My former colleague at Deutsche Bank, Joe Carson, said recently that the US economy is not in a recession, but corporate profits are in a recession. While I cling to the traditional definition of recession (two consecutive quarters of negative real GDP growth), there is another component of the US economy that is in recession: consumer sentiment.

The University of Michigan Consumer Sentiment Index rose slightly in the latest release, but remains depressed at 51.5. University of Michigan Buying Conditions for House also rose to 47.0, also a depressed reading.

While unemployment remains low, the price of gasoline is crushing the wallets of American households helping to cause a recession in consumer sentiment.

Biden feebly attempts to explain why 2 consecutive quarters of negative real GDP growth (better known as contraction) is NOT a recession.

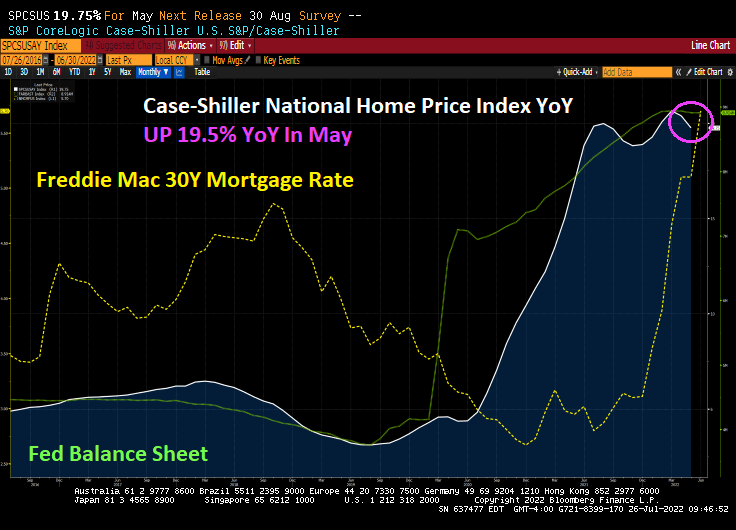

The May Case-Shiller home price indices are out and they’re a doozy. The national home price index rose 19.75% YoY. Why? You can thank The Fed’s “slowhand” approach to withdrawing the Covid-related stimulypto.

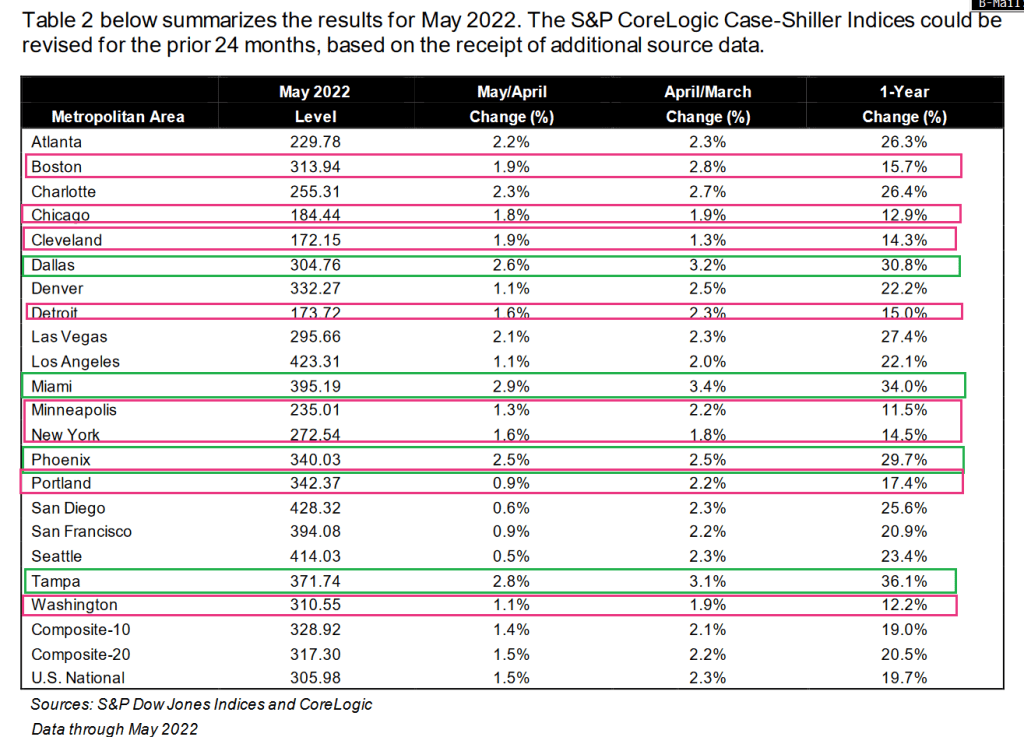

Where are home prices booming? Everywhere.

Miami, Tampa, Dallas and Phoenix (red states) are growing at over 30% YoY. Boston, Chicago, Cleveland, Detroit, Minneapolis, New York, Portland and Washington DC (blue states) are all growing at over 10% YoY. Cleveland is a blue city in a mostly red state while San Diego is a red city in an almost blue state.

Jerome “Slowhand” Powell is not shrinking The Fed’s balance sheet.

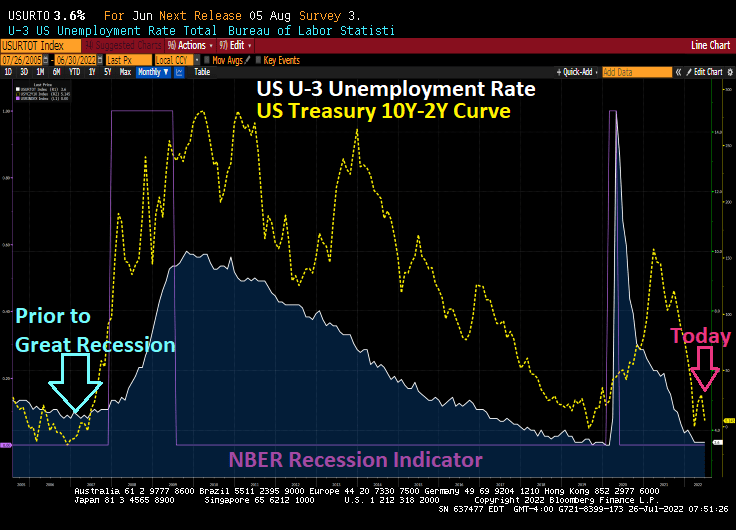

Just remember, the US economy had strong employment figures just prior to the 2008 Great Recession and financial crisis, so US Treasury Secretary Yellen, Biden’s economic cheerleader Bernstein and Obama’s economic cheerleader Sperling are all relying on a bad indicator of economic health to justify that the US economy is in great shape.

(Bloomberg) — Treasury Secretary Janet Yellen expressed confidence in the Federal Reserve’s fight against inflation and said she doesn’t see any sign that the US economy is in a broad recession.

“We’re likely to see some slowing of job creation,” Yellen said on NBC’s “Meet the Press” on Sunday. “I don’t think that that’s a recession. A recession is broad-based weakness in the economy. We’re not seeing that now.”

With US consumer prices rising at the fastest rate in four decades, a growing number of analysts say it will take a recession and higher joblessness to ease price pressures significantly. The Federal Reserve raised rates in June by the most since 1994 and is expected to approve another 75 basis-point hike this week.

Inflation is “way too high,” Yellen said, while renewing the Biden administration’s argument that it’s also high in many other advanced economies.

“The Fed is charged with putting in place policies that will bring inflation down,” said Yellen, a former Fed chair. “And I expect them to be successful.”

Dammit, Janet. All of Biden’s anti-fossil fuel orders are still in place and Biden/Pelosi/Schumer are still trying to pass the highly-inflationary Build Back (Inflation) Better bill. And The Fed still has not shrunk it massive balance sheet yet.

But Janet, the US Treasury 10Y-2Y yield curve remains inverted (historically ahead of a recession) while the Atlanta Fed GDPNow Q2 tracker is at -1.6% which would make the second quarter in a row of negative real GDP growth in a row (historically a definition of recession).

My preferred 10Y-2Y chart shows the yield curve more inverted than even prior to The Great Recession!

But in Yellen’s defense, The Fed’s preferred yield curve (implied yield on 3-month T-Bills in 18 month – 3 month T-Bill yield) is still positive, though crashing like a paralyzed falcon.

So, the Biden administration is sticking to the strong labor market story. But what the Biden Administration (and Yellen) fail to acknowledge is 1) unemployment is a lagged indicator of a recession (unemployment was low prior to the 2008 GREAT recession, then exploded and 2) there is still a tremendous amount of monetary stimulus outstanding that The Fed has taken away … yet.

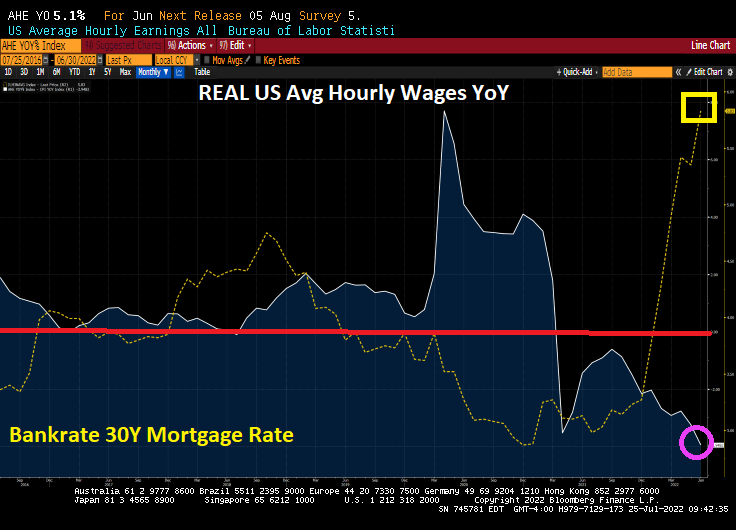

Essentially, the Biden Administration is panicking over the coming mid-year election and will say anything at this point to stay in power. So, I would probably ignore anything said by Biden, Yellen and their talking heads before the midterms elections. But when Biden’s economic advisor says that the US economy is strong, I want to ask him how having NEGATIVE wage growth is a good thing,

Let’s see if Yellen is correct and The Fed’s Fireball will tame inflation. Frankly, I think the global slowdown is the only thing that will tame inflation.

Instead of The Boston Strangler, we now have the DC Strangler. Better known as The Federal Reserve and their war on inflation.

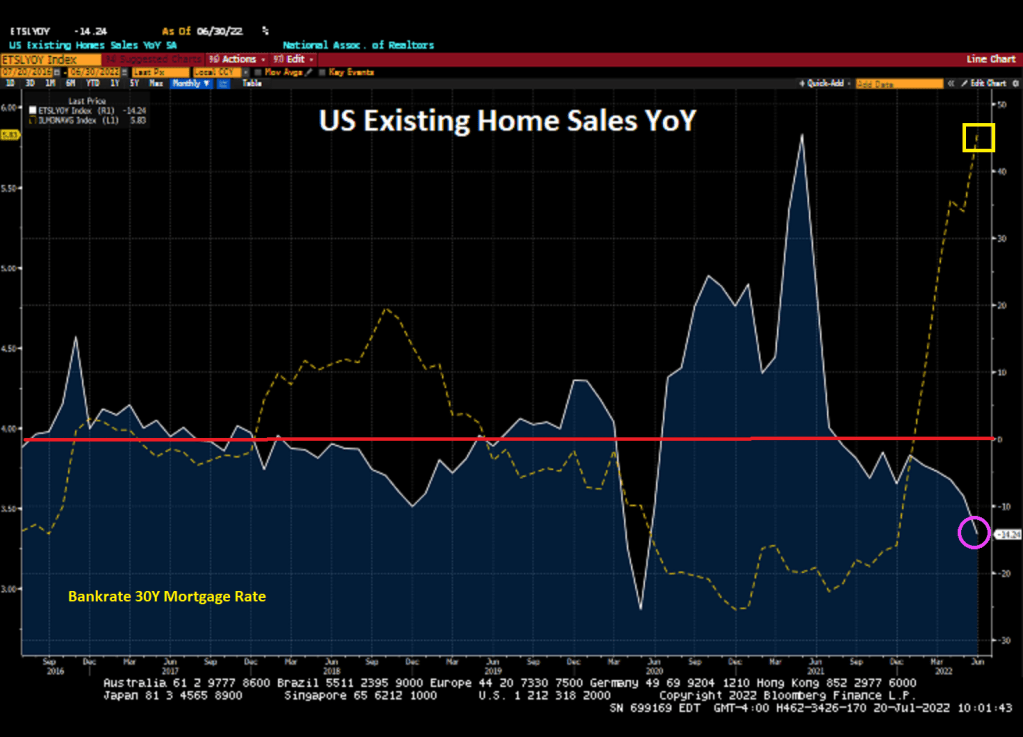

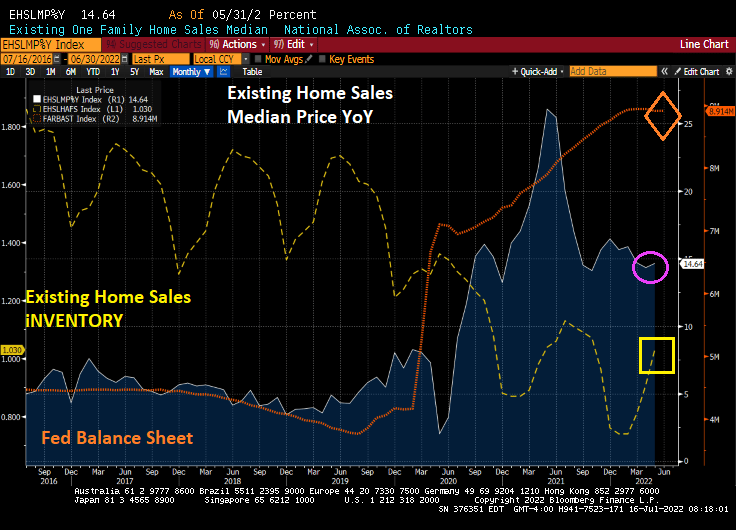

US existing home sales crashed -14.24% YoY and -5.40% MoM in June as The Fed tightens its icy grip on the housing market. Existing home sales were lower than expected at 5.12 million home sold SAAR.

Median price for existing home sales declined to 13.27% YoY as inventory available for sale remains MIA. And The Fed’s balance sheet is still out in force.

The US housing market in terms of sales has entered a bear market, but with The Fed’s balance sheet stimulus still hunting asset prices, it is a grizzly bear market in terms of affordability.

Mortgage rates are rising in part thanks to The Federal Reserve trying to control inflation (caused by Biden’s energy policies and spending). But mortgage rates are down slightly today.

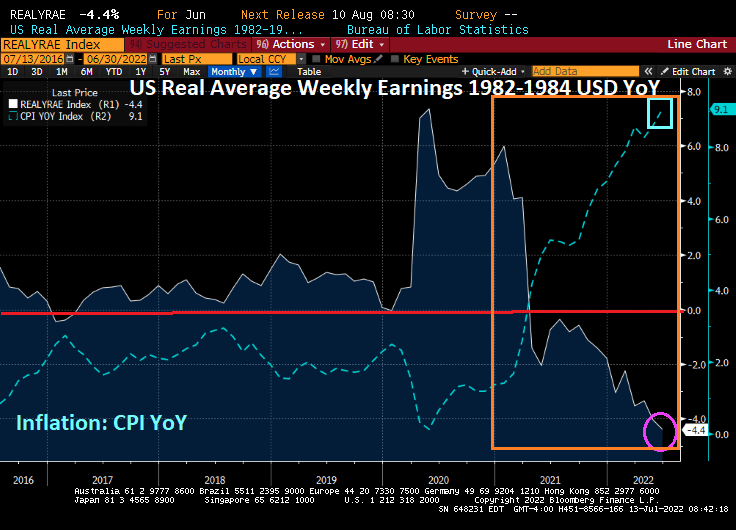

Bear in mind that REAL wage growth is negative, thanks to Bidenflation.

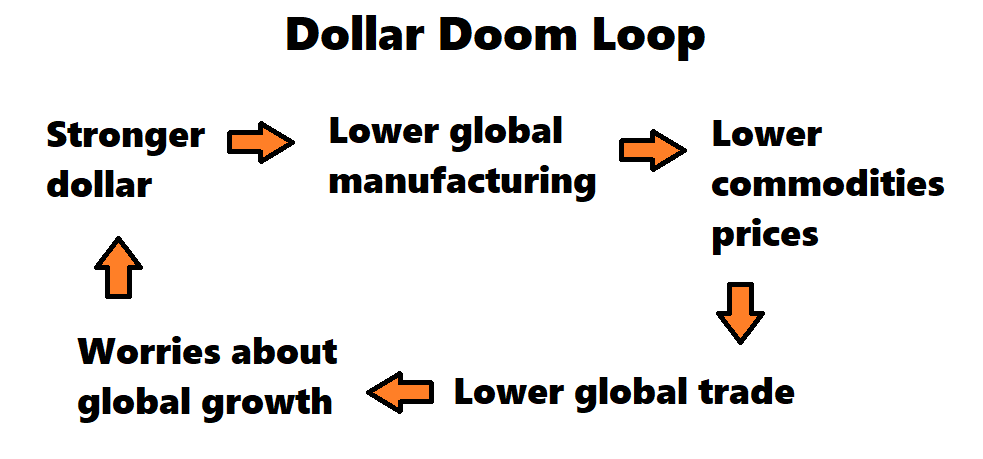

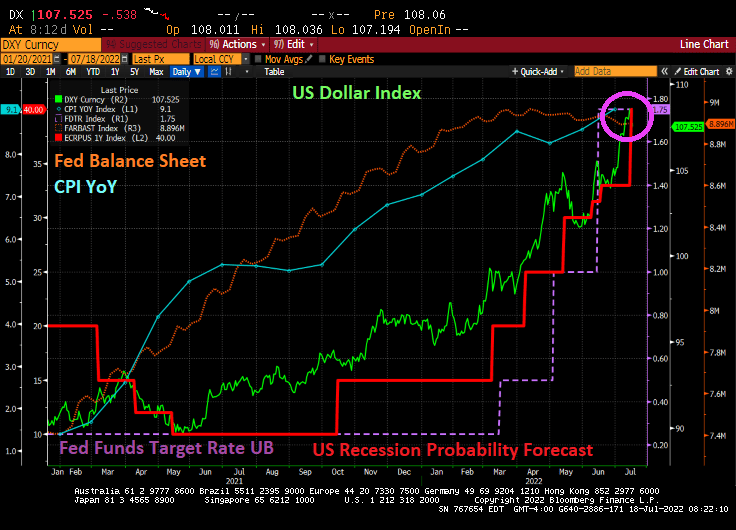

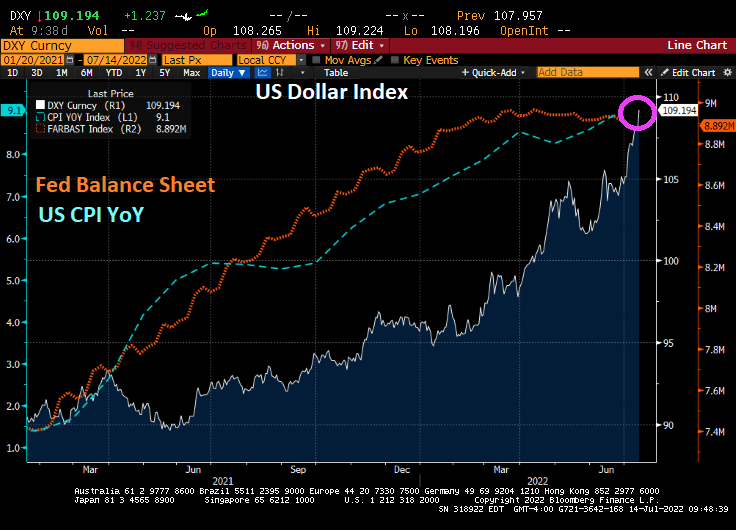

The dollar’s gain is the world’s pain — and based on its current trajectory, the world may be in for a whole lot more discomfort.

Concerns over global growth have recently sent the US Dollar Index to the strongest level on record, with the greenback hitting multi-decade highs against currencies like the euro and the yen.

But the move risks becoming a self-reinforcing feedback loop given that the vast majority of cross-border trade is still denominated in dollars, and a stronger US currency has historically translated into a broad hit to the world economy.

Against the backdrop of higher-than-expected inflation and still-elevated commodities prices, the concern is that we’re in for a dollar ‘doom loop’ like never before, according to Jon Turek, the founder of JST Advisors and author of the Cheap Convexity blog.

With the Federal Reserve hiking interest rates at the fastest pace in decades, he says, it’s much less clear what could break the feedback loop in the next few months.

The Dollar Doom Loop with US inflation causing The Fed to tighten

Under Biden’s policies, inflation hit a 40-year high (blue line), and the US Dollar (green line) is strengthening. Then we have The Fed raising the target rate (purple line) and the probability of recession rising with Fed tightening.

Is a US recession coming? The US Treasury 10Y-2Y yield curve is inverted at almost -20 basis points.

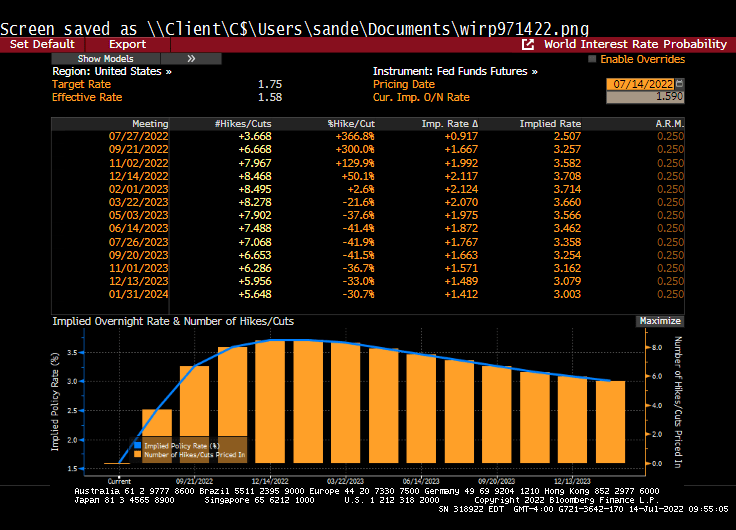

There is a Fed open market committee meeting in one week and they are expected to raise their target rate by 75 basis points according to Fed Fund Futures data. Inflation keeps rising as does the probability of a US recession. So, The Fed will keep on tightening.

Housing in the US is simply unaffordable for the middle class and low-wage workers. Combine rising food costs and gasoline/heating costs, and we have an economic disaster on our hands.

US existing home sales for June will be released on Wednesday. But can The Fed kill-off home price inflation?

A preliminary analysis of existing home sales for June is for a seasonally adjusted annual rate of 5.1 million, down 5.4% from May and down 14.2% from last June. As The Fed cranks up its target rate (green line) and eventually shrinking its balance sheet, we will see further shrinking of existing home sales this summer.

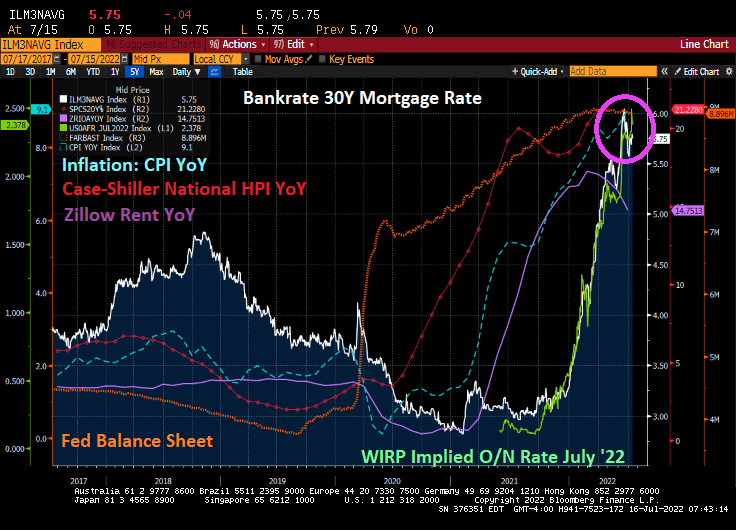

But home price inflation remains high (Case-Shiller National home price index at 21.23% YoY, Zillow’s rent index at 14.75% YoY) while the Consumer Price Index YoY is at 40-year high of 9.1% YoY. In other words, home price inflation is 233% of the stated inflation rate from Uncle Sam.

May’s existing home sales report was … sobering. There is still historically low levels of available inventory and median sales price of existing home sales was 14.64% YoY. Of course, the alternative to ownership is renting which is growing at 14.75% YoY. Simply unaffordable.

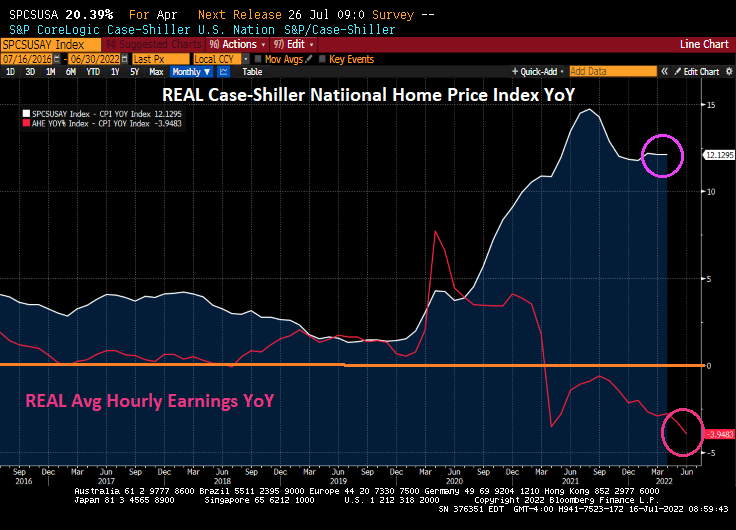

The gap between REAL home price growth (12.13% YoY) and REAL average hourly earnings (-3.95% YoY).

Consumer sentiment for housing is near the lowest level since 1982.

The Fed seems determined to remove the punch bowl in its efforts to crush inflation. But will The Fed’s efforts also crush the housing and mortgage market?

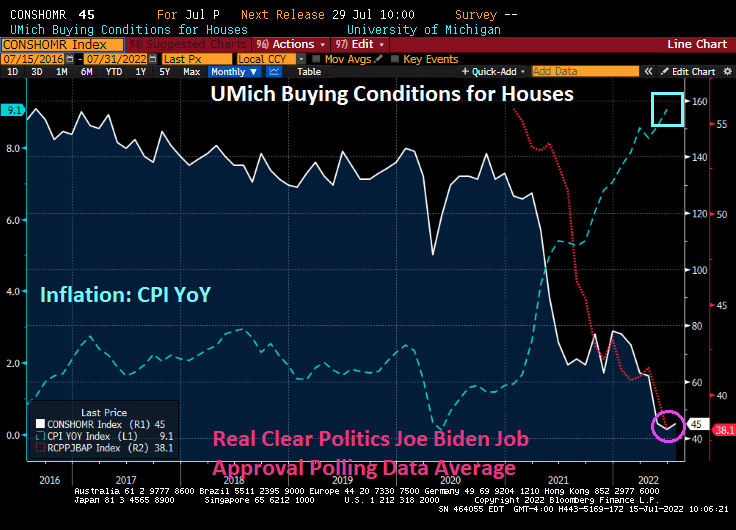

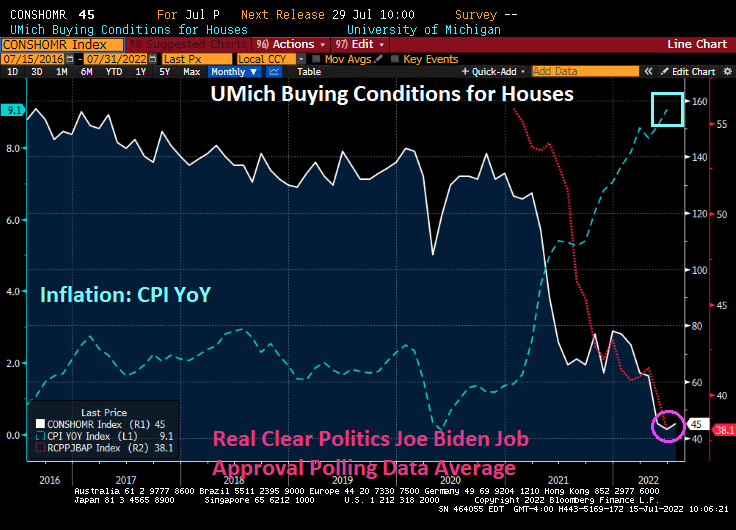

One measure of how bad things are in the US for the middle-class and low-wager workers ix consumer sentiment from University of Michigan. The latest University of Michigan survey of consumers remains depressed at 51.1.

The consumer sentiment index was at 80.7 at the beginning of 2021, but has plunged dramatically with rising gasoline, food and inflation in general. Biden’s popularity has sunk from 55.8 in January 2021 to 38.1 today.

How about housing sentiment? Housing sentiment was 134.0 in January 2021 but has plunged to a depressing 45 with inflation and rising home prices (and rent). And with declining sentiment about housing, Biden’s popularity has plunged.

Bear in mind that a strong dollar is a two-edged sword. The US Dollar Index has risen 16% year-over-year, presenting a big hurdle for US firms with business overseas.

That strength of the greenback will rise until the Fed makes a dovish policy pivot.

And that pivot is forecast to occur at the Feb ’23 FOMC meeting.

You must be logged in to post a comment.