Private payrolls added 233k jobs in October, which is a -27% decline from September’s revised private payroll figures.

The good news? Average hourly earnings growth is still positive, but fell to 3.7% YoY. But with inflation raging at 8.2% YoY, workers are getting clobbered by inflation.

Here is the rest of the story.

The Fed is now green-lighted to raise rates even higher.

Biden’s campaign promise was to unite rather than divide. But Biden has morphed into Gustaf Holst’s, Mars – Bringer of War! Both domestically and in the Ukraine.

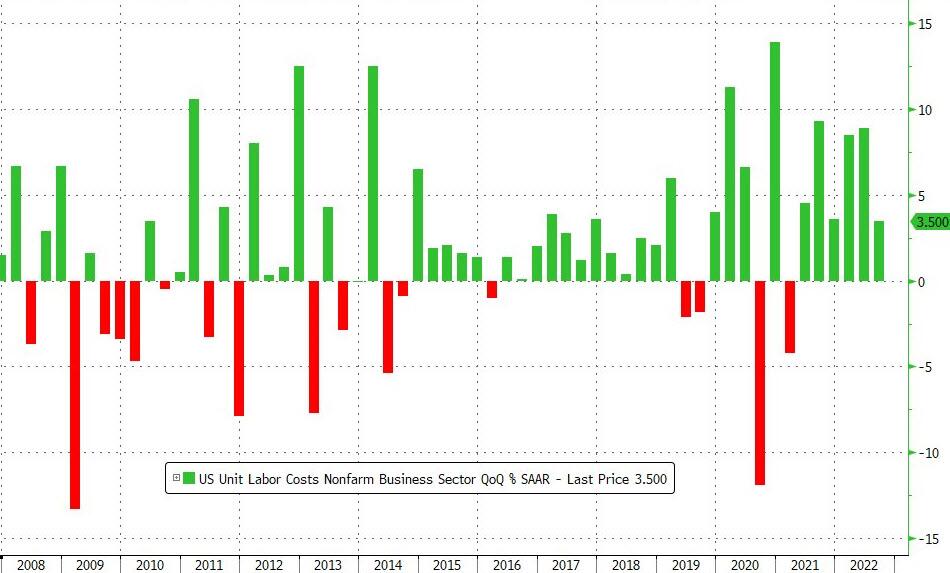

On a YoY basis, US Productivity is down for the 3rd straight quarter (and 4th quarter of the last 5).

On the mirror image of productivity, unit labor costs rose 3.5% QoQ (a notable slowing from the 8.9% QoQ growth in Q2). This was the 6th quarter in a row of rising unit labor costs (but was less than the +4.0% QoQ expected)…

However, on a YoY basis, that is the fastest growth since Q3 1982.

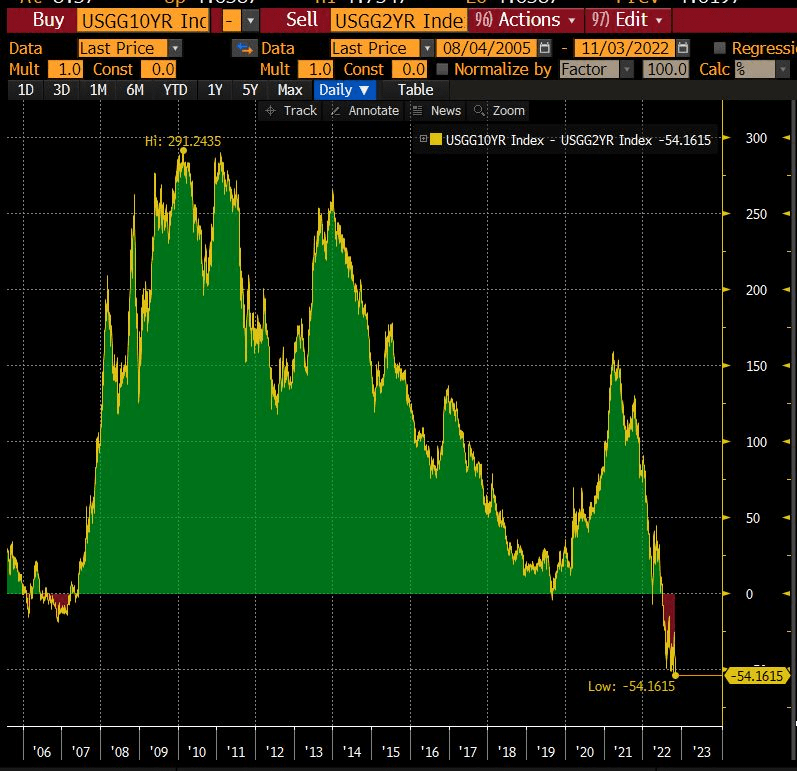

Yikes! The 2s10s Yield Curve Inversion Is the worst since the 1980s.

One reason is diesel fuel prices are up 102% under Biden’s Reign of Error. While inventory of diesel fuel down -37%. Meanwhile core inflation is up from a measly 1.3% to a whopping 6.6% at the latest inflation report.

Introducing Biden’s Thanksgiving dinner … in a can to cope with rising prices.

Just kidding. This is too clever for the clueless Biden Administration. But Karine Jean-Pierre might get as confused as Joe Biden and repeat it as one of the ways that The Biden Administration is helping consumers.

One of my friends on Wall Street wrote my yesterday claiming “The 10-year Treasury yield is set to crash. Brace for impact!” Then I logged into Bloomberg this AM and saw the 10-year Treasury yield up almost 10 basis points (although it is down -2 BPS at 10:20am). Did markets not read his comments?? Maybe they did!

Well, The Fed is doing the Tighten Up. That is, The Fed is FINALLY removing their excessive monetary stimulus left over from the Bernanke Blowout (2008 adopting Japan’s print ’till you drop model).

But as The Fed removes their monetary stimulus (rate increases), we are seeing negative effects in the housing market. I call this chart “The X Factor.”

The US Treasury 10-year yield is up to 4.3% this morning, a far cry from 1.804% when Biden was crowned as President on January 20, 2021. The 30-year mortgage rate is up from 3.67% on Coronation Day to 7.32% yesterday, an increase of … 100% (that is, the 30-year mortgage rate has doubled under Biden). At the same time, Existing Home Sales YoY have gone from -2.41% in January 2021 to -23.79% in September 2022. THAT is a HUGE decline!

University of Michigan’s consumer sentiment for housing for 77 in January 2021 to 39 in November 2022. That is a -49% decline in consumer confidence. Also a big decline.

But going back to my pal’s email, he also said that The Fed is unwinding its balance sheet at a dangerously rapid rate (orange line). Relative to just increasing it, I would agree with him. But The Fed’s balance sheet is barely declining to my eyes. The troubling thing for housing is that inflation is so hot that REAL average hourly earnings YoY (yellow line) has fallen from +0.24% growth YoY on January 25, 2021 to a horrific -2.80% YoY rate in September 2022.

Bill’s point to me is that lending is still hot (at least commercial and industrial lending or C&I) while The Fed’s balance sheet remains in force (green line).

The Fed has a lot more work to do if they want to cool the commercial lending market. They have successfully slowed down the residential mortgage market.

Joe Biden reminds me of Dennis Reynolds from “Its Always Sunny In Philadelphia.” And his D.E.N.N.I.S System. But Biden’s System is blatant politics. With the midterm elections in November and Democrats looking a bit behind, Biden is pulling out the political guns by 1) ramping up student loan forgiveness … again and 2) releasing 10-15 million MORE barrels from the Strategic Petroleum Reserve to lower gasoline prices. Particularly after his failed attempts to get the Saudis to pump more oil (too bad Biden put the kabash on US energy exploration and cancelled the Keystone pipeline).

Having said that, we can see that BEFORE the latest SPR order, the US Strategic Petroleum Reserve, meant to cope with national emergencies like … Russia dropping a nuke on the US, has declined -36% under Nuclear Joe.

At the same time, regular gasoline prices are UP 62% under Biden and the all-important diesel fuel prices are UP 101.4% under Biden.

Of course, expect The B.I.D.E.N System to do everything in its power to destroy the economy if Republicans win the midterms. Including no more SPR release.

I love to teach, but my students at Chicago, Ohio State and George Mason would fall asleep when I would discuss repurchase and reverse repurchase agreements (or REPOs and Reverse REPOs). But repos and reverse repos are a critical part of the banking system.

In short, the Repo market is a window into what’s going on behind the scenes.

As Bidenflation soars, and The Fed counterattacks, we see Fed’s repo market remains elevated. Note that The Fed’s balance sheet (orange line) is only slowly being reduced.

Right now, the risk lurking in the shadows is Balance Sheet Runoff. The Fed, the markets, the regulators, have limited experience with the Fed shrinking the balance sheet. Bottom line: there’s a risk that Balance Sheet Runoff will breaking something.

The global stock market is up again today, despite Fed tightening and a war in Ukraine. The Dow is up 1.38% and the S&P 500 is up 1.75%.

Likely cause? Rumors that The Fed and other global central banks will pivot sooner than later.

It is likely that The Fed will pivot to prevent a crash and the stock market in pricing in that pivot.

Bernanke, Yellen and Powell are NOT Paul Volcker. In fact, I am coining a new nickname for Fed Chair Jerome Powell: Pivot Powell.

The US Empire State Manufacturing Survey General Business Conditions SA index fell to -9.1 in October, continuing a downward trend along with the downward trend in Fed M2 Money stock growth.

And the global sovereign debt market is showing fear as 10-year sovereign yields drop -10 basis points. The UK 10-year is down -36.8 bps! The US is down only -6.6 bps this morning.

The US CPI for electricity is up 24% under Nuclear Joe as The Fed continues to leave their balance sheet relatively untouched.

You might have to bail on the stock market to stay warm this winter, but it is a shame that the S&P 500 index is down -25.3% in 2022 as The Fed counterattacks Bidenflation.

The US 30yr Mortgage rate just hit a new high since 2000 as The Federal Reserve counterattacks the highest core inflation rate (6.60%) since 1982.

According to the Taylor Rule (which The Fed has chosen to ignore), a 6.60% core inflation rate implied a Fed target rate of 12.40%. Not likely since Fed Funds Futures data points to …

A maximum target rate of 4.963% at the May 2023 FOMC meeting, significantly lower than the needed rate of 12.40%. The Fed is like the world’s worst bar bouncer.

Rather than accepting blame for the horrific inflation rate crushing the American middle class and low wage workers, Biden is twisting the night away.

{kind=link}

{kind=link}

You must be logged in to post a comment.