Fear the talking Fed! Various Fed Presidents are talking this week and when they do. WATCH OUT!

The latest fear mongering will be … inflation is persistent and they might have to keeep raising rates.

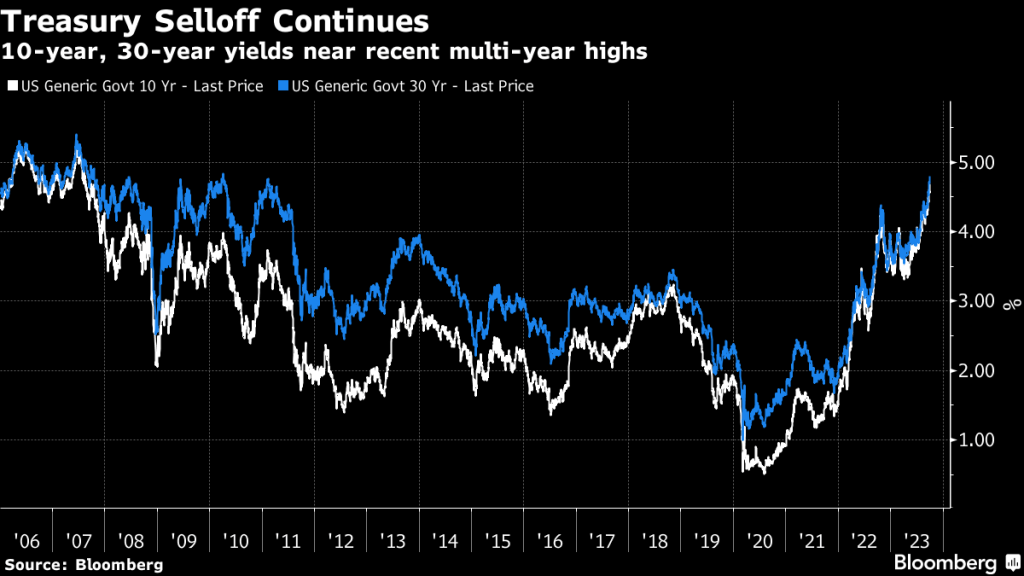

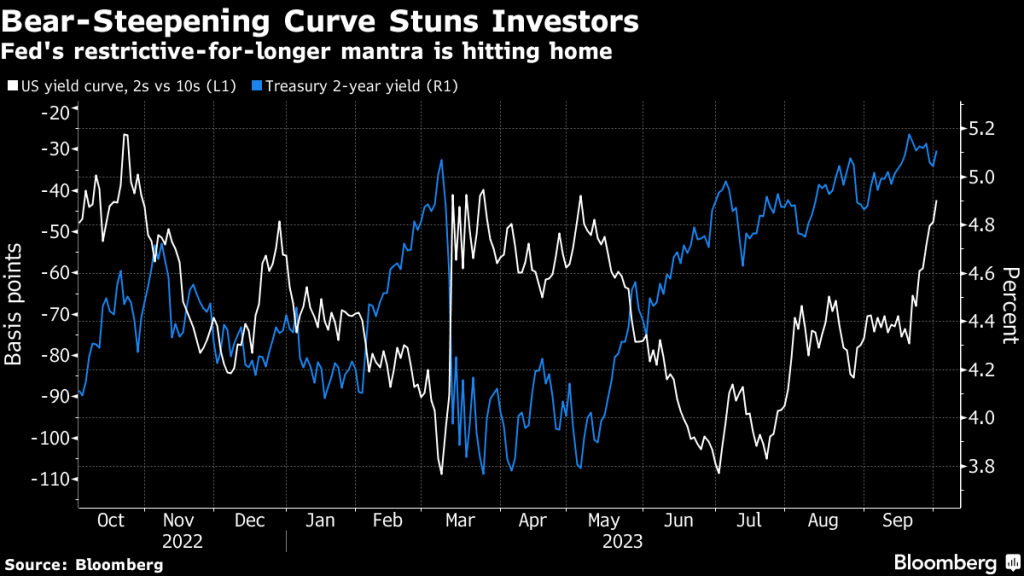

The two-year Treasury remains above 5% and the 10Y-2Y T-Curve remains inverted.

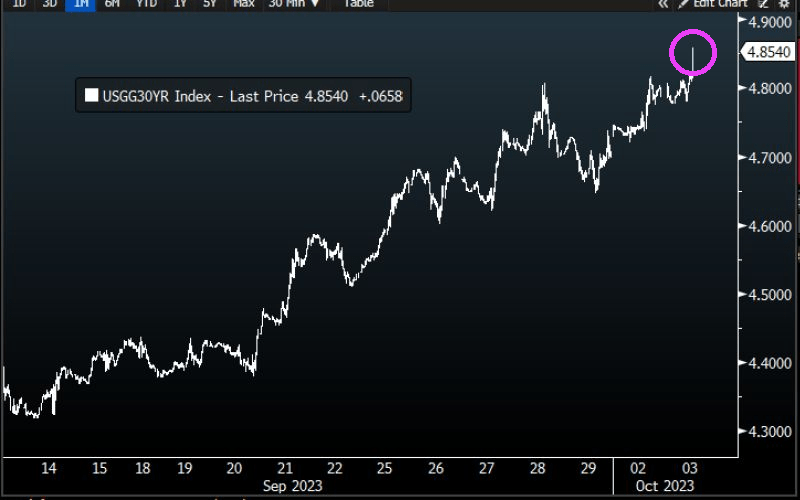

Treasury 30-year yield rose to 4.856%, HIGHEST SINCE 2007.

The likelhood of another Fed rate hike is growing.

While inflation is cooling (but still elevated), The Fed could choose to rate hikes again.

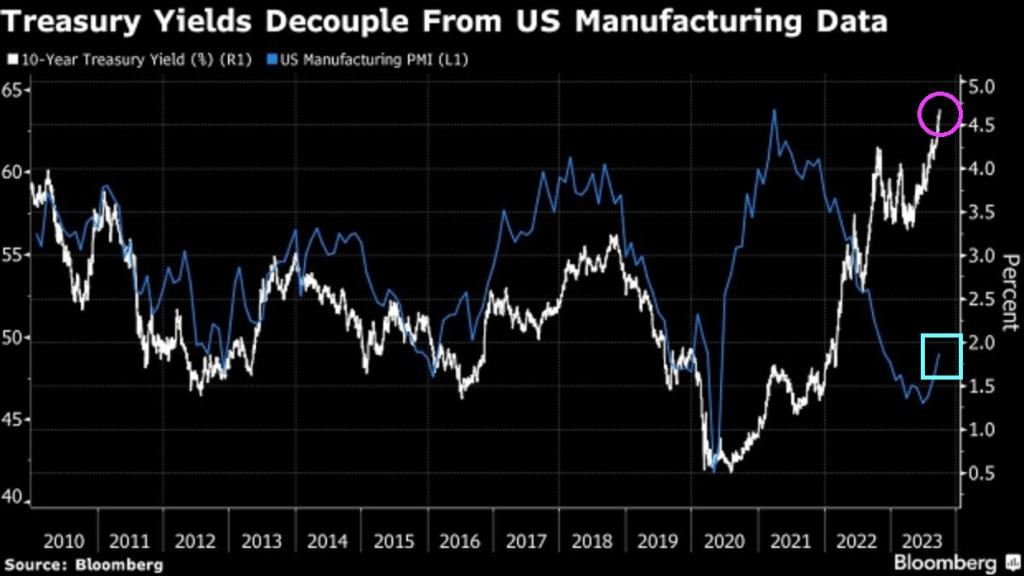

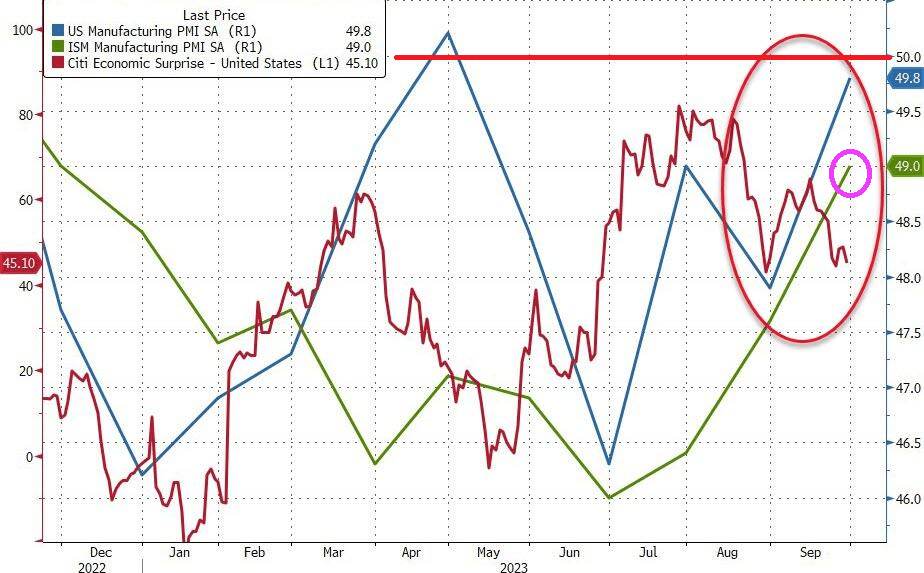

Treaury yields have decoupled from US manufacturing data.

Best picture of Lael Brainard, Director of the National Economic Council of the United States and former Federal Reserve member and talking head. Or screaming head.

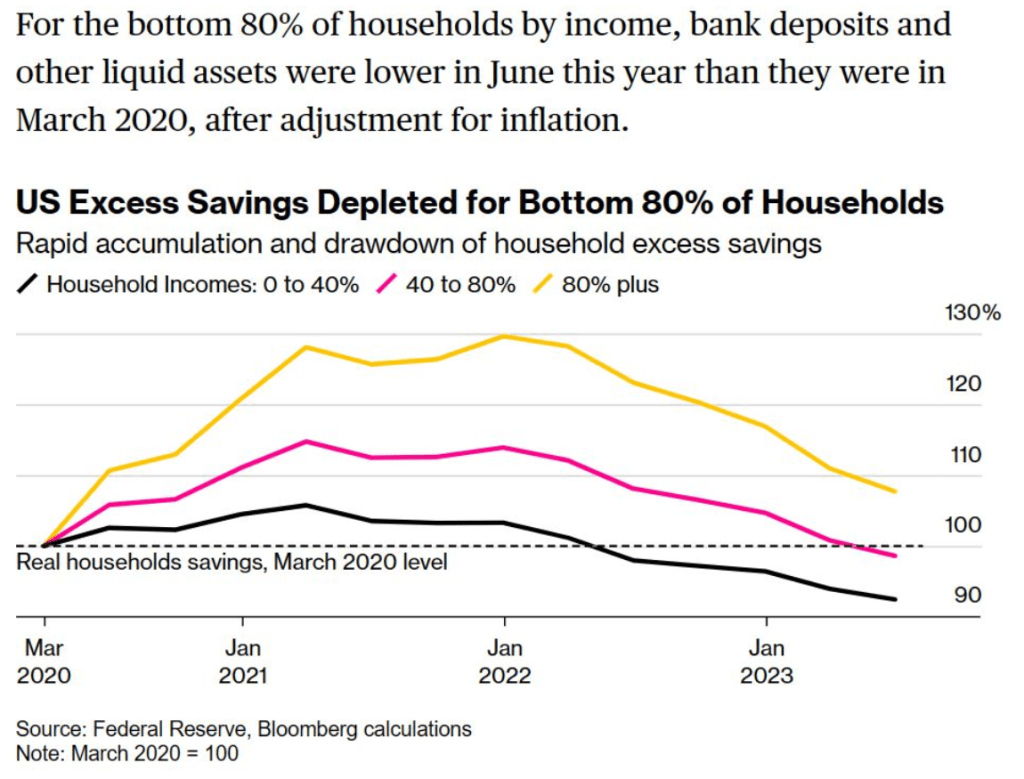

Wasting away again with Bidenomics, code for massive Federal subsidies to green energy donors. And incentives to buy impractical EVs. Imagine in an emergency and your car only goes 200 miles (and then you have to wait for an available charger to come open). Well, the top 1% are doing fine. But the bottom 80% of households by income are seeing rapid deplection of savings to cope with the rising costs of Bidenomics.

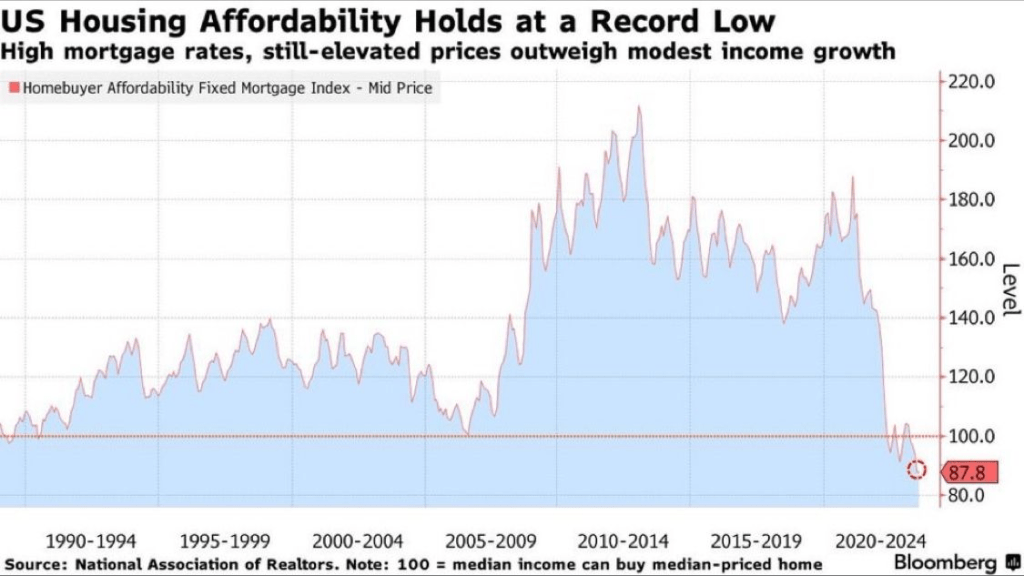

And then we have shrinking home affordability, now at a record low.

Well, it looks like Ukraine’s army is surrending in droves to Russian forces. Maybe this will end Biden’s obsession with doling billions of dollars to Ukraine. Nah, Biden will continue doling out billions to Ukraine, but this time it will be to rebuild Ukraine (while major US cities continue to rot). But in any case, Biden and Democrats refused to return to pre-Covid levels of spending.

Federal outlays (spending) has increased by 30% from January 2020, just prior to Covid. Yet, Republicans are unable (or unwilling) to get the Biden Administration and Democrats to cut Federal spending back to pre-Covid spending levels. M2 Money is up a whopping 36%.

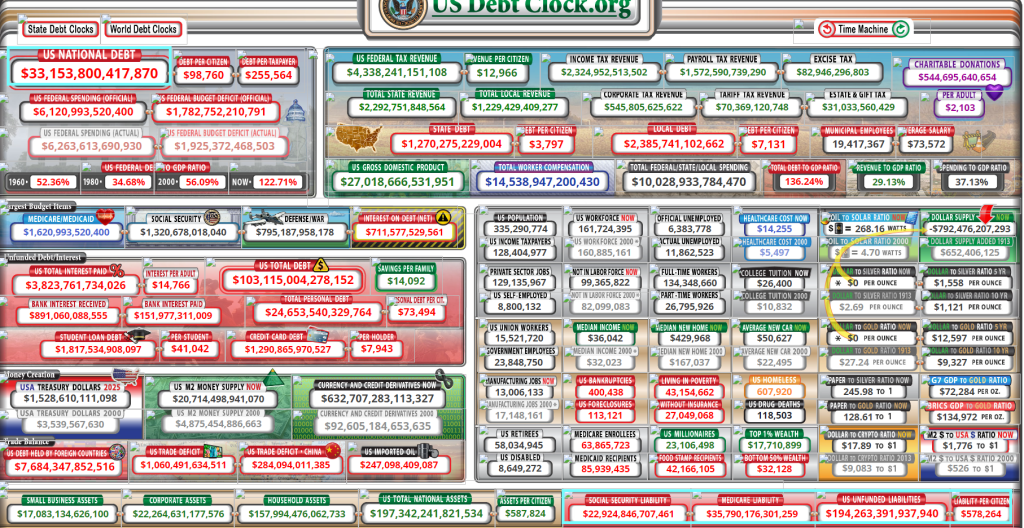

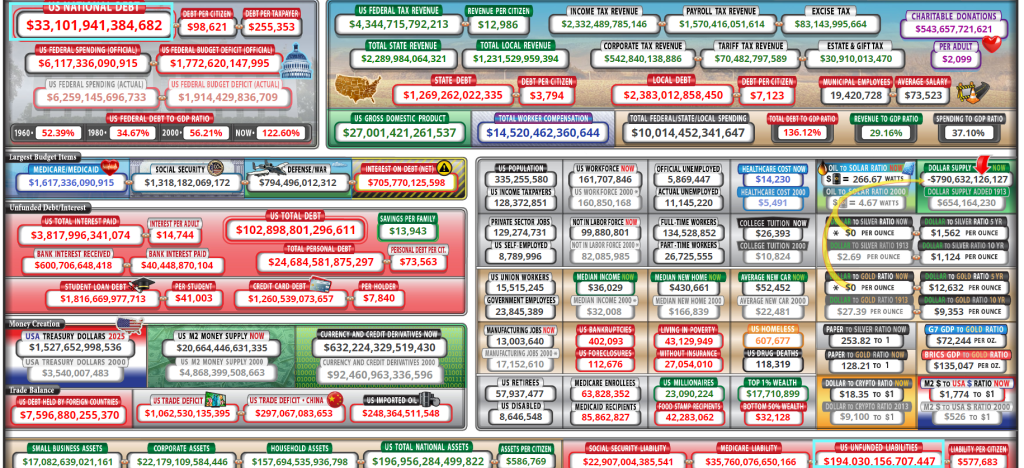

But never fear. US Federal debt is now above $33 trillion with $194+ TRILLION in unfunded liabilities. I feel dread after California governor “Gruesome” Newsom appointed The Fonz (a Democrat millionaire living in Maryland?) to replace Diane Feintstein in the US Senate.

S&P Global’s PMI Manufacturing jumped from 47.9 in August to 49.8 in September (and up from 48.9 in the flash September print). That is the highest print for US manufacturing since April but remains in contraction (below 5). That is the 5th straight month in contraction and 10th month in the last 11 in contraction (sub 50).

The ISM Manufacturing print also rose (to 49.0), up from 47.6 and better than the 47.9 exp (but still below 50 for the 10th straight month).

No, not Henry Winkler. But Laphonza Butler, a friend of VP Kamala Harris and the CEO of Emily’s List. And lauughably a resident of Maryland representing California.

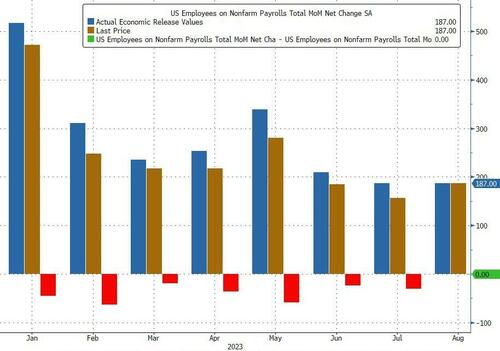

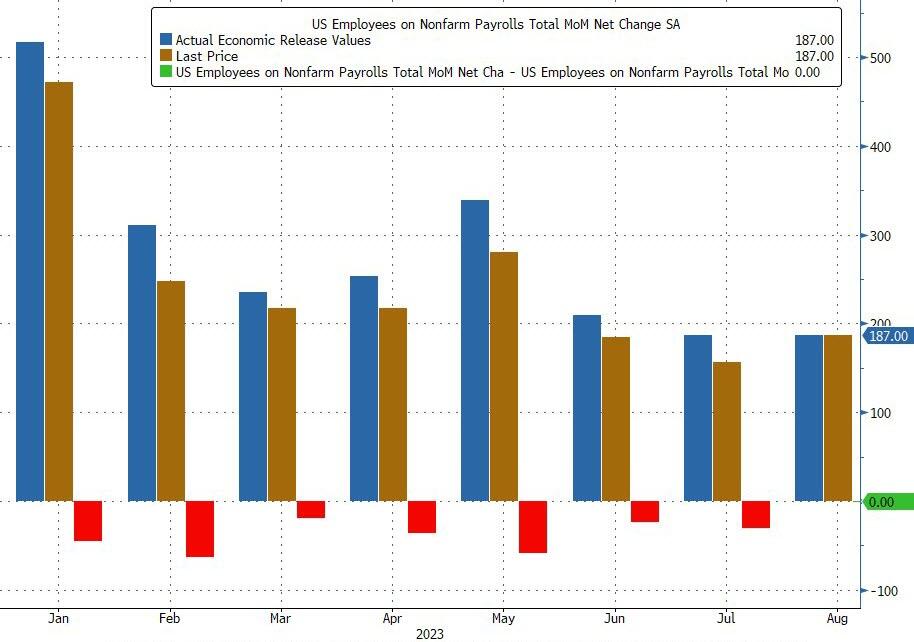

That has certainly been the case with US labor data, where as we first reported last month, every single monthly payrolls print in 2023 has been revised lower (see chart below), a 12-sigma probability and virtually impossible unless there was political pressure to massage the data higher initially and then revise it lower when nobody is looking.

But the BLS is not done: as we reported last week, besides the now traditional one-month lookback revisions the ridiculously high monthly payrolls prints accumulated over the past year will also be slowly but surely revised gradually lower at annual benchmark revisions for years to come. As Morgan Stanley chief US economist Ellen Zentner explained (full note available to pro subscribers)…

Payrolls get revised too, and we expect a downward revision. Payrolls have an annual benchmark revision that is published in February each year. The revision adjusts the level of payrolls through March of the prior year. For example, a new revision will be published in Feb-24, adjusting payroll levels from April-22 to Mar-23. And a preliminary estimation of the upcoming revision points to a decrease in payroll YoY% growth rates of -0.2pp.

But while downward payroll revisions under Bidenomics are as certain as death and taxes, what we wanted to discuss here are the just as striking downward revisions to US consumption which hit this morning alongside the comprehensive once every-five-years historical revisions to GDP. As a reminder:

Today’s release presents results from the comprehensive update of the National Economic Accounts (NEAs), which include the National Income and Product Accounts (NIPAs) and the Industry Economic Accounts (IEAs). The update includes revised statistics for GDP, GDP by industry, GDI, and their major components. Current-dollar measures of GDP and related components are revised from the first quarter of 2013 through the first quarter of 2023. GDI and selected income components are revised from the first quarter of 1979 through the first quarter of 2023.

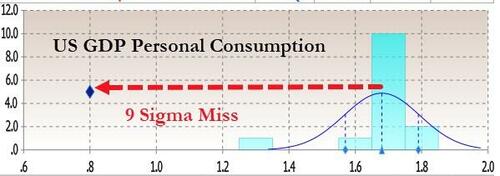

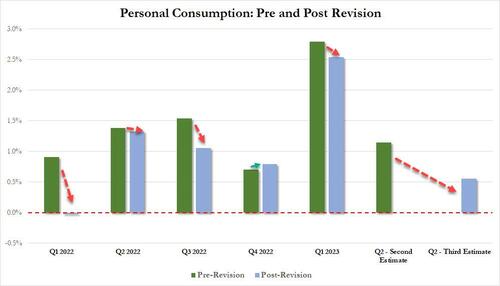

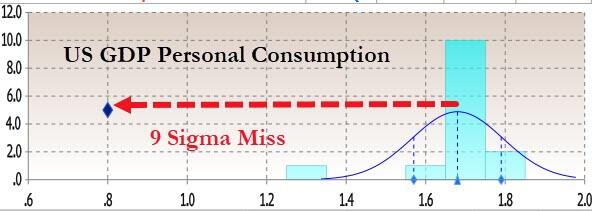

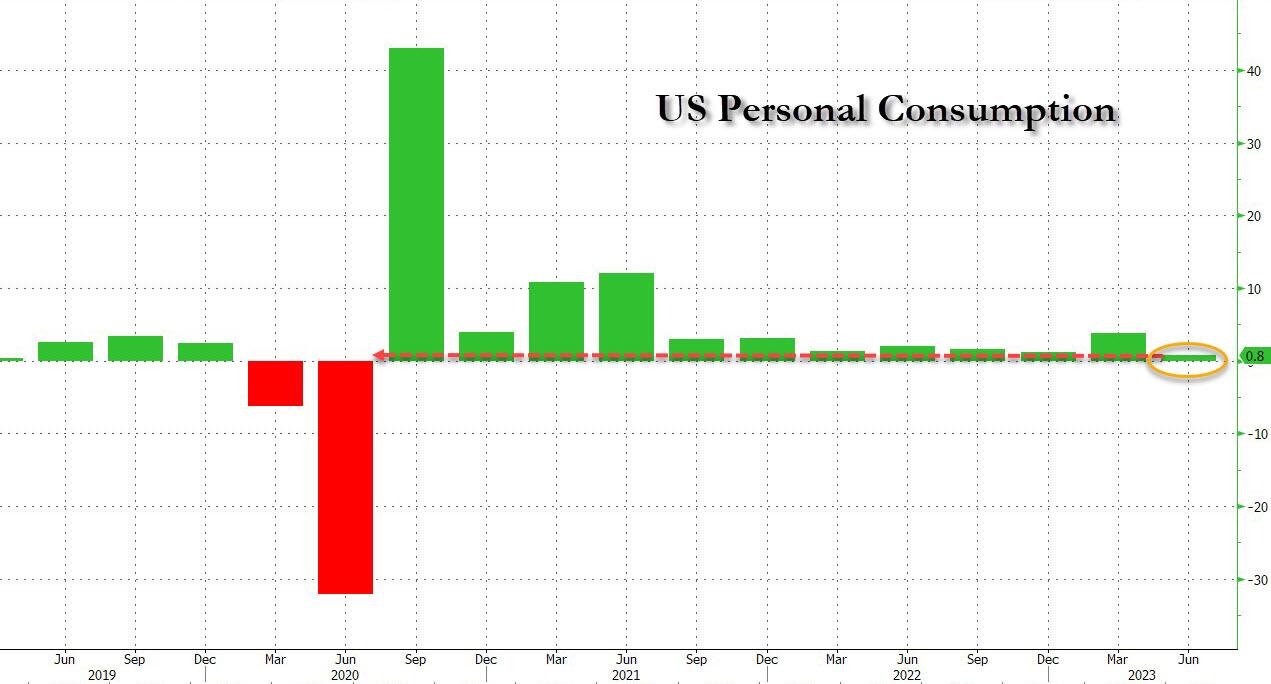

Earlier today we already noted the disaster that was Q2 Personal Consumption: instead of the 1.7% unchanged print from the second estimate of Q2 GDP, the final number was a dire 0.8%, a 9-sigma miss to estimates…

… and the worst quarterly increase since the Covid collapse in Q2 2020.

But what about other historical data? After all today’s revision impacted all data from Q1 2013? Therein, as the bard says, lies the rub.

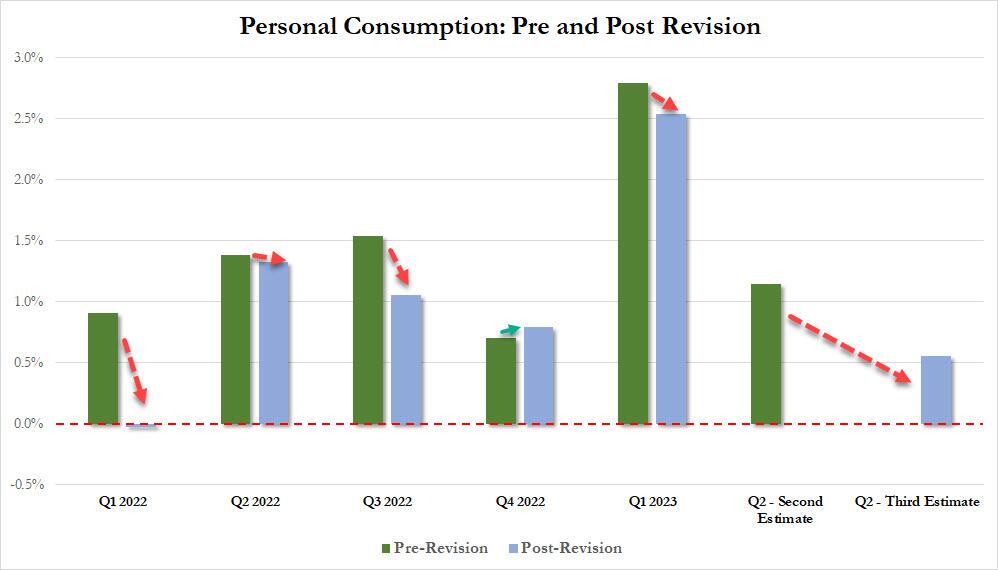

Let’s start with personal consumption, and compare the latest post-revision current data (link) with the most comprehensive pre-revision data as of last month (link). It should come as no surprise to anyone that with the (slight) exception of just Q4 2022, personal consumption in every single quarter since the start of 2022 – when the Fed aggressively started tightening and hiked rates by the most since Volcker – has been revised lower, and in some cases dramatically so.

Bloomberg also picks up on the GDP revision and looking at revisions to the historical data, writes that “the pandemic contraction is seen as being a bit less severe than previously thought: GDP is now reckoned to have dropped at a 28% annual clip in the second quarter of 2020, instead by 29.9%, as the government shut down swathes of the economy to fight the spread of the virus. But the recovery since then has been somewhat slower, according to the update. Growth last year was revised to 1.9% from 2.1%.” And of all GDP components, consumption was the weakest.

So not only was the Fed hiking at a time when personal consumption would grow much less period to period than previously expected, but the US economy was generally weaker than previously expected (as discussed here).

There’s more.

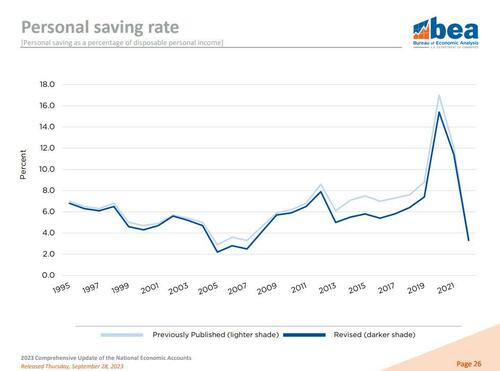

When looking at the composition of the US household’s income statement – the summary of economic accounts – we find just what we had expected: US savings were in fact far lower than previously expected.

… and indeed as the BEA chart below shows, Americans stashed away an average 8.3% of their disposable income annually from 2017 through 2022, down from a previously estimated 9.4%.

The reduction stems from an accounting adjustment that lowered personal income from mutual funds and real estate investment trusts. Additionally, as Bloomberg notes, much of the reduction in personal savings seen in the revised data occurred prior to the pandemic, so its implications for how much extra cash Americans may feel they still have now is not clear cut.

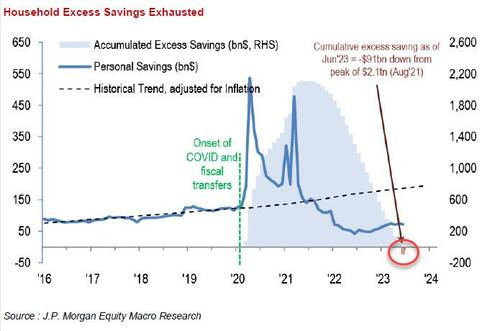

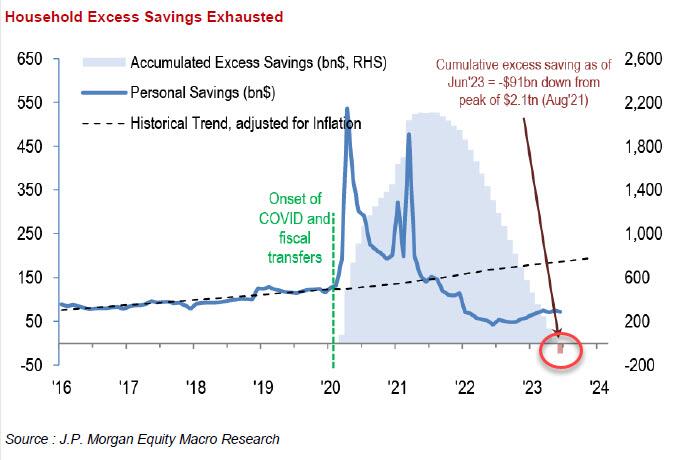

Whatever the reason for the statistical adjustment, however, one can say goodbye to even the faintest speculation that US households have any excess savings left… why they don’t, of course, because even when using the previous methodology which artificially inflated total savings, JPM calculated that excess savings had already run out…

… which means that if Q3 GDP was bad and consumption was “revised” sharply lower (odd how economic data is never revised higher under Joe BIden), Q4 – when savings are virtually non-existant – and where we also get the i) return of student loan payments; ii) the UAW strike; iii) the government shutdown and iv) oil at almost $100 and gasoline at one year highs, is about to fall off a cliff.

Yes, Bidenomics is a form of Brawdo, the economic mutilator!

Wasting away again in Biden’s Mortgage Market! Looking for our lost economy.

Mortgage rates moved to their highest levels in over 20 years as Treasury yields increased late last week. The 30-year fixed mortgage rate increased to 7.41 percent, the highest rate since December 2000, and the 30-year fixed jumbo mortgage rate increased to 7.34 percent, the highest rate in the history of the jumbo rate series dating back to 2011.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 2 percent compared with the previous week. The Refinance Index decreased 1 percent from the previous week and was 21 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 27 percent lower than the same week one year ago.

Biden’s press secretary Karine Jean-Pierre said that Biden was laser focused on reducing inflation. At least he isn’t laser focused on little girls … for the moment. But he still does seem laser focused on providing Ukraine with billions of dollars.

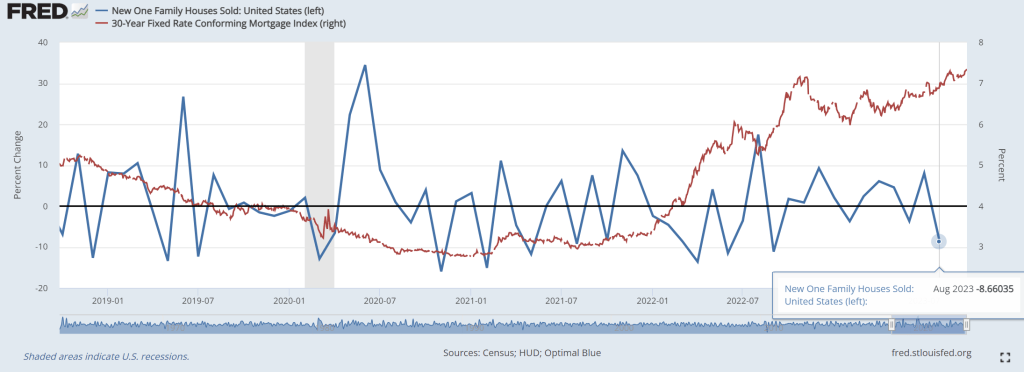

After months of soaring in the face of higher mortgage rates (and higher prices), new home sales hit a wall in August, crashing 8.7% MoM – the biggest drop since Sept 2022 (and four times worse than the -2.2% MoM expected)…

But at least new home sales were up on a YoY basis.

hat is the lowest SAAR since March…

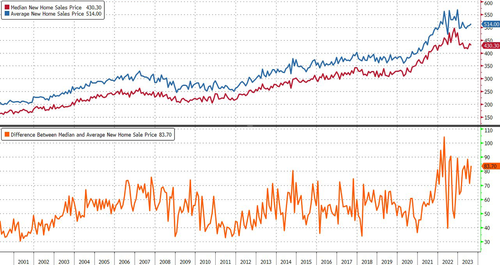

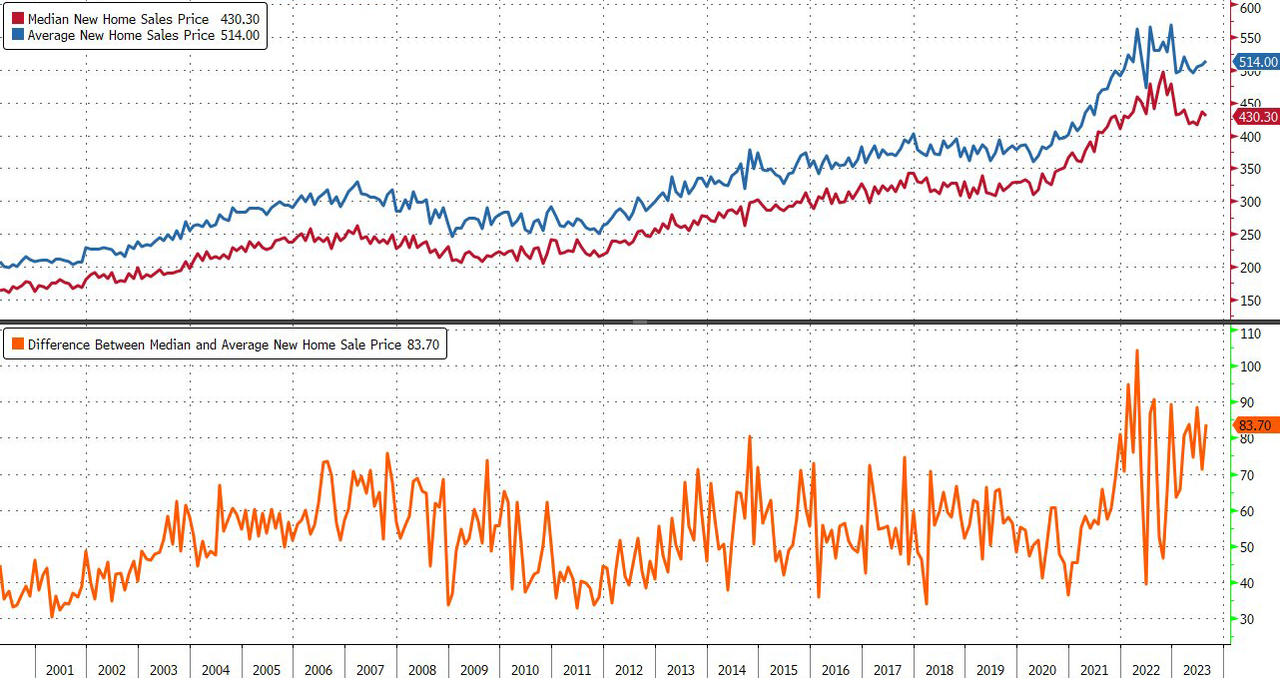

The median sales price of a new home edged lower to $430,300 (average home price rose), according to the Commerce Department’s report.

Despite the decline, that’s still well above pre-pandemic levels.

As a reminder, according to a report released Friday by Redfin Corp, nearly 60,000 deals to purchase homes fell through in August (roughly 16% of homes that went under contract last month, the biggest share of cancellations since October).

“I’ve seen more homebuyers cancel deals in the last six months than I’ve seen at any point during my 24 years of working in real estate,” Jaime Moore, a Redfin agent, said in the report.

“They’re getting cold feet.”

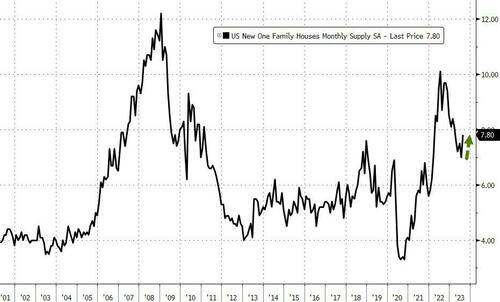

A potential silver lining is the rising in supply (but now much that is driven by a decline in the denominator – homes sold – vs numerator – homes available; is unclear)…

Is the catch-down to reality about to begin?

Source: Bloomberg

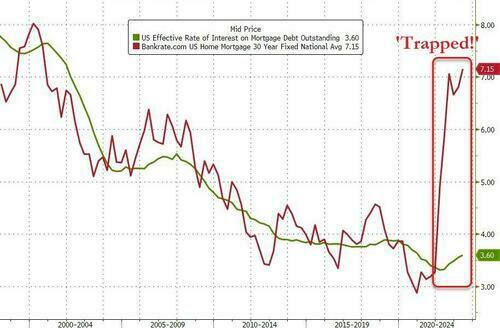

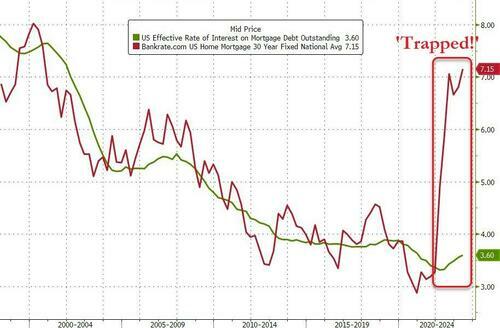

They should, given that homebuilders can’t be filling this gap – between the current 30Y mortgage rate and the effective rates that borrowers are currently paying on their home loans – (i.e. subsidizing new home sales) forever…

Source: Bloomberg

And investors are starting to wake up too…

Is Jay Powell about to get the ‘affordability’ compression he was hoping for?

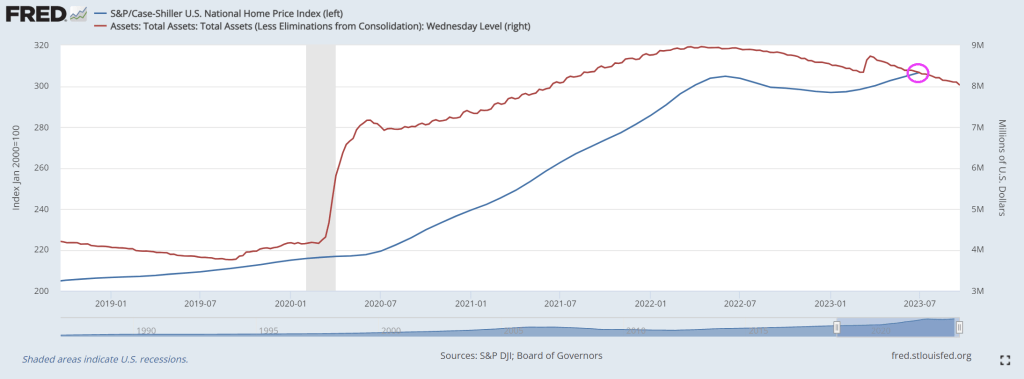

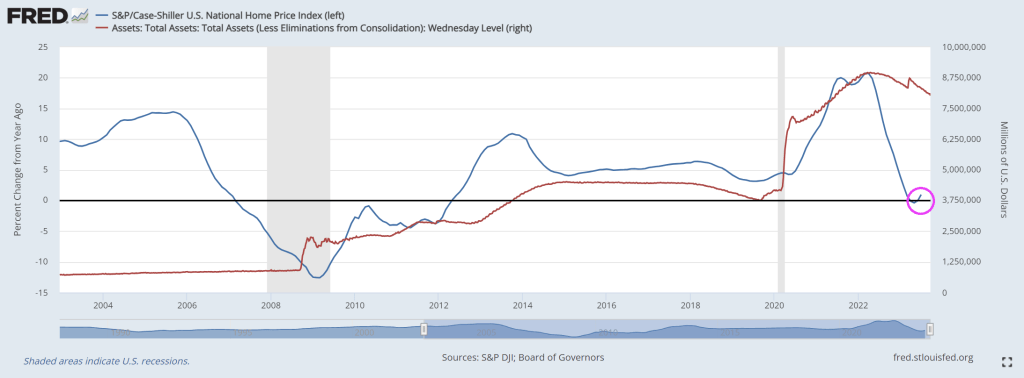

Thanks to rampant Federal spending and overstimulus by The Federal Reserve, US housing prices are simply unaffordable for many. Particularly since the Covid epidemic (Wuhan China Flu).

Yes, home prices grew in July despite rising mortgage rates. As CS Lewis wrote “That Hideous Strength” but this is about how The Fed doesn’t understand what they have done.

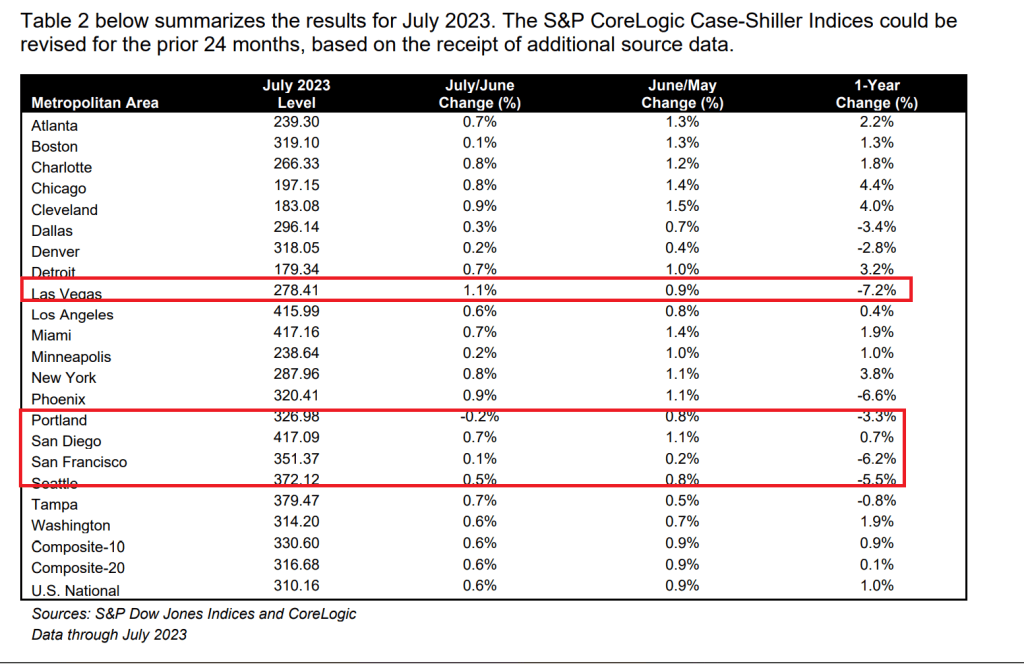

At the metro level, Las Vegas leads in YoY price declines at -7.2%. In a close second is San Francisco at -6.2%. Portland and Seattle also declined.

Here is Screamin’ Joe Biden. You know Biden is lying when he gets angry.

Donald Trump was famous for his “Make America Great Again!” campaign. Joe Biden seems to want to make America LAST again (MALA).

A newly aired “60 Minutes” segment entitled The unexpected way American tax dollars are being used in Ukraine has uncovered that the US government is paying the salaries of some 57,000 Ukrainian civic services personnel.

The report details the various ways non-military aid is being spent at a moment GOP Congressional leaders are intensely debating whether to move forward with a proposed defense budget that includes Biden’s push for $24 billion more in military assistance for Kiev.

“The U.S. has spent just over $43 billion on military aid to Ukraine since Russia invaded. That’s equivalent to about 5% of the American defense budget. European countries combined have contributed around $30 billion,” the 60 Minutes report narrates.

American taxpayers are financing more than just weapons. We discovered the U.S. government’s buying seeds and fertilizer for Ukrainian farmers… and covering the salaries of Ukraine’s first responders – all 57,000 of them.

That includes the team that trains this rescue dog – named Joy – to comb through the wreckage of Russian strikes looking for survivors.

Political commentator Collin Rugg has noted in relation to the potential government shutdown looming for Oct. 1st: “Yes, your tax dollars will be used to fund Ukrainian salaries while American citizens are forced to wait for their pay while the government remains closed,” he said on X.

Rugg is referencing the fact that the Biden administration and Pentagon have declared that Ukraine aid will remain exempt from any potential government shutdown. This means Ukrainian salaries will still be paid, even while federal employees aren’t, in the event of a shutdown.

Here’s more from the 60 Minutes video, featuring a Ukrainian woman “thanking” US taxpayers for footing the bill for Ukrainian employees, thanks to USAID funding:

Tatiana Abramova: Especially in the condition of war, we have to work. We have to pay taxes, we have to pay wage– salary to our employees. We have to work, don’t stop.

Holly Williams: Why does that help Ukraine win the war?

Tatiana Abramova: Because economy is the foundation of everything.

American officials from USAID – the agency in charge of international development – helped Abramova find new customers overseas. In the midst of war, her company is supporting over 70 families.

Meanwhile, a fresh Newsweek headline: US Will Pay Salaries to Thousands of Ukrainians During Government Shutdown…

“US taxpayers will pay the salaries of thousands of Ukrainians, even as the country faces a government shutdown at the end of September.”

But as noted above, this is more like tens of thousands of Ukrainian salaries.

“A federal government shut down will effectively begin on October 1 if Congress isn’t able to pass a funding plan that Biden signs into law,” Newsweek underscores. “If that happens, federal agencies have to stop all nonessential work and will not send paychecks for as long as the shutdown lasts.”

Appropriately, the 60 Minutes episode invoked memory of the late John McCain…

In total, America’s pumped nearly $25 billion of non-military aid into Ukraine’s economy since the invasion began – and you can see it working at the bustling farmers market on John McCain Street in central Kyiv.

The late senator is revered in Ukraine because he pushed the U.S. government to start sending arms to the country… back in 2014.

Here’s how 60 Minutes presents bipartisan support for Biden’s blank check for Ukraine:

While in Kyiv, we learned that three of McCain’s former colleagues were also in town: Democratic Sens. Elizabeth Warren and Richard Blumenthal and Republican Sen. Lindsey Graham. They don’t normally agree on much – together, though, they’re some of the staunchest supporters of U.S. funding for Ukraine’s resistance.

Indeed Zelensky himself while meeting with US Senators in Washington last week said something similar – that without continuing American funds, the war effort is doomed. He urged Congress to keep the billions in aid flowing, and sought to present that Moscow will one day expand aggression beyond just Ukraine.

* * *

Meanwhile, the “aid from the heart of every ordinary American person” will continue (whether those ordinary Americans like or not)…

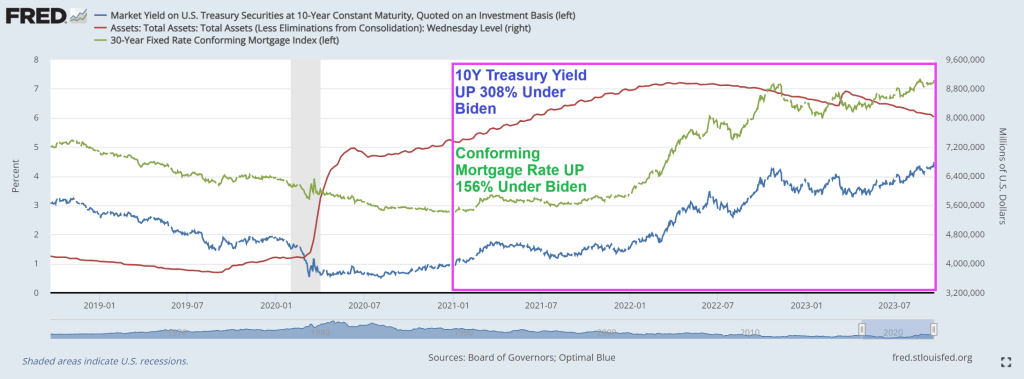

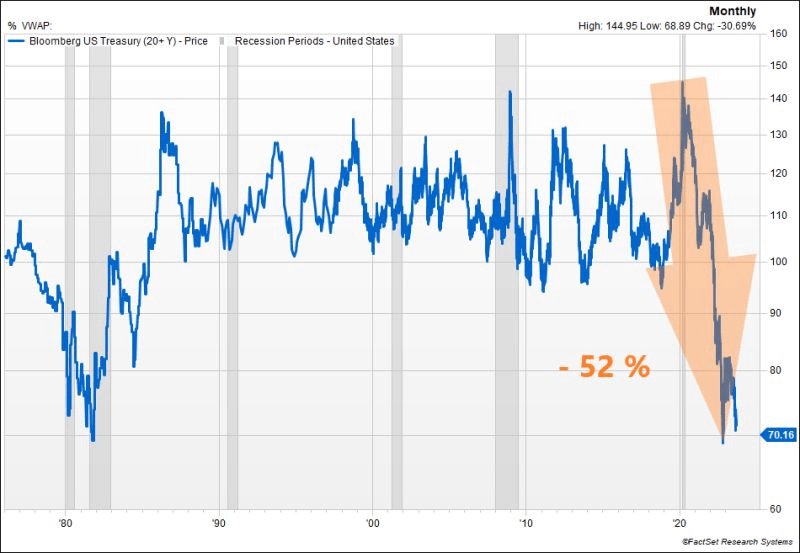

Alarm! US 10-year Treasury yields are soaring along with mortgage rates.

The US Treasury market is witnessing another significant selloff, pushing the 10y UST yield close to the 4.50% mark. The surge in real rates is remarkable, reaching 2.12% for the 10y, a level not seen since 08’. While this might appear attractive in real terms compared to historical benchmarks, could we be on the brink of a third consecutive year of negative performance for US Treasuries? To put this into perspective, such a scenario has never occurred in history.

The conforming mortgage rate is at 7.3%, up 156% under since Biden’s coronation as El Presidente of the United Banana Republics of America. Where political opponents are indicted prior to elections.

In Biden’s Banana Republic economy, the US Treasury 10y-2y yield curve remains inverted.

And then we have Mish’s chart on debt as a percentage of GDP from CBO. Remember, we used to worry about the US breaking the 80% debt to GDP level. It is now projected to be 181%. Wow.

The most recent report on US exisiting home sales showed that sales decreased in 17 of the last 19 months as The Fed tightens monetary policy to combat inflation caused by … 1) The Fed and 2) Bidenomics spending on green energy.

The US housing market will be “back in black” once Biden and Congress stop their reckless spending and borrowing. Biden has added $5,352,202 to the national debt since being selected (not by me!). That is a 19% increase in The Federal debt in just 33 months!

Not to mention the ludicrous $194 TRILLION in unfunded liabilities that the geezers in the Biden Administration (Biden is 80 and slipping into dementia) and the Geriatric wing of Congress (the US Senate) is home to fossils like Mitch McConnell (not looking well) and Diane Feinstein (90 and looking poorly). I didn’t forget about Nancy Pelosi (Communist-California) who is 83 and running for re-election. Younger doesn’t necessarily mean better since Pelosi’s nephew California governor Gavin Newsom is 55 years old and helped destroy California’s economy. Of course, the DNC will probably selected Newsom to replace scandal-ridden Biden as the Democrat in order to finish the job Obama started.

Existing-home sales slipped again in August as rising mortgage rates make housing prices the least affordable ever. Despite denials in many corners, a crash is underway.

Existing-home sales retreated 0.7% in August to a seasonally adjusted annual rate of 4.04 million.

Sales dropped 15.3% from one year ago.

The median existing-home sales price climbed 3.9% from one year ago to $407,100, an increase of 3.9% from August 2022 ($391,700). It’s the third consecutive month the median sales price surpassed $400,000.

The inventory of unsold existing homes dipped 0.9% from the prior month to 1.1 million at the end of August, or the equivalent of 3.3 months’ supply at the current monthly sales pace.

First-time buyers were responsible for 29% of sales in August, down from 30% in July and identical to August 2022.

All-cash sales accounted for 27% of transactions in August, up from 26% in July and 24% in August 2022.

And mortgage rates are now up to 23 year highs!

If Biden bows out and Newsom runs for President … and loses, Newsom always has a career in Hollywood in vampire movies. “I will suck your (economic) blood!” – Count Newsom.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.