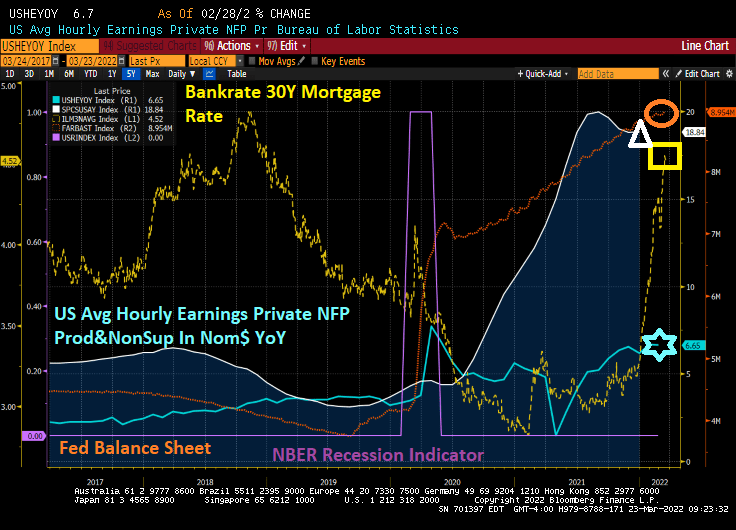

US mortgage rates are soaring, US home prices are soaring, The Fed’s balance sheet is still growing, and US average hourly earnings are growing at a fraction of home price growth.

The unafforable nature of US housing prices is similar to that of 2005-2007 when home price growth greatly exceeded wage growth.

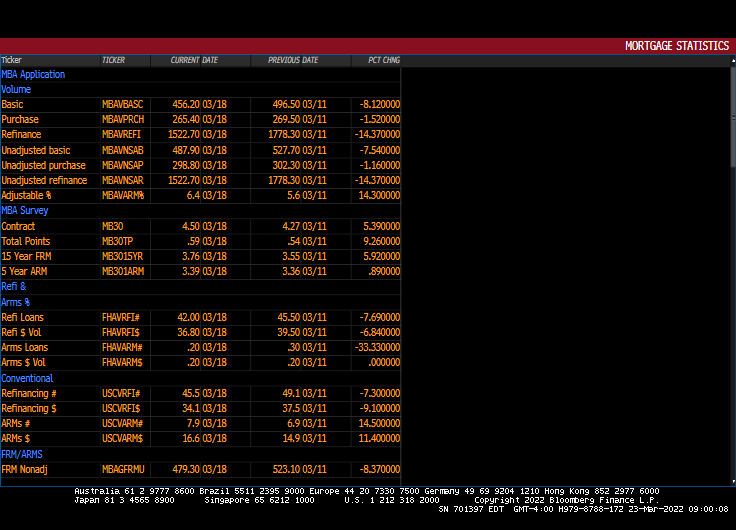

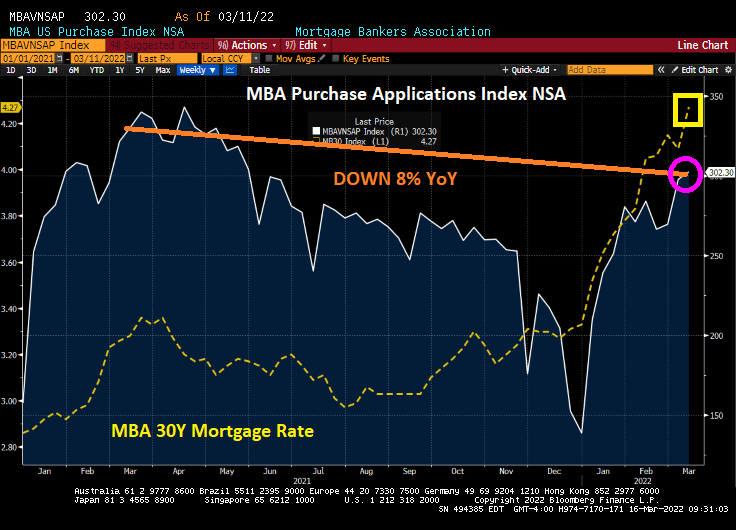

Another side effect of soaring mortgage rates: MBA refinancing applications plunged 14.37% from the preceding week.

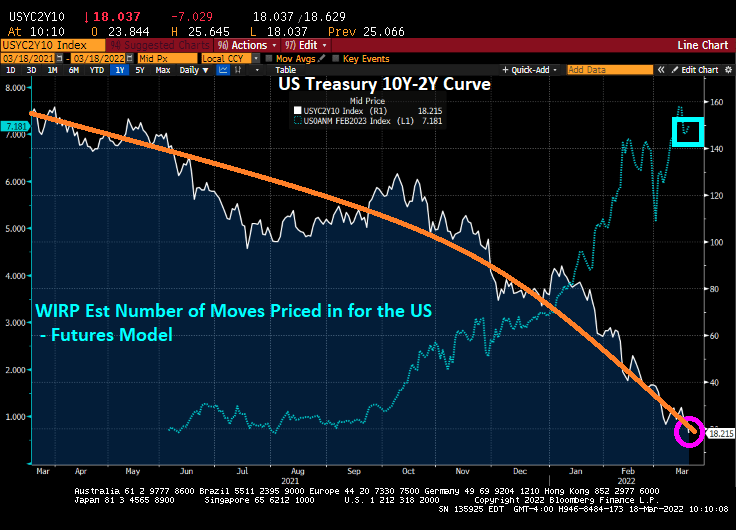

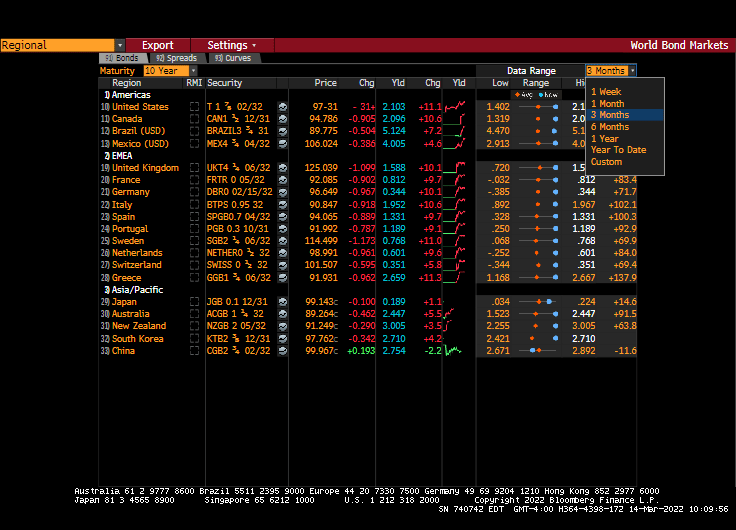

The US Treasury yield curve (10Y-2Y) is rapidly approaching inversion at 20.5 bps (where the 10-year yield is lower than the 2-year yield). But the 10Y-3M curve is generally steepening at 173.33 bps.

Of course, the driving force behind the flattening of the 10Y-2Y curve is the rapidly rising 2-year Treasury yield (orange line). The last time the 10Y-2Y curve inverted was in 2019, prior to the COVID outbreak in early 2020.

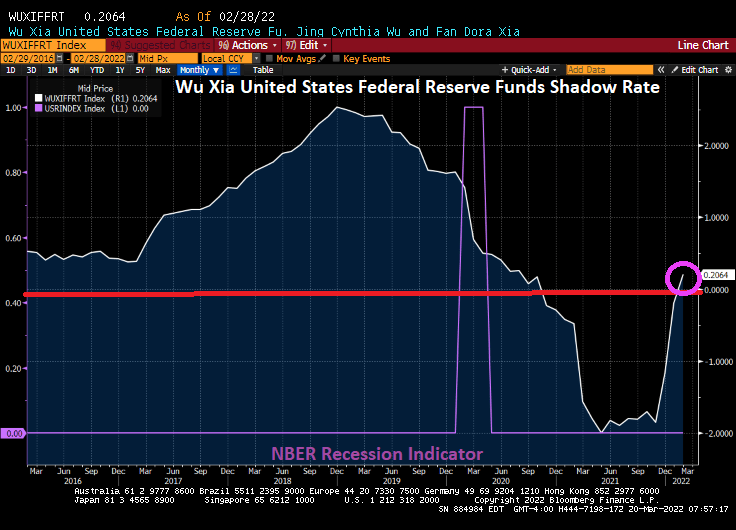

The Wu Xia United States Federal Reserve Funds Shadow Rate has finally climbed back into positive territory.

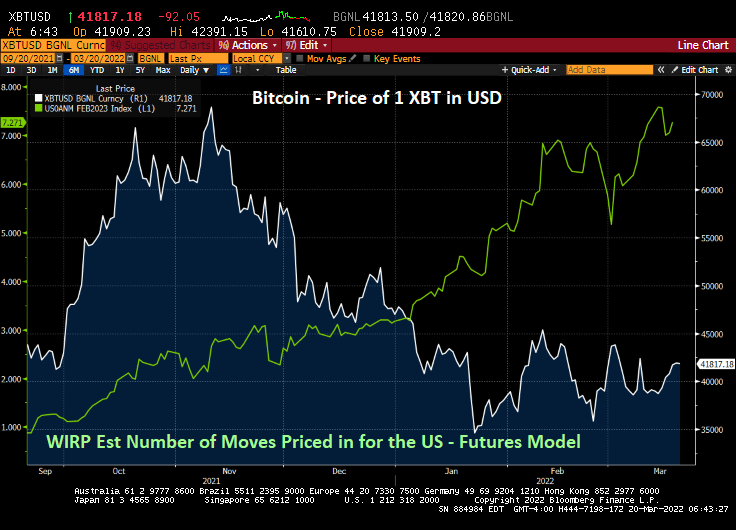

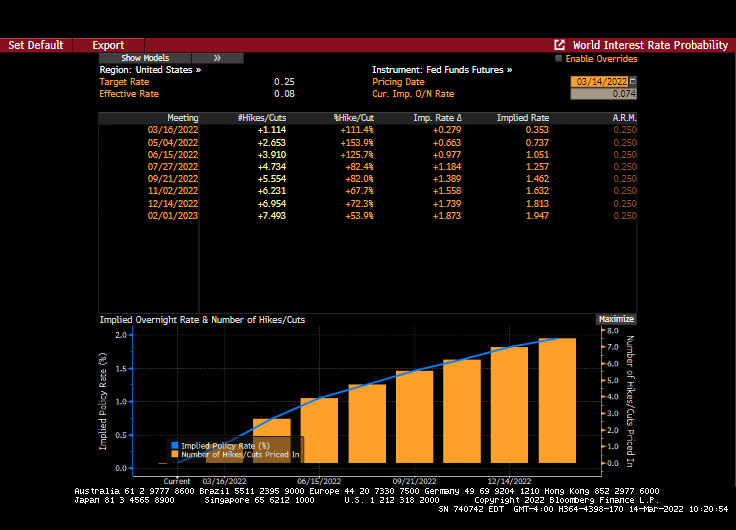

At last look, The Federal Reserve is forecast to raise their target rate 7 times over the coming year. And with the increasing forecast of rate hikes, we are seeing the cryptocurrency Bitcoin fall from near $70,000 to $41,817.

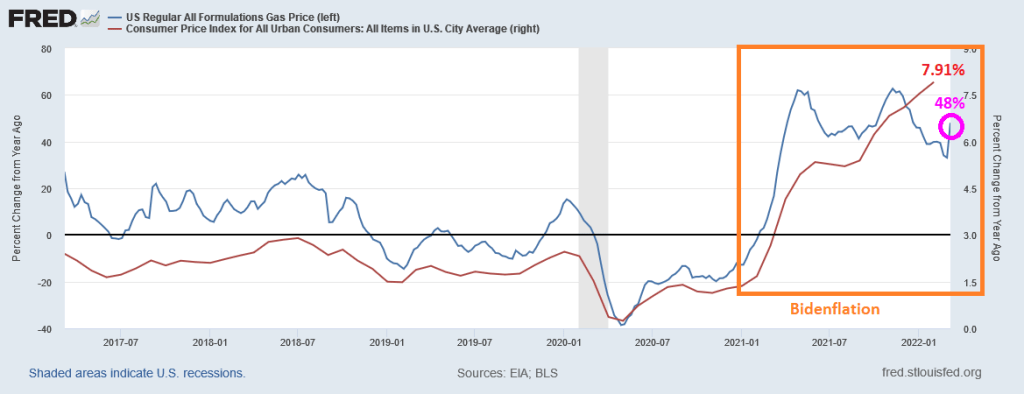

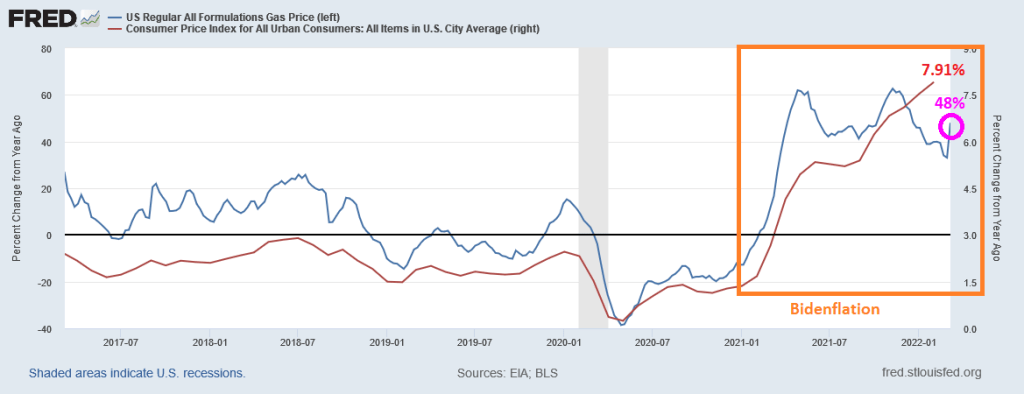

President Biden announced that he will be issuing an executive order to combat rising energy prices (the rising energy prices that he caused in the first place with … executive orders). Let’s see what happens next.

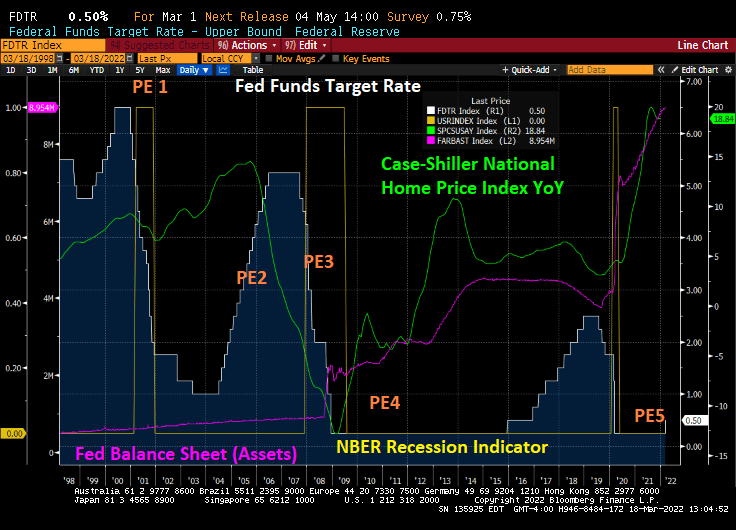

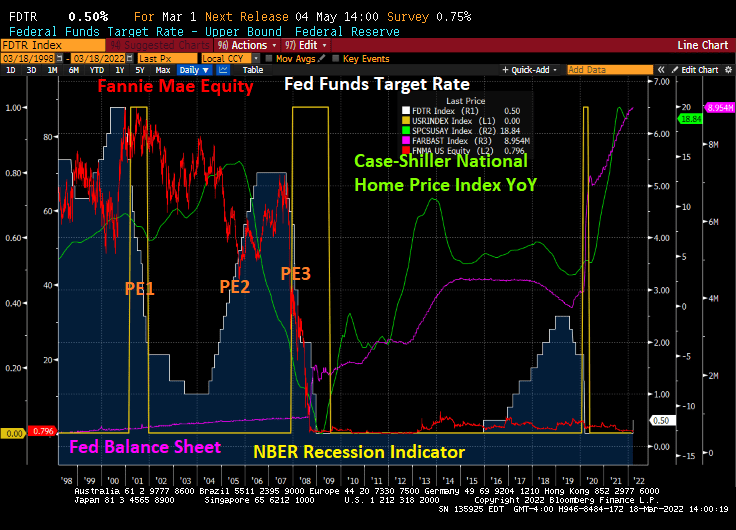

The Federal Reserve is not mentioned in the movies “The Big Short” or “Margin Call”, but The Fed’s policy errors played a big role in the demise of Fannie Mae’s and Freddie Mac’s equity prices.

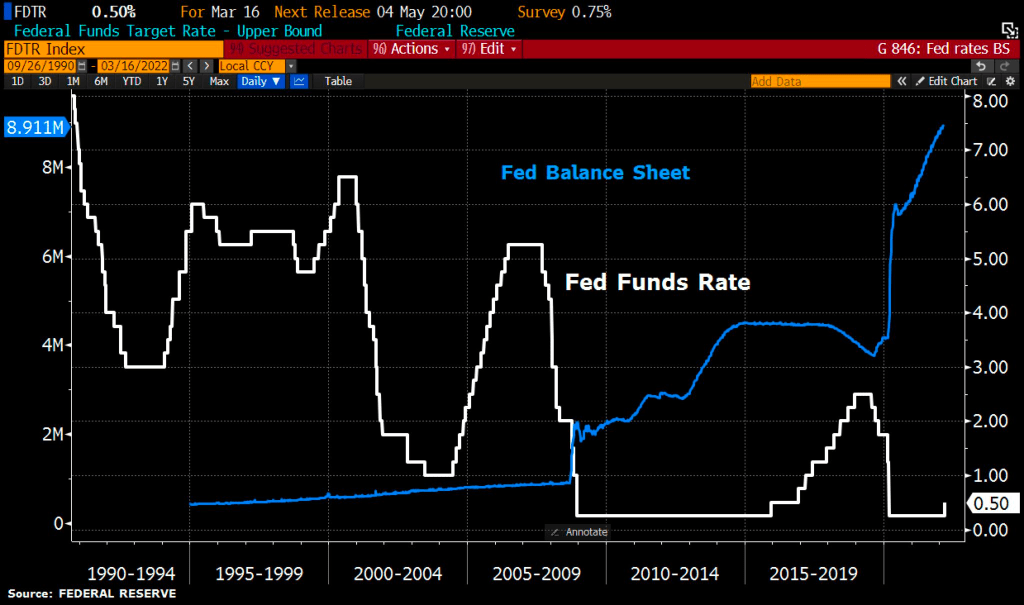

Here is a chart of The Fed’s many policies errors. Let’s start with The Fed lowering rates too fast around the 2001 recession. They pushed their target rate from 6.5% in December 2000 down to 1.75% after one year and then down to 1% (PE1). As home price growth accelerated, The Fed engaged in their second policy error — raising rates too fast resulting in a dramatic cooling of home price growth. Then came Policy Error 3: the dropping of The Fed Funds Target rate from 5.25% in September 2007 to an eventual 0.25% in December 2008.

With the election of President Obama, The Fed engaged in Policy Error 4: keeping The Fed Funds Target rate too low for too long, combined with their massive asset purchase programs (QE).

Finally, The Fed (under Yellen) finally raised The Fed’s target rate ONCE under Obama, but started raising rates once Trump was elected. The Fed also slowed their QE under Trump which as called “Fed policy NORMALIZATION.” Then COVID struck and The Fed engaged in Policy Error 5: keeping rates too low for too long … again while massively expanding their balance sheet.

Fannie Mae and Freddie Mac, the DC mortgage giants were done in by The Fed’s whipsaw Policy Error machine.

Now we are embarking on PE 5: Powell and The Fed Gang not raising rates but signalling that they will. Like the play “Waiting for Godot.”

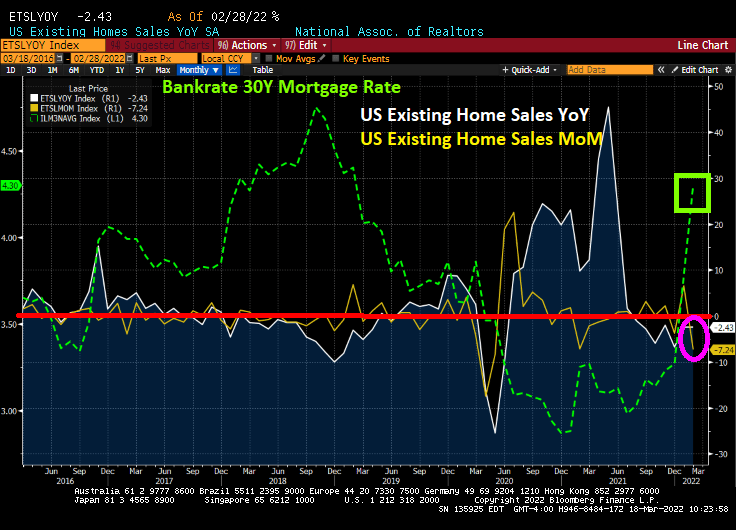

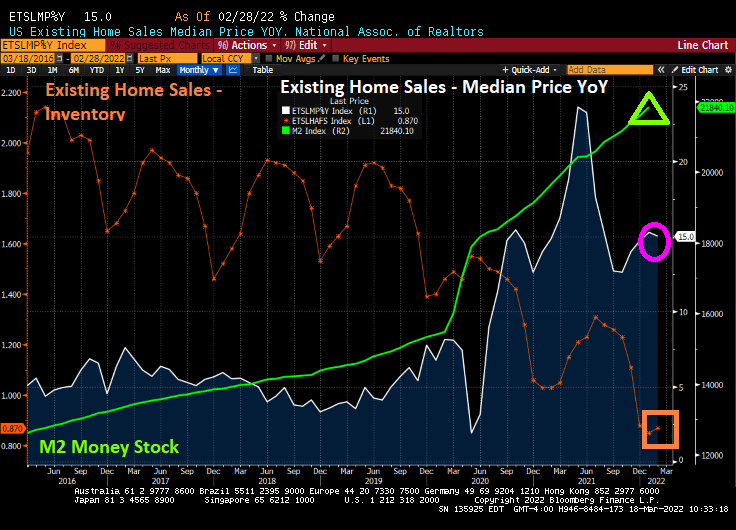

US existing home sales fell -7.24% from January as mortgage rates soar. On a YoY basis, existing home sales declined by -2.43%.

The median price of existing home sales “slowed” to 15% YoY in February as inventory picked-up slightly. And yes, Fed Stimulypto is still around and hasn’t helped increase inventory for sale.

As I said earlier, we are seeing the Treasury yield curve plunging towards recession.

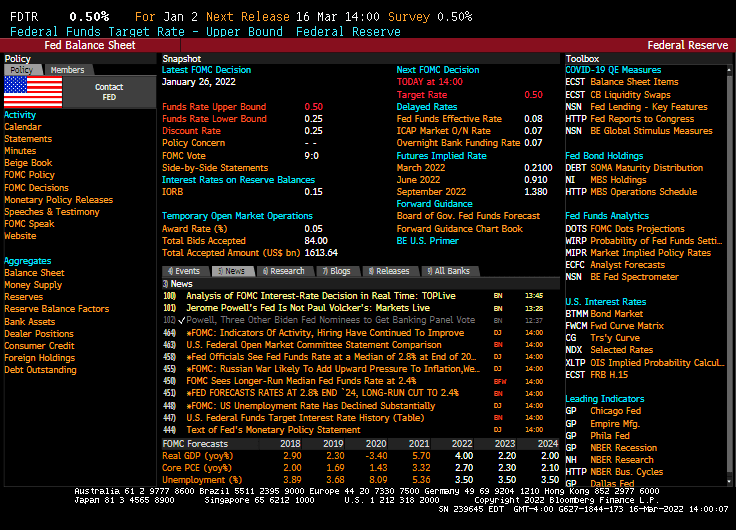

So, The Federal Reserve raised their target rate by … as expected … 25 basis points to 50 basis points.

The Taylor Rule suggests that the target rate should be 11.96%. So, Powell and The Gang are getting closer! /sarc

The short-term reaction to the measly rate increase? The Dow declined (but still in positive territory for the day) and the benchmark 10-year Treasury yield spiked to 2.23%.

On Powell’s surrender to inflation, the US Treasury 10Y-2Y curve continued to flatten.

You can see The Fed’s sloth-like response to blood-curdling inflation in the lower right-hand part of the chart.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 11, 2022.

The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 8 percent lower than the same week one year ago.

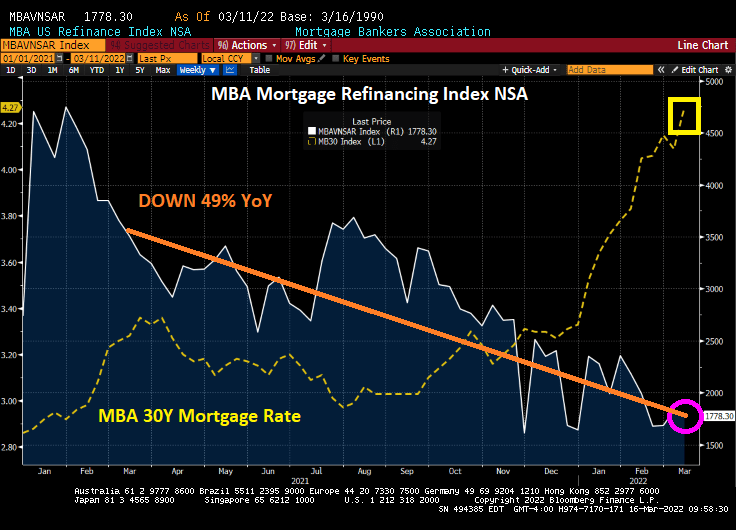

The Refinance Index decreased 3 percent from the previous week and was 49 percent lower than the same week one year ago.

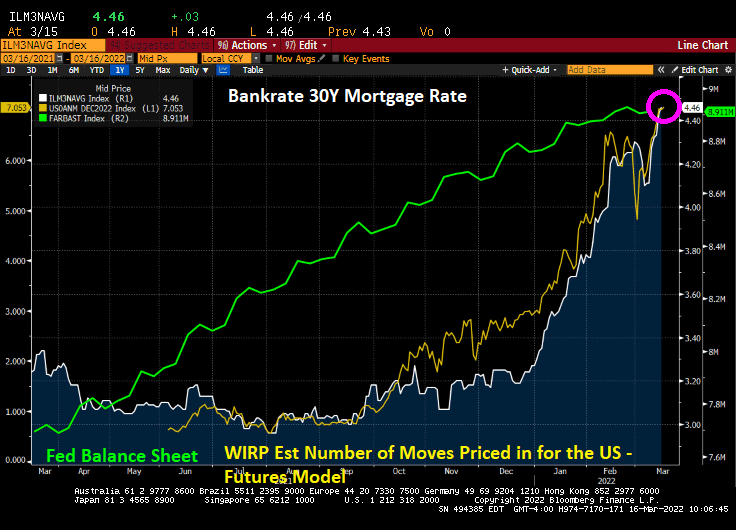

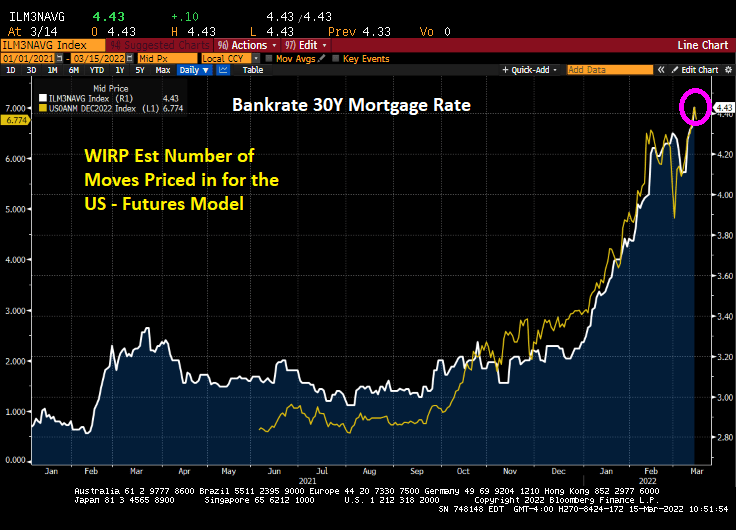

Bankrate’s 30-year mortgage rate has surged to 4.46%.

Here is a photo of alligators in Great Falls, Virginia, up-river from Washington DC. They are likely congregating for the Fed Open Market Committee (FOMC) announcement today.

Bankrate’s 30-year mortgage rate rose to 4.43%, up 55% under Biden/Pelosi/Schumer’s reign of error. Thanks to the rising Fed rate hikes priced-in the market.

The US Producer Price Index (PPI) final demand rose 10% YoY in February, further evidence of spiraling inflation under Biden/Pelosi/Schumer’s reign of error.

And speaking of Senate Majority Leader Chuck Schumer (D-NY), the Empire State Manufacturing Survey (General Business Conditions) crashed to -11.8.

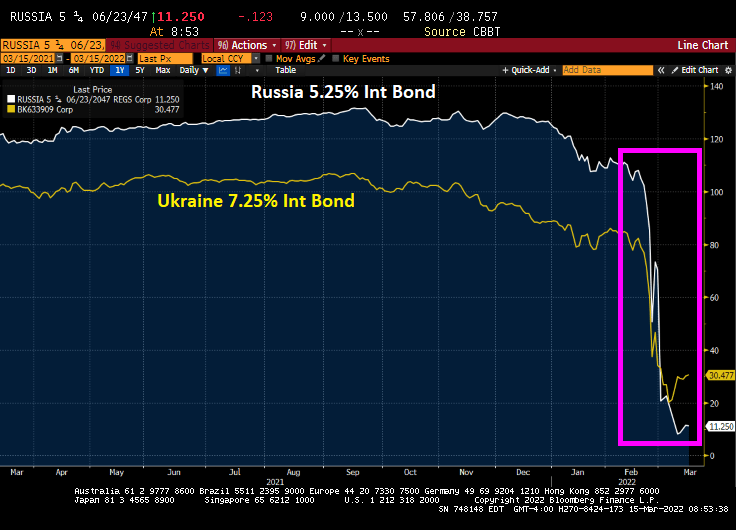

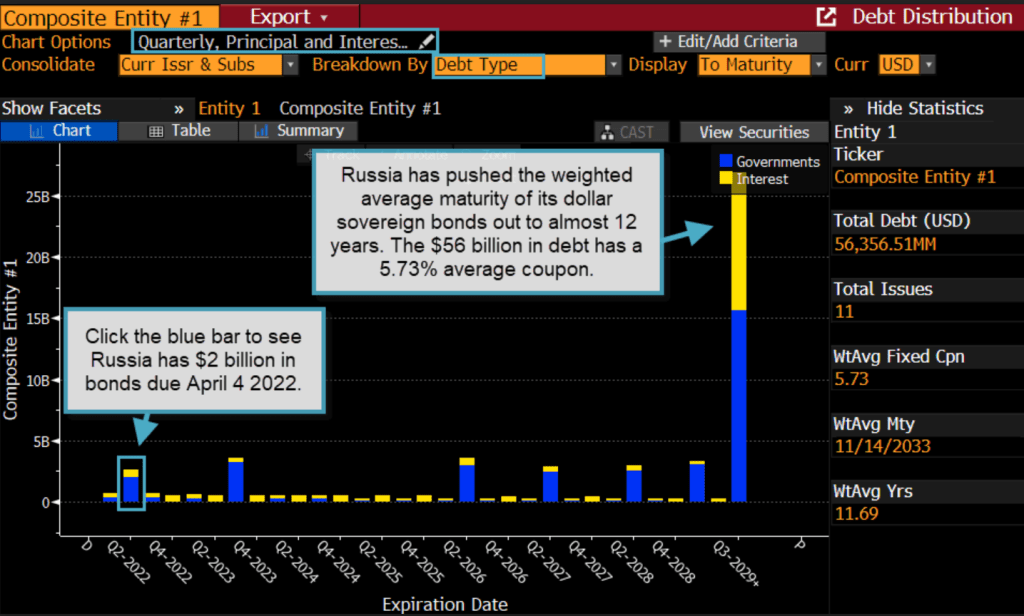

And Russia is losing the economic demolition derby with Ukraine (at least for sovereign debt).

I am still trying to figure out what House Speaker Nancy Pelosi (D-San Francisco) meant by “When we’re having this discussion, it’s important to dispel some of those who say, well it’s the government spending. No, it isn’t. The government spending is doing the exact reverse, reducing the national debt. It is not inflationary.”

Really Nancy?

Here is a chart of Federal government outlays and inflation. Massive expenditures and growth in Federal debt and the resulting inflation. Nancy?

Yes, it is the much anticipated Fed Week! The Fed Open Market Committee (FOMC) will announce it decision (probably the first rate hike under Biden of 25 basis points).

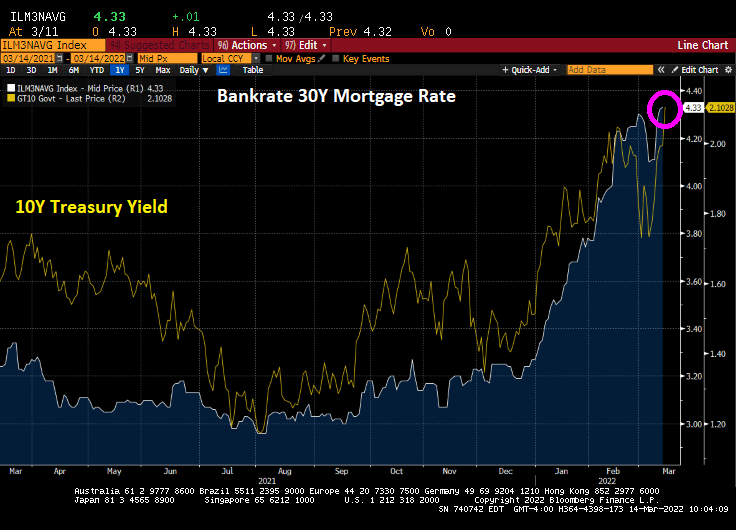

This morning, the 10-year Treasury yield rose by 11.1 basis points and the Bankrate 30Y mortgage rate rose to 4.33%.

Actually, sovereign yields are up around 10 basis points in the US, Canada, and across the pond.

Fed Funds Futures are pointing to 7 rate hikes over the next year with 1.114 rate hikes on Wednesday. That means The FOMC may raise rates MORE than the 25 basis points expected my many (including me).

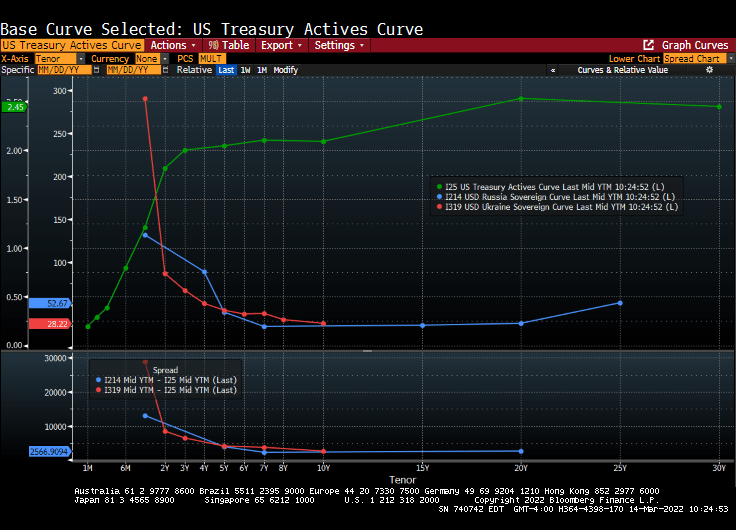

The US Treasury actives curve remains steeply upward sloping while both the Russian and Ukraine sovereign curves are steeply inverted and crashing.

Russia has pushed the weighted average maturity of its dollar sovereign bonds out to almost 12 years.

The most hilarious headline of the day is a Bloomberg opinion piece: “Fighting Inflation May Require the Fed to Be Brutal: Clive Crook” How about the Biden Administration relaxing oil drilling and pipeline restraints? Otherwise, brutal translates into causing a recession. Great suggestion, Clive! … NOT!

Well, so much for rising gasoline prices being the fault of Vlad “The Ukrainian Impaler” Putin and Russia invading Ukraine. In fact, gasoline prices were rising at a 62% YoY pace in April 2021, well before Russia’s invasion of Ukraine.

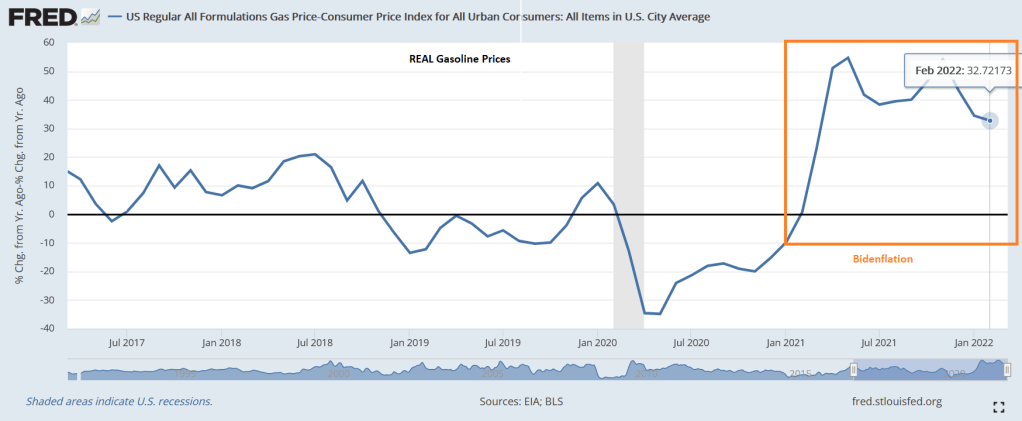

REAL gasoline prices (nominal gasoline prices less inflation) are up 32.72% YoY in February.

Press secretary Jen Psaki can take the opportunity to proclaim that REAL gasoline prices have actually declined in February.

I keep waiting for the Biden Administration and Congress to launch price controls and supply rationing rather than simply allow the Keystone Pipeline to be built and allow drilling on Federal lands.

You must be logged in to post a comment.