One of the great ironies of the Sam Bankman-Fried debacle is that while SBF was a generous donor to Democrats (and a few RINOs) and President Biden, it was Biden’s green energy policies that were part of the nail in SBF’s crypto empire. As inflation exploded upon Biden taking office (and massive overspending by Congress), The Federal Reserve jumped in to cool inflation leading to the downfall of cryptos in terms of price.

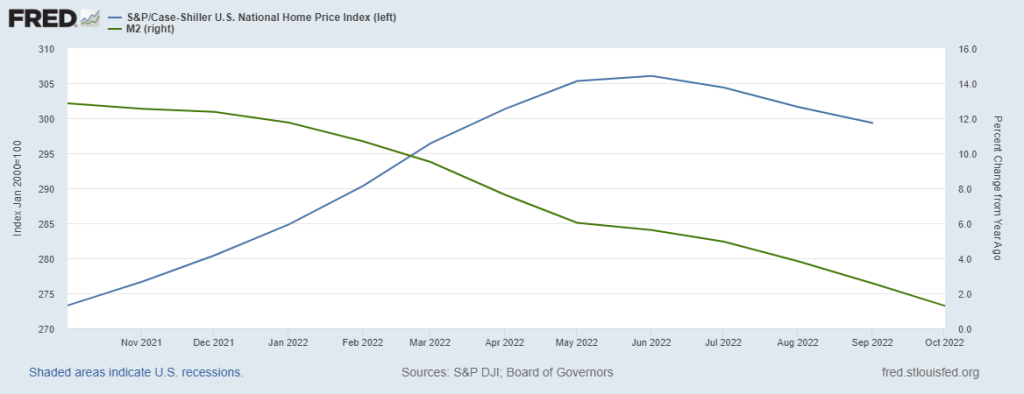

M2 Money YoY (green line) shows the massive growth money with the Covid economic shutdowns in 2020. Cryptos skyrocketed after that much money was printed by The Fed. Cryptos fell shortly after peaking in April/May 2021, then peaked again in a horrific display of asset volatility in October/November 2021.

What happened in late 2021 to crush cryptos? Ah, expectations of Fed rate increases (red line) started to soar meaning the punchbowl for cryptos was being taken away. The Fed giveth and The Fed taketh away.

The risk management question is … how did SBF and Alameda Research’s Caroline Ellison didn’t notice the relationshop between crypto prices and changing Federal Reserve monetary policy? Even worse, why didn’t investors ask questions??

Take a gander at Bitcoin relative to US diesel fuel prices (orange line) and The Fed’s inflation counterattack (red line). Sam and Sweet Caroline (who was seen walking free in NYC) must not have been monitoring how rapidly rising diesel prices would permeate the entire economy in terms of price increases. M2 Money YoY (green line) has been declining as the expectations of Fed rate tightening (red line) has increased.

SBF donated a huge amount to the midterm elections, the party that went along with Biden’s war on fossil fuels. Then inflation ensued as energy and food prices skyrocketed, leading The Federal Reserve to fight inflation by removing the monetary punchbowl. So, in a sense, SBF donations led to his own collapse.

Apparently, SBF, Caroline Ellison and the other FTXers were engaged in orgies and not paying attention to the impact of inflation and Fed policies on cryptos.

Lastly, how did Gary Genslar and the SEC not see any of this? In the same way that Fed Chair Ben Bernanke didn’t see the financial crisis as it was rapidly unfolding: eyes wide shut.

I read that Nicole Kidman underwent psychiatric treatment after filming “Eyes Wide Shut.” I saw it and was bored out of my mind.

You must be logged in to post a comment.