This is particulary dangerous since it was the worst correction in home prices since two rather nasty recessions of 1970 and 2008 (The Great Recession and financial crisis). This correction occured as M2 Money growth (green line) went negative.

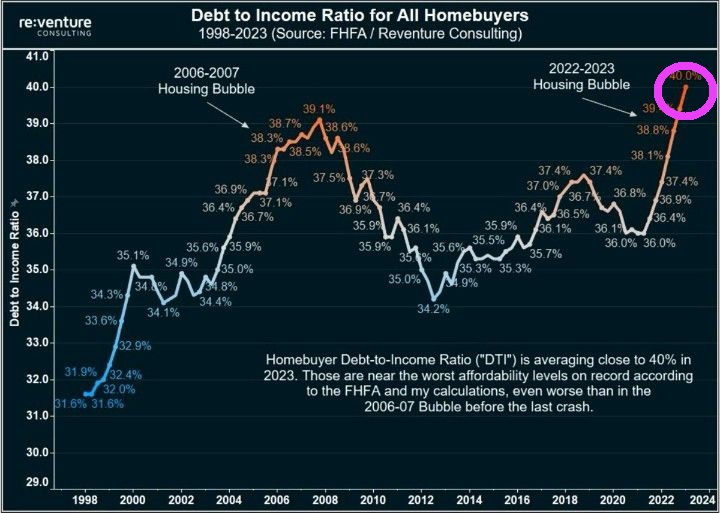

With Fed rate hikes, debt to income ratios are the highest in history.

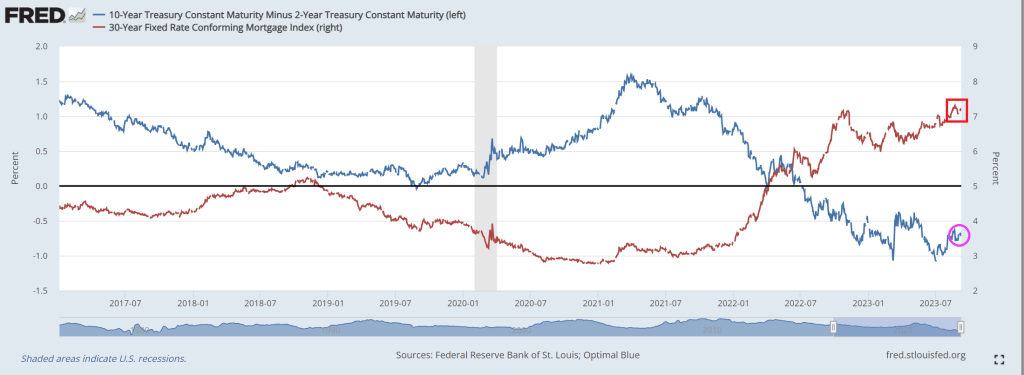

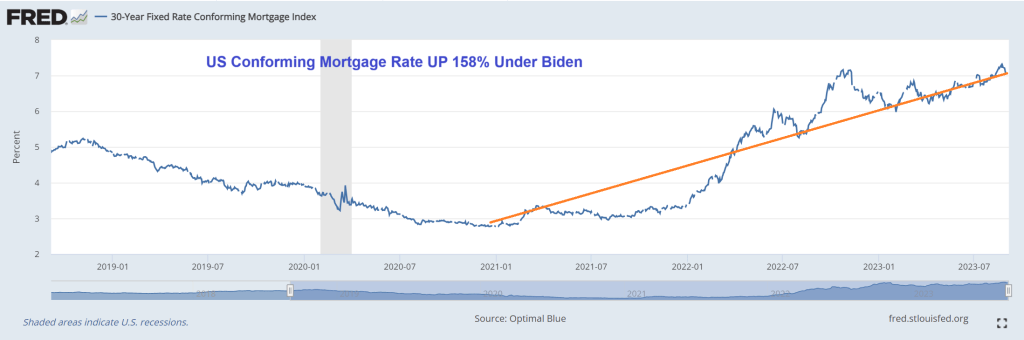

Mortgage rates are above 7% under Biden and Powell (not Baden-Powell, the founder of the Boy Scouts).

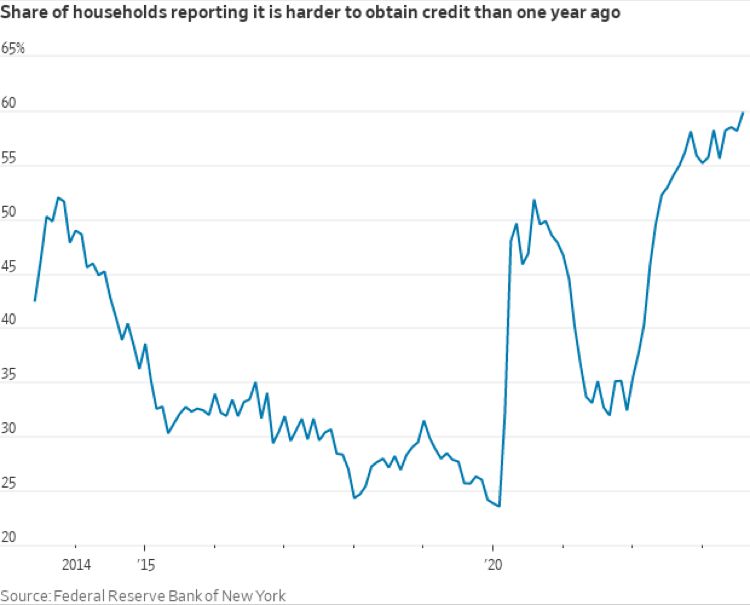

But not only are mortgage rates above 7%, but the mortgage credit box is tightening.

Actually, I have to Spain numerous times and love visiting Barcelona. But the US debt fiasco under Biden and Congressional spending sprees has led to … US credit default swap being priced worse than Spain’s CDS.

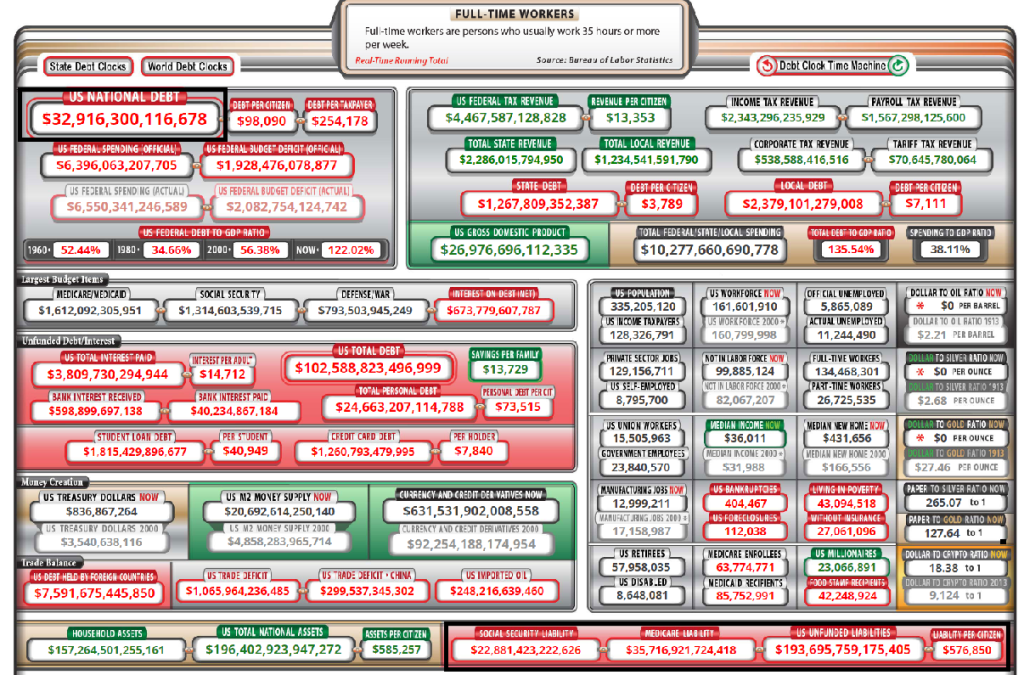

With Biden/Congress orgy of spending (and a declining economy in many important respects), the US is seeing Federal debt near $33 TRILLION and even worse, unfunded Federal liabilities (promises, promises) are at $193 TRILLION, almost 6 times the current Federal debt load.

If you are into archaelogy and fossils, Nancy Pelosi (83) has announced that she is running for re-election to The House. Hasn’t San Francisco suffered enough under Feinstein, Newsom and Mayor Breed?

But back in the USA (while Biden does his humiliate the US tour of Vietnam, India, etc, and ignores the tragedy of the 9/11 attacks), we see mortgage rates still up above 7% as the US Treasrury 10Y-2Y yield curve

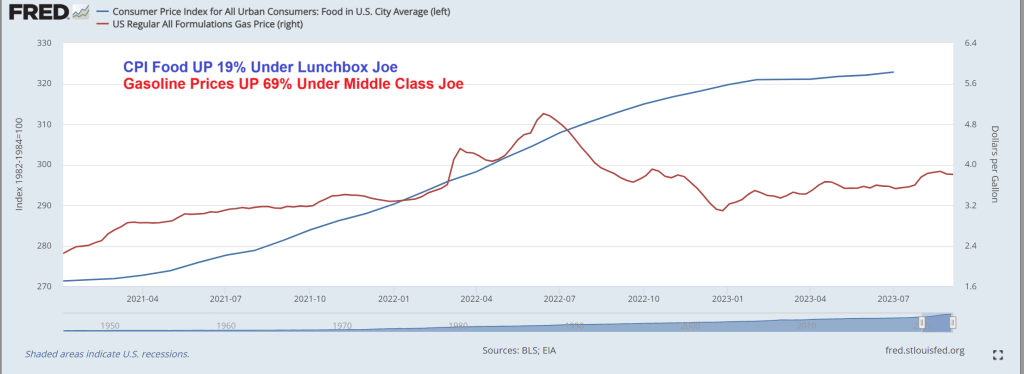

CPI food prices are up 19% under “Lunchbox Joe” and up 69% under “Green Joe”. True, the American middle class is far worse off under Bidenomics, but it is all about marketing Bidenomics at this point.

Of course, being a true RINO (Republican in name only), he won’t follow Biden around criticising him. Just critcising Trump. He is part of the Globalist Romney RINO Party (GRR).

Bidenomics is a train wreck. But unlike E. Palestine Ohio, the site of a train derailment and massive toxic spill (for which Biden has yet to visit), Bidenomics is a continuing train wreck.

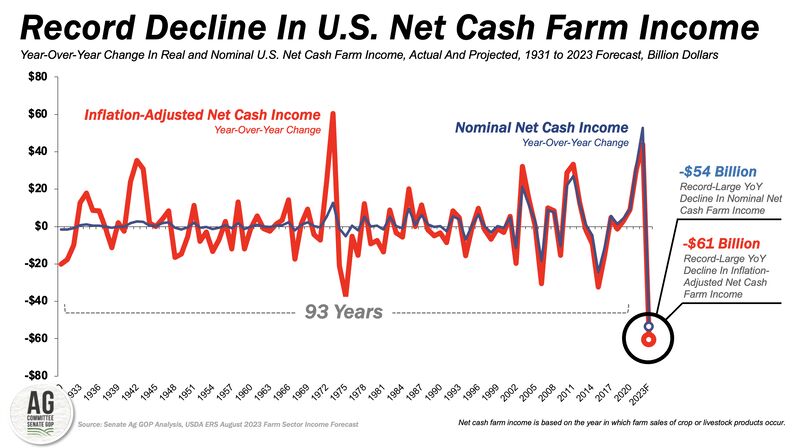

The first chart is the record decline in US net cash farm income. Now in negative growth!

Second, US office vacancy rate is now higher than the peak during the financial crisis. Of course, Covid shutdowns and work from home is the primary driver, but Democrat crime policies are making it more hazardous to work in offices in major American cities, so Bidenomics isn’t helping.

Is Biden acting on behalf of World Economic Forum’s Klaus Schwab? Well, Biden appointed John Kerry, another dimwitted former US Senator like Biden, to be his climate Czar. Kerry wants to shut down farms and starve the population, just like his Overlord Klaus Schwab.

Are Biden and America’s Progressives part of Schwab’s “Great Reset?” Where we eat insects while Biden, Kerry, Schwab and the elites feast on Wagyu beef, foie gras, and expensive champagne. Elitist Treasury Secretary Yellen looks like she could use some Ozempic!

And then we have elitist California governor Gavin “Count Yorga” Newsom opining on Biden’s great “success.” 70% of Americans say things are going badly under Biden, but California Democrat Gov. Gavin Newsom says he’s “very inspired by the master class of the last two-and-a-half years”

Ah, the elite class! Reminds me of the French aristocracy under Louis the 16th and Marie Antoinette. “Let them eat crickets!”

Bidenomics is terrible! Just a huge payoff to be big donors (the donor class) for green energy, Big Pharma and Big Defense. Now Biden is considering using ankle monitors to prevent illegal immigrants from leaving Texas and traveling to welfare-friendly blue states like California and New York rather than just enforcing the border. The middle class is truly wasting away with Bidenomics.

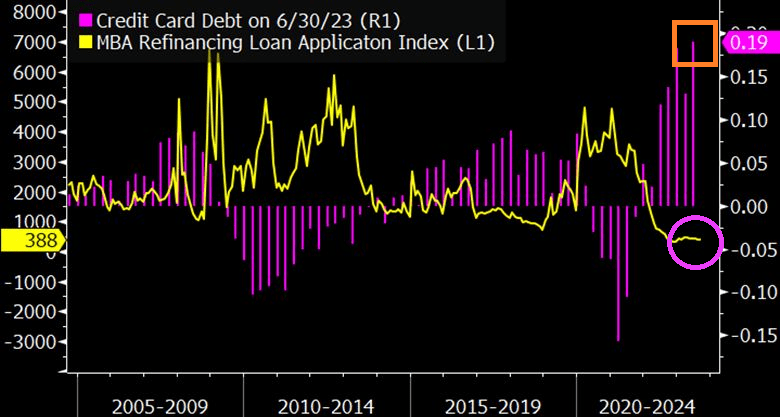

Let’s start with crashing mortgage refi demand as consumers load up on credit cards to afford rising prices thanks to Bidenomics.

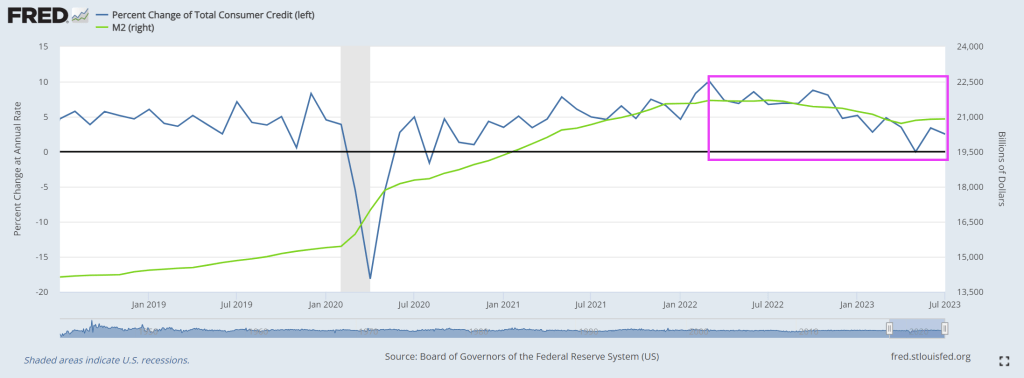

The Fed reports dramatically weakening consumer credit with negative revisions too.

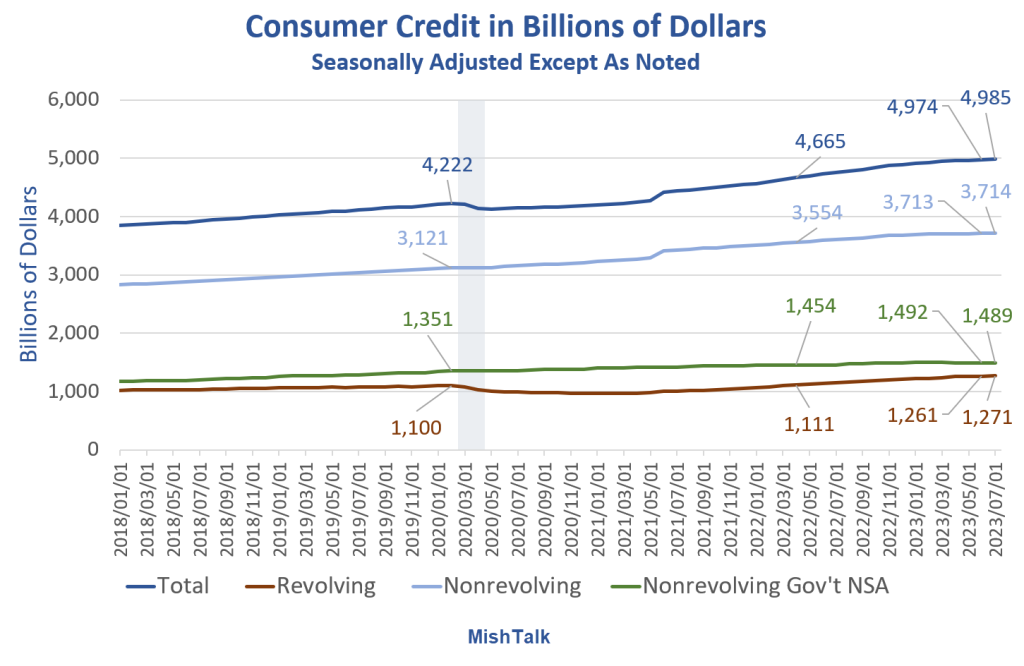

Consumer Credit data from the Fed, the last two months labeled are May and July, chart by Mish

Consumer Credit Report Revisions

Consumer Credit data from the Fed, chart by Mish

Revision Key Points

Most of the revisions are in nonrevolving, but that impacts the totals.

Nonrevolving credit rose $1 billion in July, from a negative $22 billion adjustment in June. The Fed revised a reported $3.735 trillion down to $3.713 trillion.

In turn, nonrevolving impacted the totals.

Total credit rose $11 billion in July, from a negative $23 billion adjustment in June. The Fed revised a reported $4.997 trillion in June down to $4.974 trillion.

Nonrevolving Consumer Credit in Billions of Dollars

Nonrevolving consumer credit data from the Fed, chart by Mish

Nonrevolving Credit Implications

Assuming the data is accurate (unlikely) or at least the revision direction is accurate (likely), mortgage and existing home sales data is suspect.

Real (inflation adjusted) nonrevolving credit peaked in June of 2021.

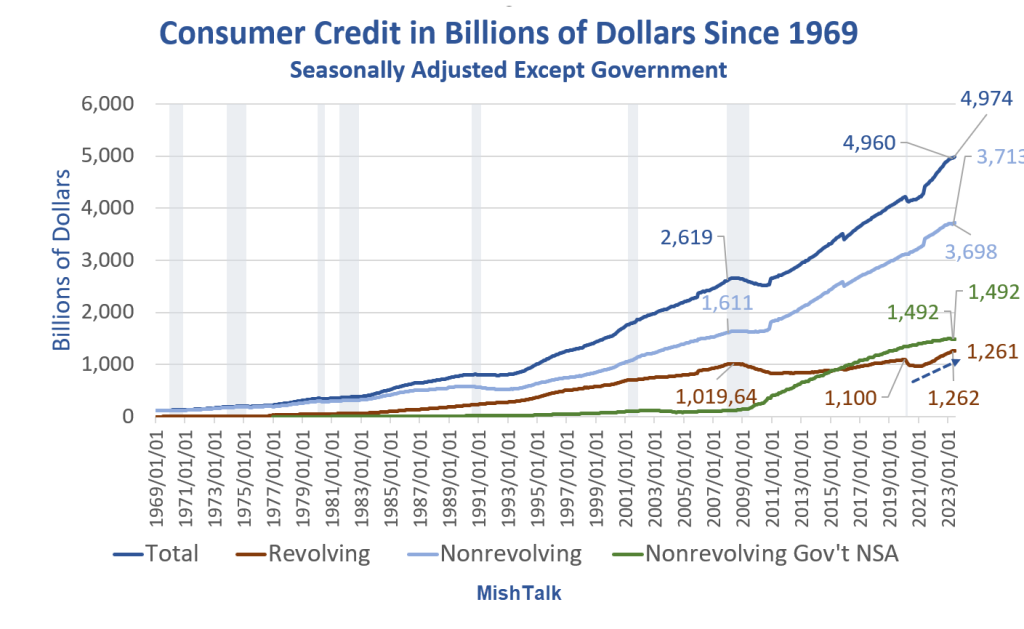

Consumer Credit in Billions of Dollars Since 1969

Consumer Credit data from the Fed, chart by Mish

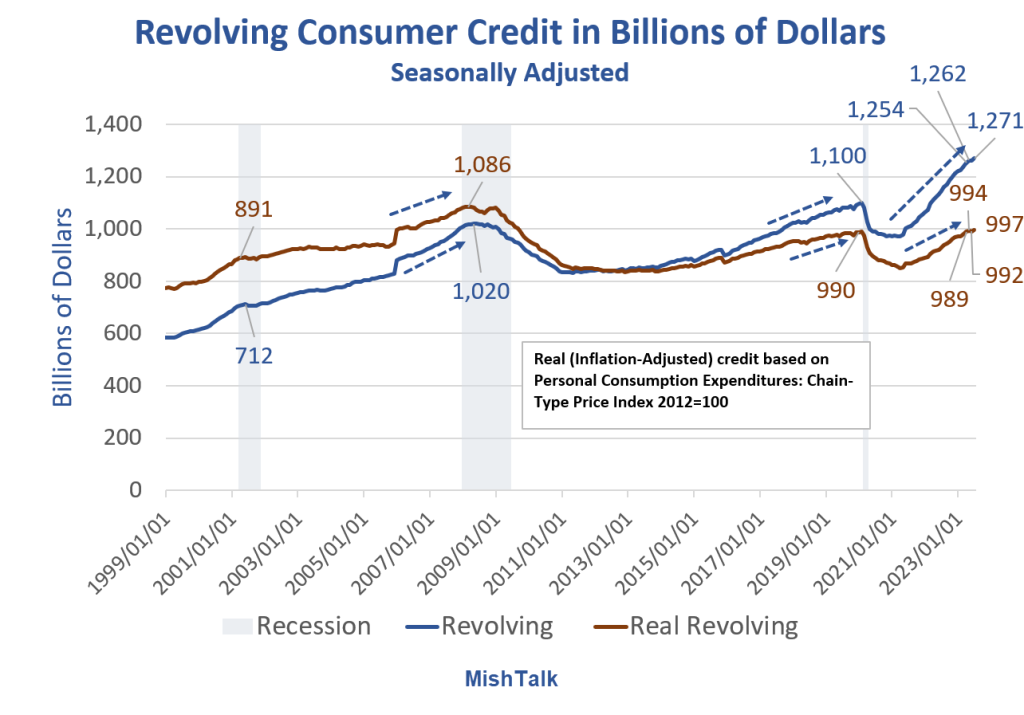

Consumers have generally done a pretty good job of avoiding credit card debt thanks to three rounds of fiscal stimulus.

However, inflation kicked in and the stimulus money has been spent. The result is the steep rise in credit card debt as noted by the blue arrow. Let’s hone in on that.

Revolving Consumer Credit in Billions of Dollars

Consumer Credit data from the Fed, Real (inflation adjusted calculation) and chart by Mish

Stunning Steepness in Credit Card Debt Accruals

The speed at which consumers are going into credit card debt is stunning.

It’s hard to maintain lifestyles with rising inflation unless wages keep up.

The BLS and Fed believe the rate of increase in inflation is falling. Assuming the data is correct, consumers are struggling anyway.

What Happens if Jobs Take a Dive?

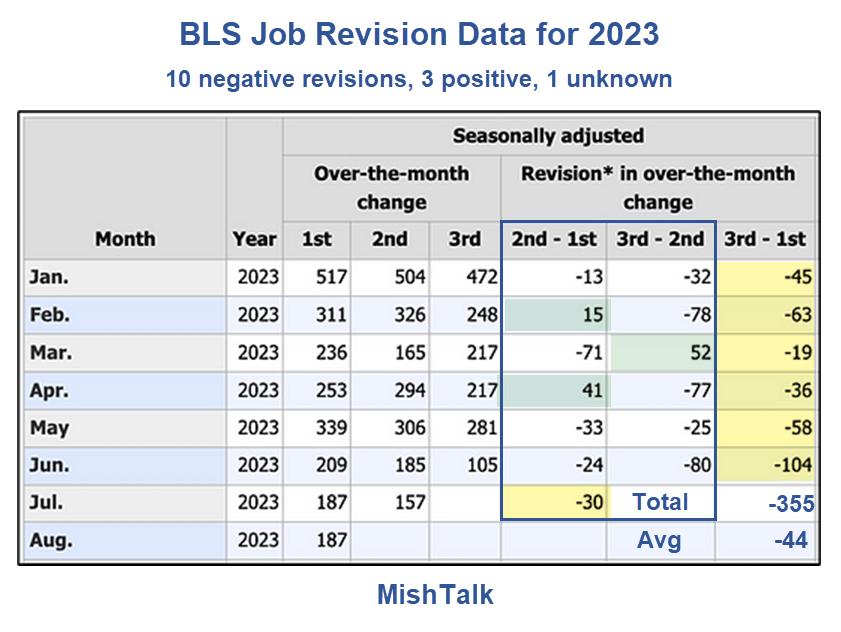

That’s actually the wrong question. Job revisions (there’s that word again) have been steeply negative.

BLS Job Revision Data from the Philadelphia Fed

Jobs are still positive, assuming (there’s that word again) you believe the numbers and more negative revisions (there’s that word again) are not in the works.

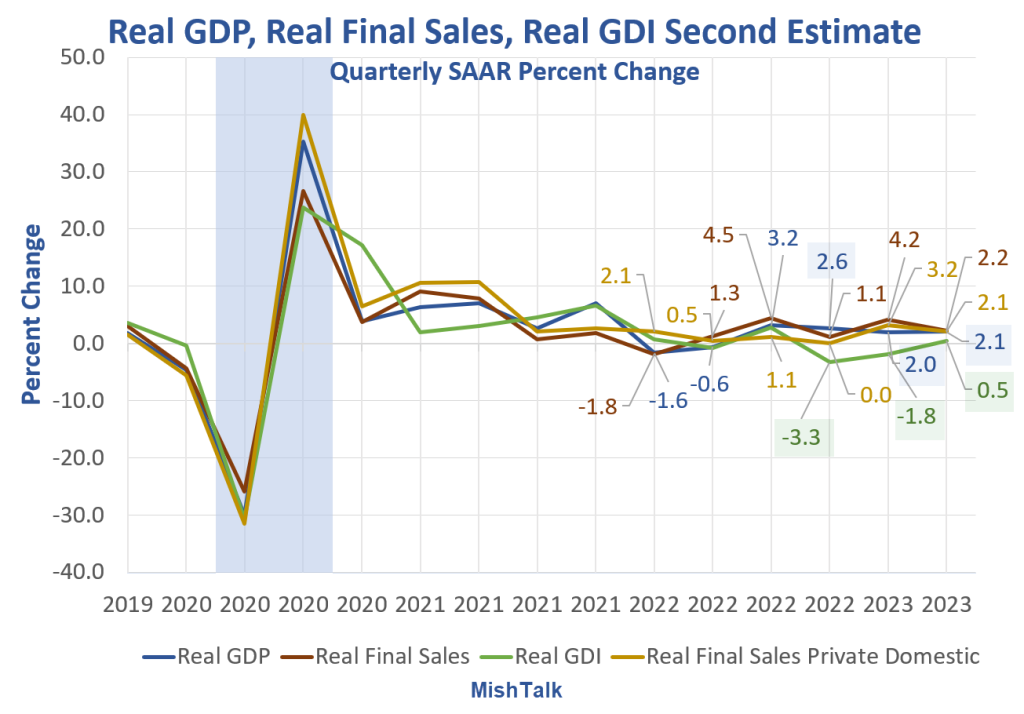

As long as you are making assumptions, if you are rah-rah on the strength of the Biden economy, you may as well assume GDP numbers are correct as well.

My assumption is GDP is flat out wrong and Gross Domestic Income (GDI) numbers are far more likely to be correct than GDP numbers. GDP and GDI are supposed to be the same but aren’t.

What a mess Biden and his Progressive backers have made. And we are forced to suffer the consequeinces of his policies. Or follies!

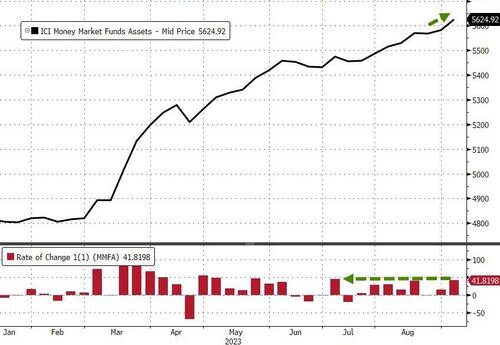

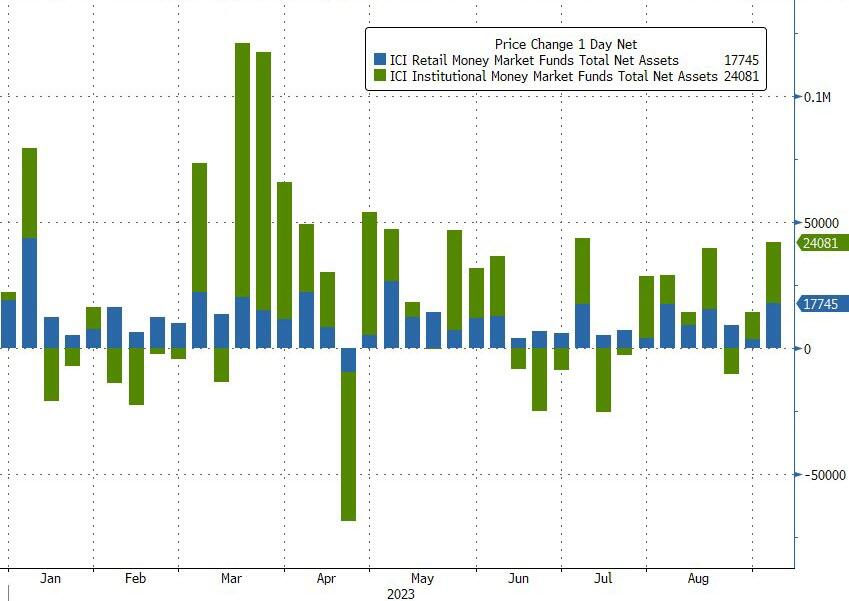

Money-market funds saw inflows for the 7th week of the last 8 with a $42BN jump (the most in 2 months) to a new record high of $5.625TN…

Source: Bloomberg

The inflow was dominated by a $24BN increase in Institutional fund assets while Retail also saw a sizable $17.7BN increase…

Source: Bloomberg

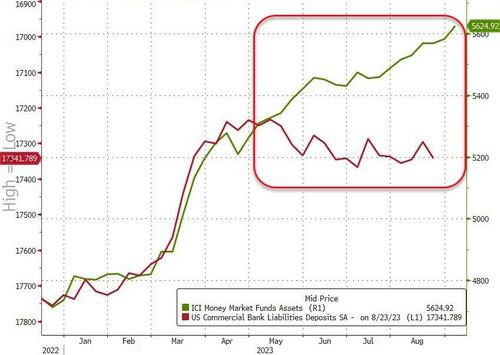

And the divergence between money-market fund assets and bank deposits continues to grow…

Source: Bloomberg

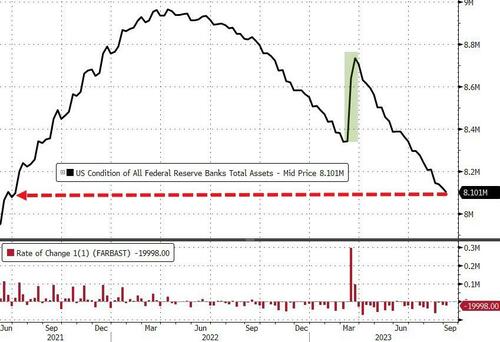

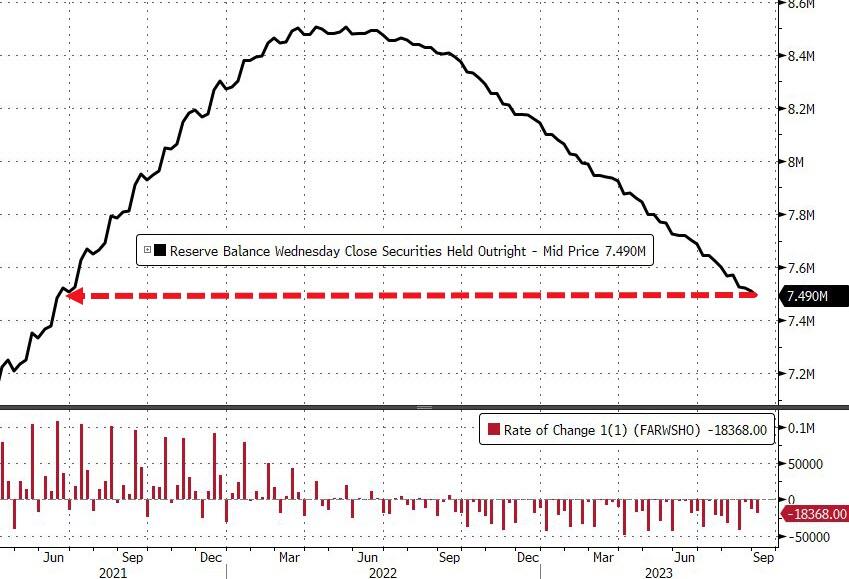

And while we actually saw huge deposit outflows (on a non-seasonally-adjusted basis) – despite The Fed’s seasonally-adjusted deposits increase – The Fed balance sheet shrank by another $20BN last week to its smallest since June 2021…

Source: Bloomberg

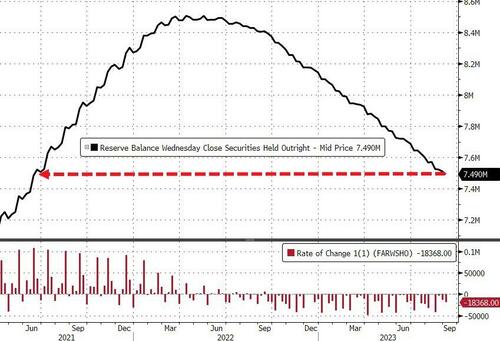

The Fed’s QT program continues apace with$18.4BN sold last week to its smallest since June 2021…

Source: Bloomberg

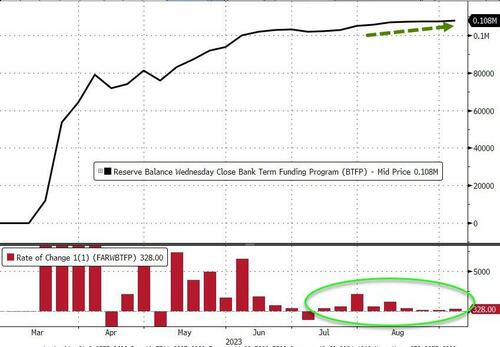

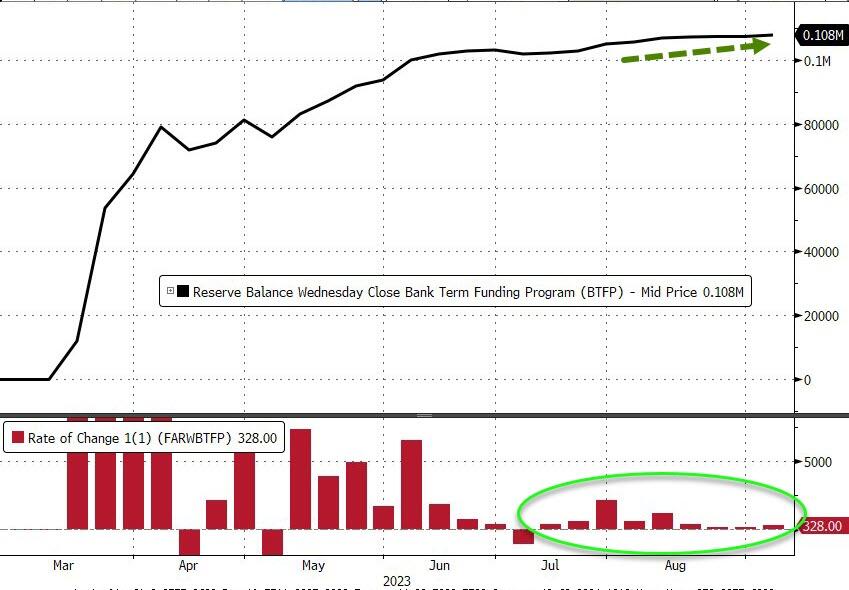

Usage of The Fed’s emergency bank funding facility jumped by $328 Million last week to a new high of $108BN…

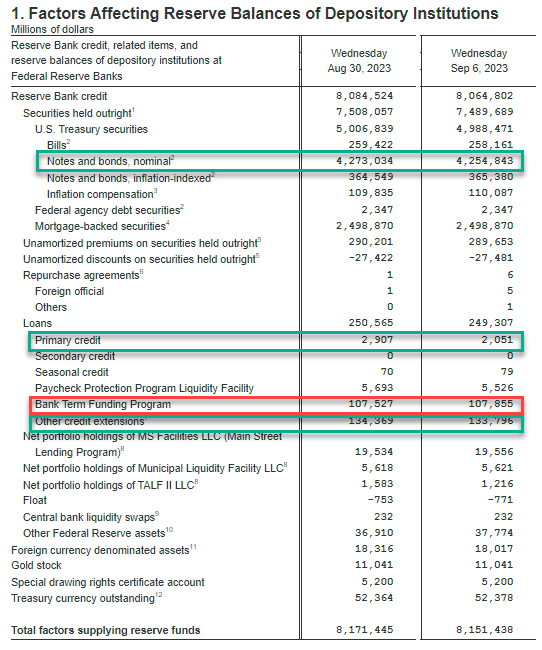

Source: Bloomberg

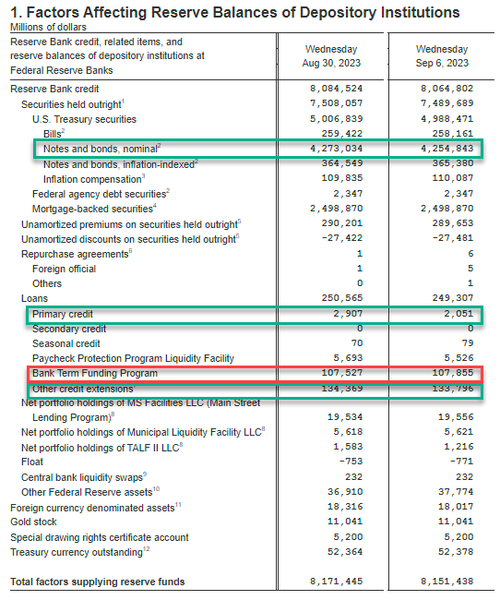

Fed BS weekly change:

Fed balance sheet QT (Notes and bonds decline): $4.255 trillion, down $18,2BN

Discount Window $2.1BN, down $800M from $.29BN

BTFP new record $107.9BN, up $400MM

Other Credit Extensions (FDIC Loans): $133.8BN, down $0.6BN from $134.4BN

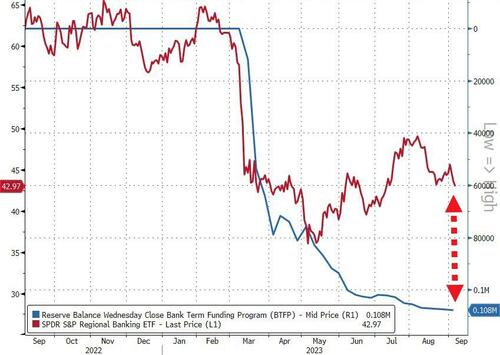

Finally, US equity markets and bank reserves at The Fed have converged a little recently, but the gap remains wide (thanks to the plunge in reverse repo balances)…

Source: Bloomberg

Tick, tock, banks!

Source: Bloomberg

You have six months to figure out how to clean up the $108 Billion hole in your balance sheet that you’re currently paying The Fed’s exorbitant rates to fill.

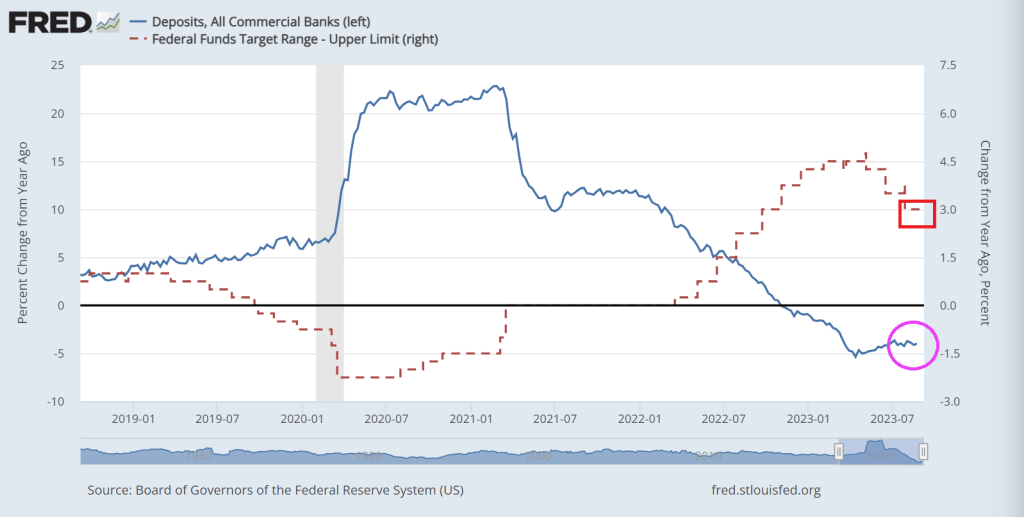

Bank deposit growth remains negative as The Fed tightens its overly accomodative monetary policy.

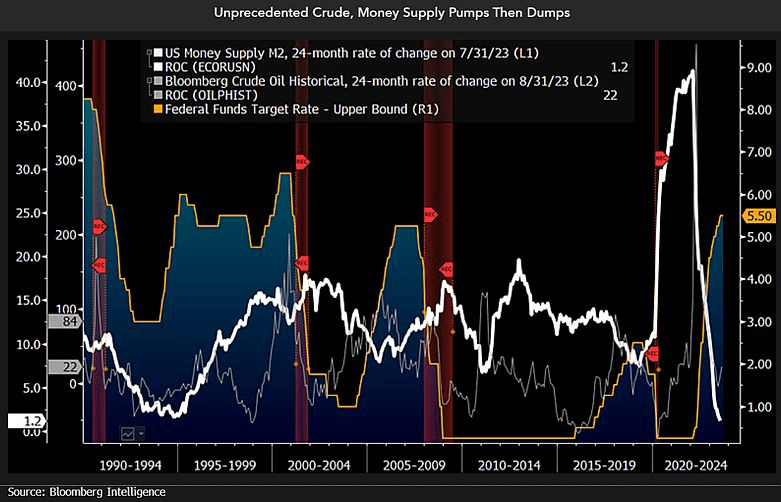

And then we have this chart showing plinging M2 Money (white line fever).

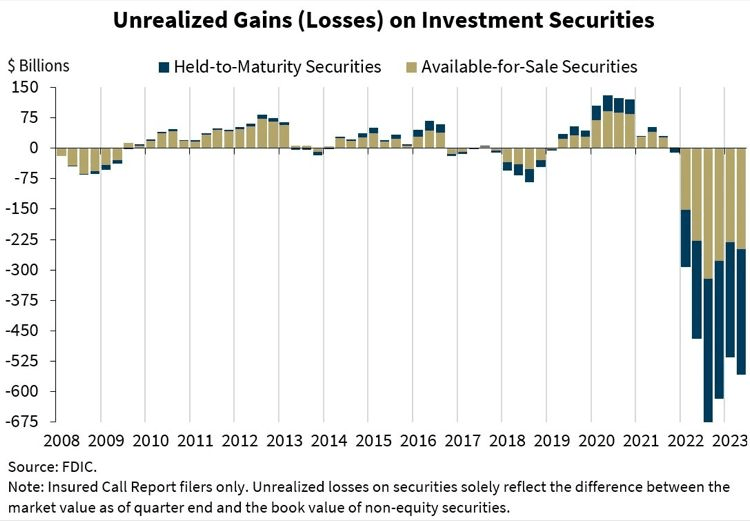

And the horrific unrealized losses on bank’s books.

Bidenomics is failing America. Primarily because Biden was one of the stupidest members of the US Senate. Not to mention nasty. Great President, America! /sarc

As Bidenomics fails to do anything other than make big donors wealthier (green energy companies, big tech and union bosses, etc), we are seeing the impacts of Fed monetary tightening to combat inflation caused by Biden/Pelosi/Schumer’s spending spree.

First, the 10-year REAL Treasury yield is close to breaching 2%.

Second, 30-year mortgage rates are now 7.62%, up over 150% under Bidenomics.

Third, mortgage purchase applications crashed to the lowest level since 1995.

Fourth, the 2-year Treasury yield just breached 5%.

Fifth, the 10Y-2Y yield curve remains deeply inverted.

Speaking of Bidenomics, US mortgage purchase demand just declined to the lowest level in 28 years.

Mortgage applications decreased 2.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 1, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The Refinance Index decreased 5 percent from the previous week and was 30 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 28 percent lower than the same week one year ago.

This is not good.

Bank deposits, a source of bank lending, are down -4% YoY as The Fed tightens rates.

Here is Lefty Frizzell’s original version of the Bidenomic’s themesong “If you’ve got the money, honey,I’ve got the time.” Like big donors receiving green energy subsidies. But not middle class mortgage borrowers.

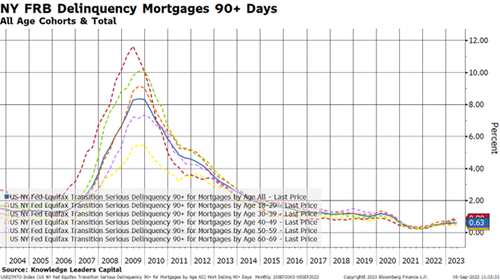

Thanks to Bidenomics, code for massive Federal spending on green energy initiatives and payoffs fo large donors, we have agonizing inflation and consumers are borrowing more and more to cope with inflation. And with the increased use of debt comes …. drumroll … delinquenices!

The US conforming mortgage rate is UP 158% under Bidenomics.

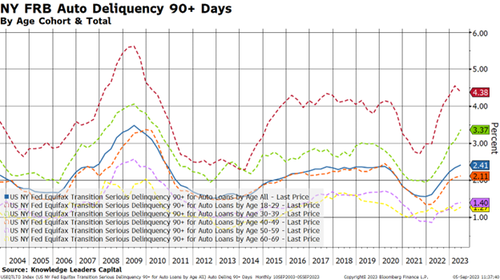

Let’s move on to some forms of consumer loans, where the story is a little more daunting.

Auto loans are definitely the epicenter of the credit cycle. While the overall average is a still somewhat tame 2.41%, younger borrowers are not keeping up. Younger borrowers have delinquency rates that are 1-2% higher than the average while the inverse is true for older borrowers. Eighteen-to-thirty-nine year-old borrowers have the highest delinquency rate in 13 years.

Somehow, I sense that used car lots are going to start filling up again as these vehicles get repossessed. This should put downward pressure on used car prices, bringing that element of inflation down. This is one of the channels through which monetary policy works.

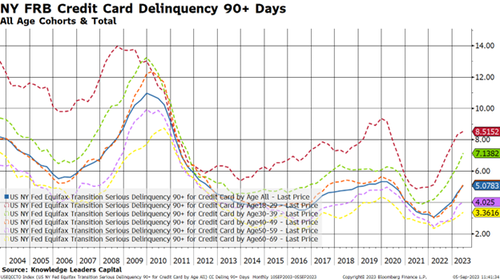

Lastly, I’ll take a look at credit card delinquencies.

Here is where we can really see the stresses building.

First, the overall delinquency rate has about doubled from 2.5% to 5% over the last couple years.

Second, older borrowers have seen a tick up in delinquency rates, a feature we don’t really see in other credit products.

Third, one in 12 younger 18-29 year-old borrowers are 90+ days late making their credit card payments.

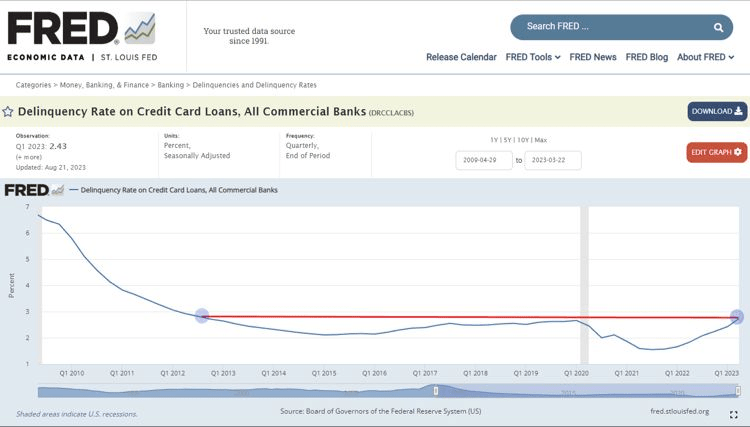

Credit Card Delinquency Rate across all commercial banks hit 2.77% in the 2nd quarter, the highest level in more than a decade.

In conclusion, we are in the early days of a consumer credit cycle. Younger borrowers are the weakest link in this analysis, and this makes me wonder where rates go when student debt payments turn back on at the end of the month.

The cost of living has been soaring, and our standard of living has been steadily going down.

Coping with inflation is tough for American households where consumer debt is up 19.$ under Biden while the free-spending Federal government’s public debt is up only 16.5%.

“In July 2023, 61% of U.S. consumers live paycheck to paycheck, unchanged from June 2023, but 2 percentage points higher than July 2022. Generally, more consumers of all income brackets reported living paycheck to paycheck in July 2023 than last year,” Alia Dudum, a money expert at LendingClub told FOX Business.

Now, 78% of consumers earning less than $50,000 a year and 65% of those earning between $50,000 and $100,000 were living paycheck to paycheck in July, both up from a year ago, LendingClub found. Of those earning $100,000 or more, only 44% reported living paycheck to paycheck.

Because consumers have so little disposable income these days, retailers all over the nation are experiencing difficulty.

In fact, UBS is projecting that 50,000 stores could close in the United States by the end of 2027…

Analysts at investment bank UBS are forecasting that some 50,000 U.S. stores are likely to close by the end of 2027, because of expected cutbacks in consumer spending, tighter credit and the continued shift to ecommerce.

Store closings could accelerate to 70,000 to 90,000 if retail sales turn out to be weaker than expected, according to UBS.

Actually, I think that losing 50,000 stores is a wildly optimistic scenario.

Hopefully I am wrong about that.

The housing market has also been going haywire.

According to Fortune, the month of August “will become the worst month for housing affordability this century”…

On Monday, the average 30-year fixed mortgage rate reached 7.48%, marking the highest level since the year 2000. Even prior to this recent surge in mortgage rates, housing affordability, as monitored by the Atlanta Fed, had already deteriorated beyond the levels seen at the housing bubble’s peak in 2006. Once this latest mortgage rate surge is factored in, August 2023 will become the worst month for housing affordability this century.

Wow.

Thanks Delaware Joe Biden (as opposed to Country Joe Stalin).

Home prices are going to have to come down, and in some areas they have already fallen quite a bit…

Homeowners are sitting on a negative equity timebomb after losing $108.4 billion on their property values this year, experts say.

The average borrower saw their home equity plummet by $5,400 in the first quarter of 2023 compared to last year – with households in Washington, California and Utah worst affected.

Do you remember the housing crash of 2008 and 2009?

Well, now the next housing crash is here, and it isn’t going to be fun.

For a while there, Joe Biden and his minions could at least boast about the employment market.

But now large companies all over America are laying off workers, and it is being reported that a staggering 1.223 million native-born Americans lost their jobs during the months of July and August…

Staggering figures have revealed that over 1.2 million US-born workers lost their jobs last month while the foreign-born workforce increased by nearly 700,000 – as migrants continue to flood across the border under the Biden administration.

Data from US Bureau of Labor Statistics show that between July and August, there was a staggering decrease of 1.223 million native-born people in the workforce – which is a low not beaten since the jobs crash when Covid hit in April 2020.

The numbers that I have shared with you are nothing to brag about.

But Joe Biden is going to keep trying to pull the wool over the eyes of the American people anyway.

Unfortunately for Biden, it has become quite clear that most Americans have lost faith in him. According to the same Wall Street Journal poll that I mentioned above, 73 percent of U.S. voters now believe that Biden “is too old to run for president”…

For Biden, one of his biggest challenges is age. The Wall Street Journal poll found that about 73% of voters think Biden is too old to run for president while only 47% think Trump is too old. Thirty-six percent of voters think that Biden is mentally up for the job while 46% of voters think Trump is mentally capable of being president.

We have never seen numbers like this for any other president.

Sadly, Biden fully intends to run again. (Especially since half-wit Jill Biden is allegedly running The White House).

And the Democrats will get behind him, because at this point no other candidate is posing a serious threat to Biden. Wait, not Gavin Newsom who almost single handedly destroyed California or Michelle Obama who has absolutely no qualifiications?? Other than being Barry Soetoro’s wife?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.