Biden’s economy and mortgage market are like a bad wine hangover. Thanks to inflation and The Fed’s tightening to fight inflation, mortgage purchase demand is down a staggering -42.4% since April 2021.

Mortgage applications decreased 5.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 12, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 5.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 6 percent compared with the previous week. The Refinance Index decreased 8 percent from the previous week and was 43 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 4.8 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 26 percent lower than the same week one year ago.

I used to think that The Kabuki Theater surrounding the raising of the US debt limit and passing a Federal budget would be over by now. But since Biden is being controlled by the hard left “Progressives” in Washington DC, he may be reckless enough to let the US default just so he can blame Republicans. And with our useless and deeply-biased main street media (MSM) just repeating Democrat talking points blaming Republicans, we may actually see a US debt default.

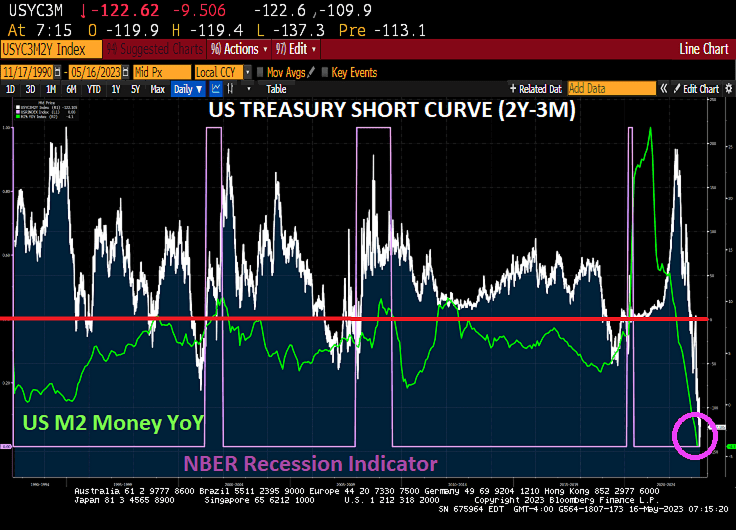

So while Yellen is warning that time is running out, notice she never encourage Blaming Biden to negotiate his insane budget downwards, we see a deeply inverted US Treasury short curve (2Y-3M).

(Bloomberg) Treasury Secretary Janet Yellen warned that “time is running out” to avert an economic catastrophe from failing to raise the debt ceiling, in remarks released as President Joe Biden and congressional leaders prepared to meet on the standoff.

Speaker Kevin McCarthy issued his own notice Monday evening ahead of Tuesday’s 3 p.m. gathering, saying, “We only have so many days left to deal with this.”

The two sides showed little signs of agreeing on much else other than the countdown in the runup to the second White House encounter on the debt ceiling in two weeks. While senior staff have been negotiating for days, Republicans are still pressing for sweeping spending cuts, while Democrats are determined to protect the president’s legislative achievements.

“We are already seeing the impacts of brinksmanship: investors have become more reluctant to hold government debt that matures in early June,” Yellen said in remarks prepared for delivery to a banking conference on Tuesday. “The impasse has already increased the debt burden to American taxpayers.”

The Treasury chief issued a fresh letter to congressional leaders Monday restating that the Treasury risks running out of sufficient cash for all federal obligations as soon as June 1. The livelihoods of millions of Americans “hang in the balance,” she said in excerpts of her speech to the Independent Community Bankers of America Capital Summit released by the Treasury.

There is the evil Hobbit! Sending a letter to Congress essentially blaming McCarthy for the fiasco when Biden could downsize his budget request to reasonable levels. But Yellen is an authoritarian Statist, not a free market type.

I wish Biden would spend more time trying to negotiate with McCarthy to end the debt crisis rather than stir up race hatred like he did at Howard University graduation. C’mon Joe! White “supremacy” is not the most dangerous terrorist threat. I would actually say that Biden, Yellen and Schumer (throw in Pelosi’s spending splurge as Speaker) are the biggest terrorist threat. They are the 4 horsemen of the US debt apocalypse.

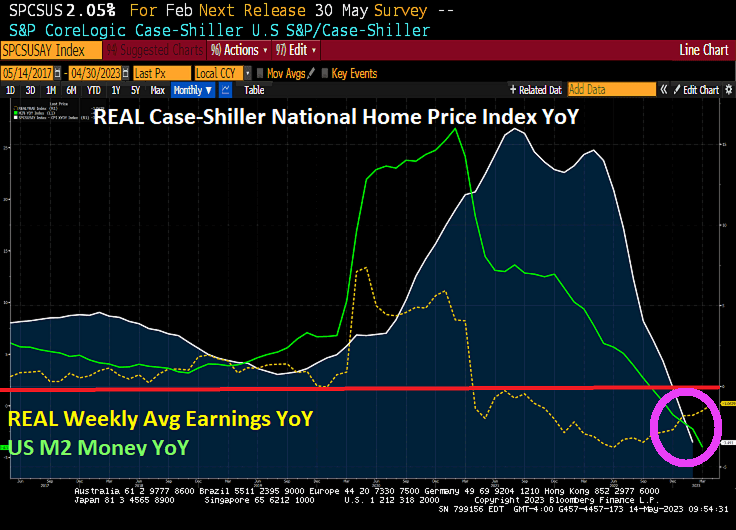

Let’s see how Bidenflation (caused by staggering Federal misspending) and years of Yellen’s TLTL (too low too long) monetary policy has caused a massive dislocation in the housing market.

The February Case-Shiller National home price index less core inflation (CPI less food and energy) year-over-year is declining by -3.5%. This is happening as REAL average weekly earnings growth is at -1.06% YoY and has been negative growth for 25 straigth months.

Look at The Fed’s massive overreaction to the unnecessary government shutdowns of economies and schools. It really sent home price growth soaring, then when The Fed starts slowing the monetary stimulus, we get the largest slowdown of REAL home price growth since 2012.

The 4 Horsemen of the US Debt Apocalypse. I would add Mitch McConnell and Fed Chair Powell, but then would have an entire Cavalry company like George Armstrong Custer had at Little Big Horn.

Another dismal economic report under “Middle class” Joe Biden.

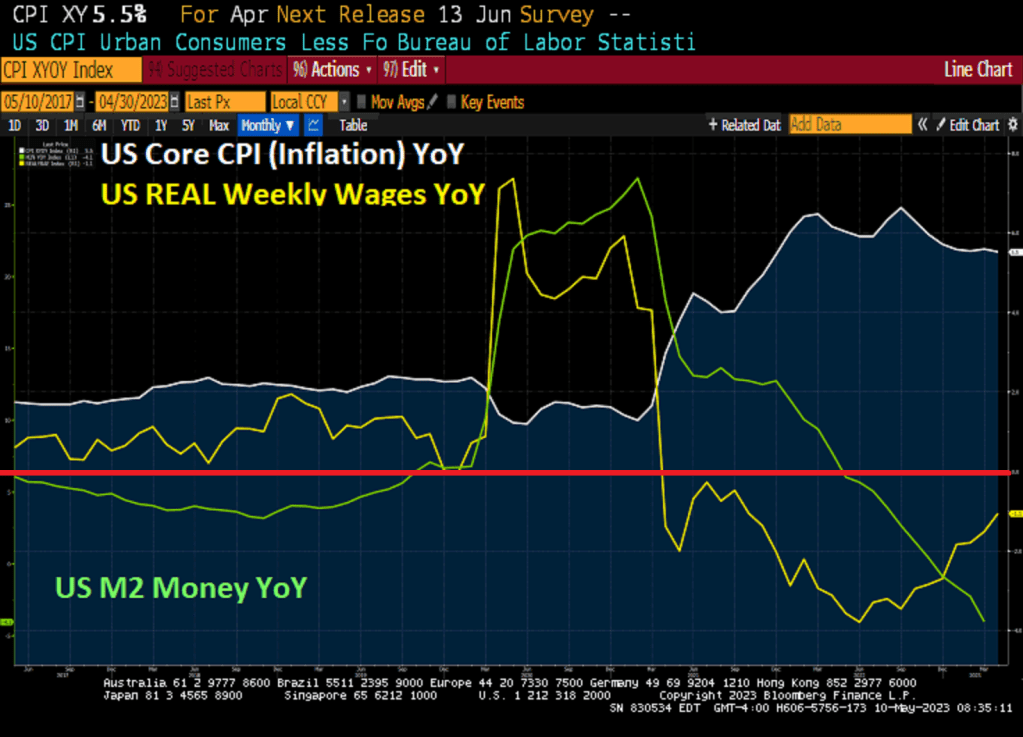

April’s inflation report is out and … it sucks. Core inflation (CPI less food and energy) remains elevated at 5.5% YoY, much higher than The Fed’s target rate of 2%. Even worse, US REAL average weekly wage growth is negative again at -1.1% YoY, negative growth for the 25th straight month.

Turns out that core inflation is higher than overall inflation. 4.9% YoY compared to core of 5.5% YoY.

Despite the hot core inflation report, Fed Funds Futures are pointing to declining rates over time.

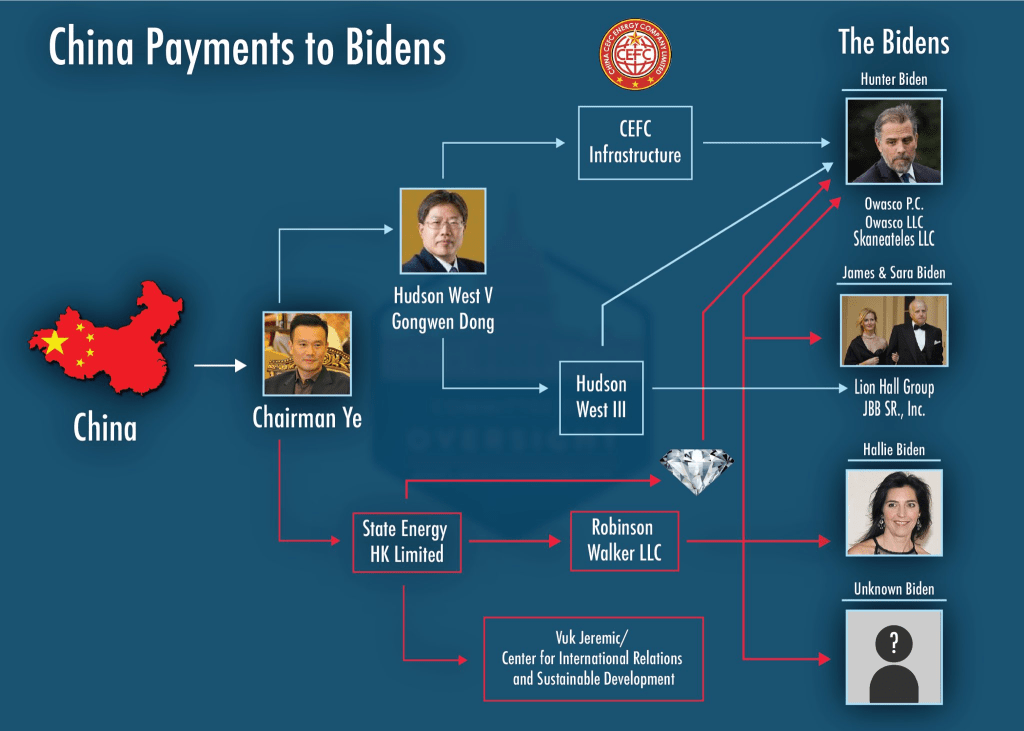

While the US middle class is getting screwed, The Biden family are raking in millions …. from China.

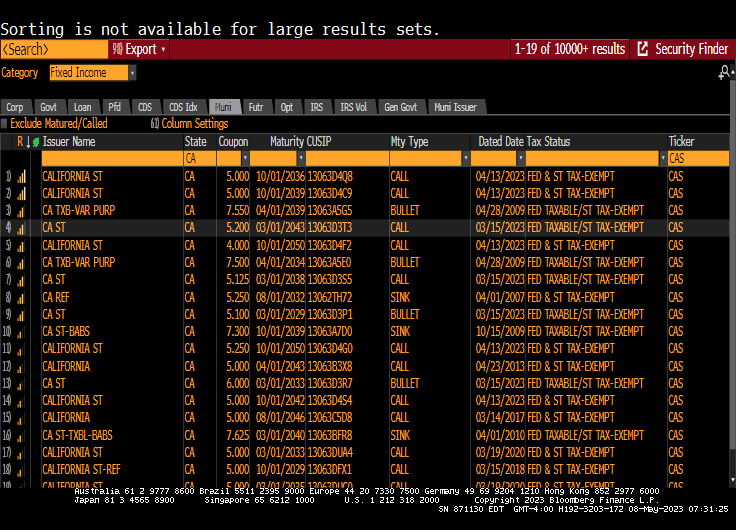

California just did what Slow Joe Biden and Senate Majority Leader Chuckles Schumer are threatening to do. Biden and Schumer still refuse to negotiate (allegedly) sending the US Federal government careening towards a staggering debt default. The source of both California and US Federal government fiscal problems? Out of control government spending, aka, government gone wild!

In any case, California borrowed approximately $20 billion from the federal government to cover unemployment benefits during the pandemic, and with Gov. Gavin Newsom’s recent decision to not pay it back, employers are now saddled with the expense, according to experts.

“The state should have taken care of the loans with the COVID money it received from the government in 2021,” Marc Joffe, policy analyst at the Cato Institute—a public policy think tank headquartered in Washington, D.C.—told The Epoch Times.

In the proposed 2023–2024 budget, $750 million was allocated to start paying down the loans, but Newsom made changes to the plan in January and withdrew the funding.

The Epoch Times’ request for comment from Newsom’s office was not returned on deadline.

The decision leaves businesses in the state responsible for the loans—as mandated by federal regulations—so the federal unemployment tax rate of .6 percent is set to increase by .3 percent annually, starting in 2023, until the loan is extinguished.

“California is just not really an employer-friendly state,” Joffe said. “This one thing will not be a difference between a business remaining open or closing, but it’s just another burden on top of the many burdens the state puts on employers.”

Twenty-two states borrowed money for unemployment insurance from the federal government during the pandemic, with all but four—California, Colorado, Connecticut, and New York—paying back their debts.

California owes the most, by far, with approximately $18.6 billion outstanding as of May 2, followed by New York’s $8 billion, Connecticut’s $187 million, and Colorado’s $77 million, according to U.S. Treasury Department data.

The discrepancy in amounts borrowed and owed by states lies in the different approaches to managing the pandemic, with California’s stricter lockdown causing unemployment to remain higher and longer, according to experts

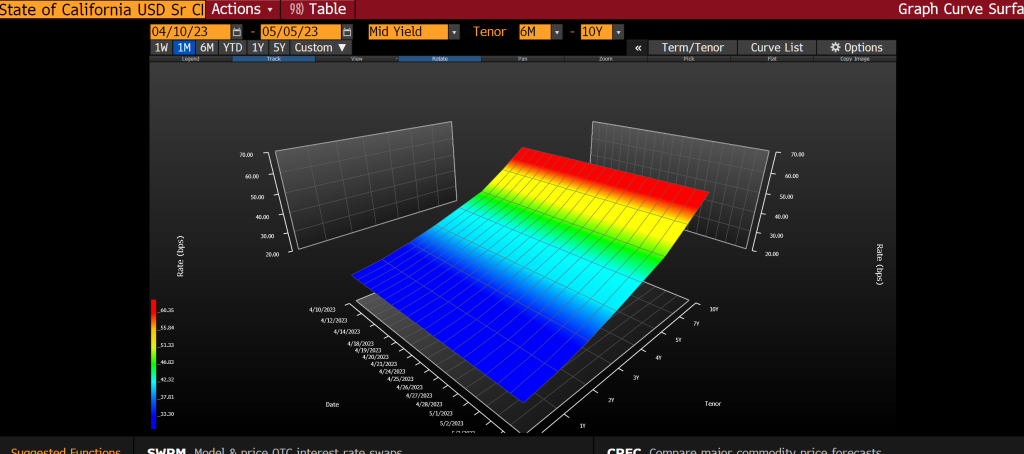

And CA CDS 1Y is tame (only 31), the CDS curve over a longer time frame looks miserable.

Now, Gruesome Newsom only default on Covid-related loans. The California municipal bond market is huge and CA has defaulted on those loans …. yet.

Speaking of insane fiscal “management,” a repartations plan in California could cost billions.

California’s reparations task force, which first convened nearly two years ago, has given the final approval to a list of recommendations on how the state may compensate and apologize to Black residents for historical discrimination. “Reparations are not only morally justifiable, but they have the potential to address long standing racial disparities and inequalities,” Representative Barbara Lee (D-CA) said during a weekend meeting. The proposals now go to state lawmakers to consider reparations legislation and a final sum, which some economists could cost the state upwards of $800B, or almost 3x the state’s annual budget.

To be initially eligible, applicants must be a descendant of Black people who were in the country by the end of the 19th century, thouqh there are not yet details on how the payments would be funded. Age, state residence, and other factors will also play a role in determining compensation.

There is the rub – how does California finance the reparations? Raise taxes (unfair to people who never did anything wrong to blacks)? Borrow billions? Given that Newsom just defaulted on loans to California might mean that there will be relucatance to lend CA billions more.

CA Governor Gavin “Slick” Newsom. The Defaulter In Chief of California.

Ok, it is well-known that Biden was the stupidest man in the US Senate. And with Washington’s Patty Murray in the Senate, that is quite an accomplishment.

But Biden is President and is still stupid and spiraling down the dementia rabbit hole. He is blaming Republicans for their budget proposal to end the debt ceiling crisis despite saying previously that he would negotitate. Apparently, Biden’s puppet masters are telling him to risk default by playing the blame game.

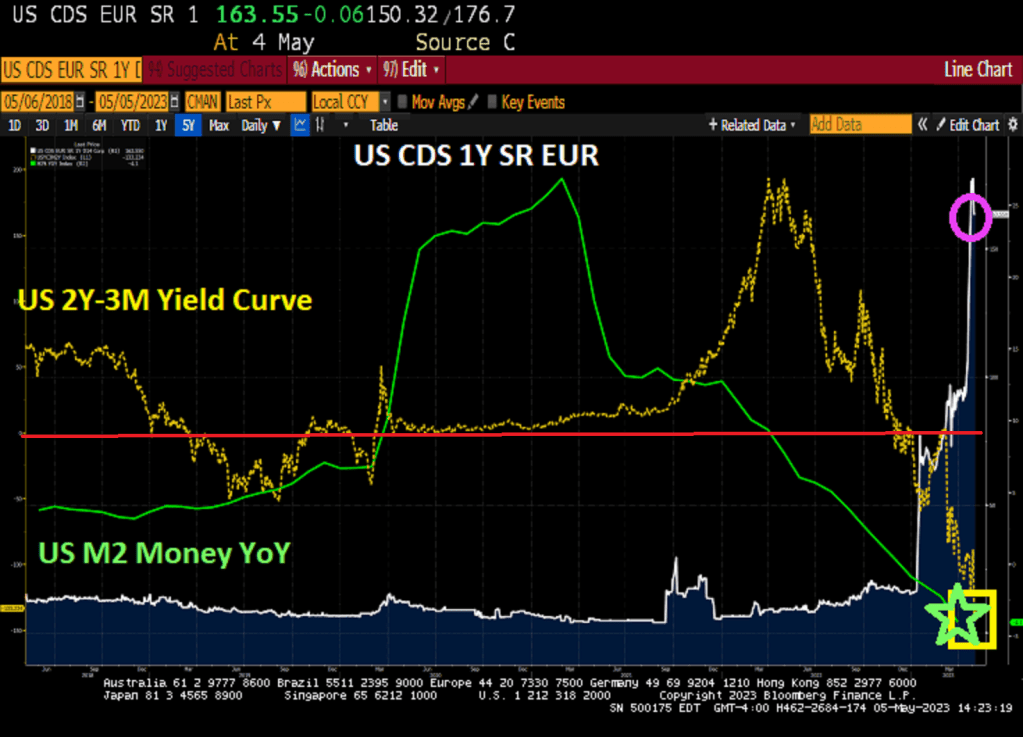

So, US credit default swap (CDS 1Y, SR, EURO) price remains elevated which indicates that Biden, Yellen and Schumer may actually default on US debt.

As M2 Money growth crashes and burns, the US Treasury 2Y-3M yield curve inverts to lowest in history.

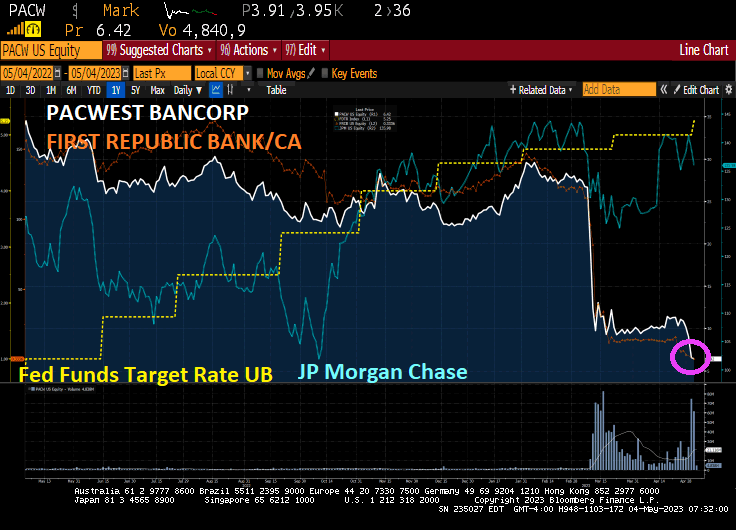

As Connor MacLeod said in the film Highlander, “There can only be one!” The US banking system under Joe Biden’s Reign of Error is like the film Highlander: apparently, there can only be one bank. And it is likely JP Morgan Chase.

Take the JP Morgan Chase (JPMC) acquisition of First Republic Bank:

In Acquiring First Republic Bank, JP Morgan Has:

Bypassed laws against acquiring bank while controlling 10%+ of US deposits

Shared $13 billion in losses with the FDIC

Received a $50 billion loan from the FDIC

Effectively bought back its own deposits

Expects to profit $5 billion+ over the next 5 years

This crisis has taught us that rules don’t matter in times of panic, particularly to regulators.

And now we have PacWest Bancorp. Lender says it’s been approached by potential investors. Bill Ackman warns US regional banking system at risk.

The turmoil at PacWest shows how investor angst still remains elevated after a string of failures and deposit outflows in the sector despite Federal Reserve Chair Jerome Powell’s assurance Wednesday that authorities were closer to containing the crisis. It’s reignited the debate over whether more US regional lenders will fall after this year’s collapse of SVB Financial Group’s Silicon Valley Bank, Silvergate Capital Corp., Signature Bank and most recently First Republic Bank.

Smaller banks are under pressure after a year of interest-rate hikes hammered the value of their bond holdings and drove unrealized losses to an estimated $1.84 trillion. Trouble in commercial real estate is adding to the pain, while depositors take their money out to seek better returns elsewhere. These stresses have put the spotlight on these lenders, which typically have fewer resources to defend themselves.

We are seeing a consolidation of the banking system .. again as smaller and regional banks fail and get gobbled up by the Too-Big-To-Fail (TBTF) banks like … JP Morgan Chase.

Biden’s Reign of Error is not over yet. His campaign slogan (which was also Bill Clinton’s campaign reelection slogan) is “Finish the job!” With Biden’s idiotic mortgage idea of punishing borrowers with good credit and giving subsidies to those with bad credit, Biden is trying to finish off the US economy and banking system.

As part of the Biden administration’s plan to make housing affordable for everyone (we’ve seen this story before), upfront fees for loans backed by Fannie Mae and Freddie Mac will be adjusted based on the borrower’s credit score. Borrowers with high credit scores will pay more in fees, while those with lower credit scores will pay less.

The Wall Street Journal cited data from Evercore ISI that shows borrowers with credit scores between 720-759 who make around 15-20% down payments will see loan-level pricing adjustment (LLPA) costs rise by .750%. Inversely, under the new adjustments, risky borrowers with a credit score below 639 and who put down only 5% of the value of their home will only have to pay 1.750%, compared with 3.750% under old rules.

Backlash over LLPA changes prompted the FHFA to publish a statement last week, calling such concerns “a fundamental misunderstanding.” The Biden administration ensures the new changes are meant to help those with poor credit scores obtain homes amid the worst housing affordability in a generation. Note that Biden did not speak on this himself since he would undoubtedly get confused and call people names. And get lost leaving the podium.

According to the FHFA, the new adjustments will redistribute funds to reduce the interest rate costs paid by risky borrowers. This sounds like socializing home buying to us.

Even more alarming is data from the American Enterprise Institute found that default rates of Fannie/Freddie owner-occupied 30-year fixed-rate purchase loans acquired in 2006-2007 were between 39.3% and 56.2% for borrowers with credit scores between 620 and 639 and less than 4% down payments. Those with credit scores between 720 and 769 and 20% down payments had default rates between 4.2% and 8.8%.

Joe Biden’s new nickname is “The Punisher.” Not only for this sick and twisted theft from people who work hard and are careful with their credit, but also for his crazy obsession with going green and driving energy prices (and inflation) through the roof.

Thanks to O’Biden (Obama/Biden) and Senate Majority Leader Chuck Schumer’s failure to negotiate a debt ceiling increase, the US has officially become a banana republic. Crazy government, lawless censoring and arrest of opposing political candidates.

The US CDS 1Y SR Eur just hit a staggering 176.53. That is the price of insuring against a debt default by O’Biden and Treasury Secretary Janet Yellen.

Is a US debt default likely? It shouldn’t be. But you never know with the circus clowns in the White House and nasty Chuck Schumer. But arresting the leading Republican Presidential candidate before the elections is pure Chavez/Maduro Banana Republic politics.

2 year Treasury yield up over 11 basis points today.

You must be logged in to post a comment.