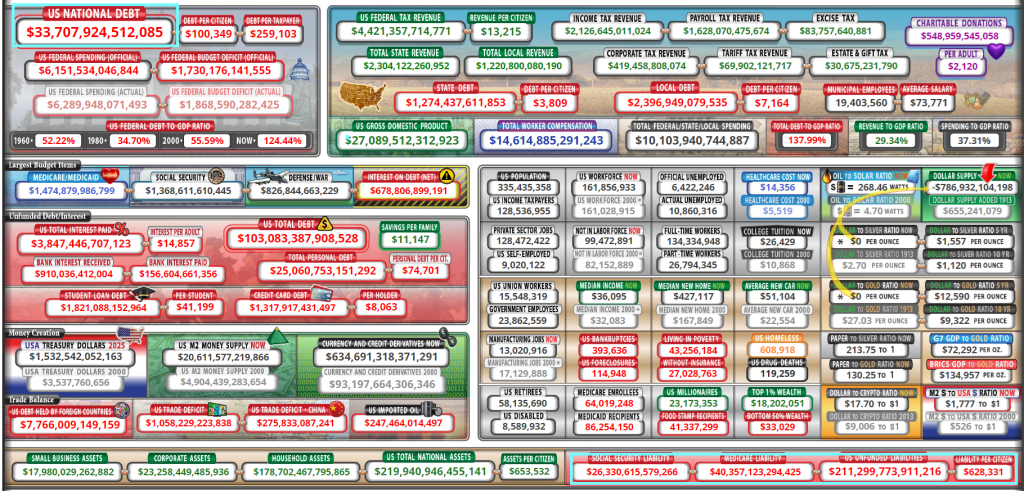

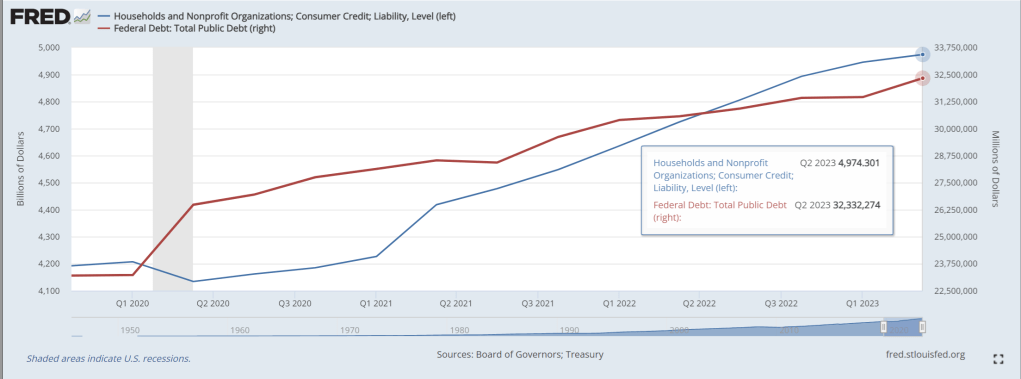

US Federal debt just hit $33.71 TRILLION. And unfunded liabilities (promises from Uncle Spam) are now $211 TRILLION. That is 526% of the the current debt load. Which means either lots of additional debt, higher tax rates or cuts in entitlements.

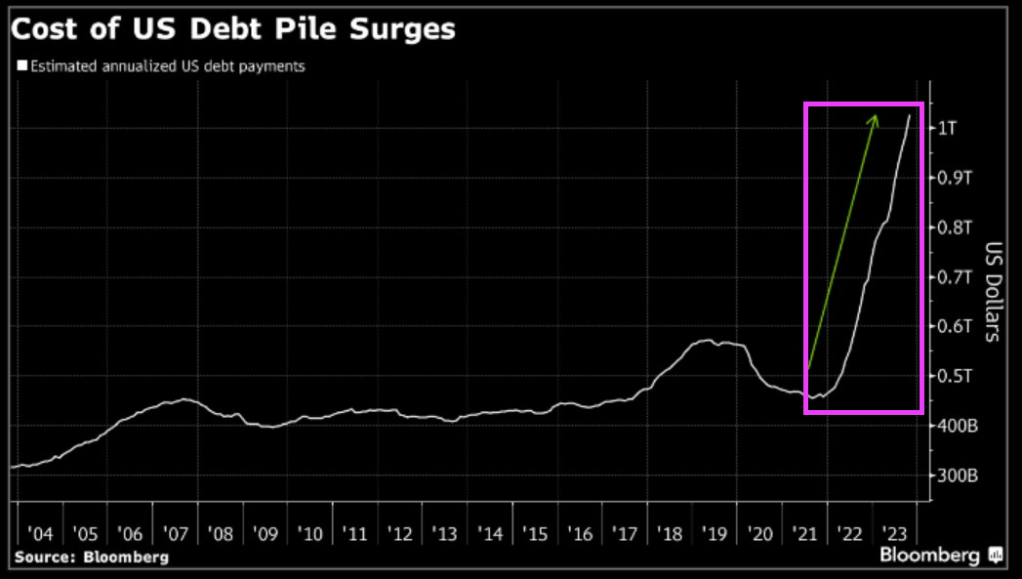

The cost of US debt continues to soars as The Fed combats Bidenflation.

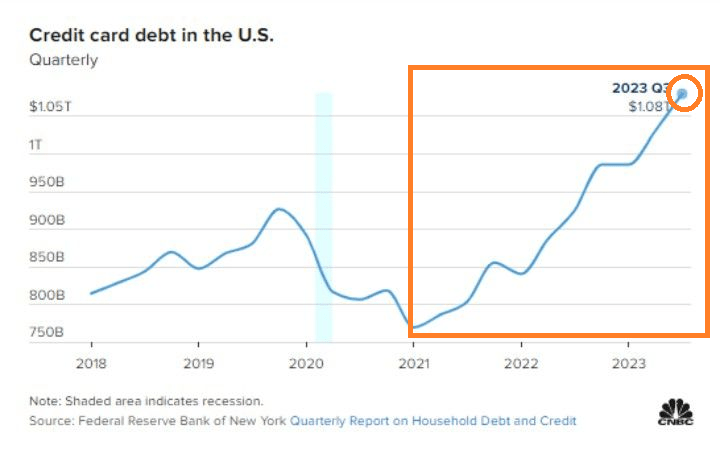

But it isn’t just Federal government debt that is exploding under Bidenomics. Consumer credit card debt has exploded under Bidenomics as consumer struggle with inflation.

US inflation is lower than it was a year ago (cheers from The View CNN and MSNBC cheerleaders), but inflation remains stubborning above The Fed’s 2% target rate and will likely remain above 2% for the nexf few years. So mortgage demand is much like inflation … mortgage demand increased in the latest week but generally is very low compared to last year.

Mortgage applications increased 2.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 3, 2023.

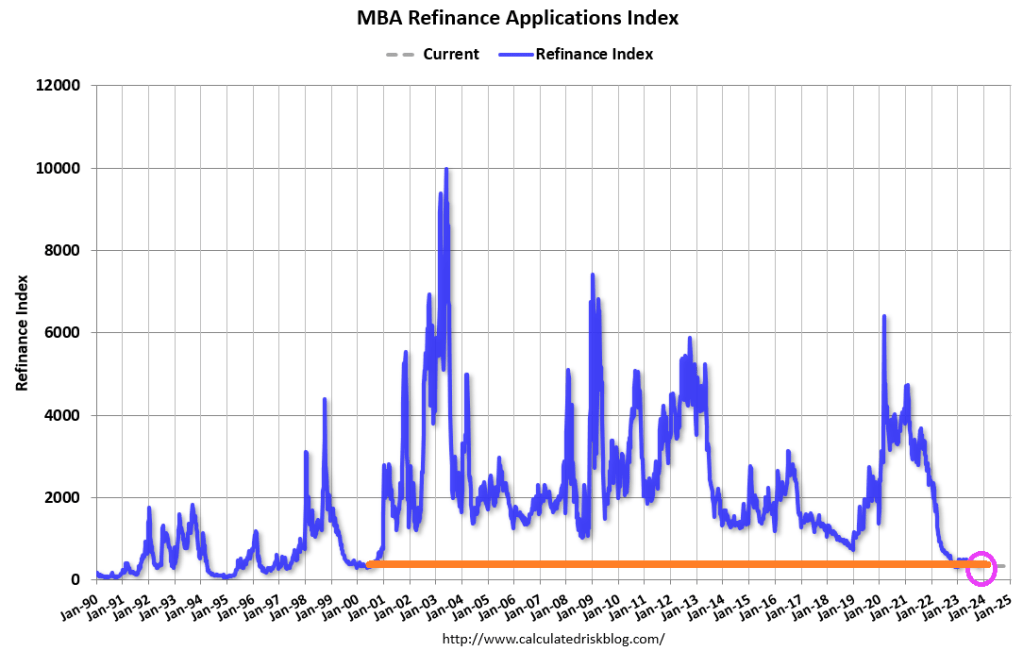

The Market Composite Index, a measure of mortgage loan application volume, increased 2.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 1 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 7 percent lower than the same week one year ago.

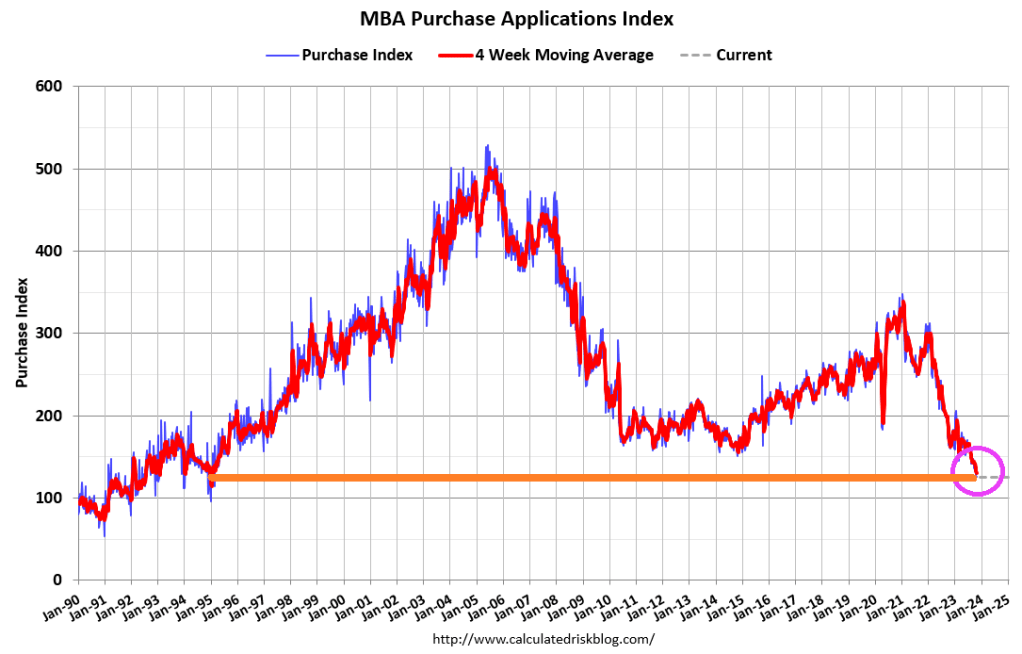

The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 20 percent lower than the same week one year ago.

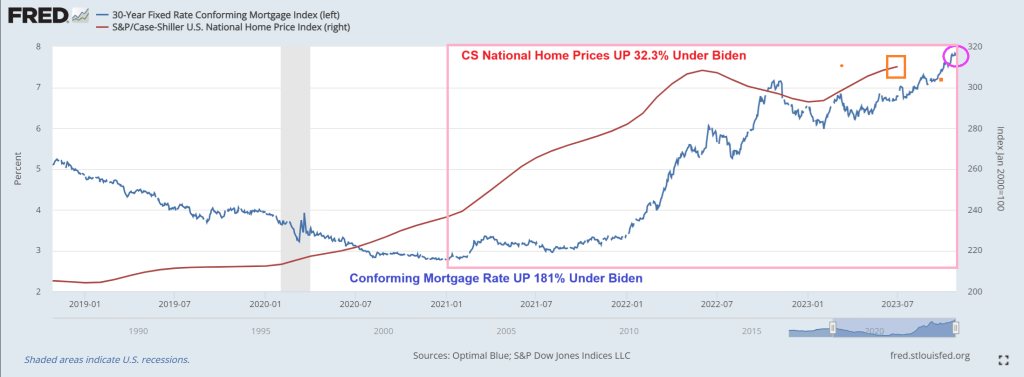

The 30-year fixed mortgage rate dropped by 25 basis points to 7.61 percent, the largest single week decline since July 2022. But, mortgage rates are up 169% under Biden and Bidenomics.

But on the middle class front, we can see “cheap rates” are a thing of the past as markets have to deal with Biden’s inflation problem and Fed rate hikes.

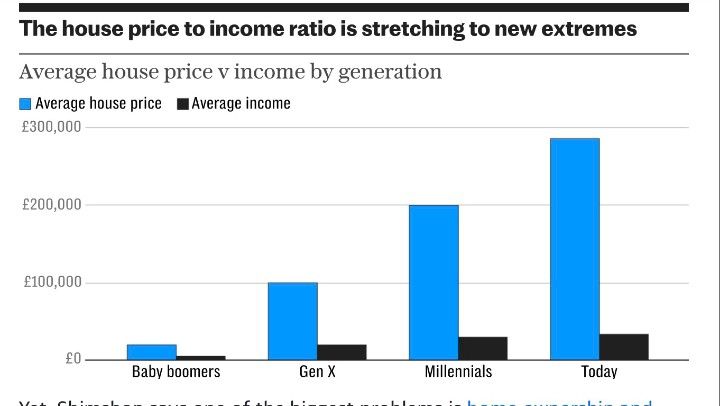

And with rising home prices under Biden, the house price to income ratio is out of control and causing pain for the middle class.

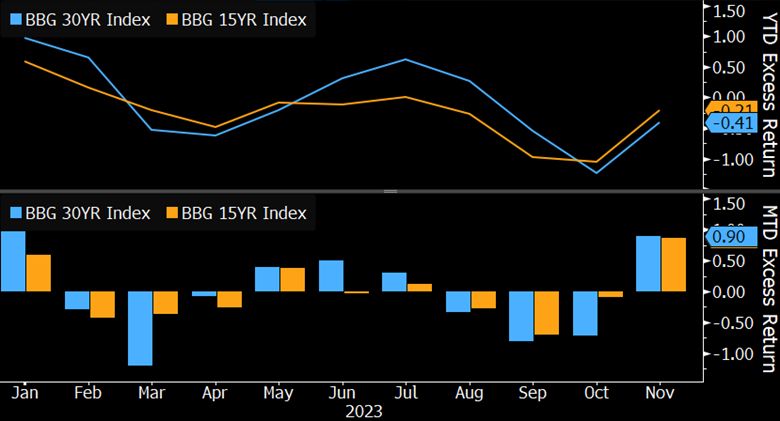

On the MBS front, we see negative returns.

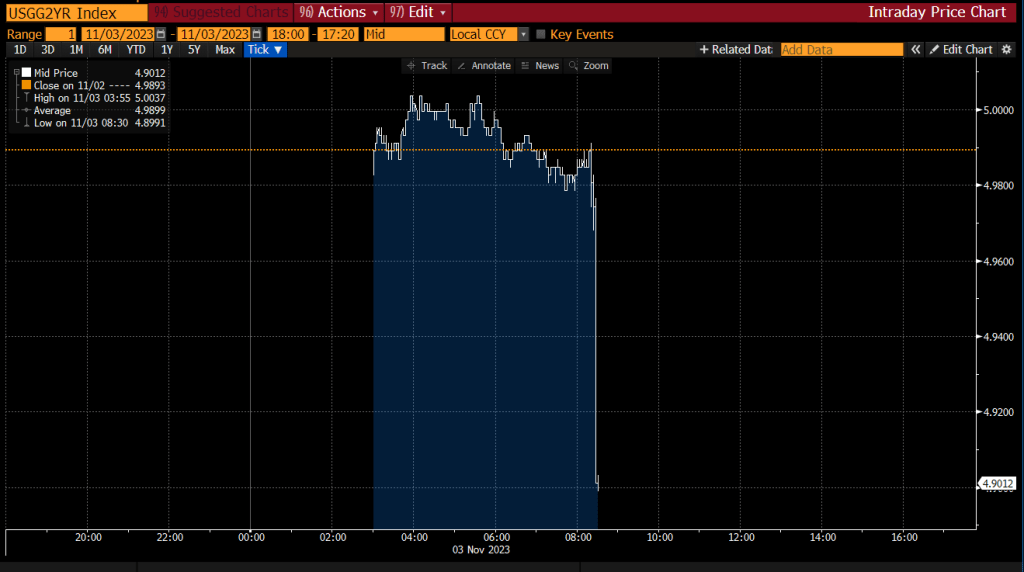

The 2-year Treasury yield is dropping faster than Biden’s polling numbers.

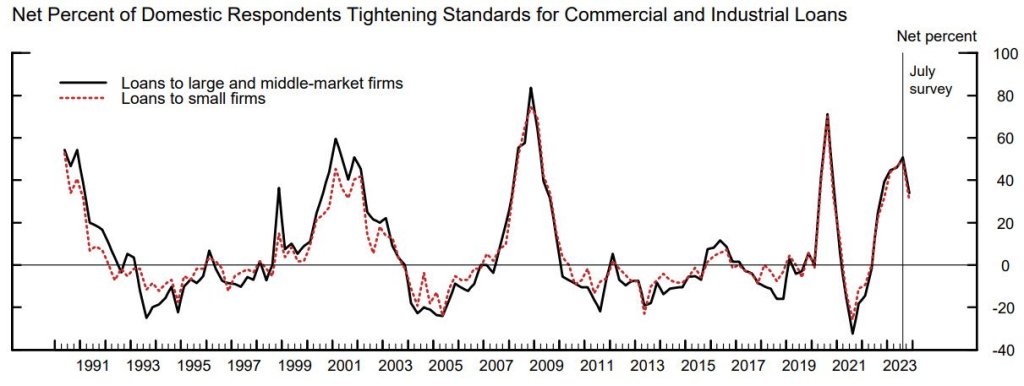

On the credit side, more lenders are tightening standards for C&I loans.

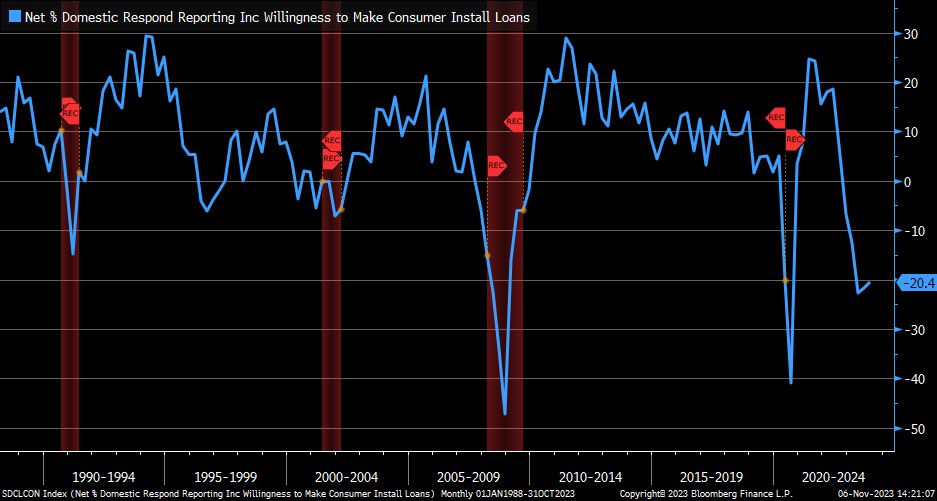

And banks remained restrictive in their willingness (or lack thereof) to make consumer loans, but there was a marginal improvement from prior release.

On the global front, Maersk announces plans to cut at least 10,000 jobs due to weakening global trade.

Here is a picture of Hinky Dink (Joe Biden) and Bathhouse Barry Soetoro. I mean Bathhouse John Coughlin, the Lords of the Levee.

No, this isn’t the tilt effect in the mortgage market where inflation is front-loaded in mortgage rates making mortgage payments quite unaffordable. Although inflation is causing mortgage rates to be up 174% under Biden (while Biden continues to brag about how Bidenomics is helping). Meanwhile, the 10Y Treasury yield is up 402% under Biden (making refinancing the US staggering debt load more difficult to refinance. Higher mortgage rates tilt the present value of mortgage payments to the front, making housing even more unaffordable. Thanks Joe!

But the Tilt effect I am talking about is the TLT effect. TLT (iShares US Treasuries 20y+ ETF) calls. Friday was the largest TLT call volume ever.

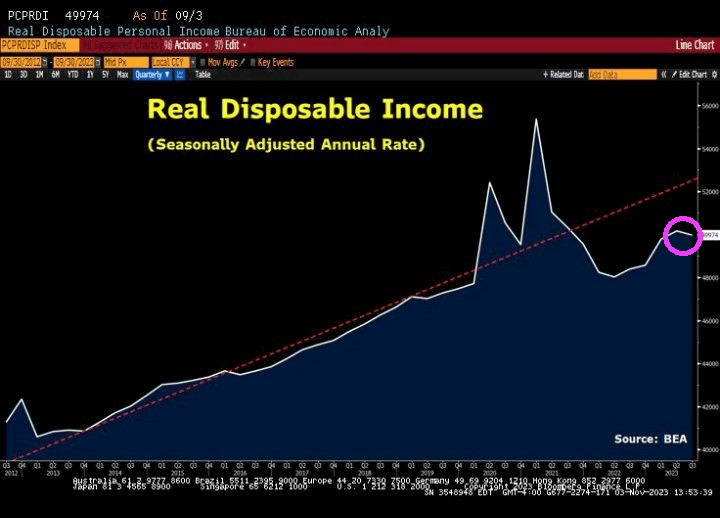

Meanwhile, US real disposable income is declining.

Call it “The Rich Men North Of Richmond” economy. Where the coastal elites drive the US economy off the cliff with insane spending and borrowing with much of the benefits flowing to big political donors, not the middle class. Think of Span Bankfraud Parboiled as an example.

President Biden loves to spend billions and go on endless vacations (he is in Rehobeth Beach Delaware yet again). He (illegally) forgave student debt, keeps spending billions on Ukraine and keeps spending on failed green energy nightmares.

Biden and his allies will tout the latest GDP numbers as an example of how marvelous Bidenomics is. BUT that GDP report was driven largely by consumer spending.

Since the Covid outbreak in 2020, Federal (public) debt is up 45%! Wow. And consumer debt is up 19% under Biden to cope with inflation (caused primarily by massive Federal spending).

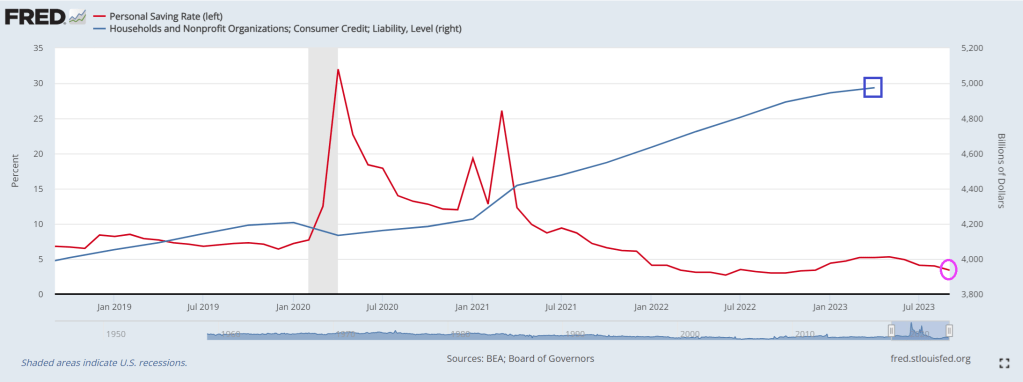

To fuel consumer spending, the personal savings rate has fallen to 3.4%. For point of reference, the personal savings rate in Februray 2020 was 7.7%, so the consumer is running out of gas thanks to inflation and spending.

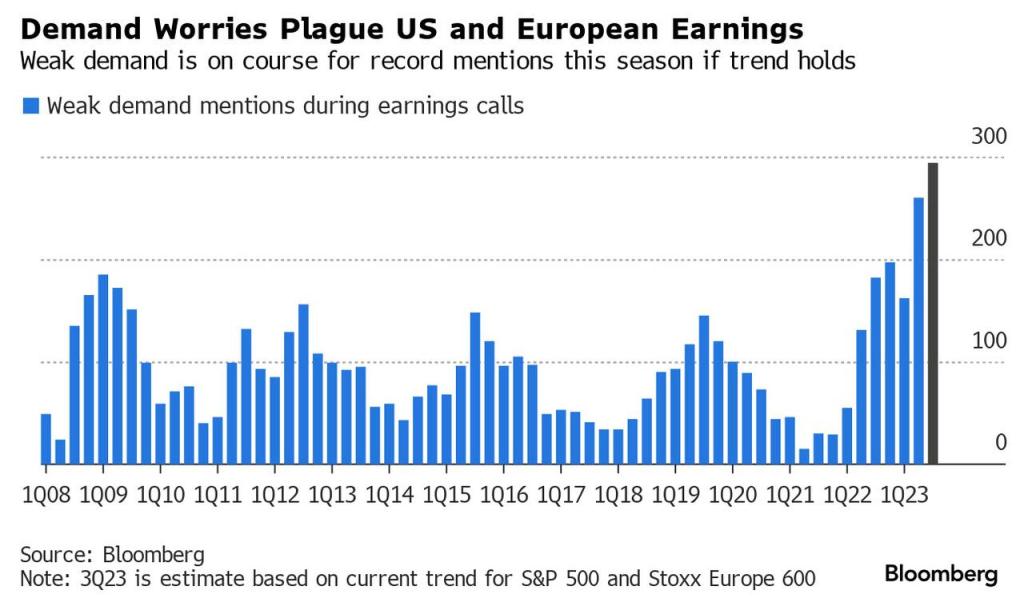

And with a debt-stressed consumer, earnings call revealed concern about continued demand.

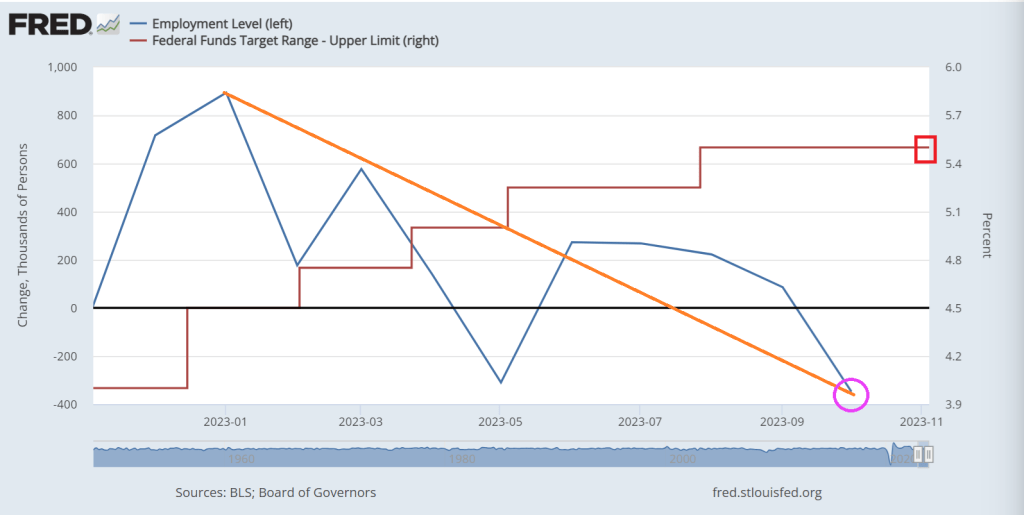

Note the trend in jobs added as The Fed tightened to fight inflation.

Appartently, Joe Biden and fellow big spenders in Washington DC, Mordor on The Potomac, don’t care about fiscal discipline. With seemingly endless spending of wars (Ukraine, Israel, Taiwan and the invasion at our southern border, and inane “green” spending,

Janet Yellen and the US Treasury will be auctioning off $776 billion of debt in the final quarter of calendar 2023, a bit below market expectations. Treasury said it will auction another $816 billion in the first quarter of 2024. So, that is yet another $1.6 TRILLION in debt.

Such large payments are negative for the economy. Interest is likely to be paid for using higher-velocity money (e.g. taxes) and received by holders less likely to spend the proceeds in the broad economy, and instead re-invest it. Independent monetary policy becomes increasingly difficult when the equivalent of 6% of US GDP is being diverted towards interest payments each year.

It’s not only the size of Treasury borrowing that’s a problem, but it’s maturity composition.

Issuance has latterly been skewed to bills, which has ameliorated the impact on liquidity as money market funds have been able to intermediate through the reverse repo (RRP) facility at the Fed. But as issuance skews back towards longer-term debt (watch for increases in auction sizes in 2y, 3y, 5y, 7y, 10y, 20y and 30y debt for insight on this), that will have an increasingly negative impact on liquidity, especially if the Treasury maintains its large cash balance at the Fed (as it said on Monday it expected to do).

The Fed has little (or no) say over any of this.

Monetary policy will become increasingly overwhelmed in such an environment, which is why today’s Fed meeting, where it is expected to keep rates on hold, is a bit of an afterthought.

Also of more consequence currently is Japan.

The BOJ’s decision to maintain negative yields and keep its yield curve control policy largely intact ladles on yet more underlying risks to the global macro environment.

Allegedly, The Fed isn’t interested in buying additional US debt, and likely China and Japan won’t be buying our debt either. But maybe the REAL Federal government, Blackrock and their friends will buy the debt!

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The Refinance Index decreased 4 percent from the previous week and was 12 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 22 percent lower than the same week one year ago. Back to 1995 levels.

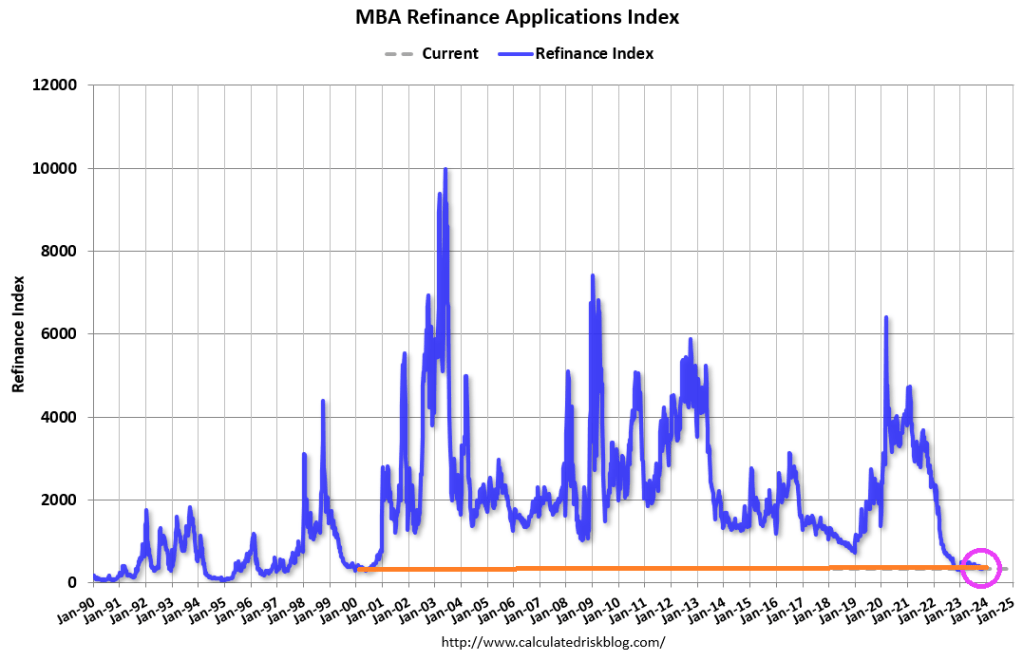

At least mortgage refinancing applications are back to only 2001 levels.

Two-year yields have risen 5%.

At least it looks like Powell will pause rate hikes … for the moment.

I want a new drug, other than Biden’s top-down, big-donor friendly Soviet-style command economy. How about a free market without Fed interest rate manipulation??

Bidenomics is best represented by the novel “The Guns of August” since American’s middle class is getting blasted by Biden’s economic policies and The Fed’s rate rate hikes. Find out where Texas Governor Abbot is bussing illegal immigrants and buy in the market!!

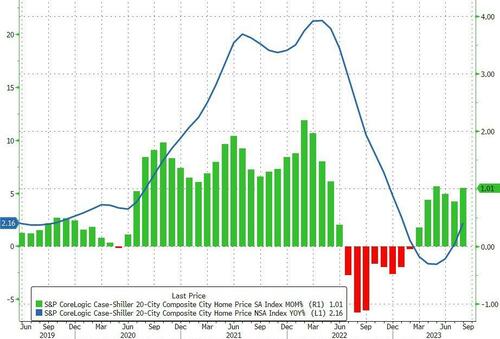

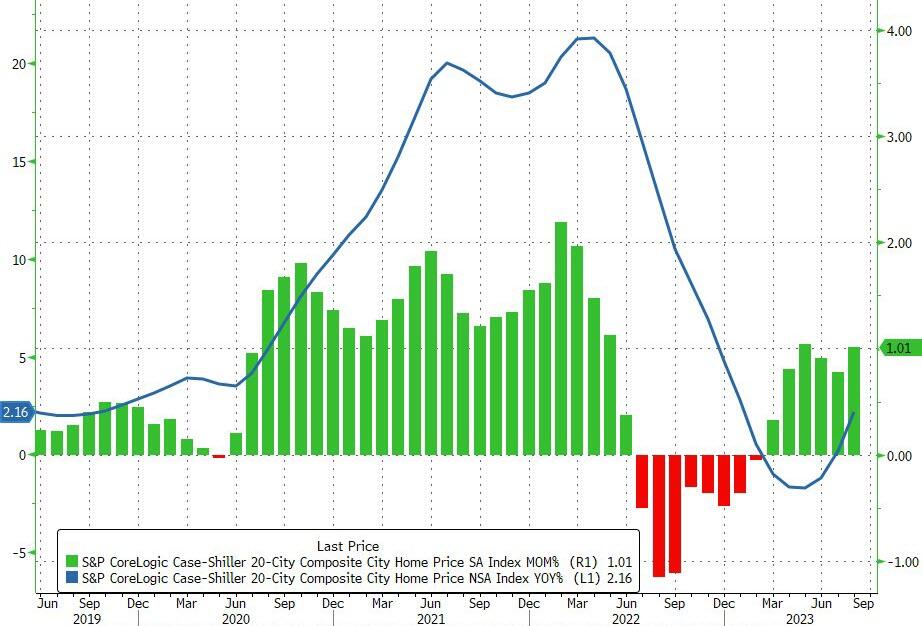

The ongoing MoM rises pushed the YoY gain in home prices at America’s 20 largest cities up 2.16%, the most since January 2023. The National Home Price index rose even faster at 2.57% YoY.

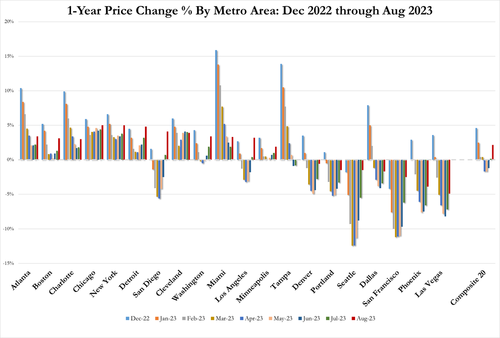

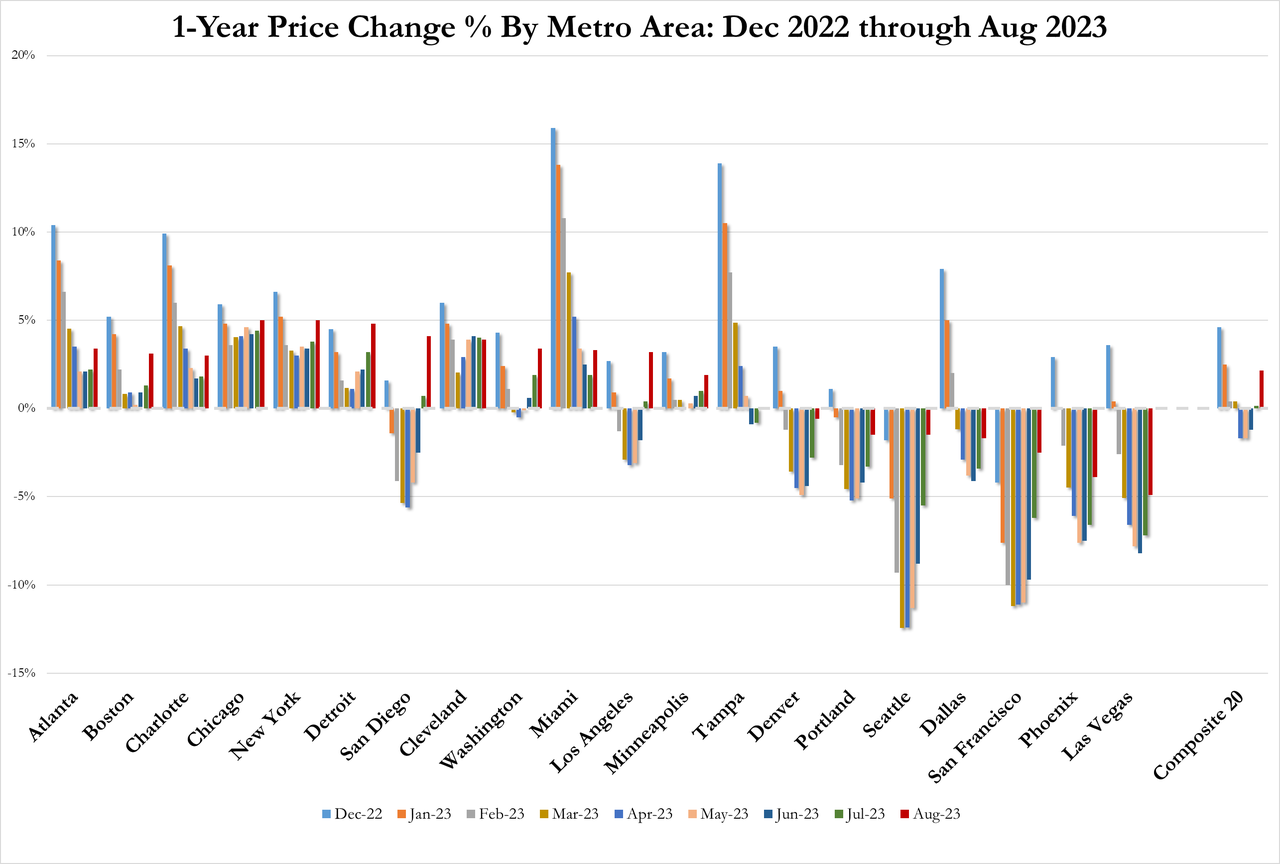

Illegal immigration destinations Chicago, New York, and Detroit all saw major home price rises (+5.0%, +4.9%, and +4.8% YoY respectively). Las Vegas, Phoenix, and San Francisco remain lower YoY (-4.9%, -3.9%, -2.5% respectively).

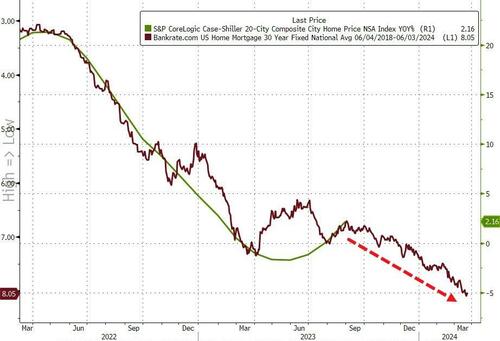

But, judging by the resumption of the rise of mortgage rates since the Case-Shiller data was created, we would expect prices to also resume their decline…

Source: Bloomberg

Inventory is going nowhere, buyers and sellers are stuck (affordability for the former and the mortgage cost gap for the latter), and The Fed isn’t cutting rates any time soon. Not pretty…

The benchmark small cap index, the Russell 2000, has hit the lowest levels since November 2020, when the world was still without a vaccine and shut down from Covid. And before Biden’s/Congress wild spending spree and debt volume explosion creating massive inflation causing The Fed to hike rates.

Speaking of over, under, sideways, down under Bidenomics, mortgage rates are up 181% and home prices are up 32.3% under Biden.

Bidenomics is a windfall for the donor class (high rate of return on campaign contributions) while the middle class gets beaten to a pulp. Waiting for Biden to lean over and creepily whisper “It’s working!” Even though it is clearly not working, at least for the middle class.

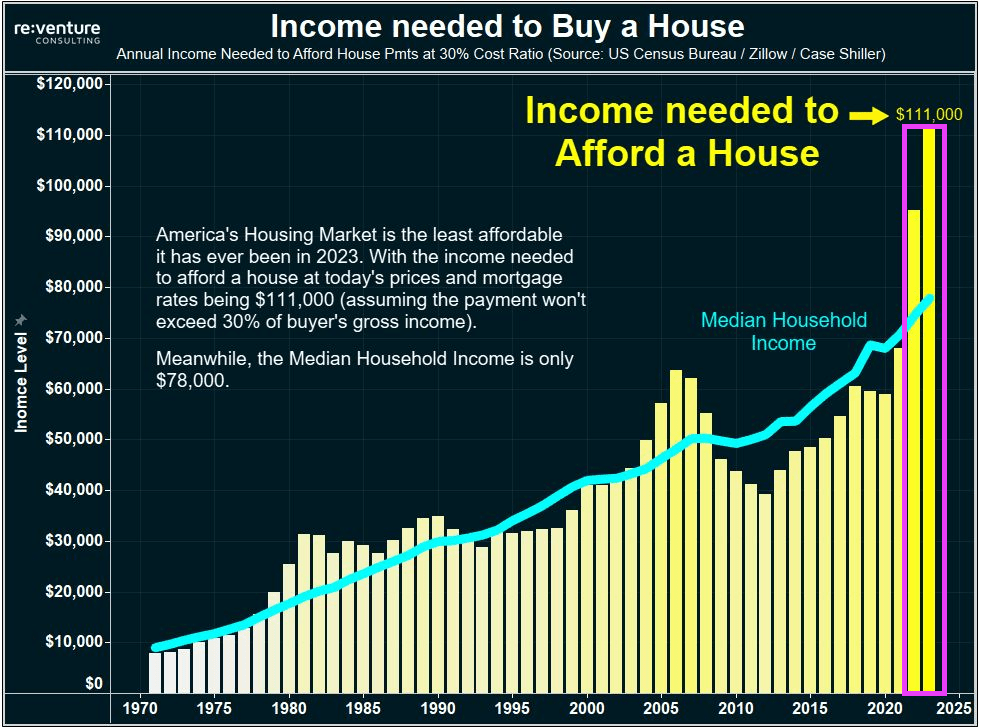

Evidence that Bidenomics is not working and destructive? Try the surging income needed to buy a house under Biden. Home prices are rising faster than median household income. As in $111,000 income needed to buy a house, while median household income is only $78,000. So, housing is simply unaffordable under Bidenomics. The Biden era is outlined in pink.

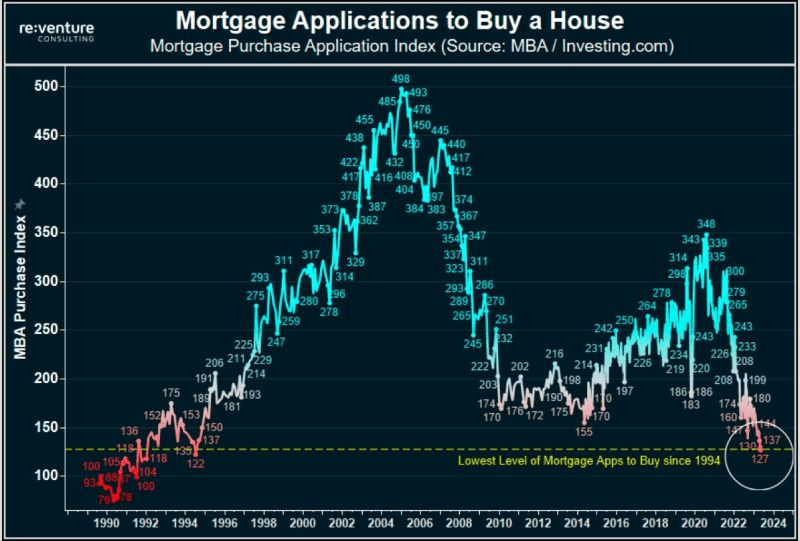

Mortgage purchase applications have collapsed to 1994 levels.

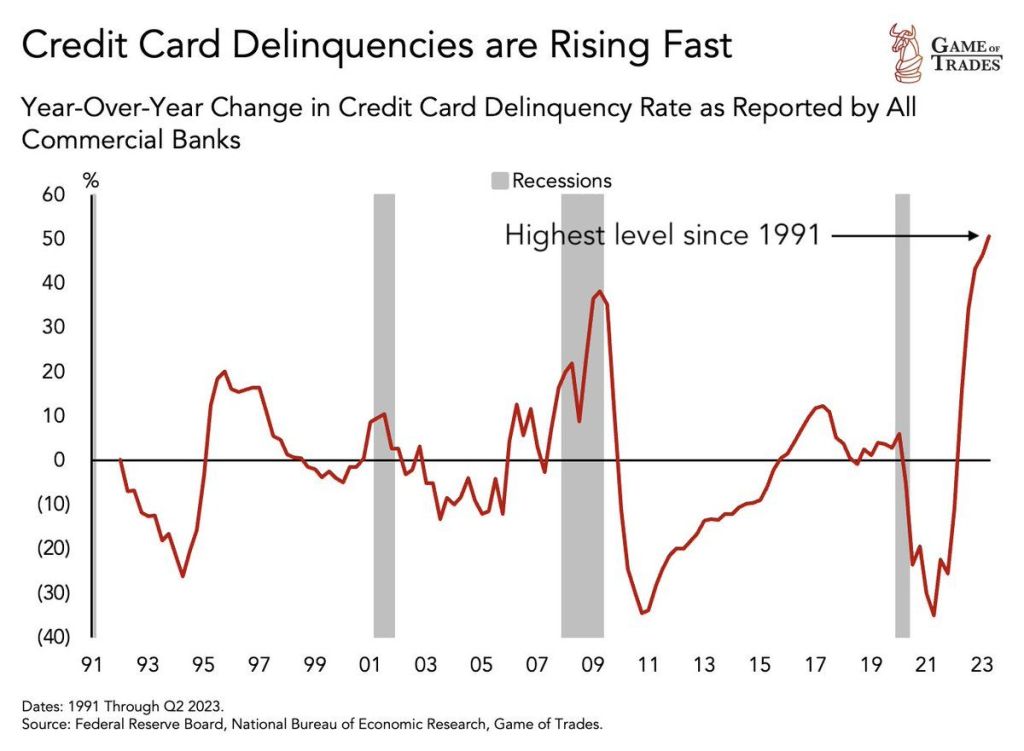

Meanwhile, stressed households are seeing credit card delinquencies at the highest level since 1991.

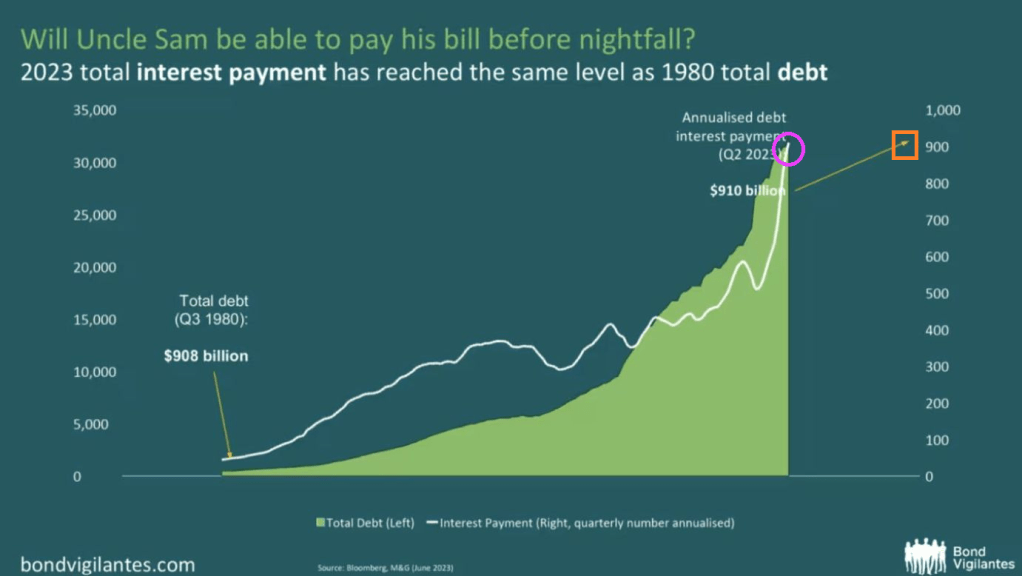

And thanks to Uncle Spam (given how Uncle Sam is destroying the middle class it is now Uncle Spam), 2023 interest payments are the same as the total debt from 1980! Spam, which the Federal government has devolved into, is very high in fat, calories and sodium and low in important nutrients, such as protein, vitamins and minerals.

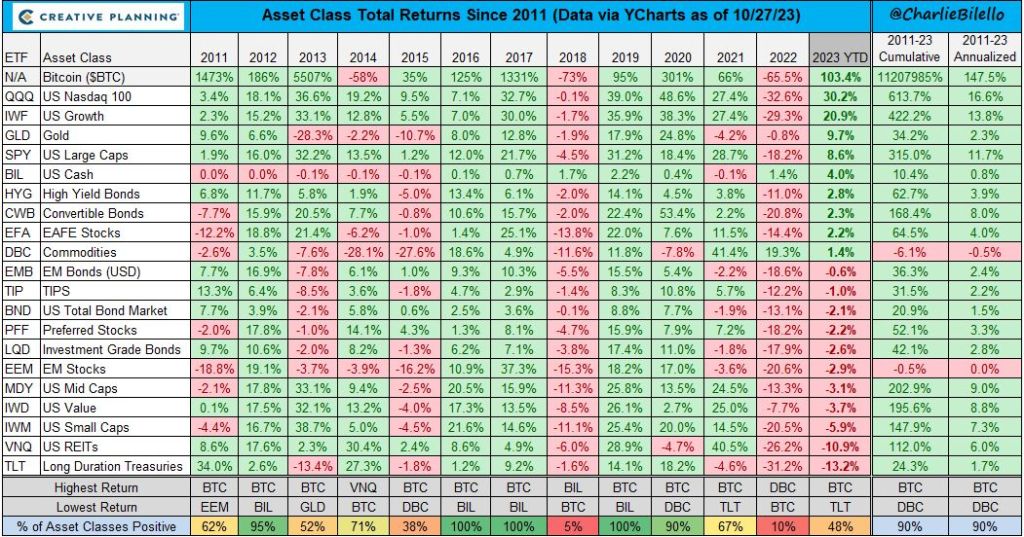

2022 was a bad year for investments under Bidenomics. 2023 year to date is showing huge gains for Bitcoin, the NASDAQ and gold. Bringing up the rear are long duration Treasuries and REITs (real estate investment trusts), both earning negative returns thus far of less than -10%.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.