Housing in the US is simply unaffordable, particularly after HUD levied new regulation rising the cost of new housing up to $31,000. Wait for this to kick into the data for mortgage demand!

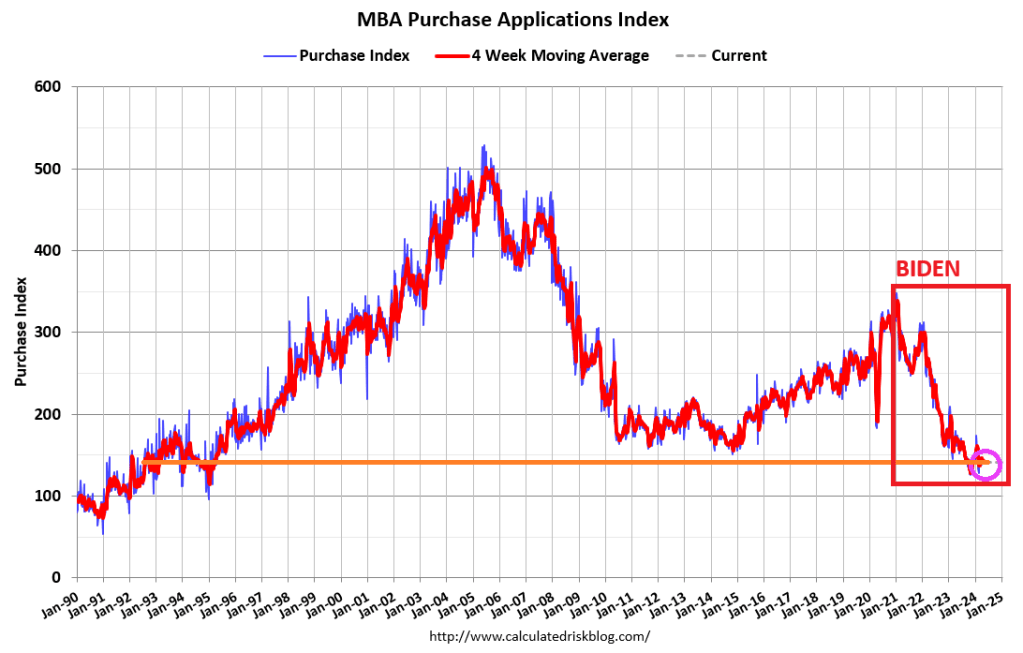

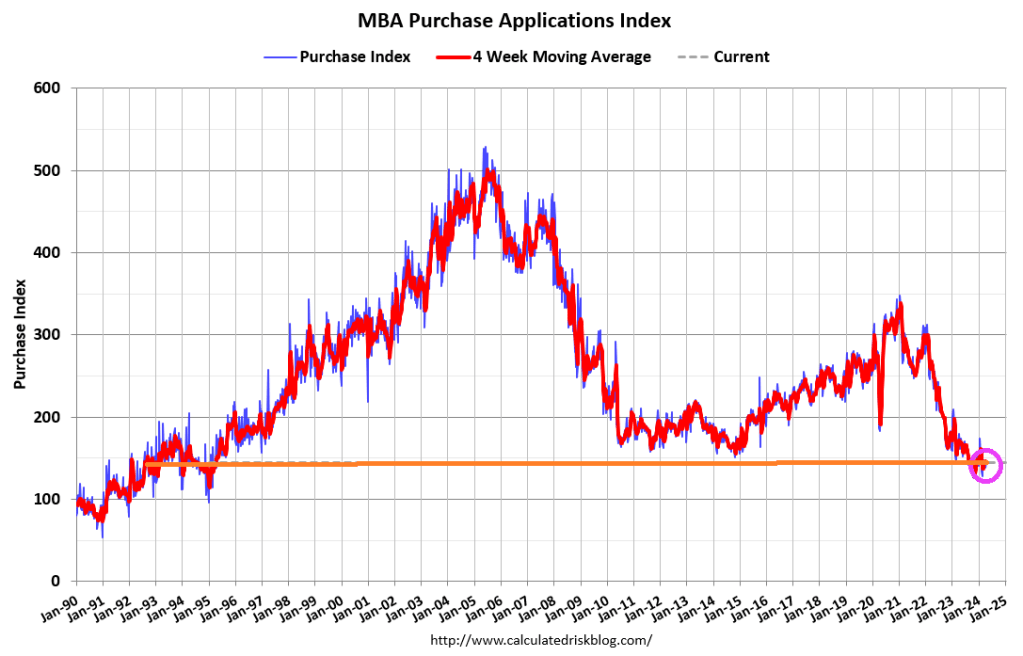

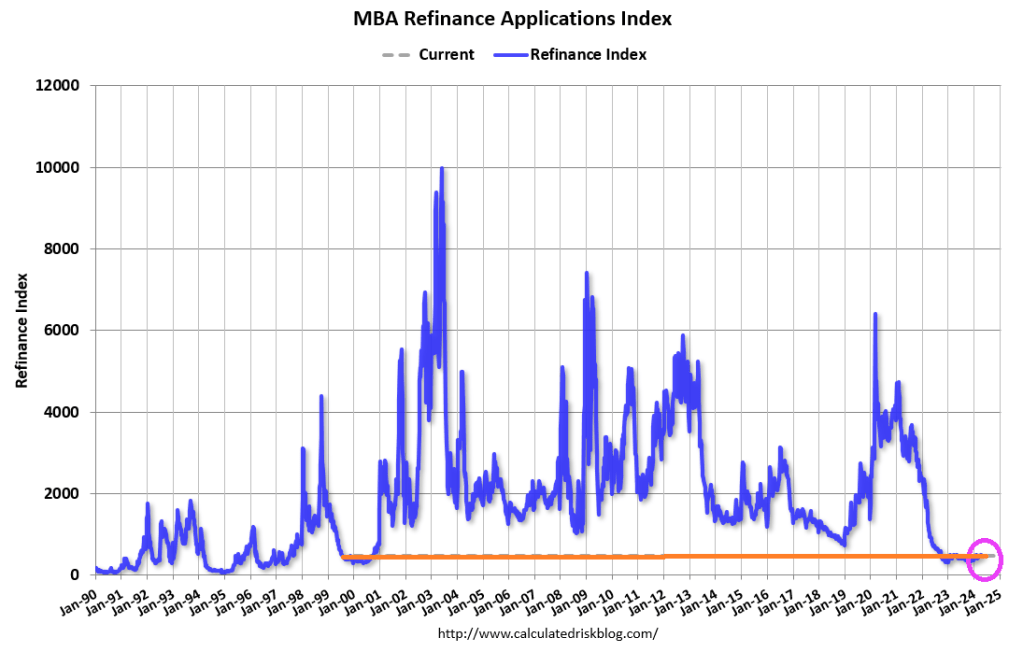

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 26, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1.4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was14 percent lower than the same week one year ago.

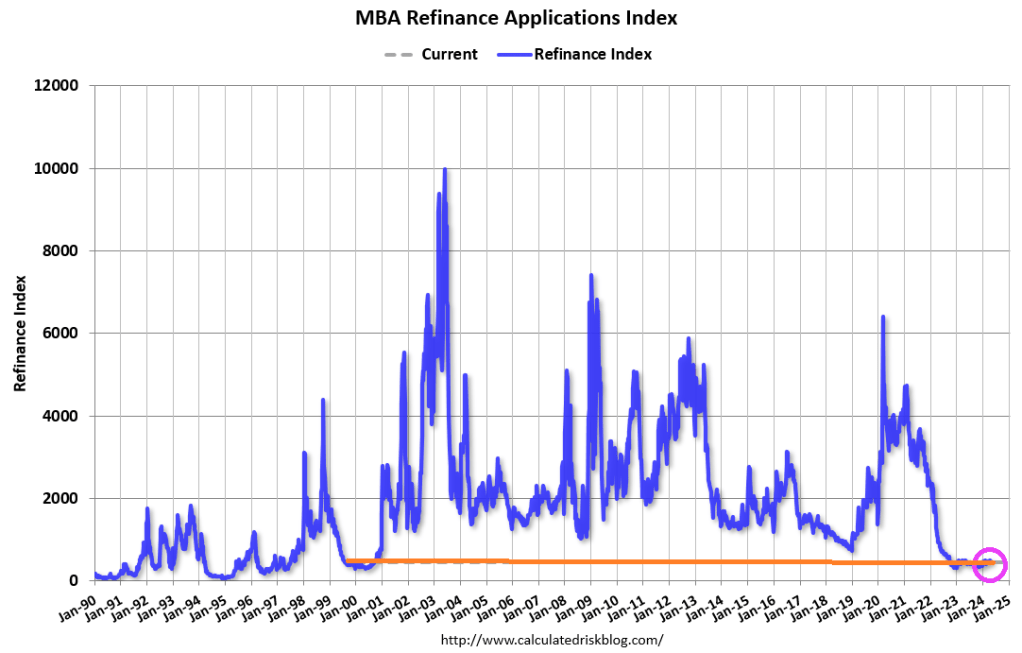

The Refinance Index decreased 3 percent from the previous week and was 1 percent lower than the same week one year ago.

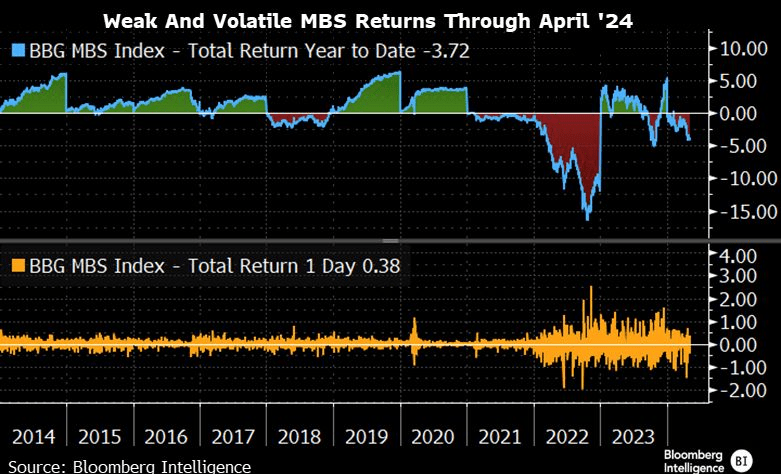

MBS returns are weak and volatile.

How is the Biden Regime making homeownership more affordable? They aren’t. The are using regulations, to drive the cost of new housing way up. New HUD energy rules will raise the cost of home construction by imposing stricter building codes. The National Association of Home Builders says the energy rules can add as much as $31,000 to the price of a new home. Payback time is 90 years (how long it will take the recoup the initial investment).

Under Biden’s “leadership” we are all addicted to gov. But at least Ukraine and Zelenskyy will be getting a guaranteed 10 years of financial support from the US … while E Palestine Ohio and Maui remain destroyed.

Janet Yellen, world class propagandist (US version of Baghdad Bob) and US Treasury Secretary under Biden, was so wrong about inflation. Instead of being “transitory”, turns out to be seemingly permanent.

Today’s Case-Shiller home price report was released for February. The National Home Price index was up 6.4% year-over-year. But look at the explosion of M2 Money and home prices. Hmm.

If we look at home prices and M2 Money on a year-over-year (YoY) basis, we can see the surge in money printing with COVID and the corresponding surge in home prices. As M2 Money growth slowed, the Case-Shiller National HPI slowed as well … until The Fed slowed the declined in M2 Money growth resulting in rising home price growth again.

So, The Fed will likely have to keep on printing. You can see Janet Yellen dancing to the thought of printing more money.

Joe Biden could barely eat his dinner at the White House Correspondents’ Dinner. And we think he is calling the shots in The White House?? Oh well. Perhaps it is Treasury Secretary Janet Yellen or Klaus Schwab of the World Economic Forum.

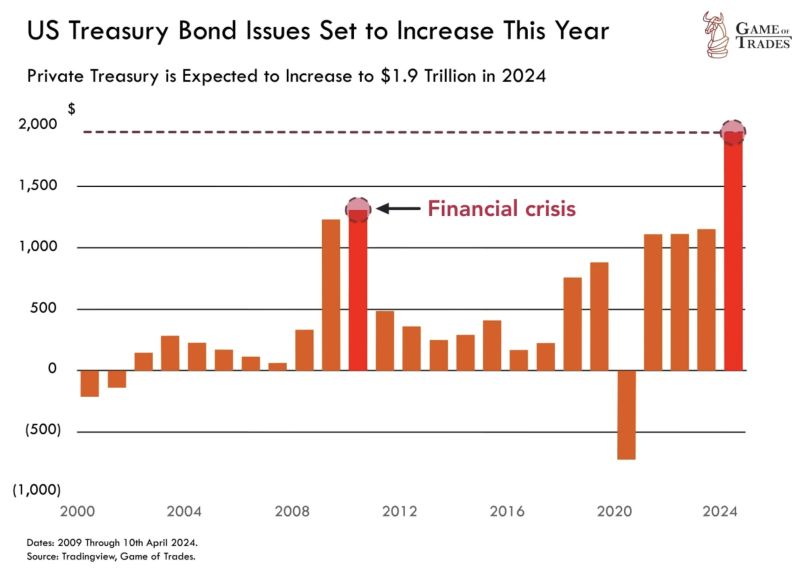

In any case, Treasury bond issuance in 2024 is expected to hit $1.9 TRILLION. Surpassing levels seen even during the 2008 financial crisis.

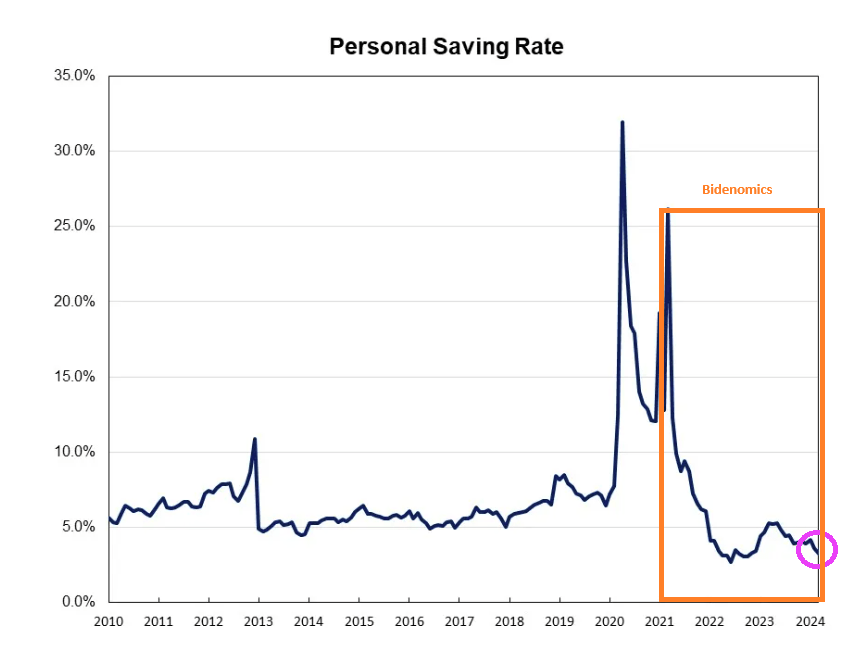

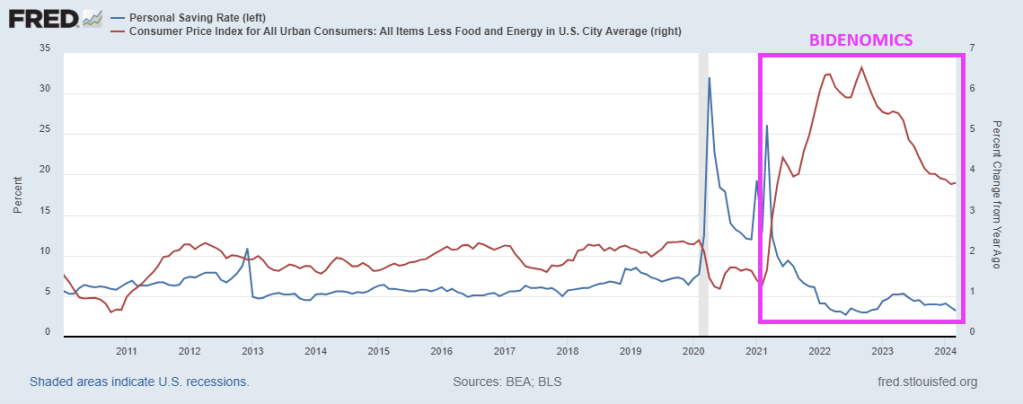

And with inflation, the US personal saving rate is near the lowest level since Obama (2010).

And with the core inflation rate still higher than anytime since 2010, households are paying more for … everything depleting their savings.

With Biden and Congress spending like drunken sailors on shore leave, and no end in sight, this will eventually explode. Ukraine, foreign aid, no border security, virtually no money for Maui fire, E. Palestine Ohio is still a wreck, etc. They always have money for someone else. And if Trump is elected in November, watch CNN and MSNBC and Biden/Congress blame Trump.

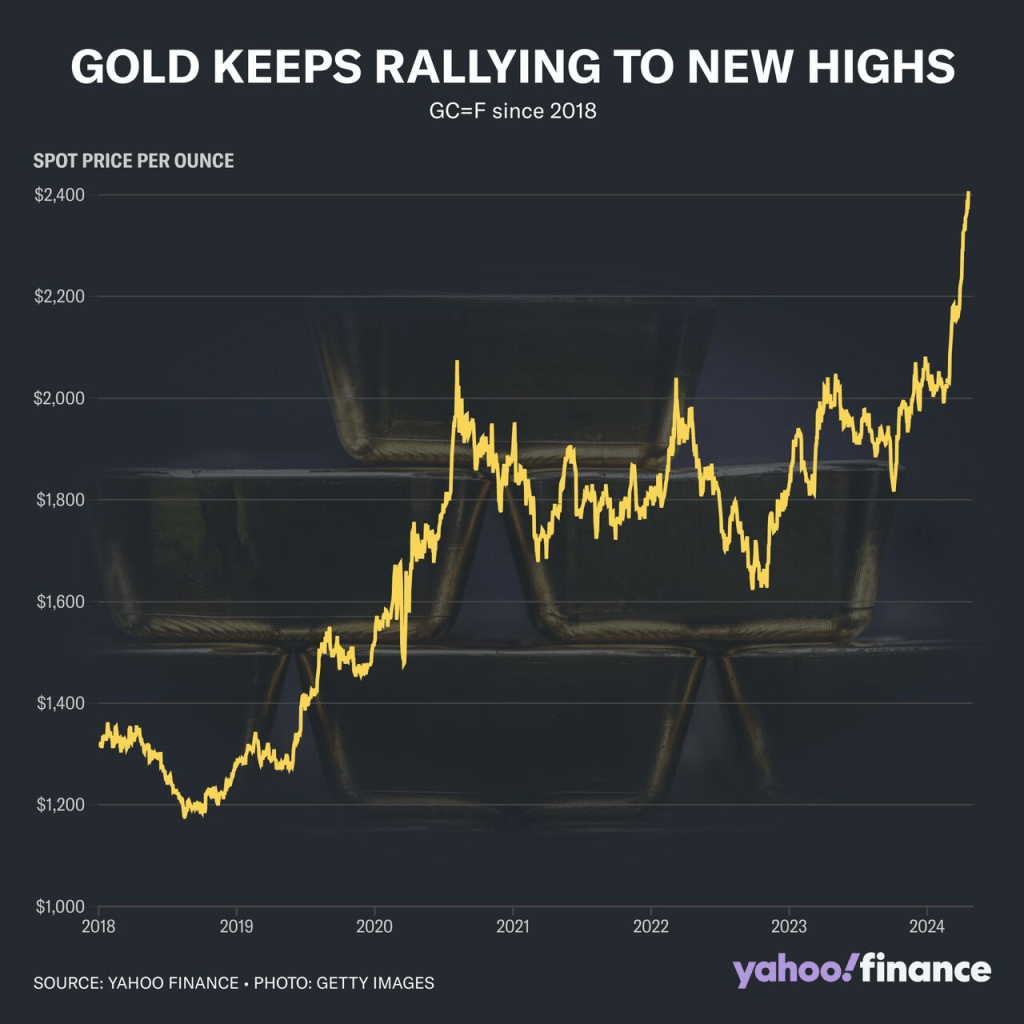

Commodities are a way to protect yourself against the government and their insane spending and debt.

My point? Gold keeps rising!

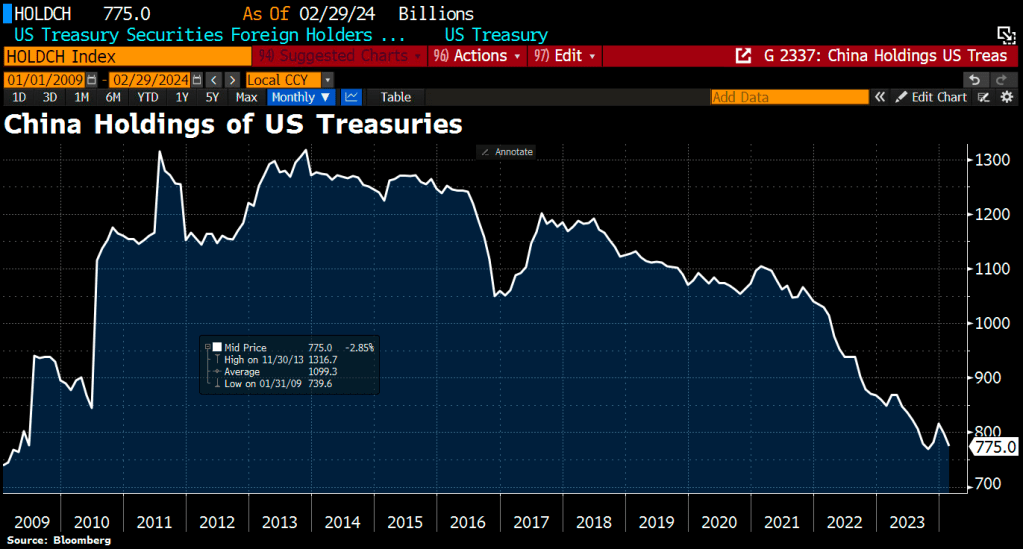

The leading foreign holder of US debt is Japan, which is following the insane path as the US and resembles a banana republic.

Former Fed chair under Obama and current Treasury Secretary Janet Yellen under Biden is Doctor Wonderful. NOT!!

I don’t know what Biden thinks is so funny. Maybe it is because House “Majority” Leader Mike Johnson (RINO-LA) gave Biden and Schumer everything they wanted (Ukraine, Israel funding but nada for security our borders). Life is good when you are stupid and mean-spiritied like Joe Biden!

Biden is so vain: capped teeth, hair plugs, constant tan, face lifts, etc.

The Green Slime! The global movement towards Green Energy (or global Marxist movement) is really The Green Slime! Or maybe it should be renamed “The Red Slime.”

And then we have Hertz dumping its inventory of EVs. A slew of used Teslas have hit the Hertz car sales website after the company announced Thursday it planned to sell off 10,000 more electric vehicles from its fleet than originally planned, bringing the fire sale’s total to 30,000. Perhaps one of the reasons you can get such a good deal on a Tesla at Hertz right now is that the outlook for EV value retention is pretty grim at the moment.

Given the incidents of electric cars catching fire, perhaps saying its a fire sales is a bad choice of words. But what it says is that DESPITE massive incentives to buy EVs, consumer demand stinks. Although Transportation Secretary Pete Buttigieg will claim the market is booming.

How bad is the trainwreck that is the Biden Regime? China is bailing on US Treasuries.

The Biden Regime is hereafter known as The Green Slime, given their horrible policies. Unfortunately, The Green Slime is here already … and Hertz knows customers don’t want them at least on a temporary basis.

The Federal Reserve is playing the song “Don’t rock the boat” ahead of the Presidential election. Despite the horrible economic news.

1) 4 months of hotter inflation (like today’s stagflationary GDP report)

2) Nearly 1.5 million full-time jobs decline with 1.9 part-time jobs created over a year

3) $2 trillion annual deficits

Leading traders to price in 1 rate cut in December 2024. AFTER THE PRESIDENTIAL ELECTION!

Under Biden, home prices are up 32.5% and conforming 30Y mortgage rates are UP 160%.

One of my colleagues at George Mason University in finance (an economics PhD) constantly quoted Lenin’s famous “You have to break a few eggs to make an omelet.” But why is it always OUR eggs that have to be cracked, never the wealthy elite.

COVID was a gift to Biden. The furious Federal spending of Q2 2020 through Q1 2021 helped keep GDP growth above recession levels.

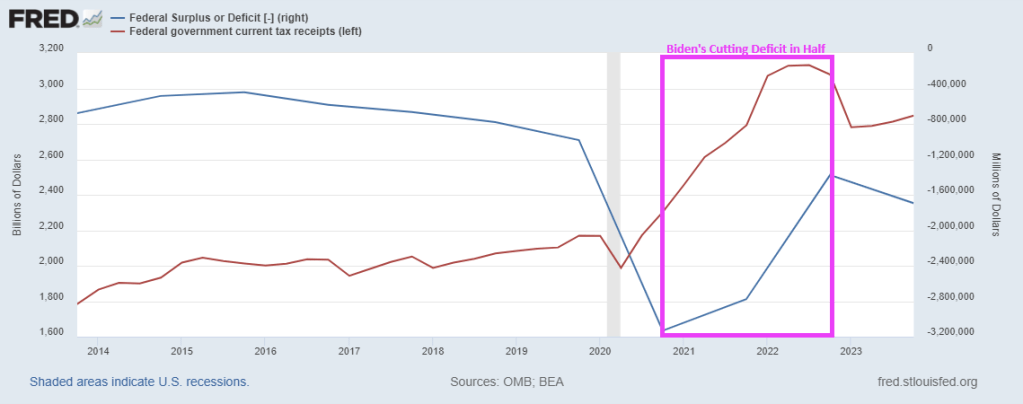

Ignore Biden’s demented rants/lies about cutting the debt in half. Biden has claimed he cut the $34+ trillion national debt by $7 billion, $1.4 trillion, $1.7 billion, $1.7 trillion, and “in half,” depending on the day he rants. He did no such thing. He is confused and is talking about the BUDGET DEFICIT (don’t look to Snopes to fact check “Trucker Joe”, they really only fact check Trump).

Not surprisingly, the Federal deficit spiked with the Covid lockdowns. But when the economy reopened, the budget deficit shrunk because … the economy was open and Federal tax receipts soared. But we are back to rising deficits again.

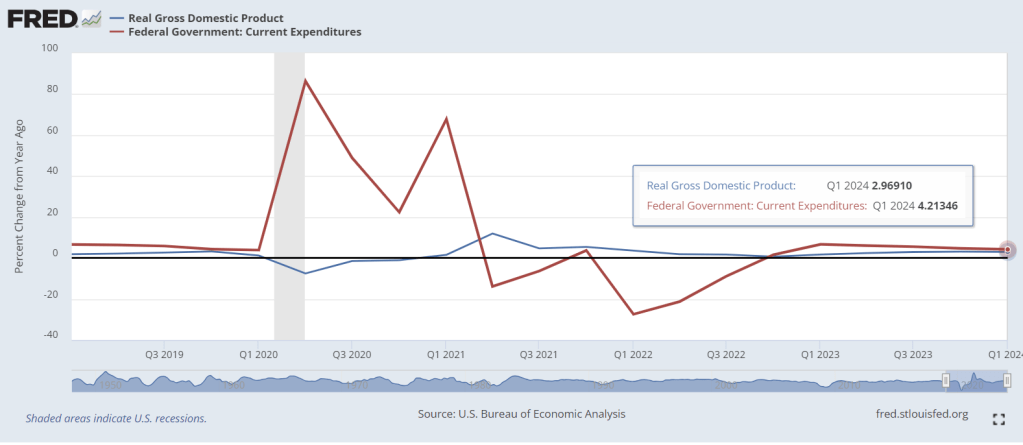

Today, Q1 GDP numbers were released and it looks great. Real GDP year-over-year was 2.97% while Federal government expenditures YoY were 4.21%. But the US is still processing the tidal wave of COVID-related spending out of Washington DC (red line). The YoY growth in Federal spending was 86.4% in Q2 2020, 48.9% in Q3 2020, 22.4% in Q4 2020, and 67.8% in Q1 2021. Like The Titanic trying to avoid the iceberg, it takes a while for massive Federal spending to work itself through the economic system.

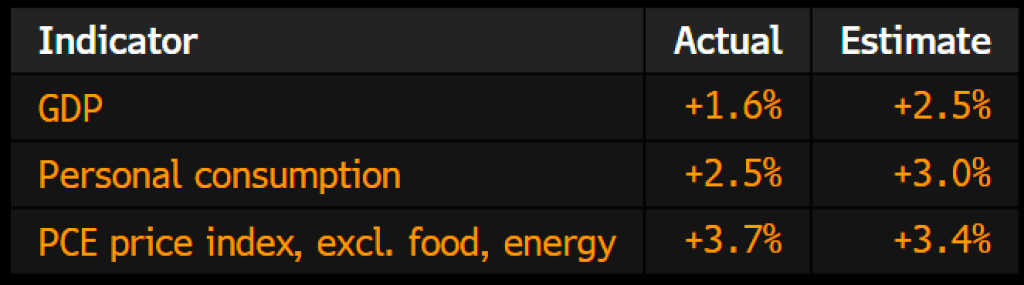

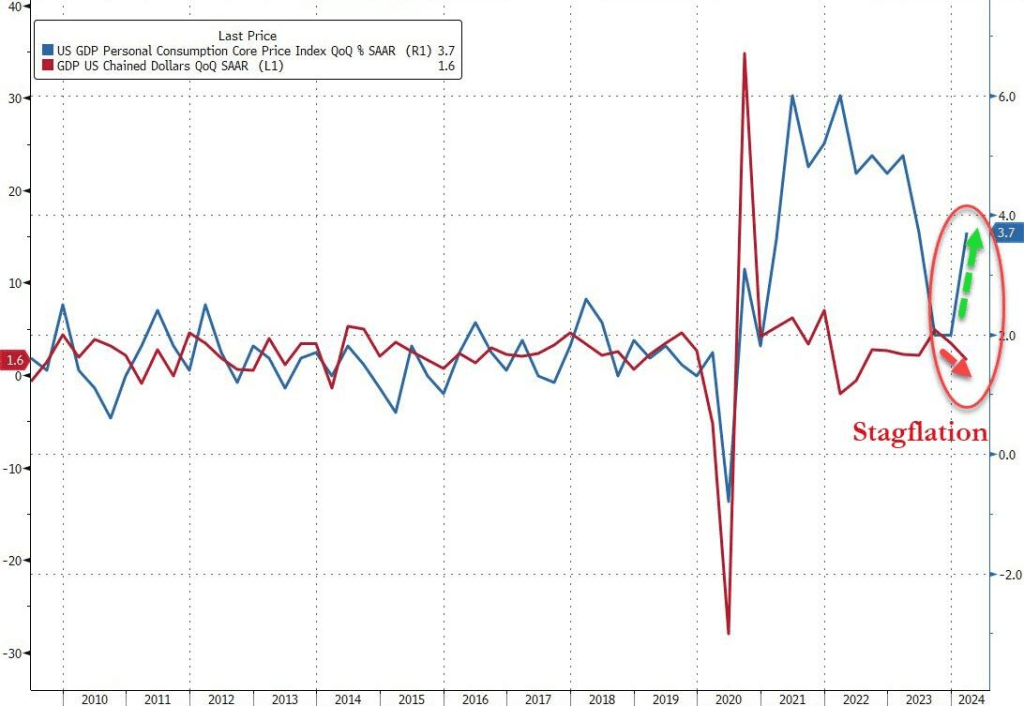

On a QoQ basis, US GDP increased by only 1.60%. Here are the contributions to GDP.

GDP QoQ was up 1.6% while Core PCE Price Index rose 3.7%. Yikes!

Are we entering Stagflation with the worst GDP print in 2 years as prices soar. As COVID stimulus seems to be wearing out.

Mortgage applications decreased 2.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 19, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 2 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index increased 0.2 percent compared with the previous week and was15 percent lower than the same week one year ago.

The Refinance Index decreased 6 percent from the previous week and was 3 percent higher than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 7.24 percent from 7.13 percent, with points increasing to 0.66 from 0.65 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

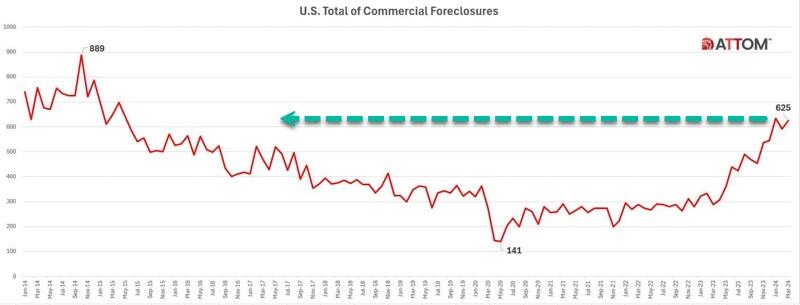

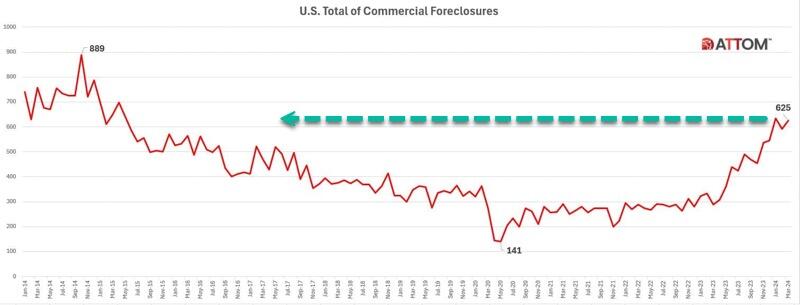

The latest report from real estate data provider ATTOM shows CRE foreclosures topped 625 in March, up 6% from February and 117% from the same period last year.

ATTOM has been tracking commercial foreclosures since 2014. The number of foreclosures is approaching the peak of 889 in October 2014.

“California began experiencing a notable rise in commercial foreclosures in November 2023, surpassing 100 cases and continuing to escalate thereafter,” the report said.

New York, Florida, Texas, and New Jersey also showed increases in CRE foreclosures last month.

Regional banks provide a bulk of the financing for the space. The ongoing mess in the lending space due to tighter conditions adds pressure to the CRE downturn. Banks are expected to set aside more money to cover potential CRE losses.

Last month, Federal Reserve Chair Jerome Powell testified on Capitol Hill, “We have identified the banks that have high commercial real estate concentrations, particularly office and retail and other ones that have been affected a lot,” adding, “This is a problem that we’ll be working on for years more, I’m sure. There will be bank failures, but not the big banks.”

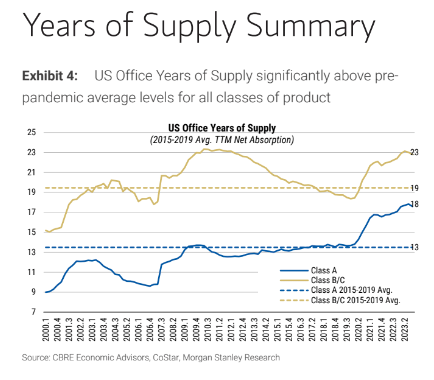

Data from a recent Treasury Department’s Financial Stability Oversight Council (FSOC) warned office vacancy rates have climbed sharply in recent years, reaching a record of 13.1% at the end of 2023.

CoStar analyst Phil Mobley recently noted the “reset in office demand has rocked US markets.”

Morgan Stanley warned earlier this year that office prices could plunge 30% due to sliding demand.

For those wondering why the excess supply of office towers can’t be converted into affordable housing, Goldman also noted that prices must drop 50% for housing conversions to make sense.

Powell has a rolling crisis on his hands. And the goal is to save the fireworks for after the election.

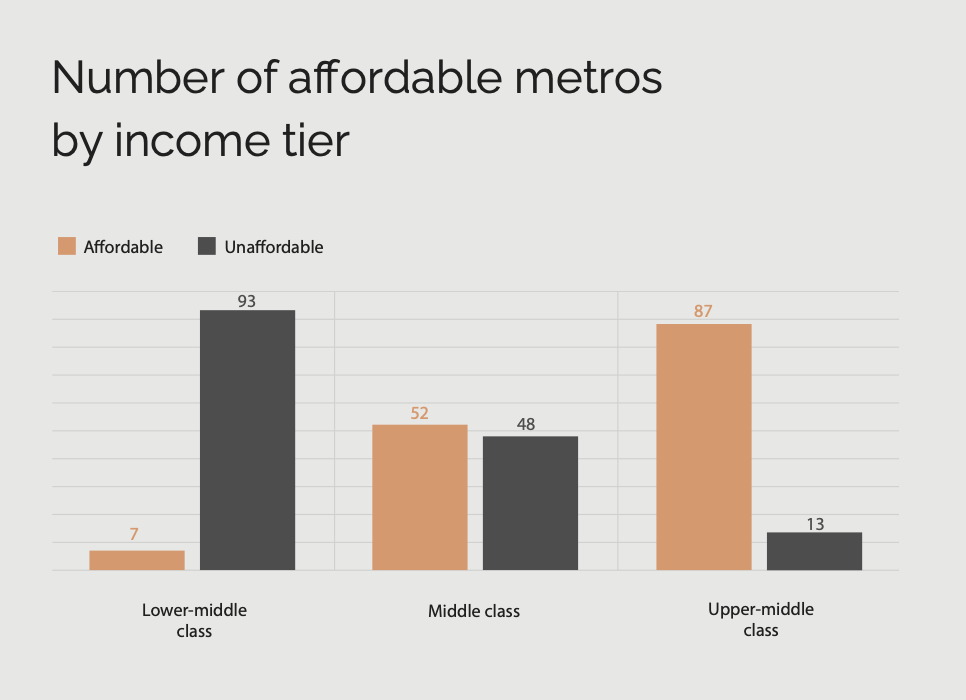

Housing is becoming an exclusively upper-class privilege in a growing number of cities.

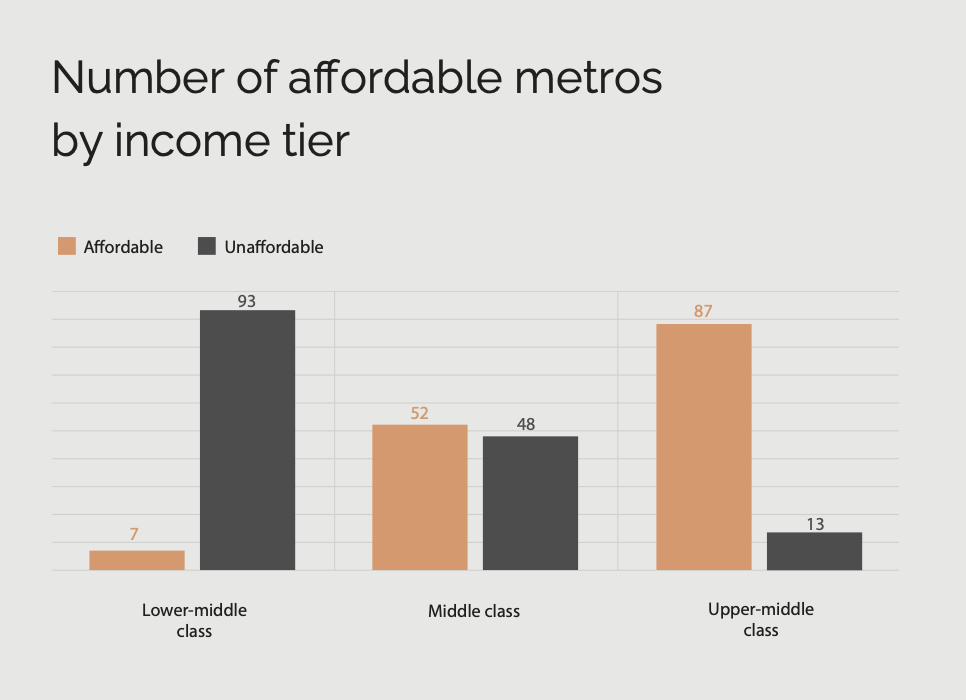

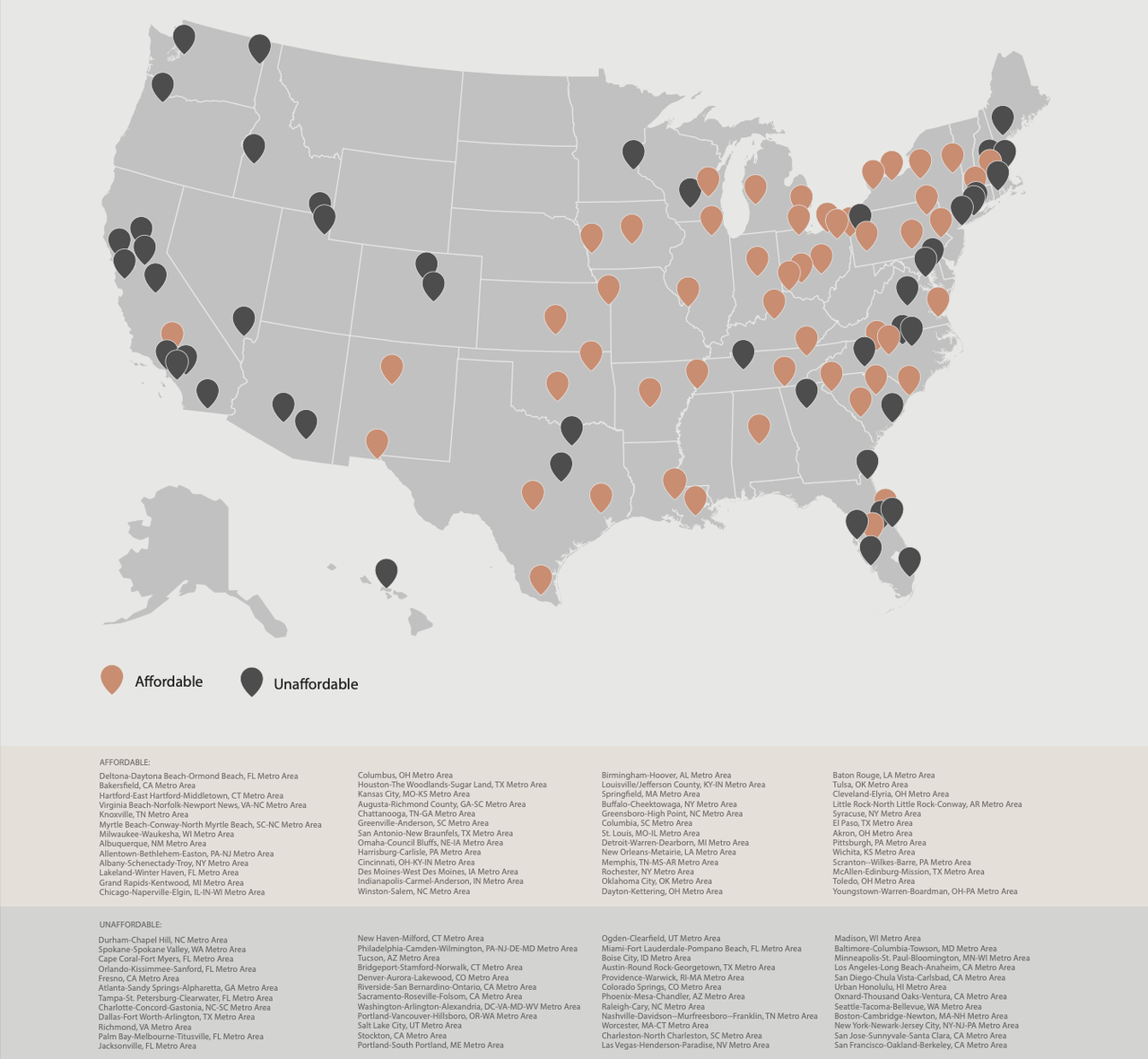

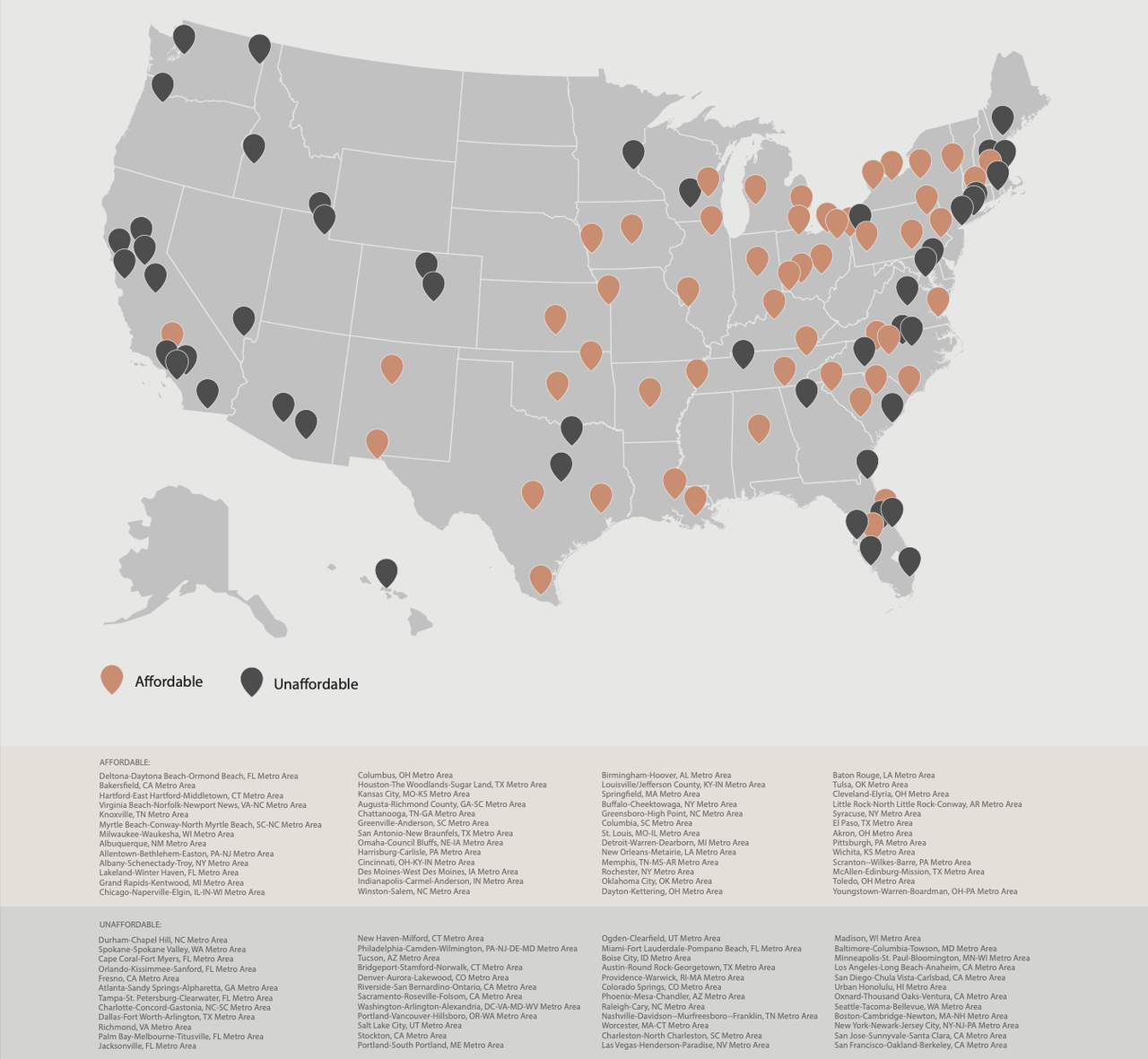

According to a new study by Creditnews Research, in 2024, middle-class households could afford to buy an average home in just 52 of the country’s 100 largest metros.

Just five years earlier, they could afford a home in 91 of the top 100 metros.

The situation is far worse for lower middle-class households, as they can only afford a home in seven of the largest 100 metros.

In total, 41 out of the 100 metros require a gross annual income of $100,000 or more to qualify for an average home. In 13 metros, an average income of more than $155,000 is needed.

In those cities, even the upper-middle class doesn’t qualify for an average home.

The study determined affordability by looking at how much income households need to earn to afford a down payment, mortgage payment, and related fees for an average home.

A home is considered affordable if monthly housing and mortgage costs don’t exceed 28% of a household’s gross income.

“There’s no two ways about it: Housing affordability has worsened significantly since Covid,” the report said. Since the pandemic, 39 of the most populous metros have fallen below the affordability threshold.

As expected, the most affordable areas for the middle class are located in the Midwest, Rust Belt, and parts of Texas, while the West Coast, Tri-State Area, and Hawaii are largely out of reach.

Affording a home is no longer a guarantee for the middle class

Being considered “middle class” doesn’t carry the same significance as it did just a few years ago.

“In the past, if you were middle class, it was almost assumed you would become a homeowner,” said Ali Wolf, chief economist of Zonda, a housing market research firm.

“Today, the aspiration is still there, but it is a lot more difficult. You have to be wealthy or lucky.”

That’s all thanks to a “perfect storm” of elevated mortgage rates, sky-high home prices, and a lack of inventory, making housing more unaffordable.

The result is that middle-income buyers, or those with an annual income of up to $75,000, could only afford about one-quarter of listings on the market last year.

According to Nadia Evangelou, the director of real estate research at the National Association of Realtors, “Middle-income buyers face the largest shortage of homes among all income groups, making it even harder for them to build wealth through homeownership.”

Mortgage rates (blue line) creep closer to 7%. Mortgage rates are UP 168% under Vacation Joe and home prices are up 32.5%.

After falling between November and January, mortgage rates are creeping back up.

According to Freddie Mac, 30-year fixed-rate mortgages reached 6.88% in the week of April 11 and at some point climbed well above 7%.

The reversal seems to be driven by a surprise spike in inflation, which has come out higher than expected for four consecutive months

“For homebuyers, the latest CPI report means mortgage rates will stay higher for longer because it makes the Fed unlikely to cut interest rates in the next few months,” said Chen Zaho, Redfin’s economic research lead.

“Housing costs are likely to continue going up for the near future, but persistently high mortgage rates and rising supply could cool home-price growth by the end of the year, taking some pressure off costs.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.