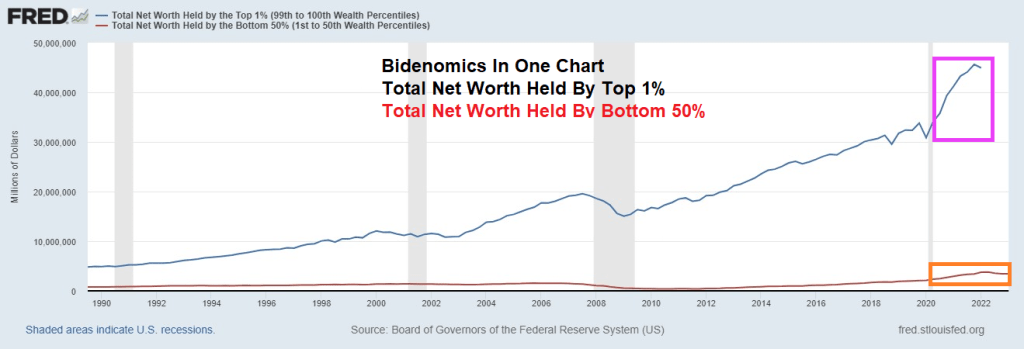

Bidenomics, massive spending on green energy mandates while curbing fossil fuel consumption, has been a true wonder for the top 1% of net worth (let’s call them The Elites). And Bidenomics, like Obamanomics, relied on super generous Federal Reserve money printing.

The result? Total Net Worth held by the top 1% has grown rapidly since the Covid outbreak and Fed monetary expansion (plus Congress going wild spending). The bottom 50%? They improved in terms of net worth

So, The Elites (top 1%) want The Fed to keep on printing money, since their net worth soars.

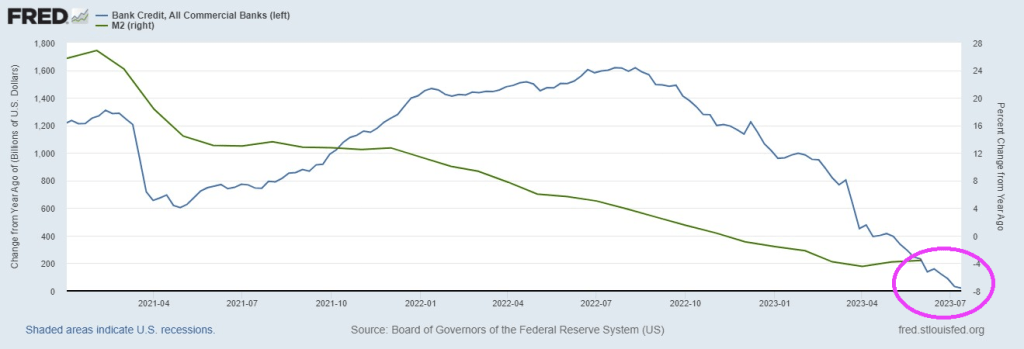

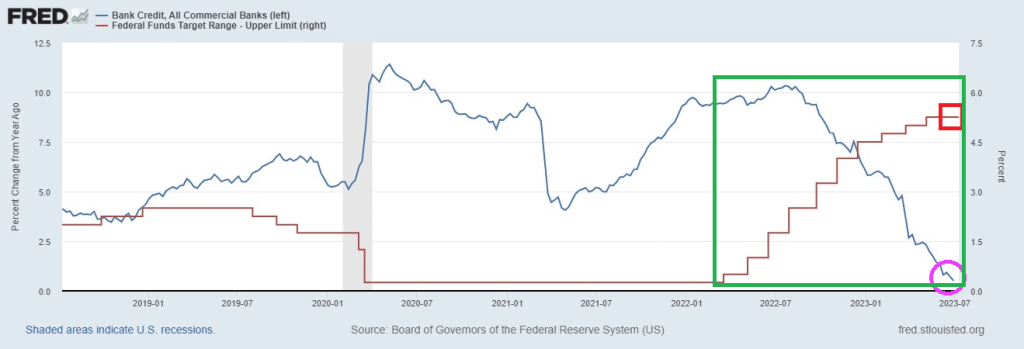

Meanwhile, US bank credit is crashing as The Fed slows M2 Money growth.

Not only is credit growth grinding to a halt, but unrealized losses on bank investment securities continues to worsen.

If you didn’t see this, then check out House testimony of extraterrestrial visitations to Earth. This has been happening since the 1950s (allegedly), so why NOW is there sudden interest in aliens? Deflection away from the horrible scandal of Biden taking money from foreign actors? Likely answer? Biden and Mayorkas will send Treasury Secretary Janet Yellen to negotiate with alien invaders giving them anmesty, free school, free food, free healthcare and directions on how to register to vote. And giving aliens preferential trade status. All for “10% for The Big Guy!”

Bidenomics relied of massive Federal spending thanks to Covid and massive monetary expansion. This led to the highest inflation in 40 years (Bidenflation). But now The Fed is slowing M2 Money growth into negative territory and hiking their target rate.

The result? Bank credit growth has crashed to 0.5% YoY. In other words, banks are no longer expanding credit for the first time since the aftermanth of The Great Recession and Financial Crisis of 2008/2009. Of course, Washington DC bailed out their bestest buddies, the banks, while middle America suffered.

As America loses steam under Biden and The Fed, 41+ countries have signed on to the BRICs gold-backed reserve currency. Unlike the USA with its fiat currency (backed by Babbling Biden and Janet “The Midget Marxist” Yellen), this reserve currency will be backed by gold.

The US has passed the 32 trillion mark in national debt, and is going much, much higher. More like 32 tons on the back of taxpayers. When we add unfunded liabilities like Social Security, Medicare and Medicaid, the tab soars to $224.5 TRILLION.

In the first six months of 2023, there were 340 corporate bankruptcies, topping every other comparable span in 13 years, according to S&P Global Market Intelligence. This is up 93 percent from the same time a year ago and higher than in 2020, when there was a spike during the early days of the coronavirus pandemic.

There were 54 recorded corporate bankruptcy filings in June, unchanged from the 54 bankruptcies in May. Last month, some of the most notable companies to submit filings were Lordstown Motors, Rockport Co., Instant Brands Acquisition Holdings, and iMedia Brands.

“Lordstown Motors Corp. filed for bankruptcy June 27, with plans to restructure its business and seek a buyer, according to a company release. The electric vehicle manufacturer’s assets include its Endurance pickup truck and related resources,” S&P noted in the July 6 report.

“Instant Brands Acquisition Holdings Inc. also sought bankruptcy protection June 12. The tightening of credit terms and higher interest rates had impacted the company’s liquidity levels, according to an official release. The company has also already secured $132.5 million from existing lenders and plans to continue discussions with its financial stakeholders.”

Year-to-date through June, 15 companies with more than $1 billion in liabilities filed for bankruptcy, such as Cyxtera Technologies, Diebold Holding, Bed Bath & Beyond, Diamond Sports Group., and Party City.

Epiq Bankruptcy, a U.S. bankruptcy filing data provider, confirmed that 2,973 total commercial Chapter 11 bankruptcies were filed in the first half of 2023, up 68 percent from the same period in 2022.

Higher Interest Rates Impacting Businesses

Banking experts purport that higher interest rates are the leading cause of the increase in corporate bankruptcies. Many businesses either maintain vast debt loans that will require refinancing or need more liquidity to stay afloat.

“The increase in commercial and individual bankruptcy filings during the first half of 2023 underscores the economic challenges faced by businesses and individuals,” said Mr. Gregg Morin, Vice President of Business Development and Revenue at Epiq Bankruptcy, in the report. “Our objective is to provide bankruptcy professionals with timely and accurate data necessary for analyzing stakeholder volumes and trends for making informed business decisions.”

The situation could be exacerbated should the Federal Reserve pull the trigger on two more rate hikes this year. The futures market is penciling in a quarter-point boost to the benchmark fed funds rate at this month’s Federal Open Market Committee (FOMC) policy meeting.

Meanwhile, according to a recent Fitch Ratings report, the corporate default rate is projected to climb to as high as 4.5 percent in 2023, up from the previous forecast low of 2.5 percent. The updated projections reflected “the tighter lending conditions and capital access resulting from stress in the banking sector and inflation uncertainty.”

However, some argue that corporate bond market indicators are “less ominous.”

“The interest rate differentials, or spreads, between the 10-year U.S. Treasury note and investment grade (IG) and high yield (HY) corporate bonds continue to hover within their average width over the past 25 years, a bond market signal indicating the likelihood of a less severe recession, with traders pricing in fewer corporate defaults,” wrote John Lynch, the CIO at Comerica Wealth Management, in a research note.

Economists contend that the worst corporate bankruptcies typically occur one or two years into a recession. Today, they are happening before the official start of an economic downturn as the U.S. economy is still expanding.

What’s happening?

“Simple,” says Mr. Pete St. Onge, a Heritage Foundation economist, “banks aren’t lending.”

“Banks are battening down the hatches, hogging their bailout money instead of lending it out,” he said in a recent podcast. “That credit crunch means not only do we get bankruptcies like in any recession, on top of that, we get a lending wall that cuts off even the healthy businesses. Of course, their jobs go down with them.”

Since the Federal Reserve launched the Bank Term Funding Program (BTFP) following the Silicon Valley Bank collapse in March, financial institutions have kept tapping into these emergency lending facilities. After hitting a record high at above $103 billion at the end of June, it remains elevated at $102 billion.

32.5 trillion in debt and $192 trillion in unfunded liabilities which means a total of $224.5 total debt + liabilities.

This is Bidenomics. Spend trillions, borrow trillions, promise entitlements. Rinse, repeat.

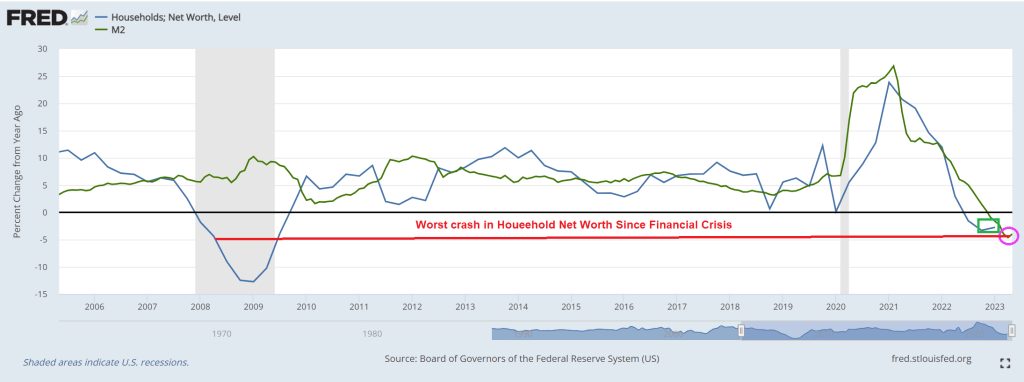

The year-over-year growth rate in Household Net Worth has been negative for 3 consecutive quarters, the worst growth since The Great Recession and Financial Crisis of 2008/2009.

Of course, the Biden family household net worth is off the charts. As is the household net worth for other Washington DC politicians like Nancy Pelosi (Communist-CA). And AOC (Communist – NY).

After yesterday’s surprise ADP jobs report, I was expecting a better June jobs report. But alas, today’s job report was a disappointment. Only 209k jobs were added in June.

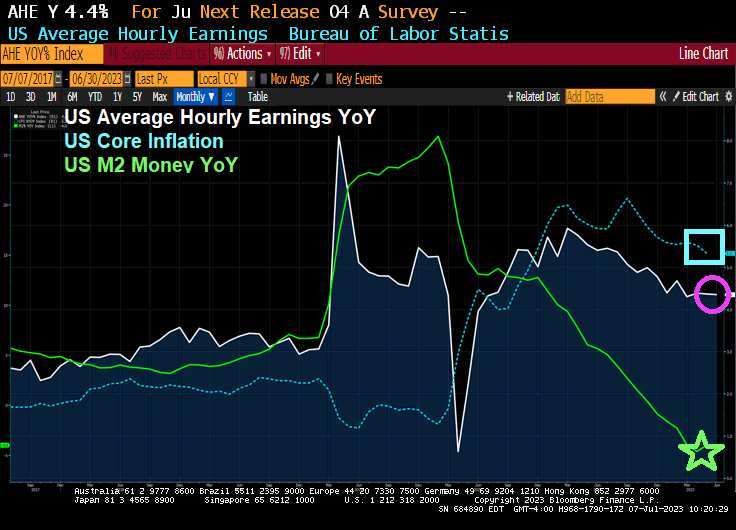

On the other hand, average hourly earnings YoY rose slightly to 4.4%. Too bad core inflation at the last reading was 5.3% YoY.

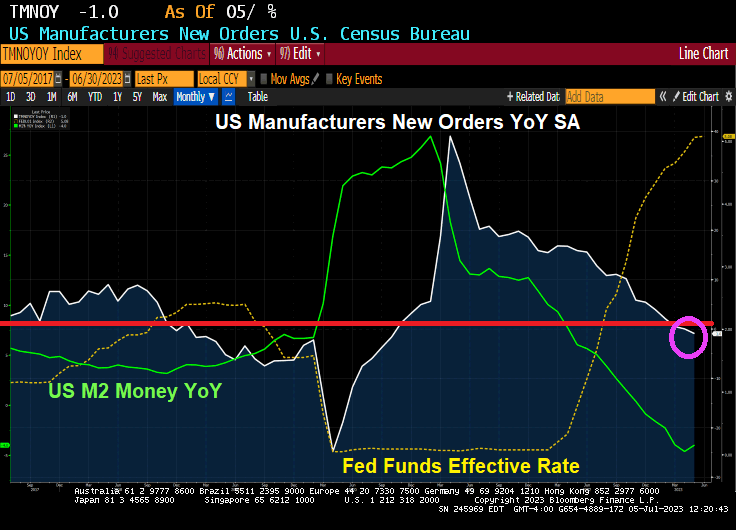

As Powell and The Gang raise interest rates, the more the economy is … slip slidin’ away. US Manufacturers New Orders YoY in May declined -1.0% for the first time since Covid.

I was hoping that the week of July 4th would start off with fireworks, but we got bad news about the economy.

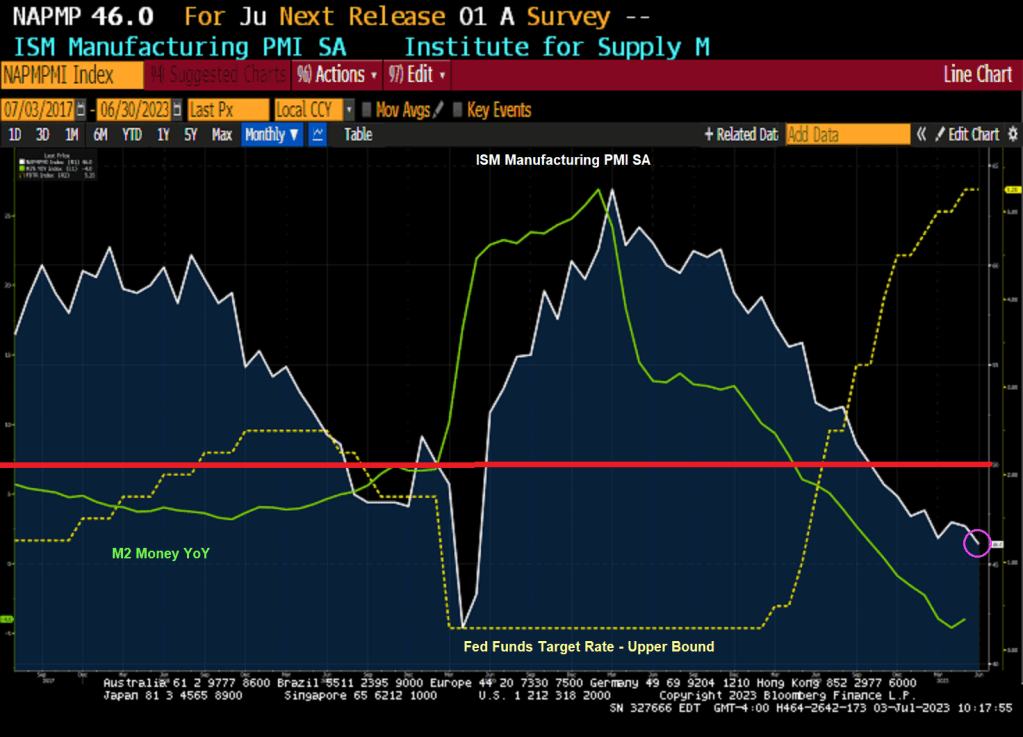

US factory activity contracted for an eighth month in June, slipping to the weakest level in more than three years as production, employment and input prices retreated.

The Institute for Supply Management’s manufacturing gauge fell to 46, the weakest since May 2020, from 46.9 a month earlier, according to data released Monday. The current stretch of readings below 50, which indicates shrinking activity, is the longest since 2008-2009.

The decline in the ISM production gauge, which also stands at the lowest level since May 2020, suggests demand for merchandise remains weak. The index of new orders contracted for the 10th straight month and order backlogs shrank, which may help explain a pullback in a measure of manufacturing employment.

The ISM gauge retreated to a three-month low and, at 48.1, indicates fewer producers adding to payrolls.

Many Americans continue to limit their spending on merchandise as they rotate to services and experiences. Others are simply tightening their belts as still-high inflation takes a toll on their incomes.

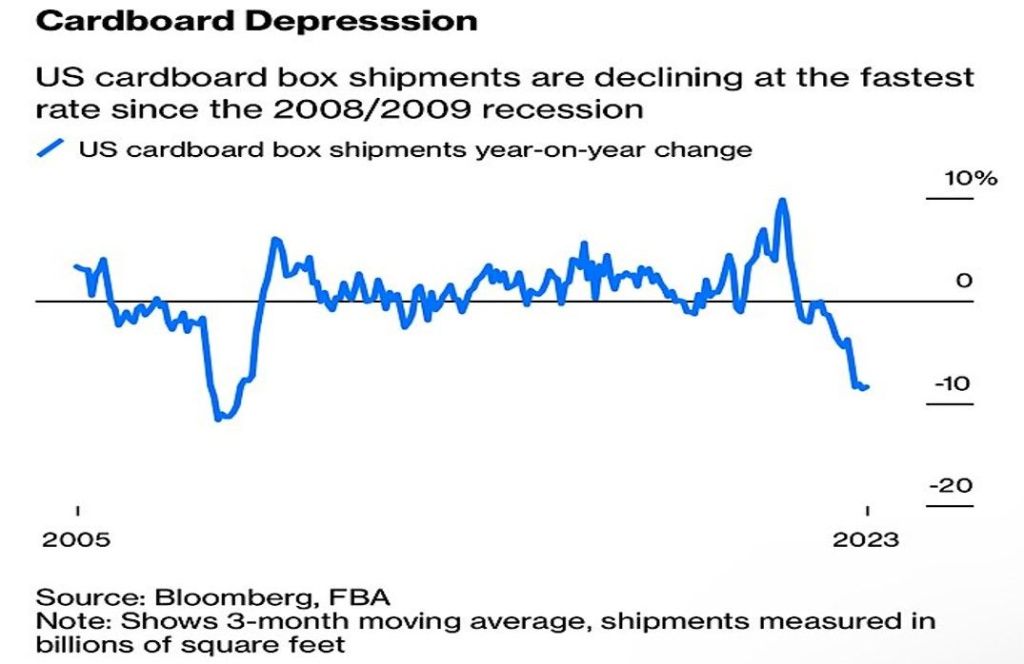

And then we have cardboard box shipments declining at fastest rate since 2008/2009.

At least Ethereum is up over 2% this morning.

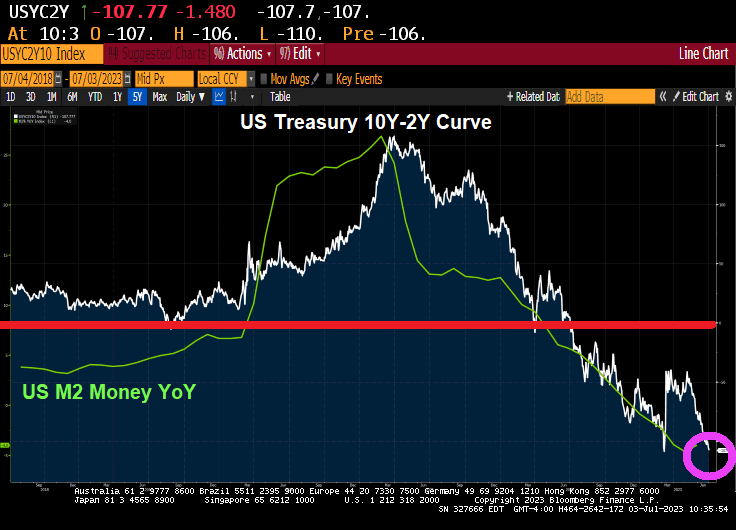

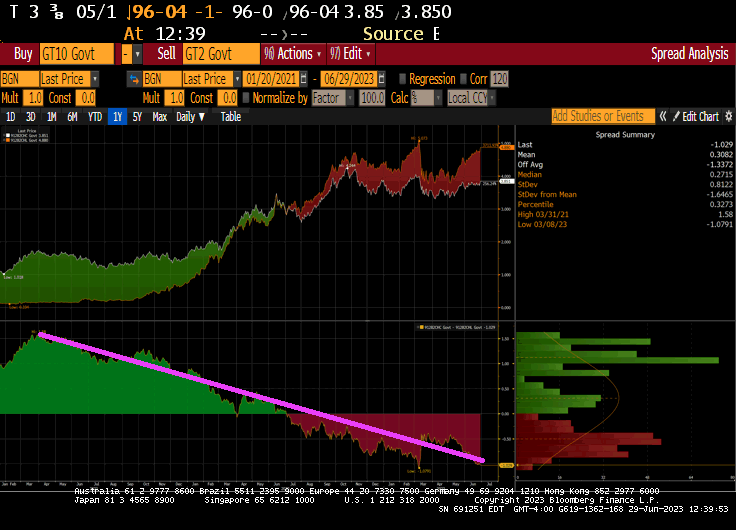

And the US Treasury 10Y-2Y keeps on diving deeper into inversion.

The University of Michigan consumer survey results are out and there is good news! Sort of.

The UMich Buying Conditions for Houses rose to 47 in July! That is the good news. The bad news? It was at 142 in the last month before Covid and the economic/school shutdowns.

That is -67% lower than under pre-Covid Trump.

Nothing has been the same since Covid (aka, the Wuhan China Lab virus) where our corrupt politicians and lame street media (aka, government cheerleaders) show no interest in finding out what really happened.

Bitcoin cash is up 21.5% today.

Gold and silver are up today. Too bad I can’t buy nickel coins.

The Walking Dead’s Megan. The honorary symbol of Bidenomics.

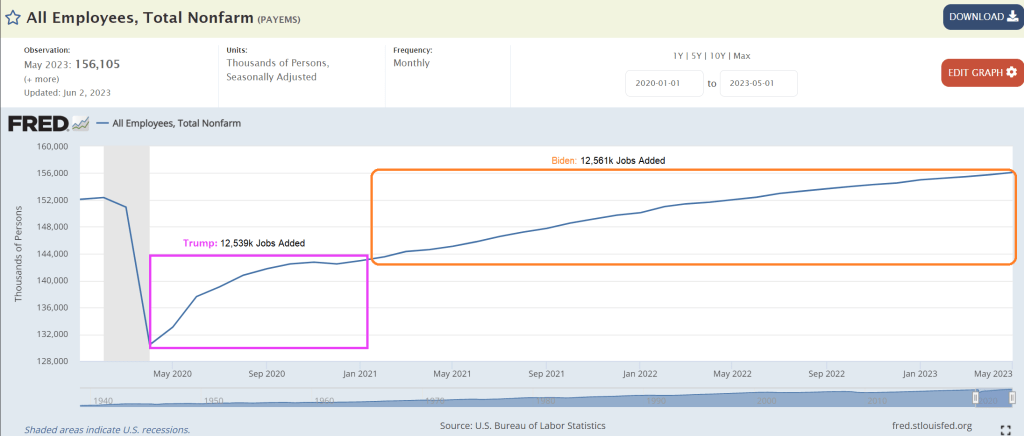

Bidenomics is a great marketing ploy where you have out of control Federal spending and magically decide to reopen the economy and school after Covid and focus only on jobs added after Biden was selected President and ignore the jobs added during Trump.

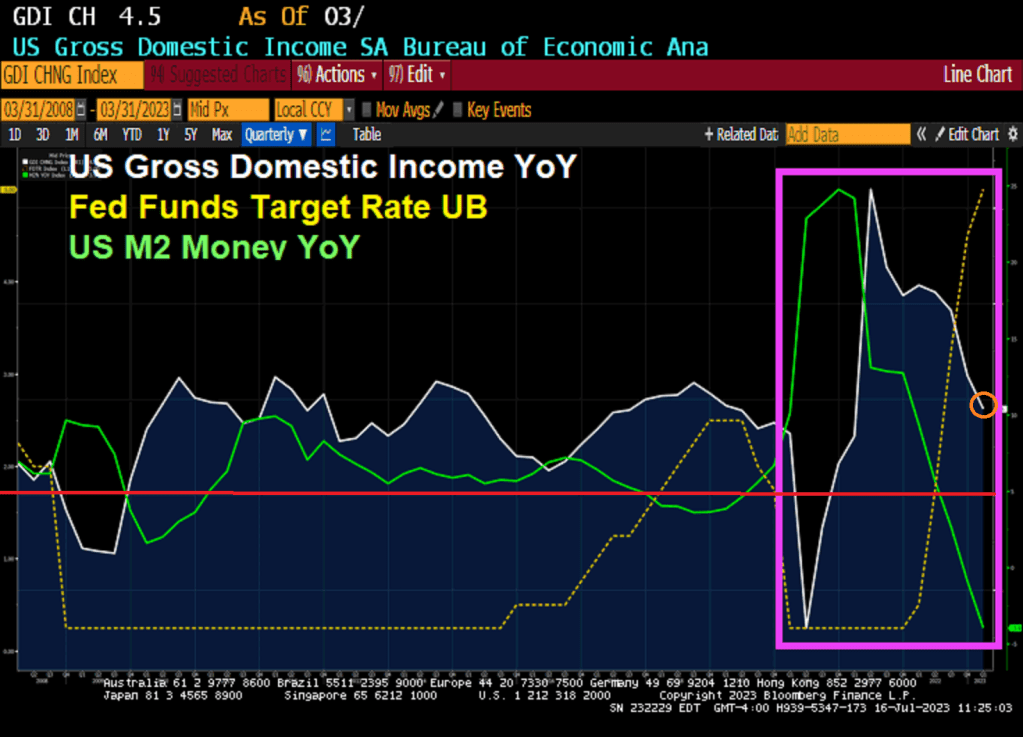

Real gross domestic income (GDI) is a measure of the incomes earned and the costs incurred in the production of gross domestic product. It’s another way of measuring U.S. economic activity. BEA also publishes the average of real GDP and real GDI.

REAL GDI dropped to -0.8% QoQ for Q1 2023. Kind of looks like Bidenomics is running out of gas.

On Biden’s claims that he created twice as many jobs as any other President, the US economy add 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs.

The US Treasury yield curve (10Y-2Y) is now inverted at -103 basis points.

As Fed stimulus wears out, so is the Treasury 10Y-2Y yield curve.

You must be logged in to post a comment.