Forbes has an interesting article on the Japanese “miracle” entitled “The $5 Trillion Inflation Time Bomb No One’s Talking About.”

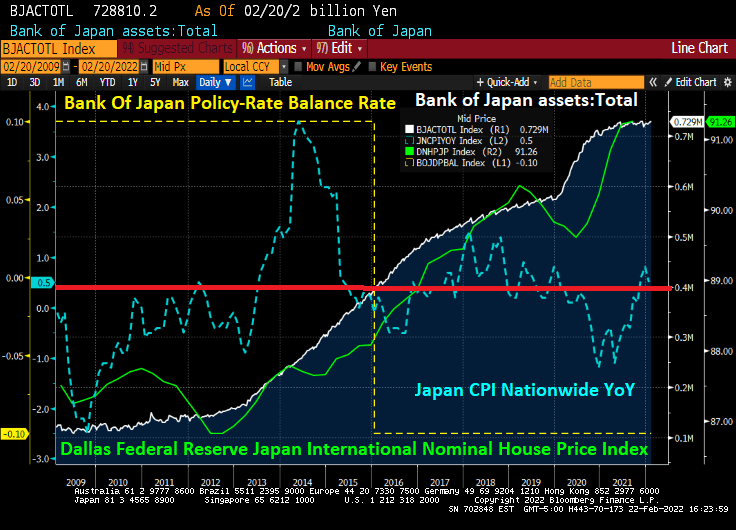

It’s taken nine years and the Bank of Japan supersizing its balance sheet to the $5 trillion mark, but Asia’s second-biggest economy finally has some inflation.

Officials in Tokyo are realizing the hard way, though, that it’s best to be careful what you wish for as bond yields spike.

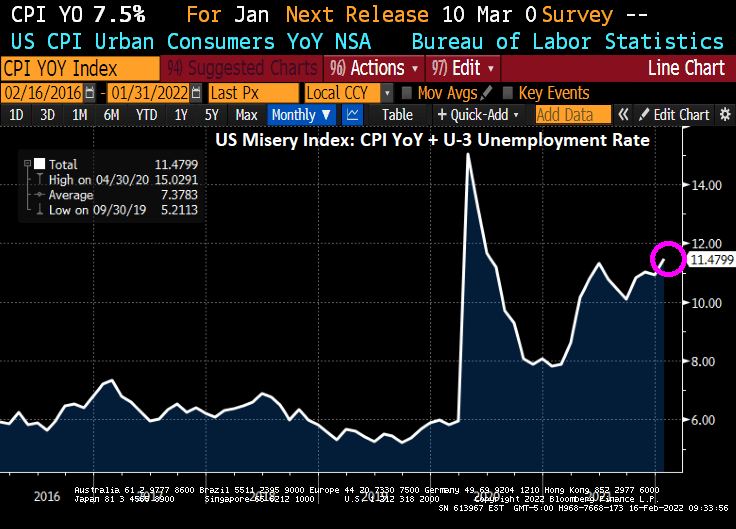

Granted, the gains in consumer prices Japan is reporting are negligible compared to those in the U.S. and China. And inflation is still a good distance from the BOJ’s 2% target. Still, the 0.5% rise in consumer prices in January year-on-year is already unnerving the bond market. It followed a 0.8% jump in December and marks the fifth straight month of increases.

The worry is that Japan’s inflation is the “bad” kind. Haruhiko Kuroda was hired as BOJ governor in March 2013 to end deflation. Kuroda unleashed tidal waves of liquidity. That drove the yen down 30%, generated record corporate profits and sent Nikkei 225 Average stocks to 31-year highs.

Despite a staggering balance sheet with a -0.10 bps policy rate, Japan has only 0.5% inflation.

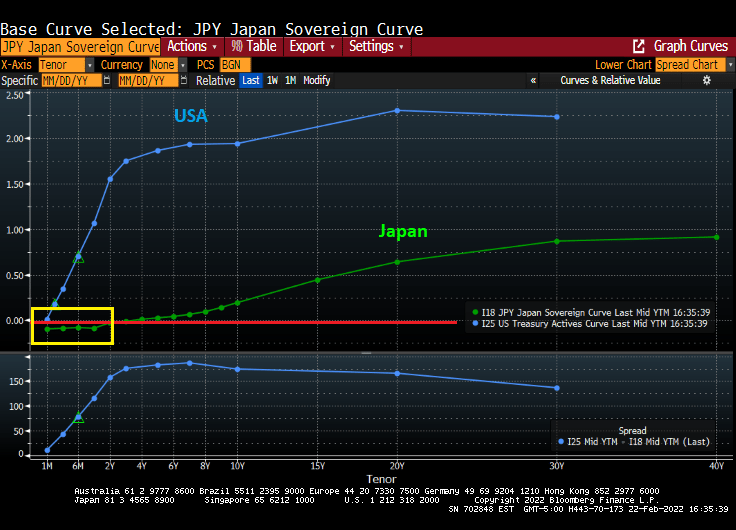

And Japan’s yield curve is negative at 3 year tenor and less.

How is it that Japan has virtually no inflation with negative rates but the USA has 7.5% inflation with a 0.25% target rate? Could it be the USA undertook massive fiscal spending related to COVID and reduced energy sources in an effort to go “green” that led to 7.5% inflation??

Good governments don’t go on wild, wasteful spending sprees and shut off energy sources like the Biden Administration and Congress.

You must be logged in to post a comment.