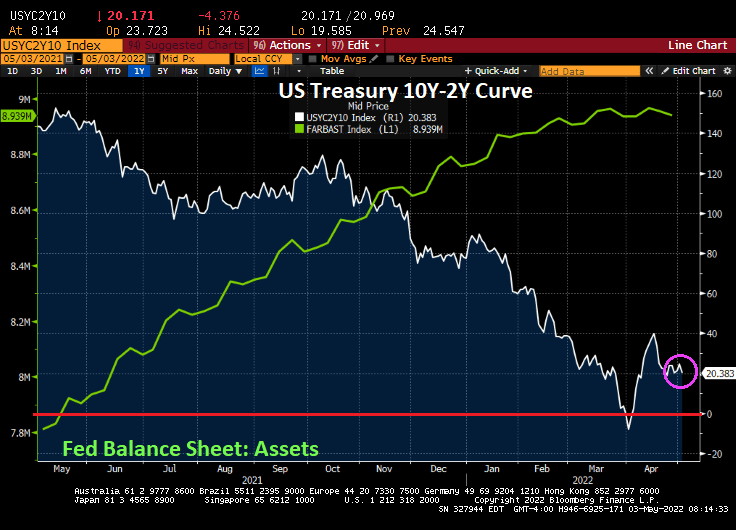

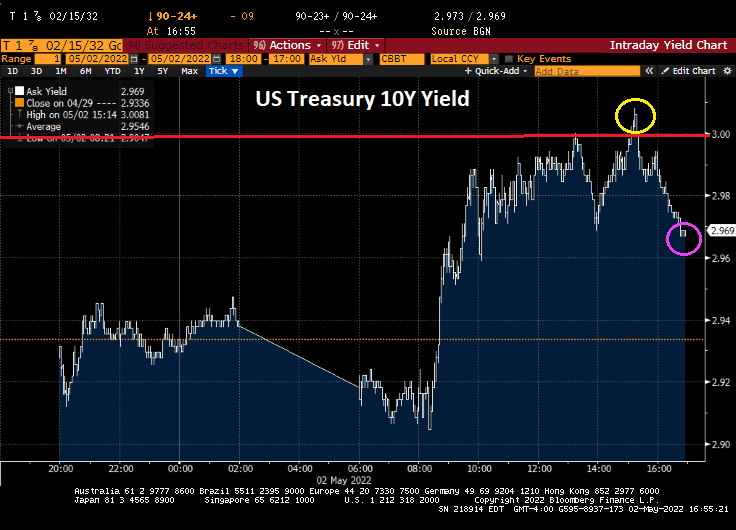

The U.S. Treasury market is showing signs of stress that may have implications for whether the curve keeps steepening.

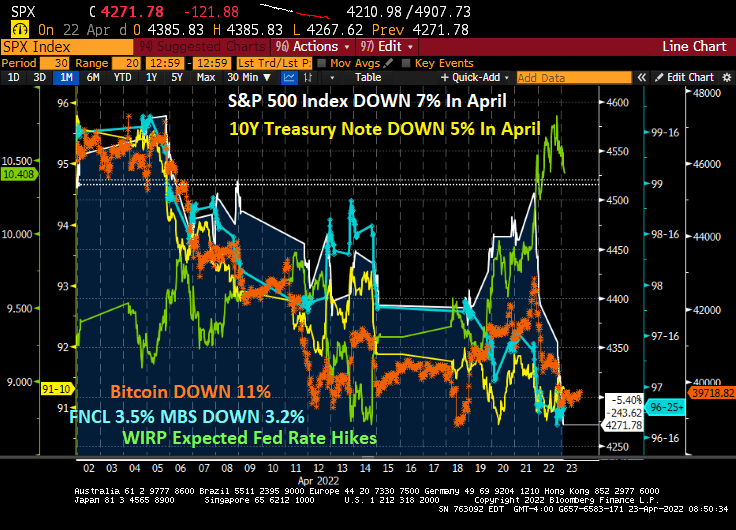

Over the past month the curve has retraced from an inversion to a steepening driven by a surge in yields on benchmark 10-year bonds. That has led to interesting outlier indications, as traders weigh the outlook for Federal Reserve interest rate increases and inflation.

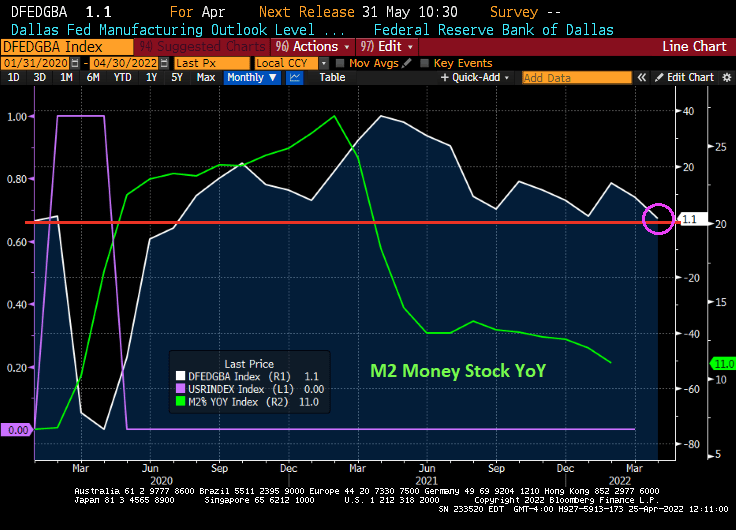

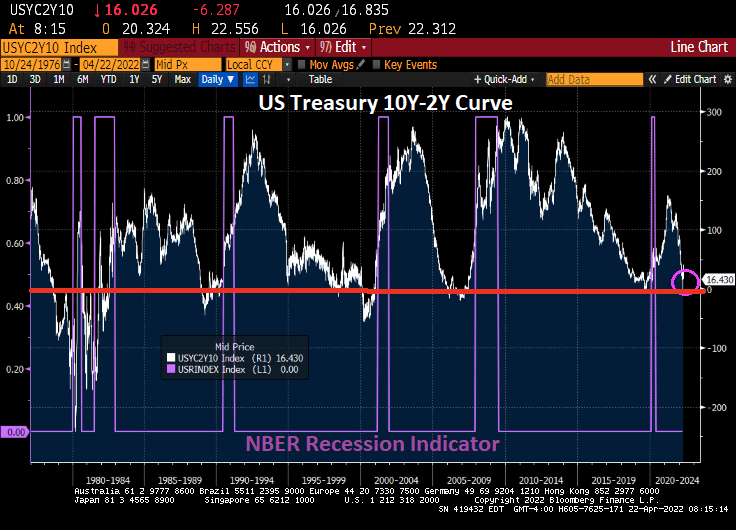

The US Treasury yield curve has settled-in at 20.383 bps (effectively zero) as The Fed continues its war on inflation.

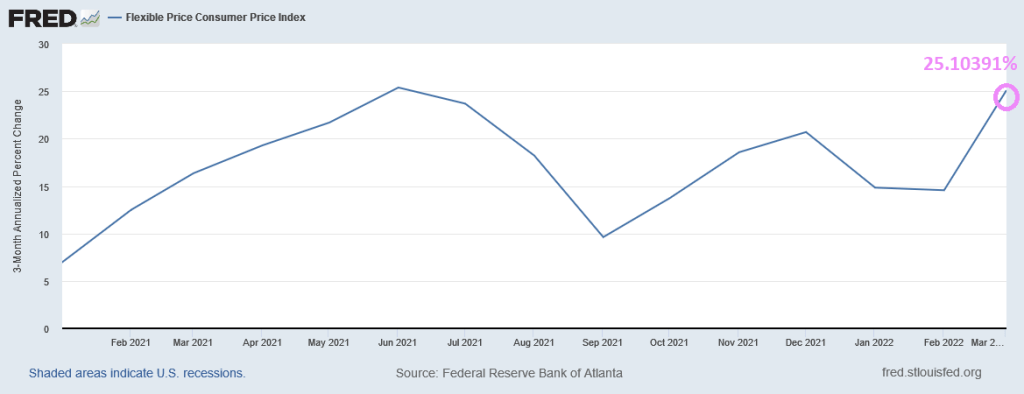

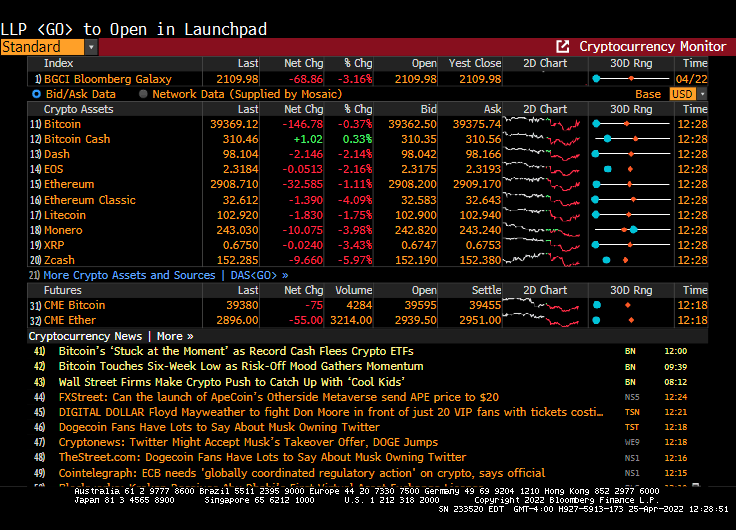

On the SOFR front, we see SOFR Coupons being slow to benefits from Fed rate hikes. So, SOFR Coupons are behaving like Stouffer’s lasagna, frozen and tasteless.

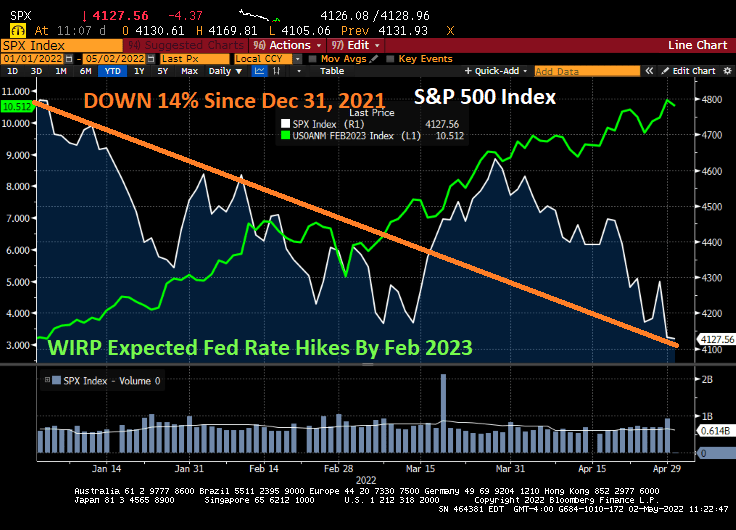

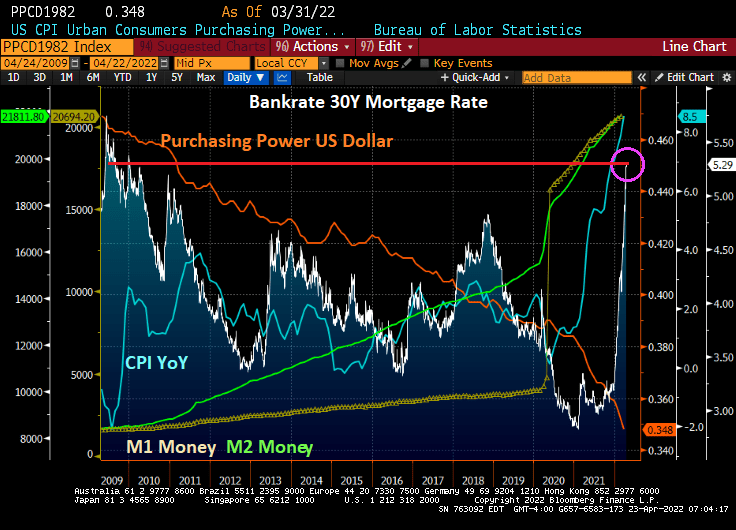

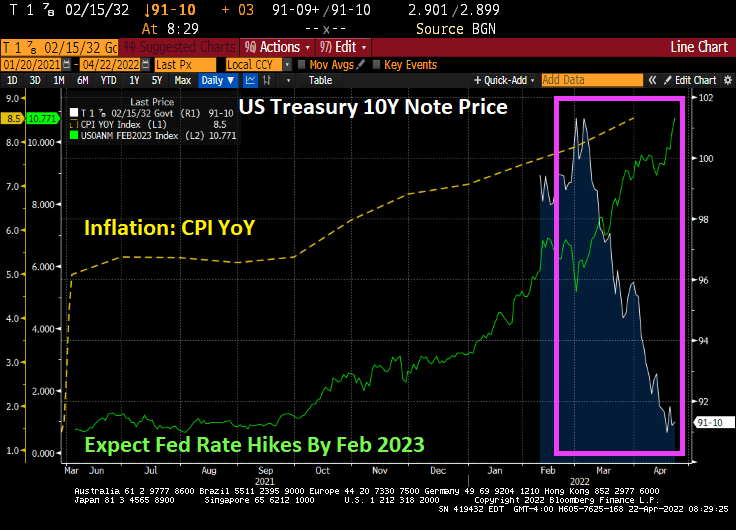

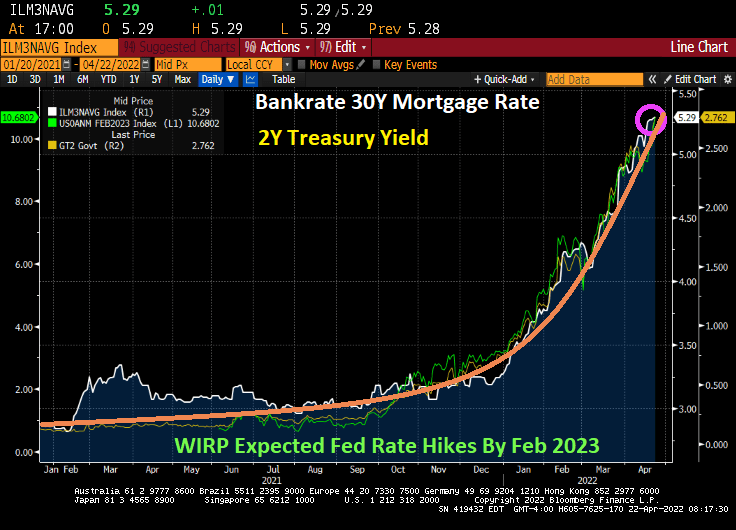

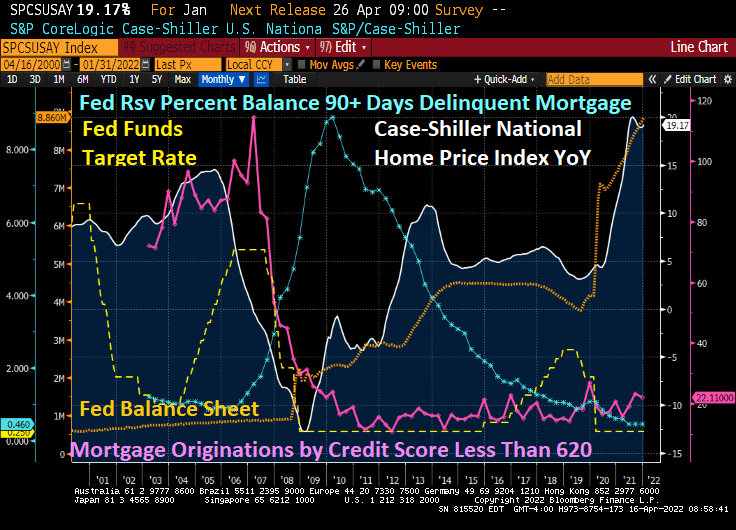

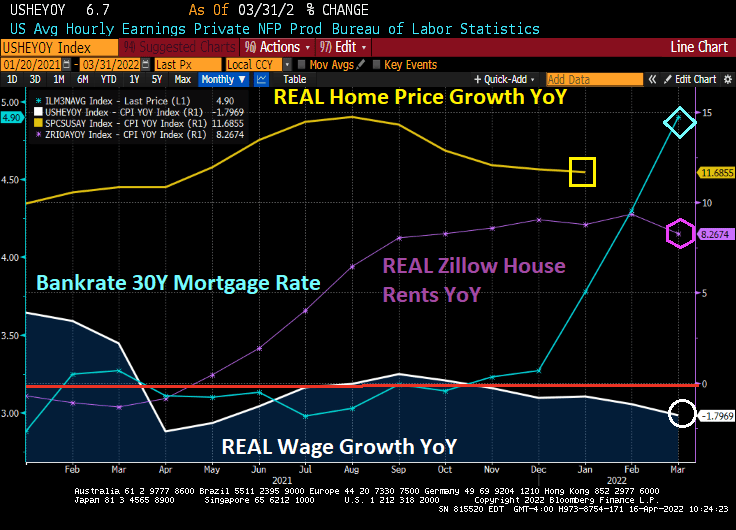

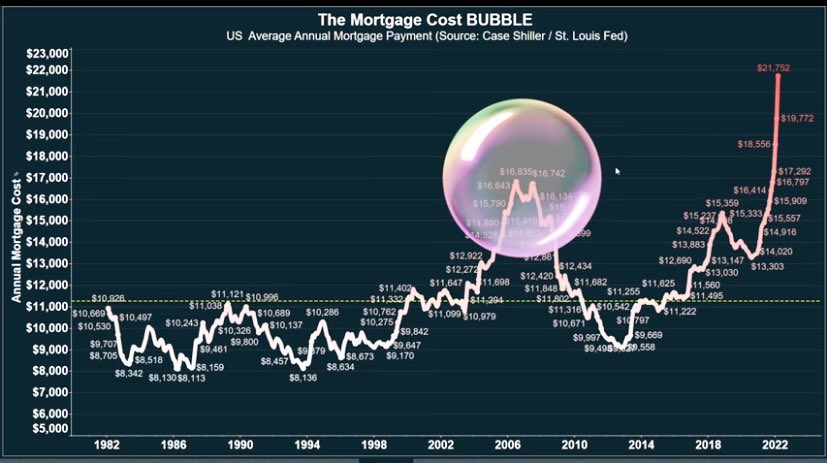

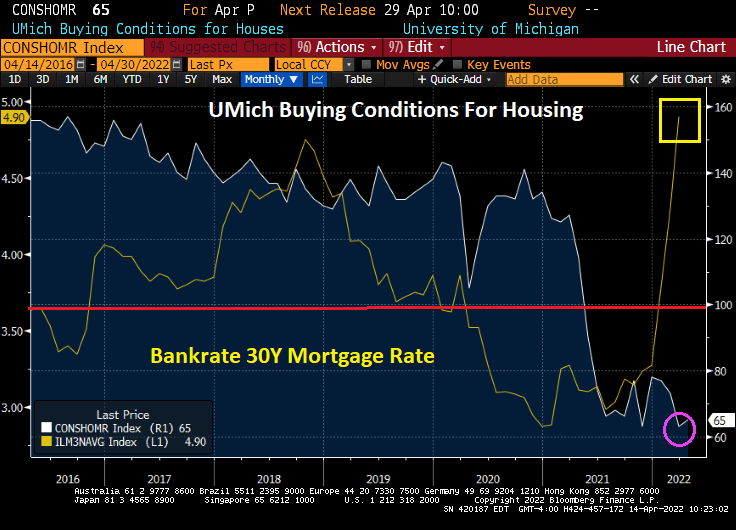

On the other hand, mortgage rates continue to soar on EXPECTATIONS of Fed rate hikes.

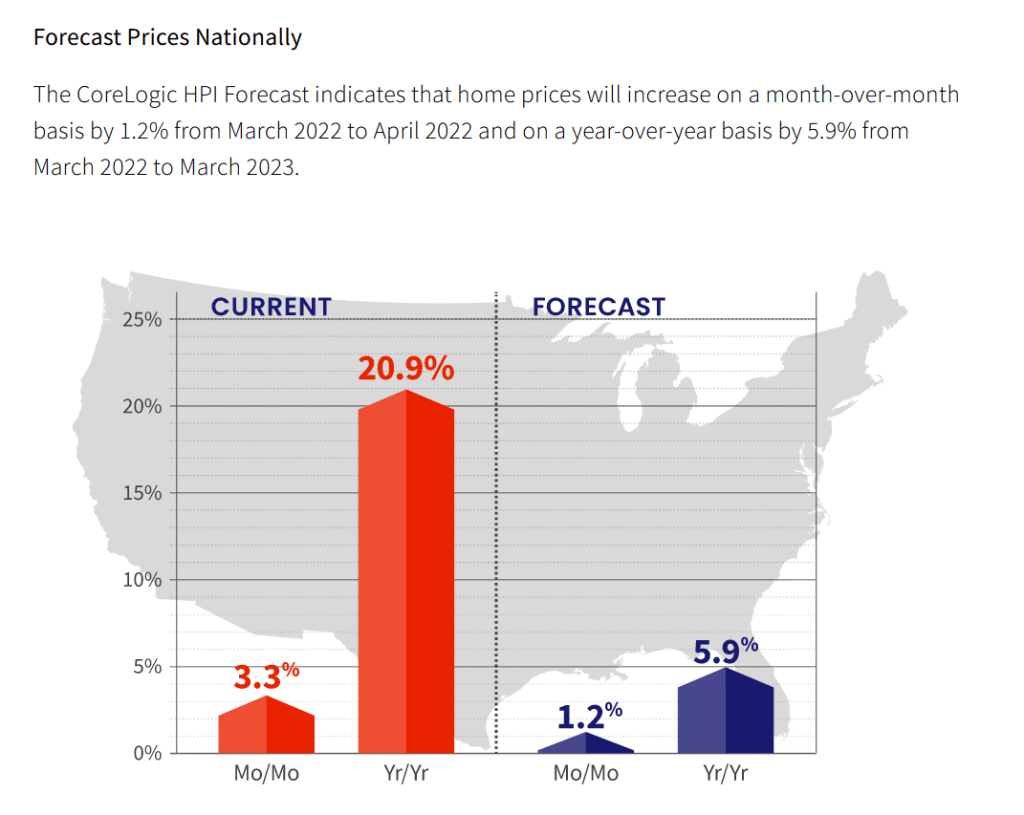

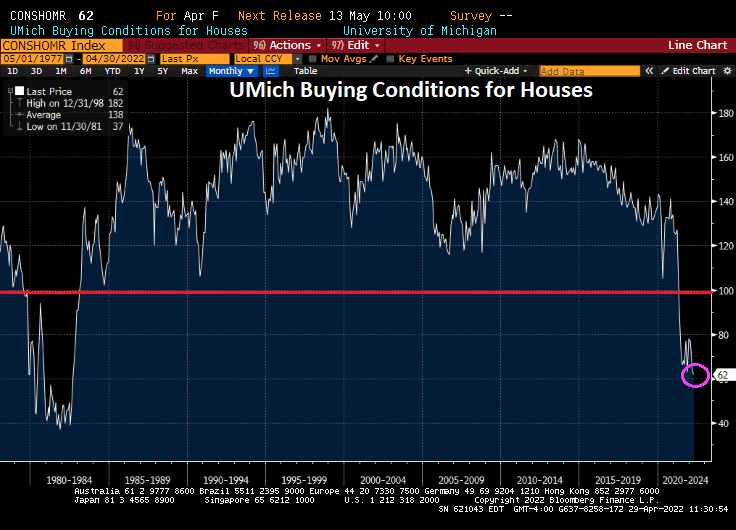

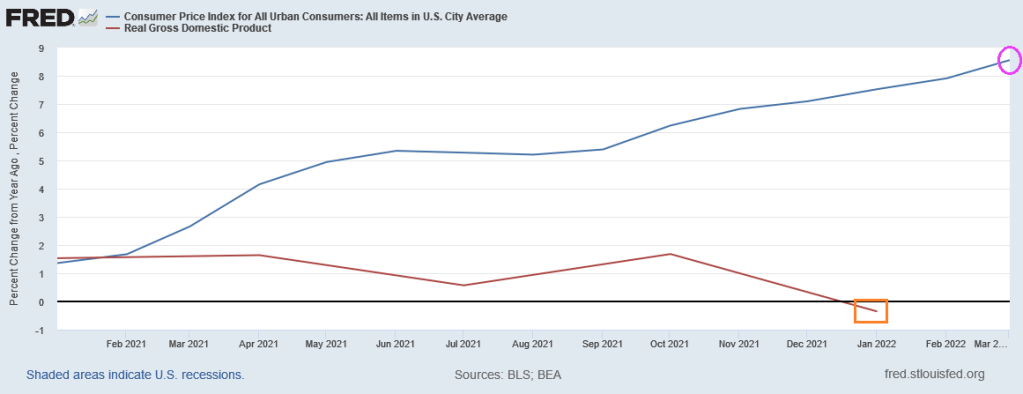

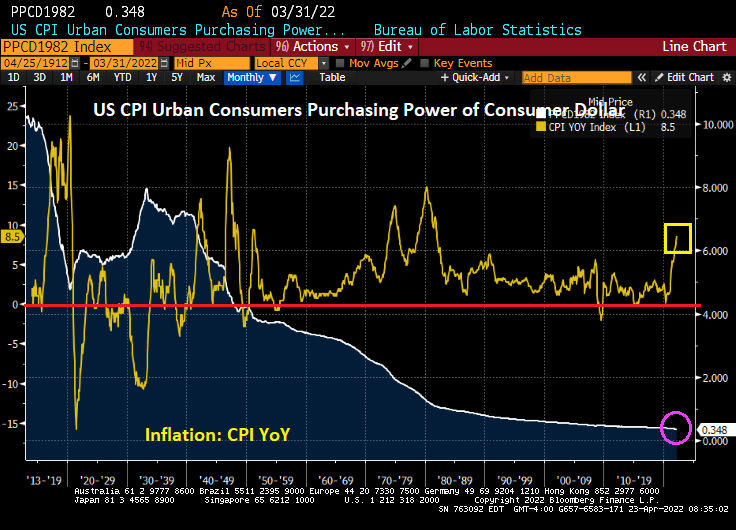

Meanwhile, CoreLogic revealed that March 2022 home prices were still sizzling at 20.9% YoY.

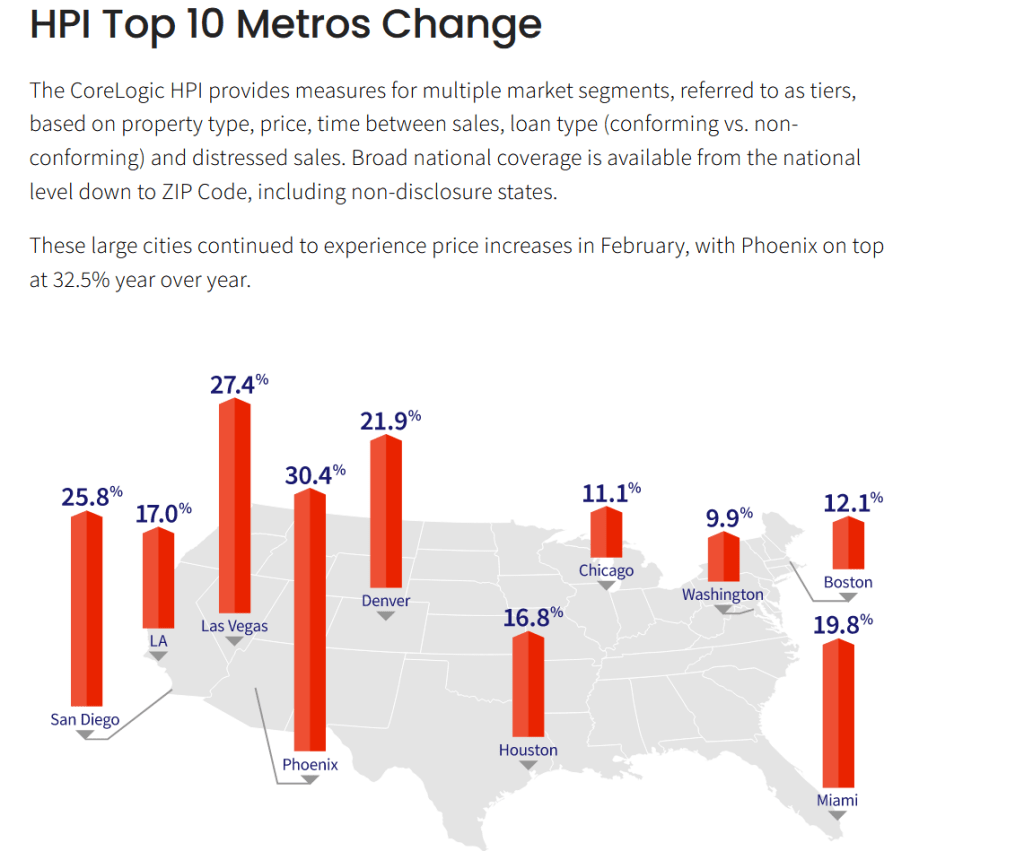

Phoenix AZ leads the top ten at 30.4% with Washington DC lagging at 9.9%.

So, its official. The Federal Reserve is best exemplified by former Yankee/Mets first baseman “Marvelous” Marv Throneberry. When players presented Mets’ manager Casey Stengel with a birthday cake but neglected to give piece of cake to Throneberry, Stengel replied to Throneberry when asked why no cake, “Because I was afraid your were going to drop it.”

Just like The Federal Reserve, the honorary Marv Throneberry of the the global economy.

Here is Marv’s baseball card from better days with the Yankees before they figured out that Marv was a terrible fielder. And strikeout quite a bit, like The Federal Reserve.

You must be logged in to post a comment.