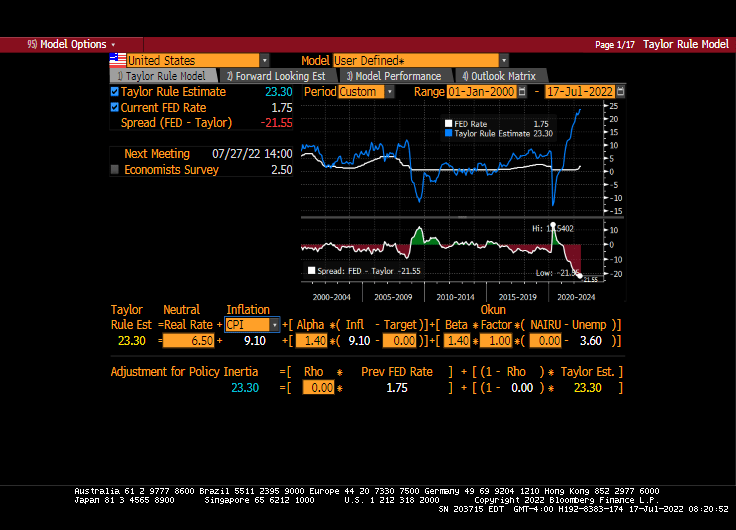

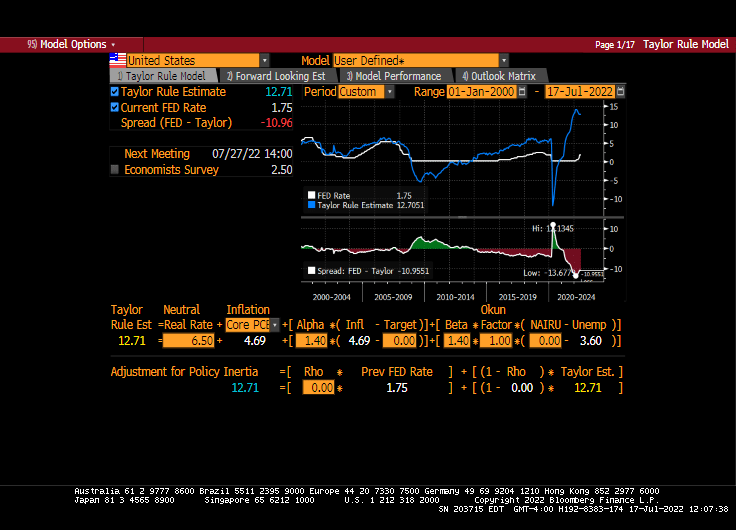

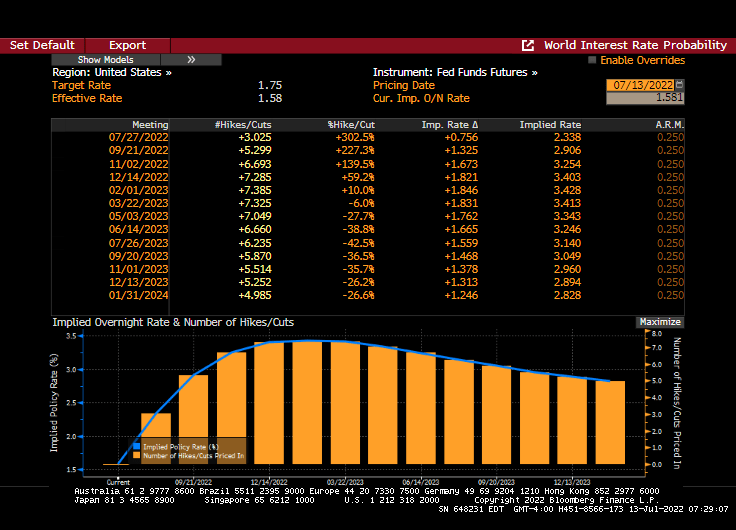

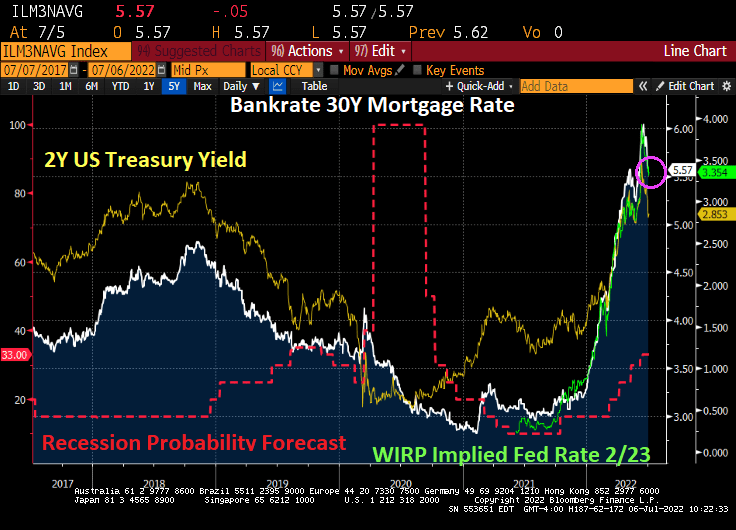

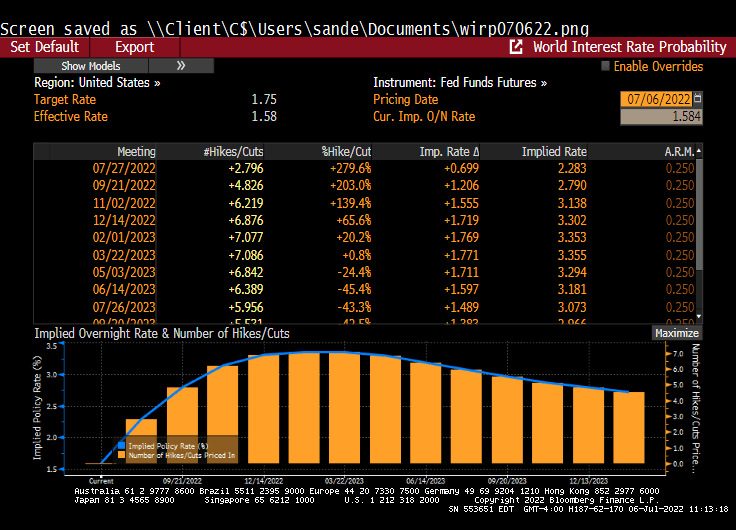

Hold on, The Fed is coming! To raise their target rate by 75 basis points at Wednesday’s FOMC meeting. Will this stem the tide of rising inflation?

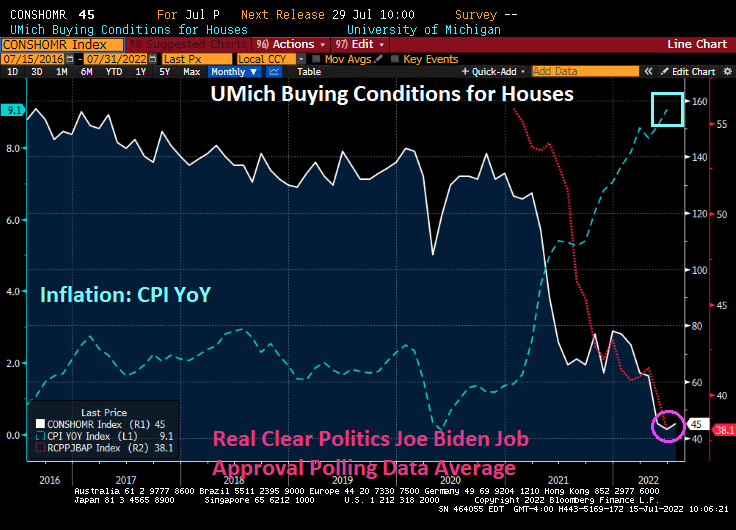

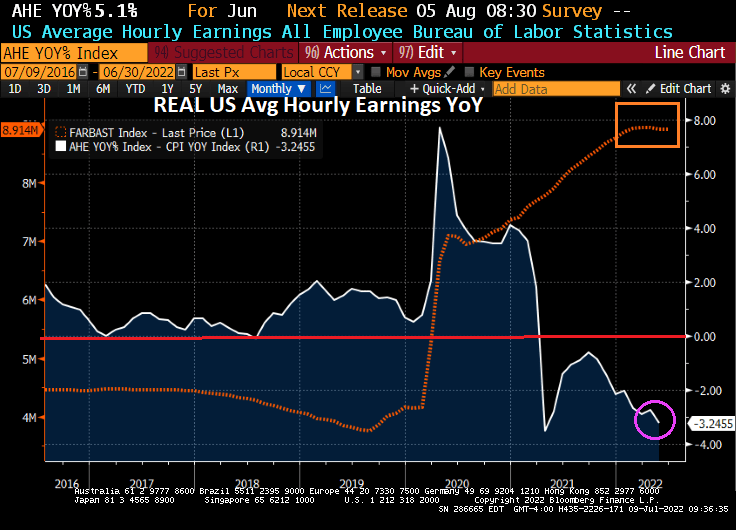

Under Biden, we have seen regular gasoline prices rise 82% despite recent declines. Diesel fuel is up 121% and foodstuffs are up 46%. And house rents keep rising at a staggering 14.75% YoY. The recent declines is more due to the global economic slowdown and central bank rate increases than anything Washington DC is doing.

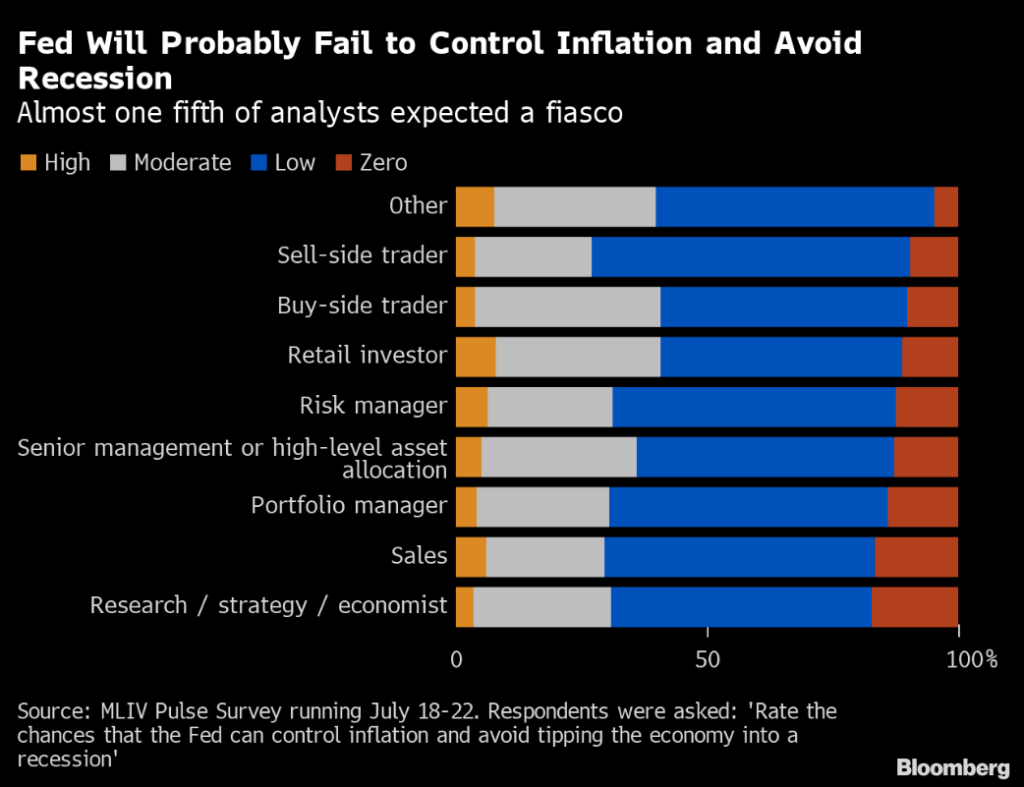

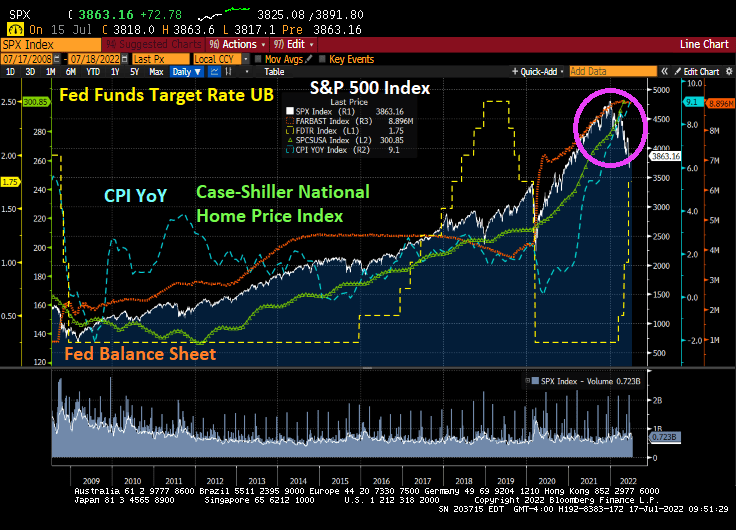

(Bloomberg) Investors are skeptical that the Federal Reserve can tame the worst inflation in four decades without driving the economy into a recession.

That’s bad news for Americans, who face the prospect of a downturn as their bills for food, rent and fuel swell. But to bond investors hit by deep losses this year, it may mean any further pain will be short-lived, as a recession will spark the US central bank to cut rates next year. That’s according to the results of the latest MLIV Pulse survey.

Over 60% of 1,343 respondents in the survey said there’s a low or zero probability that the US central bank can rein in consumer-price pressures without causing an economic contraction. The survey was conducted July 18-22 and included retail and professional investors.

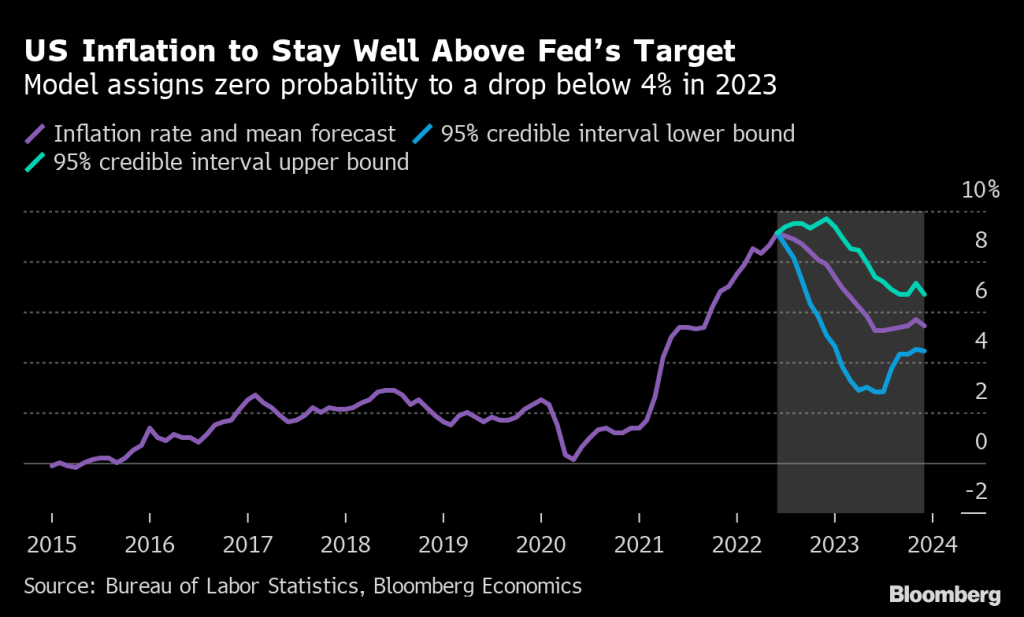

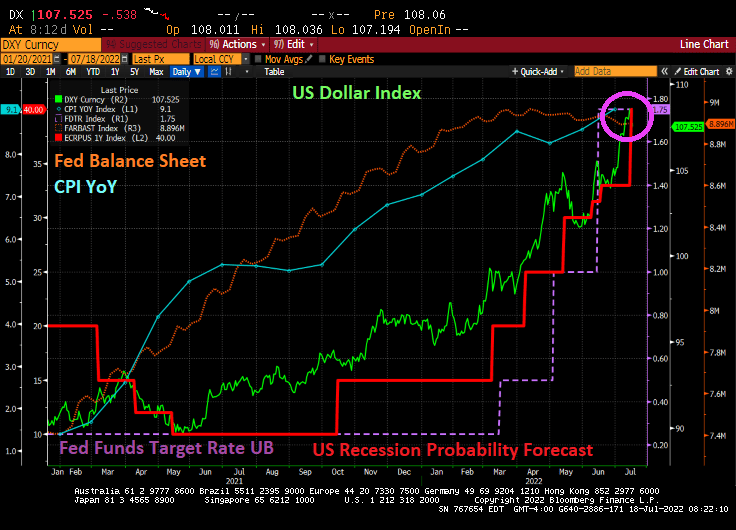

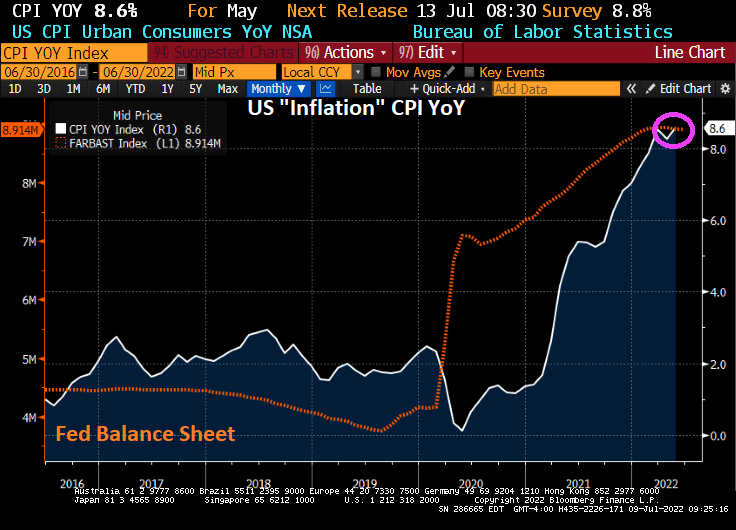

US inflation may be close to a peak, but it’s very likely to stay above 8% through year-end. Bloomberg Economics’ model assigns zero probability to a drop below 4% in 2023. Taken together with increasing recession risks, the Fed faces a tough balancing act as it attempts to bring stubborn price pressures under control without tipping the economy into contraction.

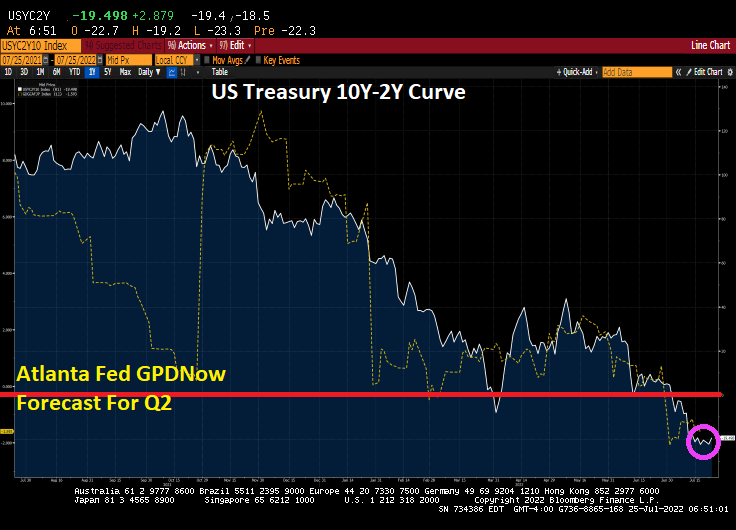

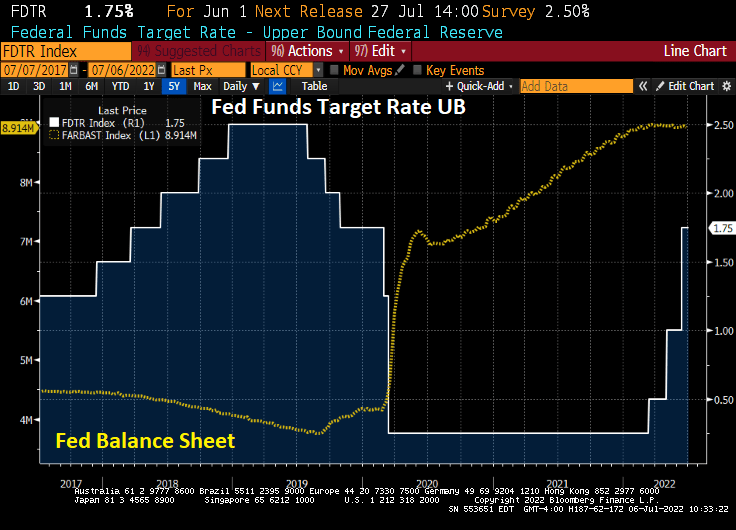

Of course, The Federal Reserve doesn’t really consider energy or food inflation, which are typically higher than core inflation. But going into Wednesday’s meeting, we see the US Treasury 10Y-2Y curve remains inverted (a signal of impending recession) and the Atlanta Fed GDPNow Q2 tracker at -1.6% after a negative Q1 reading.

Will raising the target rate (or ACTUALLY shrinking their balance sheet) reduce inflation? We shall see, but it has got to be better than Lawrence Summer’s suggestion to reduce inflation: raise taxes. Wait a minute, Larry. Inflation was caused by 1) overstimulus by The Fed combined with 2) massive Covid spending by Biden, Pelosi, Schumer and 3) Biden’s anti-fossil fuel policies. So instead of suggesting a decrease in Federal spending, Summer’s wants to give MORE of your money to Biden and Congress to spend. What an unbelievable nitwit.

Here is a picture of Larry Summers, Jay Powell and Janet Yellen attending the FOMC meeting in Washington DC.

You must be logged in to post a comment.