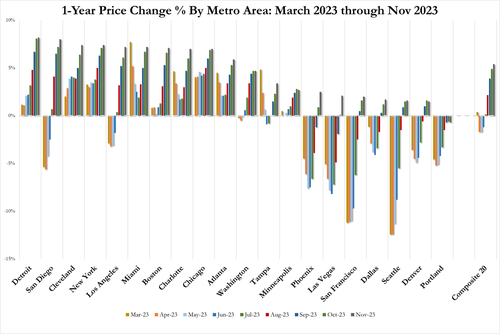

Home prices in America’s 20 largest cities rose for the 10th straight month in November (the latest data released by S&P Global Case-Shiller today), up 0.15% MoM (considerably slower than the 0.50% MoM expected and 0.63% prior).

That is the weakest MoM rise since Jan 2023.

Source: Bloomberg

That pushed the YoY price up to +5.40% (but well below the +5.8% exp)…

“November’s year-over-year gain saw the largest growth in U.S. home prices in 2023, with our National Composite rising 5.1% and the 10-city index rising 6.2%,” says Brian D. Luke, Head of Commodities, Real & Digital Assets at S&P DJI.

Six cities registered a new all-time high price in November – Miami, Tampa, Atlanta, Charlotte, New York, and Cleveland.

Portland is the only city with prices dropping YoY – who could have seen that coming?

Is this really what Jay and his pals were expecting when they embarked on an unprecedented tightening of monetary policy?

But, judging by the resumption of the rise of mortgage rates since the Case-Shiller data was created, we would expect prices to also resume their decline in the short-term…

Are prices set to shrink again (as the lag on Case-Shiller data and human’s response to rates) before re-accelerating later this year?

Yes, Cleveland hit an all-time high despite getting demolished by the Houston Texans in the wildcard game.

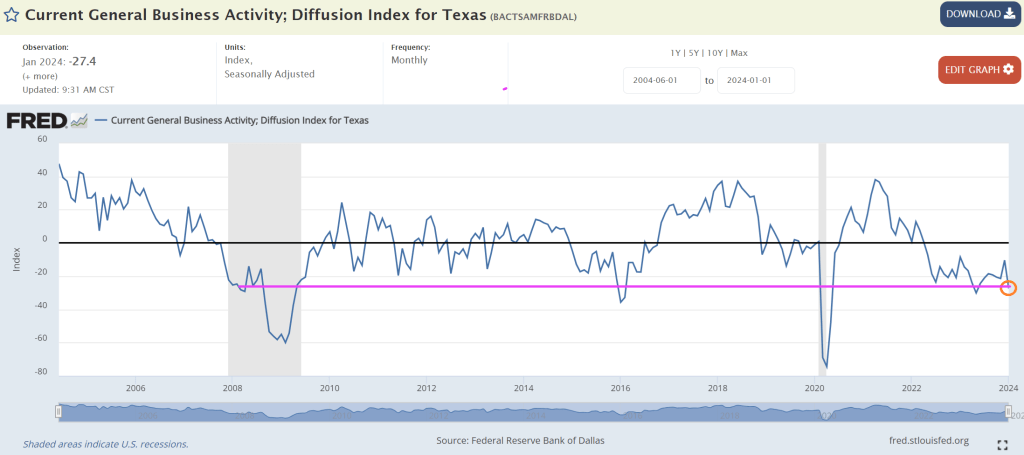

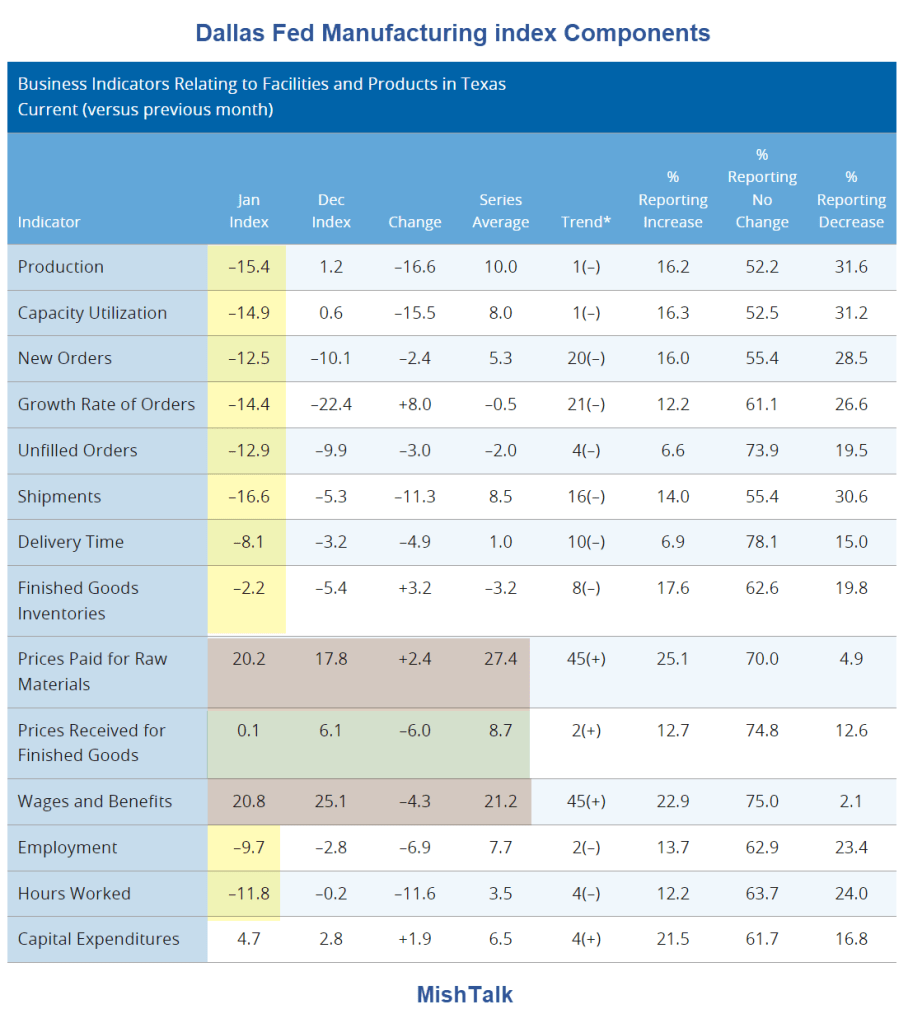

Other measures of manufacturing activity also indicated contraction this month. The new orders index ticked down from -10.1 to -12.5 in January, while the growth rate of orders index remained negative but pushed up eight points to -14.4. The capacity utilization index dropped to a multiyear low of -14.9, and the shipments index slipped 11 points to -16.6.

Perceptions of broader business conditions continued to worsen in January. The general business activity index fell from -10.4 to -27.4, and the company outlook index fell from -9.4 to -18.2. The outlook uncertainty index held fairly steady at 20.9.

Note that prices paid for raw materials soared by 20.2%.

Meanwhile, The Fed is impressed by the growth in the economy (primarily government jobs) so will likely keep rates constant this week. I wish they would look at Texas slumping!

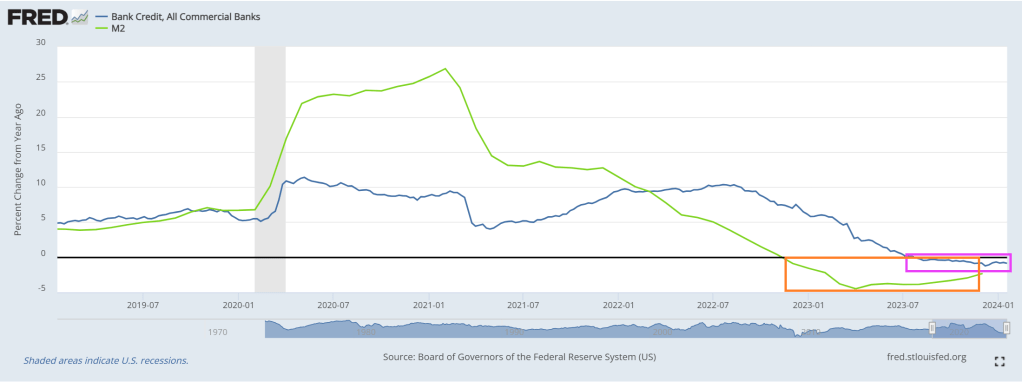

Where do we sit today? Bank credit growth has been negative for the last 26 weeks. As M2 Money growth has stalled.

What will The Fed do?

While the FOMC may start the discussions around tapering QT as soon as at this meeting, tapering itself is still a ways off, and the actual end of QT will come early next year.

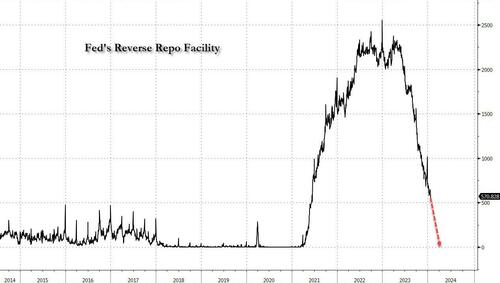

In January and May 2022, the FOMC published the principles and then the plan for QT. The fact of a taper this year is not news. More recent communication from Fed officials (for example from President Logan and Governor Waller) reinforced a preference for the reverse repo (RRP) facility to be drawn down to zero, and we infer that getting the RRP near zero will be the starting point for the taper.

Historically, the FOMC has taken at least two meetings to finalize these types of plan, and the December minutes stressed a desire to give the market lots of advance notice. As a baseline, we think the FOMC announces the parameters for the QT taper at its May meeting and enacts that taper in June, by cutting the runoff of Treasury securities in half. Because the Fed’s RRP facility has been declining rapidly, that timing could shift earlier by a month or so.

The change to shedding $30 billion per month in Treasuries would slow the pace of runoff materially, but there is clearly a chance that the subsequent pace is even slower. President Logan pointed out that running off the balance sheet slowly could ultimately allow the Fed to shrink the balance sheet even more while mitigating the risk of money market disruptions. A June taper would be consistent with our house view on the path of the RRP facility, which we expect to stand at approximately $225 billion at the end of May and be depleted by August.

We anticipate that reserves will remain broadly around current levels until RRP is depleted. But from there, we think reserves will ultimately fall to roughly $3.2 trillion, around $300 billion below current levels, and the FOMC will call off QT in early 2025. That view on the ending level of reserves reflects our outlook on the SOFR – IORB (Secured Overnight Funding Rate – Interest on Reserve Balances) spread turning positive, indicating the end of abundant reserves.

For broader markets, however, our strategy team does not expect the tapering and end of QT to be a significant event. Our rates strategists think the phenomenon is mostly in the price and, if anything, front-end swap spreads may have already overreacted to the news of an early taper. With a limited effect on rates, and the tapering and end of QT largely anticipated, our MBS and credit strategists similarly see few if any implications. Of course, some market narrative is focused on QT’s effects on the banking sector. While the intuitive notion that QT must destroy deposits is widespread, we have highlighted the data which show in fact that deposits have edged up, not down, in recent months as QT has progressed. Banks can always choose to bid for wholesale deposits, so instead of focusing on the quantity of “money” and how that changes, a better question is how bank funding costs are evolving.

So, the next step is for the Fed to shift from “talking about talking about tapering QT” to actually talking about tapering QT. Only after that step will we start to look for the end of QT, which the Fed will determine with an eye on money market conditions. In particular, the Fed is looking at whether SOFR is trading below the rate the Fed pays on reserves, in which case it will likely judge conditions to be accommodative, or above the rate the Fed pays on reserves, in which case the Fed’s calculus will change and the discussions about the end of QT will pick up steam.

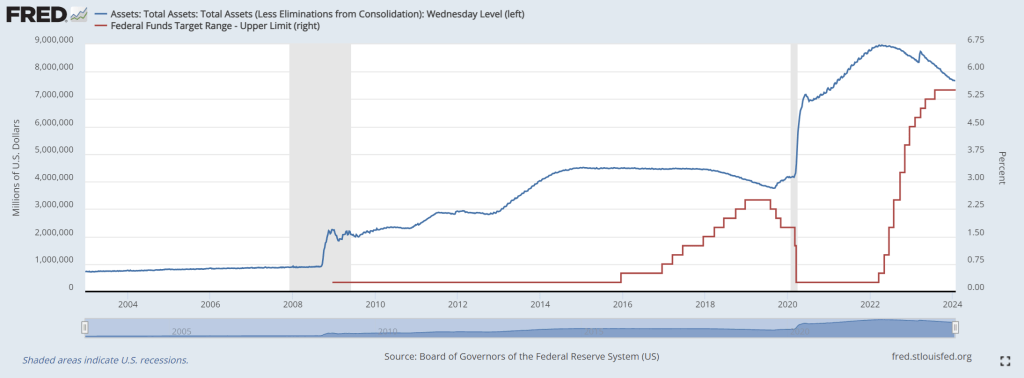

The Fed’s balance sheet remains greatly expanded despite the increase in The Fed’s target rate. Nothing has been the same since the banking crisis of 2008-2009. And Covid in 2020.

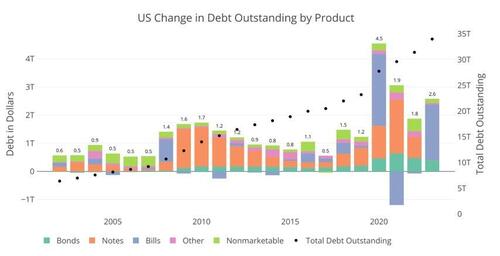

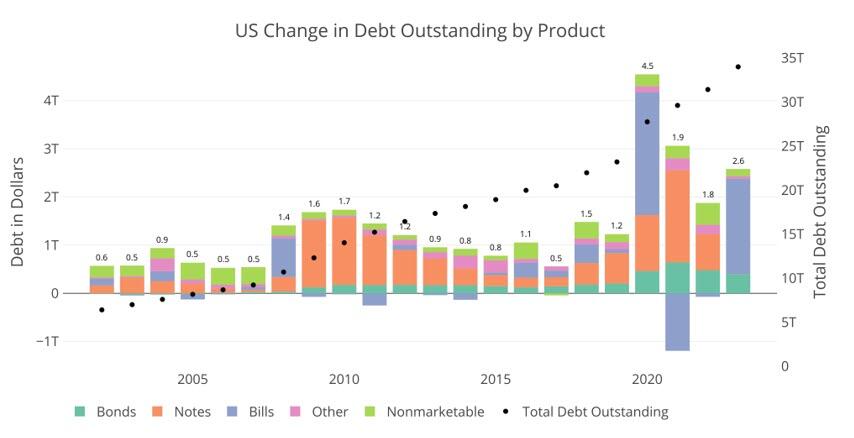

The only other times Bills were used as a primary funding source was in 2008 during the Great Financial Crisis and 2020 during Covid. Neither year came close to 77% of total new debt issuance. These were also emergency times, and specifically in 2021, almost half the short-term debt was retired in favor of Notes and Bonds to undo the 2020 Bill issuance.

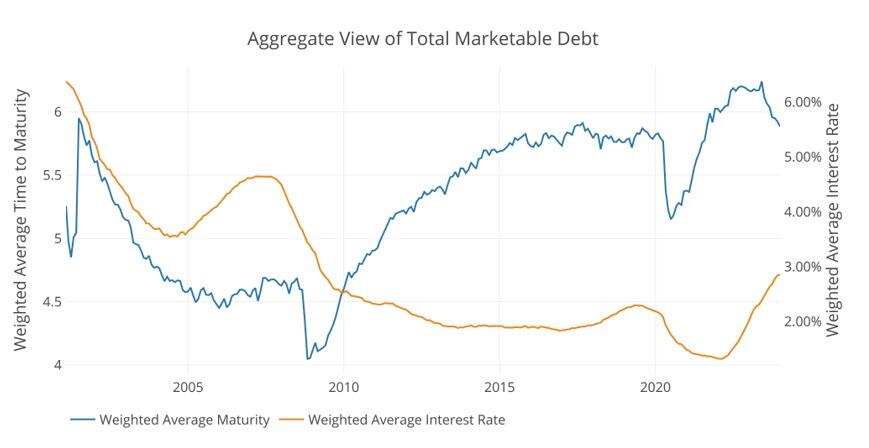

The Treasury has spent nearly two decades trying to extend the maturity of the debt. This can be seen in the blue line below that shows the average debt maturity. When the short term debt is issued in such a way, it drives down the average maturity, which causes the Treasury to have to roll-over more debt in shorter time periods. So why has the Treasury all of a sudden gone entirely to short-term debt in non-emergency times? The answer lies in the orange line, so let’s dig in.

Figure: 2 Weighted Averages

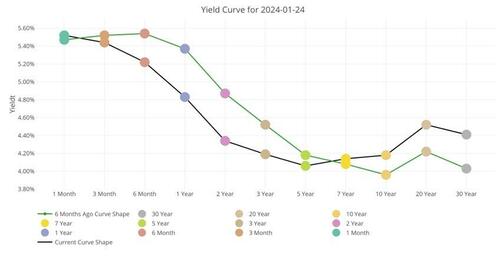

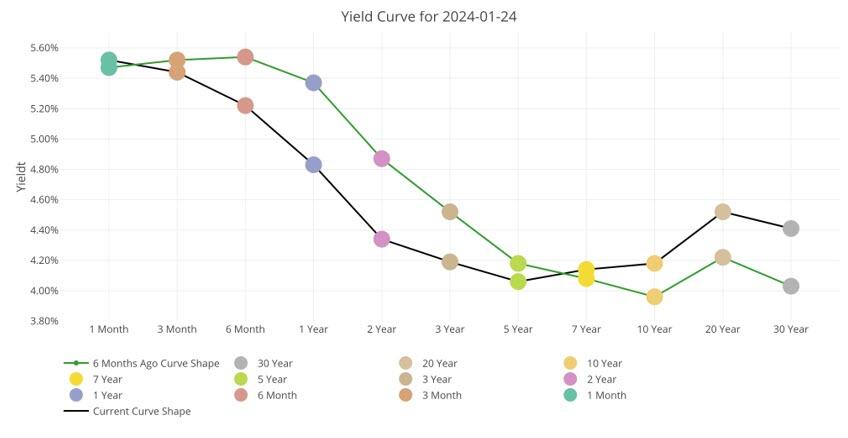

First, it is important to understand the interest rates the Treasury is facing. The chart below shows the current yield curve as it stands today and 6 months ago. As you can see, short-term rates are a full 1%-1.5% higher than medium-term. What?!? Didn’t we just see that the Treasury has specifically targeted short-term debt?

Why are they paying more than they have to? Had the Treasury financed the $2T with Notes, they would have saved $30B in interest this year alone!

Figure: 3 Tracking Yield Curve Inversion

So, why have they done this? Well, there are two potential possibilities.

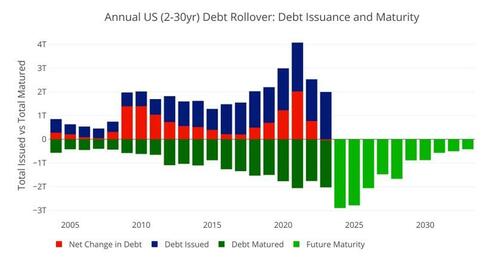

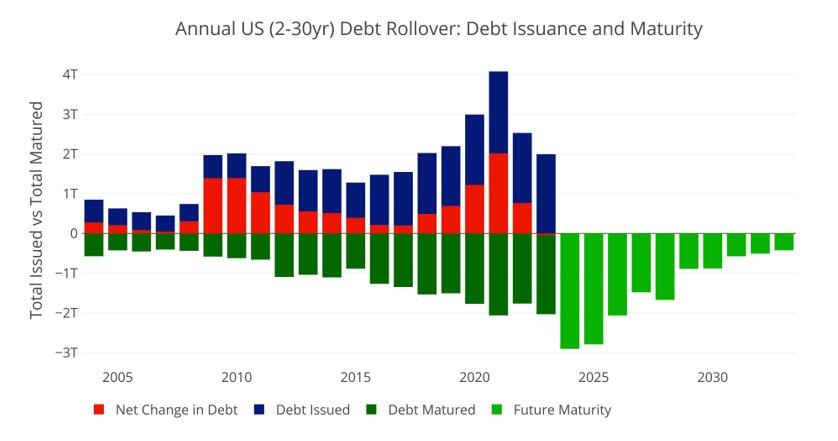

First, they may be nervous about the market’s ability to handle so much medium-term debt. The market typically digests short-term debt very easily, but it can become saturated with medium-term debt. The chart below shows the amount of medium-term debt that rolled over last year. This is not new issuance; this is debt maturing that needs to be rolled over.

As shown, nearly $2T rolled over last year. This means, had the Treasury issued Notes instead of Bills, the Market would have had to absorb a whopping $4T in new medium-term debt like they did in 2020. The difference this year is that back in 2020 the Fed bought nearly all of that debt, putting a floor under the market.

Compounding this problem further is that this year is set to be a record year in terms of debt rollover. Nearly $2.9T in Notes need to be rolled over.

Figure: 4 Treasury Rollover

Still, even with that massive amount of debt issuance, there must be more to the story. Why would Yellen specifically pay $30B more in interest just because she is concerned the about the volume of debt issuance. As Figure 1 above shows, this has never been a concern in the past except in emergency situations. Furthermore, why not issue at least some new debt as medium-term.

This lends to a second, and more probable conclusion. Long-term rates are set to fall in the very near term. The Treasury did not want to lock in for 2-7 years at 4% if it knows rates will fall. It will pay a premium ($30B this year), if it means it can lock in lower rates for longer and save the money on the back end.

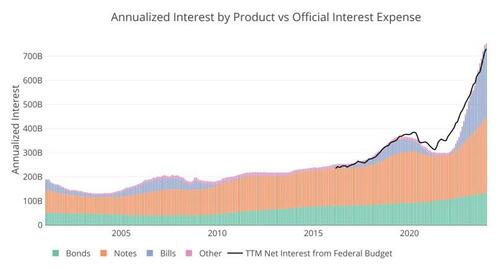

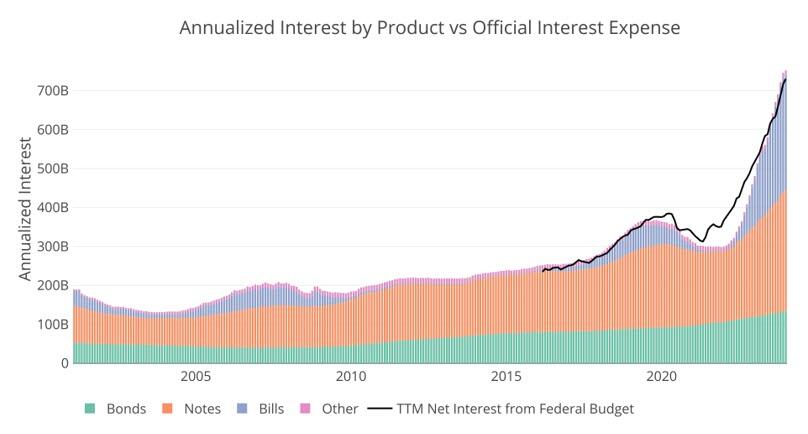

So, why are long-term rates, going to fall? Because they have to… the chart below shows the current interest owed on the national debt annualized. It’s not a pretty picture, and you can see how the interest from Bills has absolutely ballooned.

Figure: 5 Net Interest Expense

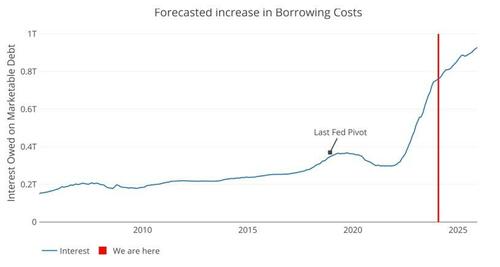

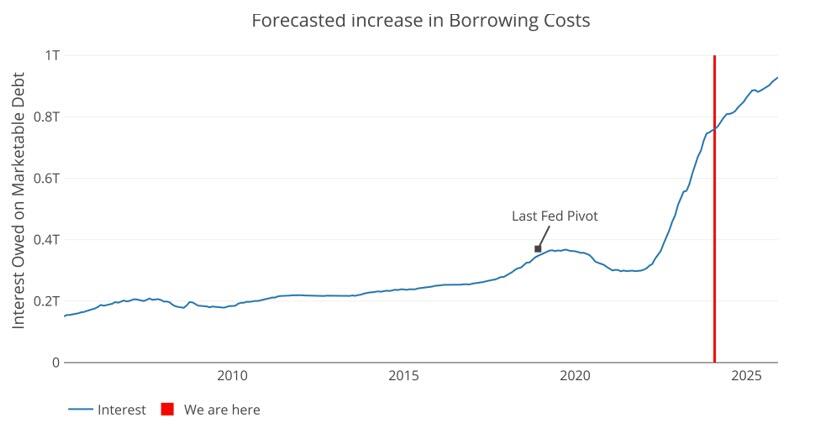

The Fed has come out with their dot plot that shows a calm glide path down. Well, we can take the debt maturity and push it forward at the projected rate of the Fed. Even given the current proposed 6 rate cuts, and getting back to 3.5% by early 2025, the trajectory for interest expense is not looking good.

Given current projections by the Fed, the Treasury will owe over $900B on interest by 2025. That is a debt death spiral. The Fed had to pivot back in 2018 when interest expense neared $400B. Next year, the cost will be more than double that!

Figure: 6 Projected Net Interest Expense

There is a potential third option. It’s an election year. Maybe Yellen is doing everything and anything to keep the financial system running smoothly. She has decided that the Treasury market must remain 100% stable and wants to take no chances. Thus, she issues tons of short-term debt, costing the tax payer an extra $30B this year and decides it’s a problem to be fixed at a later date.

While this would be wildly irresponsible and corrupt, the real argument against possibility 3 is the same as possibility 1, the market should be able to ingest at least some medium-term debt. This means the only logical conclusion is that she knows rates are coming down hard and fast. How does she know? Well, she used to be the head of the Fed.

There is no doubt, everyone in Washington can do the simple math above and recognize the Fed cannot take a glide path down. The only option is for rates to come down. Yellen just bet $2T on that outcome.

Joe, are you kidding about the sizzling economy? Karine Jean Pierre is also guilty of comedy or gross propaganda.

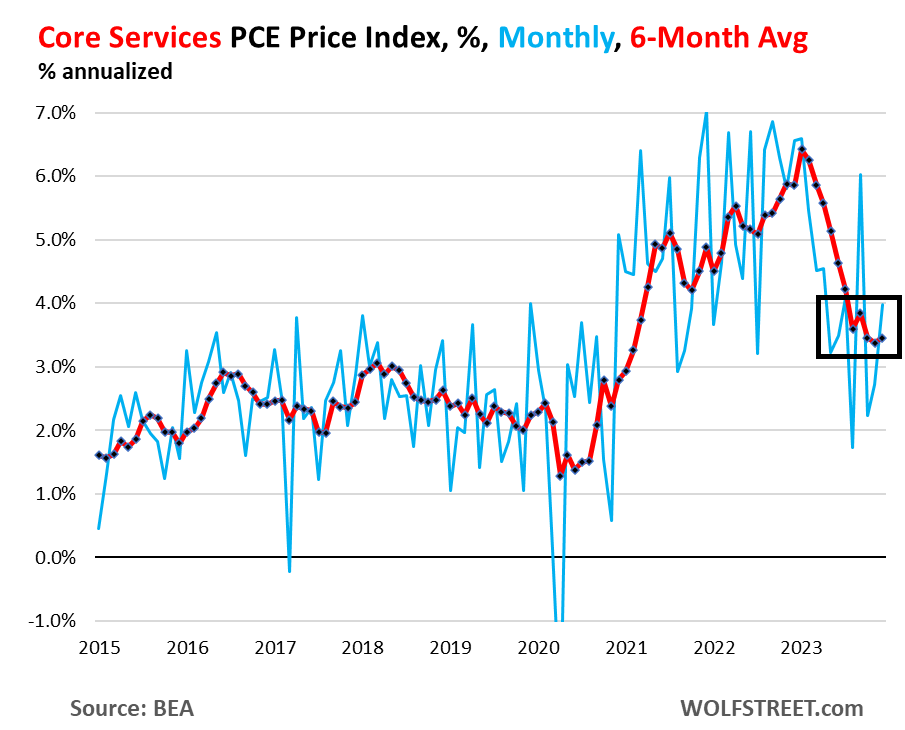

So right up front – and the Fed has been talking about this, though no one listens: The “core services” PCE price index has gotten stuck at 3.5% over the past six months annualized, and accelerated to 4.0% month-to-month annualized in December, with housing inflation stuck at about 6.7% over the past six months annualized, and with other core services components still red-hot.

The core services PCE price index rose by 0.33% in December from November, the second acceleration in a row, according to data from the Bureau of Economic Analysis today. This amounts to an increase of 4.0% annualized (blue).

The six-month moving average, which irons out the huge ups and downs of the month-to-month data, accelerated to 3.5%, and has been in this range since August, after the sharp deceleration in early 2023 (red).

Core services is where consumers spend the majority of their money, and they matter. Which is why Fed governors have said in near unison that they’re in no hurry to cut rates, but have taken a wait-and-see approach, with an eye on core services. And if it goes away, fine.

But on the surface, the PCE price index looks encouraging, and this has been the trend for months, with the overall PCE price index at +2.6% year-over-year in December, the lowest since March 2021; and with the core PCE price index at +2.9% year-over-year, also the lowest since March 2021, and aiming for the Fed’s 2% target.

The factors for the year-over-year cooling in these inflation measures have been the same for months: plunging energy prices, sharply dropping prices of durable goods after the huge spike in 2020 and 2021, cooling food inflation (with prices still rising from very high levels, but slowly), and favorable “base effects” when compared to a year ago.

But energy prices don’t plunge forever, so that will go away; durable goods prices don’t drop sharply forever either, though they can drop for a while longer to unwind some more of the price spike they’d been through in 2020 and 2021; and the base effects are going to get timed out this year, when the base of the year-over-year comparisons become the lower inflation figures of 2023.

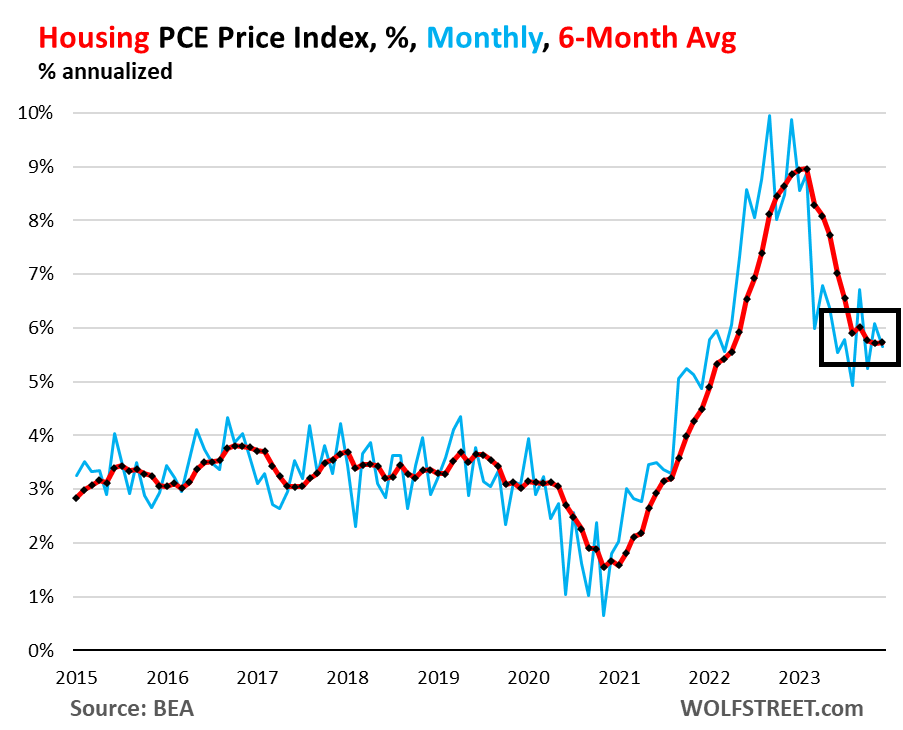

Housing inflation, still red hot and not cooling anymore. The PCE price index for housing rose by 0.46% in December from November and has been in this range since March, after the sharp slowdown early in 2023. This amounts to 5.7% annualized (blue in the chart below).

The housing index is broad-based and includes factors for rent in tenant-occupied dwellings; imputed rent for owner-occupied housing, group housing, and rental value of farm dwellings. It’s the largest component of core services.

The six-month moving average annualized, which shows the more recent trends, also rose by 5.7% in December, and has been in the same range since August (red).

So it looks like the PCE price index for housing has gotten stuck at 5.7%. This stubborn inflation in housing is a blow to theories trotted out for 18 months that housing was lagging, and that we know it will go away as an issue, etc., etc. The increases are less hot than they had been, but remain hot and have become persistent.

The major categories of core services in the PCE price index, as a six-month average of month-to-month changes, annualized:

Core services, major categories, 6-month average, annualized

Housing

5.7%

Description and chart above

Non-energy utilities

2.5%

Water, sewer, trash

Health care

2.5%

Physicians, outpatient, hospital, nursing care, dental, etc.

Transportation services

6.1%

Auto repair & maintenance, auto leasing & rentals, public transportation, airfares, etc.

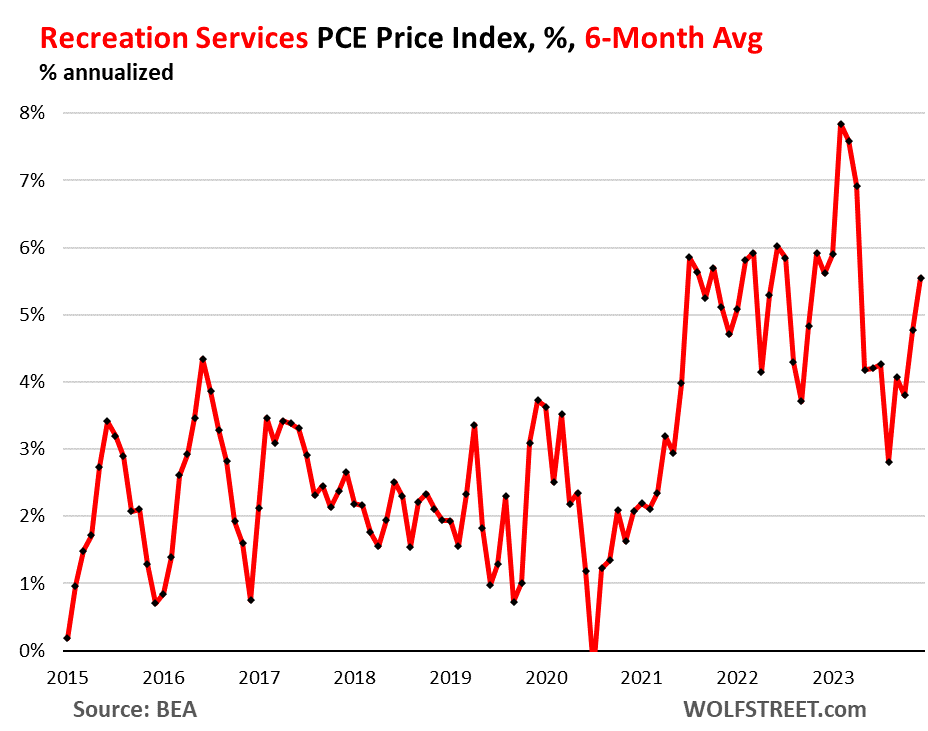

Recreation services

5.6%

Concerts, sports, movies, gambling, streaming, vet services, package tours, etc.

Food services, accommodation

2.8%

Meals & drinks at restaurants, bars, schools, cafeterias, etc.; accommodation at hotels, motels, schools, etc.

Financial services

3.5%

Fees & commissions at banks, brokers, funds, portfolio management, etc.

Insurance

2.8%

Insurance of all kinds, including health insurance

Other services

0.1%

Collection of other services

Inflation in Transportation services and Recreation services is accelerating on the basis of the 6-month moving average, with the PCE price index for Transportation services rising by 6.1%, and the index for Recreation services rising by 5.6%:

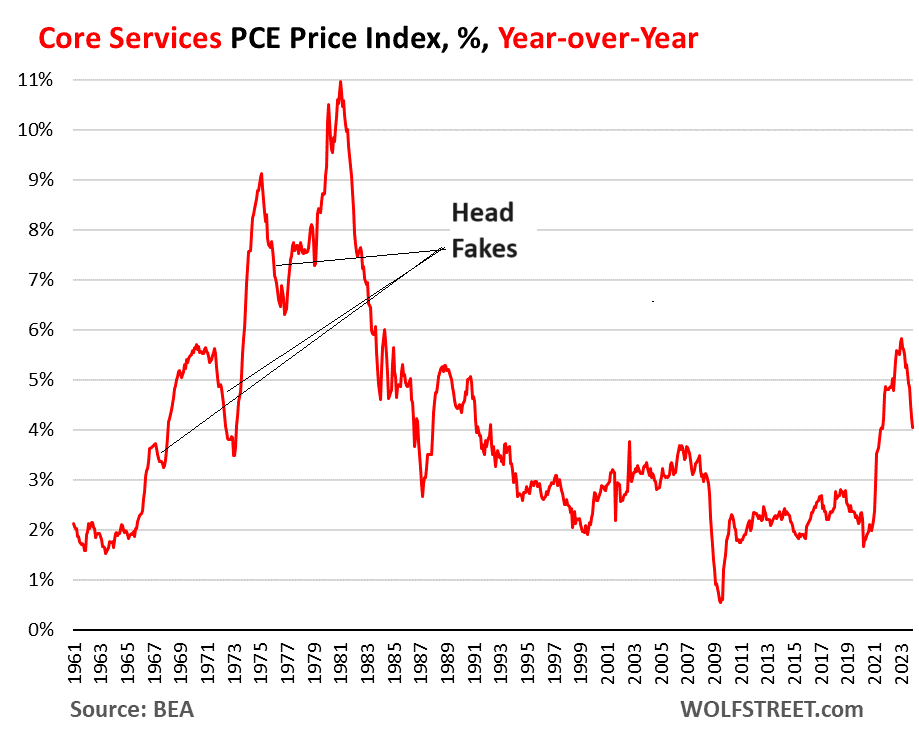

The head-fakes last time.

Inflation in services turns out to be tough to beat, and it can dish up big head-fakes. Last time we had this type of surge of inflation, so that was in the 1970s and 1980s, we thought repeatedly that we had inflation licked, only to find out that we’d fallen for an inflation head-fake. There were three head-fakes in core services on the way to the peak of 11% in 1981:

But Democrats are desperate to stay in power and rake in billons of dollars. Their strategy? Nobody But Joe. Well, except maybe Mike Obama.

Isn’t it wonderful to be 81 years old like Biden and a have a credit card with seemingly no credit limit? And partner with other octogenarians like Pelosi and McConnell to bankrupt the US? Free-spending US Senate Demagogue Democrat Chuck Schumer is only 73. But all these elderly politicians are heaping debt on to backs of younger Americans.

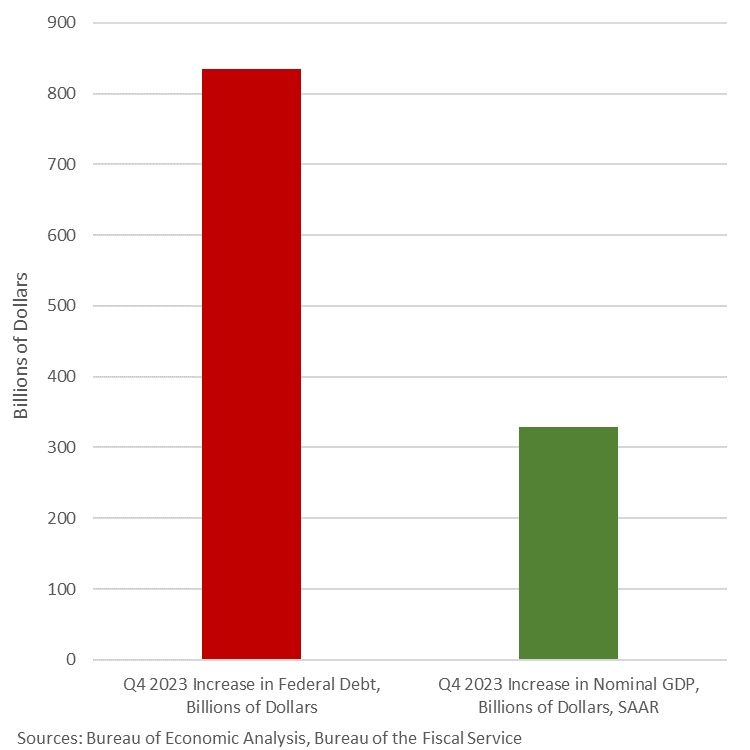

The “surprise” Q4 GDP report showed GDP rising by $182.6 billion. Unfortunately, Biden had to borrow $834 billion to get $182.6 in GDP.

Graphically, we can Biden’s folly where Q4 public debt grew almost 5 times faster than real GDP.

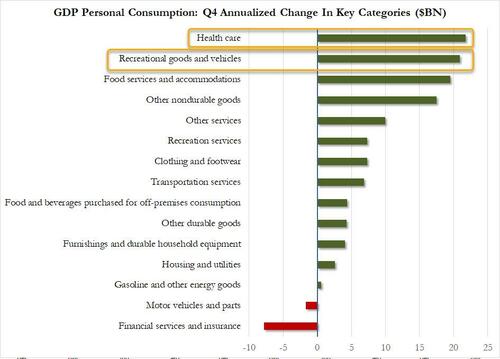

To quote Cousin Eddie from Christmas Vacation, “That there’s an RV.” Recreational goods and vehicles (aka, RVs) were second in Personal Consumption spending after America’s overpriced healthcare.

Spending on RVs makes sense since housing has become unaffordable for millions of households under Bidenomics.

Note that GDP growth was better under Trump (pre-Covid).

The increase in consumer spending reflected increases in both services and goods. Within services, the leading contributors were food services and accommodations as well as health care. Within goods, the leading contributors to the increase were other nondurable goods (led by pharmaceutical products) and recreational goods and vehicles (led by computer software). Within exports, both goods (led by petroleum) and services (led by financial services) increased. The increase in state and local government spending primarily reflected increases in compensation of state and local government employees and investment in structures. The increase in nonresidential fixed investment reflected increases in intellectual property products, structures, and equipment. Within federal government spending, the increase was led by nondefense spending. The increase in inventory investment was led by wholesale trade industries. Within residential fixed investment, the increase reflected an increase in new residential structures that was partly offset by a decrease in brokers’ commissions. Within imports, the increase primarily reflected an increase in services (led by travel).

Compared to the third quarter of 2023, the deceleration in real GDP in the fourth quarter primarily reflected slowdowns in private inventory investment, federal government spending, residential fixed investment, and consumer spending. Imports decelerated.

Current‑dollar GDP increased 4.8 percent at an annual rate, or $328.7 billion, in the fourth quarter to a level of $27.94 trillion. In the third quarter, GDP increased 8.3 percent, or $547.1 billion (tables 1 and 3).

The price index for gross domestic purchases increased 1.9 percent in the fourth quarter, compared with an increase of 2.9 percent in the third quarter (table 4). The personal consumption expenditures (PCE) price index increased 1.7 percent, compared with an increase of 2.6 percent. Excluding food and energy prices, the PCE price index increased 2.0 percent, the same change as the third quarter.

Personal Income

Current-dollar personal income increased $224.8 billion in the fourth quarter, compared with an increase of $196.2 billion in the third quarter. The increase primarily reflected increases in compensation, personal income receipts on assets, and proprietors’ income that were partly offset by a decrease in personal current transfer receipts (table 8).

Disposable personal income increased $211.7 billion, or 4.2 percent, in the fourth quarter, compared with an increase of $143.5 billion, or 2.9 percent, in the third quarter. Real disposable personal income increased 2.5 percent, compared with an increase of 0.3 percent.

Personal saving was $818.9 billion in the fourth quarter, compared with $851.2 billion in the third quarter. The personal saving rate—personal saving as a percentage of disposable personal income—was 4.0 percent in the fourth quarter, compared with 4.2 percent in the third quarter.

GDP for 2023

Real GDP increased 2.5 percent in 2023 (from the 2022 annual level to the 2023 annual level), compared with an increase of 1.9 percent in 2022 (table 1). The increase in real GDP in 2023 primarily reflected increases in consumer spending, nonresidential fixed investment, state and local government spending, exports, and federal government spending that were partly offset by decreases in residential fixed investment and inventory investment. Imports decreased (table 2).

The increase in consumer spending reflected increases in services (led by health care) and goods (led by recreational goods and vehicles). The increase in nonresidential fixed investment reflected increases in structures and intellectual property products. The increase in state and local government spending reflected increases in gross investment in structures and in compensation of state and local government employees. The increase in exports reflected increases in both goods and services. The increase in federal government spending reflected increases in both nondefense and defense spending.

The decrease in residential fixed investment mainly reflected a decrease in new single-family construction as well as brokers’ commissions. The decrease in private inventory investment primarily reflected a decrease in wholesale trade industries. Within imports, the decrease primarily reflected a decrease in goods.

Current-dollar GDP increased 6.3 percent, or $1.61 trillion, in 2023 to a level of $27.36 trillion, compared with an increase of 9.1 percent, or $2.15 trillion, in 2022 (tables 1 and 3).

The price index for gross domestic purchases increased 3.4 percent in 2023, compared with an increase of 6.8 percent in 2022 (table 4). The PCE price index increased 3.7 percent, compared with an increase of 6.5 percent. Excluding food and energy prices, the PCE price index increased 4.1 percent, compared with an increase of 5.2 percent.

Measured from the fourth quarter of 2022 to the fourth quarter of 2023, real GDP increased 3.1 percent during the period (table 6), compared with an increase of 0.7 percent from the fourth quarter of 2021 to the fourth quarter of 2022.

The price index for gross domestic purchases, as measured from the fourth quarter of 2022 to the fourth quarter of 2023, increased 2.4 percent, compared with an increase of 6.2 percent from the fourth quarter of 2021 to the fourth quarter of 2022. The PCE price index increased 2.7 percent, compared with an increase of 5.9 percent. Excluding food and energy, the PCE price index increased 3.2 percent, compared with 5.1 percent.

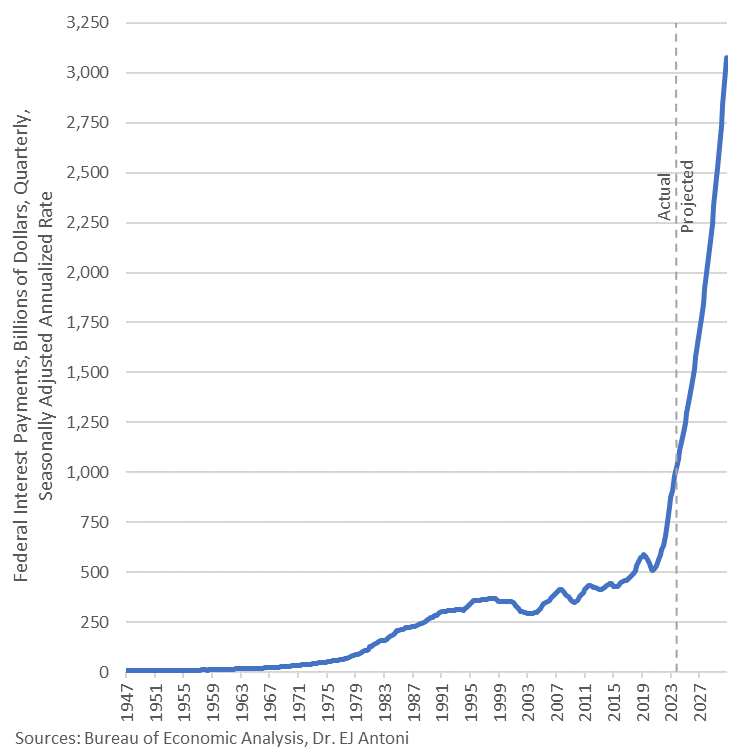

Annualized interest on the federal debt now exceeds $1 trillion and is projected to breach $3 trillion, annualized rate, by Q4 2030.

What can you get for an $834-billion increase in federal debt? Only a $328-billion increase in GDP. This economic “growth” in Q4 ’23 was fueled by gov’t expenditures and gov’t transfers, which in turn are fueled by deficits – sound sustainable?

This is Cousin Eddie’s RV. Cheaper than a house under Bidenomics!

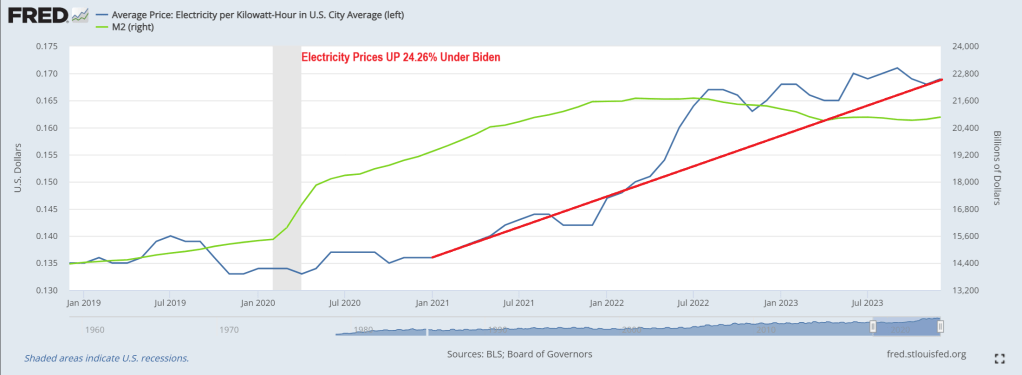

The average price of electricity has risen a whopping 24.25% under Biden and Bidenomics. Brrr!!

No wonder Biden only wants to talk about unlimited abortion and NOT the immigration (Fentanyl, child trafficing, crime, etc) fiasco at the border and continually rising prices. Or Biden’s growing wars.

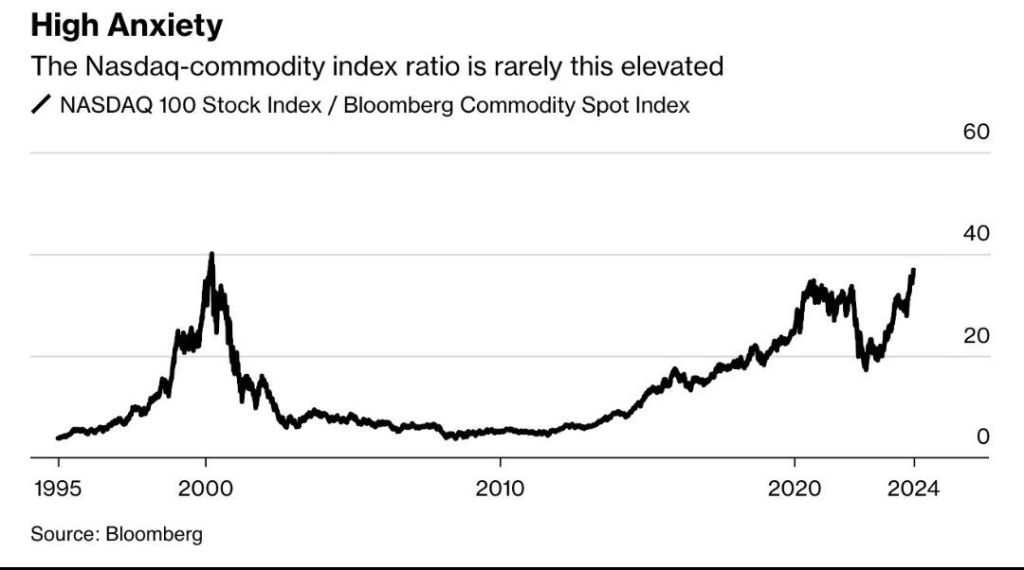

The NASDAQ commodity index RATIO is getting back to dot.com era bubble levels.

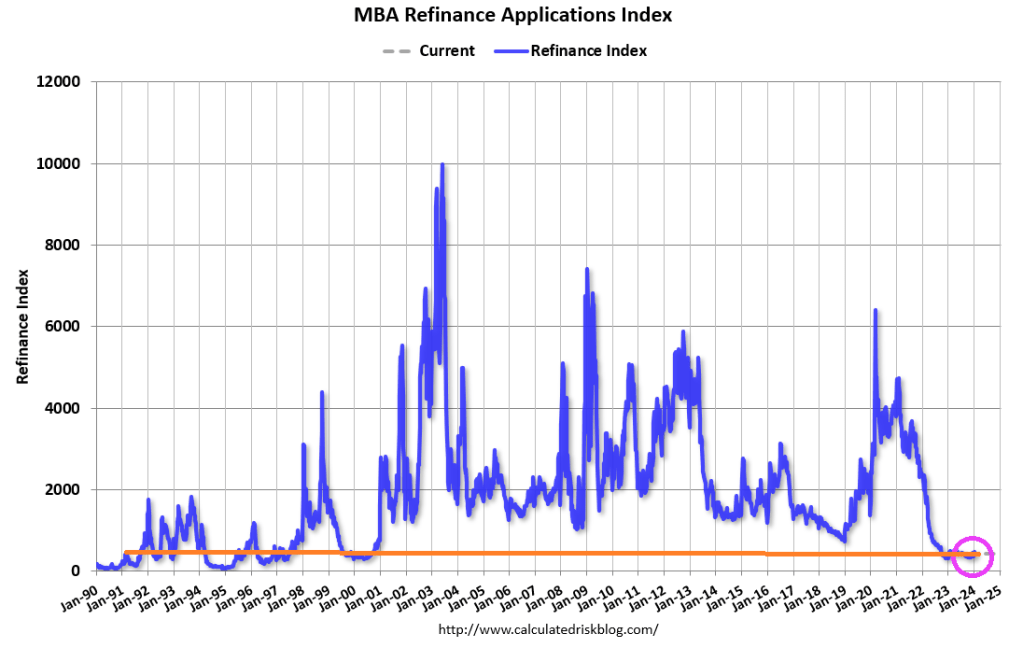

Biden’s green energy mandates, a boondoggle for China and lodestone for Americans, is leaking over to the mortgage market. That’s Bidenomics!

Mortgage applications increased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 19, 2024. The results include an adjustment to account for the MLK holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The holiday adjusted Refinance Index decreased 7 percent from the previous week and was 8 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 8 percent from one week earlier. The unadjusted Purchase Index increased 3 percent compared with the previous week and was 18 percent lower than the same week one year ago.

The unadjusted Refinance Index decreased 16 percent from the previous week and was 8 percent lower than the same week one year ago.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.