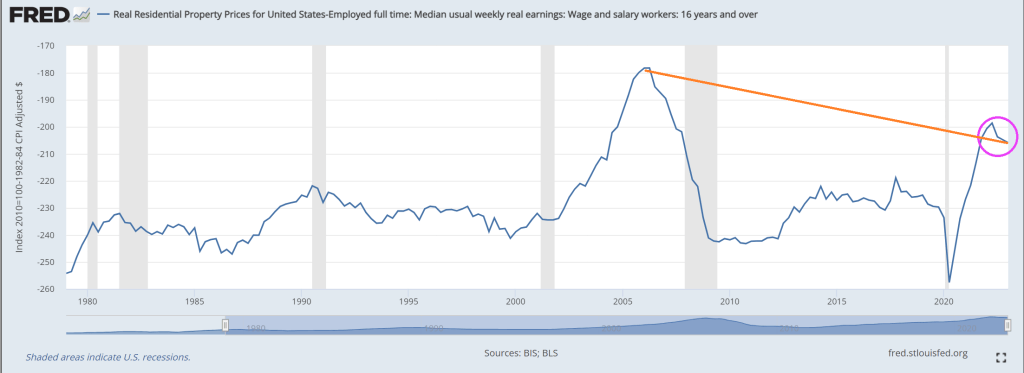

You know Bidenomics isn’t working at all when the best I can say about it is … the current housing bubble isn’t as bad as the house price bubble of 2006. We are truly in Biden’s ShamWow economy!

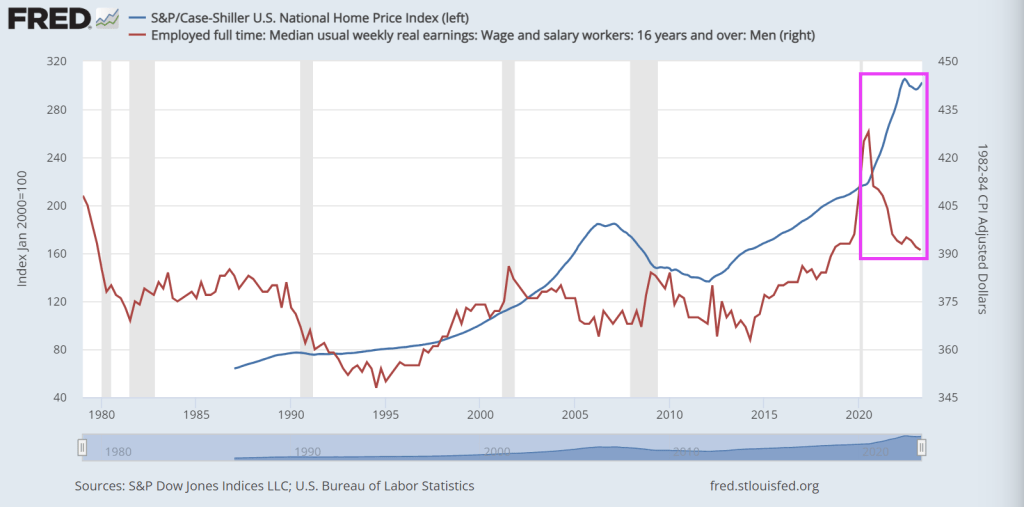

Yes, if I look at real home prices less real median earnings we can see that the ratio, while terrible, is still not as bad as the housing bubble of 2006.

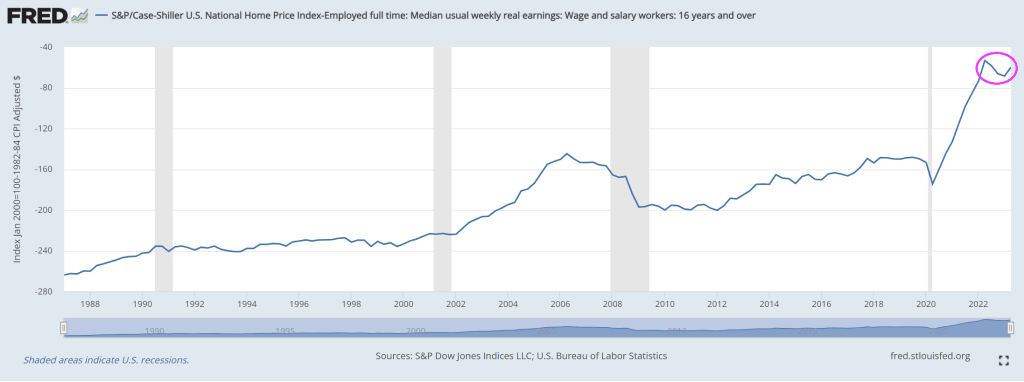

If I look at Case-Shiller National home price index less REAL median earnings, it is now far worse than in 2006.

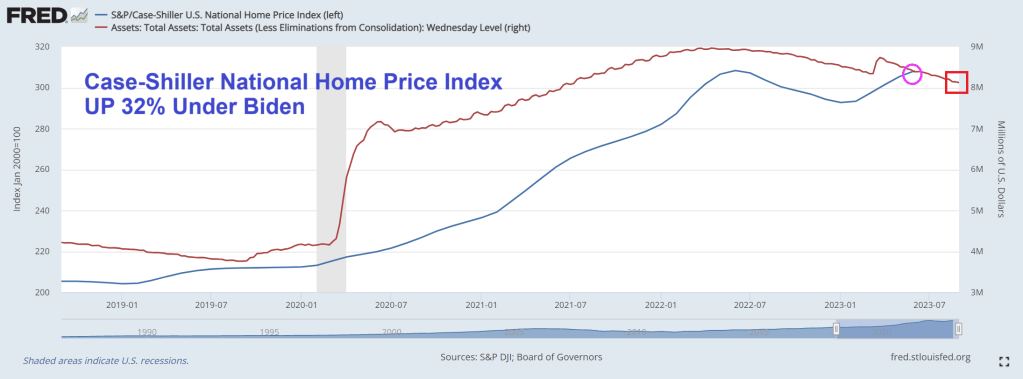

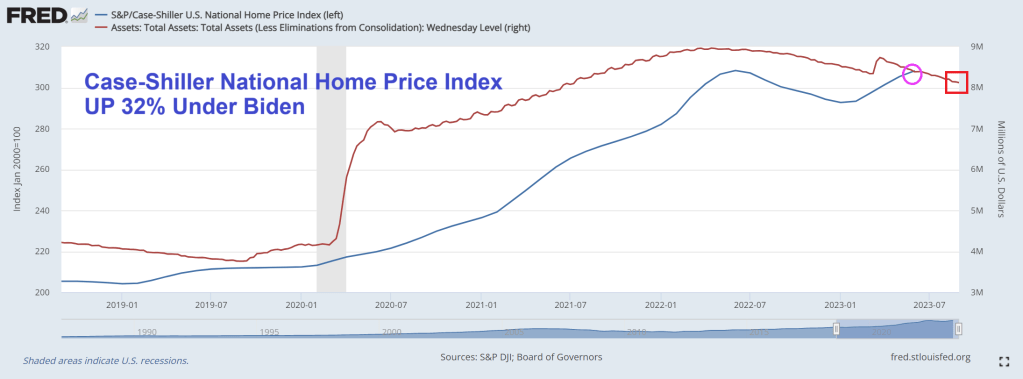

But home prices are still up 32% under Biden

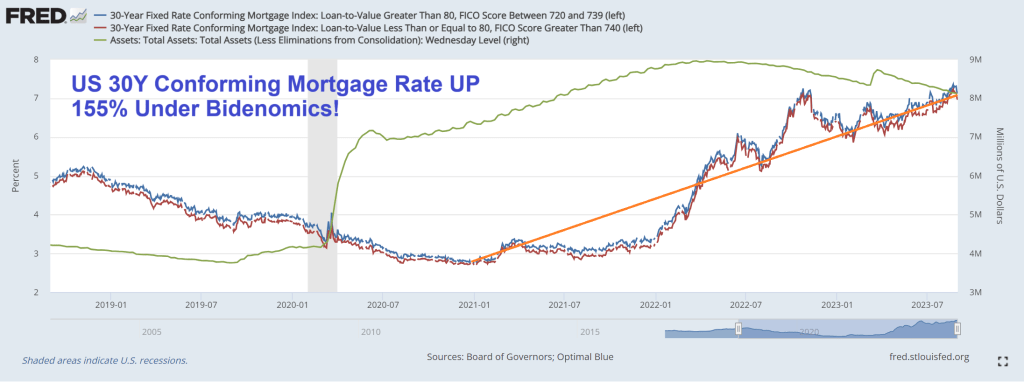

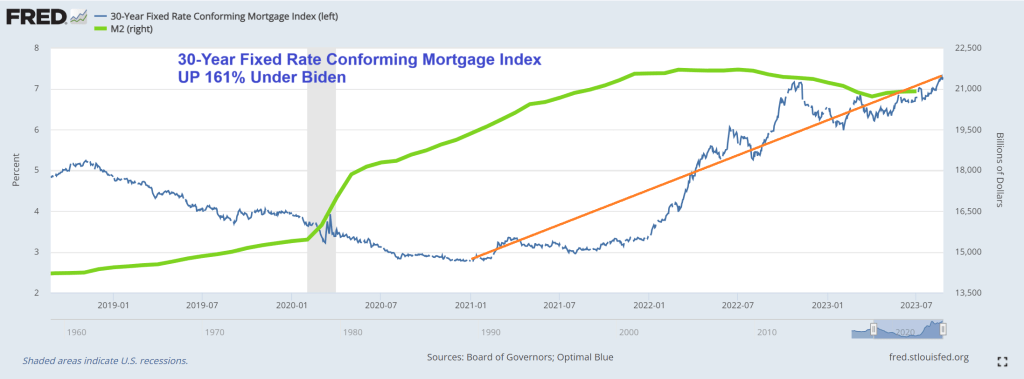

While the 30-year conforming mortgage rate is up 155% under Vacation Joe.

It should be GREEN ShamWow!. The money seems to be disappearing into the pockets of green energy donors, and Ukraine.

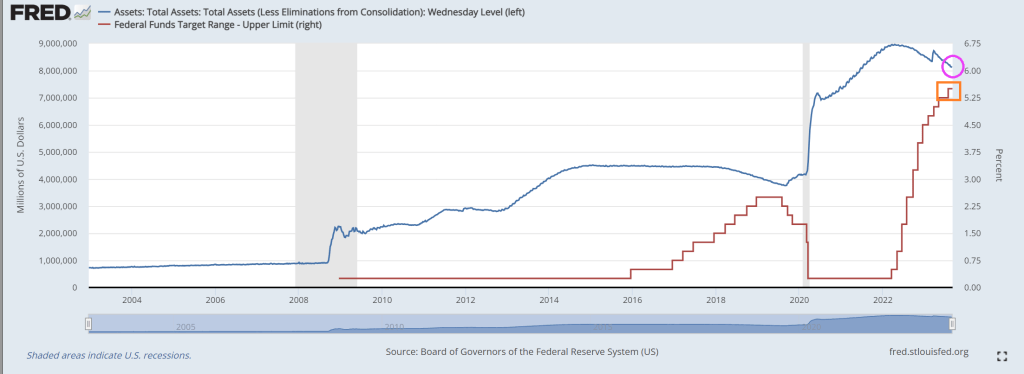

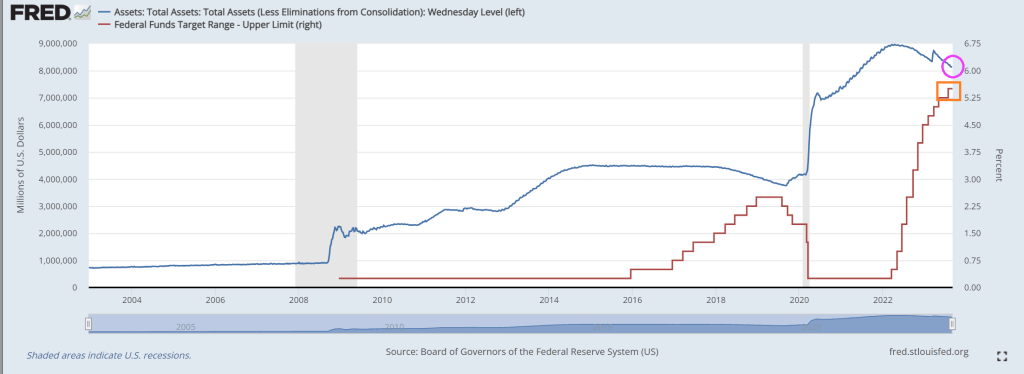

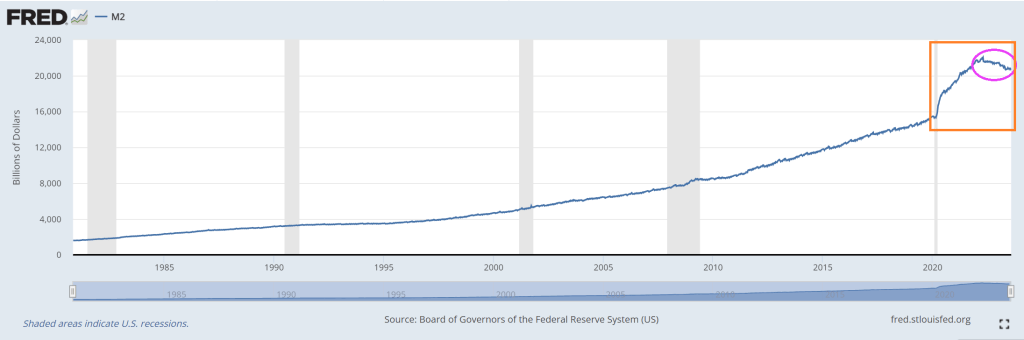

Under Bidenomics, there is still too much Fed monetary stimulus in the form of >$8 trillion on its balance sheet. While the biggest surge in Fed activity occurred with Covid, The Fed has added 10% to its balance sheet under Billions Biden.

Despite not backing off the assets purchases by The Fed, conforming 30Y mortgage rate is still up 155% under Bidenomics.

Yes, The Fed is raising its target rate to cool inflation, but doing little with its balance sheet.

The Case-Shiller national home price index is up 32% under Vacation Joe!

It seems prices are out of control and The Fed refuses to trim its balance sheet. But don’t worry, Vacation Joe is probably on yet another vacation while Maui and Flordia suffer and The Ukraine war is seeing bodies pile up. Meanwhile, he still hasn’t visited East Palestine Ohio like promised.

Soviet Joe Biden, who is a believer in Soviet-style command economies where rather than rely on free market capitalism, we now have CC (Crony Communism) running the US economy. Into the ground. But in the tradition of bad Federal policiies, Soviet Joe and Energy Secretary Granholm (with help from Congress) mandate green energy transition at all costs, watch the auto industry suffer, then bail them out. Sounds a lot of like the banking crisis of 2008 where The Federal government pushed homeownership until it helped almost collapse the banking sector, then the Federal government bailed out the banks. Rinse, repeat, bailout. And the bailout of banks in going! (Notice that The Fed has barely shrunk its $8+ trillion balance sheet!).

Automakers are looking to finish the week with strength after it was announced on Thursday that the Biden administration would be making “up to $12 billion” available to retrofit facilities to make both EVs and hybrids.

The money will include $10 billion from a US Energy Department loan program for clean vehicles and an additional $3.5 billion in financing to expand domestic battery manufacturing, according to Bloomberg.

The United Auto Workers, currently in negotiations with Detroit, has argued that a shift to EVs will cost the industry union jobs. US Energy Secretary Jennifer Granholm said on Thursday that the funding would help Detroit retain workers.

However, we’ve seen this “bailout” business model to save jobs before – at banks and during Covid, to name two examples – and it always winds up turning into a company cash grab before ultimately firing workers regardless. The UAW will try to prevent such a situation from taking place as it negotiates.

UAW President Shawn Fain “cautiously” welcomed the news after warning earlier this month that the White House should not push an EV agenda if it means the loss of jobs in Detroit.

Almost like the government should stay out of the auto industry as a whole, right? But that would make too much sense.

“The EV transition must be a just transition that ensures auto workers have a place in the new economy,” Fain said this week. Meanwhile, the Alliance for Automotive Innovation, a Washington lobby group that represents most Detroit automakers, said this week the funding “will further advance the domestic automotive supply chain and globally competitive battery manufacturing platform that automakers have already made sizable investments.”

Instead, Bloomberg calls the move the Biden administration “doubling down on efforts to support carmakers’ transition to EVs”. In a statement this week, President Biden said: “This funding will help existing workers keep their jobs and have the first shot to fill new good jobs as the car industry transforms for future generations.”

The Biden administration continues to aim for half of all vehicles on the road being EVs by 2030.

Oh and now that UAW Boss seeks 46% raise and 32-hour work week. Reminds me of Federal student loans where students run up massive amounts of debt to major in useless degrees like political “science” and gender/race studies, yet universities hire more admininstrators.

Covid is the gift that keeps on giving … to lazy bureaucrats and teachers union members. And a horror for small businesses and students since small businesse go bankrupt and students suffer from lack of education. And now The Federal Government is fearmongering (hey, that’s all they do!) ANOTHER Covid outbreak with Deep State Joe Biden advocating for more Federal spending on vaccines and telling everyone to get yet ANOTHER vaccination. And wear useless masks as a sign of obidience to The Democrat Party.

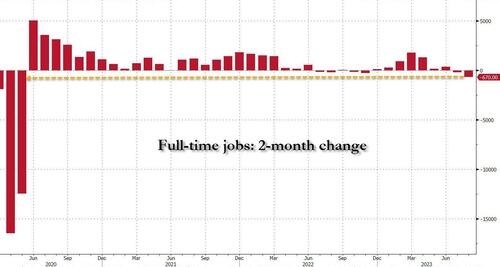

The Bureau of Labor Statistics (BLS) reported that in August the number of full-time jobs dropped again, sliding by 85K to 134.2 million, and followed the whopping 585K plunge in July which brings the two-month total drop in full-time jobs to a whopping 670K, the biggest 2-month plunge since the covid lockdowns in early 2020 when 12.5 million full-time jobs were lost in one month!

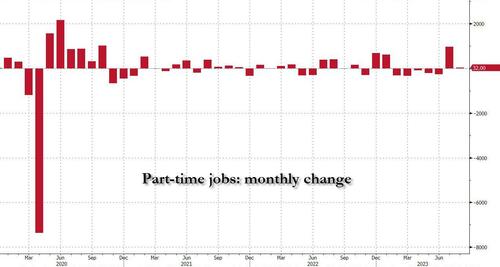

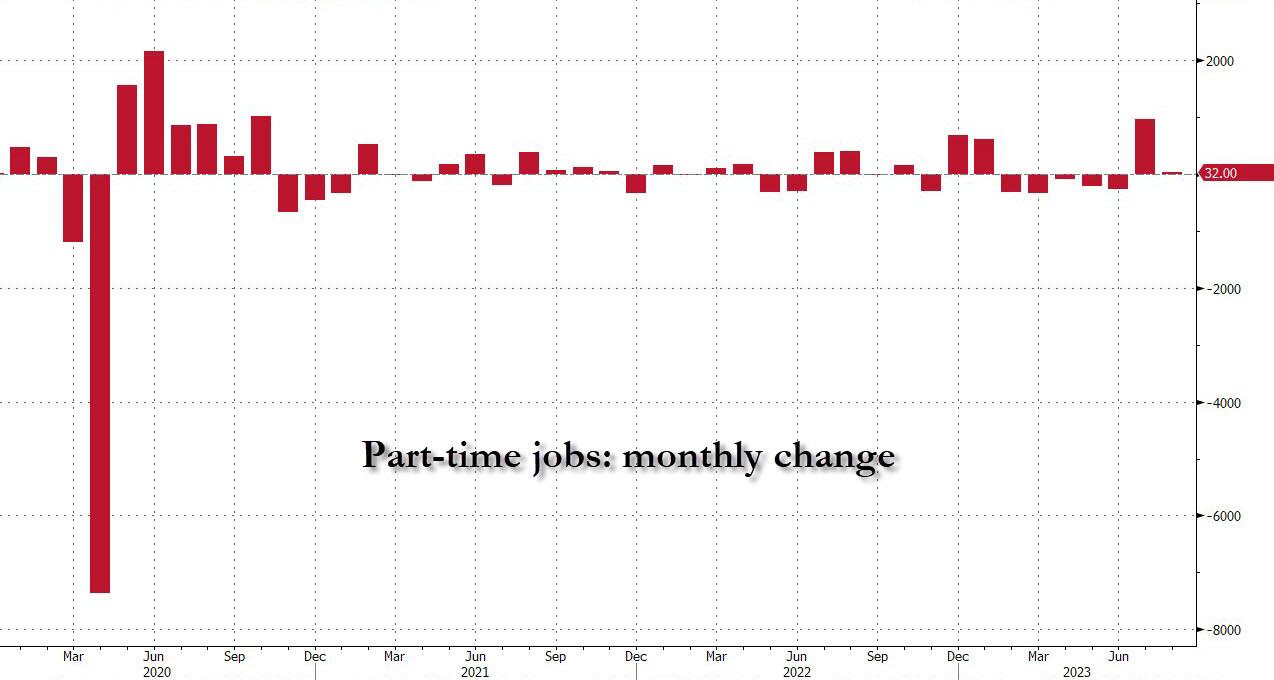

But if full-time jobs crashed how did the BLS get an increase of 222,000 employed workers? Simple: it was all in the latest jump of part-time workers. Indeed, in August the number of reported part-timers jumped by 32K and when added to the near-record 972K surge in July, the 2-month total was just over one million – 1,004,000 to be precise – to 27.185 million.

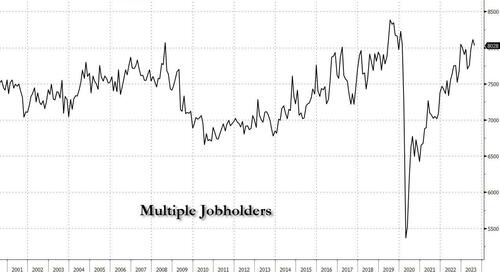

Going back to a quantitative read of the data, we look at the number of multiple jobholders – those workers who have to work more than one job at a time to make ends meet. In August this number was actually a modest silver lining, as it dropped by July, that number dropped by 85K to 8.028 million, but it remains just shy of the pre-covid record.

Given the extreme level of corruption in the Biden Administration, the Democrat Party should be renamed after New York’s Tammany Hall.

And require all people to wear a Tammany Hall fez instead of a mask.

The glories of Bidenomics is on fully display. Despite what Lyin’ Biden says, Bidenomics is only working for the elites (top 1%). How Soviet/CCP command economy of him!

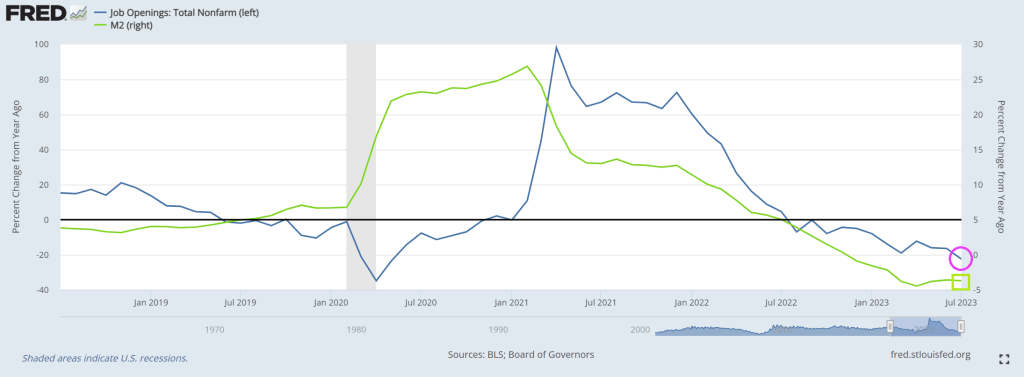

Here is an ugly chart showing Bidenomics in action! We all know that Covid unleashed a torrent of Fed monetary stimulus AND Federal spending on Covid relief and green energy subsidies (most to large Democrats donors). BUT we now have experienced 3 consectutive quarters of negative gross domestic income (GDI) growth. And nominal GDI growth is falling with falling M2 Money growth.

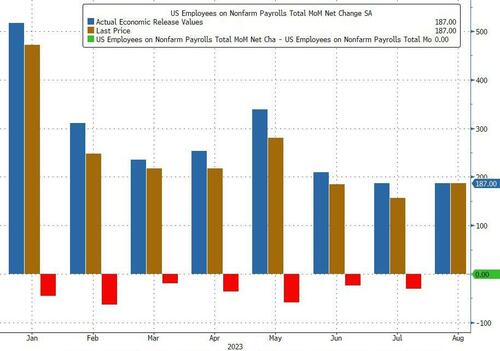

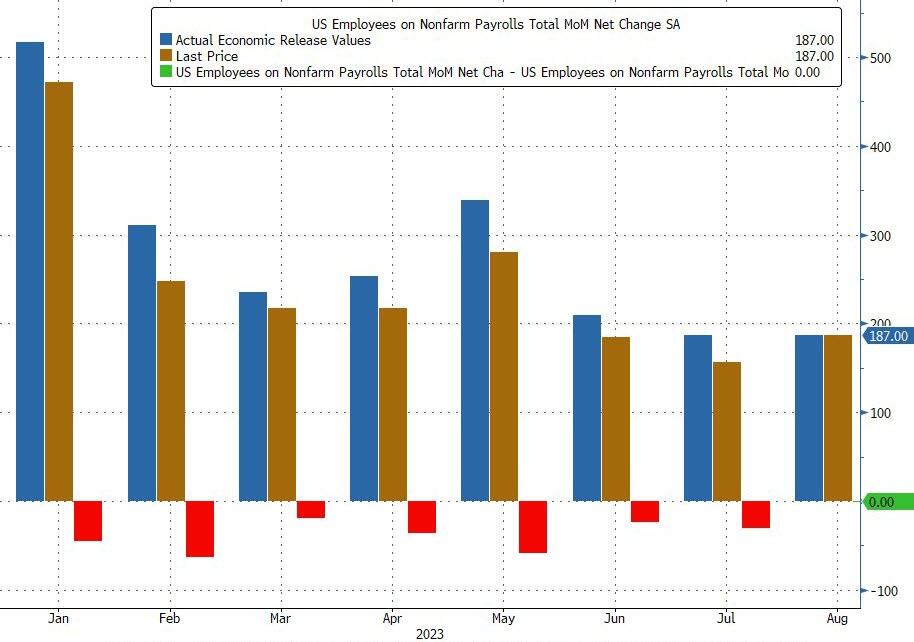

And today’s jobs report for August showed that only 187k jobs were added.

Superficially this would have meant an unchanged print from last month when the BLS also reported 187K jobs, however in keeping with recent trends that number was revised – drumroll – lower again, to 157K, meaning that every single monthly payrolls print in 20-23 has been revised lower (see chart below), a 12-sigma probability and virtually impossible unless there was political pressure to massage the data higher initially and then revise it lower when nobody is looking. (As if the mainstream media is at all honest!)

But wait there’s more: while July was revised down by 30K from +187,000 to +157,000, June was revised even more, by 80,000, from +185,000 to +105,000, which means that a number that was originally reported as 209K has been reivsed 50% lower, to 105K and a collapse vs original expectations of 230K. Here, the BLS was proud to report that “with these revisions, employment in June and July combined is 110,000 lower than previously reported.”

And we have The Conference Board’s confidence index at -65. Yikes!

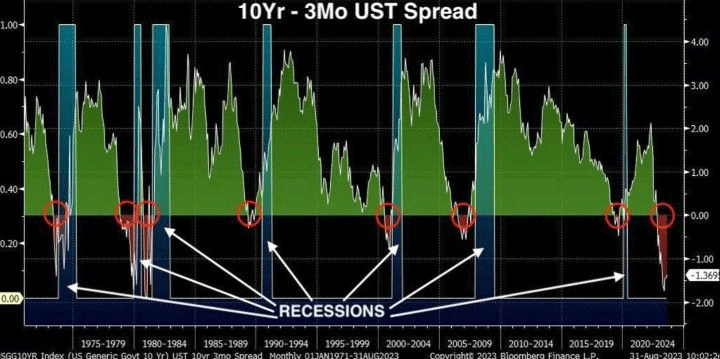

Finally, we have the 10Y-3M UST spread SCREAMING recession!

So, the economy is slowing under Bidenomics and Cadavar Joe.

Will Cadavar Joe actually go out on the campaign trail and debate ANY Democrat or Republican?? Remember, this is the man with the nuclear launch codes.

The 30-year conforming mortgage rate is currently 7.23%, up 161% under Biden and Bidenomics (code for massive Federal spending on green initiatives that go to large Democrat donors and Ukrainian oligarchs). Meanwhile, M2 Money supply is up 9.4% under Biden.

At the same time. home prices are UP 26% under Biden while Real Median Weekly Earnings are DOWN -5%.

On a sad note, it looks like The Federal government is starting to rattle its Covid saber just in time for the 2024 Presidential election. Odds are the US will ramp up online voting, early voting, etc. Think of John Fetterman (aka, Walter White’s twin brother) and the Pennsylvania voting experience.

Joe Biden is an incredibly weak President. I am not talking about his age or his deteriorating mental faculties. I am talking about ordering his attorney general to indict his chief political opponent, Donald Trump. How does the world interpret this weakness? BADLY.

The US has gone off the rails in terms of printing money, particularly since COVID struck and money printing went wild.

Under Biden’s Reign of Error and the US reckless money printing, more countries are abandoning King Dollar (based of fiat currency) and joining BRICS. Brazil, Russia, India, China, South Africa and a host of countries joining like Argentina, Saudi Arabia, Iran, Egypt, UAE, etc.

Now, the rest of the world is still stuck on the US Dollar as reserve currency … for now. But as Biden gets weaker and weaker, watch more countries join BRICs.

According to Reuters, there are over 40 countries that have expressed interest in joining BRICS. A smaller group of 16 countries have actually applied for membership, though, and this list includes Algeria, Cuba, Indonesia, Palestine, and Vietnam. Pretty soon, under Biden’s crazy leadership, we may be the last man standing in using the US Dollar as reserve currency.

Then we have the other shoe dropping with Bidenomics.

As soon as Biden took office, he set out to destroy industries that produce reasonably priced energy. He focused tremendous effort on deficit spending and borrowing to hand out “government goodies” to buy votes; recipients of this government largesse, in large part, included debt-saddled students, the green mafia, and leftist activists.

When Biden took office, inflation was under 2%, despite COVID and supply chain disruptions; shortly after, it skyrocketed to over 9%. Now inflation increases are “down” but prices remain exceptionally high compared to pre-Biden.

For example, crude oil prices, which affect almost everything and are used in over 6,000 products, are roughly double what they were when Biden took over.

President Trump focused on reduced regulations and energy independence, and implemented lower tax rates, all moves that greatly helped the American people. In contrast, Biden focuses on ensuring bureaucrats rapidly increase regulations which raises costs for everyday Americans; he’s waging economic war against us. Very few of Biden’s regulations go through Congress. From the White House archives:

Between FY 2017 and FY 2019, the Trump Administration has cut nearly eight regulations for every new, significant regulation….

The Council of Economic Advisers (CEA) estimates that this pro-growth approach to Federal regulation will raise real incomes by upwards of $3,100 per household per year.

Here are some recent reports of how well Biden policies are working:

Leading economic indicators have fallen for sixteen straight months. Maybe that is why people think the economy is moving in the wrong direction?

The current cost-of-living crisis is a manufactured one. As inflation rose, the Federal Reserve was forced to raise interest rates, which saw fewer people move. The cycle is very understandable, as simply explained in this one headline, “Housing Crunch: Home Sales Fall To Six Month Low…But Prices Rise Anyway”.

Parcel volumes are dropping by so much, freight pilots are “worried” about job security.

People are running up credit card debt and defaulting on car loans because of high inflation, and because their real wages haven’t been able to sustain them. Now, even more are falling behind on their payments. From CNN:

More Americans are failing to make payments on their credit cards and auto loans, another sign of rising financial pressure on consumers.

New credit card and auto loan delinquencies have now surpassed pre-Covid levels, according to a Wednesday report issued by Moody’s Investors Service.

After years of promoting and subsidizing electric cars, they represent around 6% of total sales, and demand is clearly slowing. It wasn’t that long ago that well-to-do people were buying these electric toys so quickly that they were placed on waiting lists; now, inventories are building because they are too impractical and expensive:

Auto News understands that there is currently a 103-day supply of unsold EVs in the United States. While it did not specify how many units are sitting on dealership lots, it says there is a higher supply of unsold EVs than any other automotive segment, except those in the ultra-luxury and high-end luxury segments with supplies also reaching over 100 days.

So what is Biden’s solution? Force people to buy them.

Here are some simple economics questions for the media and other Democrats:

Does flooding the U.S with illegals help or hurt housing availability and affordability?

Will the intentional destruction of oil and coal companies help or hurt the middle class and the poor?

Yet, the media and other Democrats brag that Biden’s economic policies are great, and when the public gives Biden poor marks, they say that we just don’t understand, and we’re not willing to get behind a candidate if they fail to make us feel “warm and fuzzy.”

Are journalists really that unaware?

Of course, they always sought to destroy Trump as his policies, even as poverty sank to record lows amongst minorities, because they don’t really care about anything but big government. According to Census data:

In 2019, the poverty rate for the United States was 10.5%, the lowest since estimates were first released for 1959.

Poverty rates declined between 2018 and 2019 for all major race and Hispanic origin groups.

Two of these groups, Blacks and Hispanics, reached historic lows in their poverty rates in 2019.

Results and facts haven’t mattered to the complicit leftist media for a long time.

And perhaps the worst mistake Biden made (amongst his laundry list of horrible mistakes, [Afghanistan retreat, not showing up to E Palestine Ohio, Bidenomics that is a payoff to green donors and BIG corporate interests, an embarrasing visit to Maui two weeks after the fire, indicting his leading political opponent, ….) is the appointment of the WORST Federal Reserve Chair (Janet Yellen) as Treasury Secretary.

Joe Biden will always be remembered for lying about never raising taxes on households making under $400,000. Inflation is a permanent tax, mostly on those making under $400,000 per year. And household essentials are up substantially under Biden: gasoline prices are up 72%, rent CPI of Primary Residence is up 16%, and food at home CPI is up 20%! That is a HUGE tax on the middle class.

When CPI falls this does not mean that prices on goods and services are going down, it only indicates that prices are rising slower than they were the month or the year before.

Another misconception about CPI is that it measures the inflation rate accurately for regular consumers on common purchases. In reality, the CPI represents mean average price rate increase for a vast basket of goods; over 94,000 items and services with over 200 separate categories. Most of these items and services you will never use or rarely purchase in the span of a year. In other words, inflation declines in uncommon goods can dilute the numbers, making it seem like inflation is dropping while prices on daily necessities continue to spike.

The CPI is weighted according to consumer spending patterns, which is where the calculations can be “adjusted” to a certain extent in an arbitrary manner. Then there is outright government manipulation through various means. As we witnessed recently with the Biden Administration’s claims that “Bidenomics” has defeated the inflation threat, what these reports don’t mention is that Biden has been dumping US strategic oil reserves on the market for the past year. And since energy prices effect the inflation of so many other categories, Biden has artificially manipulated the CPI down using one key resource.

Now that his ability to dump oil reserves has ended, CPI will rise once again along with energy prices.

The point is, it’s impossible to get a sense of the real damage from inflation without looking at the cumulative inflation in necessities (the goods and services that people are required to purchase on a regular basis to live day to day). If we throw out the CPI distraction and look at common necessities since 2020, the economic picture is far more bleak.

Overall food prices have soared by 25%-30% in only three years (again, this means that you are now paying 30% more this year for food than you were paying at the beginning of 2020). Chicken is up from $3 per pound to $4 per pound. Beef is up from $3.50 to $6 per pound. Corn is up from $3.50 per pound to $4.70 per pound. Wheat is up from $5 per pound to $7 per pound. In 2019 the average American household was spending $8100 on food annually; with a 30% increase, in 2023 Americans will be spending at least $10,500 per household.

By the end of 2019, the average rental price of a single family home was around $1450 per month. This year the price is around $2000 per month. At the beginning of 2020, the median cost of a home was $320,000; by 2023 the price skyrocketed to an average of $416,000.

For gasoline, the price in early 2020 was around $2.50 per gallon. The price has fluctuated dramatically due to Biden’s manipulation of the market using strategic reserves, but still remains high today at $3.80 per gallon.

The cost of electricity has risen swiftly, holding steady around .13 cents per kilowatt hour for a decade, then spiking to at least .17 cents per kilowatt hour by 2023.

Remember, most of these costs are static and are difficult to reduce through household spending cuts. These are not items that are easily removed from a monthly budget and the expenditures add up to considerable pressure on consumer accounts. This is probably why around 74% of the public in polls say that the economy is getting worse, not better. It’s because government statistics are not highlighting the true inflationary crisis.

When we look at the cumulative climb of prices in necessities since before the inflation crisis officially began, the truth is that Americans now have to increase their wages by at least 25%-30% on average to maintain the same standard of living they had three years ago. This is a disaster not seen since the stagflationary event of the 1970s and early 1980s. If you have a strange feeling like your bank account is being rapidly drained in recent months, that’s because it is.

And the 30-year mortgage rate is up 163% under Middle Class Joe.

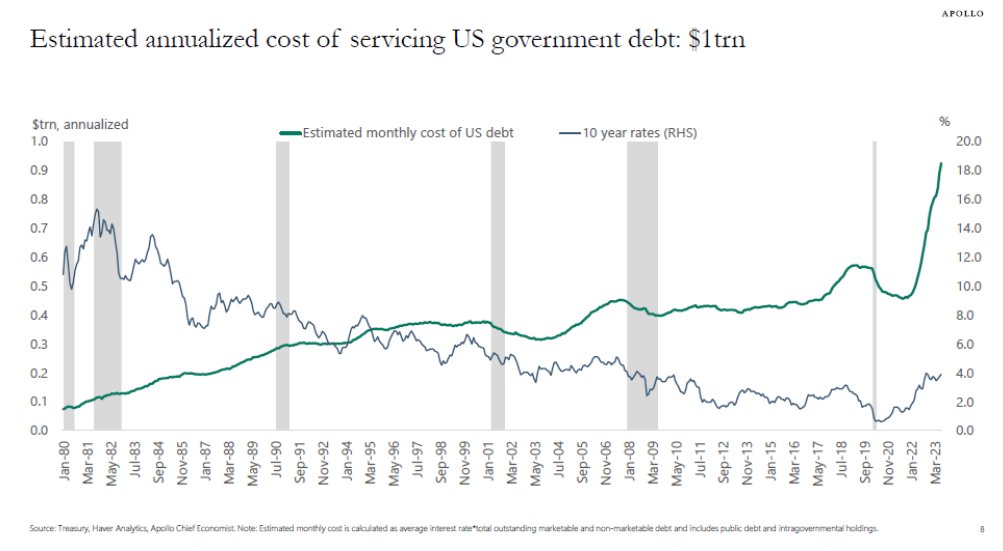

Let’s see. We have inflation that is eroding wage growth so that REAL wage growth is negative. Meanwhile, the Biden Administration and Congress are spending like they can print infinite amounts of cash with no consequences. The result? The Federal government is paying nearly $1 trillion in interest on an annualized basis.

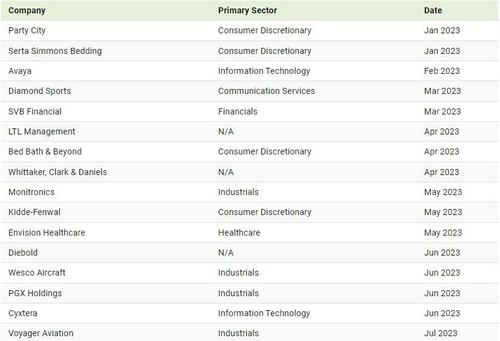

On the corporate side, we are seeing a surge in bankruptcies.

So far in 2023, over 400 corporations have gone under. Corporate bankruptcies are rising at the fastest pace since 2010 (barring the pandemic), and are double the level seen this time last year.

Below, we show trends in corporate casualties with data as of July 31, 2023:

Represents public or private companies with public debt where either assets or liabilities are greater than or equal to $2 million, or private companies where assets or liabilities are greater than or equal to $10 million at time of bankruptcy.

Firms in the consumer discretionary and industrial sectors have seen the most bankruptcies, based on available data. Historically, both sectors carry significant debt on their balance sheets compared to other sectors, putting them at higher risk in a rising rate environment.

Overall, U.S. corporate interest costs have increased 22% annually compared to the first quarter of 2021. These additional costs, combined with higher wages, energy, and materials, among others, mean that companies may be under greater pressure to cut costs, restructure their debt, or in the worst case, fold.

Billion-Dollar Bankruptcies

This year, 16 companies with over $1 billion in liabilities have filed for bankruptcy. Among the most notable are retail chain Bed Bath & Beyond and the parent company of Silicon Valley Bank.

Mattress giant Serta Simmons filed for bankruptcy early this year. It once made up nearly 20% of bedding sales in America. With a vast share of debt coming due this year, the company was unable to make payments due to higher borrowing costs.

What Comes Next?

In many ways, U.S. corporations have been resilient despite the sharp rise in borrowing costs and economic uncertainty.

This can be explained in part by stronger than anticipated profits seen in 2022. While some companies have cut costs, others have hiked prices in an inflationary environment, creating buffers for rising interest payments. Still, S&P 500 earnings have begun to slow this year, falling over 5% in the second quarter compared to last year.

Secondly, the structure of corporate debt is much different than before the global financial crash. Many companies locked in fixed-rate debt over longer periods after the crisis. Today, roughly 72% of rated U.S. corporate debt has fixed rates.

At the same time, banks are getting more creative with their lending structures when companies get into trouble. There has been a record “extend and amend” activity for certain types of corporate bonds. This debt restructuring is enabling companies to keep operating.

The bad news is that corporate debt swelled during the pandemic, and eventually this debt will come due likely at much higher costs and with more severe consequences.

The face of Bidenomics: the top 1% are gleefull (like Billions Biden), the bottom 99% are mournful.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.