Mortgage applications increased 7.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 8, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 7.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The seasonally adjusted Purchase Index increased 4 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 18 percent lower than the same week one year ago.

The Refinance Index increased 19 percent from the previous week and was 27 percent higher than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) decreased to 7.07 percent from 7.17 percent, with points decreasing to 0.59 from 0.60 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

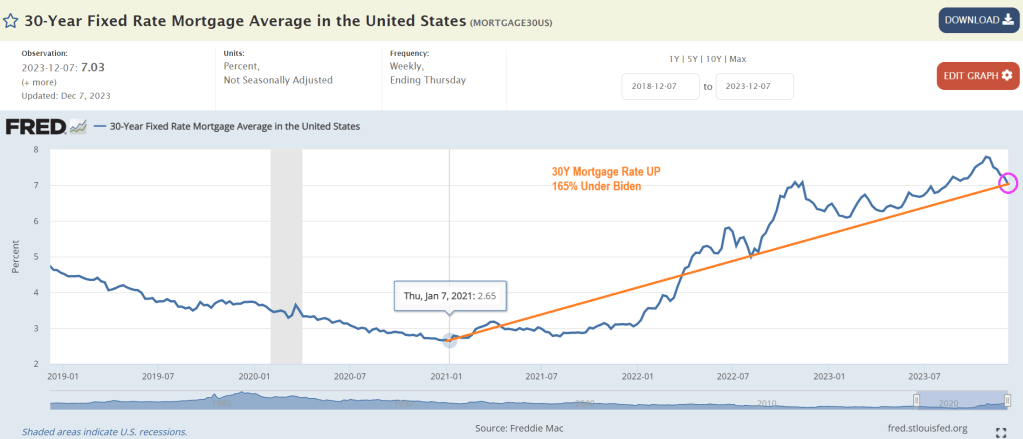

And Freddie Mac’s 30-year mortgage rate is UP 165% under Biden.

Like WEF’s Klaus Schwab, Biden doesn’t want you to have a low rate mortgage for Christmas!

President Gerald For (R-MI) might be best known for his silly attempt at “whip inflation NOW” by having “Music Man” Meredith Wilson write a song: “Whip Inflation Now!” But the second line has been forgotten: “Eat crow instead of cow.” That second line is appropriate for Bidenomics which has left America’s middle class eating crow in the housing market.

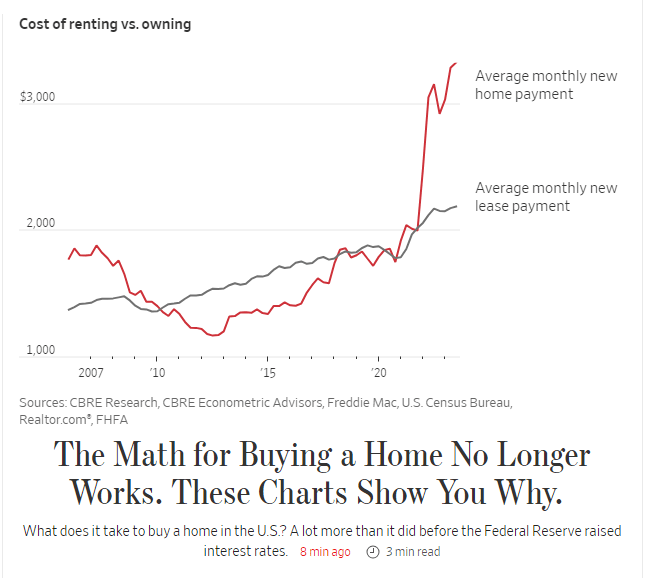

The Wall Street Journal had an interesting piece showing the rise of 30-year fixed rate mortgage payments under Biden where the average monthly new mortgage payment is now $3,222, up from $1,787, up 86%!

The 86% rise in mortgage payments is two fold. First, home prices are up 33.2% under Biden and the 30-year mortgage rate is up 181%.

Yes, Americans are eating crow under the utter failure known as Bidenomics: top down government mandates for massive green energy and other nonsense.

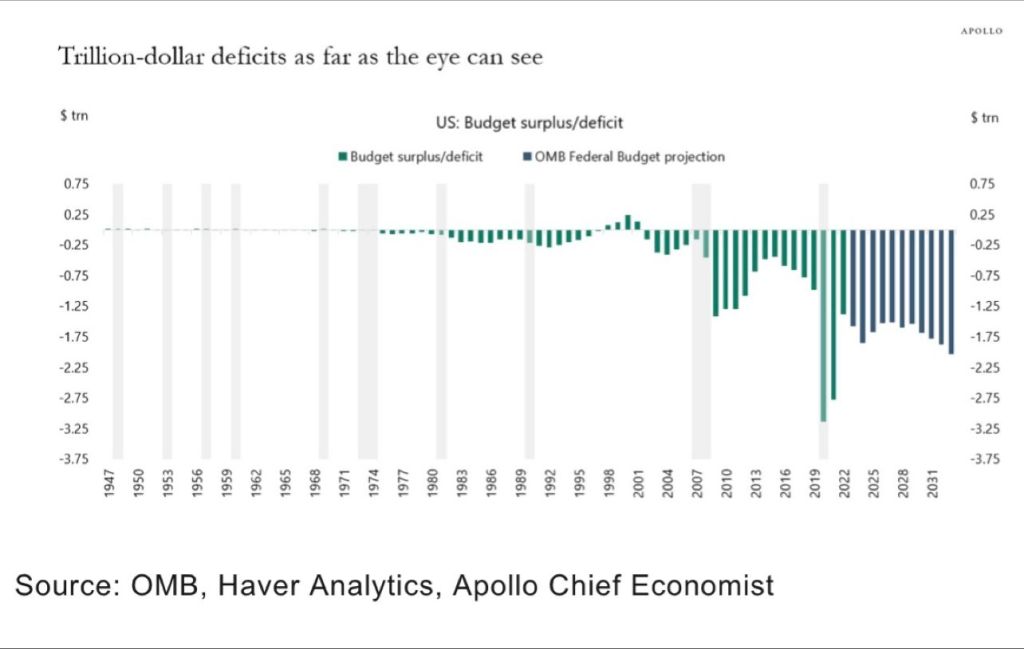

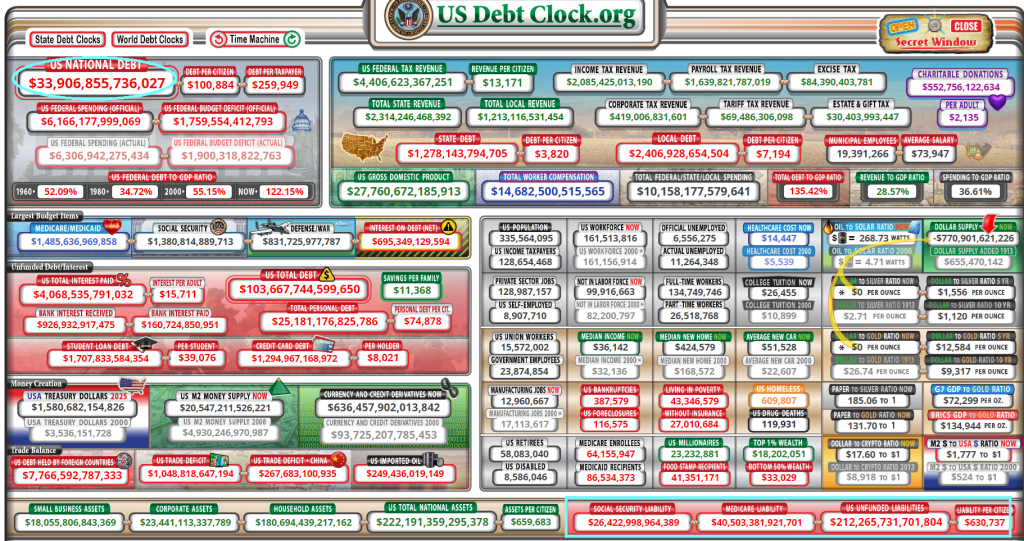

We are on a Highway To Hell! Massive Federal Budget deficits and staggering payments to Treasury from The Fed (losses on balance sheet) and $212 TRILLION in unfunded promises to the non-elites.

Under Modern Monetary Theory (or print money without consequences), we are seeing trillion dollars budget deficits with no end in sight. Nothing has been the same since the financial crisis of 2008 with The Fed’s massive intervention.

Then we have The Fed paying an ever growing amount to US Treasury for losses on their huge balance sheet.

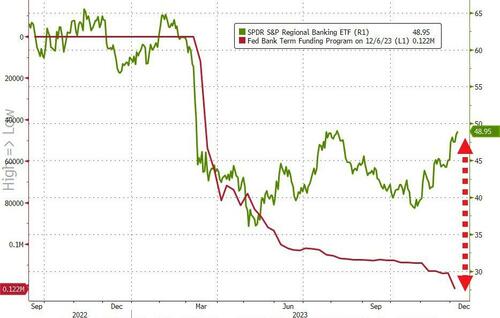

The song “Running on Empty” by Jackson Browne comes to mind when analyzing the state of American banking, especially regional banks.

Yesterday we found out that inflows to money-market funds continue to be huge ($290BN in six weeks), and more importantly, regional banks’ usage of The Fed’s BTFP bailout facility surged to a new record high (even as regional banks surged…

Source: Bloomberg

And so, with that shitshow in mind, we await the glorious manipulation of The Fed’s bank deposits data to reinforce that equity confidence.

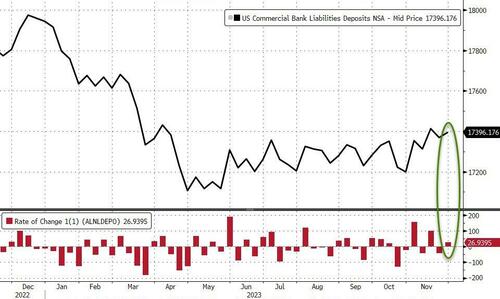

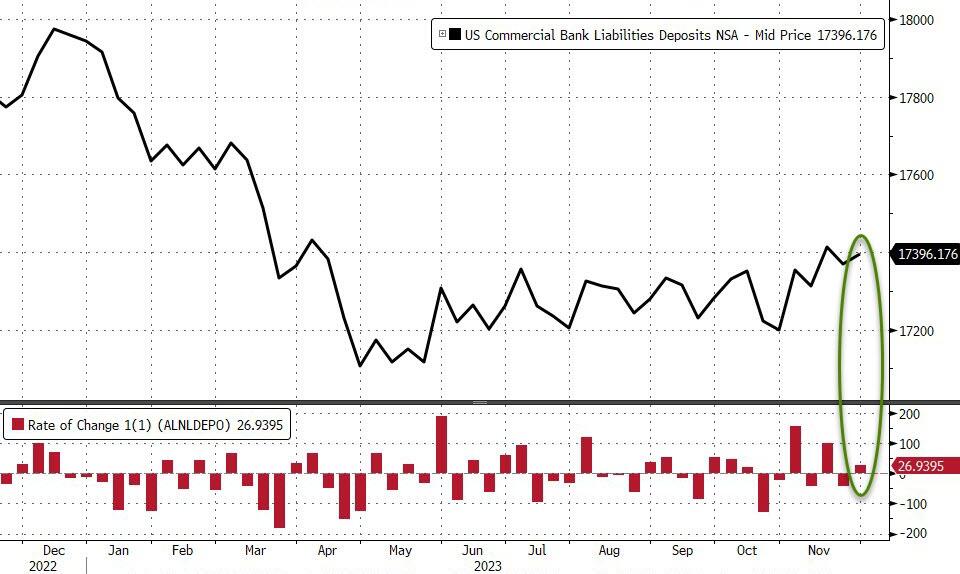

On a seasonally-adjusted basis, banks saw a $53.7BN deposit outflow…

Source: Bloomberg

However, on a non-seasonally-adjusted basis, deposits rose by $27BN…

Source: Bloomberg

And even with the outflows (SA), the divergence between soaring money-market funds and bank deposits continues to widen…

Source: Bloomberg

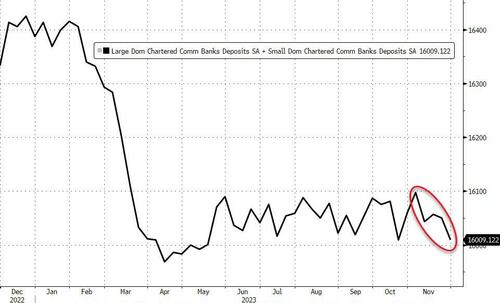

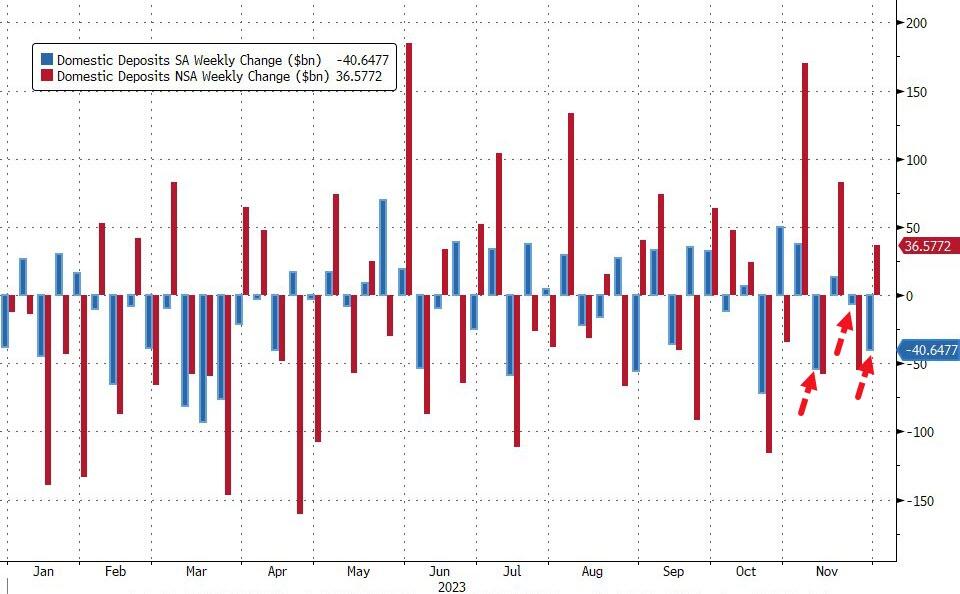

Excluding foreign bank deposits, domestic banks saw the third week of the last four of deposit outflows (-$40.6BN SA) with Large banks -$35BN (SA) and Small banks losing $5.7BN (SA). On an NSA basis, domestic banks saw inflows of $36.5BN last week with Large banks adding $32BN and Small banks adding $4BN…

Source: Bloomberg

That adds up to $88BN (SA) of deposit outflows in the last four weeks (bank to its lowest total since May…

Source: Bloomberg

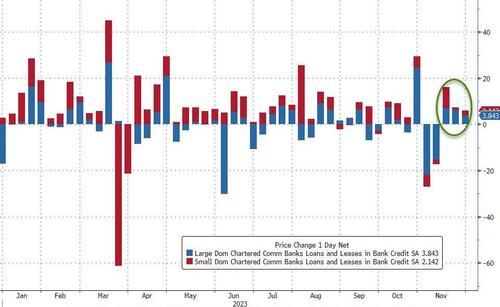

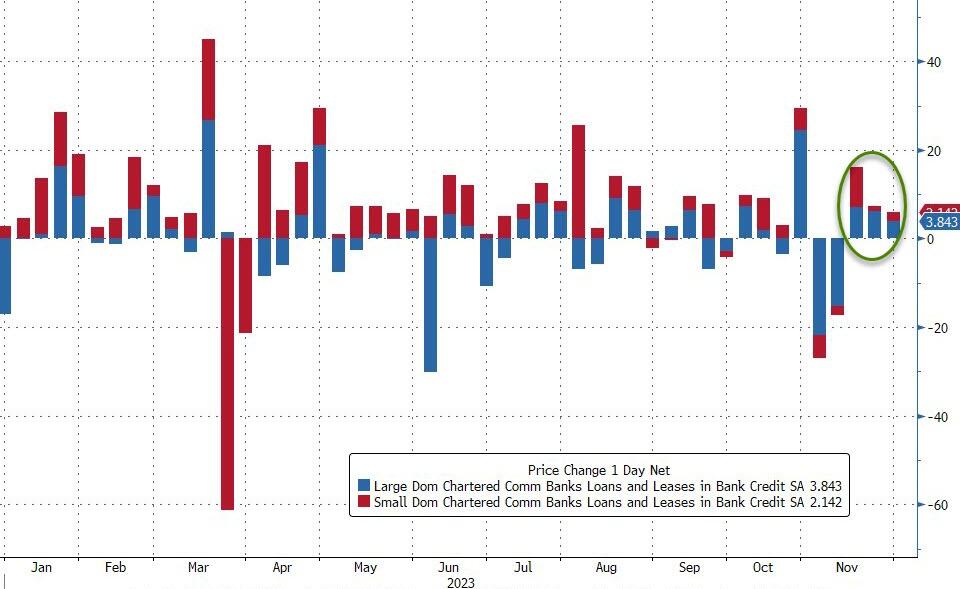

And on the other side of the ledger, despite deposits declining SA, loan volumes increased (SA) for the third week in a row with Small banks adding $2.1BN and Large banks adding $3.8BN…

Source: Bloomberg

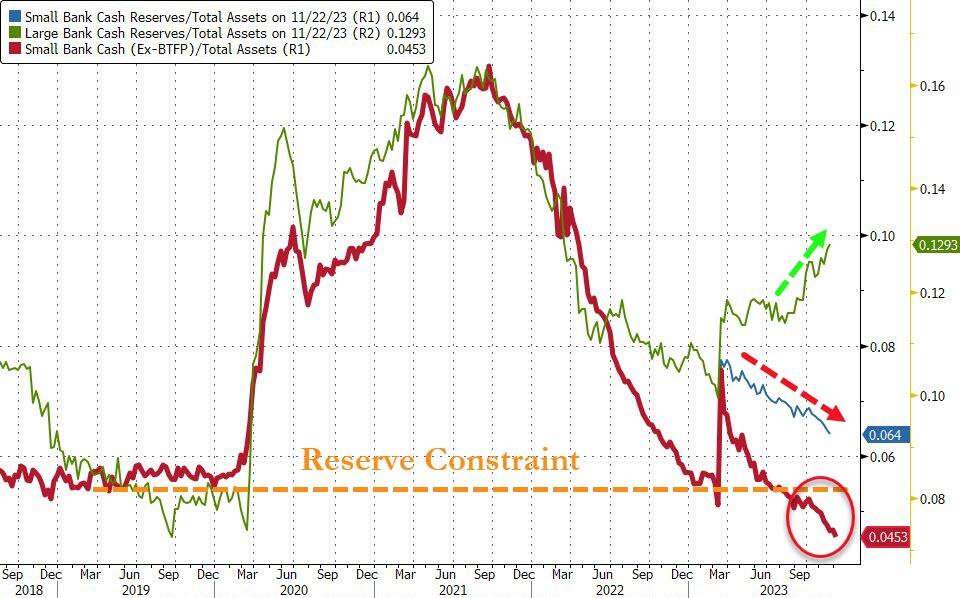

Finally, the key warning sign continues to trend ominously lower (Small Banks’ reserve constraint), supported above the critical level by The Fed’s emergency funds (for now)…

Source: Bloomberg

As the red line shows, without The Fed’s help, the crisis is back (and large bank cash needs a home – green line – like picking up a small bank from the FDIC).

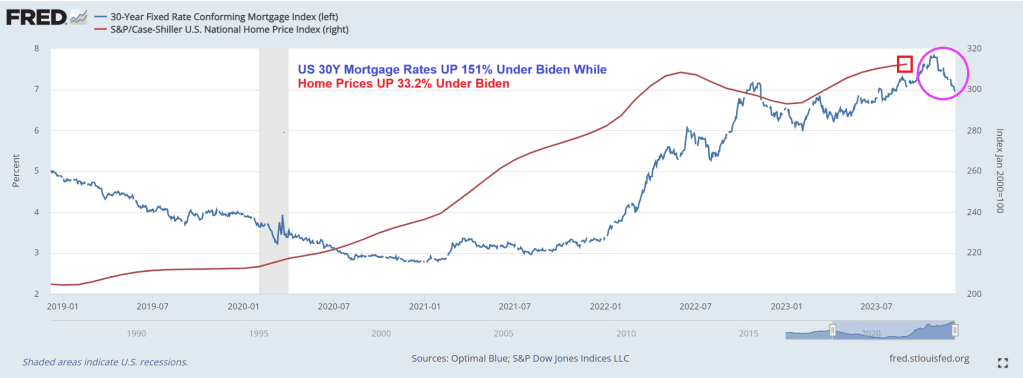

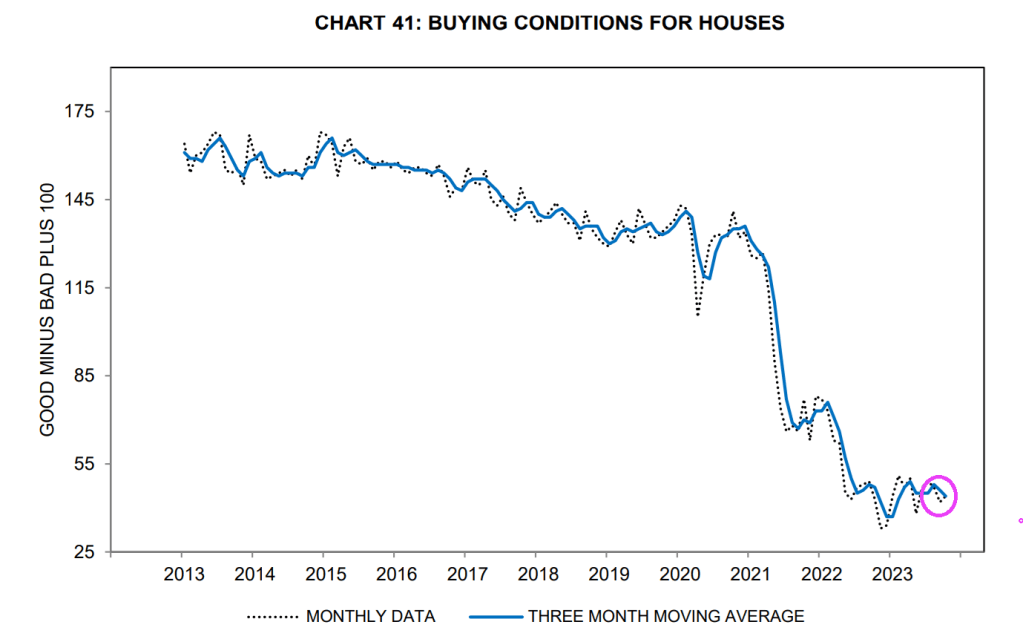

Mortgage rates, despite coming down recently, are still up 151% under Biden. And home prices are up 33.2%. So much for affordable housing for those renting.

So, “Running on Empty” applies to middle class and their ability to afford housing.

Why are buying conditions for houses so low? Well, mortgage rates, despite coming down recently, are still up 151% under Clueless Joe. And home prices are up 33.2% under Biden. So much for affordable housing for those renting.

Like the great Shoeles Joe Jackson on ChiSox and Cleveland Indian fame, Clueless Joe Biden cheated too. Except that Shoeless Joe was accused of accepting $5,000 to throw the World Series in 1919. Clueless Joe Biden and family are accused of accepting over $24 million from China, Ukraine, etc.

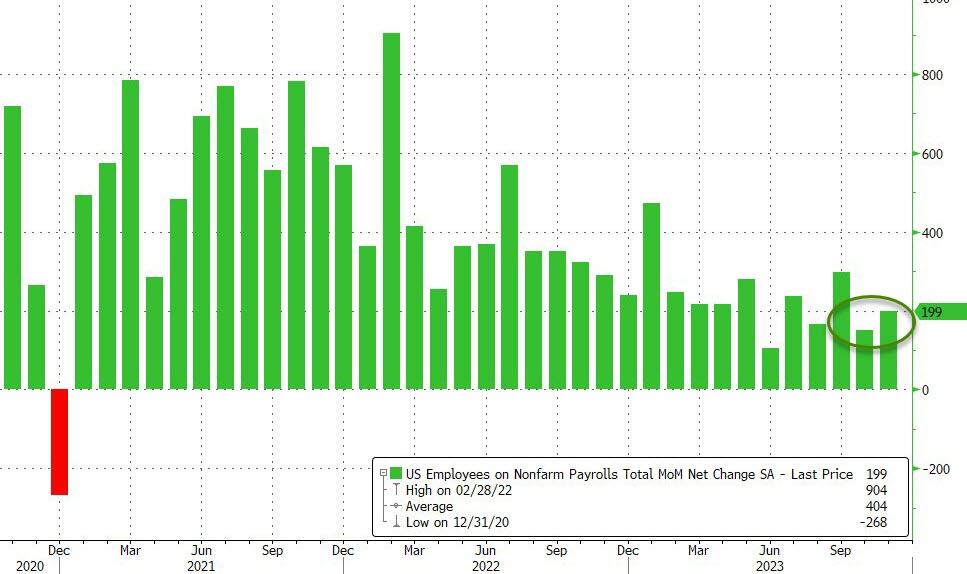

Several talking heads are salivating about the strong or solid jobs report in October. As if The Federal Reserve can’t read the jobs report. I call the report “Government gone wild!” since 51k government jobs were added in October.

Job gains occurred in health care, government, and social assistance. Employment declined in manufacturing due to strike actvity.

Total nonfarm payroll employment increased by 150,000 in October, below the average monthly gain of 258,000 over the prior 12 months. In October, job gains occurred in health care, government, and social assistance. Employment in manufacturing declined due to strike activity. (See table B-1.) Health care added 58,000 jobs in October, in line with the average monthly gain of 53,000 over the prior 12 months. Over the month, employment continued to trend up in ambulatory health care services (+32,000), hospitals (+18,000), and nursing and residential care facilities (+8,000). Employment in government increased by 51,000 in October and has returned to its pre-pandemic February 2020 level. Monthly job growth in government had averaged 50,000 in the prior 12 months. In October, employment continued to trend up in local government (+38,000). Social assistance added 19,000 jobs in October, compared with the average monthly gain of 23,000 over the prior 12 months. Over the month, employment continued to trend up in individual and family services (+14,000). In October, construction employment continued to trend up (+23,000), about in line with the average monthly gain of 18,000 over the prior 12 months. Employment continued to trend up over the month in specialty trade contractors (+14,000) and construction of buildings (+6,000). Employment in manufacturing decreased by 35,000 in October, reflecting a decline of 33,000 in motor vehicles and parts that was largely due to strike activity. In October, employment in leisure and hospitality changed little (+19,000). The industry had added an average of 52,000 jobs per month over the prior 12 months. Employment in professional and business services was little changed in October (+15,000) and has shown little net change since May.

Speaking of Govzilla, my favorite quote showing the stupidity of BIG government is … Biden’s climate envoy John Kerry. “We’ve got to cut down on farming due to ‘Climate Change’…or people are going to starve…”

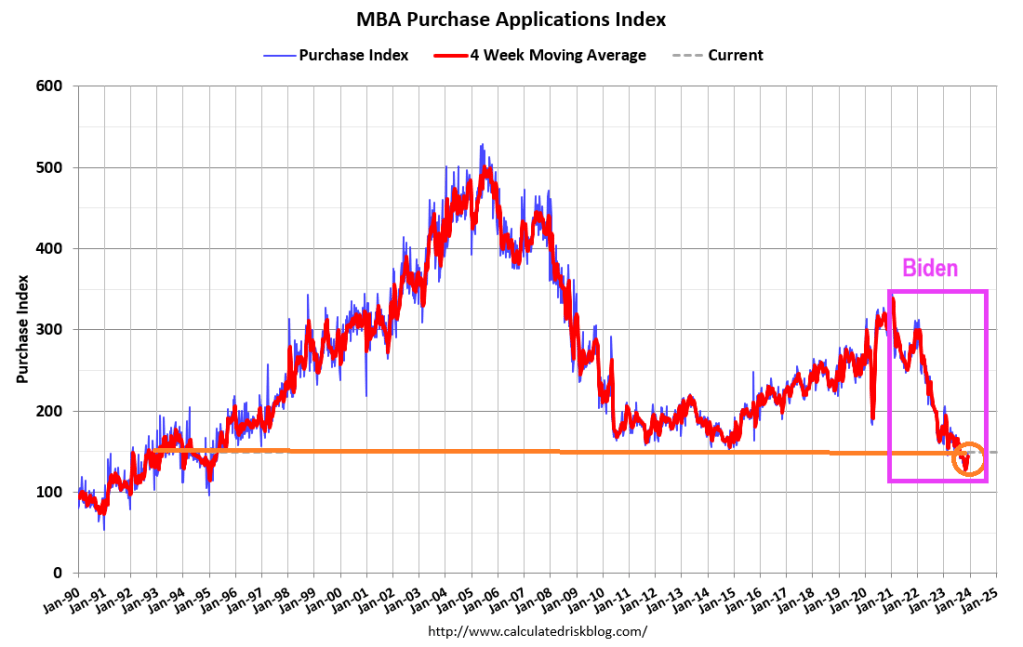

While the exciting headline is “Mortgage Purchase Demand rises 35%!” bear in mind that the level of mortgage purchase demand is still relatively low. This is volatility in mortgage applications.

Mortgage applications increased 2.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 1, 2023. Last week’s results include an adjustment for the observance of the Thanksgiving holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 43 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 0.3 percent from one week earlier. The unadjusted Purchase Index increased 35 percent compared with the previous week and was 17 percent lower than the same week one year ago.

The Refinance Index increased 14 percent from the previous week and was 10 percent higher than the same week one year ago. Mortgage rates declined last week, with the 30-year fixed-rate mortgage falling to 7.17 percent – the lowest level since August 2023.

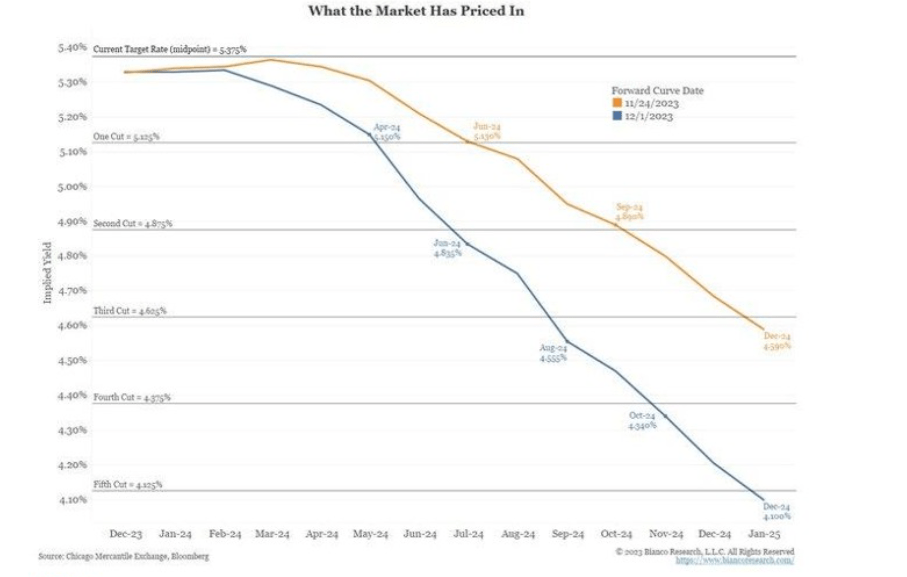

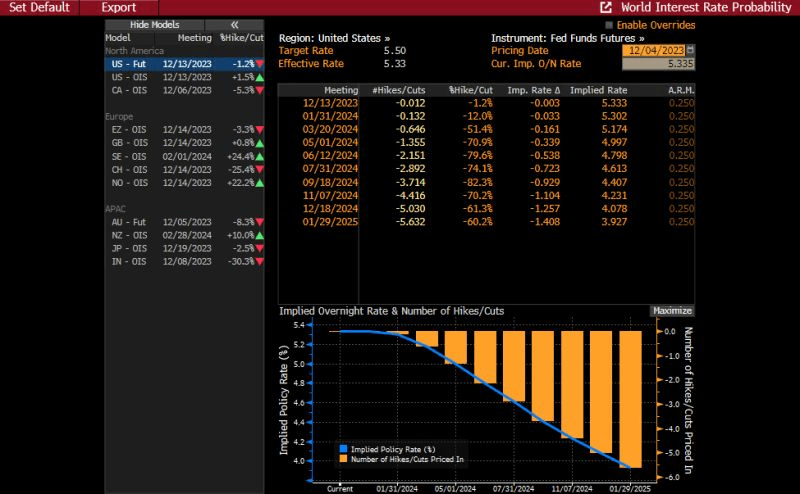

And with 5 rate cuts priced in, we should see mortgage demand increasing in 2024.

On the hotness front, here are the 10 smokin’ housing markets. Strange that the hotness score is highest for generally depressed economic cities like Manchester NH, Rochester NY and Rockford IL. Hey, at least Columbus Ohio made the top 10 on the hotness list!

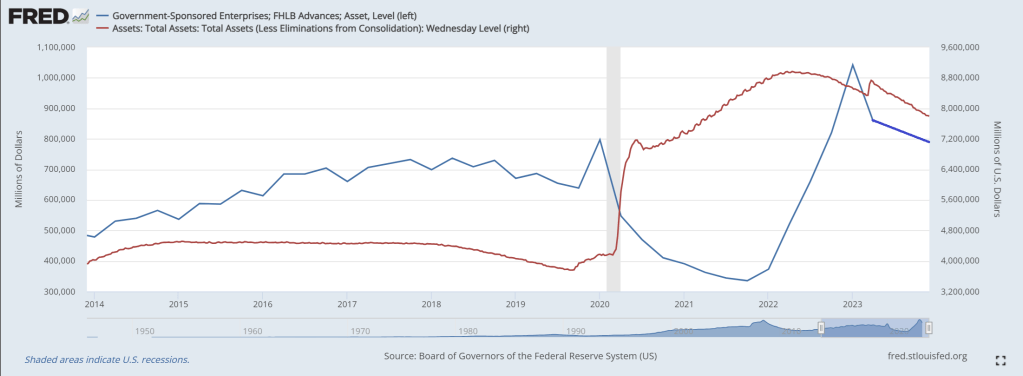

The Federal Home Loan Bank System (comprised of Federal Home Loan Banks or FLUBs) are a major source of American home loans and liquidity … at least until now.

According to a recently released report, the Federal Housing Finance Agency (FHFA) plans to propose rules that would curtail US banks’ borrowings from the Federal Home Loan Banks (FHLBs) to ensure they are not used as a “lender of last resort.” The announcement comes after the liquidity crunch in March spurred several banks to tap into the FHLB system, sending FHLB advances to a three-year high in the first quarter. During that quarter, when two large regional banks failed, FHLB advances totaled $804.39 billion, comprising 3.7% of banks’ total liabilities.

While totals have fallen since then, sitting at $602.62 billion, or 2.8% of total liabilities, in the third quarter, the FHFA is still seeking to impose limitations. Should the agency enact the new rules, banks’ liquidity options would be hindered. The FHFA wants Federal Reserve facilities to be used instead, but banks are reluctant to tap those because of the stigma attached to those sources, industry experts said.

“It is fair to argue that some banks have come to rely on FHLB funding as a crutch, and the ramp in lending to struggling banks during the mini-crisis in March is an area of continued debate,” Isaac Boltansky and Isabel Bandoroff of BTIG LLC wrote in a Nov. 11 note. “With that being said, there is still a clear stigma associated with tapping the Fed’s Discount Window and other facilities, which should be part of the conversation if the FHLB support will eventually be curtailed.”

Among the various rules the FHFA plans to propose is requiring that certain members have at least 10% of their assets in residential mortgage loans or equivalent mission assets, including assets that qualify as Community Financial Institution collateral, on an ongoing basis in order to stay eligible for FHLB financing.

The leading FLUB borrower? Columbus Ohio’s own JP Morgan Chase!

The problem is that bank credit growth has been contracting for several weeks now. 18th straight week of negative credit growth.

As FLUB advances decline with Fed balance sheet shrinkage.

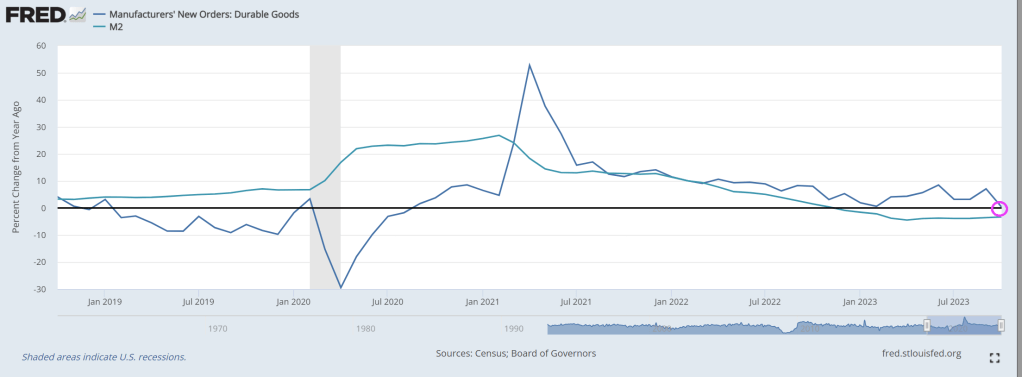

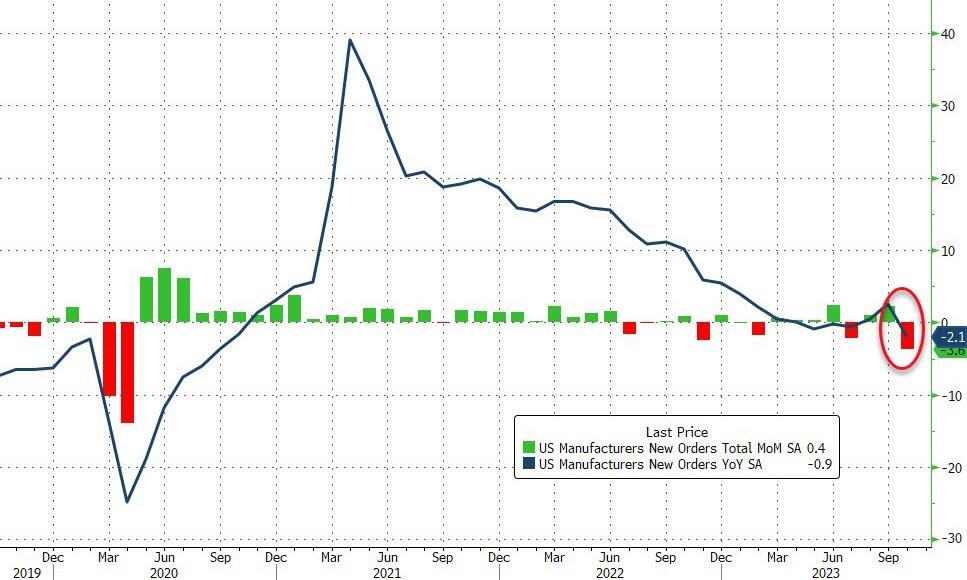

Factory orders tumbled even more than expected, down 3.6% MoM – the biggest drop since the COVID lockdowns (April 2020). September was also revised lower (making October’s decline even worse) from +2.8% MoM to +2.3% MoM…

Source: Bloomberg

The big monthly decline and revisions dragged orders down 2.1% YoY (the biggest drop since Sept 2020).

Core factory orders also dropped (-1.2% Mom), leaving them down 2.2% YoY – the eight month in a row of annual declines…

Source: Bloomberg

The final Durable Goods Orders data for October confirmed the preliminary print plunge down 5.4% MoM.

Finally, we note that it could have been a lot worse as Defense spending shot up 24.7% MoM (as non-defense dropped 15.8% MoM0…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.