As the US is engulfed in inflation while The Federal Reserve is engaged in trying to fight inflation (well, sort of), we are seeing markets taking a shellacking, particularly commodities.

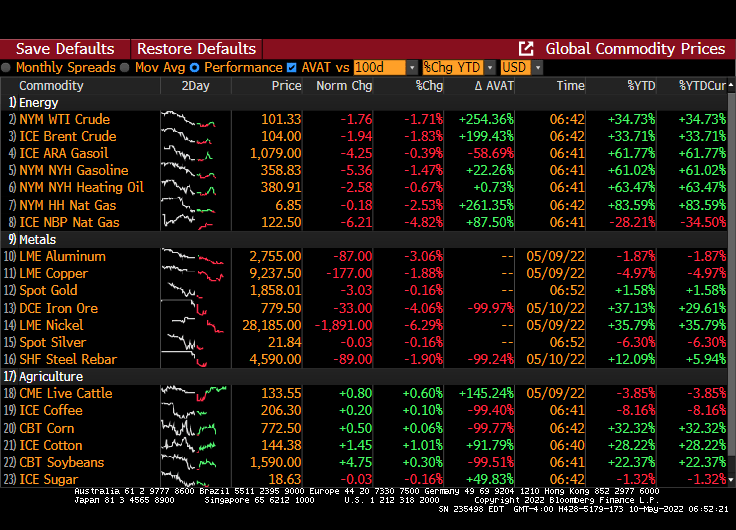

One indicator of a slowdown is declining commodity prices. Crude oil futures are down around -2.5%. Iron Ore is down -5% and steel rebar is down -3.21%.

Inflation numbers are due out Wednesday and are forecast to be 8.1% YoY (based on headline CPI). But combined with a slowing global economy, we get the dreaded “STAGFLATION.”

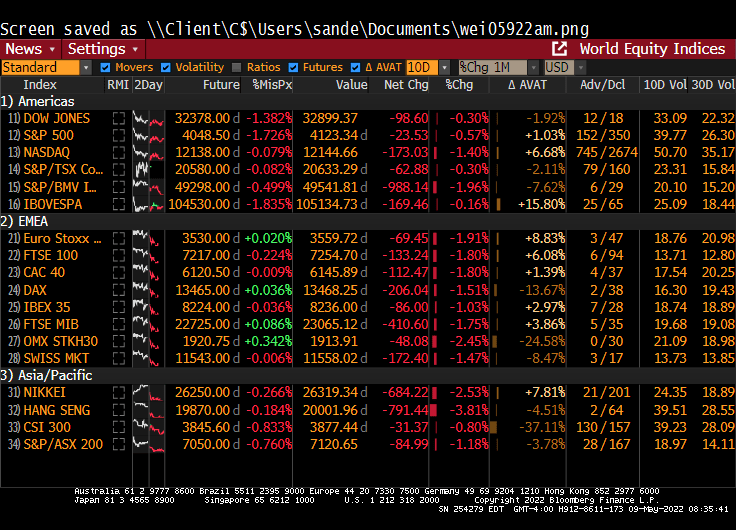

Meanwhile, the S&P 500 index futures are down around 1.726% for Monday open. Asian markets already got clobbered with the Hang Seng down almost -4%.

On the bond side, the 10Y Treasury Note yield rose to 3.20% early in the morning, but has retreated to 3.1447% as of 8:40am EST.

Both stock and bond market volatility measures are increasing.

So, is it a Blue Monday effect? Or global stagflation?

Perhaps Joe Biden and Fed Chair Jay Powell are channeling Dean Martin by letting us have it.

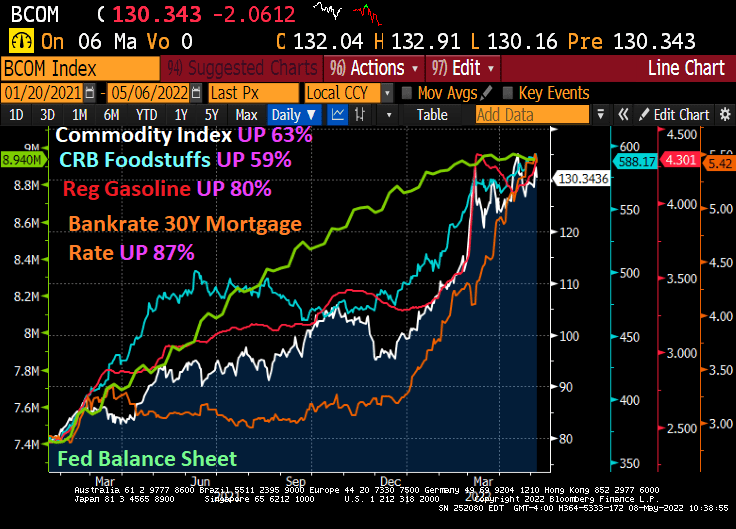

Since Obama’s 3rd term as President (aka, Biden’s installation as President on January 20, 2021), mortgage rates have risen 87%, regular gasoline prices have risen 80%, CRB foodstuffs are up 59% and Commodities are up 63%.

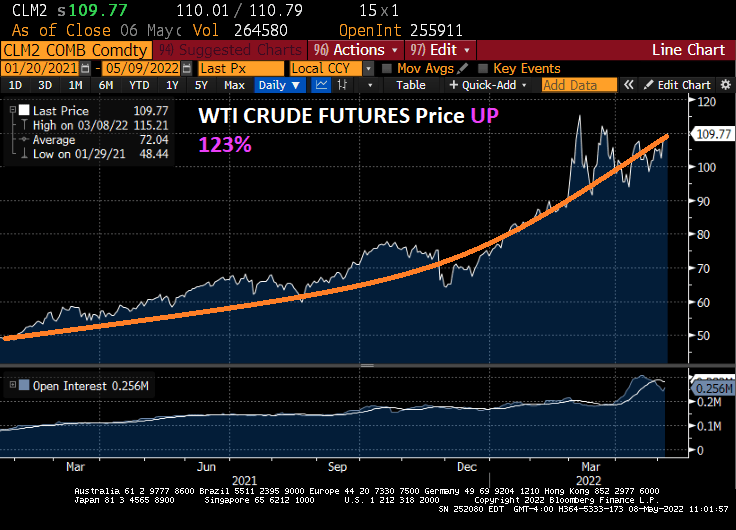

And don’t forget about America’s energy life force, WTI Crude Oil. It is UP 123% under Biden.

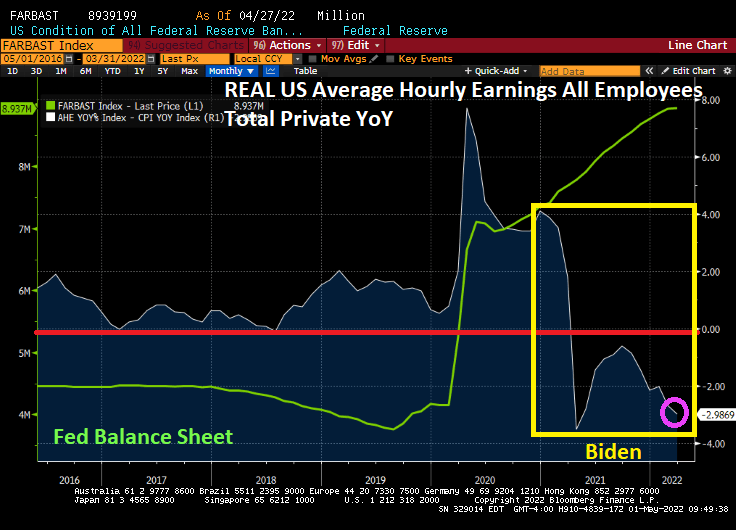

Trevor Noah was correct. EVERYTHING is more expensive under Biden. And REAL average hourly earnings YoY keeps declining.

REAL average hourly earnings YoY fell further to -3%.

Meanwhile, fertilizer prices, a key ingredient to food costs, is up 262% under Biden.

Today’s jobs report was better than expected, at 428k jobs added (versus 380k expected). Its just too bad Bidenflation is clubbing American workers to economic death.

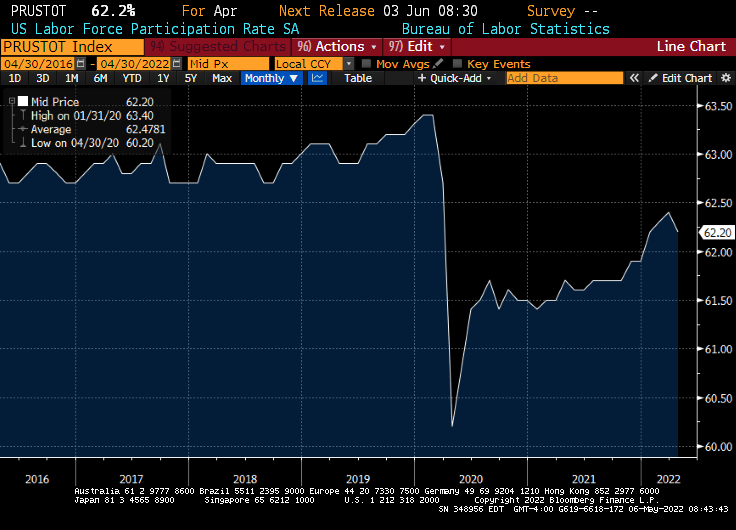

US labor force participation actually declined in April and struggles to get back to levels pre-Covid and Trump.

Here is the jobs market data for April 2022.

Leisure and hospitality sector still has a way to go after the ill-advised government shutdowns surrounding Covid.

Oddly, there are two job openings for every unemployed person.

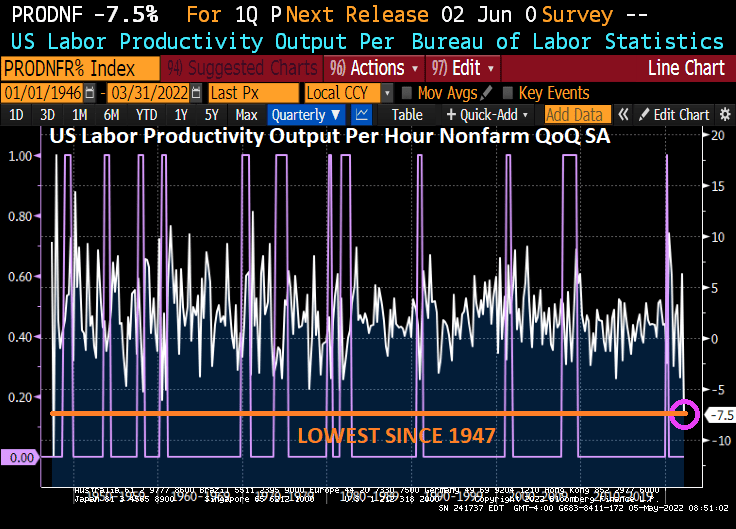

Here’s some simple Medusa math for you: negative growth + payroll gains = negative productivity. Negative productivity + high labor costs = very high unit labor costs. That’s not a pretty picture for the economy or for companies, and the Q1 figures were even worse than expected — productivity fell by 7.5%, pushing unit labor costs up by 11.6%. Nasty.

In fact, labor productivity fell to the lowest level since 1947 and President Harry Truman.

Of course, Biden’s green energy policies have led to crushing inflation.

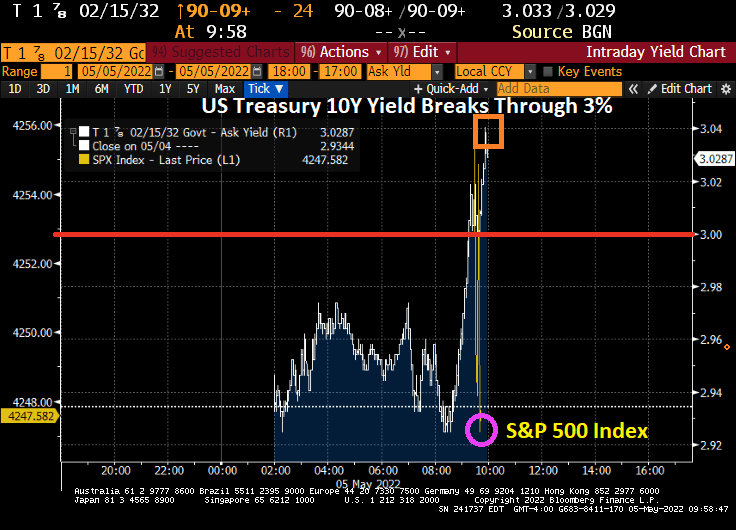

So, after Fed Chair Powell (aka, Jay The Revelator) said yesterday that “No Signs US Economy ‘Vulnerable’ To Recession”, we saw the S&P 500 index dive 1.5% and the 10-year Treasury yield break through the 3% barrier.

Biden’s policies are a Medusa-touch on the economy.

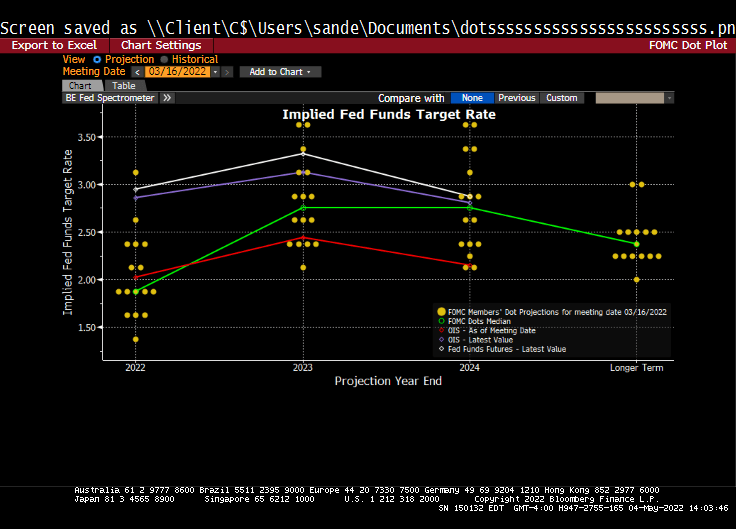

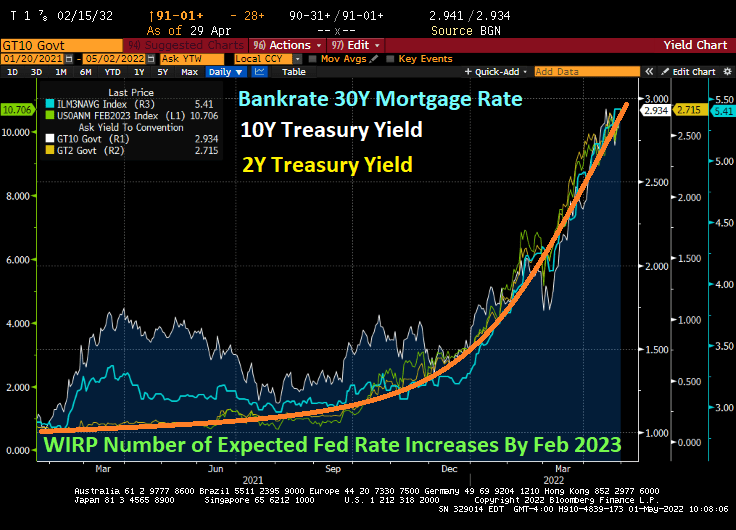

Well, the Fed’s talking heads have been saying a 50 basis point hike was coming in May … and it appeared!

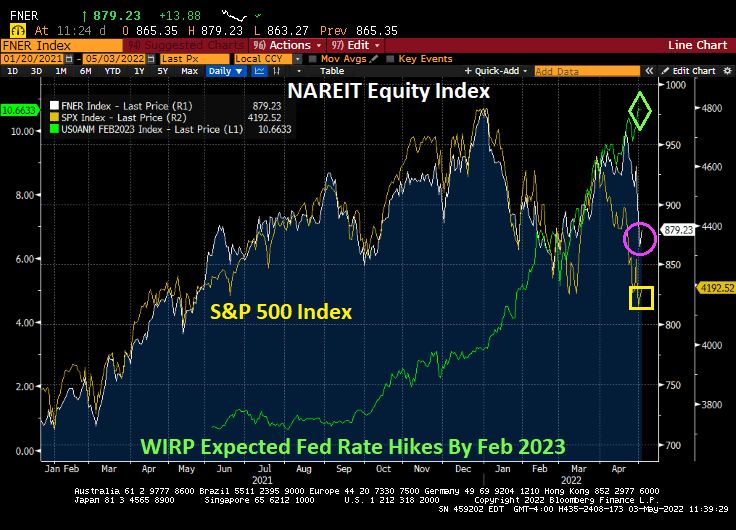

And it looks like 9 rate hikes are a comin’ by February 2023.

The Fed’s Dot Plots shows a cooling of Fed rate hikes by 2024 and beyond.

Here is the path of Balance Sheet peel-off.

The US Treasury actives curve is up by 14 bps at the 10-year tenor and up 17 bps at the 2-year tenor.

The plan will see $30 billion of Treasuries and $17.5 billion on mortgage-backed securities roll off. After three months, the cap for Treasuries will increase to $60 billion and $35 billion for mortgages.

I could read the Fed’s speech on their decision, but since The Fed has been so highly politicized, I don’t really care what they say. Only what they do.

As The Federal Reserve seems hellbent on raising interest rates to fight the rapid increases caused by Biden’s follicies, we see the S&P 500 index taking a hit in 2022, but NAREIT’s all equity index as well.

An example of how a REIT can be impacted by The Fed is the Industrial REIT index that tanked with Amazon’s declining earnings prospects.

While industrial REITs is a broad category, Amazon’s crashing EPS has certainly shocked the market.

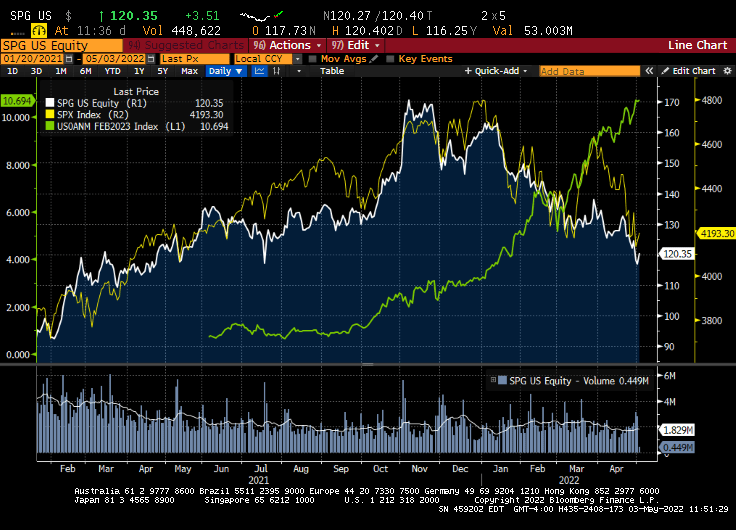

Retail REITs? How about Simon Properties? Simon Properties, a large mall REIT, go “Fauci’d” as the Covid economic shutdown really caused pain for shopping malls. Simon’s occupancy rate has increased as the economy opens back up (we hope).

Meanwhile, Simon Properties equity has declined along with the S&P 500 index as The Fed raises rates. In other words, both the S&P 500 and shopping mall REITs are getting “Fauci’d” by The Fed. Or Powell’d.

A measure of U.S. manufacturing activity unexpectedly dropped in April to the lowest level since 2020 as growth in orders, production and employment softened.

The Institute for Supply Management’s gauge of factory activity fell to 55.4 last month from 57.1, according to data released Monday. The Manufacturing Prices index remained elevated.

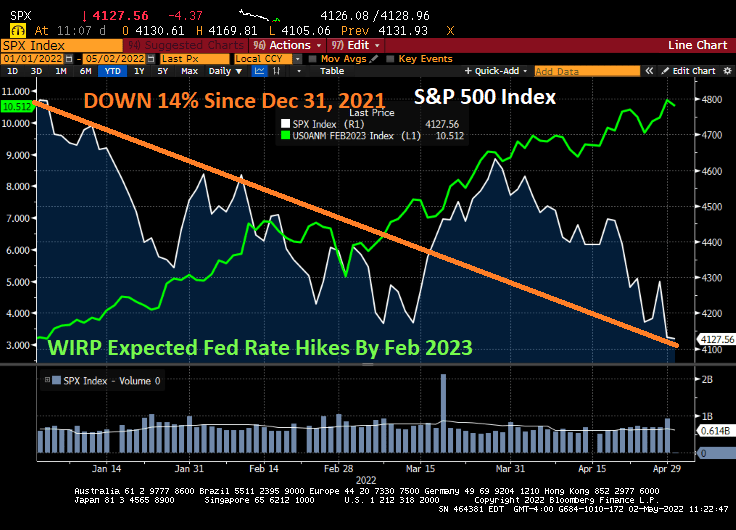

As the 10-year Treasury yield tries to breech the 3% barrier.

And as The Fed continues to threaten tightening of their monetary follicies, the S&P 500 index is down 14% since Dec 31, 2021.

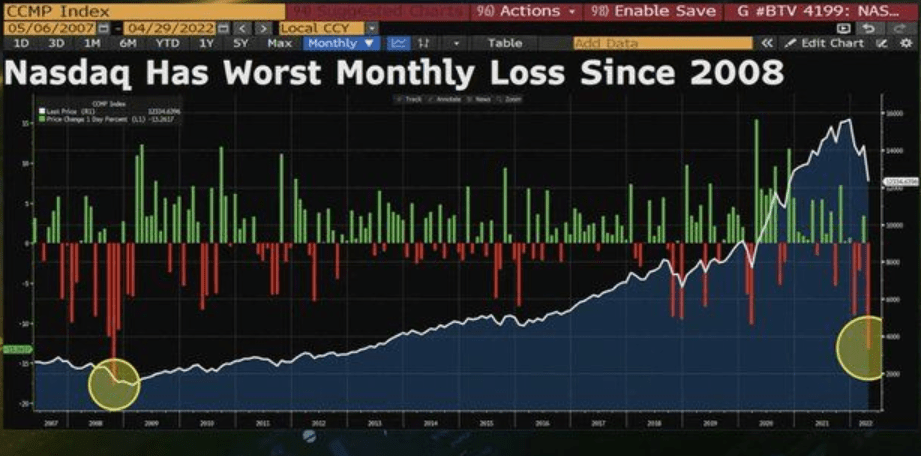

And the NASDAQ had it worst monthly loss since 2008.

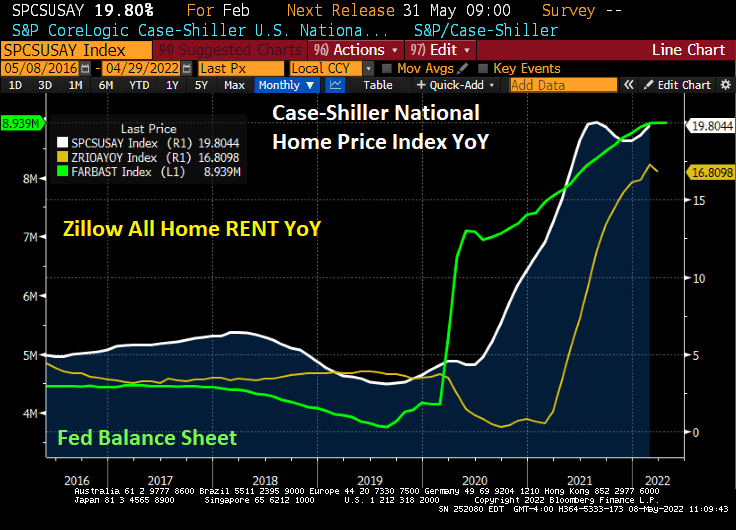

We now have the proverbial double whammy happening … soaring home prices AND soaring mortgage rates.

The theory is, of course, that The Federal Reserve will slowly remove its staggering monetary stimulus leftover from 1) the financial crisis of 2008 and 2) the Covid recession of 2020. As you can see, the sheer volume of monetary stimulus remains outstanding and it is the EXPECTATIONS of The Fed tightening that is caused the 30-year mortgage rate to rise.

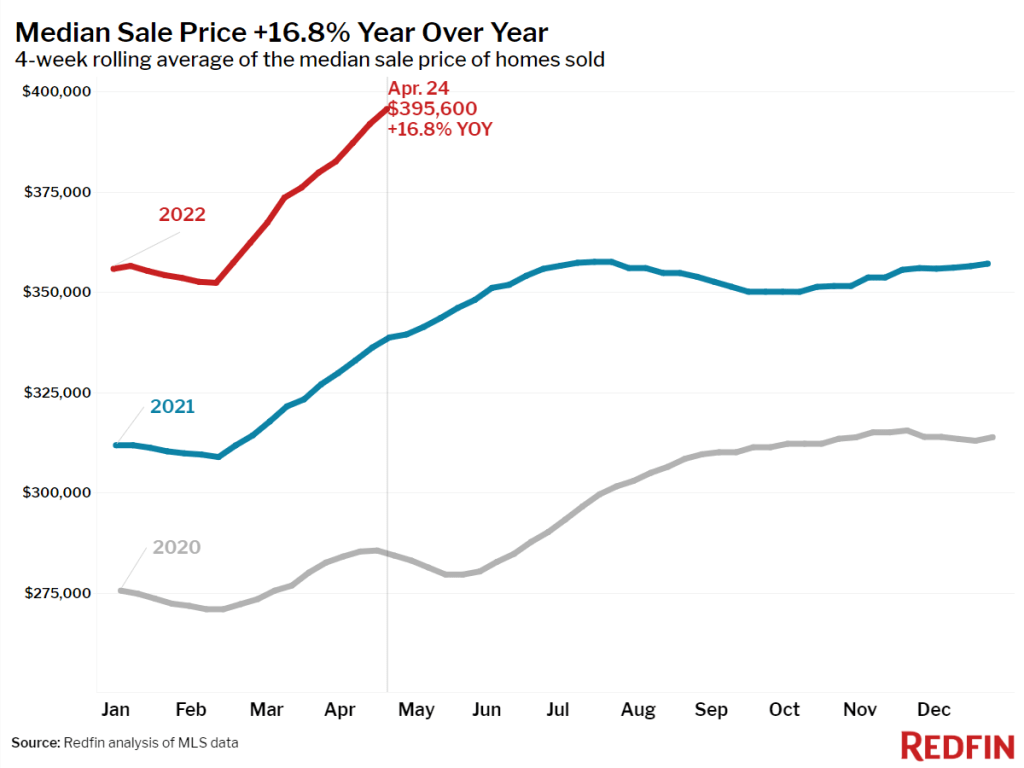

While I used the Case-Shiller National Home Price Index YoY, Redfin shows more contemporaneous home price data with April 24 median home sales price at 16.8%.

Thanks to The Fed, we are seeing homebuyer mortgage payments are up 39.4% YoY.

As inflation continues to damage America’s middle-class and low- wage workers, we may see regulations going into effect from the Consumer Financial Protection Bureau protecting consumers from … themselves.

President Biden (or whoever is pulling his strings) is inflicting a “Medusa Touch” on the US. That is, everything his administration touches turns to stone.

Let’s look at average hourly earnings. Thanks to “progressive” energy policies from Biden, REAL average hourly earnings growth has crashed and burned.

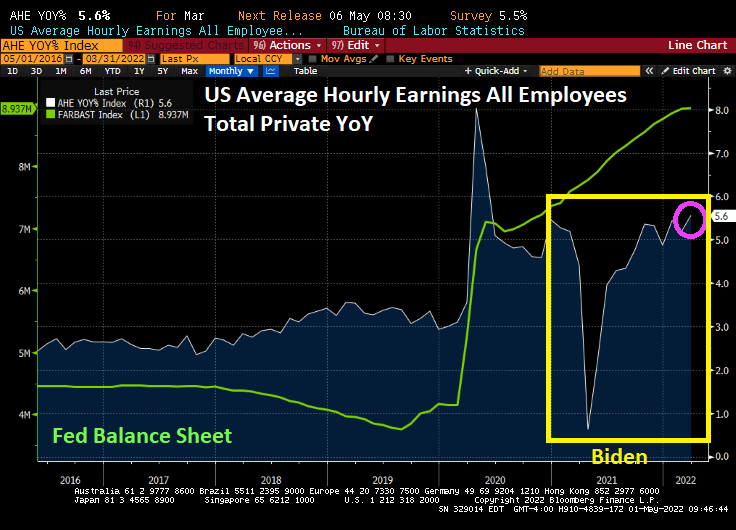

But here is the chart that the Biden Administration touts showing average hourly earnings growth at 5.6% YoY (although I doubt if Jen Psaki would leave out the massive distortion caused by The Federal Reserve’s “Let’s go crazy!” monetary policy.

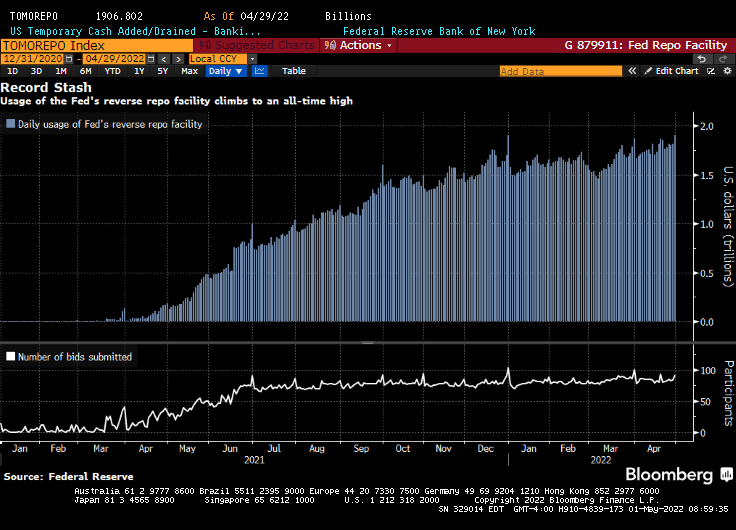

Another Medusa Touch moment is the reverse repo market. When I wrote about reverse repos before, several people wrote me saying “You don’t understand. This is a temporary problem and will vanish shortly.” However, The Fed’s reverse repo facility has now climbed to an all-time high.

Then we have the disruptive effects of The Federal Reserve deciding for us that mortgage rates are too low and should be higher.

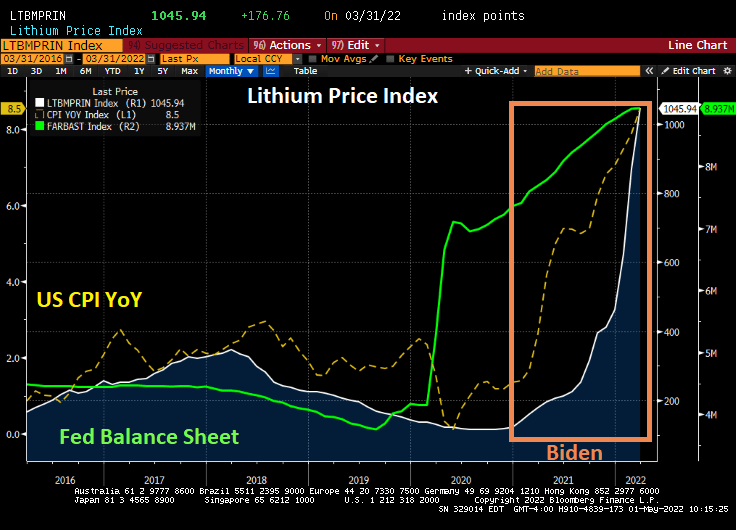

Now look at lithium prices, a key element for electric car batteries. Making the switch from Internal combustion engines to electric motors far more costly.

The list goes on and on.

Suffice it to say, everything the Biden Administration touches turns to stone.

But I wager that the Biden Administration wishes that Hunter Biden’s laptop would turn to stone.

Only an elitist DC bureaucrat like Joe Biden would laugh at inflation that is ruining the lives of millions of Americans.

You must be logged in to post a comment.