That means its initial jobs results were inflated by 439,000 positions, and the job market is not as healthy as the government suggests.

Since the government wiped out 439,000 jobs after the fact, the total percentage of jobs created by the government last year is even higher.

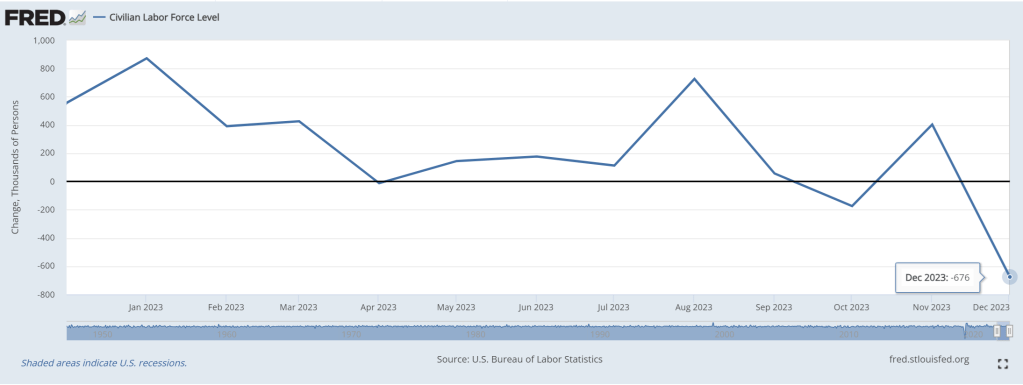

But just in December, the civilian labor force shrunk by 636,000 jobs.

Increased government hiring has been driving the jobs numbers higher. This is NOT good since government doesn’t produce anything other than regulations and red tape.

Again, the government sector in December ranked high in job creation.

The health care and social assistance sector, which relies heavily on money from government spending, created about 59,000 jobs.

The economy lost 1.5 million full-time workers since June of last year, while adding 796,000 part-time workers.

That means more workers are holding down multiple jobs to pay for a higher cost of living due to a cumulative 17.4% inflation rate under this White House.

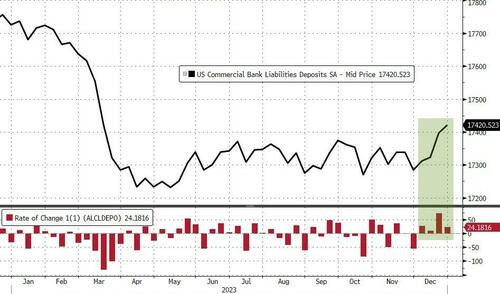

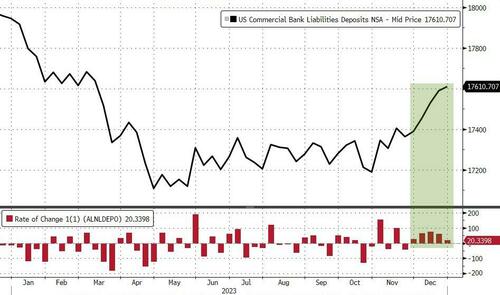

On a non-seasonally-adjusted basis, deposits rose almost in line, up $20.3BN (the fifth week of inflows in a row)…

Source: Bloomberg

Interestingly the sizable deposit inflows are occurring alongside sizable money-market fund inflows…

Source: Bloomberg

…now we know where all that reverse repo liquidation cash is going…

Source: Bloomberg

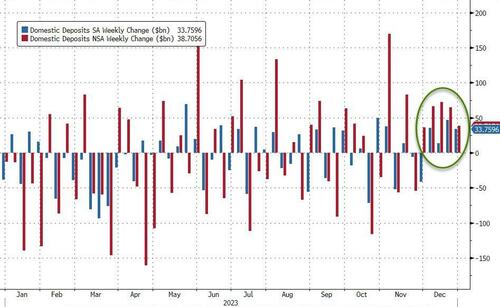

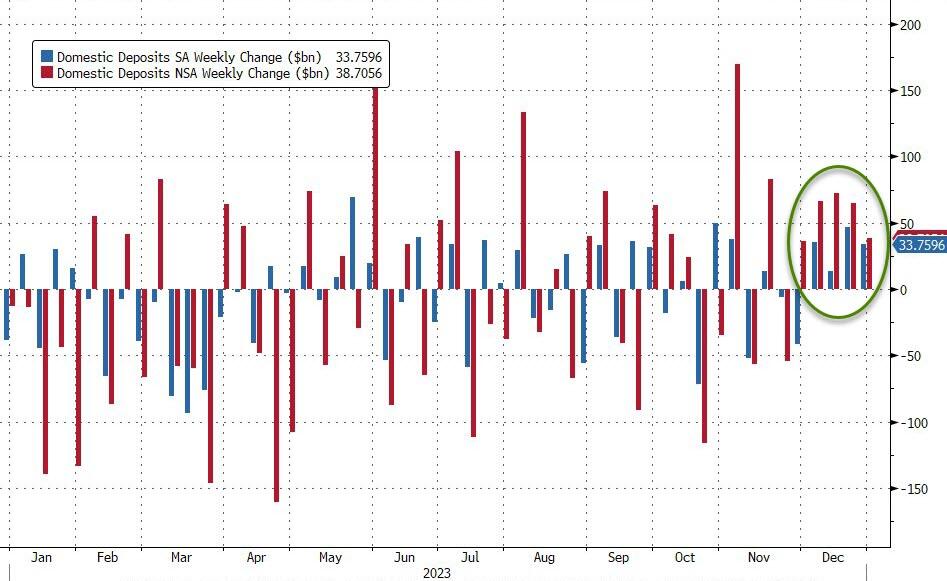

Excluding foreign bank flows, the picture is even rosier with domestic bank deposit inflows of $33.8BN (SA) and $38.7BN (NSA) – the 5th week in a row of NSA inflows…

Source: Bloomberg

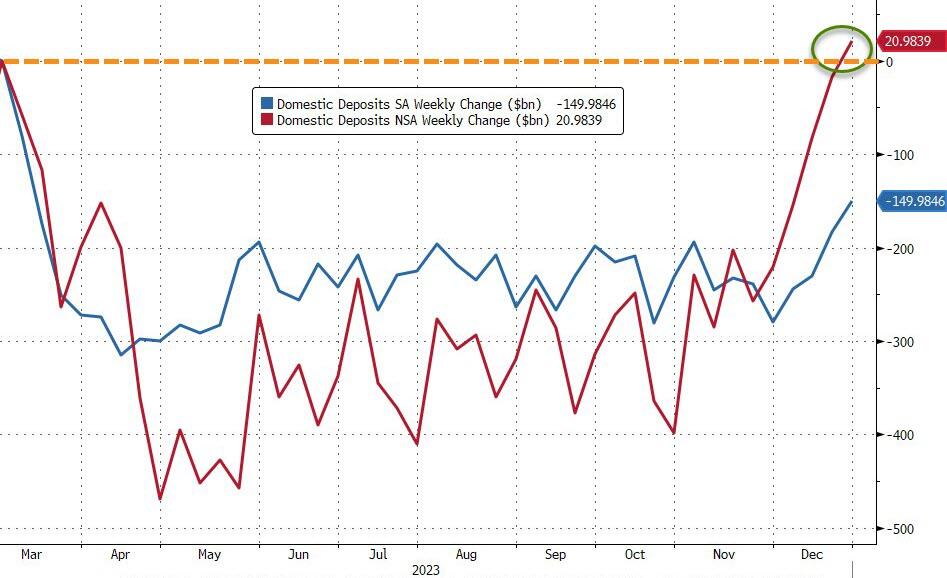

While it may surprise some, on an NSA basis, domestic bank deposits are now back above pre-SVB levels…

Source: Bloomberg

Large banks saw $24BN inflows last week and Small Banks $9.4BN (on an SA basis) and for the 5th week in a row both large and small banks saw NSA inflows (+$30BN and +$8.7BN respectively)…

Source: Bloomberg

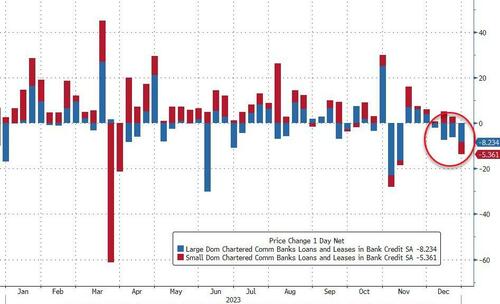

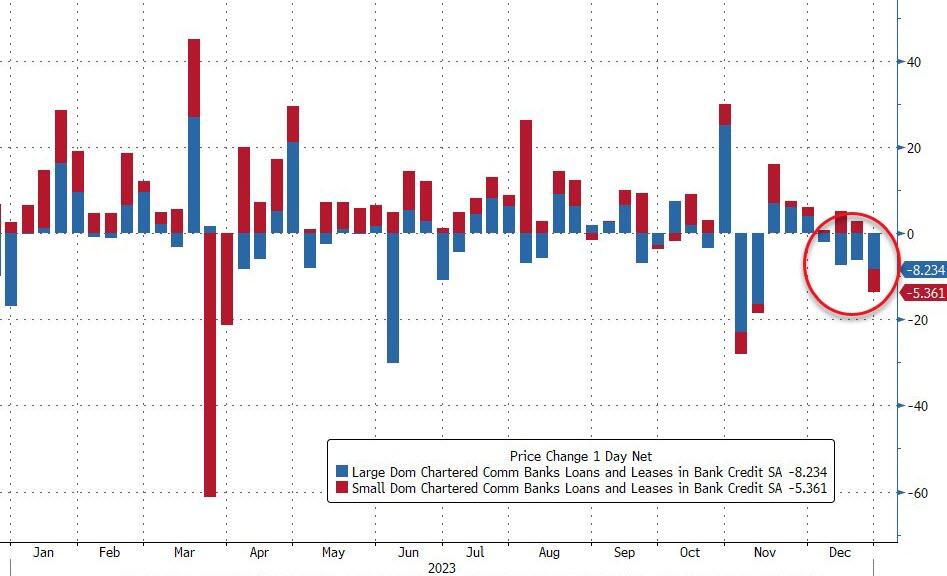

On the other side of the ledger, loan volumes continued to shrink (despite the deposit growth). Large bank loan volumes fell $8.2BN (the 4th week of falling loan volumes in a row)…

Source: Bloomberg

Which leave us continuing to highlight the fact that there is potential trouble brewing still as the key warning sign continues to flash red (Small Banks’ reserve constraint – blue line), supported above the critical level by The Fed’s emergency funds (for now)…

Source: Bloomberg

As the red line shows, without The Fed’s help, the crisis is back (and large bank cash needs a home – green line – like picking up a small bank from the FDIC).

All of which keep us wondering, are we setting up for another banking crisis in March as:

1) BTFP runs out…

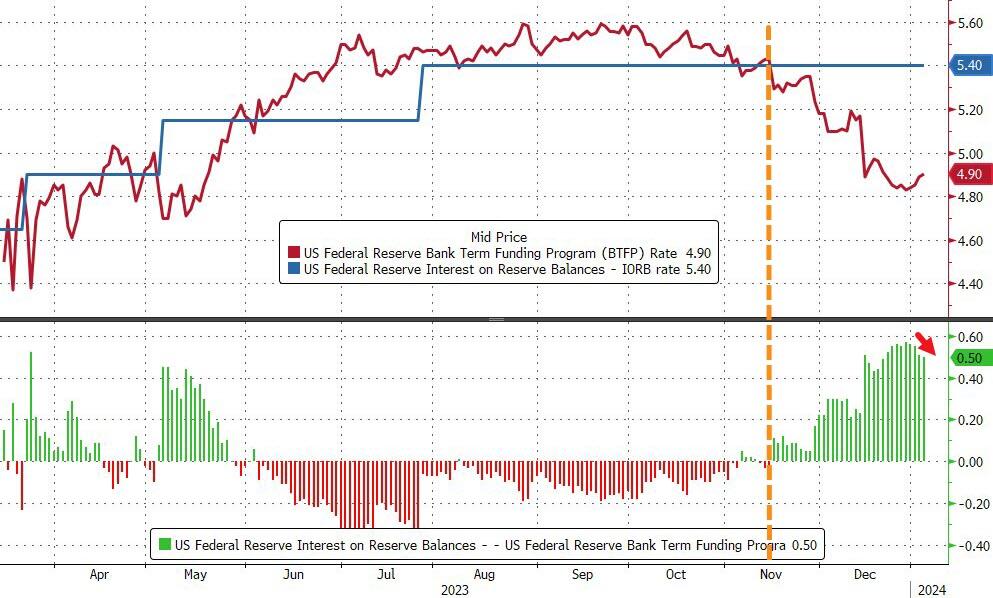

It was only a 12 month temporary program, and it is going to be hard for The Fed to keep it alive. The BTFP-Fed Arb continues to offer ‘free-money’ (and usage of the BTFP has risen by $32BN since the arb existed), but the spread has narrowed a smidge from a peak near 60bps to 50bps today…

Source: Bloomberg

Which will make it hard for The Fed to defend leaving the facility open after March when its “temporary” nature is supposed to expire.

“In justifying the generous terms of the original program, the Fed cited the ‘unusual and exigent’ market conditions facing the banking industry following last spring’s deposit runs,” Wrightson ICAP economist Lou Crandall wrote in a note to clients.

“It would be difficult to defend a renewal in today’s more normal environment.”

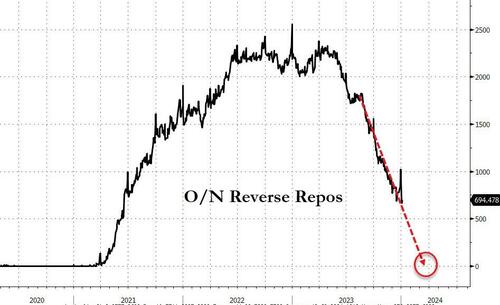

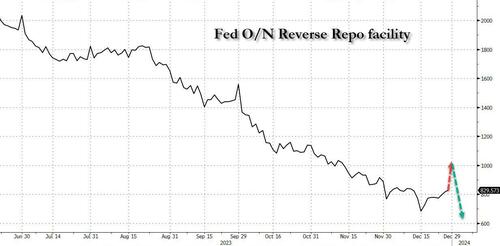

2) RRP drains to zero…

…at which point reserves get yanked which means huge deposits flight.

Source: Bloomberg

Is this the real reason why The Fed ‘pivoted’? It knows what’s coming??

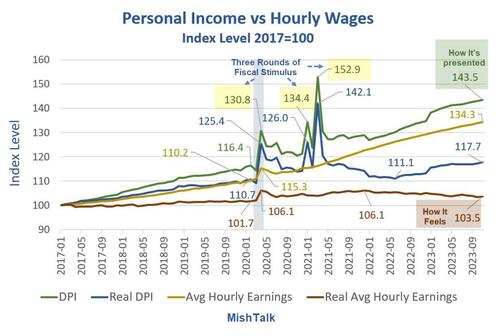

Income is rising and so are wages. Even real income is up. But real wages are another matter.

Personal income data from the BEA, hourly wages from the BLS, real hourly earnings and chart by Mish.

Personal Income vs Hourly Wages Notes

DPI means Disposable Personal Income. Disposable means after taxes.

Real DPI means inflation adjusted using the Personal Consumption Expenditures (PCE) deflator. Real DPI is a BEA calculation.

Average hourly earning are for production and nonsupervisory workers.

Real wages are deflated by the Consumer Price Index (CPI) not the PCE.

The BLS does not report a real hourly wage. I used the CPI-W index for production and nonsupervisory workers, produced by the BLS, as the deflator.

Personal Income Definition

The BEA defines personal income as “Income that people get from wages and salaries, Social Security and other government benefits, dividends and interest, business ownership, and other sources.”

Rental income is a part of other sources.

Three Rounds of Fiscal Stimulus

Round 1, March 2020: $1,200 per income tax filer, $500 per child(CARES Act) – Trump

Round 2, December 2020: $600 per income tax filer, $600 per child (Consolidated Appropriations Act, 2021) – Trump

Round 3, March 2021: $1,400 per income tax filer, $1,400 per child (American Rescue Plan Act) – Biden

The three rounds of free money fiscal stimulus (literally a helicopter drop), plus eviction moratoriums put an unprecedented amount of money in people’s hands. In addition, unemployment insurance paid people more to not work than they received working.

The third round of stimulus under Biden was totally unwarranted. However, it is also worth noting that Trump wanted a much bigger second stimulus package than the Republican Congress gave him. Trump is no fiscal hero.

The three stimulus packages, on top of supply chain disruptions, energy disruptions due to the war in Ukraine, and Bidenomics in general, set in motion the biggest wave of inflation in over 30 years.

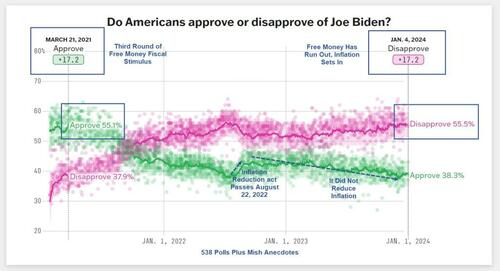

Biden went from an approval rating of 17.2 percent to a disapproval rating of 17.2 percent.

Peak Free Money

In addition to declining real wages, perhaps Biden’s big problem is the free money has run out.

Biden’s popularity peaked in March of 2021 along with stimulus. Was that a honeymoon impact or peak free money?

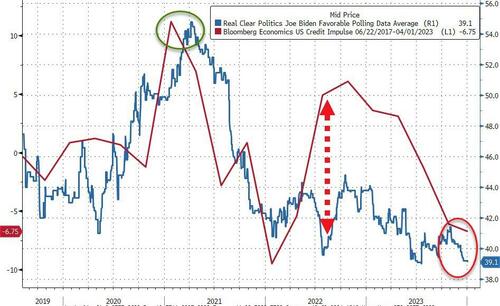

[ZH: While not a perfect indicator, the lagged US credit impulse perhaps provides a proxy for US fiscal excess and when overlaid with Biden’s approval rating, it is clear that 2022’s re-acceleration did nothing for people’s faith in him… and it’s only got worse…]

I suspect a bit of each coupled with hope of more free money, especially student loan forgiveness.

Sending free money to Israel and Ukraine does not help perceptions of how Biden is doing. And neither does the border or ridiculous energy regulations that cost people money.

Biden keeps telling people what a great job he has done.

I don’t believe it and most don’t either. And that shows up in the polls no matter what reason you assign.

Can Biden scrounge up some more stimulus? Because the private sector is not doing well under “Open Borders Biden.”

But to quote Cousin Eddie from Christmas Vacation, “Now hold on to your wad.” While the headline screamed remarkable, please note that the civilian labor force actually declined. As did the Employment-population ratio (to 60.1).

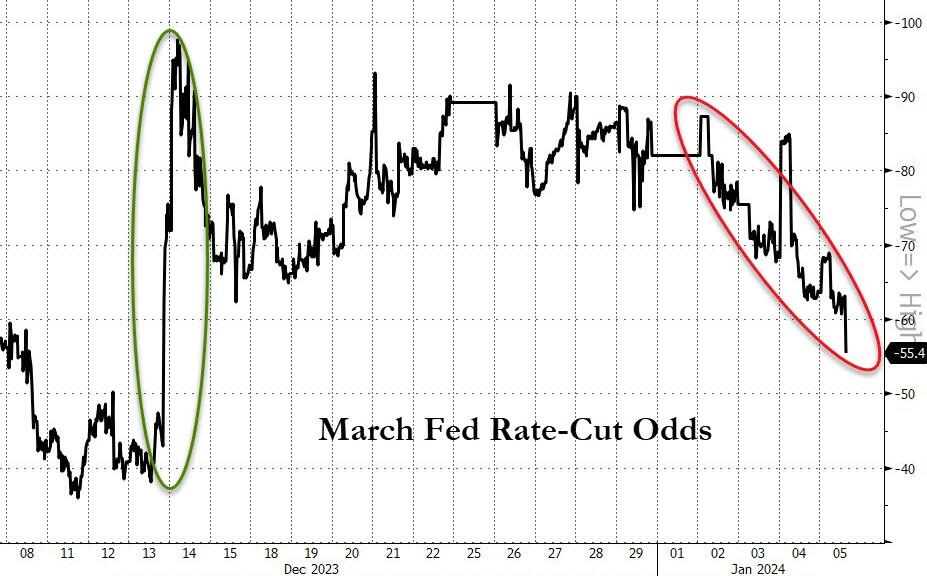

On the jobs report, the 2 year Treasury yield spiked to 4.4726%.

The odds of a March rate hike are decreasing.

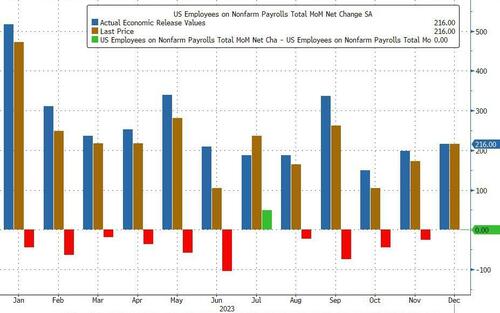

But next month today’s print will likely be revised sharply lower (perhaps even below 175K, meaning today was a miss). Why do we say that? Because once again the BLS revised not just one but both previous months sharply lower:

October revised down 45K from 150K to 105K

November revised down 26K from 199K to 173K

This means that ten of the past 11 jobs reports have been revised substantially lower.

There was some unexpectedly weakness in the labor force participation rate which dropped to 62.5% from 62.8%, missing expectations of an unchanged print. That’s because the number of people not in the labor force soared from 99.695MM to 100.540MM, an 845K increase largely due to a change in historical “data.”

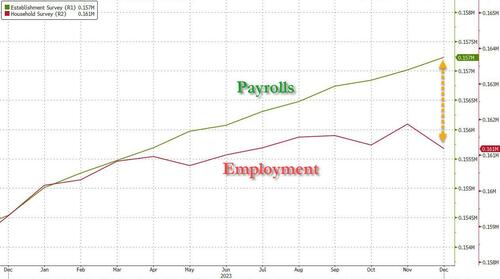

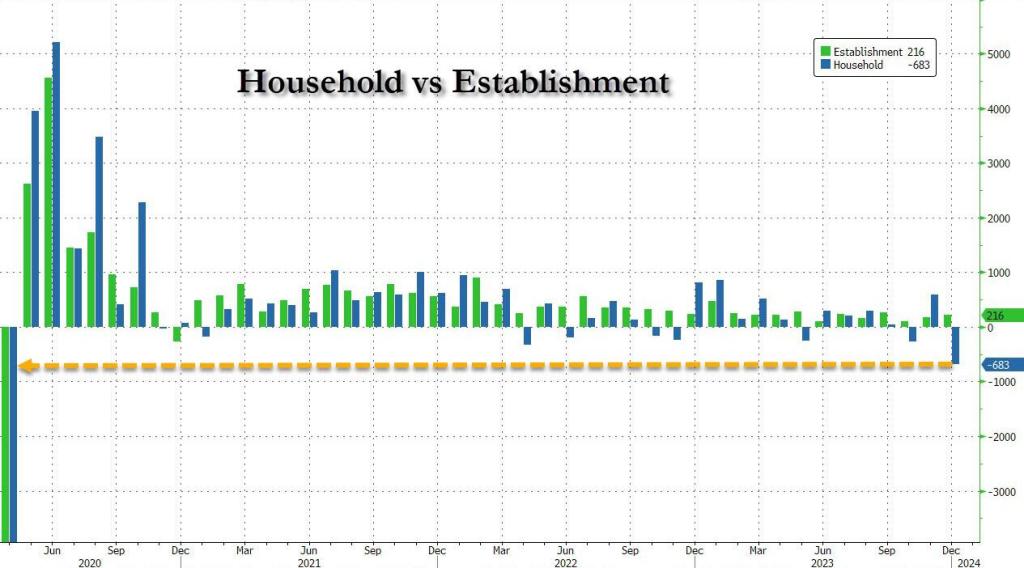

Consider the usual split between the Household and Establishment surveys: here, while payrolls reportedly increase by 216K (at least until they are revised lower next month), the Household Survey showed a plunge in employment of 683K!

Sadly, government employment increased by 52,000 in December. Employment continued to trend up in local government (+37,000) and federal government (+7,000). Government added an average of 56,000 jobs per month in 2023, more than double the average monthly gain of 23,000 in 2022.

But the biggest shocker is that the number of full-time jobs actually plunged by 1.5 million in December to the lowest since Feb 2023, while part-time jobs exploded higher by 762K to the highest on record. And there was another record: in the number of multiple jobholders. We will shortly have a post breaking all of this down.

The Household Survey showed a decline of an unprecedented 683K jobs.

So government is the largest growth in jobs (it is Biden after all and all he knows is government). Sad, since government produces nothing but taxes, regulations and debt. THAT is what Biden knows how to do!

Some content on this page was disabled on May 23, 2024 as a result of a DMCA takedown notice from Adtech lt, UAB. You can learn more about the DMCA here:

What a way to close out 2023! I need to find Happy Gilmore’s “Happy Place.”

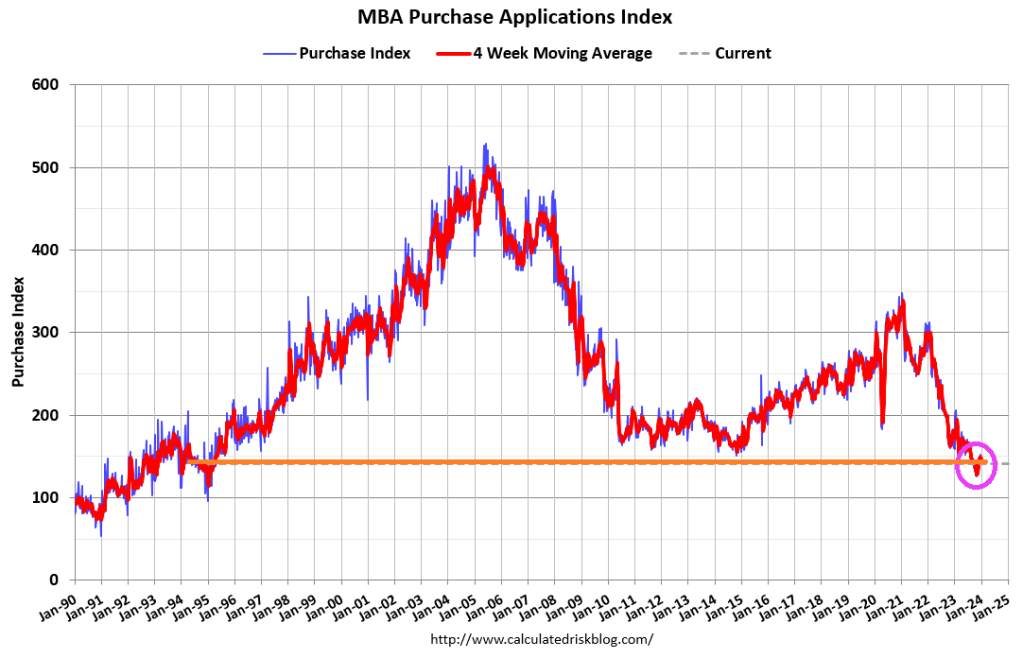

Mortgage applications decreased 9.4 percent from two weeks earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 29, 2023. The results include adjustments to account for the holidays.

The Market Composite Index, a measure of mortgage loan application volume, decreased 9.4 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 38 percent compared with two weeks ago. The seasonally adjusted Purchase Index decreased 5 percent compared with two weeks ago. The unadjusted Purchase Index decreased 34 percent compared with two weeks ago and was 12 percent lower than the same week one year ago.

The unadjusted Refinance Index decreased 43 percent from two weeks ago and was 15 percent higher than the same week one year ago.

The Fed continues to fight inflation. but rates cuts are forecast for 2024. But remember, mortgage rates are down slightly, but still up 130% under Biden.

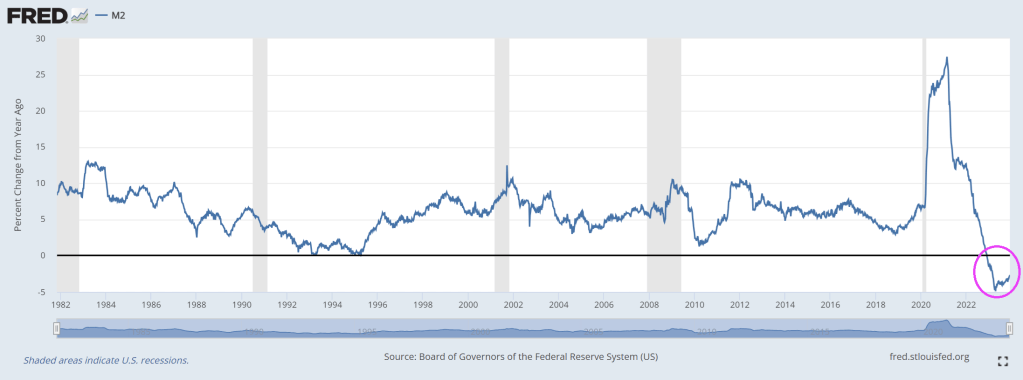

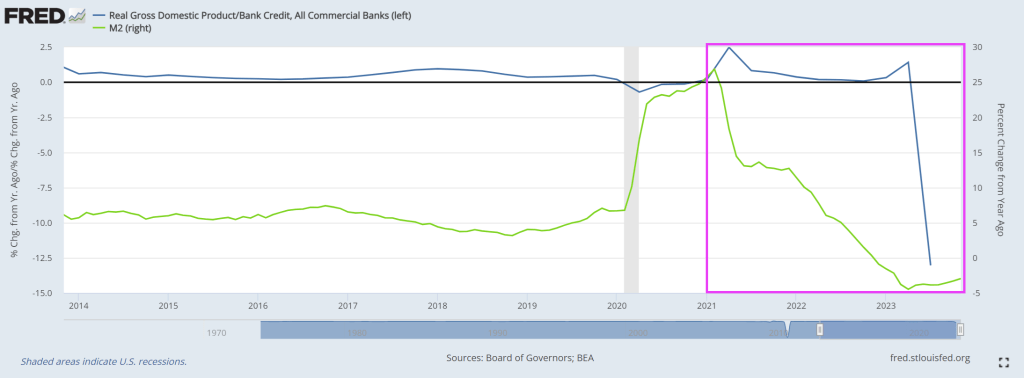

Take a look at this chart of real GDP YoY / Bank Credit YoY on the left axis and M2 Money growth on the right axis. I call this the velocity of bank credit. And it is sucking wind! Crashing to -13 in Q3.

Then we have US manufacturing PMI saw only two months in 2023 that were not in contraction and ended on a decidedly poor note with the final December print dropping to 47.9 (from 48.2 flash and 49.4 prior).

Source: Bloomberg

Across the board it was ugly with:

Renewed contraction in output as orders fall at sharper pace

Rates of inflation pick up

Joint-fastest drop in employment since June 2020

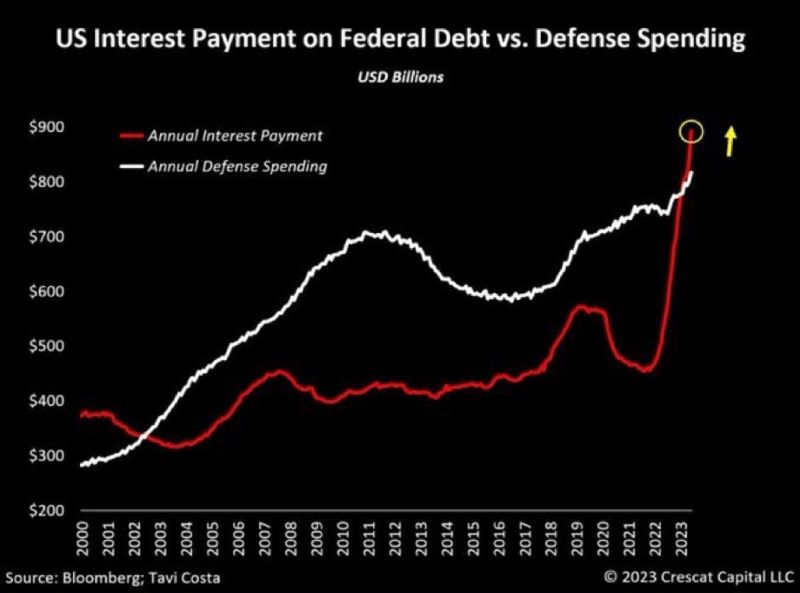

How bad is Biden’s fiscal policy? US interest payments on our bloated Federal debt is now higher than defense spending. Biden isn’t tuff enough to moderate spending or the border invasion.

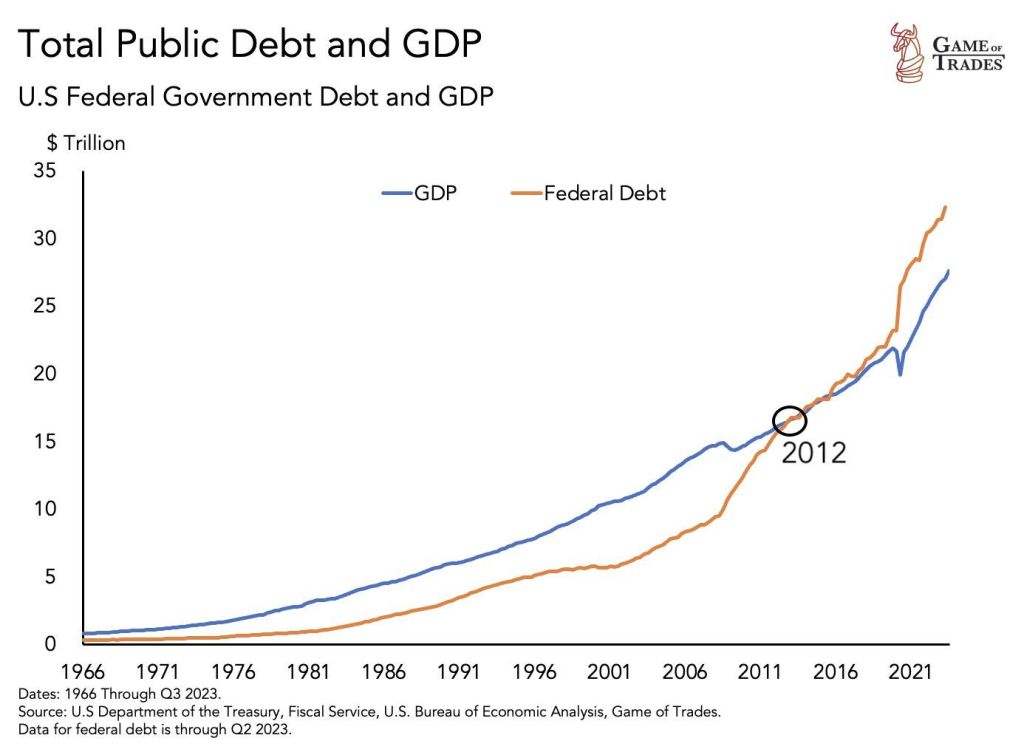

US government debt is now bigger than the US economy. This was unseen until 2012 when debt surpassed GDP for the first time.

In addition to almost $34 trillion in debt from our crazy spending, out-of-control government, we are on the hook for almost $213 TRILLION in unfunded liabilites (promises made to Americans that will likely not be honored).

The sad thing about the US Debt Clock summary is the $632,195 share per citizen of unfunded liabilties. That raises two questions. First, how can California’s Ken doll Governor Gavin “Greasy” Newsom give away free healthcare to ALL illegal immigrants? Second, since the invasion of illegal immigrants began under Biden/Mayorkas, will they be on the hook for the unfunded liabilities which they disordinately consume? Not likely. Maybe we should charge each illegal immigrant $632k admission fee.

California’s Ken doll Governor and fiscal imbecile Gavin Newsom.

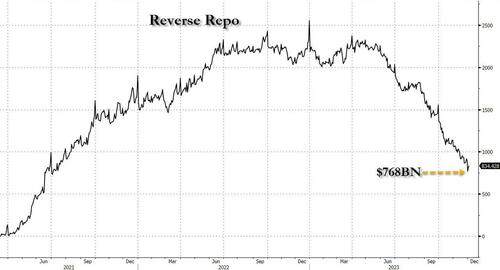

We didn’t have long to wait because just a few days later, on December 1 (just after the customary month-end window dressing period) when reverse repo tumbled to a fresh multi-year low of $765 billion…

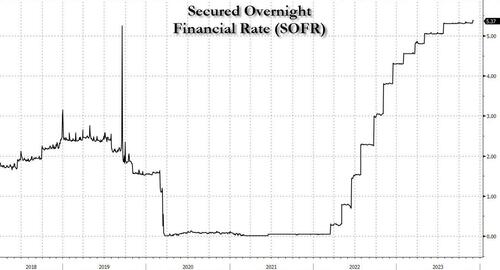

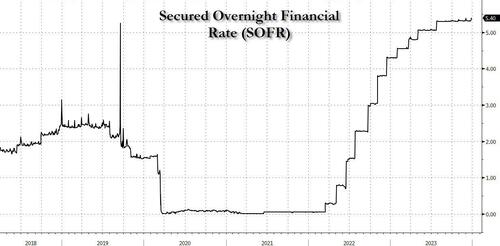

… things indeed broke as we explained in “Sudden Spike In SOFR Hints At Mounting Reserve Shortage, Early Restart Of QE” (in which we correctly previewed the coming Fed pivot at a time when most were still dead certain that Powell would only care about inflation for months to come): that’s when the the all-important SOFR rate (i.e., the new Libor) unexpectedly jumped 6bps to 5.39%, the highest on record…

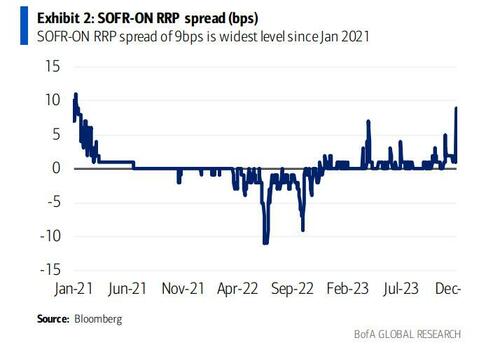

… also resulting in the largest SOFR spike vs ON RRP since Jan ’21, which hit 6bps.

The spike caught almost everyone by surprise, even such Fed-watching luminaries as BofA’s Marc Cabana because it was with “no new UST settlements, lower repo volumes, and lower sponsored bi-lateral volumes.” More ominously, and confirming our take from three weeks ago, Cabana warned at the time (full note here) that “the move is consistent with the slow theme of less cash & more collateral in the system” – i.e., growing reserve scarcity – and “may have been exacerbated by elevated dealer inventories, bi-lateral borrowing need, and limited excess cash to backstop repo. If funding pressure persists, it risks Fed re-assessment of ample banking system reserves & potential early end to QT.”

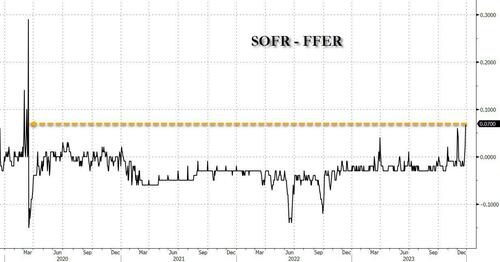

Then, the mini liquidity crisis disappeared almost as fast as it emerged, as SOFR rates eased off and the SOFR-Fed Funds spread normalized once GSE cash entered the market as it does every month….

… until today when not only did SOFR hit a new record high, ironically at a time when the market is pricing in more than 6 rate cuts in 2024…

… but the spread between the SOFR and the effective Fed Funds rate just spiked to the highest level since the March 2020 repo crisis…

.. with a similar move also observed in the spread between SOFR rate and the O/N Reverse Repo which similarly blew out to the widest since the start of 2021.

While there was no specific catalyst behind the sudden spike, two factors are the likely culprits: the year-end liquidity crunch, and the recent sharp increase in the Fed’s reverse repo facility, which has increased from a multi-year low of $683 billion on Dec 15 to yesterday’s $830 billion, and which STIR strategists expect will shoot up above $1 trillion in today’s final for 2023 reverse repo operation as a whopping $300+ billion in short-term liquidity in pulled from markets in just days.

That’s the bad news.

The good news is that come 2024 in a few hours, and specifically the first day of trading on Jan 2, we expect the reverse repo facility to plummet back to $700 billion once the year-end window dressing is over (especially with total US debt rising above $34 trillion to start the year), and floods the system with fresh liquidity which will stabilize the monetary plumbing at least until reverse repo dips below that key level of $700 billion at which point we expect the SOFR spikes to become a daily occurrence, and one which the Fed will no longer be able to ignore.

Indeed, one can already see traces of this in the repo market, where the rate on overnight GC repo first surged to 5.625% at the open on the final trading day of December before dropping to 5.45%, according to ICAP. It has since climbed back to 5.50%. But that’s still lower than where repo rates for Dec. 29 were trading during the prior session, as markets now start frontrunning the coming reverse repo liquidity flood.

Of course, once reverse repo eventually tumbles to $0 some time in March, all bets are off and the narrative shift to the next QE will begin.

“Say, can I sniff you if you take Trump off of Maine’s Presidential ballot??”

Nobody but Biden could so handicap an economy with horrible fiscal policies, massive debt, inflation and open borders. And then go to the Virgin Islands for yet another taxpayer paid vacation. Biden has spent 40% of his Presidency on vacations.

Bidenomics is a disaster for the US middle class. And Bidenomics with its inflation has led The Fed to counterattack and raises interest rates, leading to losses for The Federal Reserve (which is paid for by US Treasury) of over $130 billion.

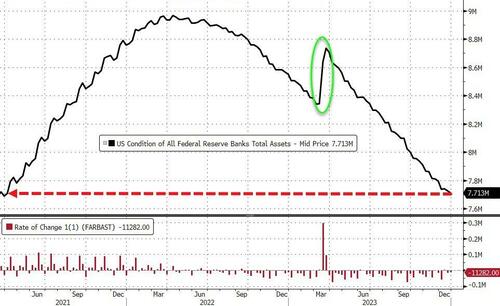

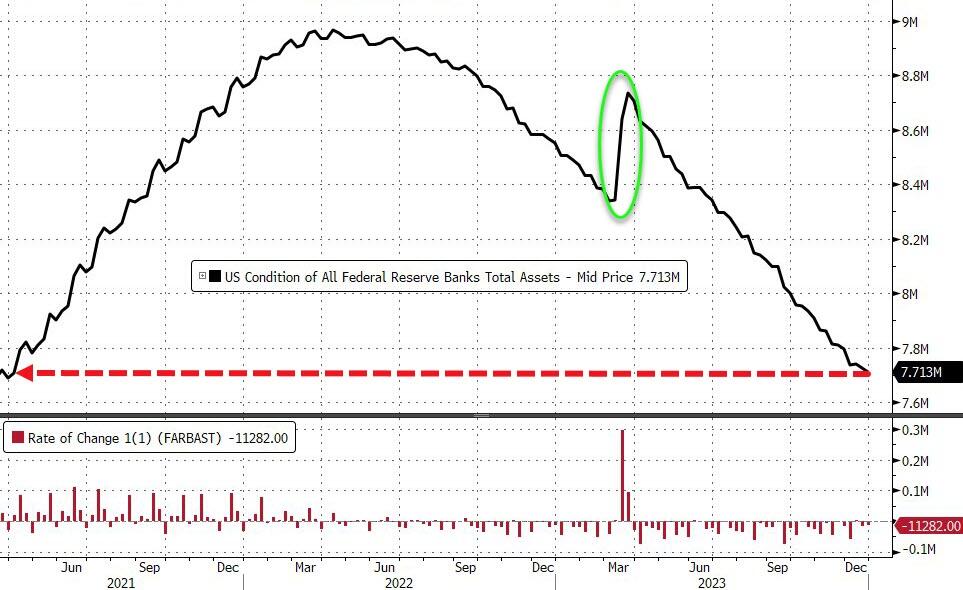

The Fed’s balance sheet shrank by $11.3BN last week to its lowest level since March 2021, but still remains elevated.

Source: Bloomberg

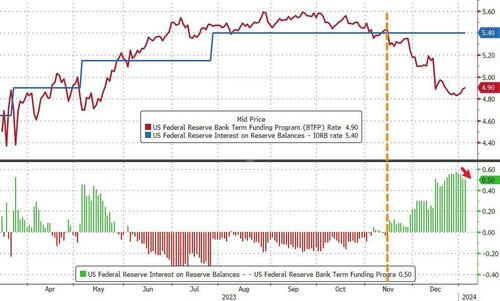

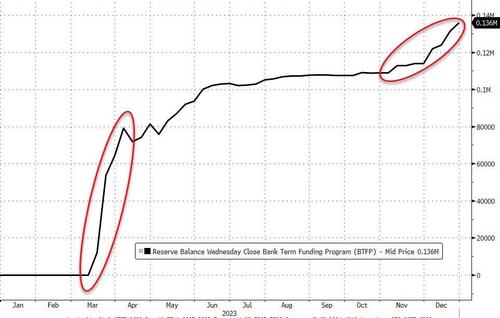

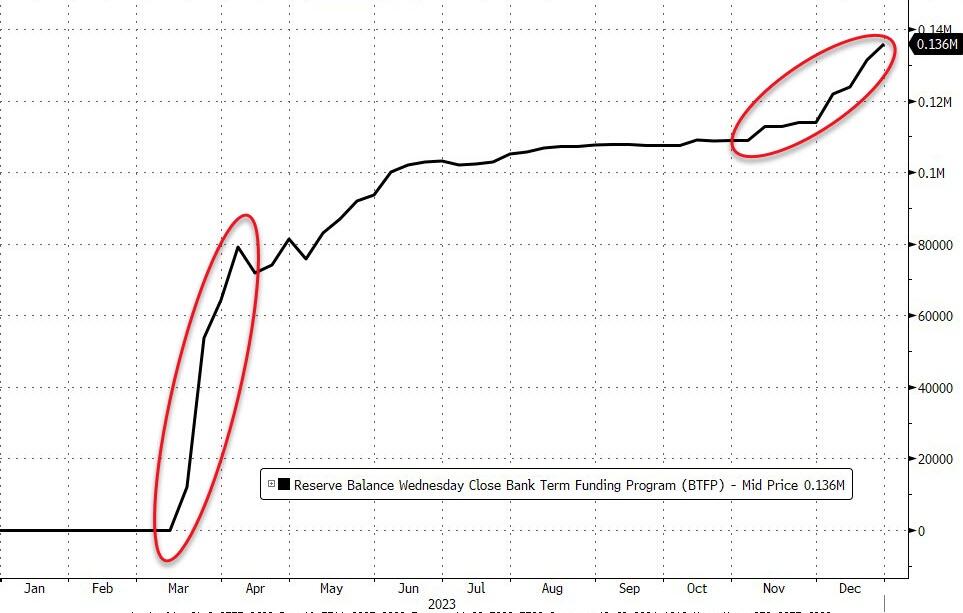

Usage of The Fed’s bank bailout facility rose by another $4.5BN last week to a new record high of $136BN…

Source: Bloomberg

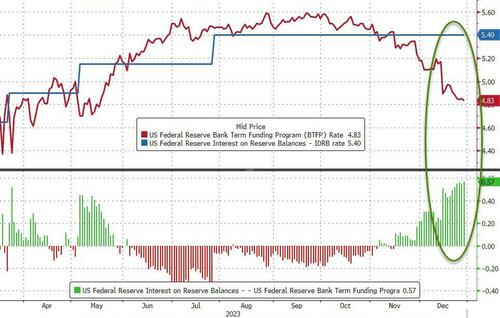

The BTFP-Fed Arb continues to offer ‘free-money’ (and usage of the BTFP has risen by $26.7BN since the arb existed):

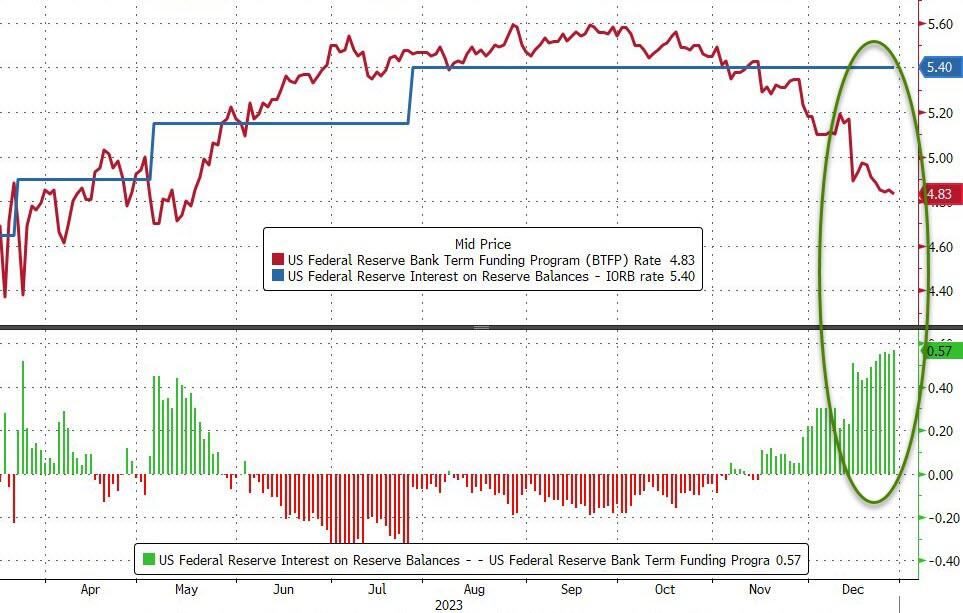

The rate on the Fed’s Bank Term Funding Program – which allows banks and credit unions to borrow funds for up to one year, pledging US Treasuries and agency debt as collateral valued at par – is the one-year overnight index swap rate plus 10 basis points.

That figure is currently 4.83%, down from 5.59% in September.

For institutions that have an account at the Fed, they can borrow from the BTFP at 4.83% and park that at the central bank to earn 5.40% – the interest on reserve balances.

Source: Bloomberg

The 57bp spread is the widest level since the Fed introduced the facility to support a struggling banking system after the collapse of California’s Silicon Valley Bank and Signature Bank in New York.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.