The University of Michigan’s consumer sentiment index for housing for October just fell to its lowest level since 1992 as The Fed counterattacks against Bidenflation, causing mortgage interest rates to rise.

Of course, despite slowing home price growth, expensive home prices are really hurting along with expensive rents. But how sustainable are high home prices when REAL average hourly earnings growth is negative??

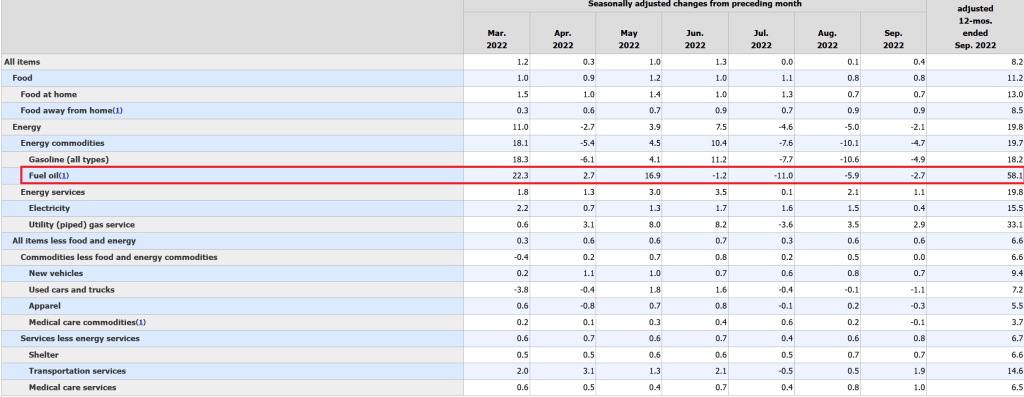

To begin with, headline inflation remains high at 8.2% YoY while CORE inflation (headline less food and energy) rose to 6.6% YoY.

Meanwhile, REAL average weekly earnings growth YoY further declined to -3.8% YoY.

On the bond front, the Bank of America ICE bond volatility index rose to Great Recession/banking crisis levels (also achieved during the Covid government shutdowns).

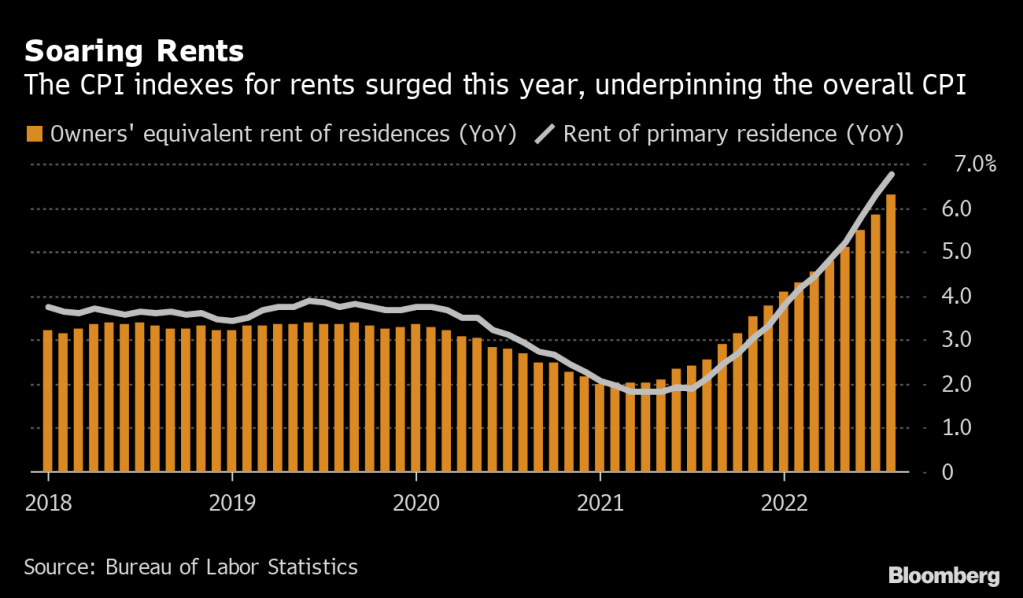

But back to the low-ball BLS inflation data. The biggest gain in price is … fuel oil at 33.1% YoY. Food at home rose 13.0% while gasoline rose 18.2%. Rent, according to the BLS, rose 6.6%.

Biden has probably been told by Ron Klain and Susan Rice that this is a good report.

The US Producer Price Index (Final Demand) printed at a higher than expected 8.5% YoY, throwing cold water on the notion that inflation is “transitory.”

A key US inflation measure due Thursday is set to return to a four-decade high, underscoring broad and elevated price pressures that are pushing the Federal Reserve toward yet another large interest-rate hike next month.

The so-called core consumer price index that excludes food and energy is projected to rise 0.4% in September from the prior month and 6.5% from a year earlier, matching the rate seen in March that was the highest since 1982.

The overall CPI, however, is expected to decelerate to a still-rapid 8.1% annual pace, restrained by a decline in gasoline prices, based on the median estimate.

I feel sorry (sort of) for people like White House Press Secretary Karine Jean-Pierre who has to read ridiculous scripts in defense of awful Federal policies. For example, yesterday she touted Biden’s “accomplishments” of rising real disposable US income and declining gasoline prices. What? Doesn’t she read Confounded Interest?? /sarc

First, REAL disposable personal income growth for the US is NEGATIVE and has been since Biden and Congress embarked on their green energy crusade driving US inflation to its highest level in 40 years. Not exactly a great sales point for the midyear elections.

If we look at REAL average hourly earnings growth, a similar measure, we see that it is negative also. So, what on earth is Jean-Pierre talking about?

She also mentioned that gasoline prices are falling. Except that they are rising again. Apparently her talking points were from September.

Then we have diesel fuel prices, the backbone of the shipping industry, rising like crazy as Biden drains the strategic petroleum reserve.

Meanwhile, The Federal Reserve is tightening their uber-loose monetary policies (thanks Bernanke, Yellen and Powell). Will The Fed pivot to help with the midterm elections OR will The Fed keep trying to extinguish inflation by raising rates and withdrawing Fed monetary stimulus?

Inflation is a multi-headed hydra (from Greek Mythology). It is composed of 1) monetary stimulus (that The Fed is slowly withdrawing), 2) massive, reckless Federal spending and 3) Biden’s anti-fossil fuel mandates. So, when the inflation numbers are out later this week, it will be fun to dissect the damage being done to the US economy and middle-class/low-wage workers.

Take Los Angeles, for example. The life blood of the shipping industry, diesel fuel, is UP 176% under Biden, despite declining for a short period of time. And the DOE Strategic Petroleum Reserve is DOWN -34.7% under Biden.

Here is a photo of Jerome Powell (Fed Chair) trying to fight the inflation hydra. Unfortunately, one of the inflation hydra heads is The Federal Reserve itself.

Yesterday, I told my family “The good news is that Rotolo’s Pizza tastes even better reheated in the morning. The bad news? I ate the only two piece left.”

Which brings me to the September jobs report. The good news is that 263k jobs were added to the US economy. That means 10,521k jobs have been added in the 21 months under Biden! (Bear in mind that 12,100k jobs were added in the 7 months under Trump following the Covid economic shutdown, yet no media outlet trumpeted that accomplishment).

The bad news? While nominal average hourly earnings grew by 5% YoY, when I subtract Bidenflation from that number I get -3.06% growth. Or should I say that REAL wages are shrinking under Biden.

Now for the “Biden Miracle” of jobs being added. Here is a chart of NFP jobs added (white line) against M2 Money and headline inflation. Both The Fed and the Federal government pumped trillions into the economy leading to the highest inflation rate in 40 years. Once governments stopped with their Covid shutdown nonsense, jobs would return regardless of who was President. BUT Federal spending and Fed money printing went off the rails in early 2020.

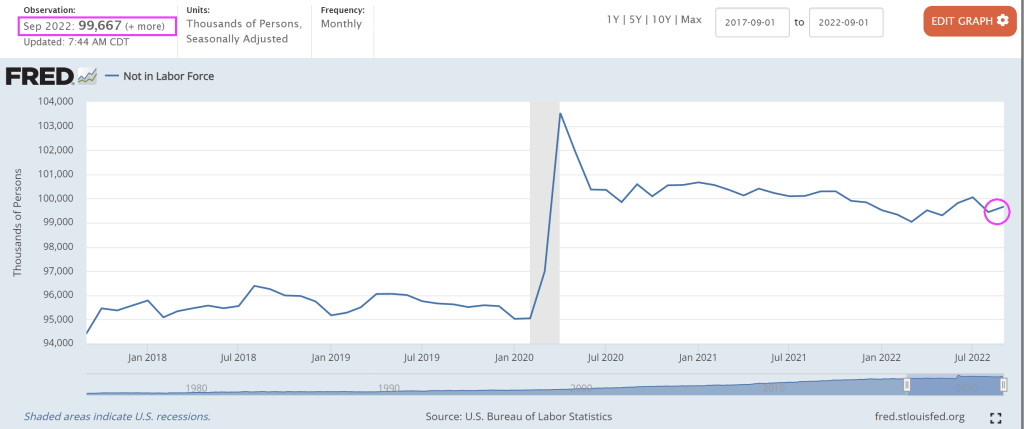

As Paul Harvey used to say, “Here is the rest of the story.” Labor force participation fell in September and the U-3 unemployment rate fell slightly to 3.5%.

But labor force dropouts increased leading U-3 unemployment to decline. The number of people NOT in the labor force grew to nearly 100 million. Nothing has been the same since Covid.

So what will The Fed do? According to Fed Funds Futures data (WIRP), The Fed will keep raising rates until March ’23 then slowly start lowering interest rates again.

And with that “positive” jobs report, The Dow is down almost -500 points and the NASDAQ is down over -3%.

And with Fed tightening, we are seeing a collapse in M2 money supply.

What do we have? Regular gasoline prices are UP 61.4% under Biden, the strategic petroleum reserve is DOWN -35% before Biden’s latest release of another 10 million barrels. Foodstuffs are UP 50% under Clueless Joe, and heating oil futures are UP 130% under dementia Joe.

And thanks to free-spending Joe, Nancy and Chuckie, US public debt is at $31.1 TRILLION. That is ANOTHER 12% in national debt under the 4 Horsemen of the Economic Apocalypse.

For an additional 12% in national debt (to be paid by our children and grandchildren), we have crippling inflation.

Challenger US Job Cut Announcements for September rose 67.6%, the highest since … Covid-19 outbreak in early 2020. This comes after the JOLTS (job openings) fell the most since … Covid-19.

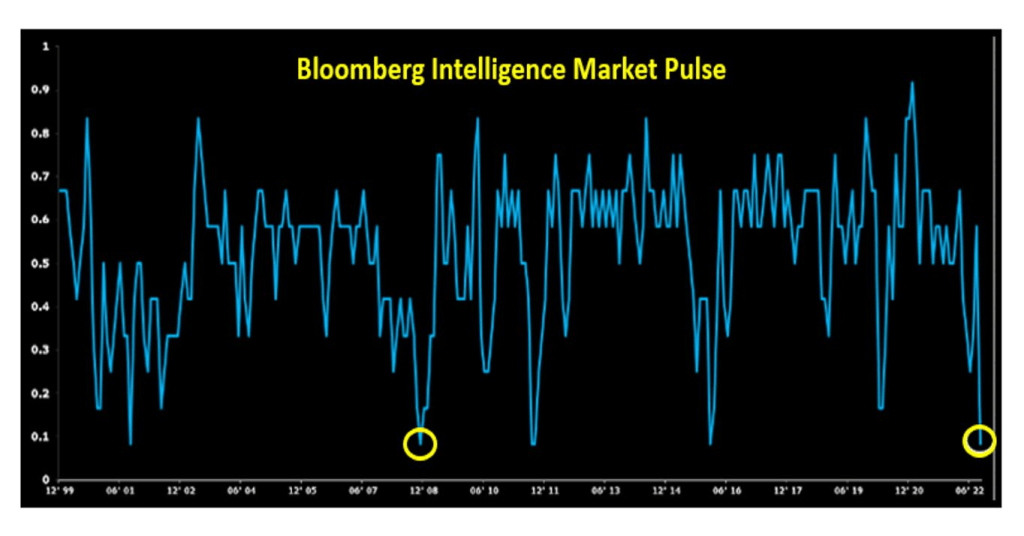

This index quantifies sentiment using 6 factors — price breadth, pairwise correlation, low vol perf, defensive vs. cyclical sector perf, high vs. low leverage perf and high yield spreads.

Pension funds hold large positions in US Treasuries and Agency Mortgage-backed Securities (MBS). As does America’s central bank, The Federal Reserve. All are suffering losses as The Fed fights inflation.

(Bloomberg) — Week by week, the bond-market crash just keeps getting worse and there’s no clear end in sight.

With central banks worldwide aggressively ratcheting up interest rates in the face of stubbornly high inflation, prices (created by The Fed, Biden’s Green Energy Follicies and reckless Federal spending) are tumbling as traders race to catch up. And with that has come a grim parade of superlatives on how bad it has become.

On Friday, the UK’s five-year bonds tumbled by the most since at least 1992 after the government rolled out a massive tax-cut plan that may only strengthen the Bank of England’s hand. Two-year US Treasuries are in the middle of the the longest losing streak since at least 1976, dropping for 12 straight days. Worldwide, Bank of America Corp. strategists said government bond markets are on course for the worst year since 1949, when Europe was rebuilding from the ruins of World War Two.

The escalating losses reflect how far the Federal Reserve and other central banks have shifted away from the monetary policies of the pandemic, when they held rates near zero to keep their economies going. The reversal has exerted a major drag on everything from stock prices to oil as investors brace for an economic slowdown.

And as The Fed tries to combat stubborn inflation (caused by The Fed, Biden’s Green Energy folly and reckless Federal spending), you can see the US government security liquidity is worsening.

At least inflation has produced one “positive.” REAL mortgage rates are NEGATIVE since Freddie Mac’s 30-year mortgage rate less headline inflation is currently -2.975%.

Then we have Agency MBS (example, FNCL 3% MBS) plunging like a paralyzed falcon as duration risk increases with Fed rate tightening.

Fed Funds Futures data points to tightening until May ’23, then a reversal of rate hikes.

You must be logged in to post a comment.