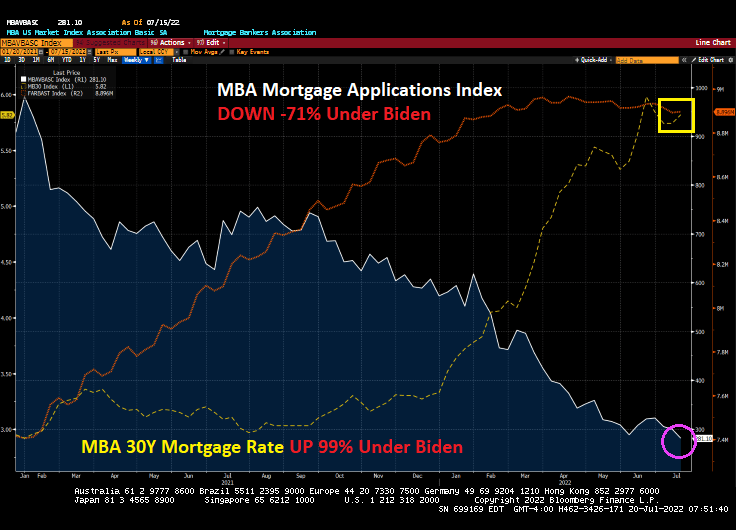

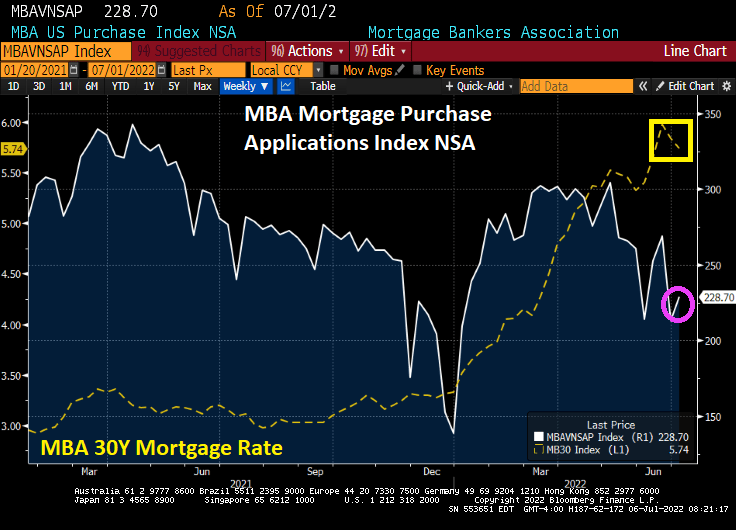

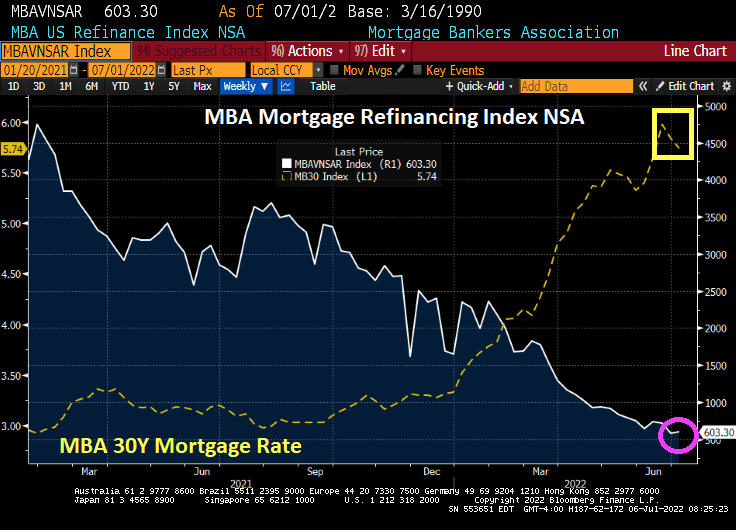

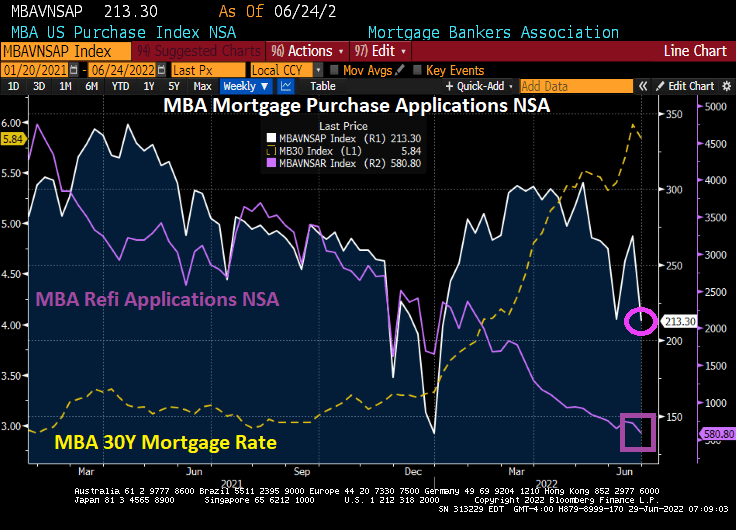

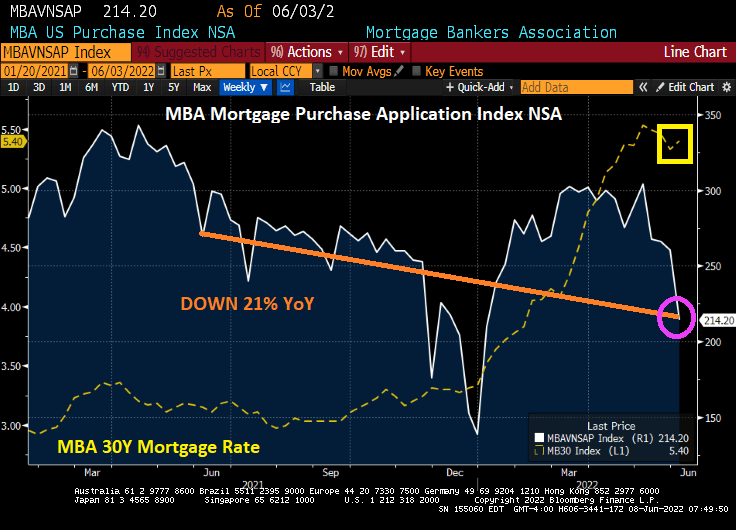

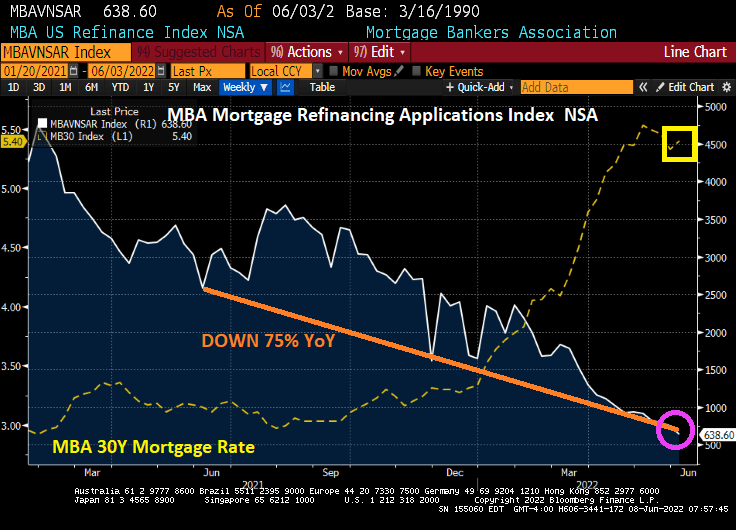

Mortgage application volume dropped and remained at a multi-decade low last week (back to 1997), led by an 8 percent decline in refinance applications, which now make up only 30 percent of all applications. Purchase applications have declined in eight of the last nine weeks, as demand continues to shrink due to higher rates and a weaker economic outlook.

Mortgage applications decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 26, 2022.

The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 23 percent lower than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 83 percent lower than the same week one year ago.

Just wait for The Federal Reserve to start unwinding its enormous balance sheet!

Unfortunately, Powell and Company don’t have a …

You must be logged in to post a comment.