While members of the Biden Administration party at DC nightclubs, the rest of America are drinking Carlo Rossi wine (a favorite of mine in high school!) and eating Spam.

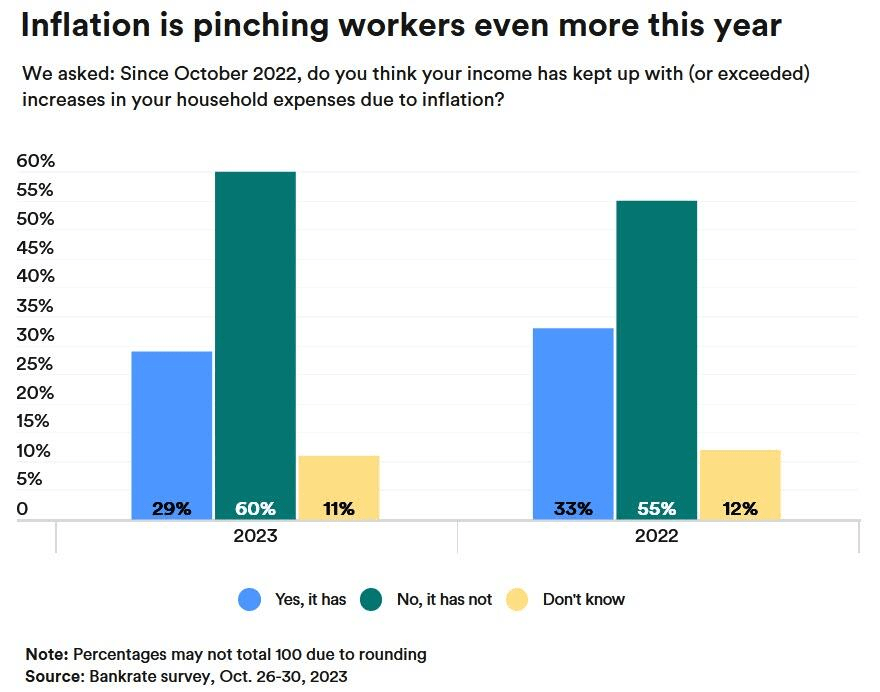

While hourly pay has increased, inflation has outpaced it.

Spending on basic survival needs like food, transportation, housing, and energy has increased, with households in the Mountain West facing the highest rates of inflation.

“We choose January 2021 as the base month because it was the last time inflation was within recent historical norms,” the report reads.

“Due to a combination of higher inflation rates and higher average household spending, inflation is imposing the highest monthly costs on families in the states of Colorado, Utah, and Arizona,” the report adds.

Families in Colorado and Washington, DC, are experiencing inflation costs higher than the national average.

Things are even worse in 2023 regarding inflation ravaging worker’s income. Over 60% of Americans reported that their wages were lagging well behind inflation.

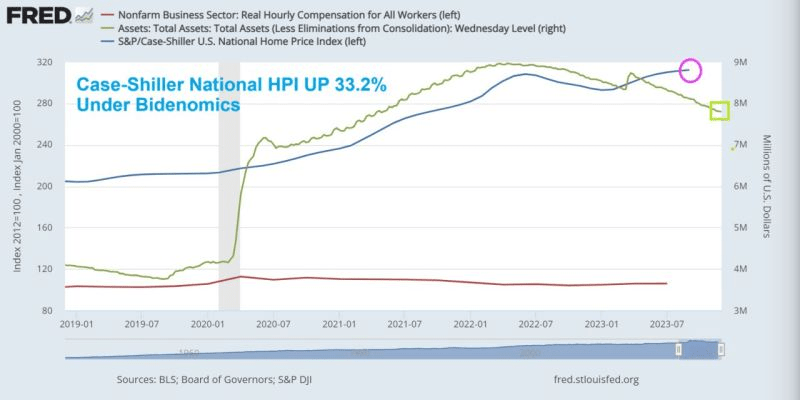

Since January 2021, US purchasing power of the US Dollar is down a whopping -15.4% under Biden.

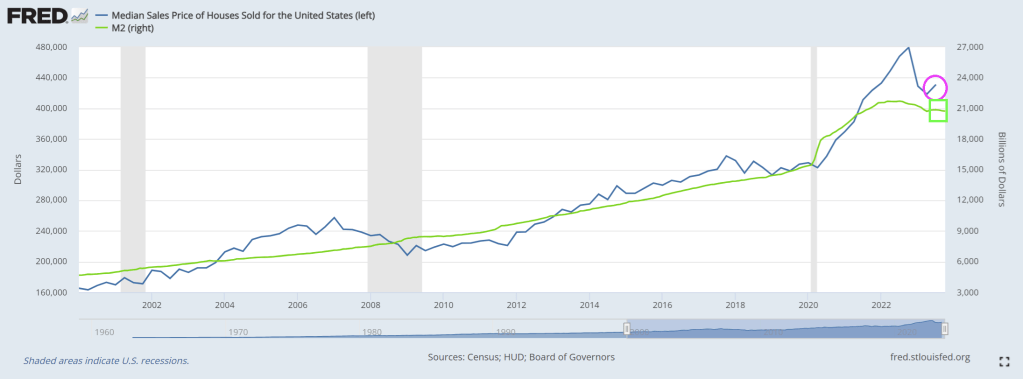

And home prices are up 33.2% under Biden, much of it due to The Feral Reserve money printing to fund Biden’s folicy initiatives. (I saw Biden claim he wrote the Inflation Reduction Act … the one thing we know is House legislation is written by an army of Congressional staffers, not El Presidente).

Home prices up 33.2% and purchasing power of US Dollar down -15.4% under Biden.

And like magic, Biden made $11,400 disappear from household income to pay for Bidenomics.

Median home prices are up a whopping 20% under Biden and his signature Bidenomics, growing the economy from the inside-out (?) instead of top-down. Excuse me Joe, Bidenomics is pure top-down Soviet-style economic planning. Markets be damned! The end result? Housing is far more expensive under Biden as are down payments.

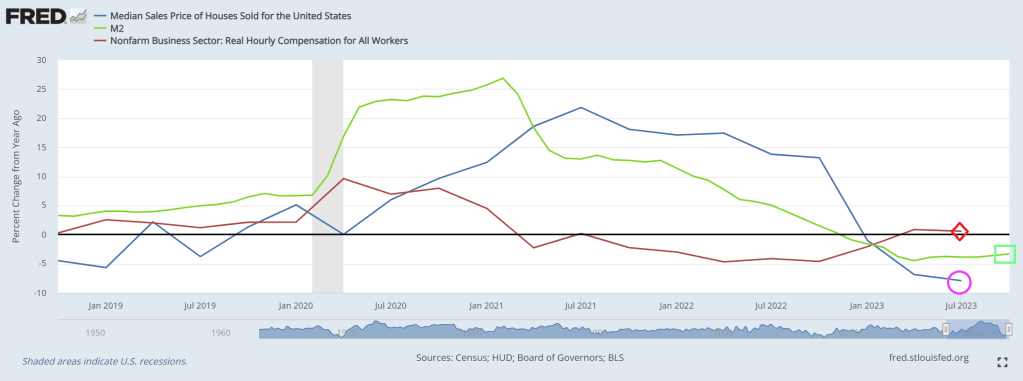

If we look at year-over-year (YoY), we can see the burst of Covid-related spending and M2 Money growth (green line) that surged in 2020/2021. And rising home prices followed shortly thereafter. But as M2 Money growth slows, median home price growth declined into negative growth. The only factor that is positive is real hourly compensation (red line). But that is barely above 0%.

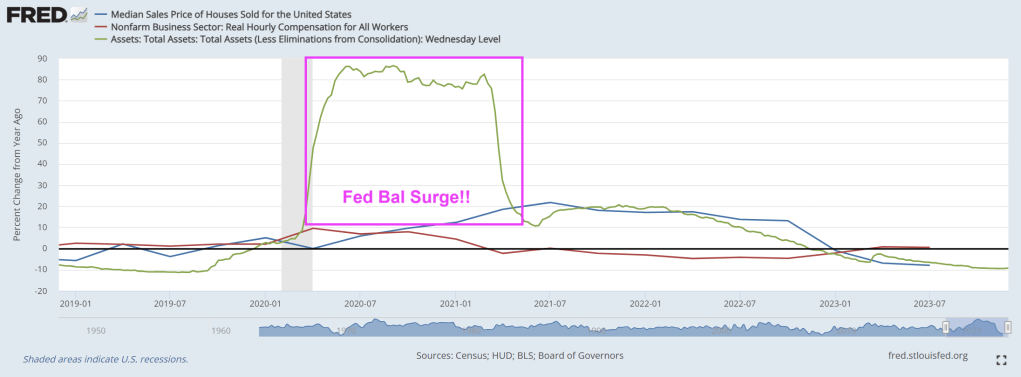

If we look at The Fed’s balance sheet surge (much like a storm surge), you can see the 2020/2021 overreaction to Covid and the various government shutdowns (along with school shutdowns).

The problem is that The Fed is shrinking their balance sheet like Biden shuffles. Maybe The Fed is following Biden’s lead: slow walking, incoherent messaging. And with the Fed storm surge of 2020/2021, Case-Shiller national home price index is up 33.2% under Bidenomics. Good luck with that down payment if you are renting and want to become a homeowner.

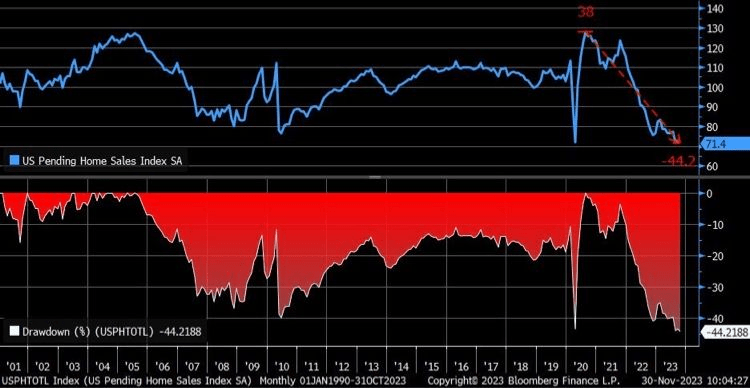

Pending home sales crash is showing why government usually fails to deliver sensible outcomes.

After all, Biden (and his overlord Obama) are truly addicted to gov solutions. Which means they are doomed to fail, as most government policies do.

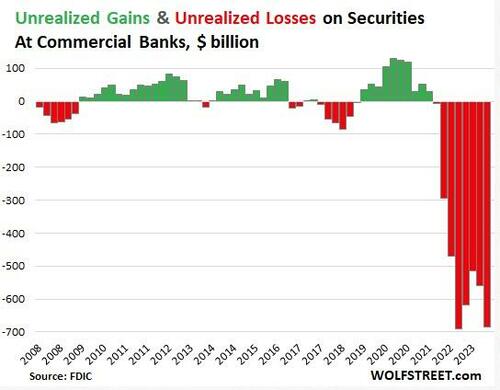

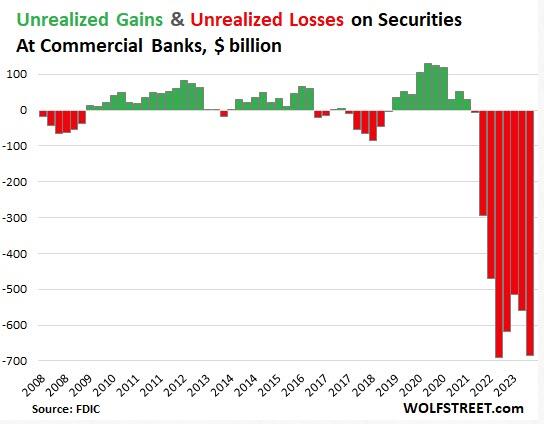

Unrealized losses on securities held by US banks exploded by 22% in the third quarter.

Of course, unrealized losses don’t really matter — until they do.

This is yet more evidence that the financial crisis that kicked off last March continues to bubble under the surface.

Unrealized losses, primarily on US Treasuries and mortgage-backed securities rose by $126 billion in Q3 and now total $684 billion, according to the FDIC’s quarterly bank data release.

Current unrealized losses are only slightly below the record set in the third quarter of 2022. This reflects the fact that the FDIC took over three failed banks earlier his year and ate their unrealized losses when it sold the banks’ assets, thus wiping them from the books.

Unrealized looses on securities are divided between two accounting methods.

Unrealized losses on held-to-maturity (HTM) securities jumped by $81 billion to $391 billion.

Unrealized losses on available-for-sale (AFS) securities jumped by $45 billion to $293 billion.

It’s important to understand these are only paper losses. Ostensibly, the banks will hold these bonds until maturity and then will be paid their face value. If it plays out this way, there won’t be any real losses.

The problem is that these unrealized losses drastically decrease a bank’s liquidity. If it has to sell bonds in order to raise capital, the bank will experience significant losses. This is exactly what took down Silicon Valley Bank last March.

Here’s what happened.

SVB sold a large portion of its bond portfolio at a $1.8 billion loss. At the time, SVB CEO Greg Becke said the bank made the sale “because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients.”

The bank bought the bonds when interest rates were low. As a result, the $21 billion available for sale (AVS) bond portfolio was not yielding above cash burn. Meanwhile, rising interest rates caused the value of the portfolio to fall significantly. The plan was to sell the longer-term, lower-interest-rate bonds and reinvest the money into shorter-duration bonds with a higher yield. Instead, the sale dented the bank’s balance sheet and caused worried depositors to pull funds out of the bank.

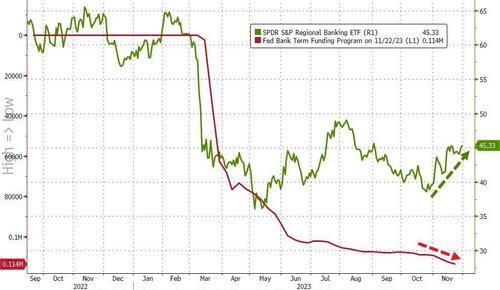

WolfStreet explained more generally how these “irrelevant” unrealized losses can suddenly become relevant.

Banks, via a quirk in bank regulations, don’t have to mark these securities to market value, but can carry them at purchase price. The difference between market value and purchase price is the ‘unrealized gain or loss’ that the bank must disclose in its quarterly financial filings, so that we the depositors can see them and get spooked by them and yank our money out, us billionaires and centimillionaires first, on the two fundamental principles of investing: 1, he who panics first, panics best; and 2, after us the deluge.”

The Federal Reserve set up a bailout program to allow banks to deal with this problem. Instead of selling bonds at a loss, cash-strapped banks can go to the Fed’s Bank Term Funding Program (BTFP) and borrow against them “at par” (face value). This allows banks to use these undervalued assets to raise cash (at least temporarily) without realizing big losses on their balance sheets.

As unrealized losses rise, banks continue to tap into this bailout program more than nine months after the crisis kicked off.

In effect, the Fed managed to paper over the financial crisis with this bailout program.

It basically slapped a bandaid on it. But it has not addressed the underlying issue – the impact of rising interest rates on an economy and financial system addicted to easy money.

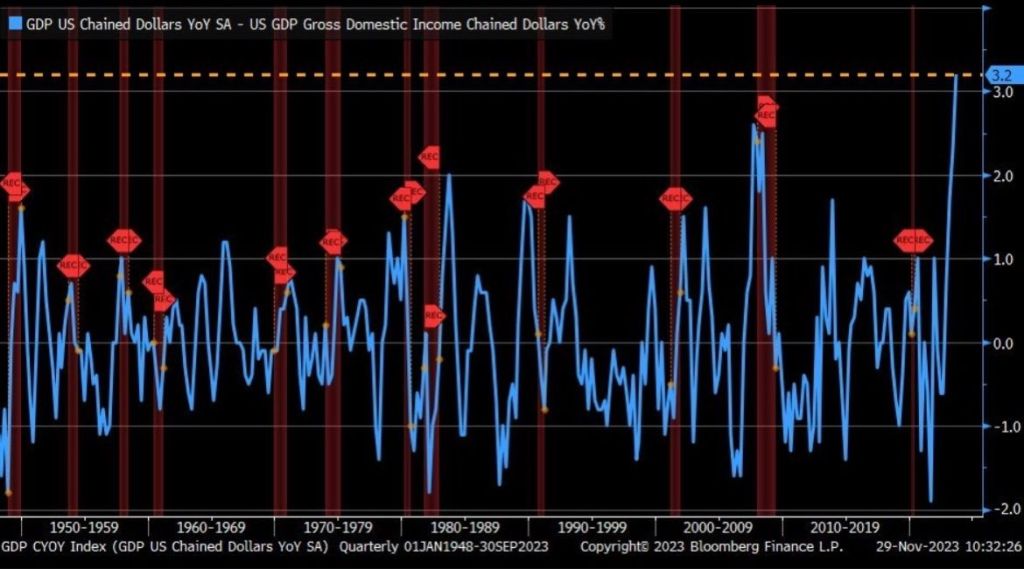

Remember, the US is on the cusp of a REAL recession, thank to Bidenomics.

The spread between real GDP and real Gross Domestic Income (GDI) just hit an all-time high. Even higher than The Great Recession of 2009.

Might as well have AC/DC’s Angus Young as US Treasury Secretary instead of tone-deaf Janet Yellen.

Despite The Fed’s attempts at cooling inflation down to 2%, we are seeing a re-animation of price increases. this time with home prices.

On a year-over-year basis, the Freddie Mac National FMHPI was up 6.0% in October, from up 5.1% YoY in September. The YoY increase peaked at 19.1% in July 2021, and for this cycle, bottomed at up 0.9% in April 2023. …

vv

Austin TX is the big loser, down -11.2% from peak. Followed by Idaho (largely people escaping from Newsomland (California) and speculators. The sixth leading area is Lake Havasu AZ.

As of October, 7 states and D.C. were below their previous peaks, Seasonally Adjusted. The largest seasonally adjusted declines from the recent peak were in Idaho (-4.5%), Utah (-2.7%), D.C. (-2.0%), and Nevada (-1.6%). Nevada, Idaho and Utah are now known as the Mild, Mild, West due to sagging home prices.

For cities (Core-based Statistical Areas, CBSA), here are the 30 cities with the largest declines from the peak, seasonally adjusted. Austin continues to be the worst performing city.

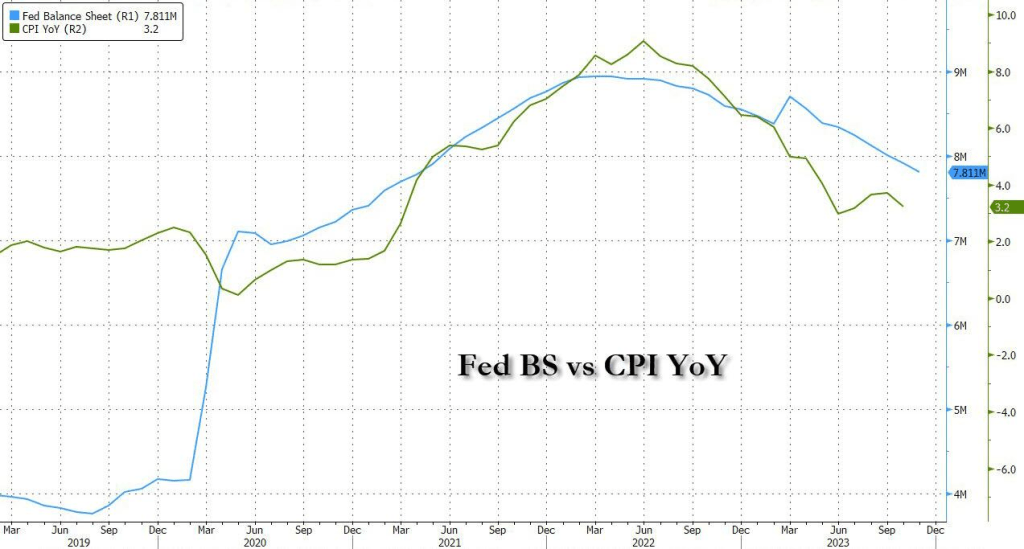

Speaking of inflation and The Fed, Biden claiming he lowered inflation is laughable if it wasn’t so sad. It is all The Fed. And their timidness is shrinking their balance sheet is contributing to persistent inflation.

So, yes, inflation is growing again. This time it is persisent and growing.

But was it organic growth or simply The Federal Government funding the defense and green energy industies with trillions in spending?

One factor has been government spending which grew an unsustainably 4.7% in real terms over the last year. Outside the pandemic, this is one of the fastest rates in decades and works at a cross purpose with monetary policy objectives.

Bidenomics is code for massive Federal spending (and debt) to fund Federal priorities: wars in Ukraine, Israel and likely involvement around Taiwan. And the costly switch to green energy (but not nuclear, for some reason).

If the US economy growing simply to function as a war machine and wealth transfer mechanism from the middle class to the 1%, we are on the Highway To Hell. Personal consumption contributed 2.44% to the bottom line GDP print in Q3, down from the pre-revision number of 2.69% but well above Q2’s 0.55%.

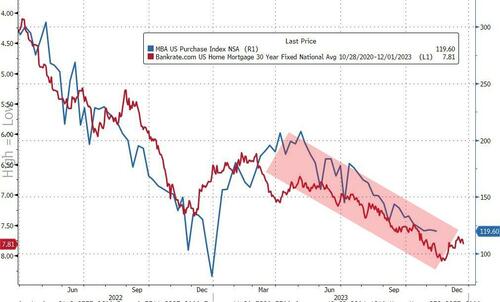

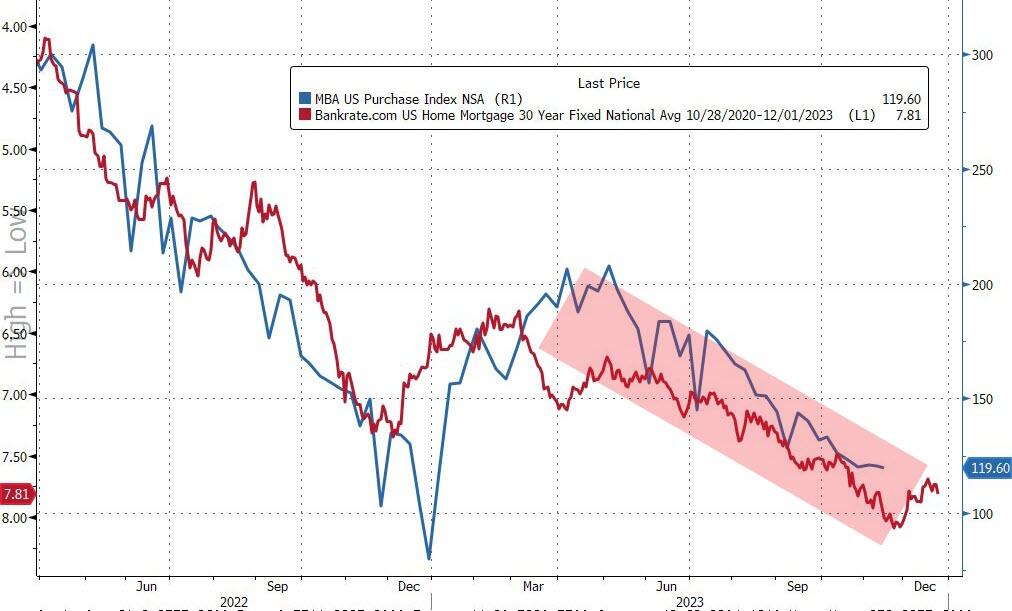

As a reminder, The Mortgage Bankers Association’s index of home-purchase applications tumbled to 120 – the lowest level since 1995 – as mortgage rates hit 8% for the first time in 23 years in October.

Source: Bloomberg

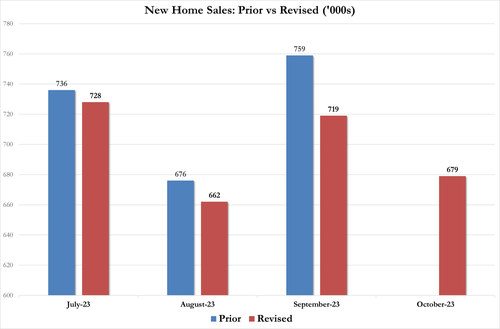

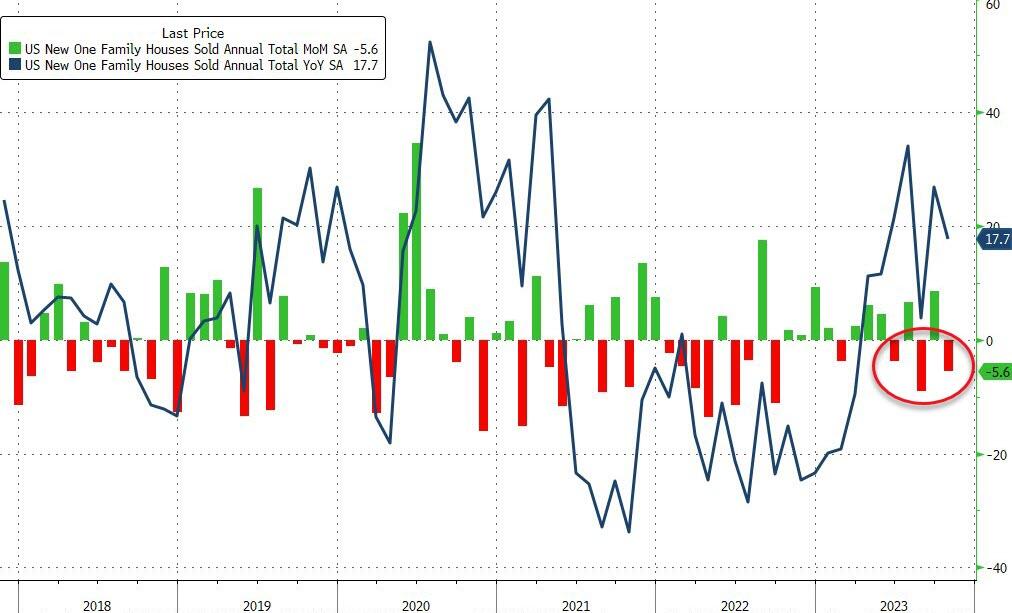

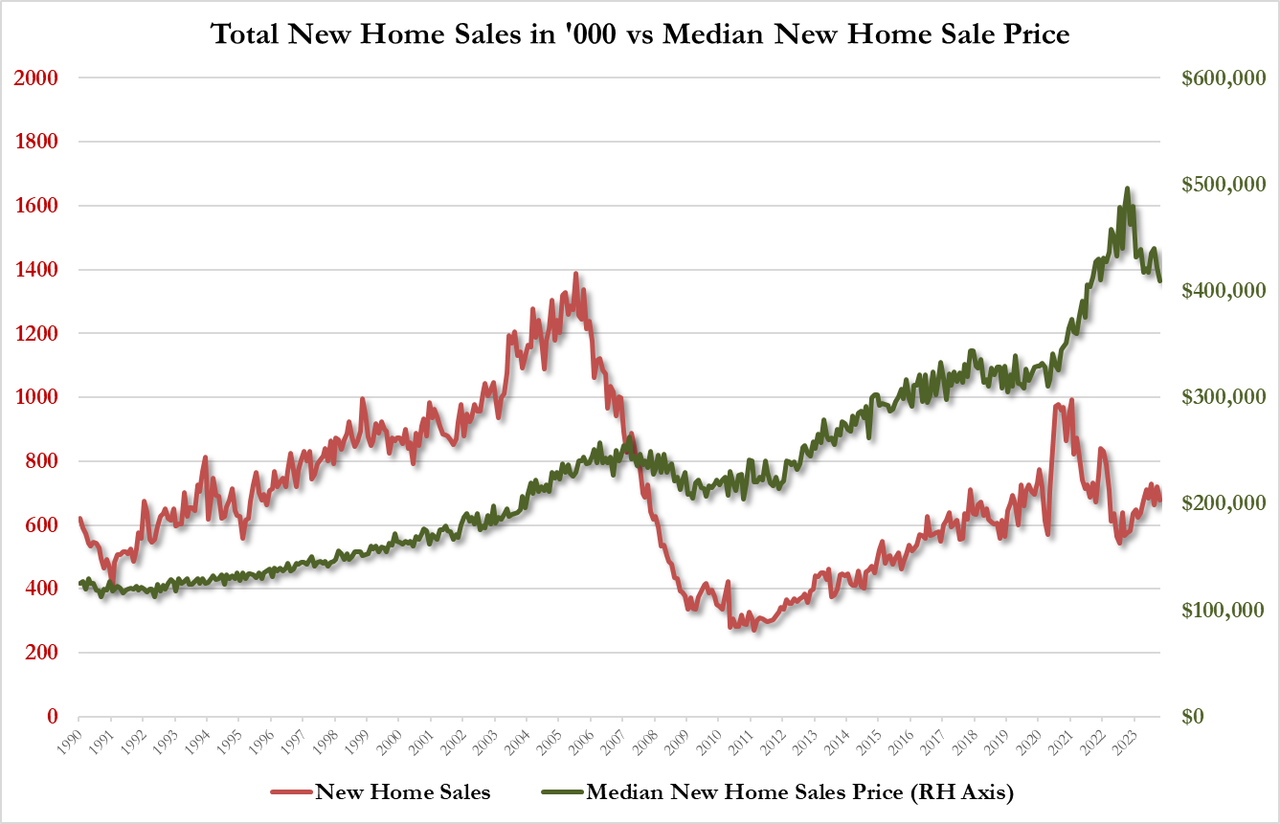

So, it should be no surprise that new home sales were even worse than expected, plunging 5.6% MoM (and making it even worse, the 12.3% MoM jump in Sept was revised down to +8.6%)…

Source: Bloomberg

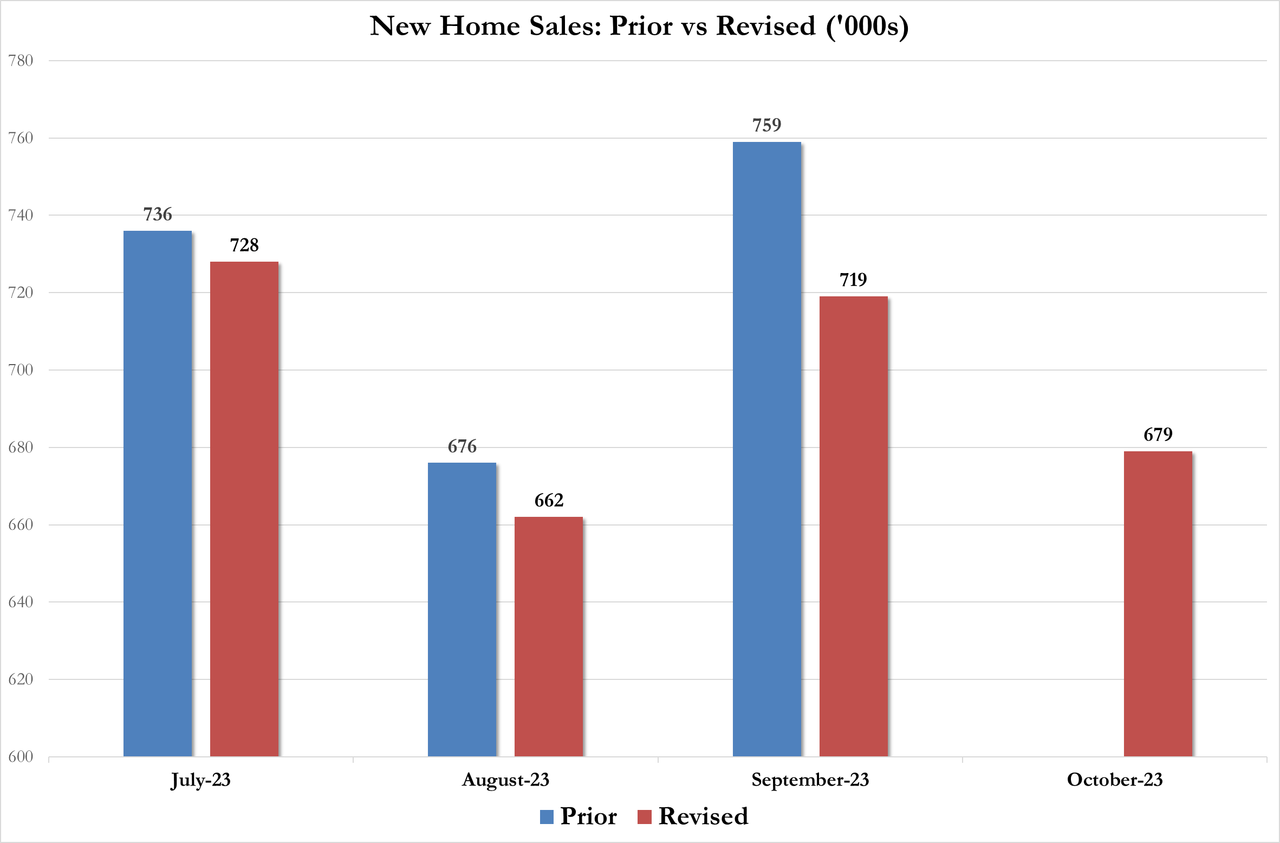

The trend of downward revisions continues…

The New Home Sales SAAR of 679k is flat from April (that was below all economists’ forecasts)…

Source: Bloomberg

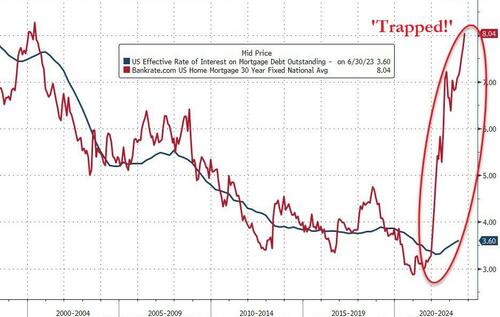

It appears the homebuilders finally hit their wall eating the gap between these two lines was just not sustainable…

Source: Bloomberg

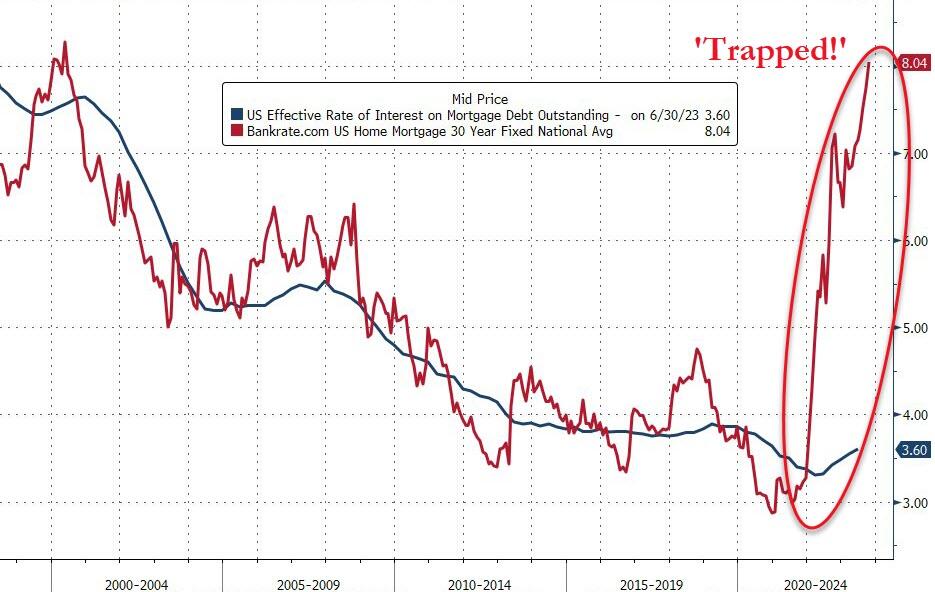

And as we noted previously, homebuilders can’t be filling this gap either – between the current 30Y mortgage rate and the effective rates that borrowers are currently paying on their home loans – (i.e. subsidizing new home sales) forever…

Source: Bloomberg

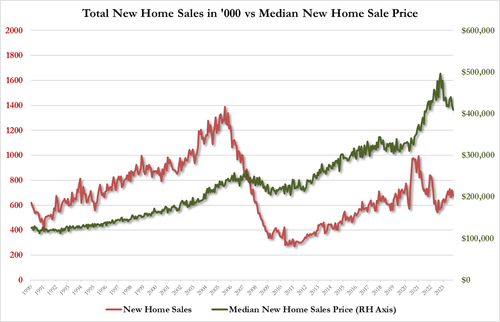

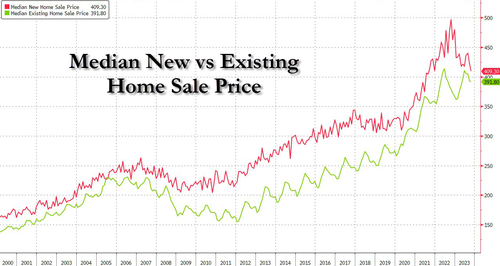

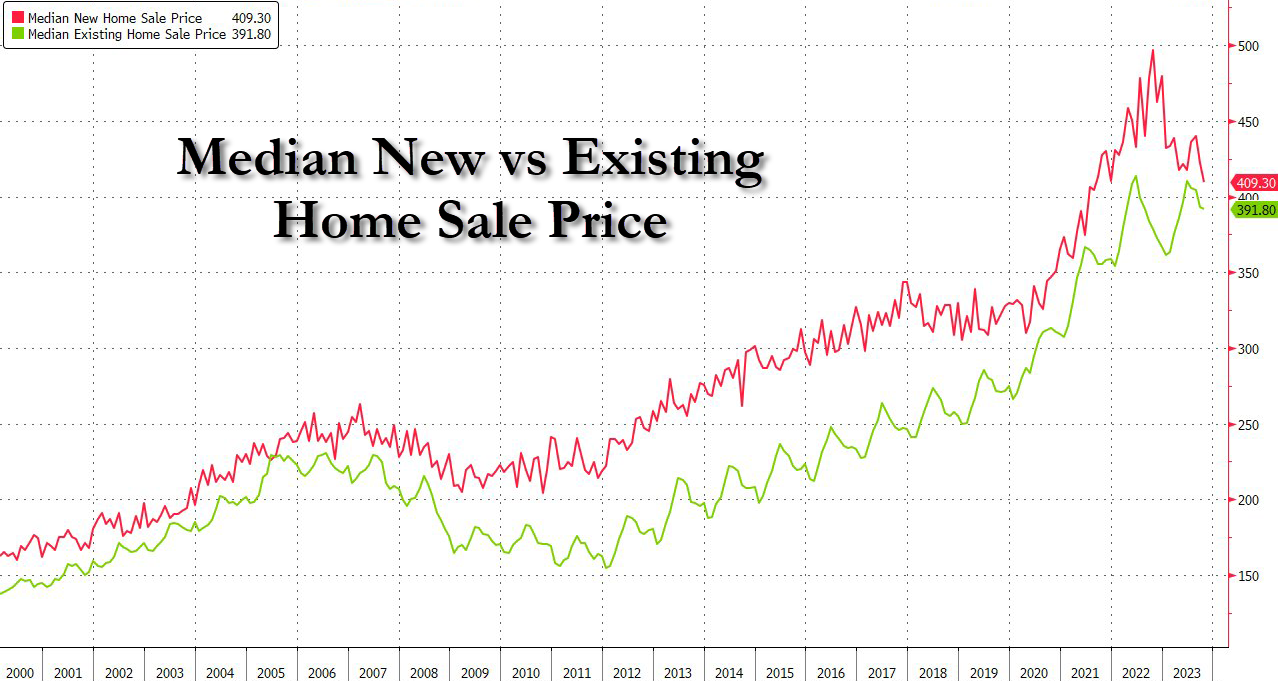

The median new home price fell 17.6% y/y to $409,300; average selling price at $487,000

That is the lowest median price since Aug 2021, catching back down to existing home prices…

Source: Bloomberg

Is Powell winning his war on affordability? Or crushing the middle class’s main source of wealth? Or is it Hammer Time??

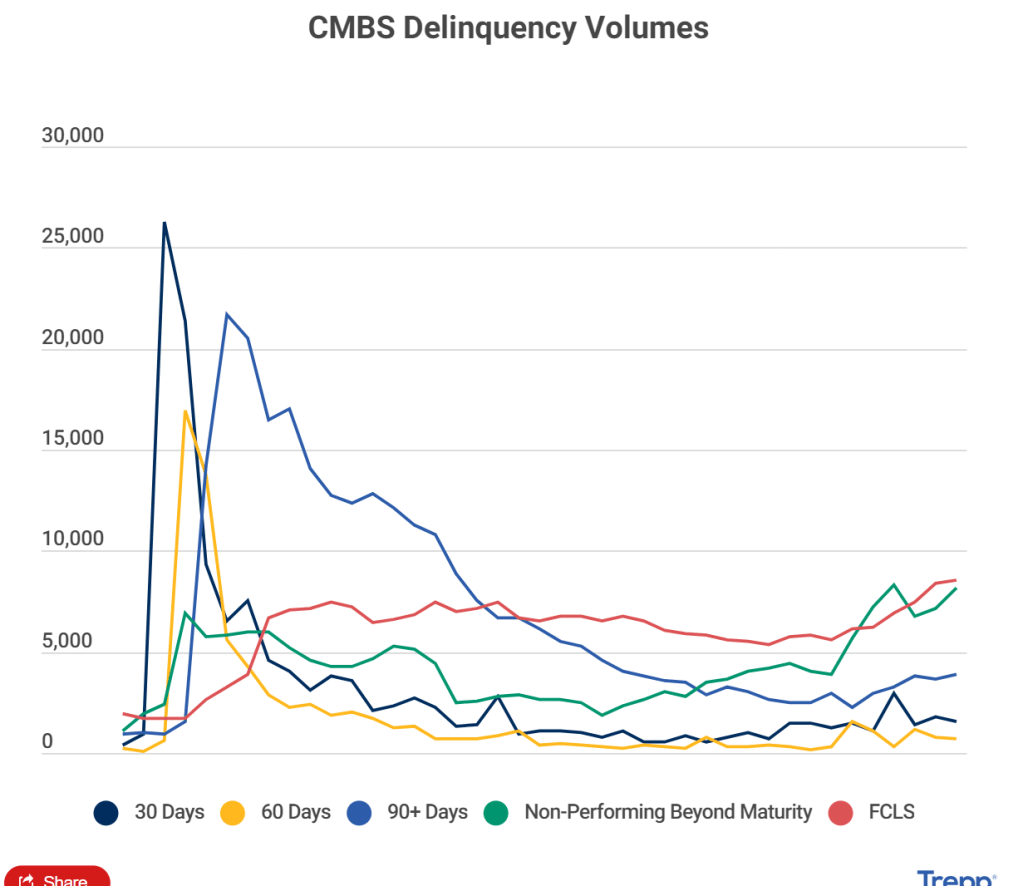

According to Trepp, the volume of CMBS delinquency increased 49.4% during 10 months through October.

Looking for more? This piece has been taken from Trepp and Commercial Real Estate Direct’s Q3 2023 Quarterly Data Review. Access the magazine here.

The volume of CMBS loans that are classified as delinquent increased by 49.4% during the 10 months through October to $27.91 billion. That volume amounts to 5.07% of the $601.98 billion universe tracked by Trepp. In contrast, delinquencies at the end of last year amounted to 3.03% of the $616.15 billion universe then extant.

Office Sector Drives Increase in Delinquency Volumes

The driver of the increase was the office sector, which had a 261% increase in delinquency volumes over the 10-month period through October. A total of 199 loans with a balance of $9.59 billion, or 5.91% of all CMBS office loans were at least 30 days late with their payments, as of the end of October. At the end of last year, 115 loans with a balance of $2.65 billion, or 1.63% of office loans, were delinquent.

The sector’s prospects are unlikely to improve as office occupancy rates have declined in most of the country’s major markets. That’s been driven by a substantial pullback in demand from office-using tenants.

Hit especially hard have been loans with floating coupons that are maturing and need interest-rate cap agreements in place before they qualify for term extensions. Those rate caps have skyrocketed in price in lockstep with interest rates.

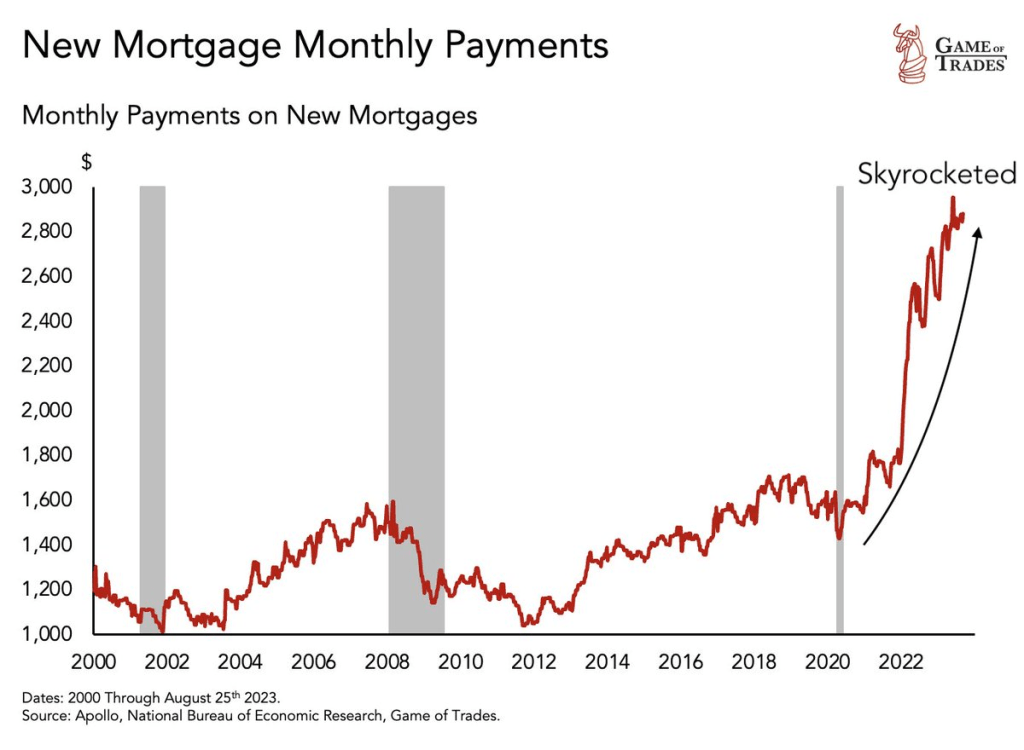

On the residential side, The Fed is helping drive mortgage payments through the roof!

The Federal Reserve reminds me of The Stones’ song “Tumbling Dice.” Why? The Fed can’t tell if inflation is cooling or re-accelerating. Hence, they are just rolling dice.

Let’s start with mortgage rates, a critical component of the housing and CRE markets. Mortgage rates remain up 163% since 2021, not great for housing affordability. Despite recent small declines in the mortgage rate. The 10Y-2Y Treasury curve is also going deeper into reversion … again.

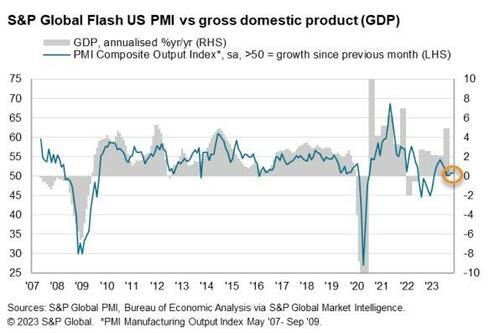

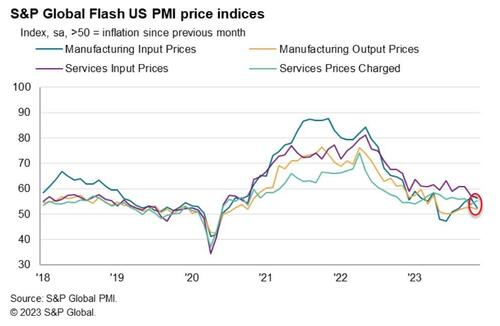

However, the data was more mixed with US Manufacturing falling more than expected to 49.4 – back into contraction – (vs 49.9 exp) from 50.0 in October. However, US Services unexpectedly rose from 50.6 to 50.8 (exp 50.3).

“The US private sector remained in expansionary territory in November, as firms signalled another marginal rise in business activity. Moreover, demand conditions – largely driven by the service sector – improved as new orders returned to growth for the first time in four months.

The upturn was historically subdued, however, amid challenges securing orders as customers remained concerned about global economic uncertainty, muted demand and high interest rates.

Businesses cut employment for the first time in almost three-and-a-half years in response to concerns about the outlook. Job shedding has spread beyond the manufacturing sector, as services firms signalled a renewed drop in staff in November as cost savings were sought.

“On a more positive note, input price inflation softened again, with cost burdens rising at the slowest rate in over three years. The impact of hikes in oil prices appear to be dissipating in the manufacturing sector, where the rate of cost inflation slowed notably.

Although ticking up slightly, selling price inflation remained subdued relative to the average over the last three years and was consistent with a rate of increase close to the Fed’s 2% target.”

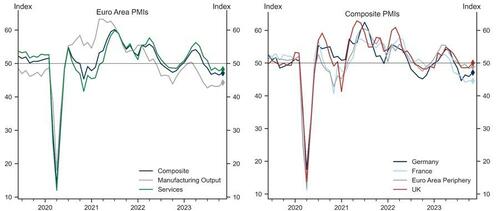

The US data comes after yesterday’s Euro area composite flash PMI increased by 0.6pt to 47.1, above consensus expectations, driven by a meaningful acceleration in Germany and the periphery, partially offset by a marginal decline in France. In the UK, the composite flash PMI improved meaningfully and entered expansionary territory at 50.1, above consensus expectations, on the back of a pickup in both sectors, with the services sector index entering positive territory at 50.5.

Goldman sees three main takeaways from today’s data.

First, we see a potential turning point in Euro area activity, with forward-looking indicators all improving in November, potentially setting a positive stage for the remainder of the year and the beginning of 2024. While the improvement seems to be broad-based, the upside surprises in the manufacturing sector in Germany and the Euro area as a whole may point to early signs of the sector’s revival.

Second, inflationary pressures, after moderating for some time, show signs of renewed intensification in the Euro area, as reflected by the output and input price components ticking up in November.

Third, UK growth momentum was meaningfully better than last month, and is picking up across the board, with the headline and services indices coming in above 50. This, however, is now accompanied by an increase in cost pressures, with both the input and output price indices edging up in November.

Finally, back to the US, S&P Global found that US business uncertainty was also heightened among US firms, as expectations regarding the year-ahead outlook slipped to the weakest since July.

A record 130.7 million people are expected to shop in stores and online in the U.S. on Black Friday this year, the National Retail Federation (NRF) estimates. The event is known for crowds lining up at big-box stores at dawn to scoop up discounted TVs and home appliances.

But at 6 a.m. on Friday at a Walmart in New Milford, Connecticut, the parking lot was only half full.

“It’s a lot quieter this year, a lot quieter,” said shopper Theresa Forsberg, who visits the same five stores with her family at dawn every Black Friday. She was at a nearby Kohl’s (KSS.N) store at 5 a.m.

Fifth Avenue, one of the world’s top shopping streets, is dead quiet on Black Friday — at least by New York’s boisterous standards.

The strip of high-end shops from brands like Louis Vuitton and Cartier has largely recovered since its pandemic lull, where vacancies had once reached nearly 30% in Midtown East. Some vestiges of that struggle remain, with a few empty storefronts covered up or filled with little art installations. Yet the street has managed to keep its title as the most expensive retail area on the planet by rent per square foot, according to Cushman & Wakefield.

Mortgage rates up 163% since 2021, manufacturing PMI in contraction and Black Friday shopping muted. Not good. The Fed is rolling the dice on what to do next.

Even Biden’s press secretary Karine Jean Pierre admitted that all the slogans and hype about Bidenomics is a losing message. The economy is terrible for the middle class and low-wage workers. But excellent for the 1% donor and political elite class. But housing is very important to the middle class … and housing is simply unaffordable.

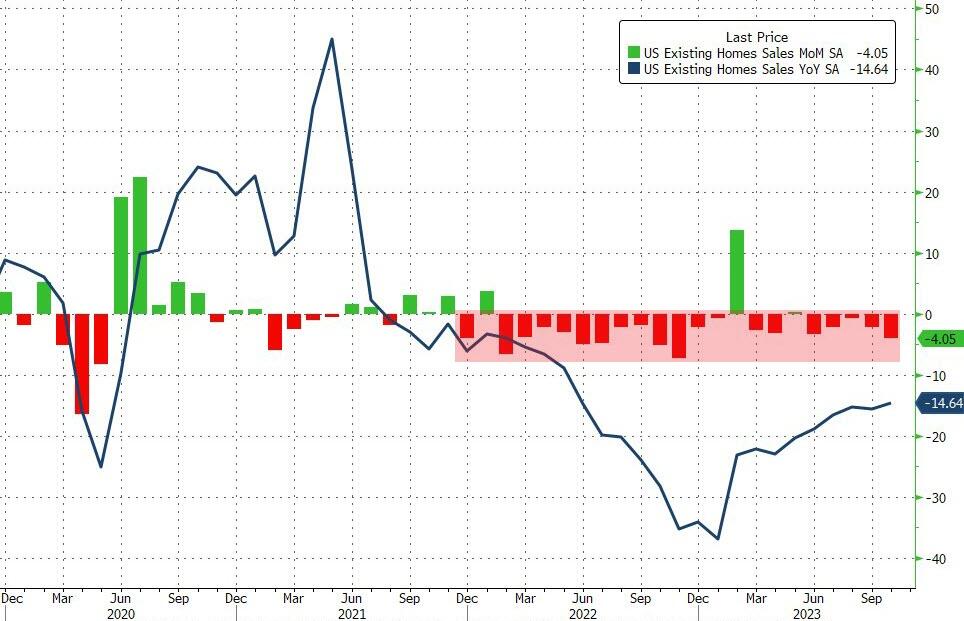

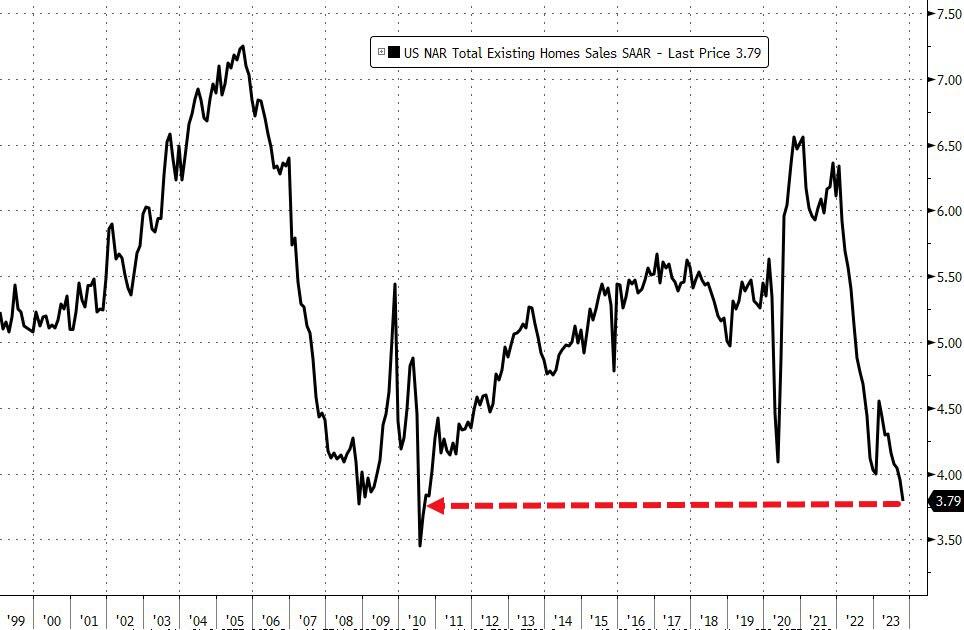

With housing affordability at its lowest since at least the early 1980s, (and homebuilder sentiment slumping as mortgage rates rose), it’s no surprise that analysts expected existing home sales in October to tumble 1.5% MoM.

Sales actually fell 4.1% MoM (far worse than expected and down for the 20th time in the last 23 months) with September’s 2.0% MoM decline revised even lower to -2.2% MoM. That decline left existing home sales down 14.6% YoY.

Source: Bloomberg

The total existing home sales SAAR plunged to 3.79mm – the lowest since the tax credit expired in Aug 2010…

Source: Bloomberg

Sales fell in three of four regions, while they were unchanged in the Midwest. They hit a record low in the West and matched an all-time low in the Northeast

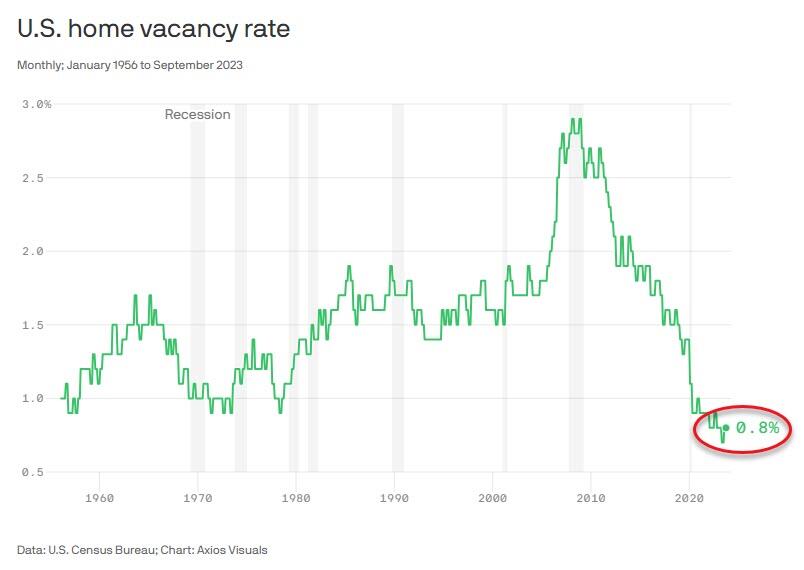

Finally, the percentage of homes that are vacant fell to the lowest level on record in August, and ticked up only slightly in September…

Ever the optimistic,Lawrence Yun, NAR’s chief economist, suggested that:

“Fortunately, mortgage rates have fallen for the third straight week, stirring up buying interest,” adding “though limited now, expect housing inventory to improve after this winter and heading into the spring.”

Good luck with that idea Larry!

Yun added that nearly a third of homes sold above their list price, indicating that multiple offers are still occurring with the median selling price climbed 3.4% from a year earlier to $391,800, the highest for any October in data back to 1999.

Even though the number of homes for sale ticked up from a month earlier to 1.15 million, it’s still the lowest for any October in the series.

Finally, first-time buyers made up a historically low 28% of purchases in October.

After all, the US economy and housing markets are addicted to goverment. (Addicted To Gov!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.