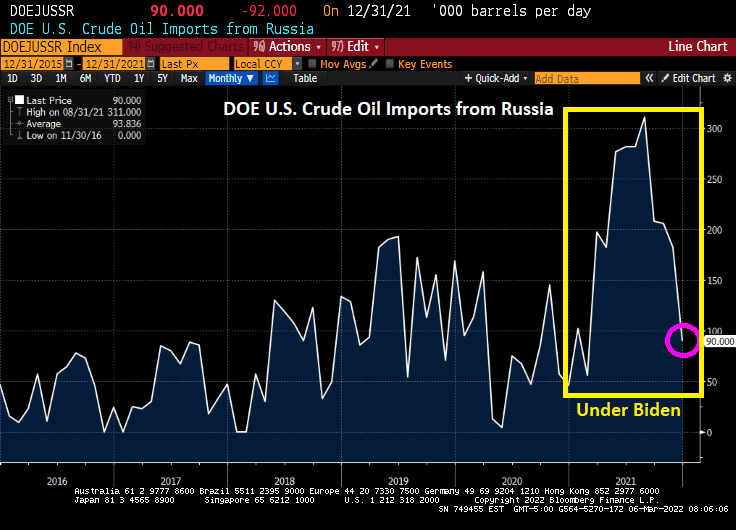

Russia is still engaged in its invasion of Ukraine. And the US continues to import crude oil from Russia. In fact, US crude oil imports from Russia soared under Biden only to decline again in December 2021.

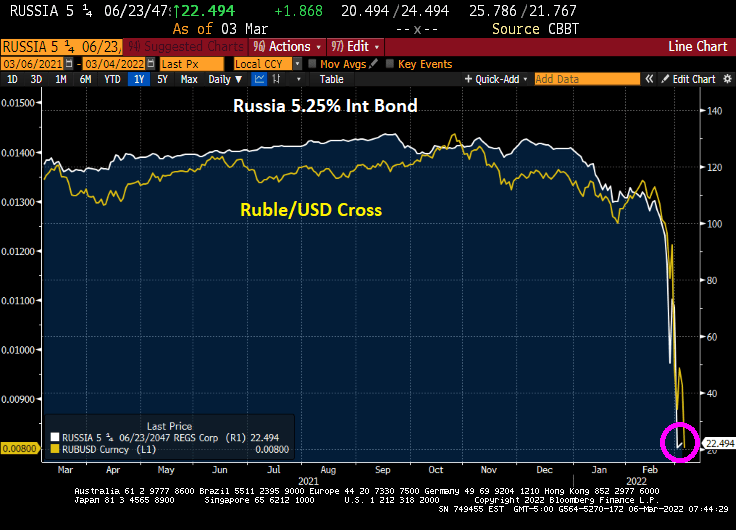

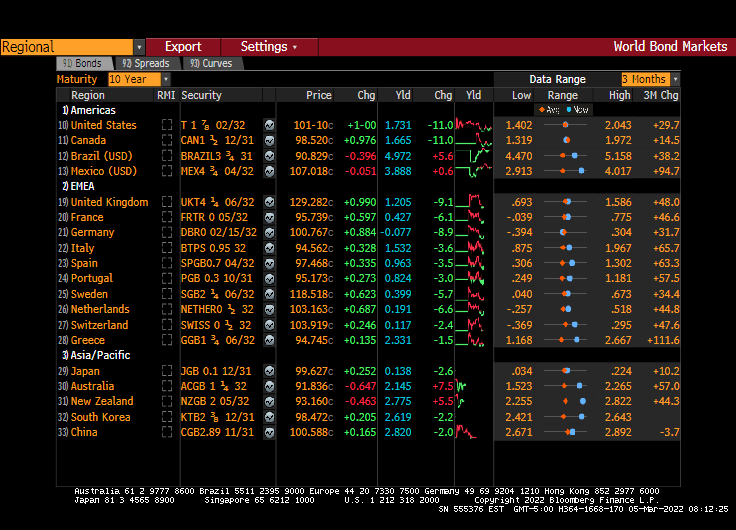

On the sovereign bond and currency front, the 5.25% coupon Russian international sovereign bond has crashed to 22.494. And the Ruble/USD cross has crashed as well.

Sberbank Bank 5 1/8% corporate bond has crashed to 25.

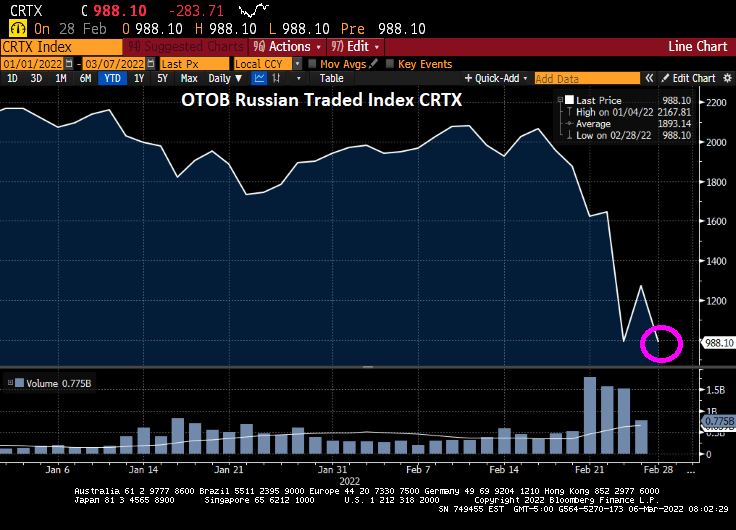

The Russian blue-chip stock market (OTOB Russian Traded Index CRTX) has crashed by over 50% since the invasion of Ukraine.

Fortunately, I like Cheerios for breakfast made from oats, since wheat futures are soaring.

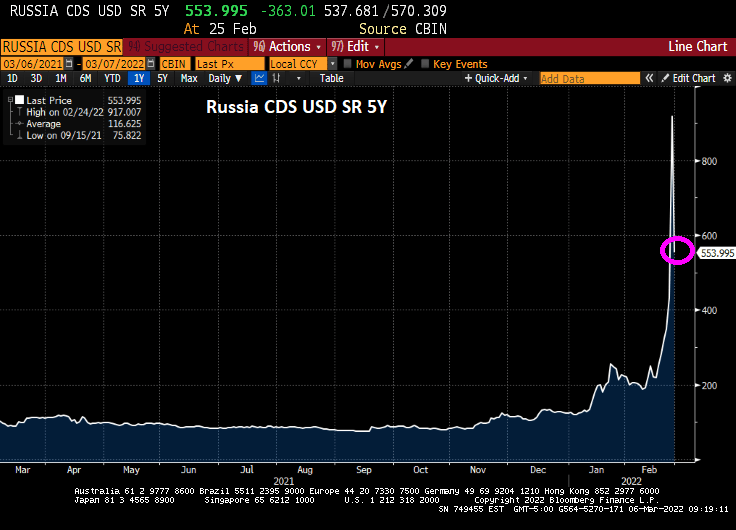

Russia’s Credit Default Swap (CDS) 5Y has dropped to a still-elevated 554.

The US really needs to ban Russian crude oil imports, since Biden’s failed in game theory by cutting US energy exploration on Federal lands and offshore drilling.

War is hell, as Vlad “The Ukrainian Impaler” Putin has demonstrated.

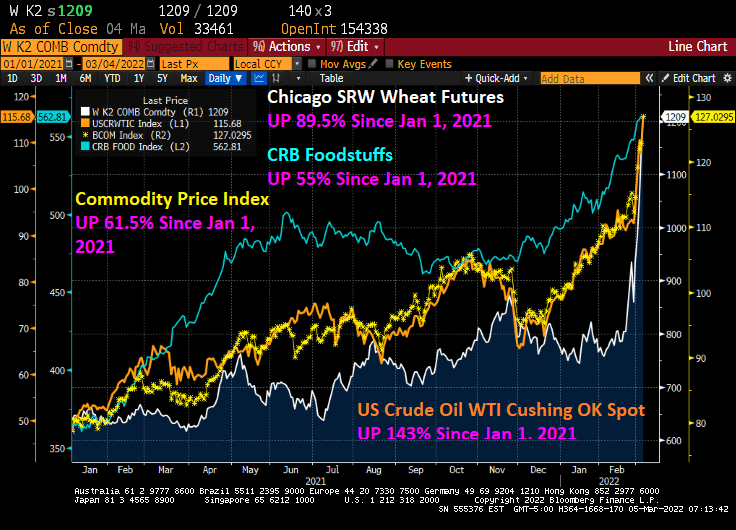

This has been a brutal week for consumers. With the Russia/Ukraine conflict raging and Congress seems determined to not allow for additional oil and gas production, and Biden’s anti-fossil fuel edicts still in place, we are seeing dramatic price increases in wheat (UP 89.5% since January 1, 2021), WTI Crude (UP 143% since January 1, 2021), and food stuffs (UP 55% since January 1, 2021).

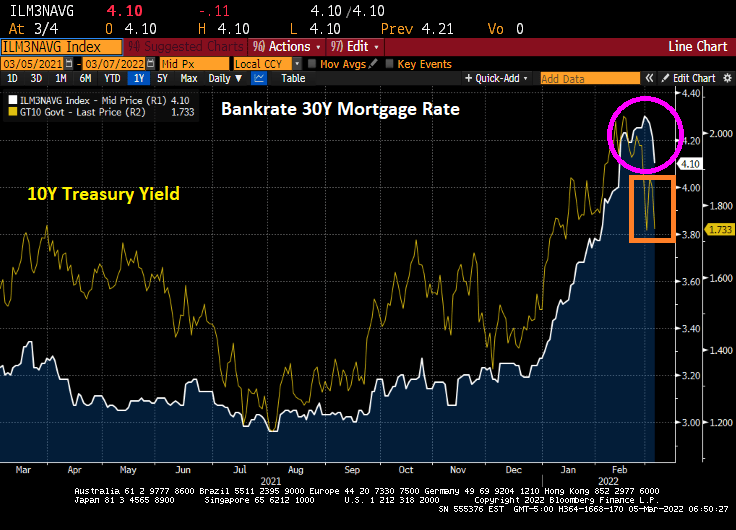

Bankrate’s 30-year mortgage rate has actually been falling the last several days, which is good for prospective home buyers as the 10-year US Treasury Note yield has been declining.

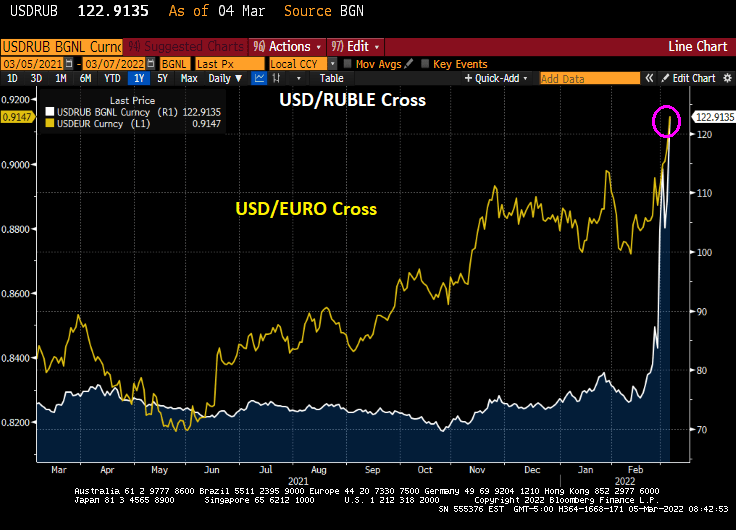

The USD/Russian Ruble cross is skyrocketing and the USD/Euro is doing likewise. Russians visiting the US will find that their trip is suddenly unaffordable (as do many American citizens will its rampant inflation). As Bruce Willis said in “Die Hard,” “Welcome to the party, pal.”

On Friday, the US Treasury 10-year yield declined 11 bps.

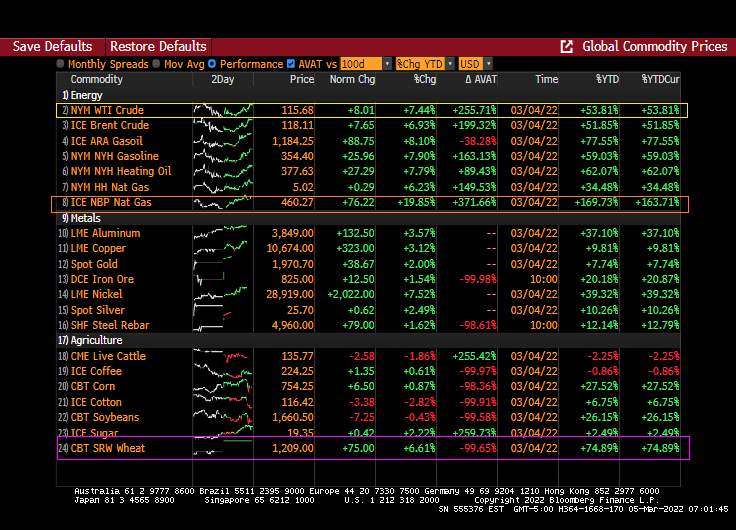

And energy prices continue to soar, particularly UK Natural Gas Futures that rose 19.85% overnight.

The US inflation data will be released on March 10th and the consensus is that February CPI inflation will rise to 7.9% YoY.

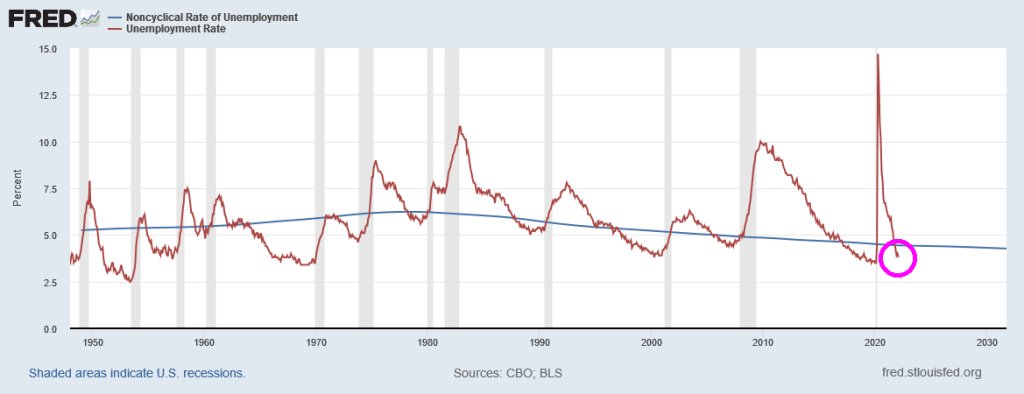

But even the latest unemployment rate report (3.8%) is signalling that The Fed should be raising interest rates since it is lower than the Natural Rate of Unemployment or NAIRU (4.44%).

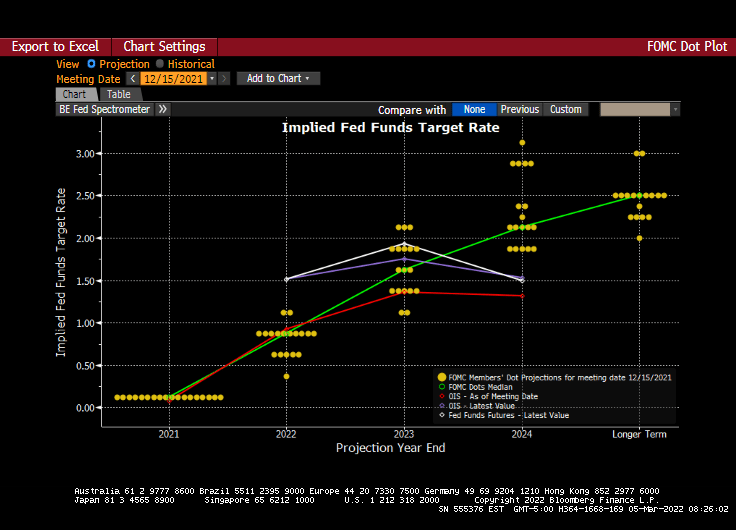

And we have the next Fed policy error on March 16th. The Fed dots plot looks like the glide slope for an aircraft, but the message is that rates will be going up at future meetings.

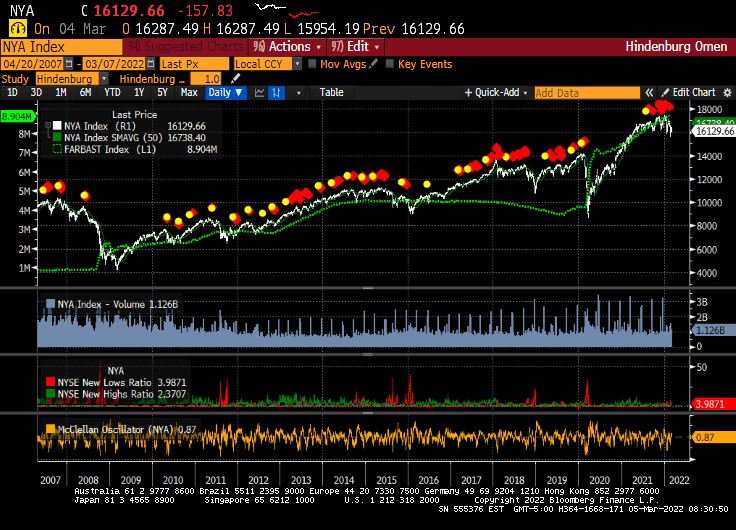

And just for amusement, I present to you the infamous Hindenburg Omen chart that forecast the 2008/2009 stock market correction. Since that correction, the Hindenburg Omen has been flashing “danger” but the only correction was the COVID-linked correction of early 2020. While the Hindenburg Omen is flashing red right now, The Federal Reserve’s balance sheet (green line) has protected against market corrections. Let’s see what happens if and when The Fed decides to remove the epic monetary stimulus.

Its anyone’s guess as to whether The Fed will actually tighten monetary policy.

Russia is still attacking Ukraine and I am still seeing stories about actor/comedian Bob Saget’s cause of death. So now for something completely different.

And this doesn’t include the inflation in prices caused by the Russian invasion of Ukraine. Yet.

US Personal Consumption Expenditures (PCE) price index rose by 5.2% in January, the fastest rate since mid-1983.

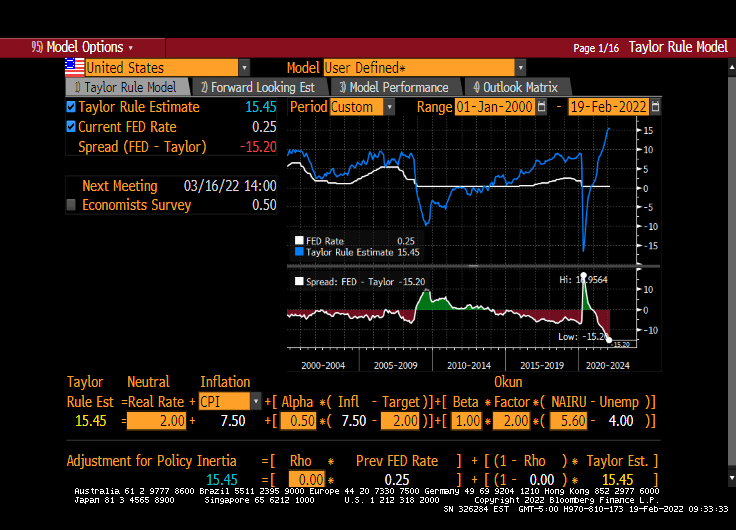

With CPI inflation at 7.5% YoY, the Taylor Rule suggests a Fed Funds target rate of 13.35%, higher than the current rate of 0.25%. Overstimulated much??

I admit, I follow market data to get a signal of what is happening to mortgage rates and I got one. With Putin and Russia invading Ukraine, markets are in turmoil

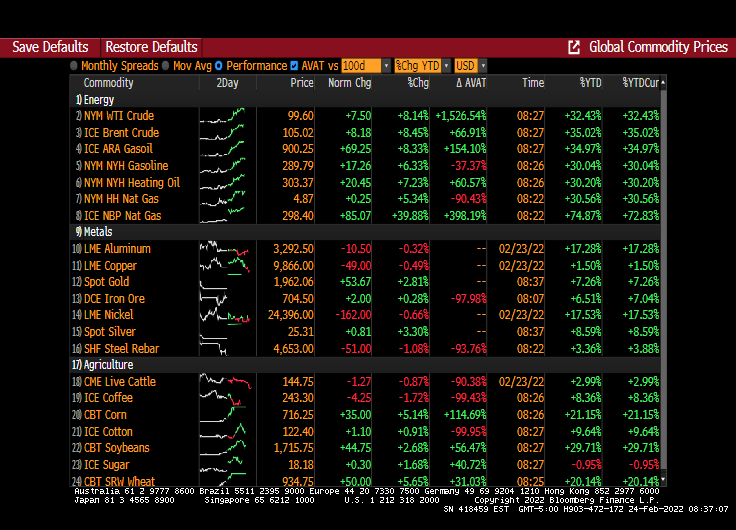

WTI Crude is up 8.14% this morning, Brent Crude is up 8.45% and NBP (UK) Natural gas is up 40%.

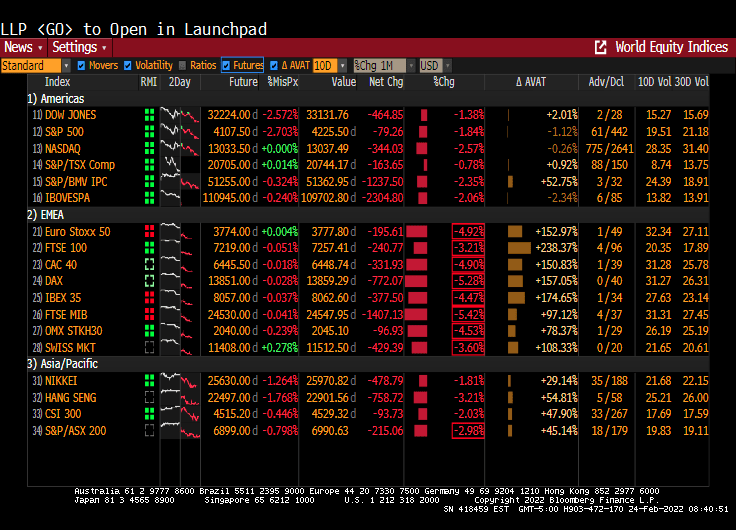

Europe is having a bad day equity market-wise. Eurostoxx 50 was down 4.92%. The US Dow is braced for a 2.5% opening.

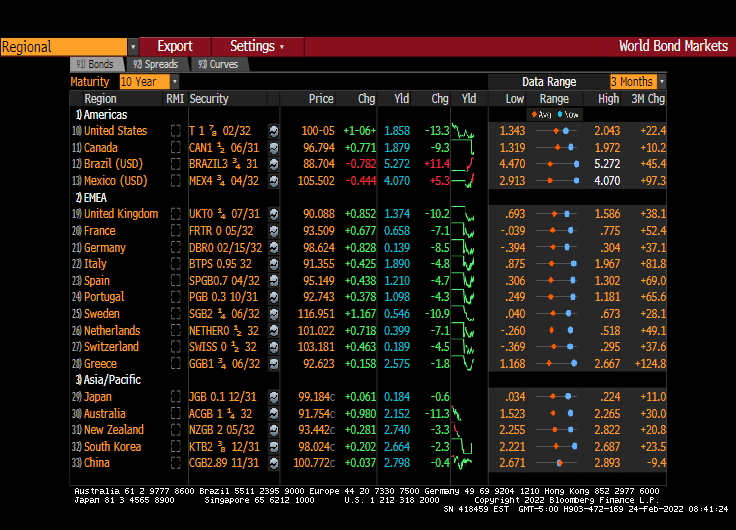

Now to bonds. The 10-year Treasury yield is down 13.3 bps this morning. Sweden and UK are down 10 bps as well.

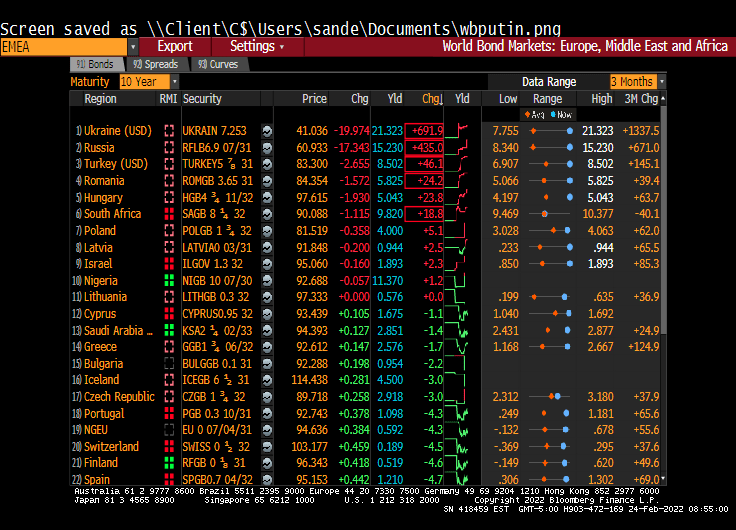

How about the new Russian front? Ukraine’s 10y yield rose 691.0 bps while Russia’s 10Y yield rose 435 bps.

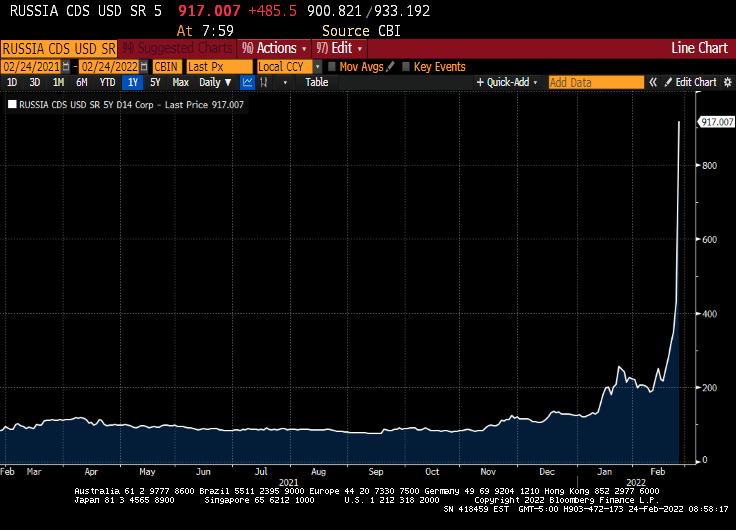

Russian 5Y Credit Default Swaps (CDS) leaped to a Greek-like 917.

Well, it looks like the sanctions imposed by Winken (US VP Harris), Blinken (US Secretary of State) and Nod (US President Biden because he always looks half-asleep) apparently didn’t work as intended.

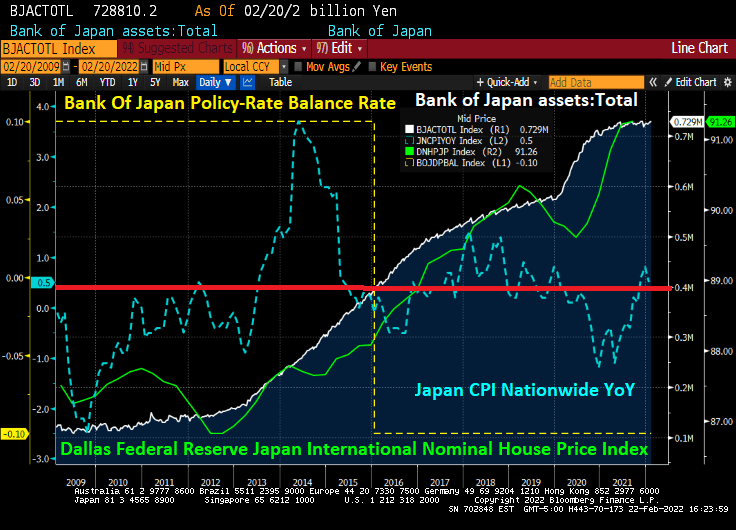

It’s taken nine years and the Bank of Japan supersizing its balance sheet to the $5 trillion mark, but Asia’s second-biggest economy finally has some inflation.

Officials in Tokyo are realizing the hard way, though, that it’s best to be careful what you wish for as bond yields spike.

Granted, the gains in consumer prices Japan is reporting are negligible compared to those in the U.S. and China. And inflation is still a good distance from the BOJ’s 2% target. Still, the 0.5% rise in consumer prices in January year-on-year is already unnerving the bond market. It followed a 0.8% jump in December and marks the fifth straight month of increases.

The worry is that Japan’s inflationis the “bad” kind. Haruhiko Kuroda was hired as BOJ governor in March 2013 to end deflation. Kuroda unleashed tidal waves of liquidity. That drove the yen down 30%, generated record corporate profits and sent Nikkei 225 Average stocks to 31-year highs.

Despite a staggering balance sheet with a -0.10 bps policy rate, Japan has only 0.5% inflation.

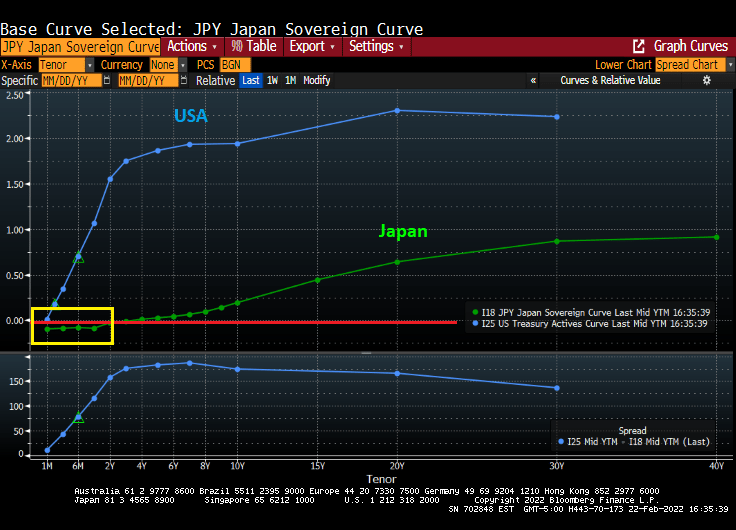

And Japan’s yield curve is negative at 3 year tenor and less.

How is it that Japan has virtually no inflation with negative rates but the USA has 7.5% inflation with a 0.25% target rate? Could it be the USA undertook massive fiscal spending related to COVID and reduced energy sources in an effort to go “green” that led to 7.5% inflation??

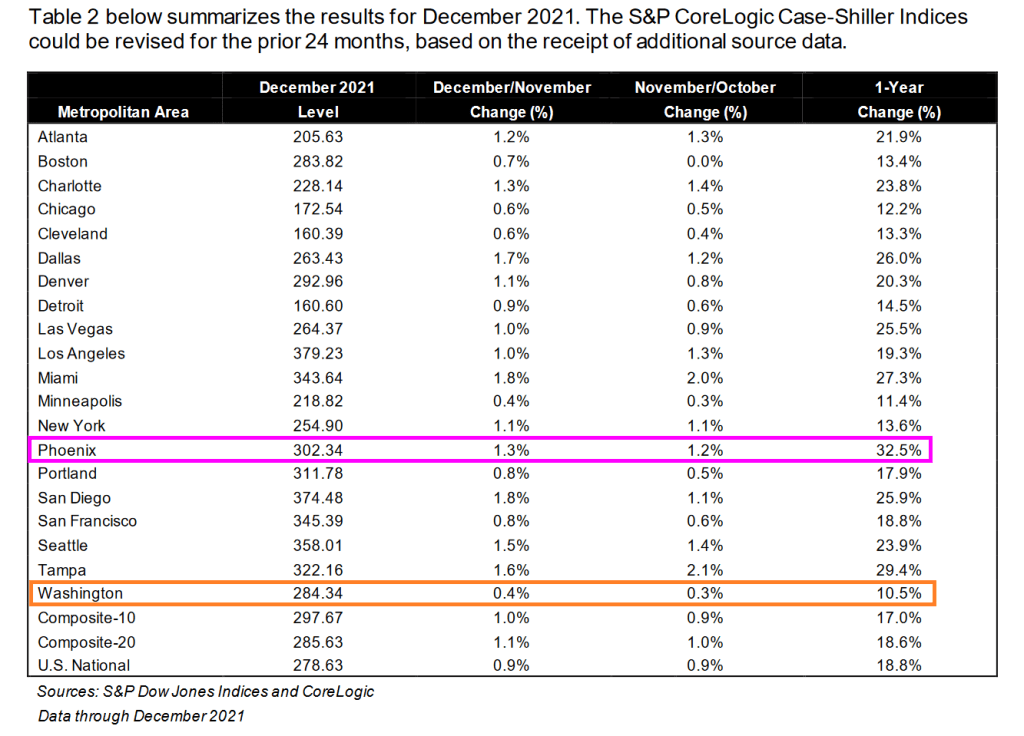

All 20 metro areas in the Case-Shiller 20 index grew at 10% or higher YoY with my former home city Phoenix leading the way at 32.5% YoY house price growth. Washington DC, aka Mordor on The Potomac, was in last place at 10.5% YoY.

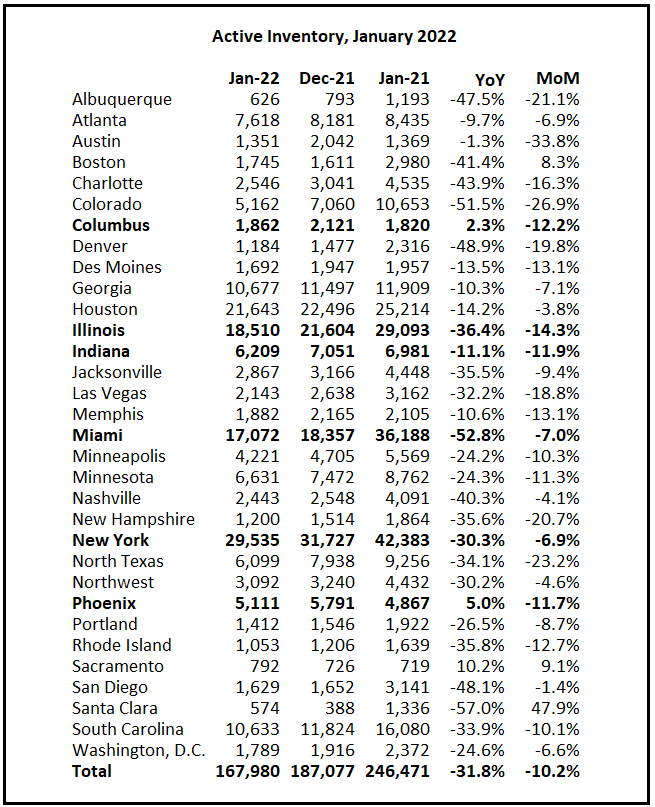

In terms of active inventory of housing, only Phoenix and Columbus Ohio are showing positive growth in active inventory YoY. But even Phoenix and Columbus saw a decline MoM (or month-over-month).

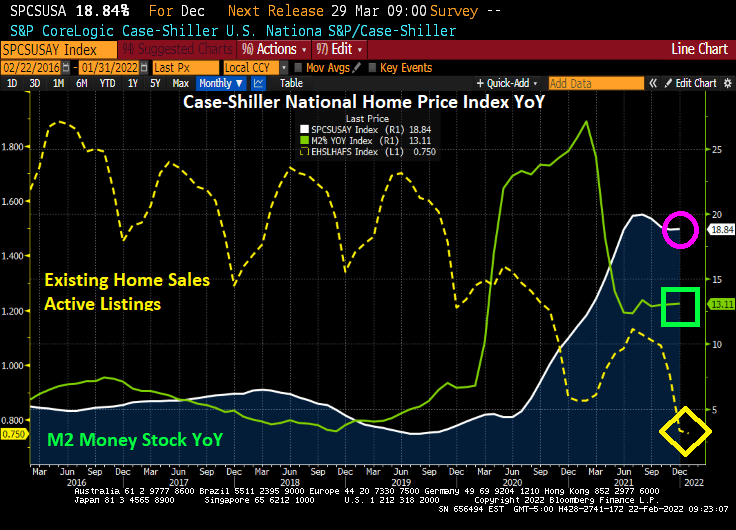

Including Existing Home Sales Active listings in the first chart, we see The Federal Reserve continuing to pump money at at 13.11% clip while active inventory is at an all-time low.

As US/Russian tensions grow over Ukraine, The Federal Reserve may be forced to postpone or reduce planned rate increases and balance sheet trimming.

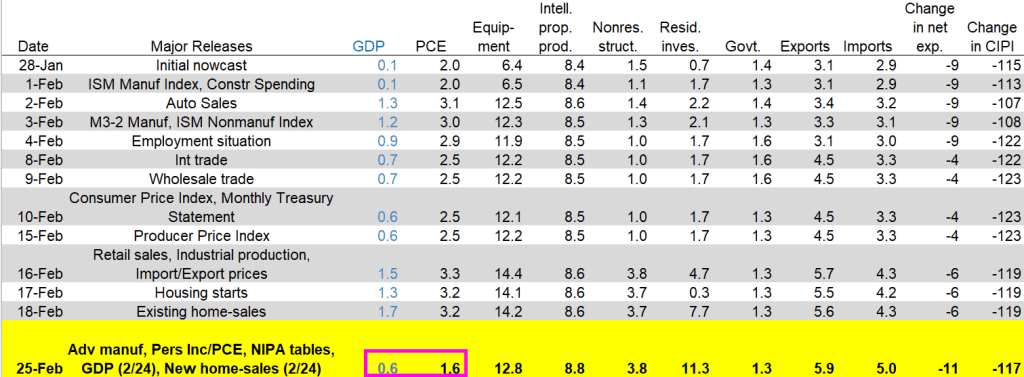

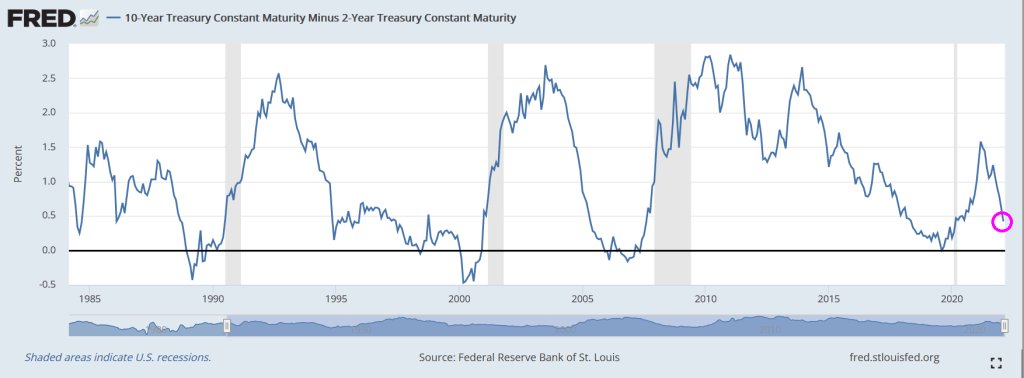

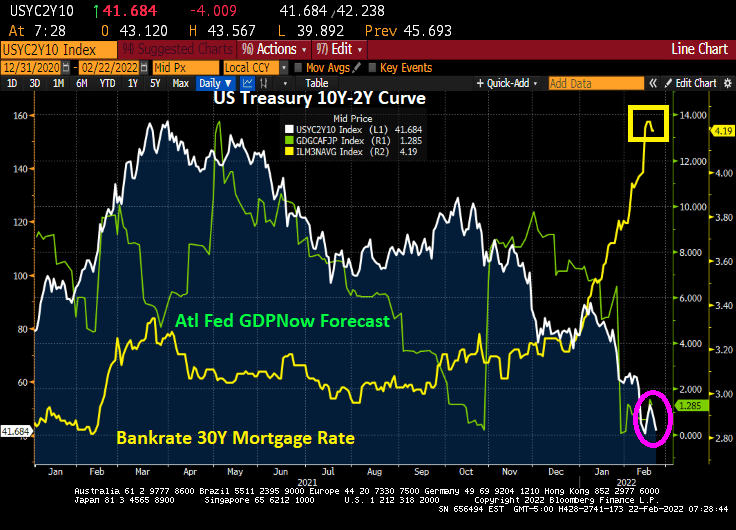

But in addition, we see US GDP slowing to near zero (1.285%) as the US Treasury 10Y-2Y yield curve has flattened to 41.684 BPS. The good news? Bankrate’s 30Y mortgage rate increases have slowed to 4.19%.

On a different note, I noticed the Chicago Bulls logo when turned upside-down looks like a space alien violating a crab.

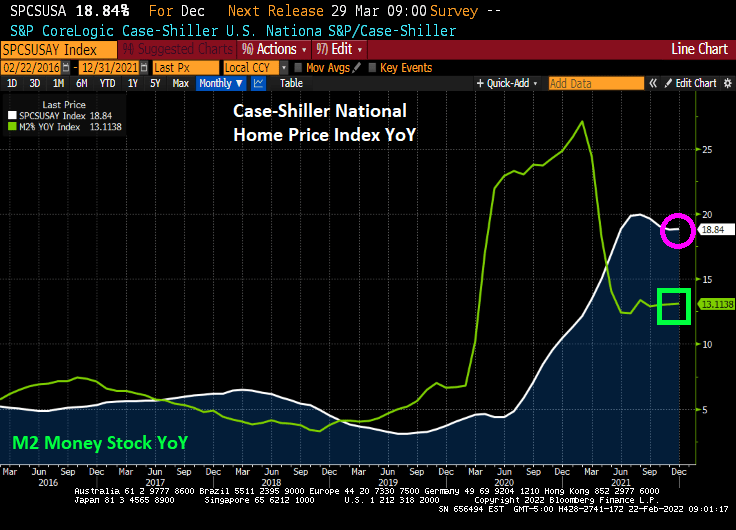

In January 2020, just prior to the COVID outbreak in the US, the Case-Shiller national home price index was growing at 4% YoY, the Zilliow rent index (all homes) was growing at 2.92% YoY and REAL average hourly earnings were growing at 0.52% YoY.

Then COVID struck and the Federal government dumped trillions of dollars of stimulus into the economy and The Federal Reserve massively expanded its balance sheet. Now the US has home prices growing at a 18.8% rate, rents (for those who can’t afford to purchase a home) growing at 14.91% and REAL hourly earnings growing at -1.80%.

The site Apartment List has an even bleaker view of rent growth, with rents in January 2022 having grown by 18% YoY.

Now that COVID is fading, we see New York City rents growing at 33.5% YoY followed by Florida and Arizona cities at 29.3% and higher rates. Irvine CA is seventh at 28%. The slowest growing city is Oakland, CA is growing at only 0.5%.

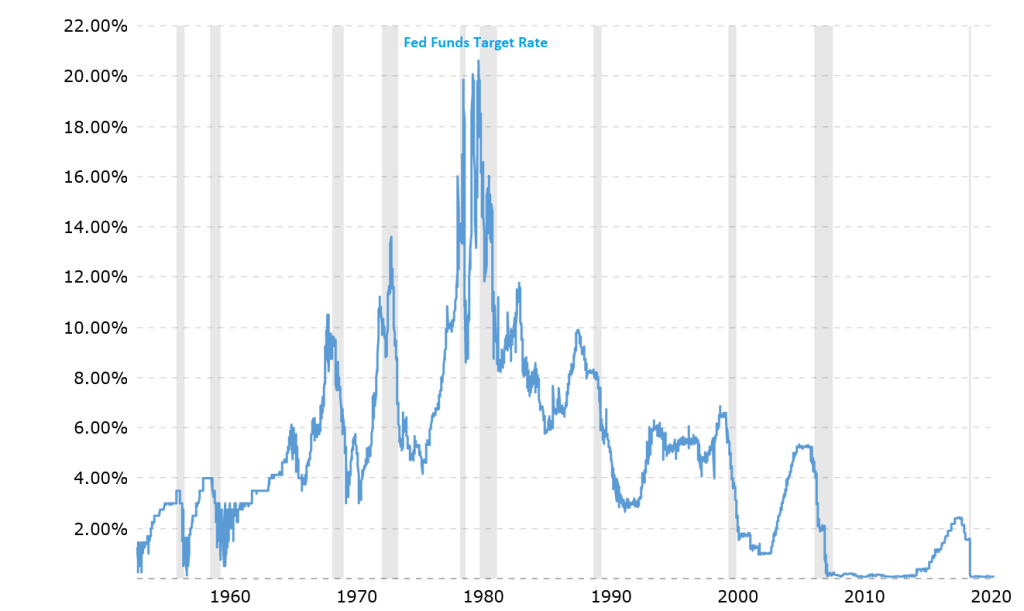

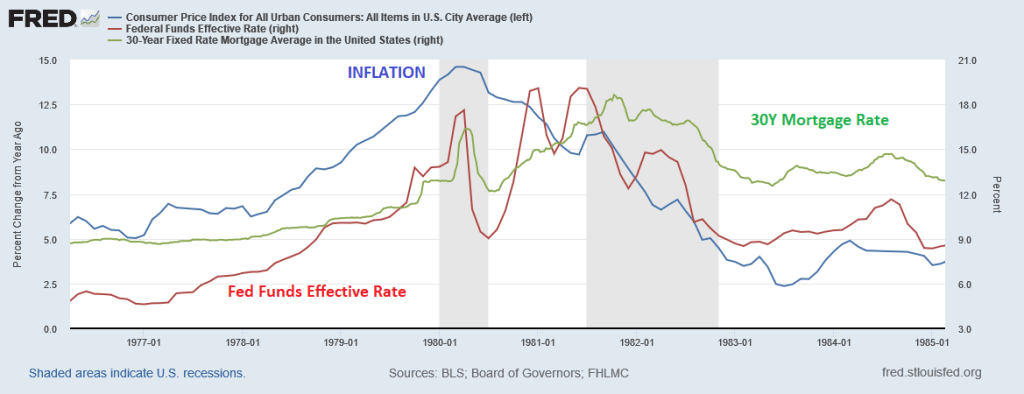

In August 1979, when Paul Volcker became chairman of the Federal Reserve Board, the annual average inflation rate in the United States was 11%. Inflation peaked in 1980 at 14.6%. Volcker raised the federal funds rate from 11.2% in 1979 to 20% in June of 1981.

Inflation (defined as CPI YoY) declined from over 14.6% in 1980 to 3.6% by 1985. But 30-year mortgage rates resumed their upward trajectory and peaking in October 1981 at 18.63 before beginning a gradual decline as inflation was tamed.

But will Powell enact another Volcker moment by raising the target rate abruptly?

The bank is joining others on Wall Street in ramping up bets for faster policy tightening, after U.S. consumer prices posted the biggest jump since 1982 in January. Goldman Sachs Group Inc. is forecasting seven hikes this year, up from its earlier prediction of five.

“We now look for the Fed to hike 25bp at each of the next nine meetings, with the policy rate approaching a neutral stance by early next year,” the JPMorgan team, led by chief economist Bruce Kasman, said in a research note.

January U.S. inflation readings “surprised materially to the upside,” the economists wrote. “We now no longer see deceleration from last quarter’s near-record pace.”

On inflation, the economists said a “feedback loop” may be taking hold between strong growth, cost pressures, and private sector behavior that will continue even as the intensity of current price pressures in the energy sector eventually fade.

Strong growth? 1.3% is strong growth??

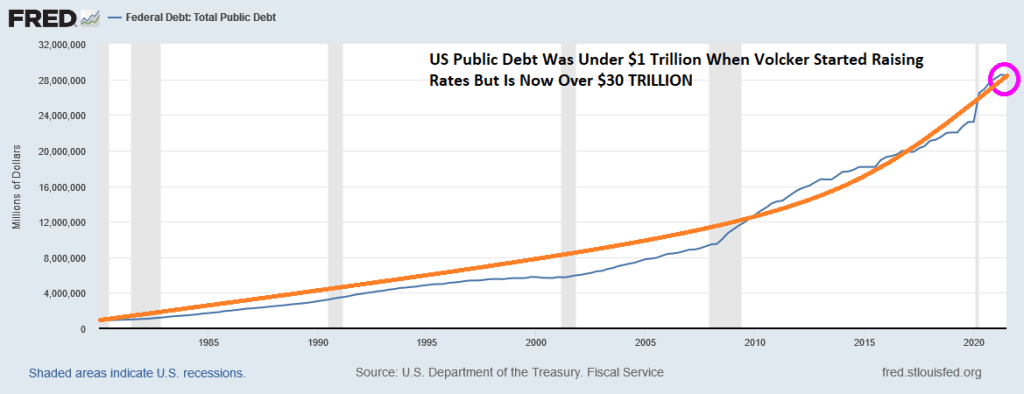

Be that as it may, the US economy is at a different place today than under President Jimmy Carter. When Volcker started raising The Fed Funds Target rate, US public debt was still under $1 trillion. It has ballooned to over $30 trillion today.

9 rate increases is above what is being priced in The Fed Funds FUTURES market which is 6 rate increases over the coming year.

With 7.5% inflation, the Taylor Rule suggests a target rate of 15.45%. Talk about “Shock and Awful!”

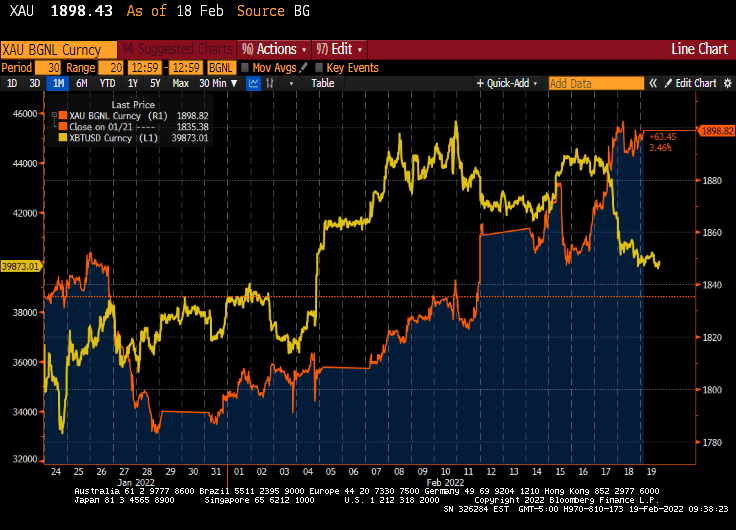

We are starting to see GOLD (gold) surging and Bitcoin (yellow) falling as The Fed prepares “shock and awful” rate hikes and Biden continues to beat the war drums over Russia invading Ukraine.

If The Fed actually raises rates 9 times and dramatically pares back its massive monetary stimulus, it will be “shock and awful.”

You must be logged in to post a comment.