Has anyone considered the impact of Biden/Mayorkas’s open southern border with Mexico? Other than the crime, stress on existing services like healthcare, schools and Social Security. But where will the 8 million illegal immigrants reside? Well. the Biden Administration has an answer: throw money at it! This time, $45 billion to convert empty office space to homes. Not just for illegals, but for anyone.

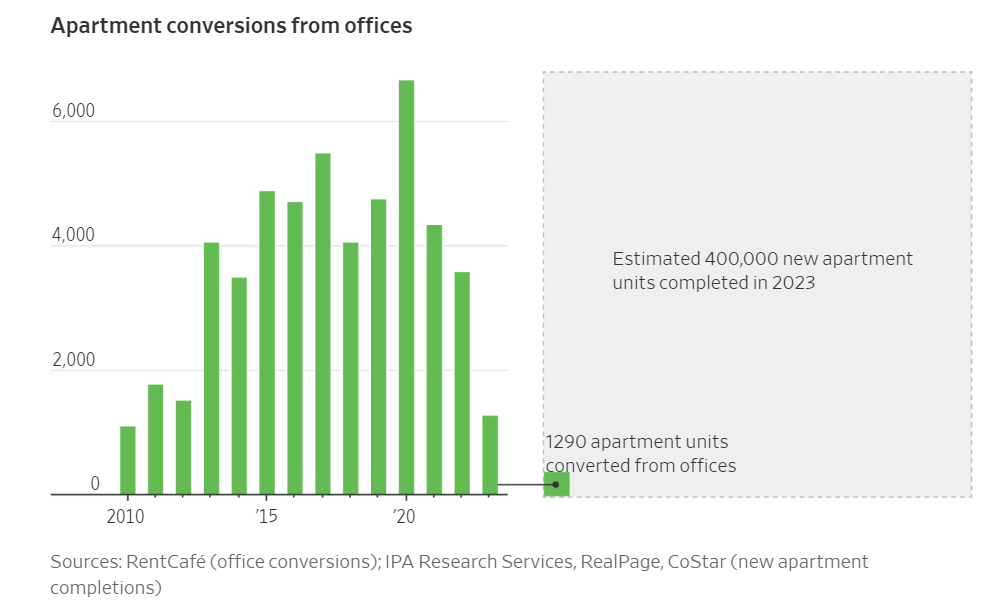

Only 3,575 apartment units were converted from office space last year. The already fraught process now faces even more challenges.

The Wall Street Journal explains why in its report Turning Empty Offices Into Apartments Is Getting Even Harder

Cities hoping to convert emptying office buildings into apartments are running into financing issues, stagnating rental markets and other challenges that are bottling up their efforts.

Developers last year created just 3,575 apartment units in the U.S. through office conversions, according to an analysis by rental listing site RentCafe. That amounts to less than 1% of all apartments built that year through new construction.

Federal and local governments are also trying to give conversions a boost. The White House said last month that it was updating guidance for existing grants and spending programs to make billions in federal dollars available for these projects. It also said it would seek the conversion of more government-owned properties into housing.

Some cities, such as Washington, D.C., New York and San Francisco, are also taking steps to encourage more conversions. Tax incentives and faster approvals are “rocket fuel” for these projects, said Sheila Botting, a principal at commercial property brokerage Avison Young.

Even so, the process has always been fraught with difficulty and few office buildings are natural candidates. Conversions are easiest in older, lower-quality and mostly empty buildings with small floors. But less than 1% of office space in the biggest U.S. cities ticks those boxes, according to Avison Young.

In significant ways, the conversion process is getting even harder now. Slowing rent growth might make apartment conversions less attractive to investors, if the trend persists into next year. Asking rents for apartments have fallen 1.2% nationally over the past 12 months, according to rentals website Apartment List.

Projects Not Economical

Without massive subsidies these projects are not economically feasible. Many aren’t even with massive subsidies.

In downtown Dallas, developer Wolfe Investments seeks to convert an 18-story, 1950s office tower into residential apartments, but has recently been fighting off foreclosure from its lender, Thistle Creek Partners, court records show.

Developers of One Camelback, a 200,000-square-foot office building in central Phoenix, are trying to convert it into what would be one of the city’s most expensive rental-apartment properties. A website advertises $8,000-a-month apartments, with floor-to-ceiling windows and crystal-clear views of nearby mountains.

But the developers, Sagamore Capital and partners defaulted on a loan of about $70 million. The project’s lender, Delphi Financial Group, has moved to foreclose. An auction of One Camelback is set for later this month, according to documents filed in Maricopa County, Ariz.

Biden Throws $45 Billion in Federal Funds to Convert Offices into Homes

On October 29, Mish (Mike Shedlock) commented Biden Throws $45 Billion in Federal Funds to Convert Offices into Homes

Questions abound. Assume you can convert offices into homes, who wants to live in them? Is a tear down cheaper?

The government has 1,500 office buildings nationally and leases on almost 200 million square feet of additional space that it does not need. Instead of canceling leases and selling the real estate, it’s going to convert them into clean energy spaces.

With enough subsidies, developers will try nearly anything. Then when the projects fail, the developers ask for more money.

How is this Being Paid For?

Taxpayers of course. But Biden is funneling $45 billion from clean energy incentives in the ridiculously named Inflation Reduction Act (IRA) into housing conversions.

You might also be wondering what this has to do with clean energy, and the answer is nothing. The questions keep piling up and I have answers.

What’s Really Going On Here?

Biden is hoping to spread the IRA dollars around to buy more votes.

But to do so, he is taking money away from his other pet projects to fund the idea of the moment. His idea of the moment is to do something about the price of rent.

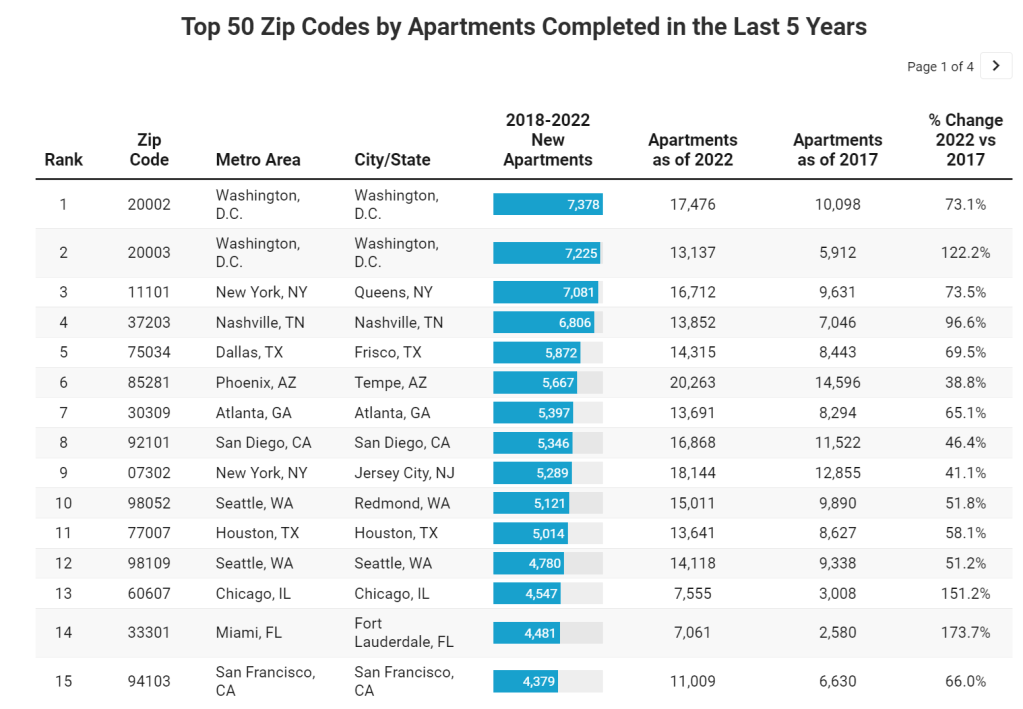

According to RentCafe, Washington DC had two zip codes that led the nation in apartments completed in the last five years (up to 2022).

Why is the private sector doing so few conversions? THAT is the right question. The answer? Office-to-housing conversion is hard and the demand may not be there. But with 8 million illegal immigrants having crossed the border, Biden has to do something. So Biden steps in with $45 billion to convert empty office space to homes. And I have to ask: is this a shadow wealth transfer to large Democrat-controlled cities as an apology for the havoc caused by Biden/Mayorkas open border policy?? Just asking!

So if an idea is really bad and won’t work, like solar power in areas with limited/spotty sunlight or wind turbines in areas with little/sporadic wind, Federal and State governments are always on stand-by to do something really stupid. Like rent control, which creates even worse distortions.

You must be logged in to post a comment.