The US Empire State Manufacturing Survey General Business Conditions SA index fell to -9.1 in October, continuing a downward trend along with the downward trend in Fed M2 Money stock growth.

And the global sovereign debt market is showing fear as 10-year sovereign yields drop -10 basis points. The UK 10-year is down -36.8 bps! The US is down only -6.6 bps this morning.

Over the past year, the dollar has been on a tear: The U.S. Dollar Index, which measures the dollar’s strength against a basket of foreign currencies, is up 18%. And up 25.2% under 80-year old US President Joe Biden (well, he will be 80 in November).

For tourists, a strong dollar is great news. It means you get more for your money abroad.

But for investors, a beefed-up buck is decidedly bad news.

When the dollar strengthens, that means foreign revenues are going to translate into fewer dollars. Those earnings are going to come in lower and any overseas investment you own is going to hurt you in a rising dollar environment.

The University of Michigan’s consumer sentiment index for housing for October just fell to its lowest level since 1992 as The Fed counterattacks against Bidenflation, causing mortgage interest rates to rise.

Of course, despite slowing home price growth, expensive home prices are really hurting along with expensive rents. But how sustainable are high home prices when REAL average hourly earnings growth is negative??

Mortgage applications decreased 2.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 7, 2022. As mortgage rates soar with Federal Reserve tightening.

The Refinance Index decreased 2 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 39 percent lower than the same week one year ago.

Inflation is a multi-headed hydra (from Greek Mythology). It is composed of 1) monetary stimulus (that The Fed is slowly withdrawing), 2) massive, reckless Federal spending and 3) Biden’s anti-fossil fuel mandates. So, when the inflation numbers are out later this week, it will be fun to dissect the damage being done to the US economy and middle-class/low-wage workers.

Take Los Angeles, for example. The life blood of the shipping industry, diesel fuel, is UP 176% under Biden, despite declining for a short period of time. And the DOE Strategic Petroleum Reserve is DOWN -34.7% under Biden.

Here is a photo of Jerome Powell (Fed Chair) trying to fight the inflation hydra. Unfortunately, one of the inflation hydra heads is The Federal Reserve itself.

Another casualty of The Fed’s tightening and reduction in M2 Money supply are … the mortgage and housing markets. The US mortgage rate has soared to 7.04% (highest since 2000) and mortgage DEMAND has fallen to the lowest level in recorded history.

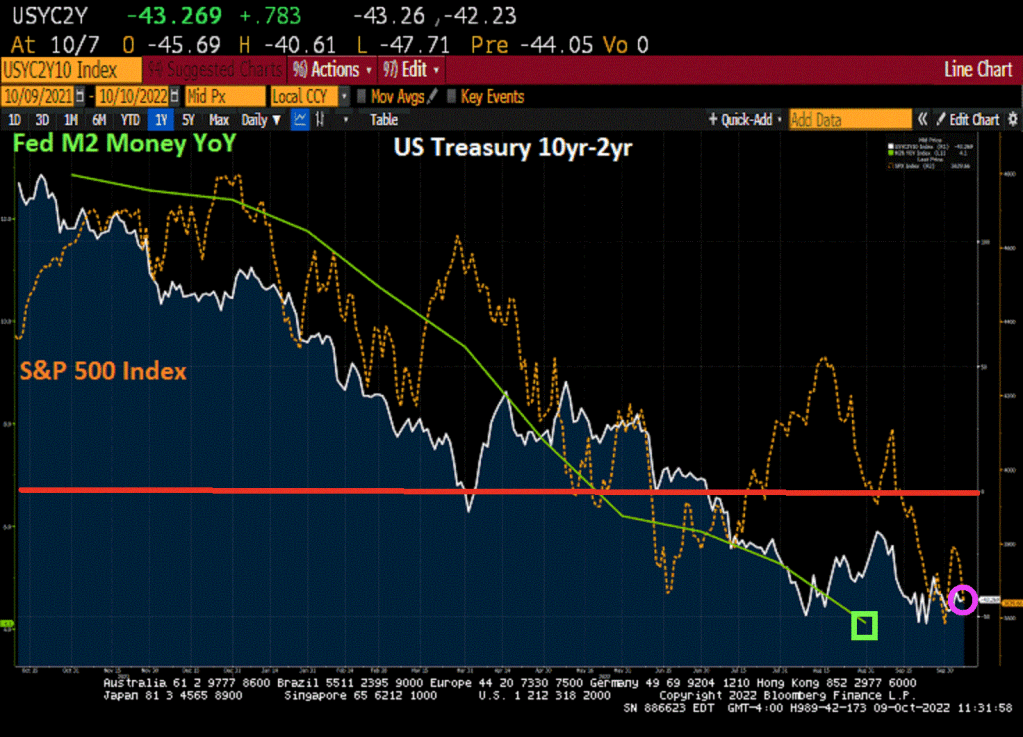

Here is my chart from yesterday showing the inversion of the US Treasury 10yr-2yr curve and decline in the S&P 500 index as The Fed tightens.

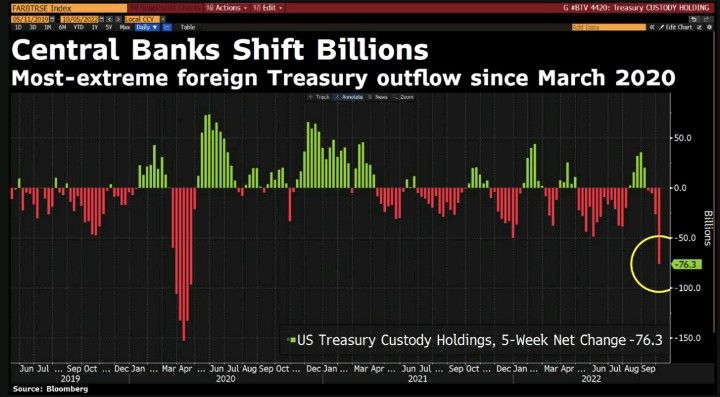

And then we have this chart showing the most-extreme foreign Treasury outflow since March 2020.

At least The Fed is predicted to start cutting rates again in March 2020.

Yes, Biden and Powell have reenacted Kevin’s famous chili spill. And Ben Bernanke, the creator of QE from late 2008 was just award the Nobel Prize in economics for distorting financial markets.

Sweet home DC! At least for the ruling elites. For the rest of us mortals, Bidenflation is crushing our finances.

To combat Bidenflation, The Fed has signaled that they will continue to raise interest rates. But at what cost?

(Bloomberg) — The world’s leading central banks are finally pushing their interest rates into restrictive territory, causing fears of overkill in financial markets and stoking chatter that policymakers may need to pivot at some point.

And with the withdrawal of monetary stimulus comes the slowdown of US M2 Money growth (green line). And with that slowdown, we see a declining stock market and an inverted US Treasury yield curve.

Of course, Biden could reverse his green energy agenda and allow for oil and natural gas exploration … again. Or begin building nuclear power plants again. But nooooo.

Another peril is rising mortgage rates.

Here is the S&P 500 against global liquidity.

Speaking of Freddie King, here is Joe Biden’s favorite song: hideaway.

Yesterday, I told my family “The good news is that Rotolo’s Pizza tastes even better reheated in the morning. The bad news? I ate the only two piece left.”

Which brings me to the September jobs report. The good news is that 263k jobs were added to the US economy. That means 10,521k jobs have been added in the 21 months under Biden! (Bear in mind that 12,100k jobs were added in the 7 months under Trump following the Covid economic shutdown, yet no media outlet trumpeted that accomplishment).

The bad news? While nominal average hourly earnings grew by 5% YoY, when I subtract Bidenflation from that number I get -3.06% growth. Or should I say that REAL wages are shrinking under Biden.

Now for the “Biden Miracle” of jobs being added. Here is a chart of NFP jobs added (white line) against M2 Money and headline inflation. Both The Fed and the Federal government pumped trillions into the economy leading to the highest inflation rate in 40 years. Once governments stopped with their Covid shutdown nonsense, jobs would return regardless of who was President. BUT Federal spending and Fed money printing went off the rails in early 2020.

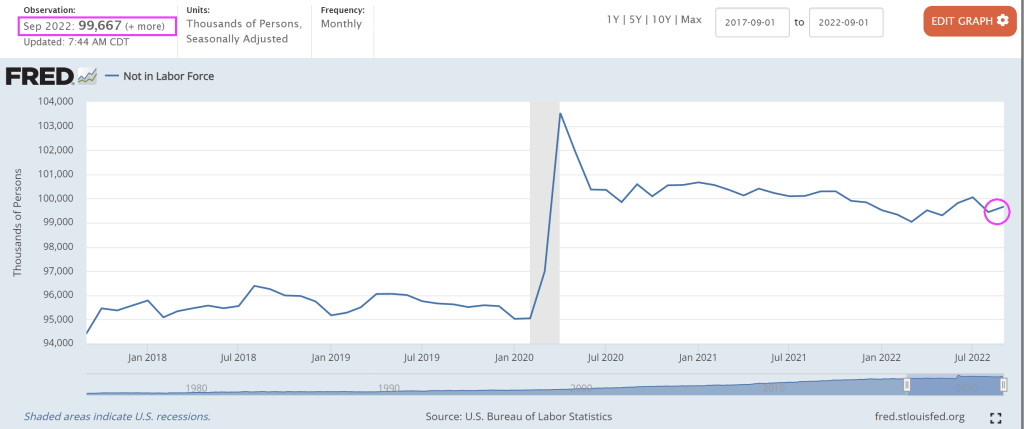

As Paul Harvey used to say, “Here is the rest of the story.” Labor force participation fell in September and the U-3 unemployment rate fell slightly to 3.5%.

But labor force dropouts increased leading U-3 unemployment to decline. The number of people NOT in the labor force grew to nearly 100 million. Nothing has been the same since Covid.

So what will The Fed do? According to Fed Funds Futures data (WIRP), The Fed will keep raising rates until March ’23 then slowly start lowering interest rates again.

And with that “positive” jobs report, The Dow is down almost -500 points and the NASDAQ is down over -3%.

And with Fed tightening, we are seeing a collapse in M2 money supply.

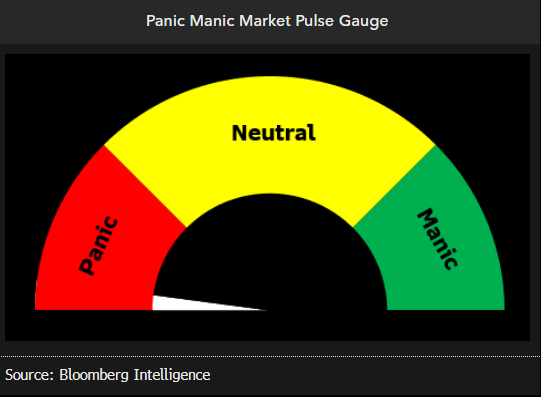

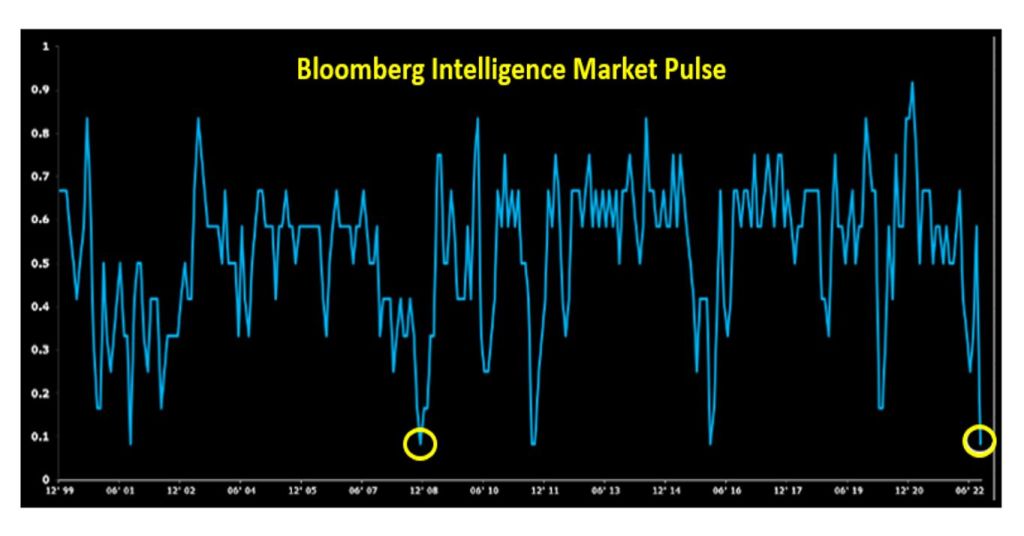

Bloomberg’s market pulse gauge is signalling panic.

The Bloomberg market pulse index quantifies sentiment using 6 factors — price breadth, pairwise correlation, low vol performance, defensive vs. cyclical sector performance, high vs. low leverage performance and high yield spreads.

What do we have? Regular gasoline prices are UP 61.4% under Biden, the strategic petroleum reserve is DOWN -35% before Biden’s latest release of another 10 million barrels. Foodstuffs are UP 50% under Clueless Joe, and heating oil futures are UP 130% under dementia Joe.

And thanks to free-spending Joe, Nancy and Chuckie, US public debt is at $31.1 TRILLION. That is ANOTHER 12% in national debt under the 4 Horsemen of the Economic Apocalypse.

For an additional 12% in national debt (to be paid by our children and grandchildren), we have crippling inflation.

You must be logged in to post a comment.