And with it, ISM Manufacturing Report for December is showing weakness. New orders (orange line) is down to 45.2 (below 50 is contraction) and the prices paid is down to 39.4 (white line). All this is happening as The Fed raises its target rate (yellow line) and removes monetary stimulus (green line).

This gives us “The Devil’s Tower” looking economic spike after massive Covid-related monetary stimulus and Federal government repeated stimulus.

Speaking of Already Gone, look at the US Treasury 10Y-2Y yield curve with slowing M2 Money growth. Yield curve inversion is more about vanishing M2 Money growth than it is a forecast of recession.

The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

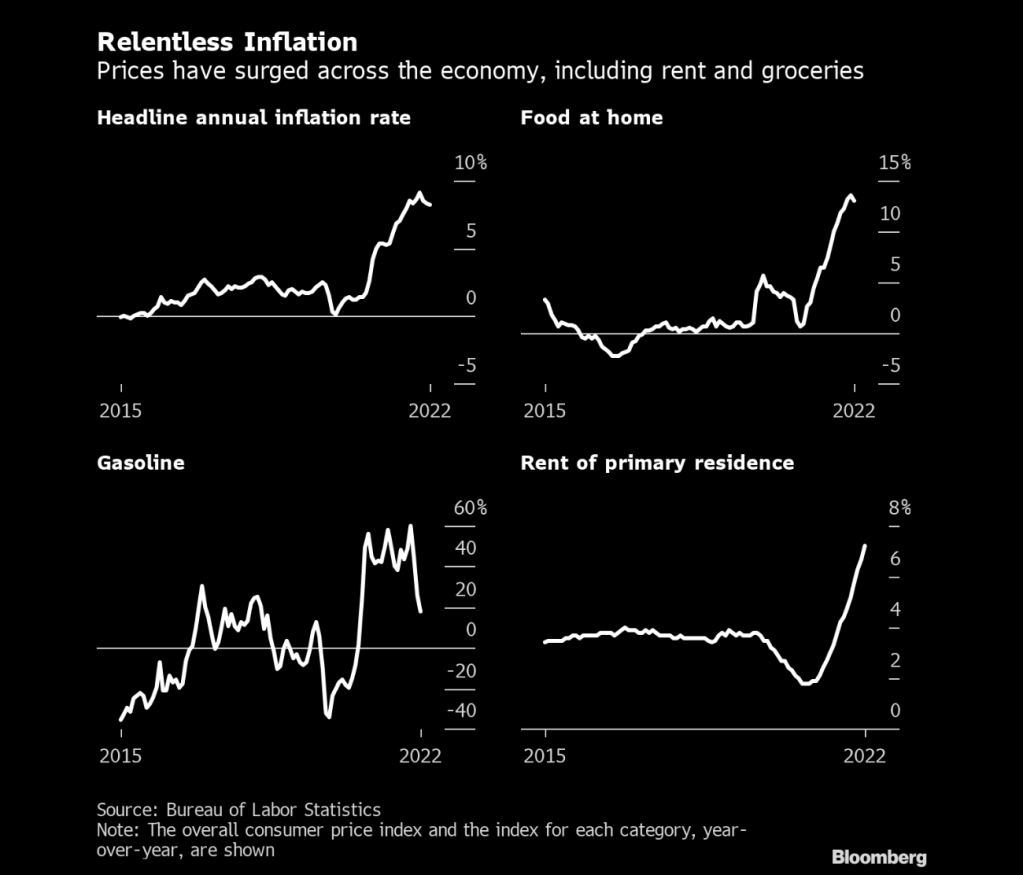

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

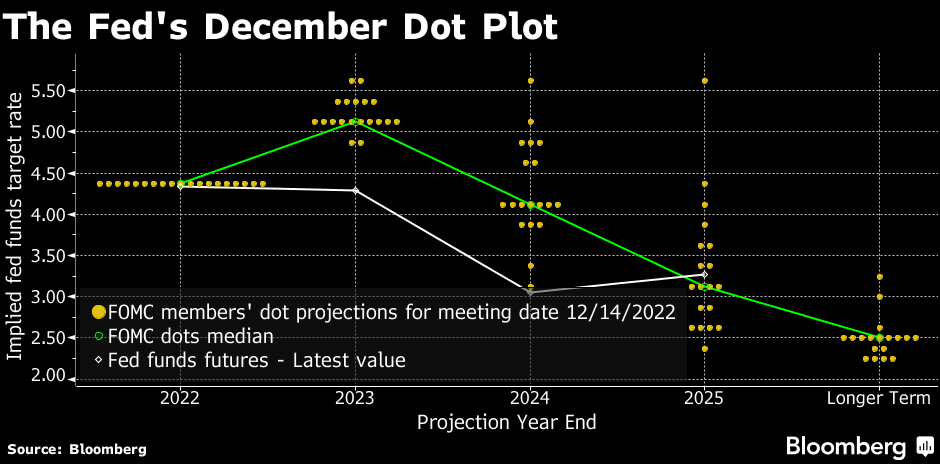

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

Here is a chart (courtesy of Zero Hedge) showing reported payrolls and REVISED payrolls. Somehow, I don’t think Jean Pierre (Biden’s spokesperson, not the French chef) will be touting “Unlike Trump, our administration barely added any jobs in March, April, May and June 2022.

How will this revelation influence the Fed’s open market committee (FOMC) going forward knowing that the Biden Administrations job creation claims are wildly overstated?

Perhaps it doesn’t matter since Bernanke, Yellen and Powell don’t follow any rules (like the Taylor Rule), but generally with job creation almost nonexistant in March through June of 2022, The Fed should be cutting rates like mad. But wait! Can they with significant inflation?

The good news is that inflation is coming off its peak, but will take a while to get to The Fed’s 2% target. Hence The Fed may raise their target rate since they cannot achieve it will energy price up substantially since Biden became President.

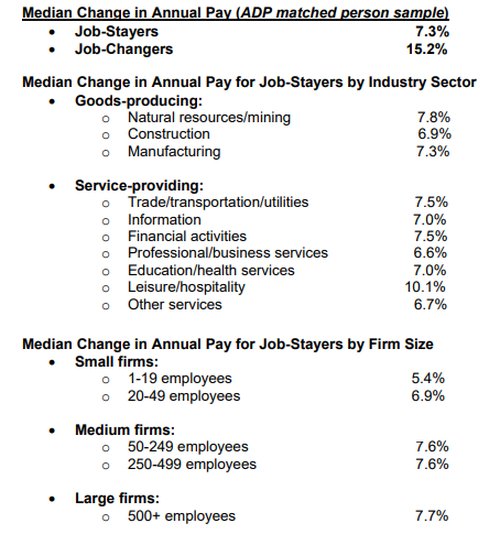

Unlike yesterday’s ADP jobs report (only 127k jobs added), the official Federal government report shows 263k jobs added. I like the ADP report, but The Fed pays attention to the BLS numbers. So, …

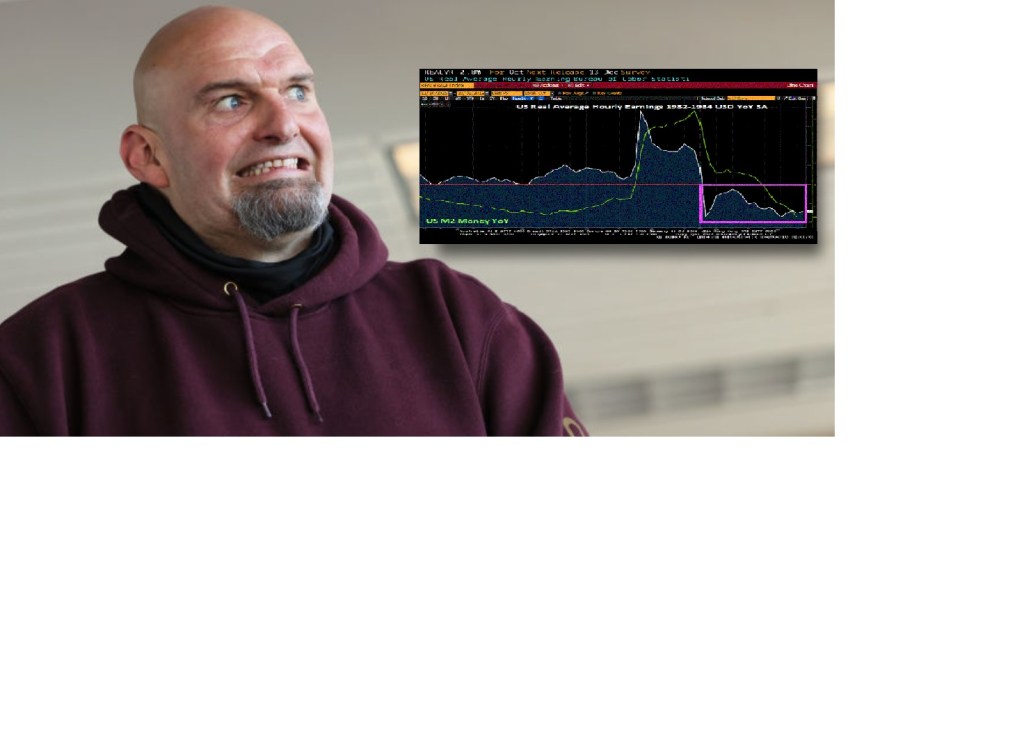

U.S. employers added 263,000 jobs in November, and the nation’s unemployment rate stayed the same at 3.7 percent, according to data released Friday by the Labor Department. Meanwhile, average hourly pay for workers rose 5.1 percent from a year earlier, to $32.82 from $31.23. But the US headline inflation rate at the last reading was 7.7% YoY that equates to -2.2% REAL Average Hourly Earnings YoY.

Mortgage rates fell to 6.51 yesterday, but expectations of Fed rate hikes (WIRP) and the 10-year Treasury yield are up today. In fact, the 10-year US Treasury yield is up 10 basis points this morning. This will likely translate to higher mortgage rate today.

Inflation is still the humming dragon crushhing the US middle class and at last report stood at 7.7% YoY. Average hourly earnings YoY rose to 5.1% in November, which is good. But inflation takes a huge bite out that number, resulting in -2.2% YoY REAL average hourly earnings.

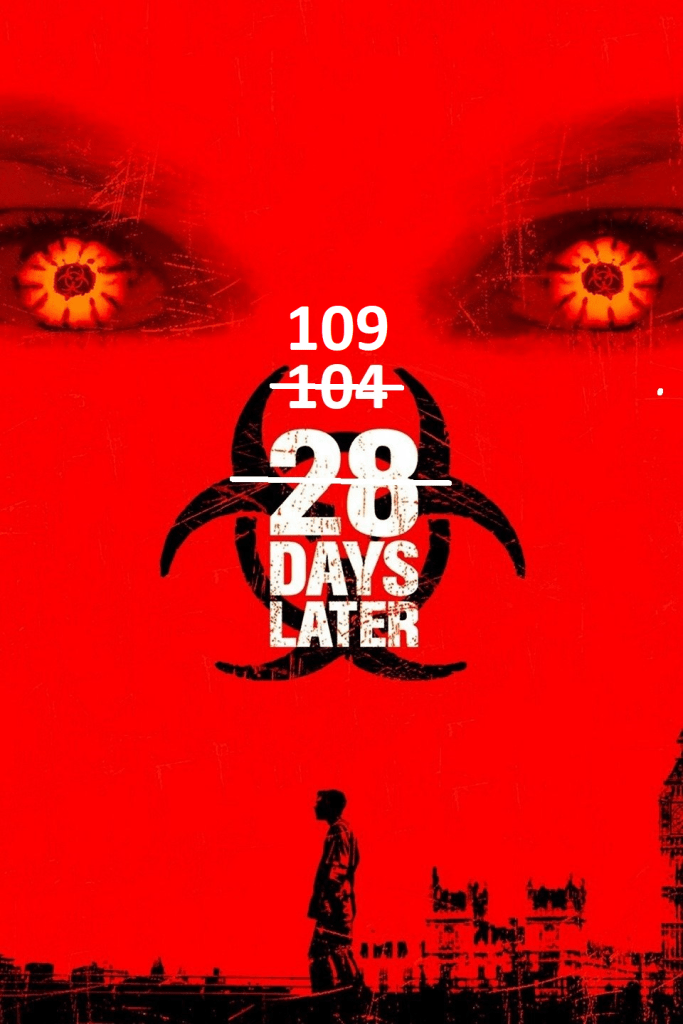

And the US 10Y-2Y Treasury yield curve has been inverted for 109 straight days.

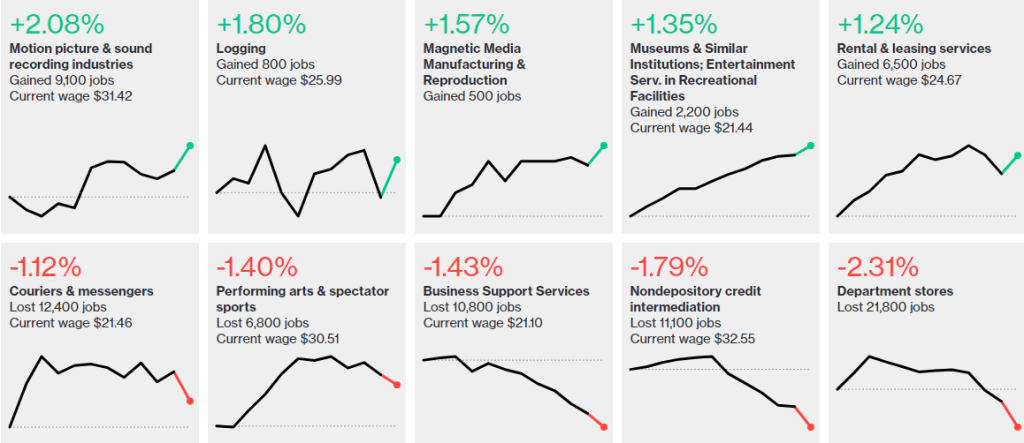

Here is the rest of the jobs report.

The biggest gainer? Motion picture and sound recording industries followed by logging (with rising energy prices, people have to heat their homes somehow).

As soon as Bidenflation started soaring with his war on fossil fuels and manic Federal spending, we saw The Federal Reserve starting to remove the excessive monetary stimulus, but Congress didn’t cancel its spending spree.

We ADP jobs report yesterday was ugly (+127k jobs added after +239k jobs added in October). Now we have the Challenger, Gray and Christmas jobs report for Novemeber … and it is terrible. An increase of 416.5% in job cuts.

Today, the US Personal Consumption Expenditures data was released. It shows that the CORE PCE YoY fell to a still high 5%.

If The Fed actually followed any rules other than CNTRL PRINT, we can see that with Core PCE YoY of 5% (or 4.98% to be exact), the Taylor Rule estimate for where The Fed Funds Target rate should be is … 9.78%

Yes, The US Treasury 10Y-2Y yield curve remains inverted, for the 104th straight day. And Bankrate’s 30-year mortgage rate has dropped -57 basis points since November 3, 2022.

This comes after a gruesome Pending Home Sales and mortgage applications reports today.

The US housing market is slowing, to be sure. Yesterday’s existing home sales (EHS) report revealed that US EHS were down -28.43% YoY and the median price of EHS slowed to 6.6% YoY.

But that is just the surface of the EHS report for October. Once I removed inflation (CPI YoY) from the numbers, we are left with REAL median price of EHS growth of -1.17% and REAL average hourly earnings YoY of -3.0% YoY. The REAL 30-year mortgage rate is -5.25%. That reveals how horrible inflation is in the US.

It is important to note that EHS numbers are lower in October than they were before Covid stimulypto (my name for the massive spending spree by Congress and massive injection of monetary stimulus by The Fed. Even the REAL 30-year mortgage rate is negative at -0.5254%.

The inflation numbers are out for October and they still stink (headline inflation still sizzling at 7.7% YoY).

But the number that really irks me is … REAL average hourly earnings growth is at a horrifying -2.8% YoY because of Biden’s terrible policies (aka, Bidenflation).

Real average hourly earnings growth YoY has been negative since March 2021. That is 19 straight months of negative earnings growth under Biden/Pelosi/Schumer’s reign of error.

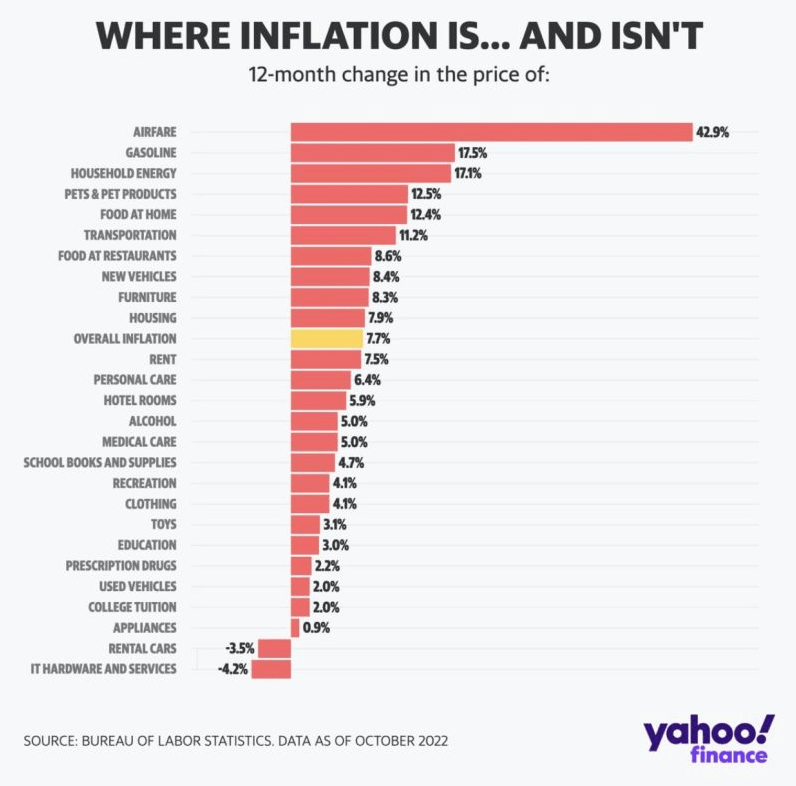

Overall, airfares are leading followed by gasoline and household energy.

So, Pennsylvania elects this guy to perpetuate Biden/Pelosi/Schumer’s awful policies?

The US midterm elections are Tuesday. I was denied an absentee ballot for some reason, but I will get my disabled body over to the local precinct to cast my ballot.

Fortunately for Democrats, the next inflation report is not due out until November 10th. Because the forecast for the next inflation report is ugly.

Headline CPI YoY = 7.9%

Core CPI YoY = 6.5%

These numbers are slightly lower than the last inflation report, but Americans are still suffering mightily under Biden’s Reign of Error.

Diesel fuel prices, the lifeline of the food industry, is up 102% under Biden’s mandates with the inventory of diesel fuel down 36%.

Inflation is relentless like Jason from Halloween.

You must be logged in to post a comment.