Argetina’s inflation rate just hit 102.5% as their M2 Money printing hit 80%

Argentina’s central bank is considering raising its benchmark rate on Thursday for the first time since September after inflation data showed prices increased by more than 100% annually last month, according to two people with direct knowledge.

The monetary authority’s board will consider an increase after leaving the key Leliq rate unchanged at 75% for several months, the people said, asking not to be named discussing internal decisions. The board has not yet decided on the size of the hike in case they opt for such move, they said.

A cautionary tale for Washington DC spendacrats and Fed officials.

Brought to the same country that gave us Statist Juan Peron and his wife Eva.

Apparently, the NEO financial crisis (not the subprime, but The Fed’s “too low for too long” crisis) is still with us.

Credit Suisse Group AG’s top shareholder, whose stake has lost more than one-third of its value in three months, ruled out investing any more in the troubled Swiss bank as a bigger holding would bring additional regulatory hurdles.

“The answer is absolutely not, for many reasons outside the simplest reason, which is regulatory and statutory,” Saudi National Bank Chairman Ammar Al Khudairy said in an interview with Bloomberg TV on Wednesday. That was in response to a question on whether the bank was open to further injections if there was another call for additional liquidity.

Credit Suisse says it has identified material weaknesses in its internal control over financial reporting as of December 31, 2022 and 2021, according to the annual report.

The material weaknesses relate to the failure to design and maintain an effective risk assessment to identify and analyze the risk of material misstatements in its financial statements and the failure to design and maintain effective monitoring activities relating to: – Providing sufficient management oversight over the internal control evaluation process to support the Group’s internal control objectives – Involving appropriate and sufficient management resources to support the risk assessment and monitoring objectives Assessing and communicating the severity of deficiencies in a timely manner to those parties responsible for taking corrective action

And it could simply be that Credit Suisse was caught in the Central Bank “Bear Trap” where banks get clobbered as interest rates rise.

Credit Suisse’s CDS (credit default swap) is soaring!

And on the “it ain’t over till its over” news from Credit Suisse, the US Treasury 2-year yield plunged -40.4 basis points.

And the US Treasury 10-year yield plunged -24.8 basis points.

The official logo of the Federal Reserve should be Munch’s The Scream.

Well, the banking fiasco CREATED BY THE FEDERAL RESERVE is still with us. Why? Because the FDIC guaranteed deposits above $250,000 for the first time in history, bailing out millionaires/billionaires. I call this Crony Socialism (but I repeat myself).

Congress doesn’t understand banking, only how to spend money.

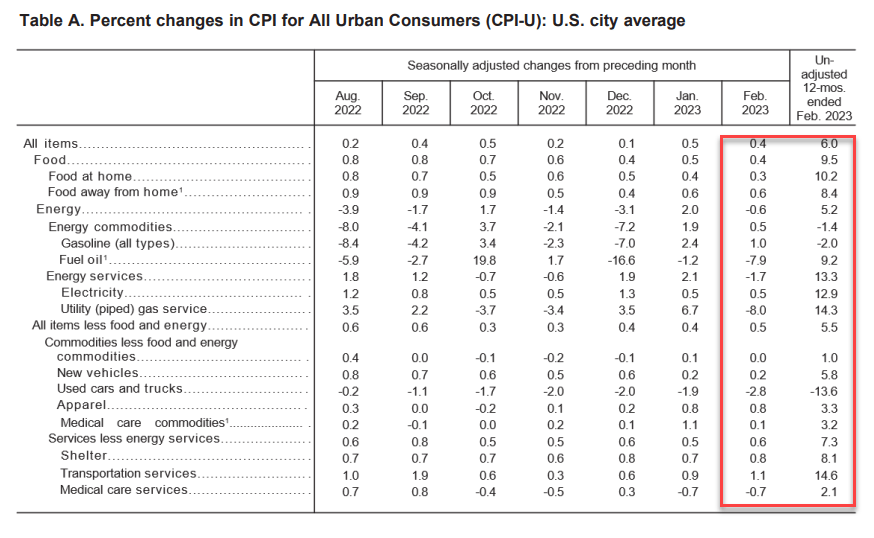

While headline inflation (CPI) came in a 6% (considerably higher than The Fed’s 2% target), core inflation came in at 5.5% year-over-year (YoY), which was expected.

The truly nasty number is today’s inflation report is that weekly earnings YoY remained the same at a terrible -1.9%. Meaning that inflation is higher than nominal wage growth. This is the 23rd straight month of negative real weekly earnings. Well done, Fed and Biden!

Food is up 10.2% YoY. Electricity up 12.9%, shelter up 8.1%.

On the news, the US Treasury 2-year yield rose 34.3 basis points.

Somehow I doubt that Biden’s press secretary will tout 23 straight months of negative weekly earnings growth as one of Biden’s economic accomplishments.

All together now. The Fed has been printing too much money for too long and Biden restricts fossil fuel production. Ad in rampant Federal spending and we have INFLATION. Inflation led to The Fed to raise rates. And with rate increases and down go the banks.

Of course, The Fed and Biden Administration will overeact (e.g. offering deposit insurance on ALL deposits above $250,000 creating moral hazard risk). As such, we are seeing gold prices soar by 2% this AM.

In adddition to gold rising 2%, natural gas futures are up 6%

The Silicon Valley Bank failure (along with NY’s Signature Bank) are sending shock waves through the global economy. Not because of the incompetence of bank regulators, but because of the reaction function from the FDIC and Fed.

The 10-year Treasury yield is down -26 basis points in the AM. And the Fed Funds Target Rate is expected to drop to 4.7%.

Its not just the US Treasury yield that declined -26 basis points. European sovereign yields are down too (Germany 10-year is down -32.9 basis points).

Look at the 2-year Treasury yield. Its down -54.6 basis points.

On a sad note, Resident Biden is calling for stricter regulations for the banking industry, already one of the most regulated sectors of the economy. How about less politics and just make them do their ^*T^R jobs!

Its just like The Fed. The Taylor Rule says that The Fed’s target rate should be 10.29%, but now the terminal rate has been lowered to 5.475%, almost half of where the target rate should be.

Today’s jobs report for February was a huge disappointment IFF you expected another blowout jobs report like the one from January (504k jobs added). February saw just 311k jobs added, a decline of -38.3% MoM.

And just like that, The Fed’s terminal rate fell to 5.475%, a far cry from the 10.29% rate according to the Taylor Rule.

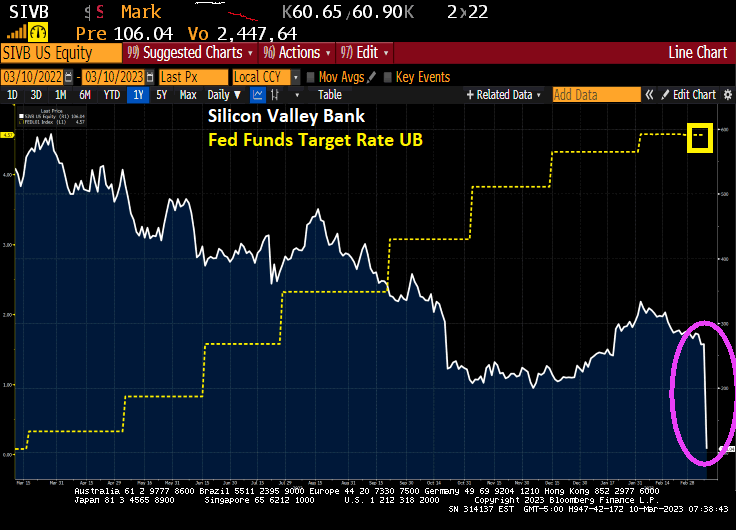

Let’s see if The Fed holds course with Silicon Valley Bank collapsing in biggest failure since 2008.

Silicon Valley Bank became the biggest US lender to fail in more than a decade after a tumultuous week that saw an unsuccessful attempt to raise capital and a cash exodus from the tech startups that had fueled the lender’s rise.

Regulators stepped in and seized it Friday in a stunning downfall for a lender that had quadrupled in size over the past five years and was valued at more than $40 billion as recently as last year.

The move by California state regulators to take possession of the lender, known as SVB, and appoint the Federal Deposit Insurance Corp. receiver underscores the impact that the US’s rapid interest-rate increase is having on smaller lenders. SVB is the second regional lender to fold this week after Silvergate Capital Corp. announced it was voluntarily liquidating its bank, spurring a broader selloff in bank stocks.

The FDIC has set up a bridge bank to handle the failure of SVB. VERY rare. The last bridge bank was for IndyMac Bank from LA.

SVP is the second biggest bank failure in US history after Washington Mutual (WAMU).

Now here we are again with yet another bank contagion. First it was Silicon Valley Bank, now it is First Republic Bank (down -28% at opening).

And there is a trading halt on First Republic. But YoY growth on FRC’s earnings of -34.7% is horrendous.

At least cryptobank Silvergate isn’t down as much as Silicon Valley Bank and First Republic Bank.

And the SPDR Regional Bank index is getting clobbered as Fed withdraws stimulus.

SVB’s management’s solution appears to have been to seek out yield through a lot of long-duration bonds. The bank started to lose deposits as VCs pulled cash/burnt through operating capital.

SVB’s CEO Greg Becker saw this coming and dumped his holdings.

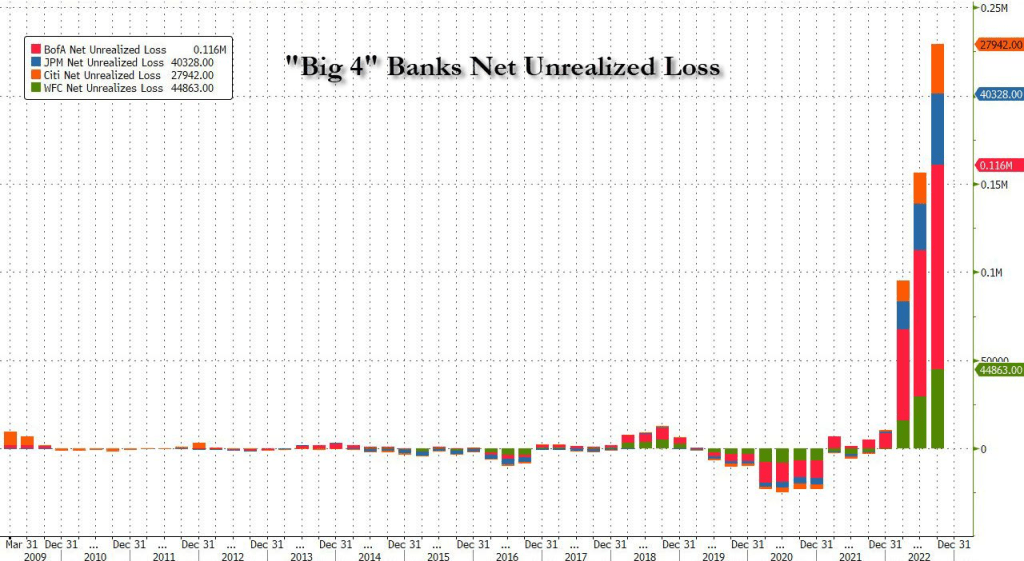

While waiting on the February jobs report from the US Bureau of Labor Statistics (BLS), I noticed that the big 4 banks (Bank of America, JPMorgan Chase, Citi and Wells Fargo) are drowning in net realized losses as The Federal Reserve combats 1) too many years of loose monetary policy under former Fed Chair Janet Yellen and 2) too much spending under Pelosi, Schumer and … McConnell.

At a micro level, we have Silicon Valley Bank (SVB) SVB Is racing to prevent a bank run as funds advise pulling cash.

Panic is spreading across the financial world as concerns about the financial stability of Silicon Valley Bank prompt prominent venture capitalists including Peter Thiel’s Founders Fund to advise startups to withdraw their money.

The turmoil followed a surprise announcement from Santa Clara, California-based SVB that it was issuing $2.25 billion of shares to bolster its capital position after a significant loss on its investment portfolio. The stock plunged 44% in premarket trading before exchanges opened in New York on Friday, set to extend its 60% decline on Thursday. Bonds had posted record declines, igniting a broad selloff in US bank shares that also spread to Asia and Europe. In the US, the KBW Bank Index on Thursday had its worst day since June 2020, as its members shed more than $90 billion of value. In Europe, the biggest banks lost more than $40 billion from their market caps on Friday.

Management’s solution appears to have been to seek out yield through a lot of long-duration bonds. The bank started to lose deposits as VCs pulled cash/burnt through operating capital.

You must be logged in to post a comment.