The Federal Reserve is reversing its excessive monetary stimulus policies left over from the financial crisis of 2008 (and Covid) and the mortgage industry and potential home buyers are paying the price.

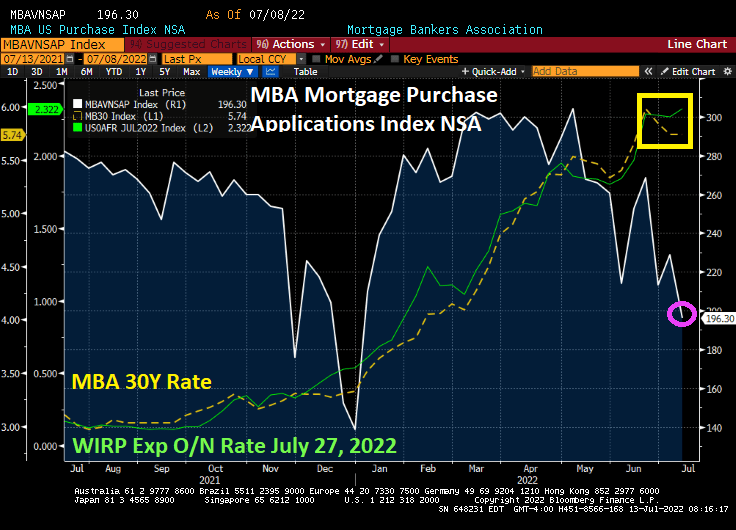

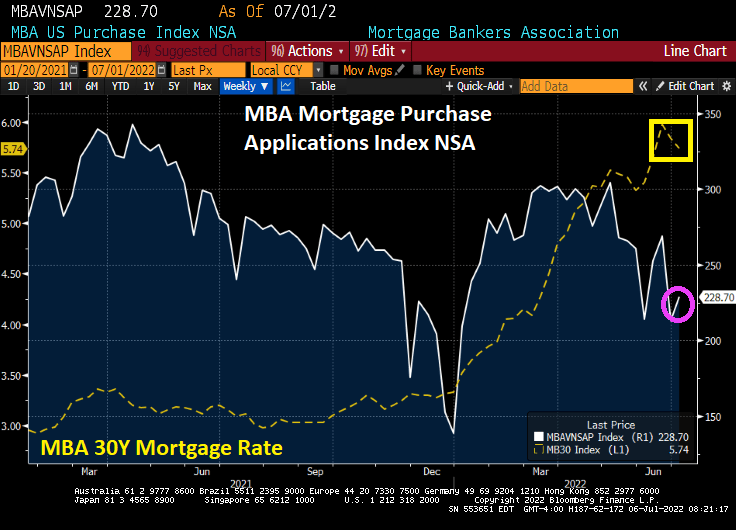

Mortgage applications decreased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 8, 2022. This week’s results include an adjustment for the observance of Independence Day.

The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 14 percent compared with the previous week and was 18 percent lower than the same week one year ago.

The Refinance Index increased 2 percent from the previous week and was 80 percent lower than the same week one year ago.

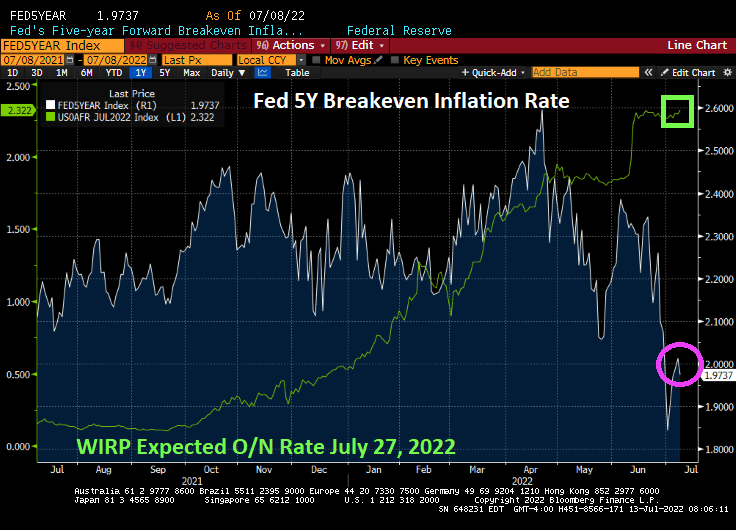

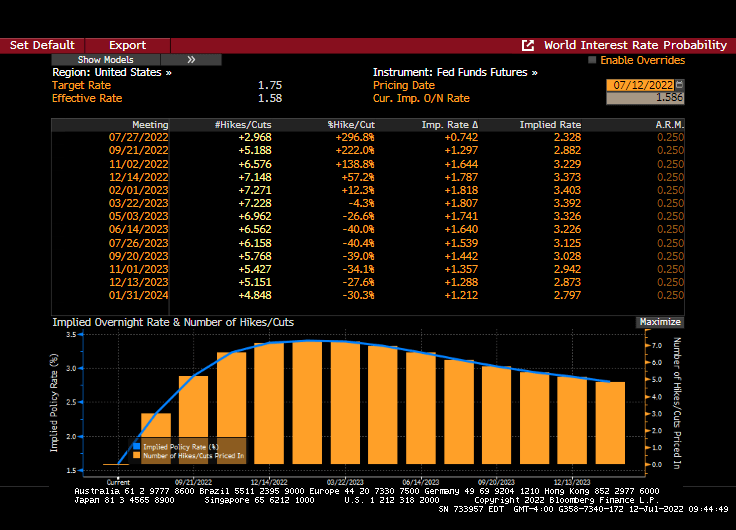

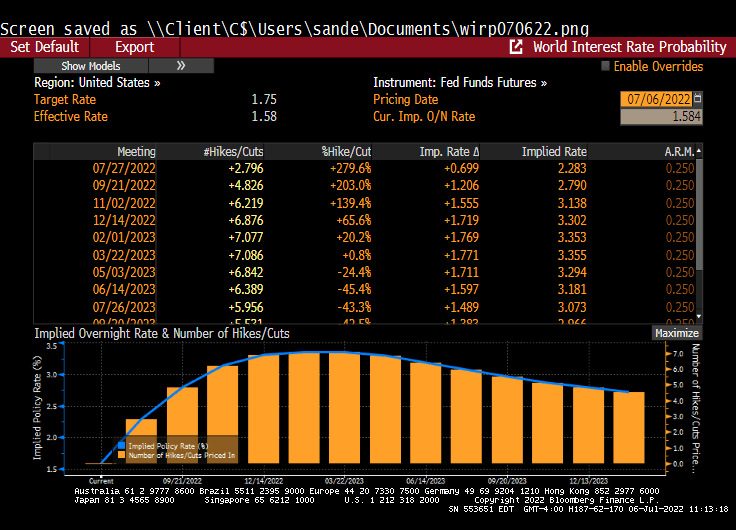

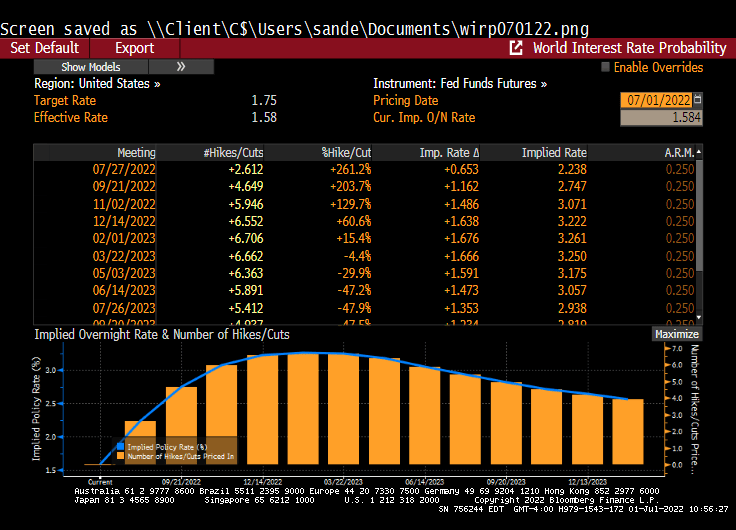

Here we go loop de loop! Traders are pricing in a 75 basis point rate increase at the July FOMC meeting despite collapsing Fed 5-year inflation breakeven rates.

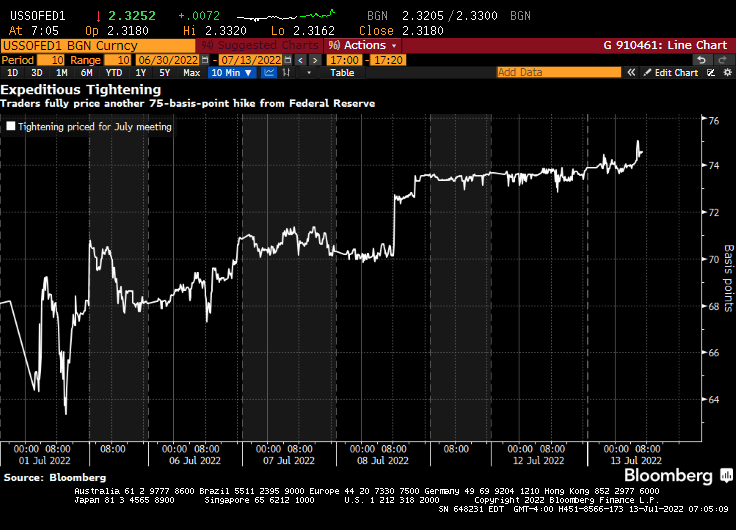

Money markets are betting on a three quarter-percentage point hike by Federal Reserve officials later this month, wagering the US will need to ramp up the pace of monetary tightening to tame inflation.

The repricing comes ahead of a key inflation report due Wednesday. The headline figure for June is set to accelerate to 8.8% year over year, the highest since 1981.

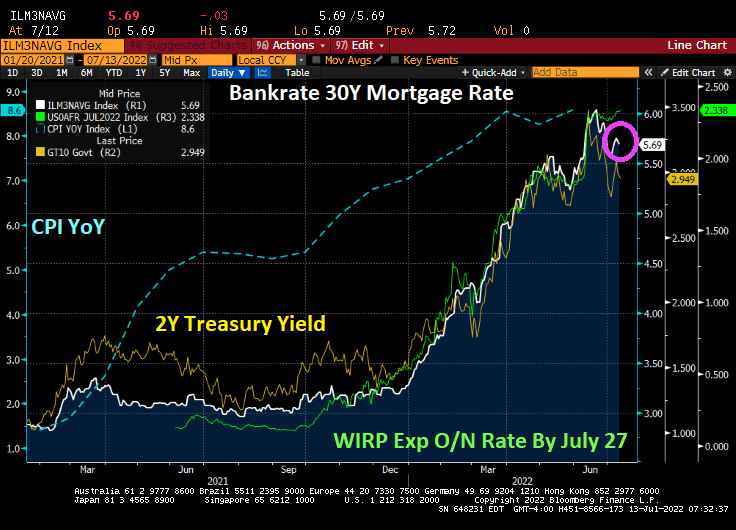

Bankrate’s 30Y mortgage rate fell slightly ahead of today’s inflation report with the expectation of The Fed hiking their target rate by 75 basis points to 2.338% at the July 27th Fed Open Market Committee meeting.

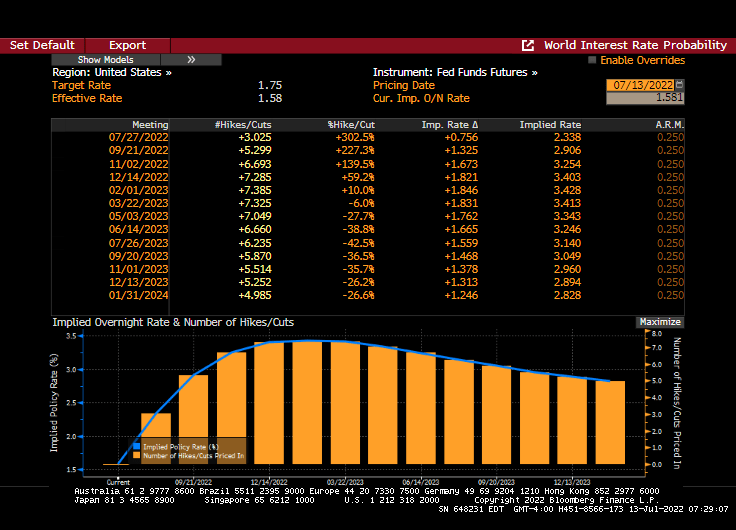

Trader expectations from Fed Funds Futures data:

Last night I watched “The Shallows” on Peacock TV. I thought from the title that it was going to be a biography of The Federal Reserve, but it was a film about a surfer being attacked by a shark.

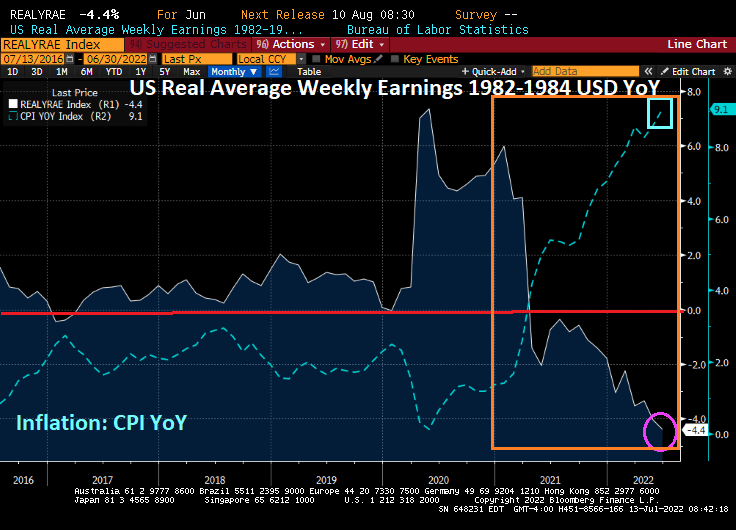

We are all aware that inflation is soaring, since the Covid outbreak in 2020 and the massive overaction by The Federal Reserve and Federal government in terms of stimulus spending and economic lockdowns.

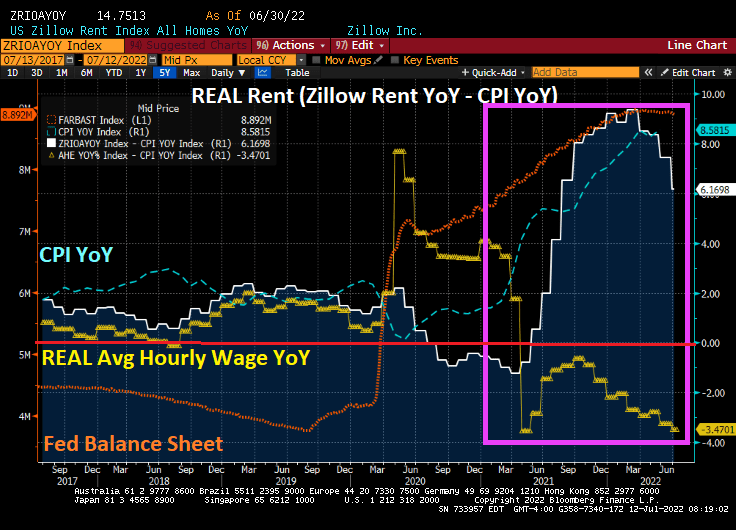

Things were “normal” before Covid in that REAL housing rent (white line) and REAL average hourly earnings YoY (yellow line) moved together. But after Covid shutdowns and Federal stimulus “relief” (orange line), we see that inflation (blue line) took off along with the growth in housing rent. The problem, of course, is that REAL average hourly earnings YoY has been declining. I call this “The Great Divide in housing affordability”.

The question, of course, is whether The Federal Reserve will continue their “war on inflation” with a 75 basis point rate increase.

Inflation is at its fastest pace in 40 years, and is expected to increase even higher in tomorrow’s inflation report.

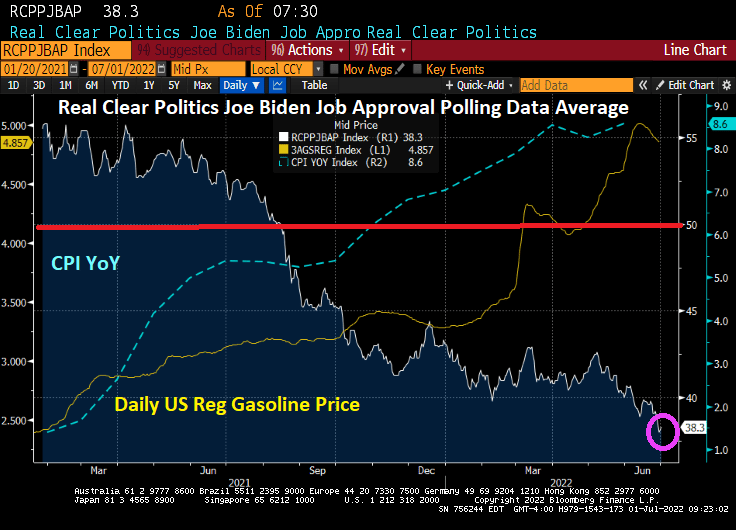

Gasoline prices have been dropping recently, but remain above $4.50 per gallon (regular gas price was $2.40 per gallon on Biden’s inauguration day. And no, it wasn’t the Biden Administration selling nearly 1 million barrels of crude oil from the strategic petroleum reserve to the Chinese government-owned Sinopec that Biden’s son Hunter is an investor (so, The Big Guy aka Joe Biden gets a 10% piece of the action). It is a slowing global economy that is helping to lower gasoline prices.

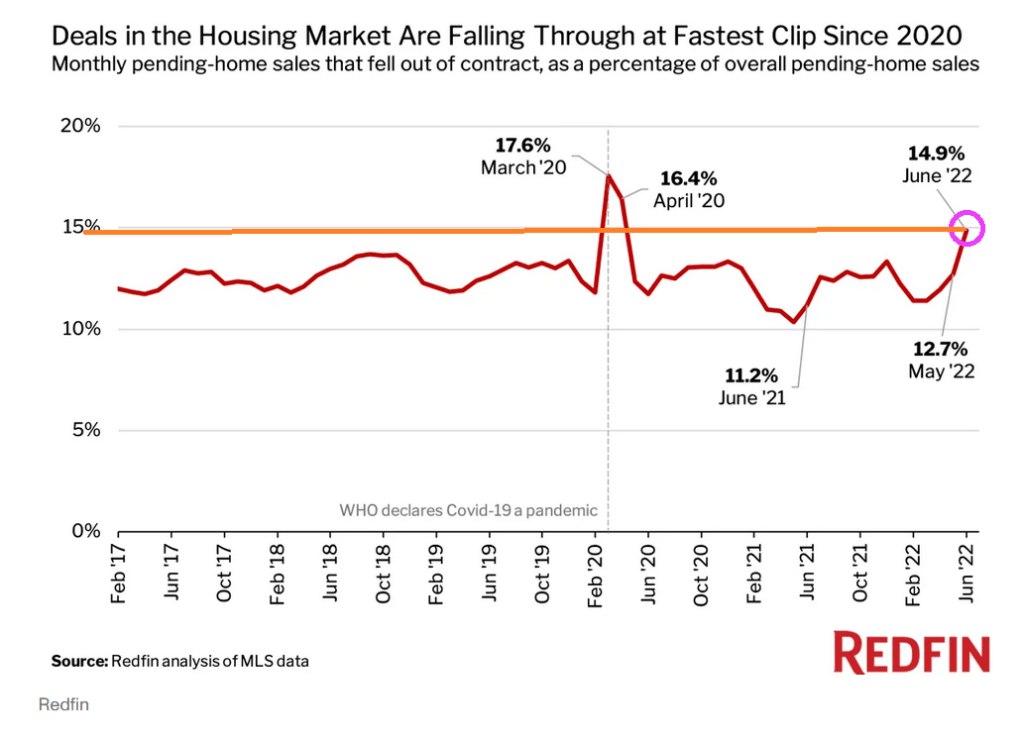

With rising mortgage rates, we are seeing a surge in pending home sales cancellations.

Atlanta Fed’s Raphael Bostic thinks that the US economy is so strong that it can easily handle a 75 basis point increase at the next FOMC meeting. Fortunately, he is not a voting member.

Generally speaking, The Federal Reserve cuts rates as a recession approaches. But not this time!

The Federal Reserve is expected to raise their target rate by 75 basis points at the next FOMC meeting.

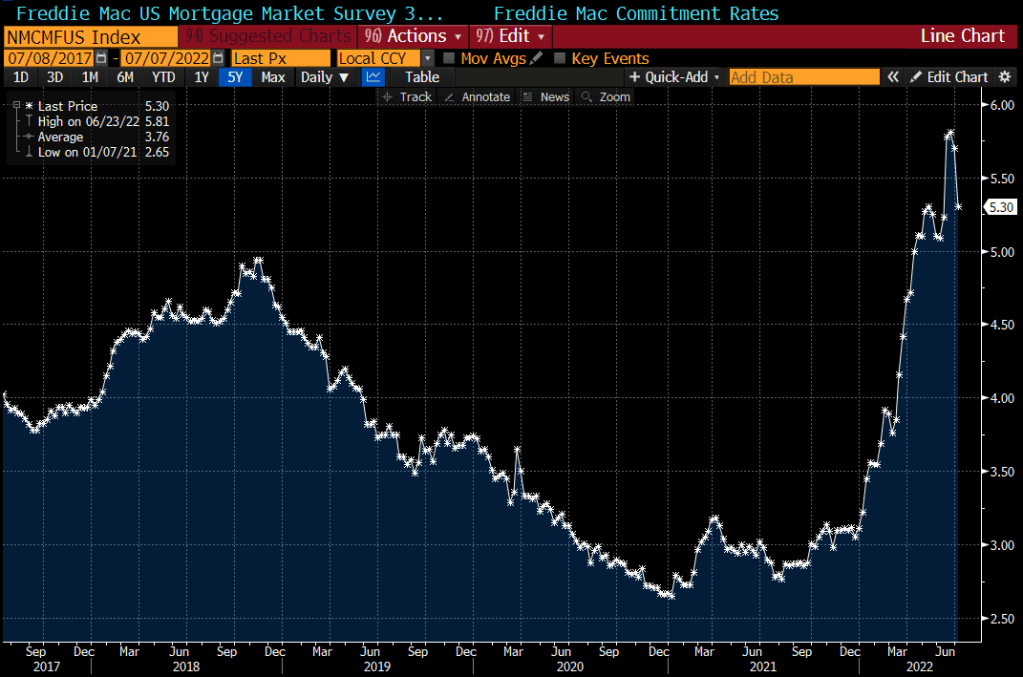

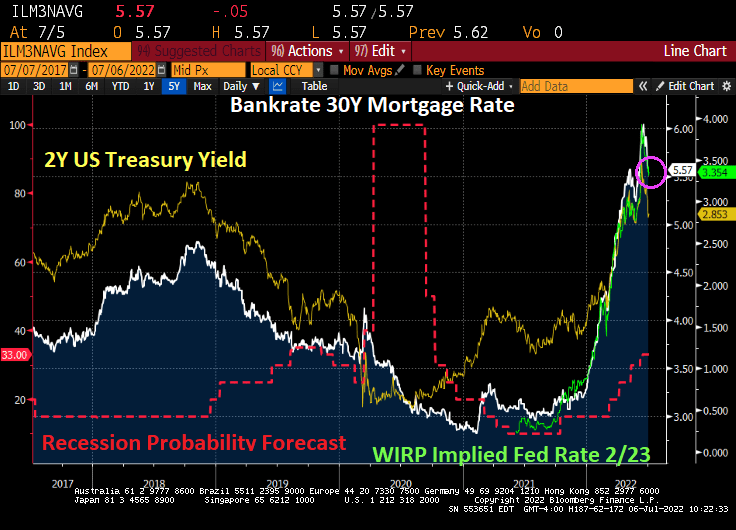

We are already seeing Fed rate hikes being priced into the mortgage markets, as Bankrate’s 30-year mortgage rate fell to 5.57% after rising above 6% in June. The reason? Recession fears have caused Treasury yields to fall.

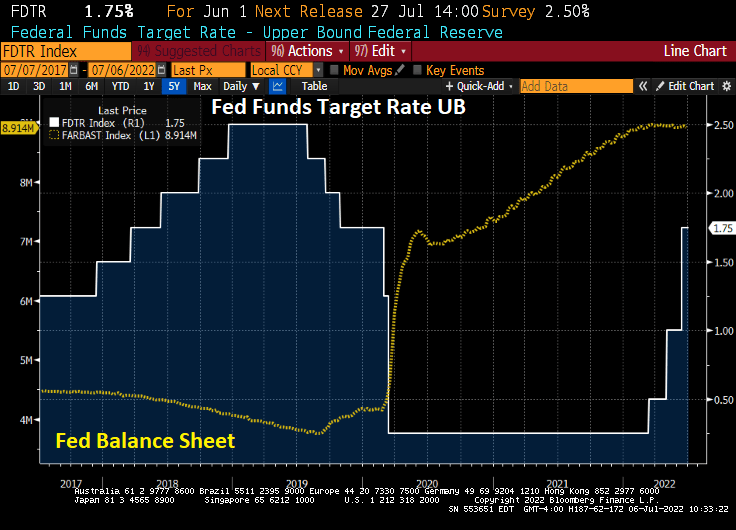

The Fed is hiking their target rate, but has been sloth-slow in unwinding their balance sheet.

Yes, The Fed has been sloth-slow in removing the Covid-related stimulus. But is The Fed trying to pull a “Volcker” by raising rate to choke off inflation EVEN IF THE ECONOMY ENTERS RECESSION? Fed Funds Futures data is pointing to a reversal of Fed rate hikes by Feb 2023.

Here is Fed Chair Jerome Powell showing the amount of Covid-related stimulus removed recently.

Well, this is one way to get inflation under control … crash the economy. And inflation fears growing, we are seeing mortgage rates declining and mortgage applications increasing.

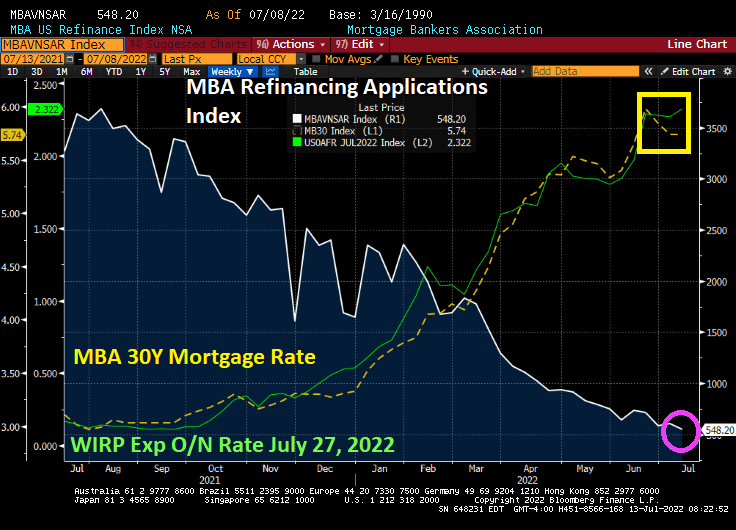

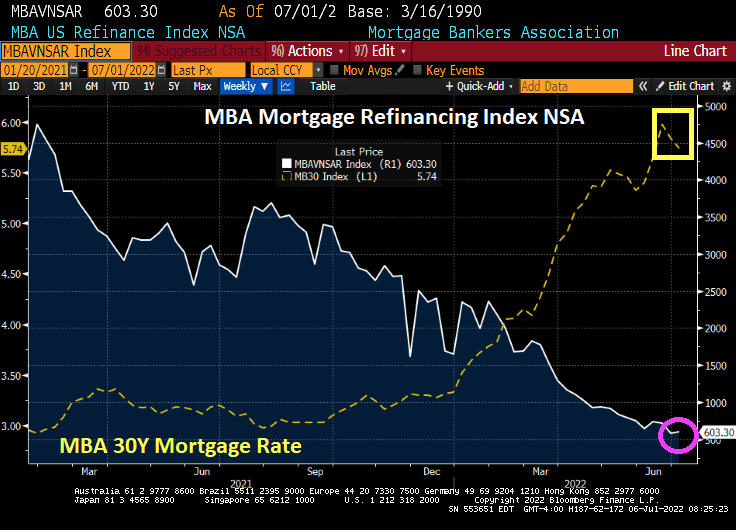

Mortgage applications decreased 5.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 1, 2022. This week’s results include a holiday adjustment to account for early closings the Friday before Independence Day.

The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index increased 7 percent compared with the previous week and was 17 percent lower than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 78 percent lower than the same week one year ago.

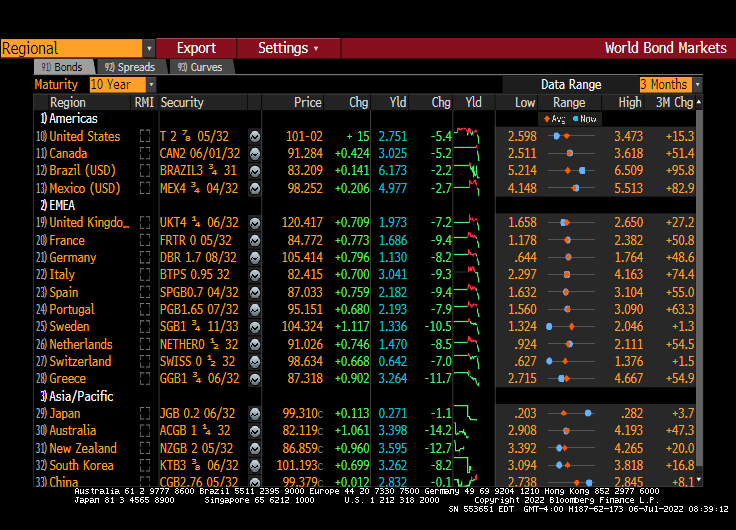

TED refers to the difference between the three-month Treasury bill and the three-month LIBOR based in U.S. dollars, a measure of fear in the market.

The 3-month TED spread is rising awfully fast. A sign of impending recession.

US bank credit default swaps (CDS) are rising fast as inflation gets ugly.

The US Treasury 10Y-3M curve is bumping against the zero barrier.

I am still shaking my head at President Biden chastising gasoline stations for not lowering prices at the pump when refiners are near full capacity and the Biden Administration is doing nothing to increase the supply of US-source non-green energy.

As The Fed raises rates in their attempt to wrangle inflation, we are seeing an about-face in the US housing market.

The pandemic-related Fed monetary stimulypto begat a housing boom that is careening to a halt as the fastest-rising mortgage rates in at least half a century upend affordability for homebuyers, catching many sellers wrong-footed with prices that are too high. It’s an astonishing turnaround. Just a few months ago, house hunters felt pushed to make offers within days, waive inspections and bid way above asking. Now they can sleep on it and maybe even shop for a better deal.

It doesn’t mean real estate is heading for a crash on the order of 2008. But when a market reaches these heights, even a drop toward normalcy will feel steep. And of course, a recession could make everything worse.

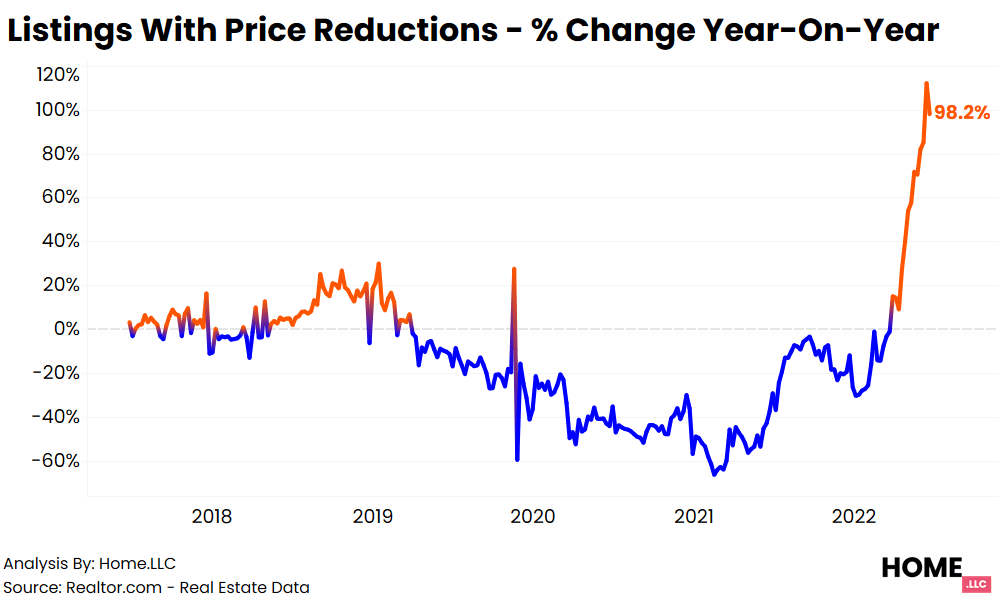

Dallas, Phoenix AZ and Las Vegas NV are leading in the price-slashing derby.

No, not the Claus von Bülow kind of reversal of fortune where has was accused of killing his wife. But this murder is coming from The Federal Reserve hiking interest rates even when they know that doing so could lead to a recession. And Biden’s anti-fossil fuel energy policies.

And investors in the Fed Funds Futures market see The Fed changing its rate-hiking ways in February 2023.

Inflation is what is killing the US economy and millions of households. Financially speaking.

And Biden’s approval ratings are sinking faster than The Titanic. In other words, he’s just killing us.

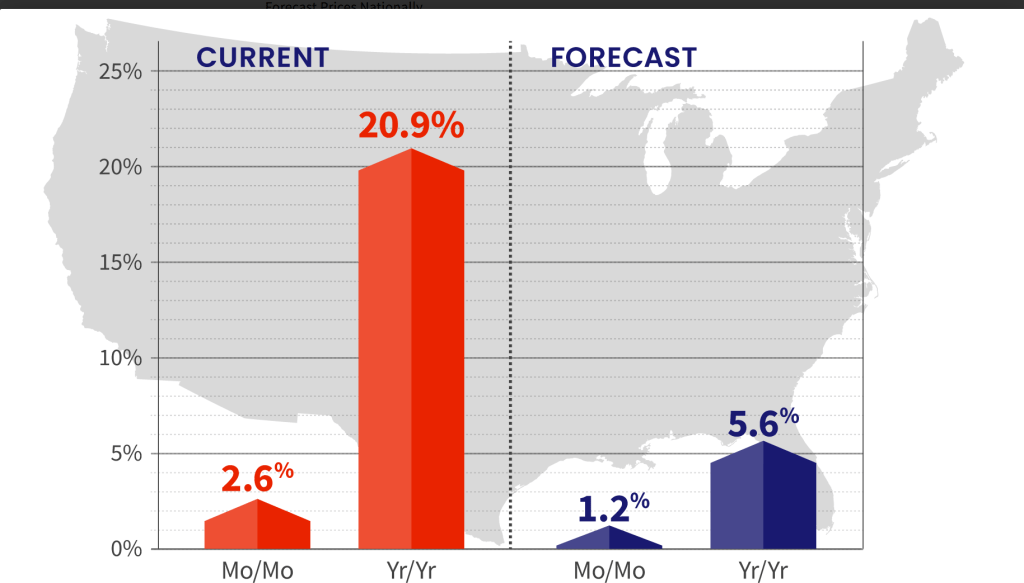

And then we have turbulence in the housing market as Fed intentions are driving up mortgage rate which helped listings with price reductions at 98.2% YoY.

Biden’s energy policies plus The Fed’s war on inflation will result in an economic reversal of fortune.

You must be logged in to post a comment.