“One of the most cowardly things ordinarily people do, Is to shut their eyes to facts.” – C.S. Lewis

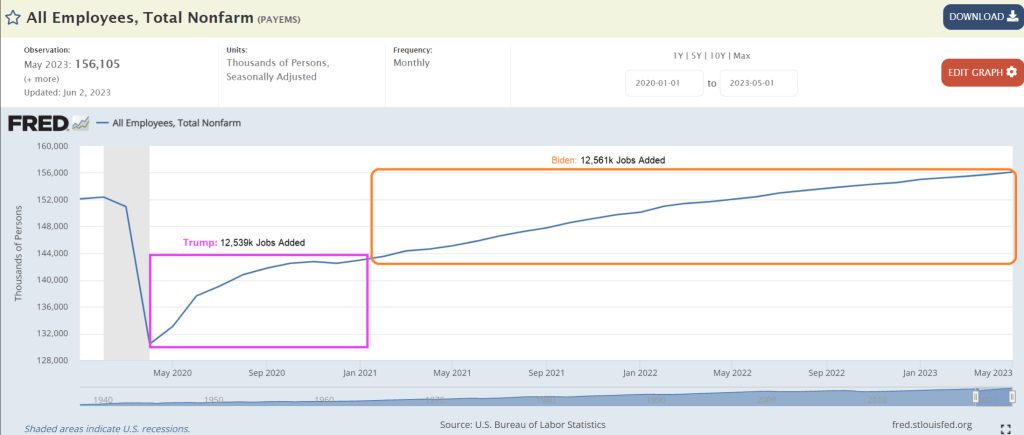

Okay, we know Biden lies constantly and misrepresents facts (hey, he is a politician like Adam Schiff (D-CA). But this graphic praising Bidenomics with Biden having created the most jobs (average per month) since Carter (notice they left out Democrat darling Jimmy Carter!!!). In this absurd graphic, Biden wins by “creating” over 400k jobs per month while Trump lost jobs per month. Riveting … except that it is completely misleading.

Actually, the US economy added 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs. So, Biden took over twice as long to create jobs after Covid than it did under Trump. Simply opening the economy and schools produced that magical claim by Biden. And the National Teacher’s Union and Randi Weingarten worked with Fauci to orchestrate shutting down schools. Blaming Trump for local governments shutting down the economy is pure bunk.

12.53 millions jobs added / 8 months = 1.56 million jobs average per month. Biden? 12.56 million jobs added / 30 months = .43 million jobs average per month. So, Trump averaged more than 3x the job growth post-Covid than Biden.

Here is the “glories of Bidenomics” from the White House. As Biden likes to say, pure malarkey!

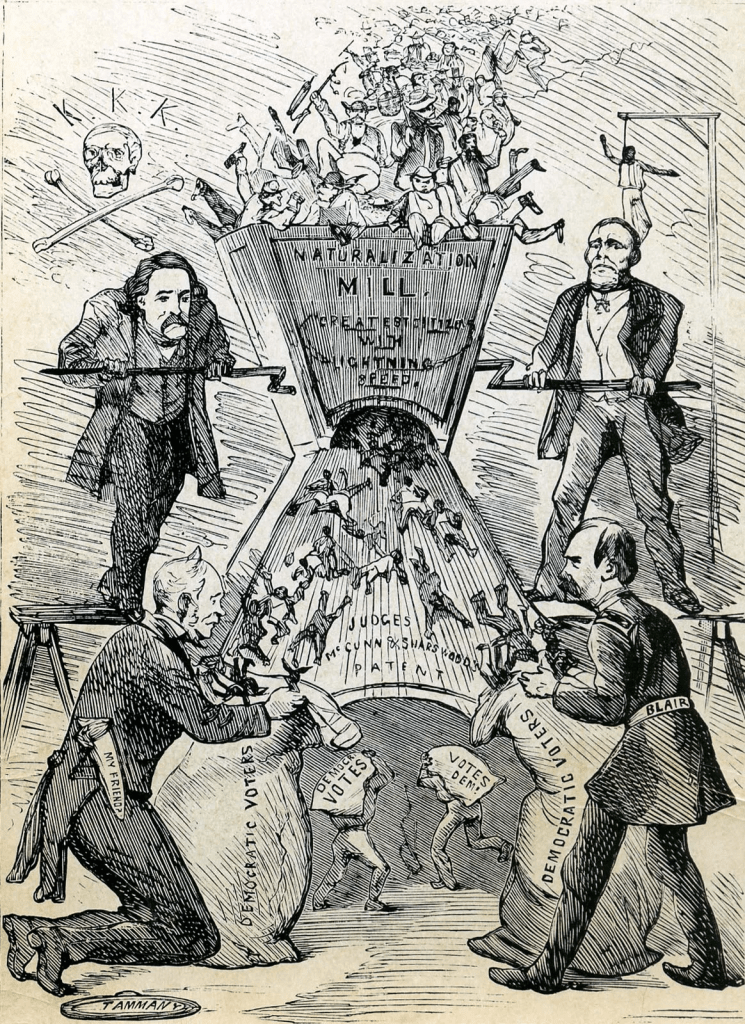

I wonder if the Democrat Party is a rebirth of New York City’s Tammany Hall corrupt political movement of the 1800s? Is Biden Boss Tweed? Or is Obama Boss Tweed with Biden as his nasty, dimwitted henchman?

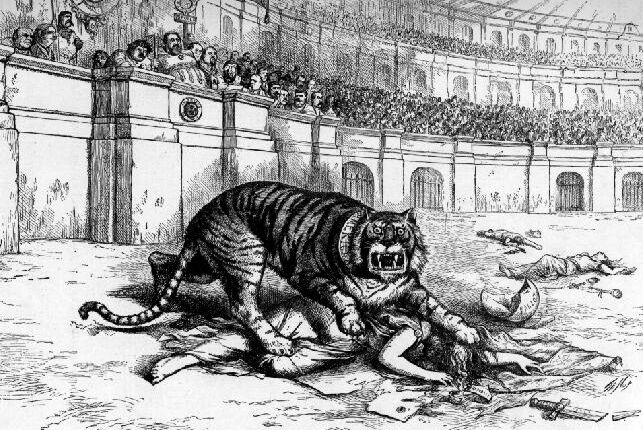

In 1871, Thomas Nast denounces Tammany as a ferocious tiger killing democracy. The image of a tiger was often used to represent the Tammany Hall political movement. Sounds an awful lot like today’s Democrat Party.

Starwood Capital Group’s Barry Sternlicht recently told Bloomberg’s David Rubenstein about the ongoing crisis in the commercial real estate sector, equating it to a severe “Category 5 hurricane“. He cautioned, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

Currently, the biggest problem in the CRE space is sliding office and retail demand in downtown areas. Couple that with high-interest rates, and there’s a disaster lurking for building owners. According to Morgan Stanley, the elephant in the room is a massive debt maturity wall of CRE loans that totals $500 billion in 2024 and $2.5 trillion over the next five years.

Senior markets editor for Bloomberg, Michael Regan, chatted with John Fish, who is head of the construction firm Suffolk, chair of the Real Estate Roundtable think tank and former chairman of the board of the Federal Reserve Bank of Boston, in the What Goes Up podcast to discuss the biggest problems in the CRE market.

Fish warned that “capital markets nationally have frozen” and “nobody understands value.” He said, “We can’t evaluate price discovery because very few assets have traded during this period of time. Nobody understands where the bottom is.”

For a sense of recent price discovery trends, we were the first to point out to readers of a wicked firesale of office towers in the downtown area of Baltimore City:

As for the overall CRE industry, Goldman Sachs chief credit strategist Lotfi Karoui recently told clients, “The most accurate portrayal of current market conditions with Green Street indicating a 25% year-over-year drop in office property values.”

Sooooo, Powell and The Fed will likely raise rates this week. And maybe a few more times over the next few months. And The Fed remains defiant about taking away the Covid monetary stimulus.

As The Federal Reserve is poised to continue it inflation-fighting crusade, the US economy is rapdily approaching DEFLATION. US Producer Price Index FINAL DEMAND fell to 0.1% YoY in June.

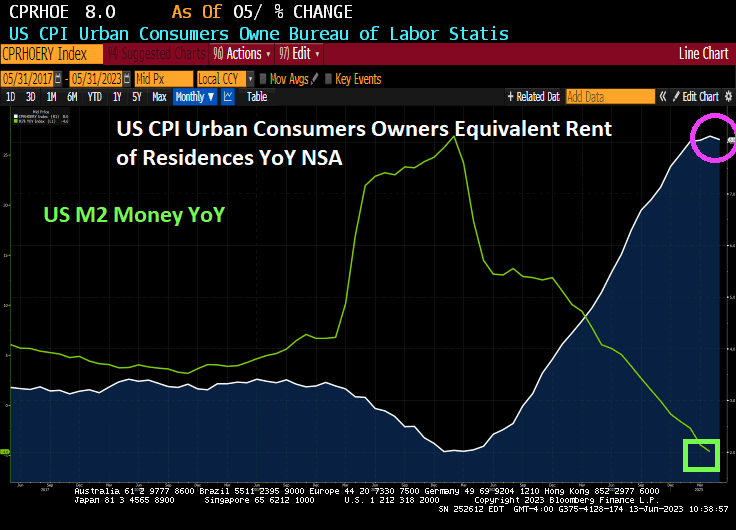

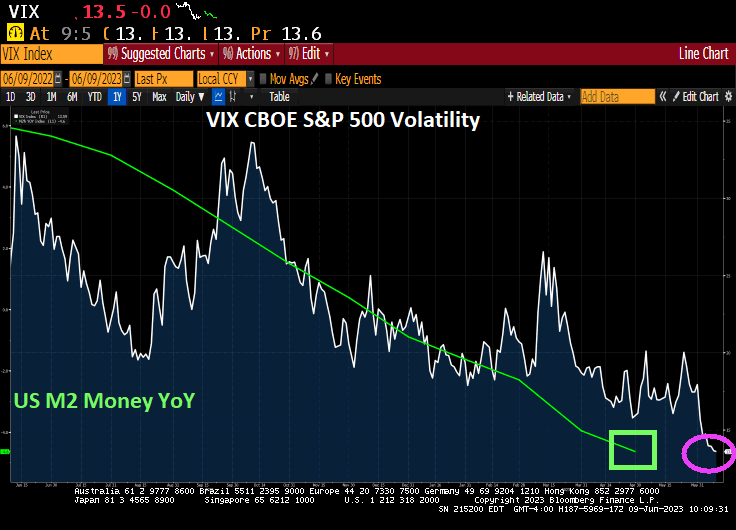

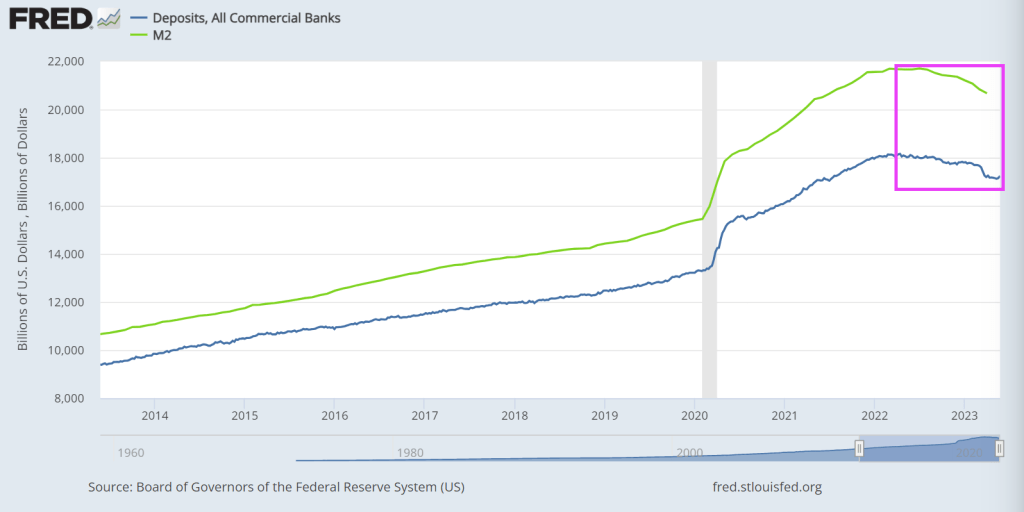

Bidenomics, the combination of insane monetary stimulus and insane directed Federal spending towards going green at all costs, is running out of steam. M2 Money growth was last measured to be -4% YoY and the US Dollar is down -8.2% since September 2022.

The US has passed the 32 trillion mark in national debt, and is going much, much higher. More like 32 tons on the back of taxpayers. When we add unfunded liabilities like Social Security, Medicare and Medicaid, the tab soars to $224.5 TRILLION.

In the first six months of 2023, there were 340 corporate bankruptcies, topping every other comparable span in 13 years, according to S&P Global Market Intelligence. This is up 93 percent from the same time a year ago and higher than in 2020, when there was a spike during the early days of the coronavirus pandemic.

There were 54 recorded corporate bankruptcy filings in June, unchanged from the 54 bankruptcies in May. Last month, some of the most notable companies to submit filings were Lordstown Motors, Rockport Co., Instant Brands Acquisition Holdings, and iMedia Brands.

“Lordstown Motors Corp. filed for bankruptcy June 27, with plans to restructure its business and seek a buyer, according to a company release. The electric vehicle manufacturer’s assets include its Endurance pickup truck and related resources,” S&P noted in the July 6 report.

“Instant Brands Acquisition Holdings Inc. also sought bankruptcy protection June 12. The tightening of credit terms and higher interest rates had impacted the company’s liquidity levels, according to an official release. The company has also already secured $132.5 million from existing lenders and plans to continue discussions with its financial stakeholders.”

Year-to-date through June, 15 companies with more than $1 billion in liabilities filed for bankruptcy, such as Cyxtera Technologies, Diebold Holding, Bed Bath & Beyond, Diamond Sports Group., and Party City.

Epiq Bankruptcy, a U.S. bankruptcy filing data provider, confirmed that 2,973 total commercial Chapter 11 bankruptcies were filed in the first half of 2023, up 68 percent from the same period in 2022.

Higher Interest Rates Impacting Businesses

Banking experts purport that higher interest rates are the leading cause of the increase in corporate bankruptcies. Many businesses either maintain vast debt loans that will require refinancing or need more liquidity to stay afloat.

“The increase in commercial and individual bankruptcy filings during the first half of 2023 underscores the economic challenges faced by businesses and individuals,” said Mr. Gregg Morin, Vice President of Business Development and Revenue at Epiq Bankruptcy, in the report. “Our objective is to provide bankruptcy professionals with timely and accurate data necessary for analyzing stakeholder volumes and trends for making informed business decisions.”

The situation could be exacerbated should the Federal Reserve pull the trigger on two more rate hikes this year. The futures market is penciling in a quarter-point boost to the benchmark fed funds rate at this month’s Federal Open Market Committee (FOMC) policy meeting.

Meanwhile, according to a recent Fitch Ratings report, the corporate default rate is projected to climb to as high as 4.5 percent in 2023, up from the previous forecast low of 2.5 percent. The updated projections reflected “the tighter lending conditions and capital access resulting from stress in the banking sector and inflation uncertainty.”

However, some argue that corporate bond market indicators are “less ominous.”

“The interest rate differentials, or spreads, between the 10-year U.S. Treasury note and investment grade (IG) and high yield (HY) corporate bonds continue to hover within their average width over the past 25 years, a bond market signal indicating the likelihood of a less severe recession, with traders pricing in fewer corporate defaults,” wrote John Lynch, the CIO at Comerica Wealth Management, in a research note.

Economists contend that the worst corporate bankruptcies typically occur one or two years into a recession. Today, they are happening before the official start of an economic downturn as the U.S. economy is still expanding.

What’s happening?

“Simple,” says Mr. Pete St. Onge, a Heritage Foundation economist, “banks aren’t lending.”

“Banks are battening down the hatches, hogging their bailout money instead of lending it out,” he said in a recent podcast. “That credit crunch means not only do we get bankruptcies like in any recession, on top of that, we get a lending wall that cuts off even the healthy businesses. Of course, their jobs go down with them.”

Since the Federal Reserve launched the Bank Term Funding Program (BTFP) following the Silicon Valley Bank collapse in March, financial institutions have kept tapping into these emergency lending facilities. After hitting a record high at above $103 billion at the end of June, it remains elevated at $102 billion.

32.5 trillion in debt and $192 trillion in unfunded liabilities which means a total of $224.5 total debt + liabilities.

This is Bidenomics. Spend trillions, borrow trillions, promise entitlements. Rinse, repeat.

Biden’s massive spending spree (aka, Build Back Better) has a new name: Build Back Bankrupt!

According to Epiq, Commercial Chapter 11 Filings Increased 68 Percent in the First Half of 2023.

NEW YORK – July 03, 2023— The 2,973 total commercial Chapter 11 bankruptcies filed during the first six months of 2023 represented a 68 percent increase over the 1,766 filed during the same period in 2022, according to data provided by Epiq Bankruptcy, the leading provider of U.S. bankruptcy filing data. Individual Chapter 13 filings increased by 23 percent during the same period.

Overall commercial filings registered 12,107 for the first half of 2023, representing an 18 percent increase from the commercial filing total of 10,258 for the first half of 2022. Small business filings, captured as Subchapter V elections within Chapter 11, totaled 814 in the first six months of 2023, a 55 percent increase from the 525 elections during the same period in 2022.

Overall commercial filings increased 12 percent in June 2023, as the 2,123 filings were up from the 1,891 commercial filings registered in June 2022. The 404 commercial Chapter 11 filings in June represented a 9 percent increase from the 371 filings in June 2022. Total Subchapter V elections within Chapter 11, experienced a 111 percent increase from 94 in June 2022 to 198 in June 2023.

“The increase in commercial and individual bankruptcy filings during the first half of 2023 underscores the economic challenges faced by businesses and individuals,” said Gregg Morin, Vice President of Business Development and Revenue at Epiq Bankruptcy. “Our objective is to provide bankruptcy professionals with timely and accurate data necessary for analyzing stakeholder volumes and trends for making informed business decisions.”

Total bankruptcy filings were 217,420 during the first six months of 2023, a 17 percent increase from the 185,352 total filings during the same period a year ago. Total individual filings also registered a 17 percent increase, as the 205,313 filings during the first half of 2023 were up from the 175,094 filings during the first six months of 2022. The 85,390 individual Chapter 13 filings in the first half of 2023 represent a 23 percent increase over the 69,367 filings during the same period in 2022.

All chapters increased in June 2023 compared to June 2022, with 37,700 total bankruptcy filings representing an increase of 17 percent from the 32,198 filed in 2022. Total commercial filings were up 12 percent from 1,891. Total Individuals were up 18 percent from 30,307.

While not the Epiq data, the Bloomberg Corp Bankruptcy Index shows the rise in bankruptcies as The Fed fights Bidenflation.

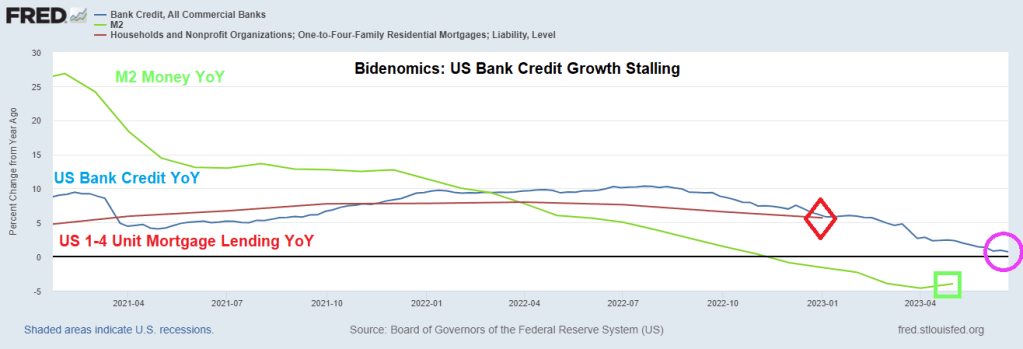

Bidenomics is based on massive Federal spending and massive Fed monetary stimulus. But like all stimulus, it wears off. Such is the case with bank lending as The Fed raises interest rates.

US bank credit year-over-year (YoY) has stalled to a lowly 0.7% rate as M2 Money growth YoY increases slightly to -4%.

Its figures. With the Socialist Federal Reserve manipulating interest rates and Biden/Congress spending like drunken sailors trying to manipuate economic growth, it makes sense that Biden wants to explore Bill Gate’s idiotic idea of blotting out the sun to prevent global warming.

Of course, Biden can hide at any of his 4 mansions and wear his Ray-ban Aviators to avoid the horror of his policies.

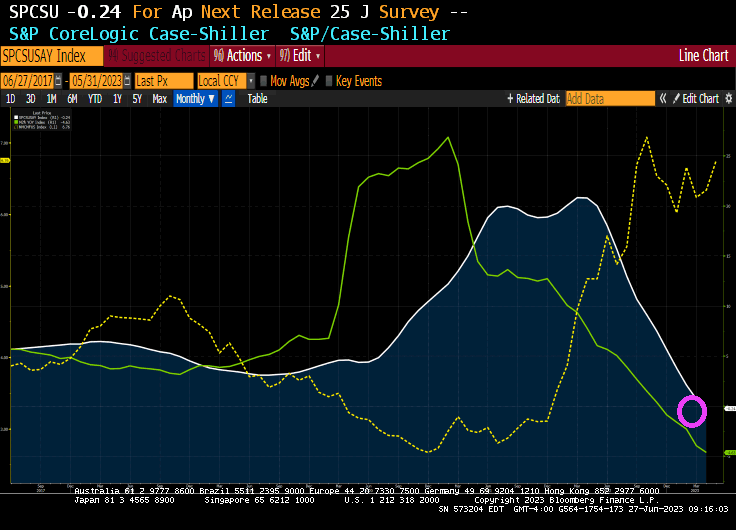

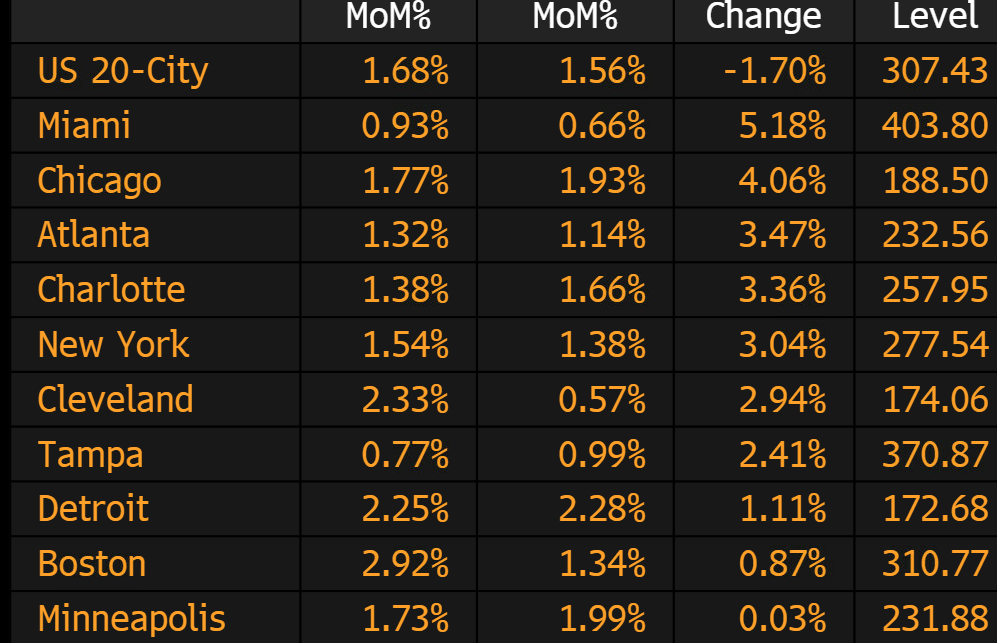

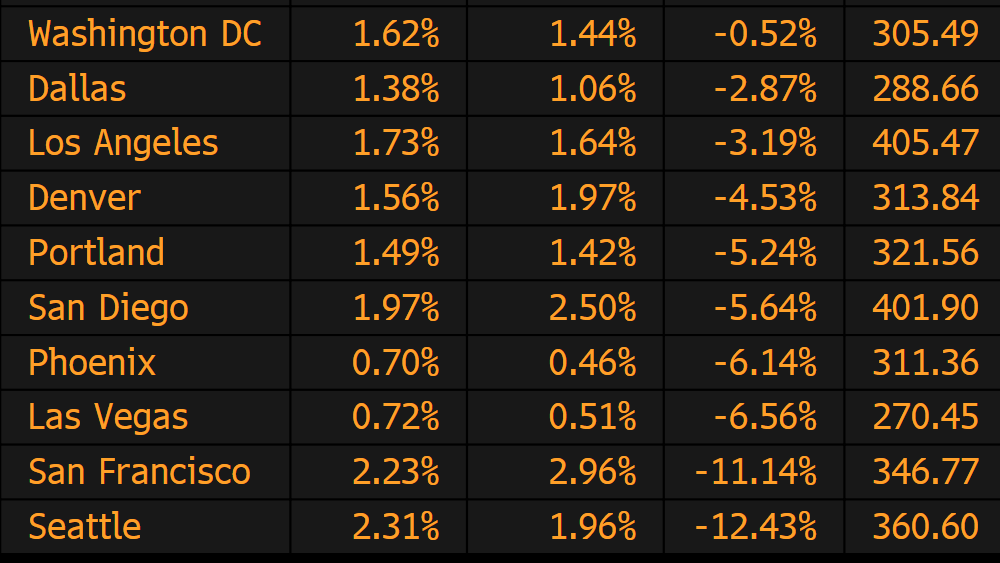

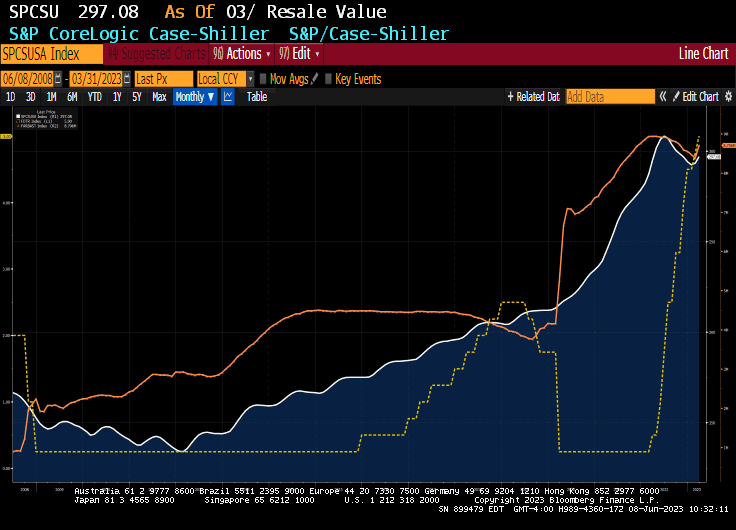

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a -0.2% annual decrease in April, down from a gain of 0.7% in the previous month. The 10-City Composite showed a decrease of -1.2%, down from the -0.7% decrease in the previous month. The 20-City Composite posted a -1.7% year-over-year loss, down from -1.1% in the previous month.

The winners in April? Miami and … Chicago?

The biggest losers in April? Seattle and San Francisco both suffered YoY losses over -11%.

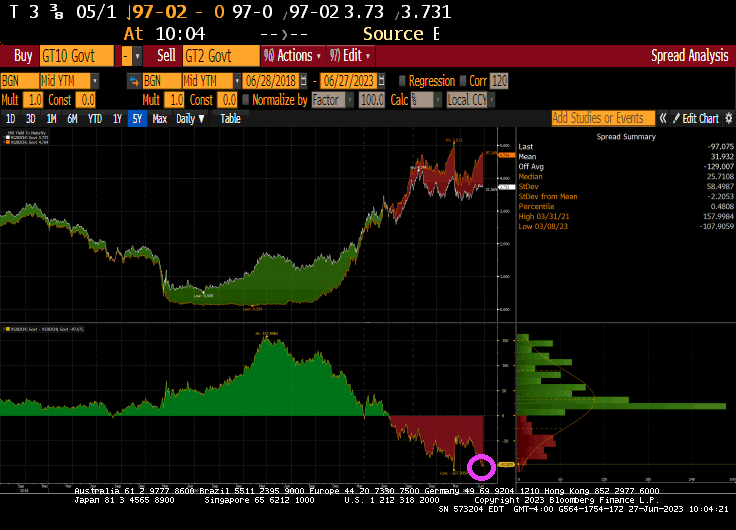

The US Treasury 10Y-2Y yield curve remains steeply inverted at -97 basis points.

Okay, Joe Biden was generally regarded as the dumbest member of the US Senate and mean-spirited (I won’t repeat podcaster Joe Rogan’s opinion of Biden). Now we realize how brazenly corrupt Biden is (taking bribes from China and Ukraine to influence American poliicies). Not only is Biden an attrocious human being, but his policies have damaged the US middle class terribly thanks to inflation.

Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

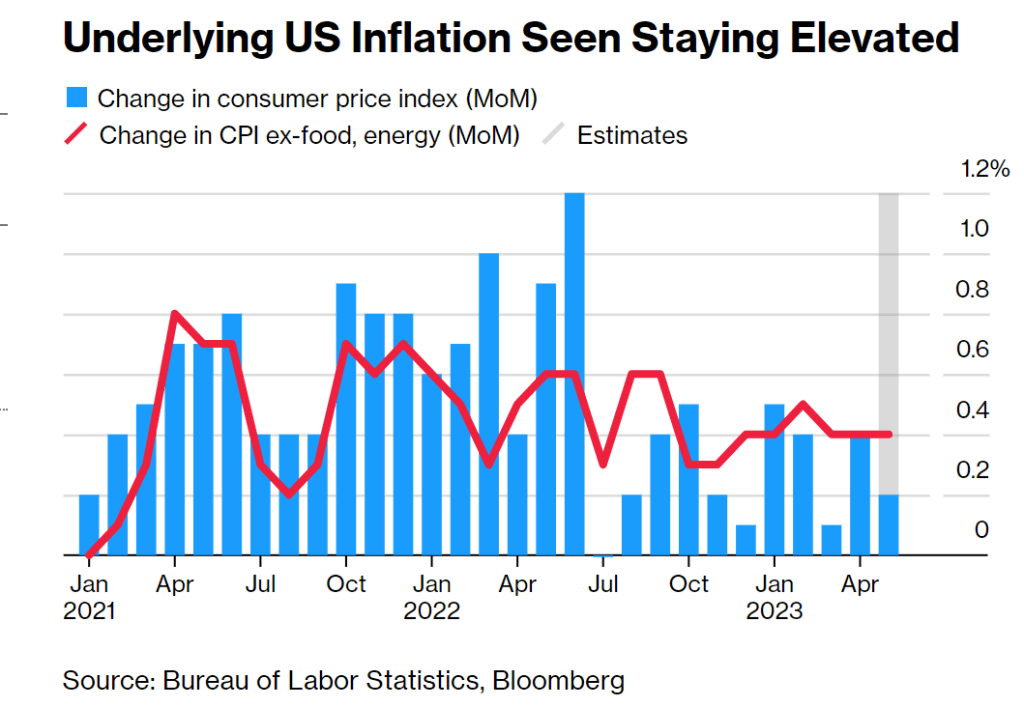

Source: Bureau of Labor Statistics, Bloomberg

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee.

Remember, there is still over $8 TRILLION in Fed assets held sloshing around the economy. The Fed never really removed the excess liquidity and it continues to stoke asset bubbles.

Bear in mind that The Fed is pausing at 5.25% Fed Target Rate, while the Taylor Rule suggests rate hikes to 10.12%. So, Foul Powell is pausing at just over the half way mark.

Of course, Biden’s and Congress’ massive spending spree is causing inflation, and The Fed has no control over Biden/Congress irresponsible spending.

You must be logged in to post a comment.