The talk of a gasoline tax “holiday” out of Washington DC is pure Kabuki theater. It is purely a sign of the times with Biden still trying to blame Putin for rising gasoline prices and inflation and ignoring his anti-fossil fuel policies that helped drive energy prices AND inflation through the roof.

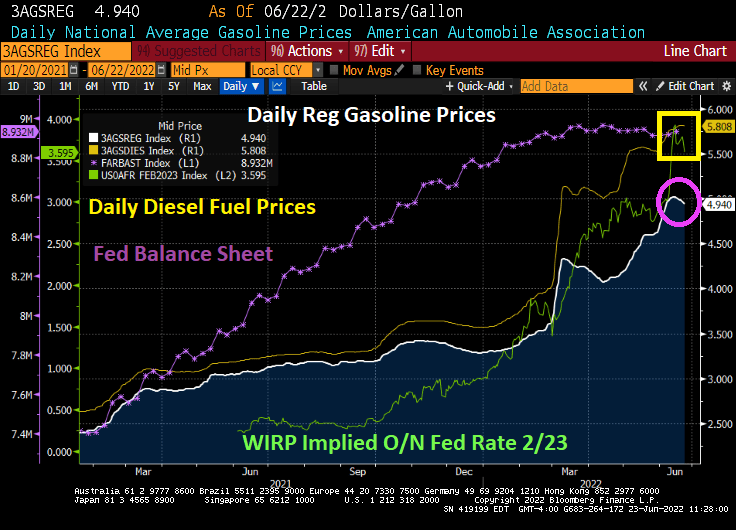

Daily regular gasoline prices have dipped below $5.00 to $4.94 while diesel fuel, the lifeline of the shipping industry, rose slightly to $5.80. I guess the folks shipping food and other goods don’t get a holiday.

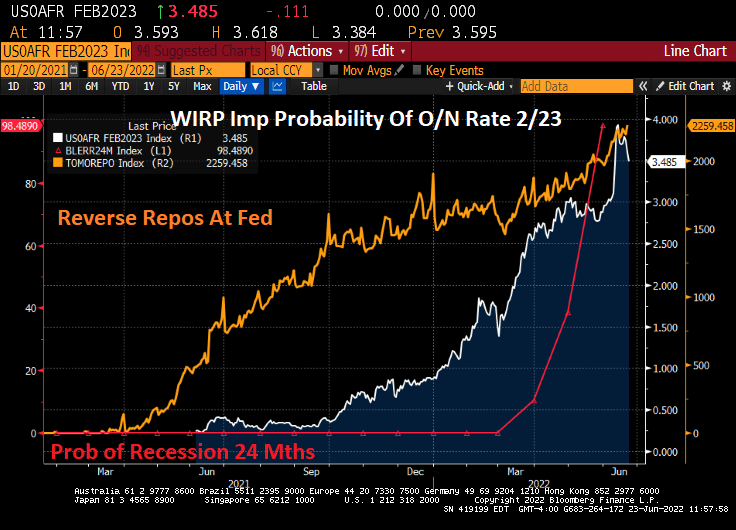

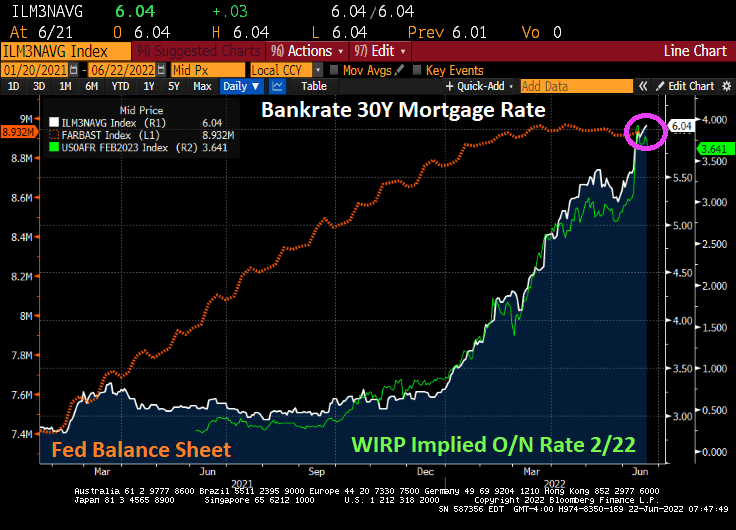

Note that the implied Fed target rate has fallen a bit as the probability of a recession increases.

And why are banks stashing so much money at The Fed in the form of reverse repos? Fear of recession, perhaps?

The Biden Administration is settling all kinds of records, and none are good.

You must be logged in to post a comment.