On the corporate side, US bankruptcies in 2023 had the worst start to a year since 2010 and the financial crisis.

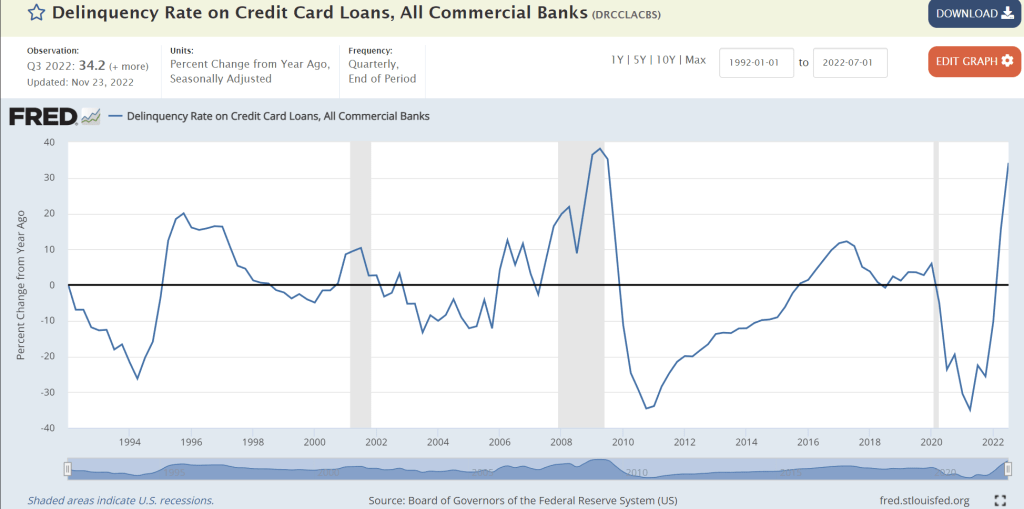

On the personal finance side of the ledger, the delinqueny rate on credit cards is growing at the faster rate since 2010.

Throw in 22 straight months of negative REAL wage growth, and have a scary situation facing middle America.

And the shate of outstanding subprime auto debt (30 days or more delinquent) is up to the highest rate since … well, you know when. The financial crisis of 2009-2010.

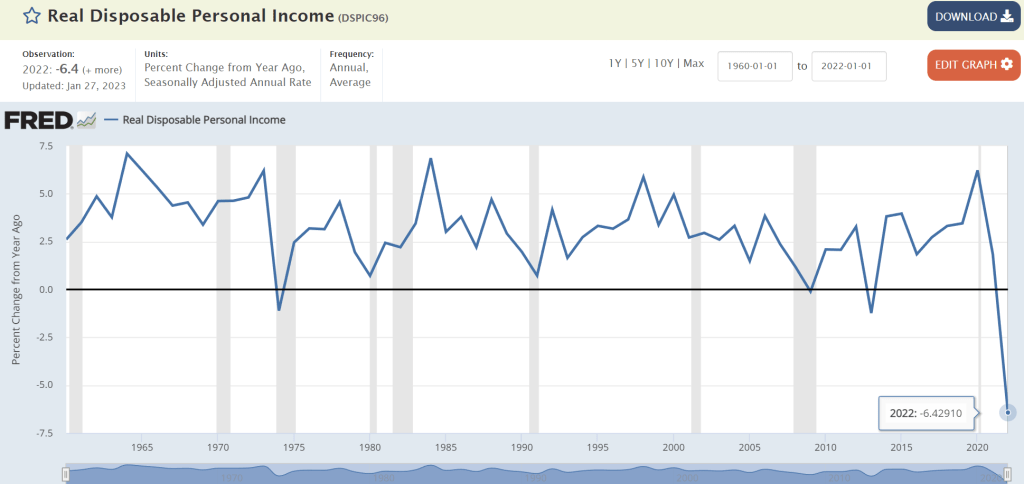

President Biden touts his economic plan as being a great success. But the data says otherwise. Real Disposable Personal Income, for examplge, was down -6.4% year-over-year (YoY) in 2022. That is the WORST reading since The Great Depression.

And to cope with inflation, Americans have expanded their credit useage, but credit card delinquencies are through the roof.

So much for “Middle Class Joe” and The Forgotten Man. Biden hasn’t forgotten, he just doesn’t care.

We got trouble in Potomac City! No, I’m not talking about the numerous Top Secret documents that Biden carelessly left in his garage in Delaware and the UPenn Biden Center. And they found more over the weekend. I’m talking about the US Treasury 10Y-2Y yield curve being inverted for 135 straight days. And thanks to inflation, REAL wage growth has been negative for 21 straight months.

All this is happening while M2 Money growth (green line) stalls to 0% YoY.

Swaps 5Y are rising as The Fed withdraws monetary stimulus.

Silvergate Capital Corp. shares plunged after the bank said the crypto industry’s meltdown triggered a run on deposits, prompting the company to sell assets at a steep loss and fire 40% of its staff.

Customers withdrew about $8.1 billion of digital-asset deposits from the bank during the fourth quarter, which forced it to sell securities and related derivatives at a loss of $718 million, according to a statement Thursday. Executives said on a conference call that Silvergate may become a takeover target.

“In response to the rapid changes in the digital asset industry during the fourth quarter, we took commensurate steps to ensure that we were maintaining cash liquidity in order to satisfy potential deposit outflows, and we currently maintain a cash position in excess of our digital asset related deposits,” Chief Executive Officer Alan Lane said in the statement.

The collapse of Sam Bankman-Fried’s FTX sparked a crisis for Silvergate, which held deposits for FTX units and Alameda Research, the trading firm at the heart of the crypto exchange’s downfall. Lawmakers are also scrutinizing the bank.

Silvergate plunged 44% to $12.34 at 9:48 a.m. in New York, the steepest decline since the La Jolla, California-based company went public in November 2019. The stock is down 91% in the past 12 months. Signature Bank, which said in December that it intended to shed as much as $10 billion deposits from digital-asset clients, fell 5.8% to $111.05.

Silvergate Capital Corporation operates as a bank holding company. The Company, through its subsidiary Silvergate Bank provides a banking platform for innovators, especially in the digital currency industry, and developing product and service solutions addressing the needs of entrepreneurs. Silvergate Capital serves customers in the United States.

Silvergate once saw the crypto industry as giving it a huge growth opportunity. Over the course of a decade, it transformed itself from a firm catering to small businesses into a publicly traded company known for providing banking services to major crypto clients such as Coinbase Global Inc. and Gemini Trust Co. — as well as FTX and Alameda Research.

At least Solana is on the rise.

Sam Bankman-Fried will go down in history as commiting one of the greatest financial frauds in world history. Why did he have four meetings with Biden’s top staffers prior to FTX’s crash and burn?

2022 is one of the record books and not in a Tiger Woods way. Call it a year of pain.

First, the US enacted policies that drove up energy prices (goin’ green) that reverberated through the entire economy in the form of higher prices. Second, The Federal Reserve, in attempt to combat runaway inflation, started removing the excessive monetary stimulus that had been around since Fed Chair Bernanke initiated QE, the seemingly unlimited purchase of Treasury and Agency MBS securities. Janet Yellen continued the massive asset purchases and zero interest rate policies or ZIRP. Now that inflation has struck the American middle class hard, we are seeing Fed Chair Powell doing what Bernanke and Yellen wouldn’t do — remove the monetary punchbowl.

Using Robert Shiller’s on line data, US stocks and bonds have had an awful year, the worst combined year since 1871.

US equity returns have been demolished under the NEW dual mandate (goin’ green = rising prices = Fed tightening).

Let’s see how two of the most famous investment gurus did in 2022, Warren Buffet and Cathie Wood. Buffet’s Bershire Hathaway Class A equity was UP 4% in 2022, while Cathie Wood’s ARK Innovation ETF collapsed by -67% in 2022.

Here is the clinker. The US economy (as well as the global economy) seem dependent on “cheap money” from Central Banks like The Federal Reserve. So the question is … will The Fed pivot? Fed talking heads are saying no, but Fed Funds investors are saying yes to a pivot after June 2023.

Ulysses S Grant was the President the last time the combined stock and bond market was this bad.

US housing starts plunged -16.4% since the same time last year (aka, YoY) as The Federal Reserve continues tightening its monetary policy.

Since October (aka, MoM), housing starts only dropped -.049% in November. 1-unit detached starts were down -4.06%. But multifamily (5+) starts were up 4.85% MoM.

Building permits were down -11.24% from October to November (baby, its cold outside!) and down -22.4% since November 2021 (aka, YoY).

The 12-month-ahead probability of recession spiked in November across all of yield curve models. The deterioration in the outlook was most significant in the one that relies on the 3-month/18-month forward spread — Fed Chair Jerome Powell’s favored model — which now sees a 59% chance of recession next year, compared with almost 0% six months ago. Yield curve models see the strongest signal for recession starting around September 2023.

We assess the probability of recession in the months ahead by looking at a suite of models: three yield curve models — which take as their sole input the spreads between 2-year/10-year, 3-month/10-year, and 3-month/18-month forward US Treasury yields, respectively — as well as a model that takes 13 financial and macroeconomic indicators as inputs.

All three yield curves inverted further in November, indicating higher probability of a downturn next year. Notably, the 3-month/18-month forward curve inverted for the first time this year, and the model based on that indicator suggests a 59% chance of recession in 12 months (vs. 32% for the same reference period in the prior update) — that would be in November 2023.

My favorite yield curve is the 10-year – 2-year curve which has been inverted for 112 straight days.

The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

The start of a new week and the US Treasury 10-year yield is up 10 basis points, always a noteworthy change. And with it, the 30-year mortgage rate should climb.

Since Biden/Pelosi/Schumer are in a lame duck session with Republicans taking the House in January, let’s see if Republicans can halt the insanity in Washington DC.

Be that as it may, Fed Funds Futures are pointing at a 50 basis point rate hike at the December 14th FOMC meeting.

Seriously, how is The Federal Reserve going to cope with $204 TRILLION … and growing Federal debt AND unfunded liabilities?

You must be logged in to post a comment.