Biden’s green energy policies (limiting supply) caused a tremendous surge in energy prices and food prices (one has to pay to get food shipped!). But in order for The Fed to cool inflation, they are in the process of tightening their loose monetary policy since late 2008.

One of the consequences (intended or unintended) is that as mortgage rose, homebuyer mortgage payments rose 45.5% YoY.

As The Federal Reserve battles inflation (caused by excessive monetary stimulus since 2008), Biden’s green energy policies and excess Federal government spending), we can see that the US Treasury 10yr-2yr yield curve has inverted to -54.4 basis points, the lowest since 1982 after Fed Chair Paul Volcker’s war on inflation.

The US Treasury 10yr-2yr yield curve typically inverts (or goes below zero) several months prior to a recession and is most inverted since 1982.

Fed Funds futures data points to the target rate rising to 4.613% by the May ’23 FOMC meeting … then declining.

Since this is rather miserable news for the economy, I will now play my favorite Bruce Springsteen tune, Sherry Darling.

At least the Dow Jones mini-me futures are up this morning.

The US Dollar/Euro cross currency is rising with Fed tightening.

As expected, The Federal Reserve raise their target rate by 75 basis points today. While that sounds like an inflation (blue line)-crushing rate hike, look at the slowly shrinking Fed Balance Sheet (gold line).

Of course, the risk of a recession (dark blue line) is on the increase.

Given the increasing likelihood of a recession, The FOMC’s Dots Project shows The Fed’s target rate increasing to 4.625% in 2023, then gradually declining to 2.5% in the long run.

Fed Funds Futures data points to a peak in May 2023.

It was not immediately clear why buyers had submitted requests for capacity when Russia has given no indication since it shut the line that it would restart any time soon.

Russia, which had supplied about 40% of the European Union’s gas before the Ukraine conflict, has said it closed the pipeline because Western sanctions hindered operations. European politicians say that is a pretext and accuse Moscow of using energy as a weapon.

But German inflation, using CPI, is only 7.9%. Something has to give!

On the western front (US), the US Treasury 10yr yield is up +10.2 bps. And sovereign yields in Europe are all above 10 bps.

Even Obama’s economic advisor, Larry Summers, is wondering why Biden won’t allow pipelines to be build to reduce energy prices and reduce inflation.

Having said that, US mortgage rates are now the highest since 2008 and continue to rise with the expectation of more Fed rate hikes this year. Even core inflation is on the rise motivating The Fed to do more tightening since they aren’t receiving any help from Biden on energy or Congress in terms of massive spending of our money.

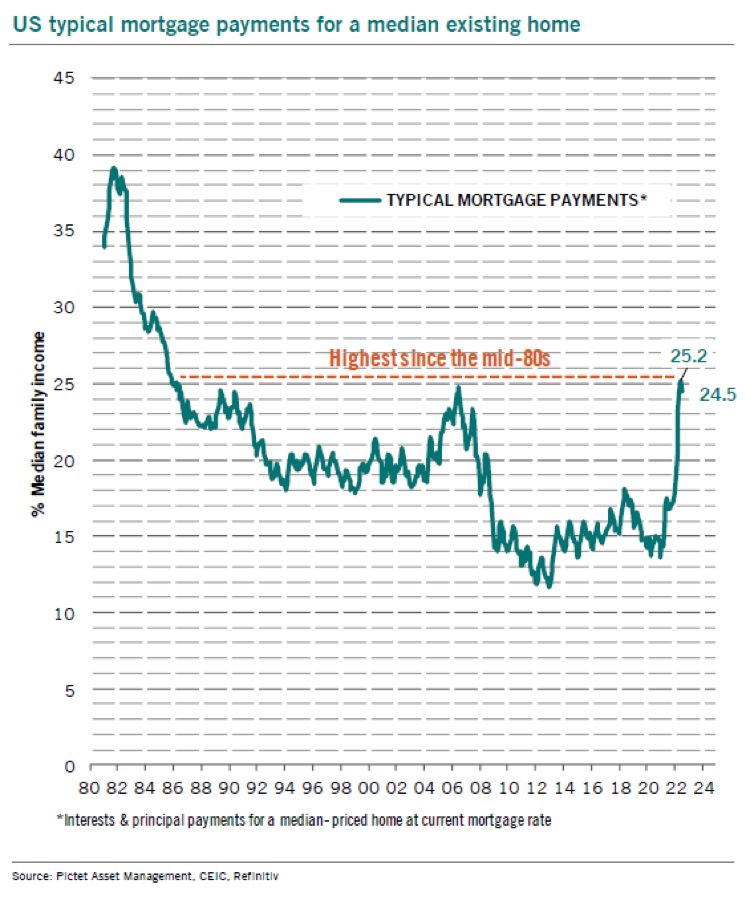

Mortgage payments for a median existing home in the US is back to the mid-1980s.

Data from Fed Funds futures implies that The Fed will raise their target rate to 4.50% by March 2023, then slowly lower rates.

Futures are down with the prospect of a 75 basis point bump in rates tomorrow. The Dow Jone Mini is down -167 points.

The National Association of Home Builders market index fell more than expected in September to 46, the lowest reading since 2012 (if I exclude the Covid economic shutdown).

Note that the NAHB market index is declining along with at the increase in the 30yr mortgage rate.

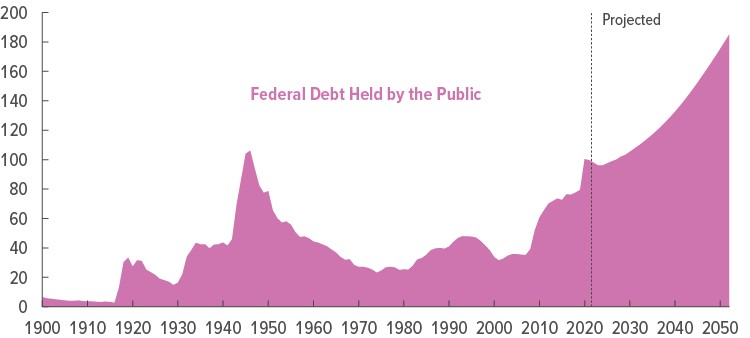

The Federal Reserve’s Open Market Committee (FOMC) will announce their latest round of rate increases on Wednesday, September 21st, at 2pm EST. Will the members of the FOMC discuss the fact that the US debt load is now at a whopping 123% of GDP?? Or will the FOMC only discuss inflation in its deliberations?

The Fed is expected to raise the upper-bound of their target rate to 3.25%, a 75 basis point increase in a futile attempt to cool inflation. Yet the rampant spending by Biden, Pelosi and Schumer (3 of the 4 Horsemen of the Economic Apocalypse) has raised the Federal Debt to GDP ratio to 123%. Even more disturbing, M2 Money Velocity (GDP/M2 Money) is near the all-time low. Meaning that rampant Federal spending is doing little to increase GDP.

Inflation is stubborn because “goin’ green!” by 1) restricting US fossil fuel production and exploration and 2) Biden/Congress endless spending splurge since Covid. So, The Federal Reserve has a tough problem: cooling inflation while US energy prices are up 54% under Biden. And those higher energy prices have percolated through the entire economy in terms of food prices and heating prices.

Where do we sit? The US Treasury 10yr-2yr yield curve remains inverted (a sign of impending recession). Mortgage rates are the highest in 14 years as The Fed tightens.

If we look at Fed Funds Futures data, we can see that traders expect The Fed’s target rate to rise to 4.395% by March 2023’s FOMC meeting. Then traders expect The Fed to take their enormous foot off the tightening pedal.

Yes, inflation is crushing the middle class and low-wage workers. Average hourly earnings YoY after we subtract inflation are negative.

Taylor Rule? Currently, the Taylor Rule based on Core inflation of 4.56% YoY suggests a Fed target rate of 9.14%. Since traders anticipate the target rate to peak at 4.395%, The Fed will almost be halfway towards cooling inflation.

The problem is … Fed Chair Powell and Treasury Secretary Yellen don’t like rules limiting their “power.” Powell and Yellen think the Taylor Rule is a New Jersey ham product.

Its a beautiful morning here in Columbus Ohio! Unfortunately, things are not so beautiful for the US economy.

Let’s begin with the US Treasury 10yr-2yr yield curve slope. Historically, the yield curve inverts prior to a recession. As of this sunny morning, the US Treasury yield curve is inverted and sinking further into inversion. Notice that headline inflation (blue line) has increased declined slightly after hitting 40-year highs as The Federal Reserve begins SLOWLY trimming their balance sheet (orange line). The green line is the expectation of Fed rate hikes by the December 2022 FOMC meeting indicating further monetary tightening.

Goldman Sachs Group Inc. cut its US economic growth estimates for 2023 after recently boosting its predictions for Federal Reserve interest rate hikes.

US gross domestic product will increase 1.1% in 2023, economists including Jan Hatzius wrote in a note Friday, compared with a forecast of 1.5% previously. The projection for 2022 was left unchanged at 0%.

Goldman raised its federal funds rate forecast by 75 basis points over the last two weeks for a terminal rate forecast of 4% to 4.25% by the end of 2022.

Then we have Federal Express which plunged -43.85 points on Friday. I use this an example on how inflation begat Fed tightening that begat an economic slowdown.

The Biden Administration is cheering the “Inflation Reduction Act” and the recent decline in the rate of inflation to a gut-wrenching 8.3% YoY. Bear in mind that since Biden was sworn-in as President, WTI Crude Oil is UP 75%, gasoline prices UP 54%, food prices are UP 48% and the Strategic Petroleum Reserve is DOWN -32%.

Then we have Gold and Bitcoin relative to the INVERSE of the US Dollar since Biden was installed as President.

Raging US inflation is resulting in Federal Reserve monetary tightening, causing the 30-year US mortgage rate to hit it highest level since November 2008 (the beginning of Fed Quantitative Easing). Bankrate’s 30-year mortgage rate just hit 6.28%, the highest rate in 14 years.

The Biden Administration will be remembered for crippling inflation, the highest in 40 years AND the highest mortgage rate in 14 years.

And with Fed chatter about hiking rates, Dr T (me) predicts pain for the mortgage market.

You must be logged in to post a comment.