a consumer spending slowdown at causal diners while many trade down for McDonald’s value menu. Even then, we’ve reported consumers have shown that menu items at the fast-food chain have become too expensive.

On the commodity side, Spot Silver is up 1.46%. Iron Ore is up 1.60%, but I don’t think my neighbors would appreciate me taking delivery on 10 tons of iron ore on my driveway! Heating oil is up 2.90%.

On the crypto side, bitcoin is up 20.84 (0.08%) with Ethereum up slightly more.

Bitcoin and silver doing well as the US Dollar loses ground since September 2022.

So, since the coronation of King Barack in 2009, US public debt has grown by 200% and just breached $32 trillion. US M2 Money is up 152% since Obama/Biden and The Fed’s Balance sheet is up 275% and M2 Money Velocity is down -30% since Obama/Biden.

Fridays are always fun in the market. Bitcoin is up 3.23% as The Fed took a pause yesterday.

Note that bitcoin and gold are moving together since March 2023 as the US Dollar deteriorates. And expectations of Fed rate hikes (yellow dashed line) increases.

On the housing front, the University of Michigan Buying Conditions for Houses rose to 50, far below the 142 level before Covid and Gov’t Gone Wild!!

Fed Governor Christopher Waller said Friday headline inflation has been “cut in half” since peaking last year, but prices excluding food and energy (aka, CORE inflation) has barely budged over the last eight or nine months.

“That’s the disturbing thing to me,” Waller said during a question-and-answer session following a speech in Oslo, Norway. “We’re seeing policy rates having some effects on parts of the economy. The labor market is still strong, but core inflation is just not moving, and that’s going to require probably some more tightening to try to get that going down.”

At a separate event Friday, Richmond Fed President Thomas Barkin said inflation remained “too high” and was “stubbornly persistent.”

“I want to reiterate that 2% inflation is our target, and that I am still looking to be convinced of the plausible story that slowing demand returns inflation relatively quickly to that target,” Barkin said in a speech in Ocean City, Maryland. “If coming data doesn’t support that story, I’m comfortable doing more.”

The Federal Open Market Committee paused its series of interest-rate hikes Wednesday, but policymakers projected rates would move higher than previously expected in response to surprisingly persistent price pressures and labor-market strength.

The consumer price index this week showed headline inflation slowed, but core prices excluding food and energy continued to rise at a pace that’s concerning for Fed officials. Employers continued adding jobs at a rapid clip in May, and job openings climbed in April, recent data showed.

Barkin warned that prematurely loosening policy would be a costly mistake.

“I recognize that creates the risk of a more significant slowdown, but the experience of the ’70s provides a clear lesson: If you back off inflation too soon, inflation comes back stronger, requiring the Fed to do even more, with even more damage,” he said. “That’s not a risk I want to take.”

Policy Report

Separately, the Fed released a new report Friday that said tighter US credit conditions following bank failures in March may weigh on growth, and that the extent of additional policy tightening will depend on incoming data.

“The FOMC will determine meeting by meeting the extent of additional policy firming that may be appropriate to return inflation to 2% over time, based on the totality of incoming data and their implications for the outlook for economic activity and inflation,” the Fed said in in its semi-annual report to Congress.

Read More: Fed Says Tighter Credit Conditions to Weigh on US Growth

The Fed report, which provides lawmakers with an update on economic and financial developments and monetary policy, was published on the central bank’s website ahead of Chair Jerome Powell’s testimony before the House Financial Services Committee on June 21. He will appear before the Senate banking panel the following day.

“Evidence suggests that the recent banking-sector stress and related concerns about deposit outflows and funding costs contributed to tightening and expected tightening in lending standards and terms at some banks beyond what these banks would have reported absent the banking-sector stress,” the report said.

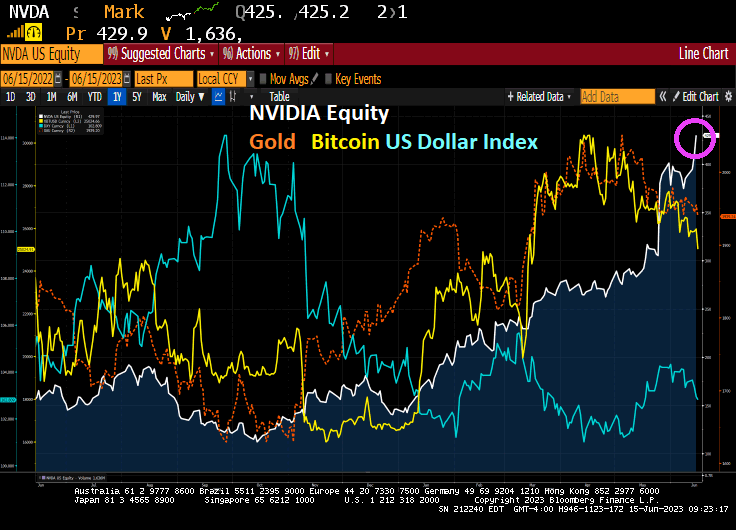

The Artificial intelligence (AI) boom is resulting in Nvidia’s stock soaring to 429.9. At the same time, Bitcoin (yellow), the US Dollar (blue) and Gold (gold) are declining.

Of course, markets are dynamic and gold/silver are likely to start up again along with bitcoin and other cryptos..

The leading crypto today? Dogecoin!

AI versus no intelligence. I give you Resident Joe Negan.

The Fed will annouce a pause at today’s FOMC meeting, so don’t look for mortgage rates to do much today.

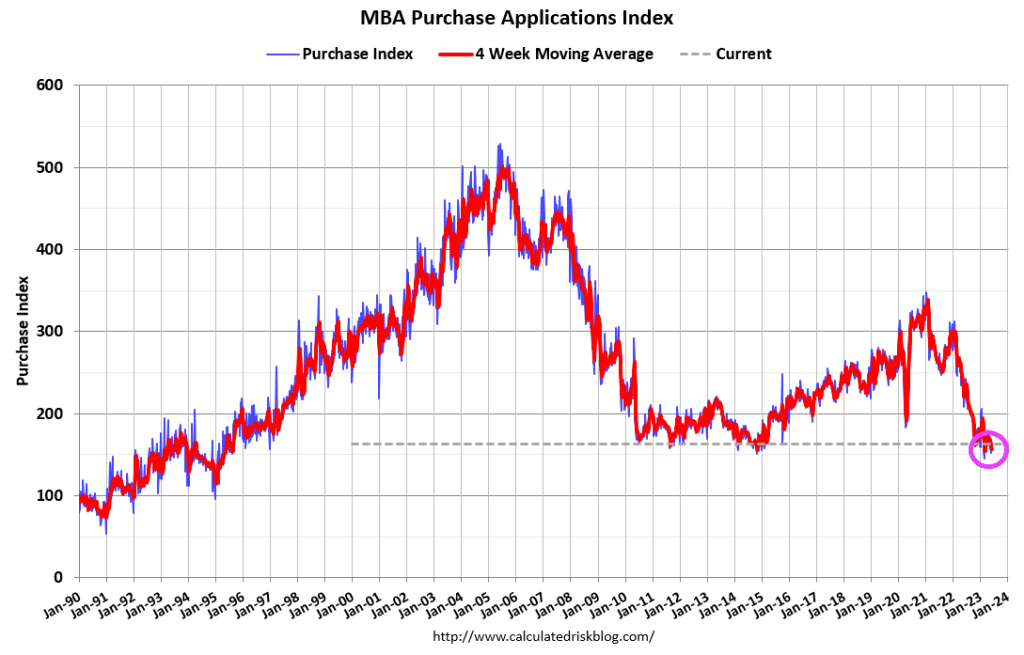

Mortgage applications increased 7.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 9, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 7.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 18 percent compared with the previous week. The Refinance Index increased 6 percent from the previous week and was 41 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 8 percent from one week earlier. The unadjusted Purchase Index increased 17 percent compared with the previous week and was 27 percent lower than the same week one year ago.

Mortgage rates declined for the second straight week, with the 30-year fixed rate decreasing to 6.77 percent. Mortgage applications were up over the week, but remained well below levels from a year ago.

Joe Biden’s new nickname is “The 5 Million Dollar Bribe Man.” Sort of like Steve Austin.

Tomorrow is the Federal government’s inflation report. As it stands today, overall inflation is slowing as M2 Money growth crashed. Core inflation remains persisitently high (white line), rent is still getting worse (orange dotted line at 8.1% YoY. What about food? Online food prices are up 8.2% YoY.

Shopping online is a good place to find cheaper computers and appliances, but grocery prices are still rising at a fast clip.

Prices of consumer goods sold online fell 2.3% in May in the US, the ninth consecutive month of declines and the biggest drop since the pandemic started, according to data from Adobe Inc. That was mainly due to steep decreases in discretionary categories.

Essential items like food, pet products and personal care, however, are seeing persistent inflation. Online grocery prices increased 8.2% from last year — although the pace of inflation has been abating since peaking at 14.3% last September.

Americans have been shifting more of their discretionary purchases to services over the past year, cutting spending on items for the home.

Online prices for appliances were down 7.9% in May from last year, the largest drop in digital-prices data from Adobe going back to 2014. Online prices for computers slumped 16.5% and electronics were down 12%.

The Adobe Digital Price Index was developed with the help of Austan Goolsbee before he became president of the Federal Reserve Bank of Chicago this year. The gauge analyzes one trillion visits to retail sites and more than 100 million items to track price changes.

Yes, Biden and Congress have levied a devastating tax on Americans. Rent and food are two of the largest household expenditures and they are up 8.1-8.,2% YoY.

Nicolas Maduro of Venezuela must be envious of Joe Biden. I don’t think even Maduro has the stones to have his politiical opponent charged with espionage in the run-up to a Presidential election. Particularly when the US President has been bribed by China and Ukraine and has similiar sensitive document hoarding issues (at least Trump didn’t leave boxes of sensitive documents in a garage like Biden did when he keeps his Chevy Corvette).

So where do we sit today after Biden has signed the debt ceiling increase and massive spending splurge?

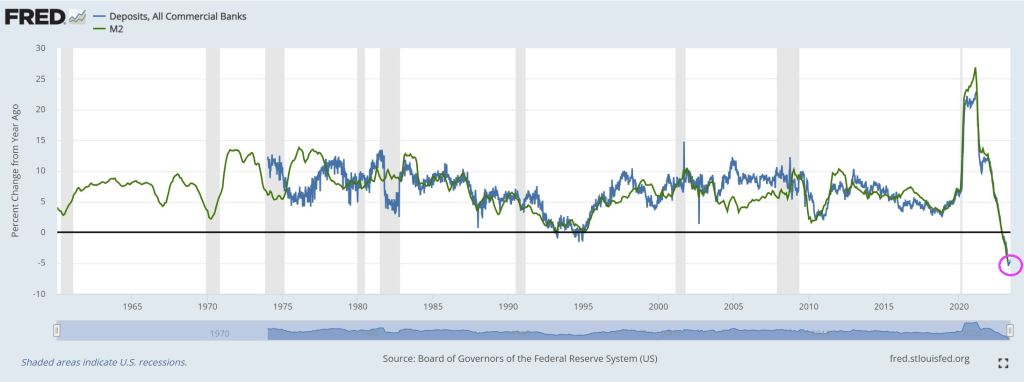

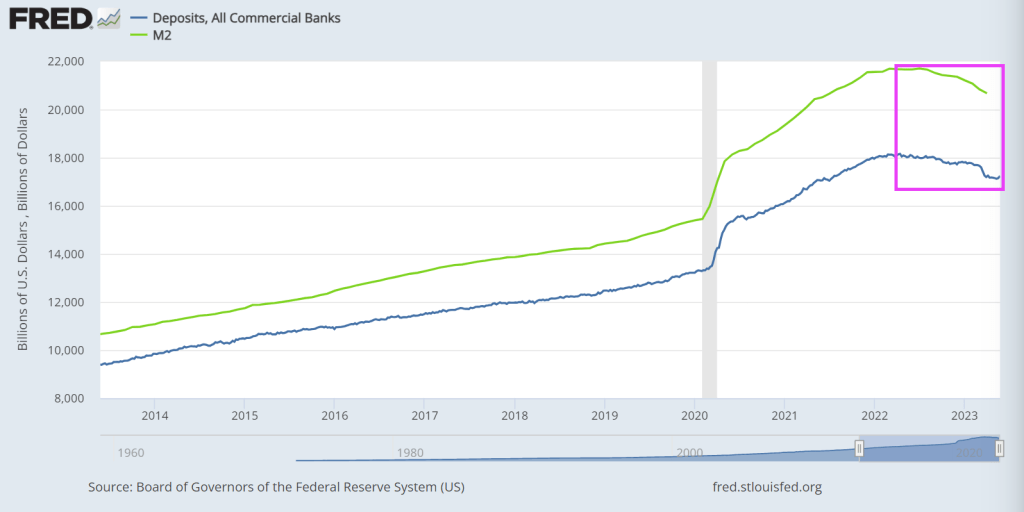

First, look at the crashing bank deposit problem. Well, the solution is for The Fed to fire up the money printing press! Keep on printing!

This not surprising if you have read Nobel Laureate George Stigler’s treastise on regulatory capture. Essentially, big corporations (big media, big tech, big banking, big pharma, big defense, big agriculture, etc.) essentially own Congress, the Biden Administration and Federal regulators. After all, Biden has been bribed with millions of dollars by China and Ukraine and, like a Banana Republic, has is avoiding prosecution and instead prosecuting his political opponent, Trump. Don’t worry, if they get Trump that will indict DeSantis for something.

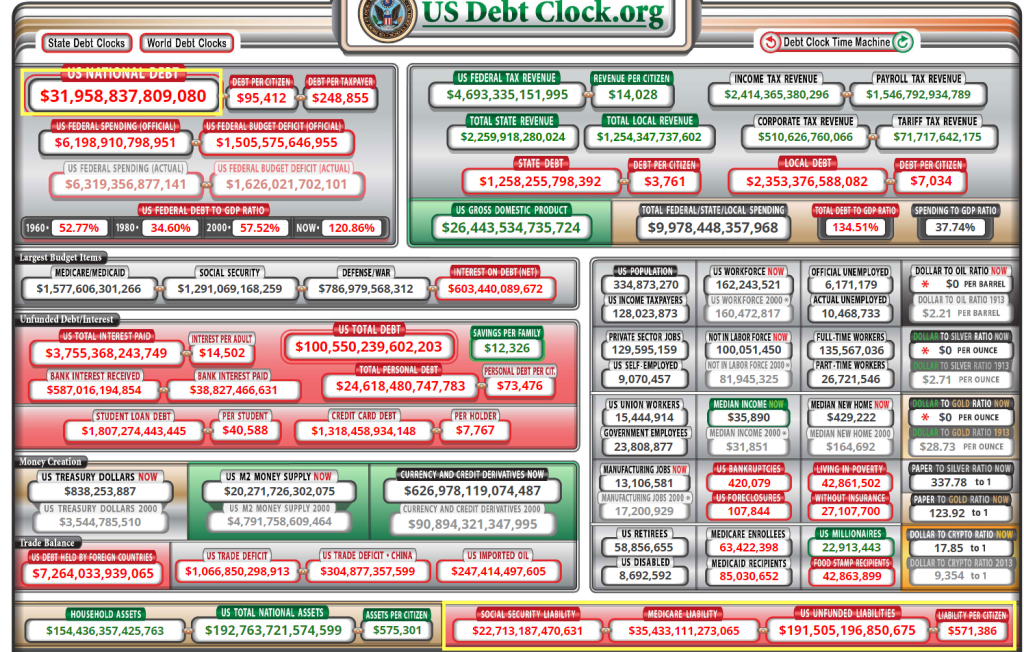

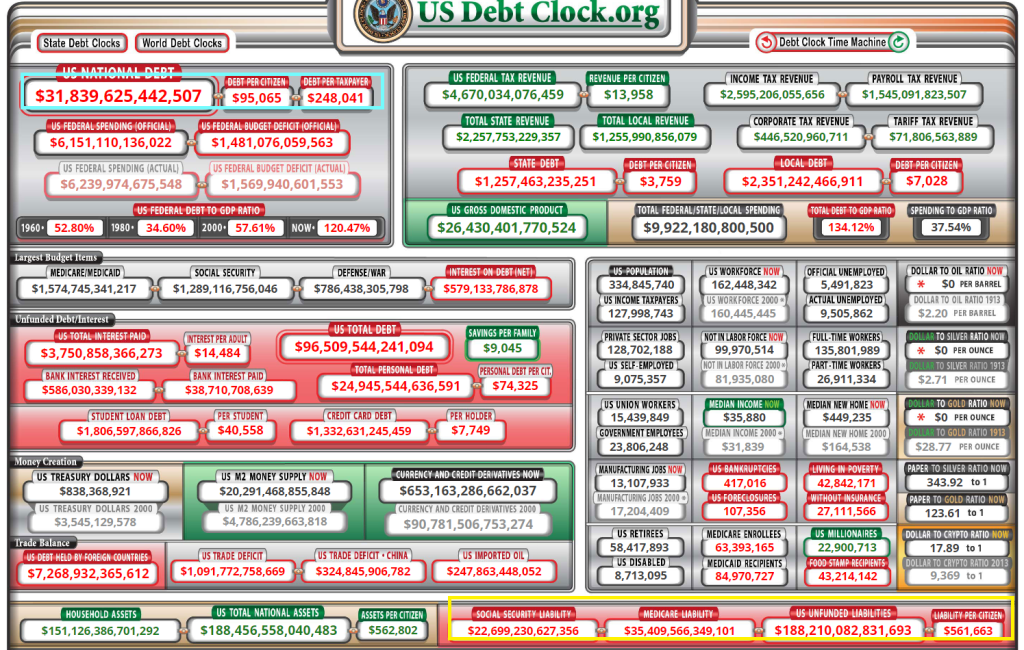

US debt stands at $31.8 TRILLION with $188 TRILLION in unfunded liabilities (which means higher personal taxes and much more debt).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.