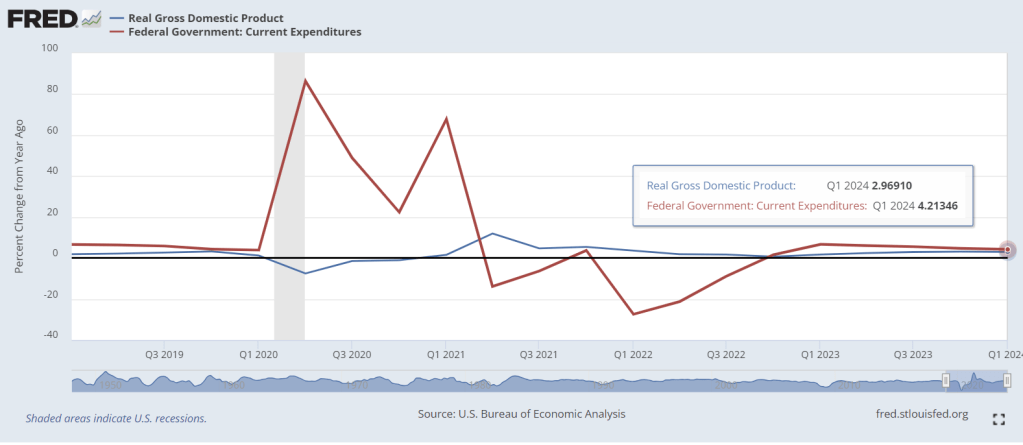

COVID was a gift to Biden. The furious Federal spending of Q2 2020 through Q1 2021 helped keep GDP growth above recession levels.

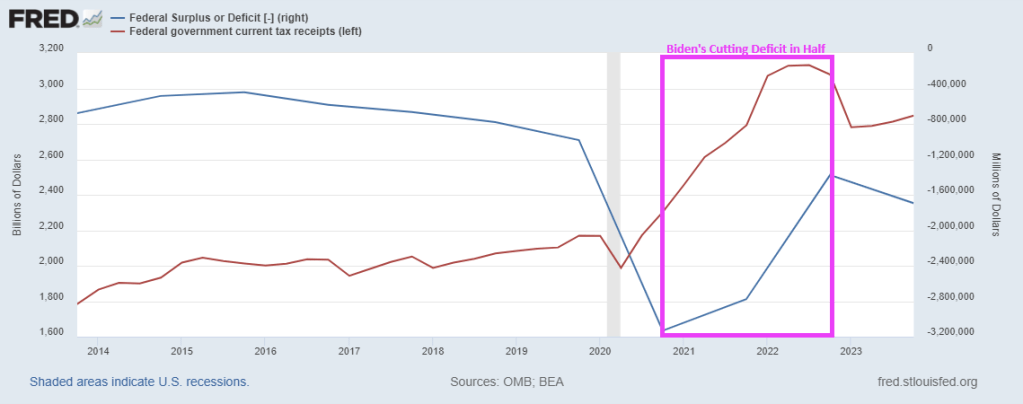

Ignore Biden’s demented rants/lies about cutting the debt in half. Biden has claimed he cut the $34+ trillion national debt by $7 billion, $1.4 trillion, $1.7 billion, $1.7 trillion, and “in half,” depending on the day he rants. He did no such thing. He is confused and is talking about the BUDGET DEFICIT (don’t look to Snopes to fact check “Trucker Joe”, they really only fact check Trump).

Not surprisingly, the Federal deficit spiked with the Covid lockdowns. But when the economy reopened, the budget deficit shrunk because … the economy was open and Federal tax receipts soared. But we are back to rising deficits again.

Today, Q1 GDP numbers were released and it looks great. Real GDP year-over-year was 2.97% while Federal government expenditures YoY were 4.21%. But the US is still processing the tidal wave of COVID-related spending out of Washington DC (red line). The YoY growth in Federal spending was 86.4% in Q2 2020, 48.9% in Q3 2020, 22.4% in Q4 2020, and 67.8% in Q1 2021. Like The Titanic trying to avoid the iceberg, it takes a while for massive Federal spending to work itself through the economic system.

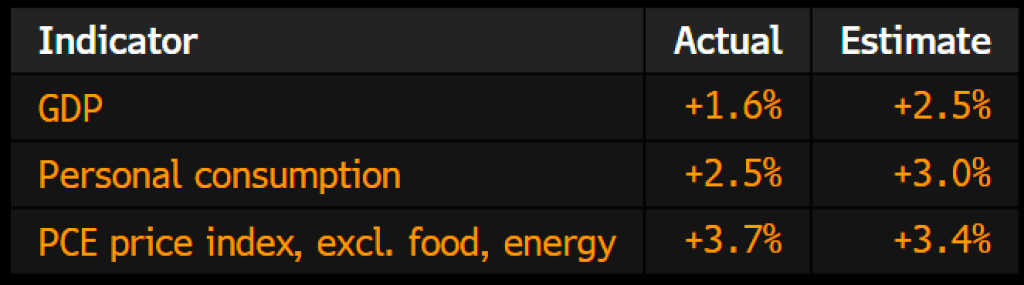

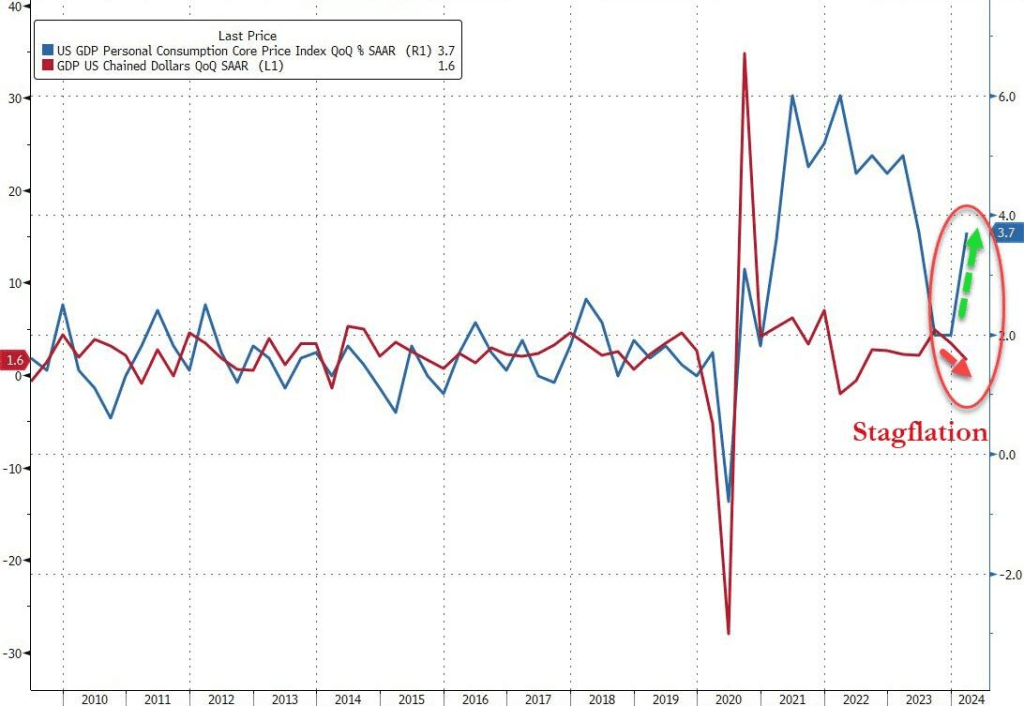

On a QoQ basis, US GDP increased by only 1.60%. Here are the contributions to GDP.

GDP QoQ was up 1.6% while Core PCE Price Index rose 3.7%. Yikes!

Are we entering Stagflation with the worst GDP print in 2 years as prices soar. As COVID stimulus seems to be wearing out.

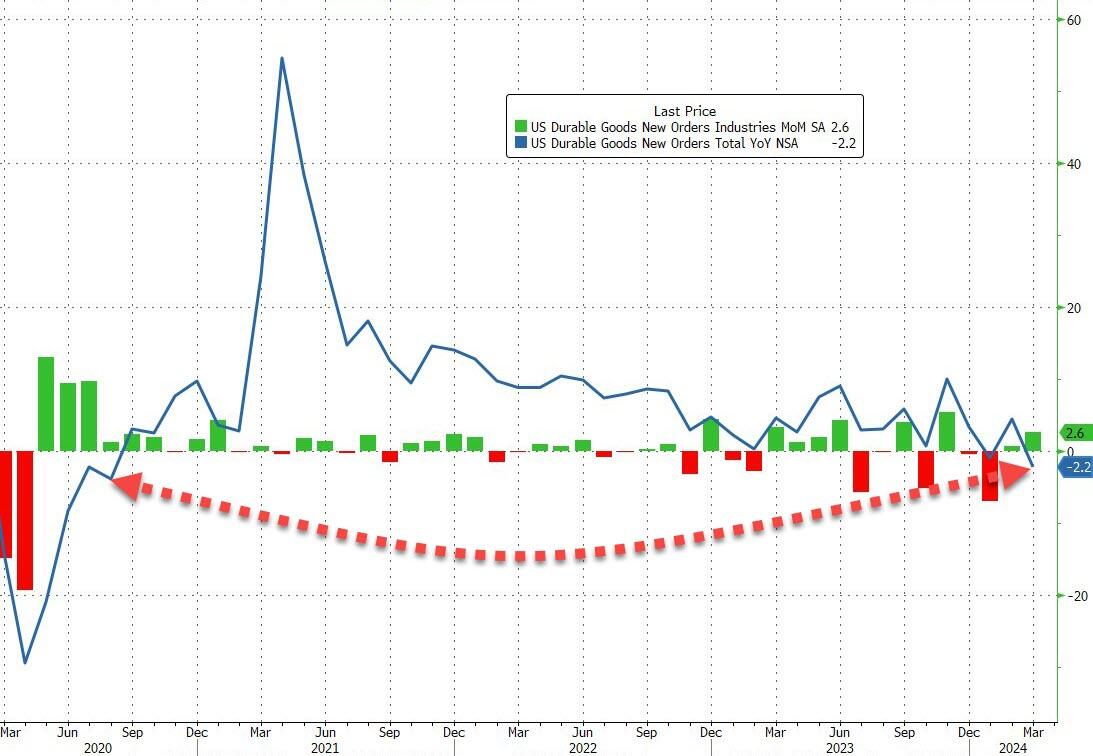

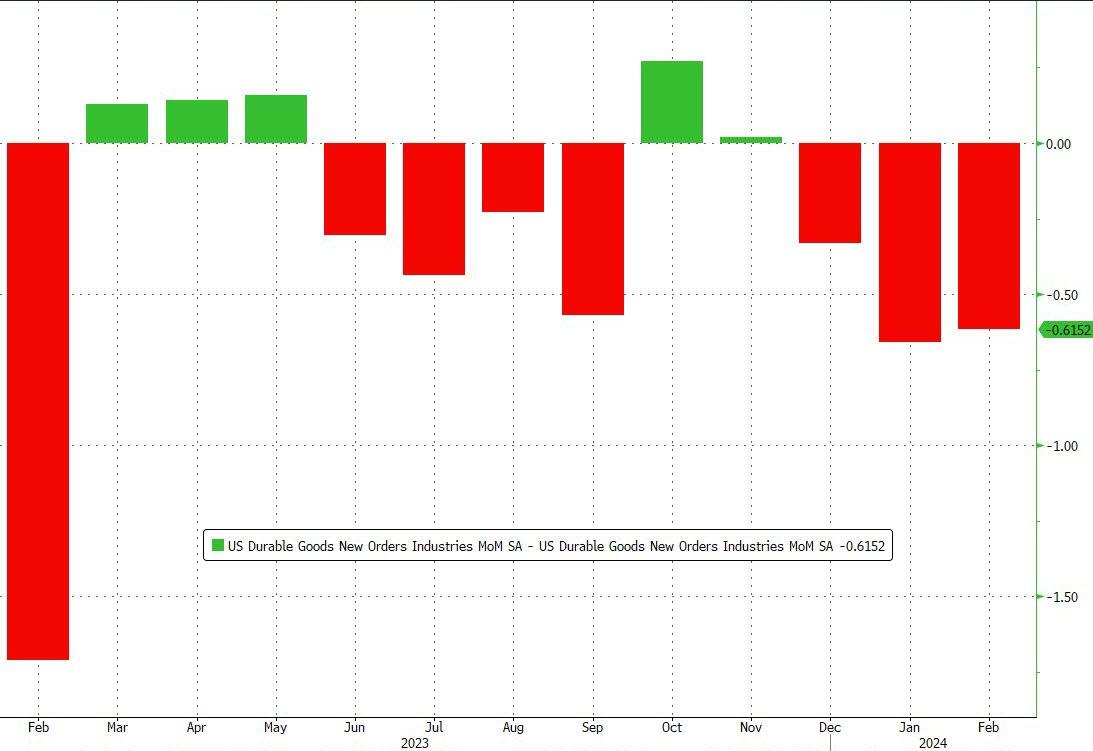

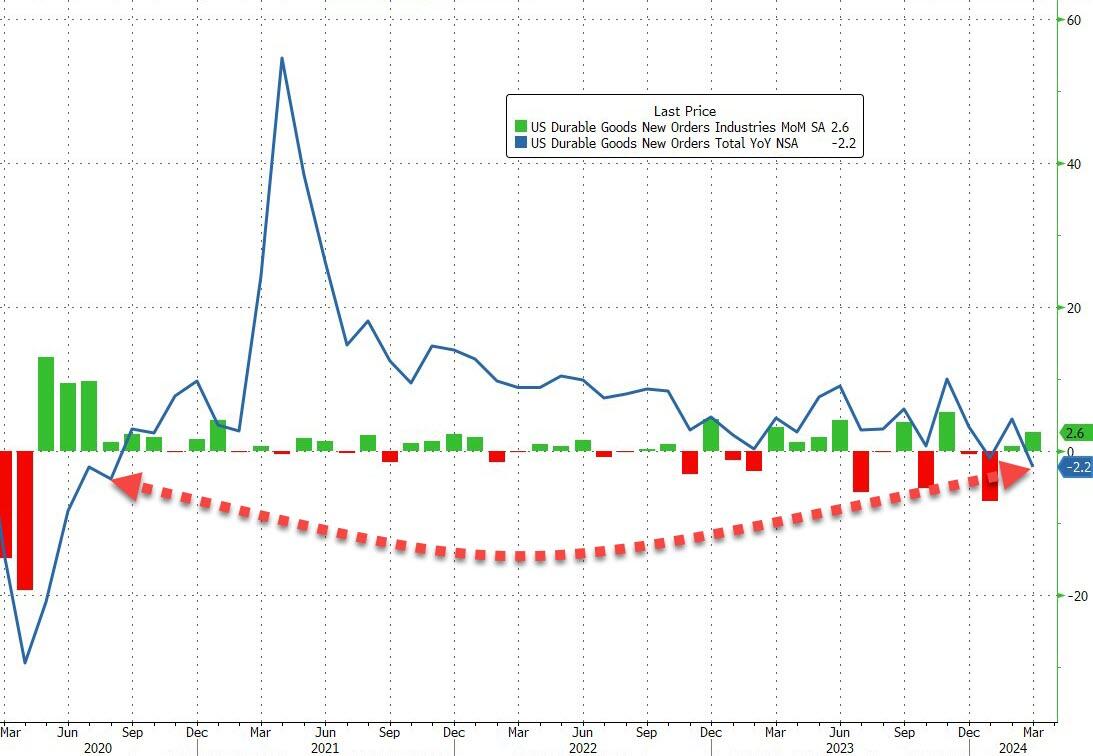

Manufacturer’s Durable Goods New Orders growth peaked in April 2021, thanks in part to M2 Money Growth peaking in February 2021. And its been all downhill since then.

This is the 8th downward revision of durable goods orders in the last year…

Source: Bloomberg

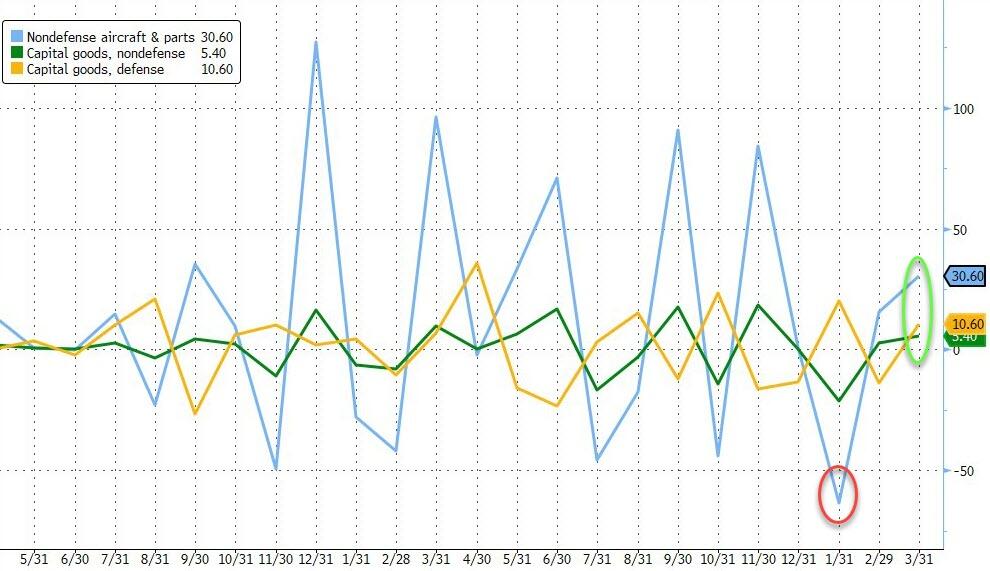

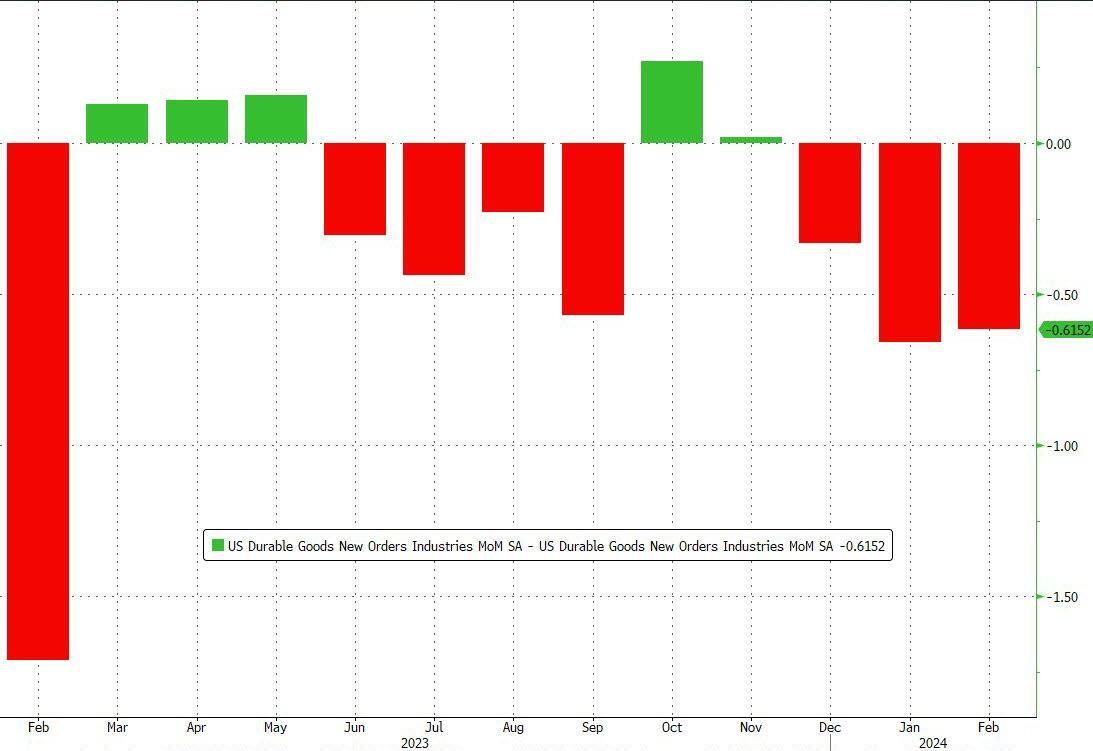

Under the hood, defense and non-defense capital goods orders rose with non-defense aircraft orders surging over 30% MoM…

Source: Bloomberg

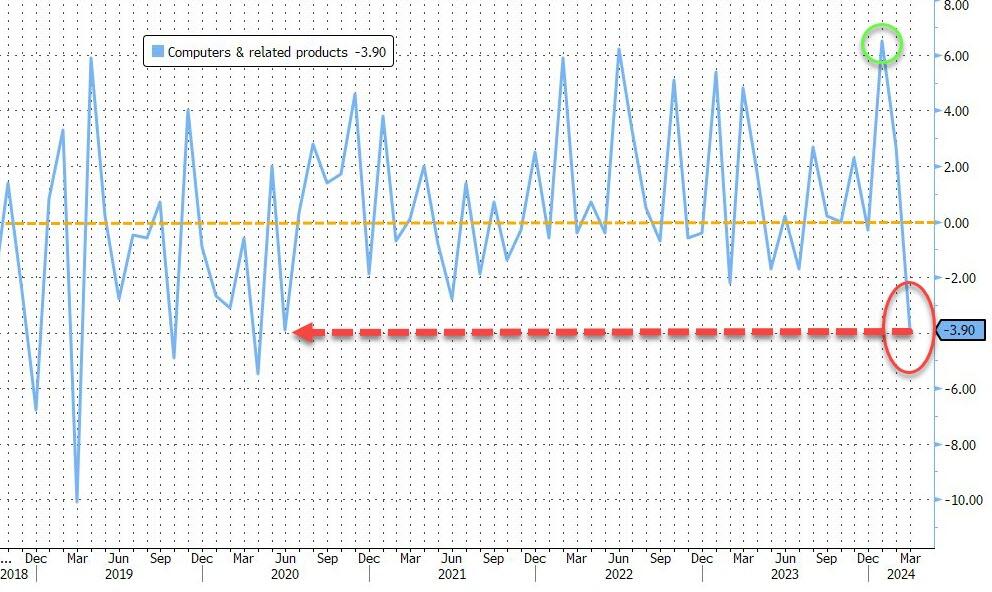

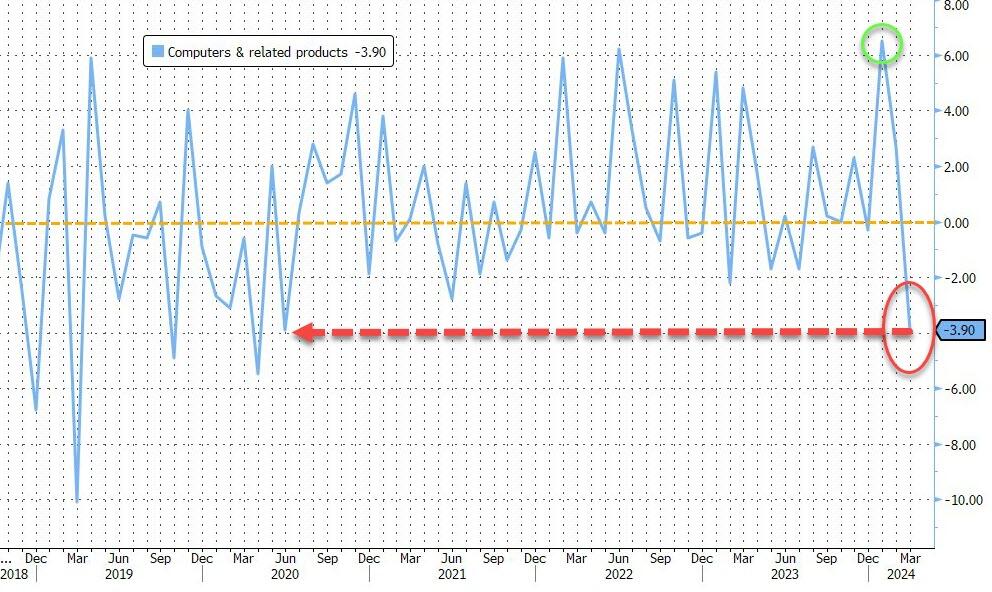

But… it looks like the AI bubble just burst as Computer & related Products orders plunged 3.9% MoM – the biggest drop since COVID lockdowns…

Source: Bloomberg

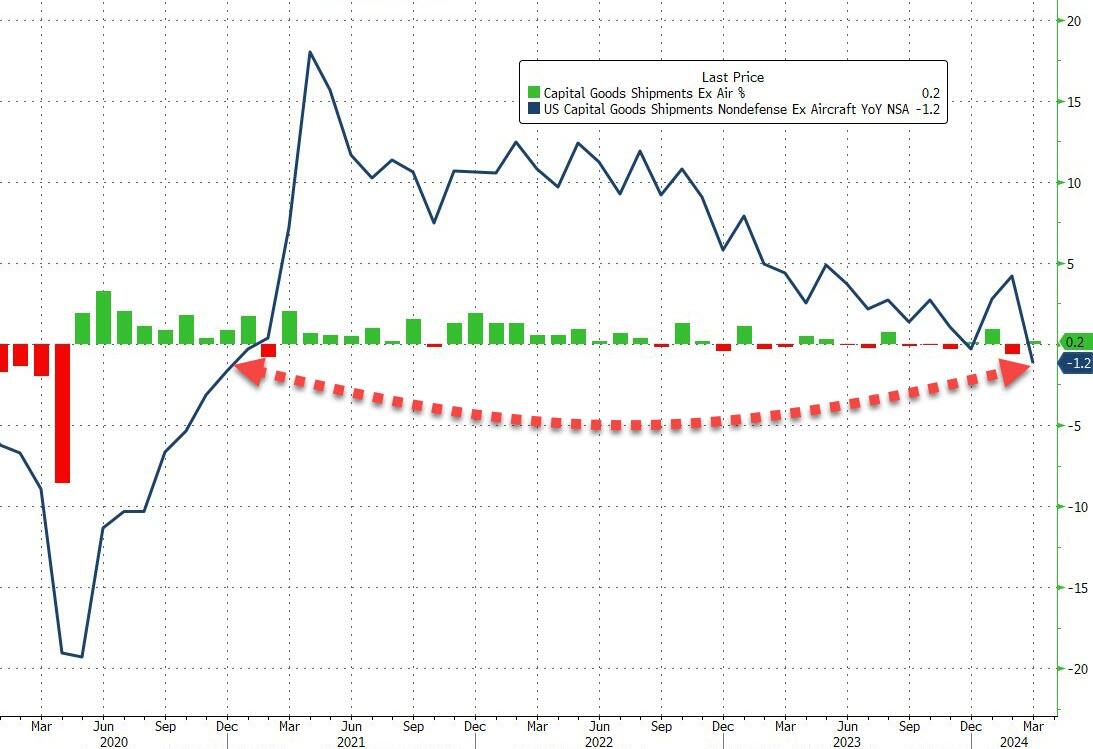

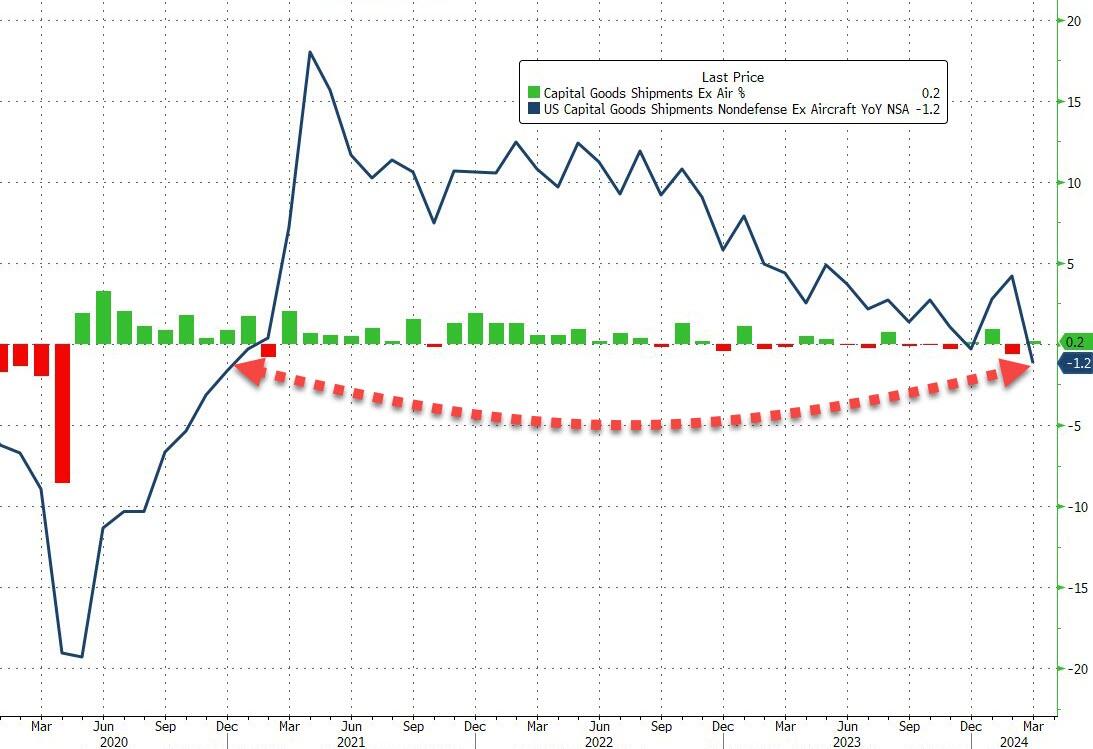

Finally, and more problematically, core capital goods shipments – a figure that is used to help calculate equipment investment in the government’s gross domestic product report – saw only a small 0.2% MoM rise, which left core shipments down 1.2% YoY – the biggest YoY drop since the COVID lockdowns…

Source: Bloomberg

Now that Biden is considering a NATIONAL CLIMATE EMERGENCY granting him 130 War-like powers, I shudder to think for much green spending he will initiate.

Biden: “How many times does Trump have to prove we can’t be trusted?”

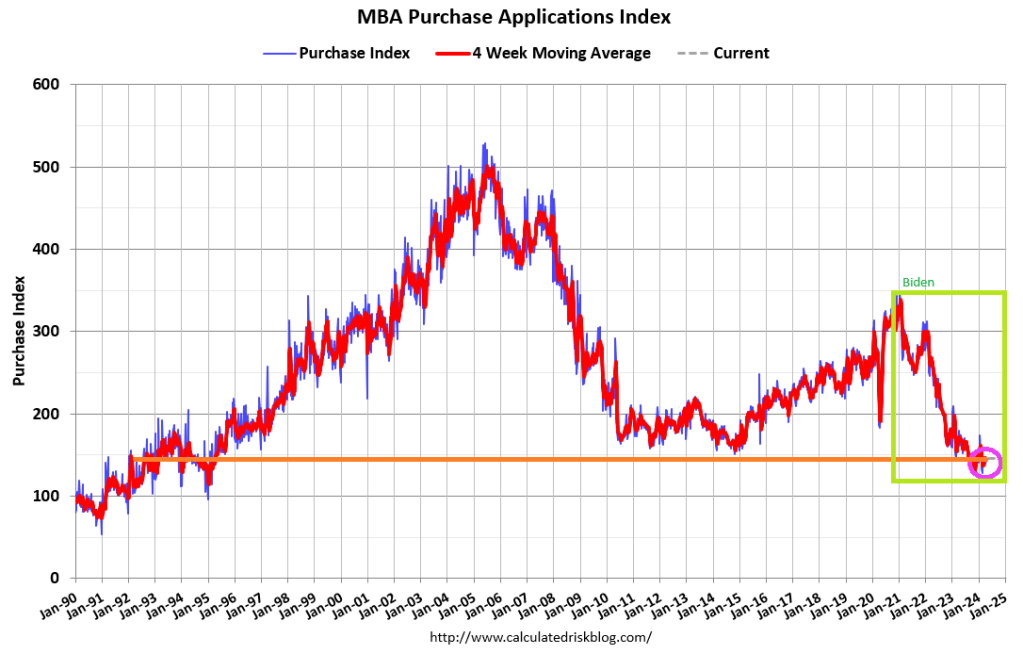

Mortgage applications increased 3.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 12, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 4 percent compared with the previous week. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 10 percent lower than the same week one year ago.

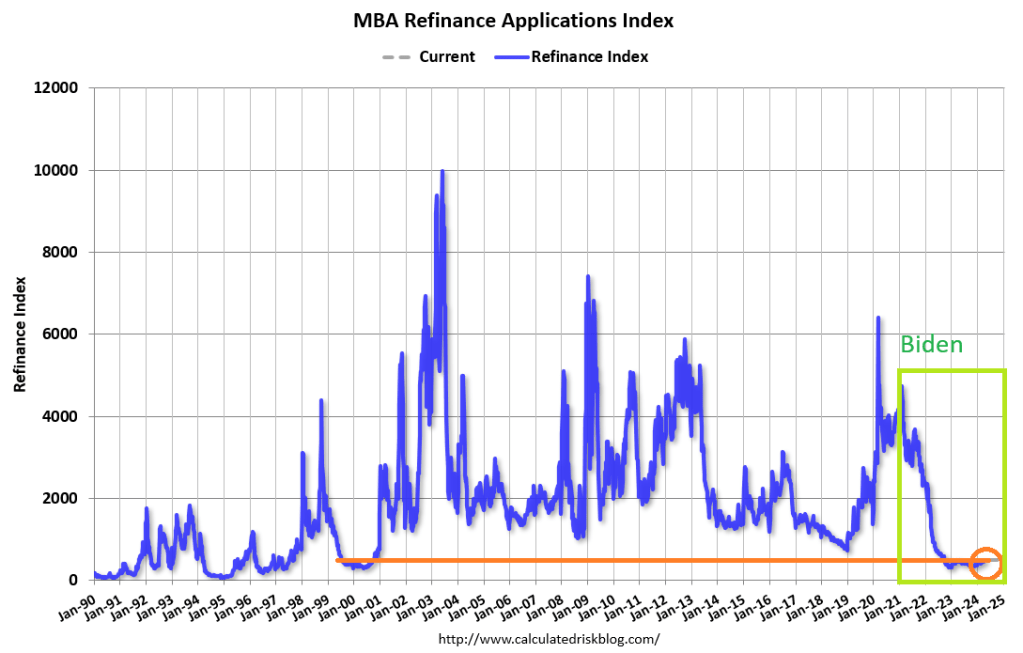

The Refinance Index increased 0.5 percent from the previous week and was 11 percent higher than the same week one year ago.

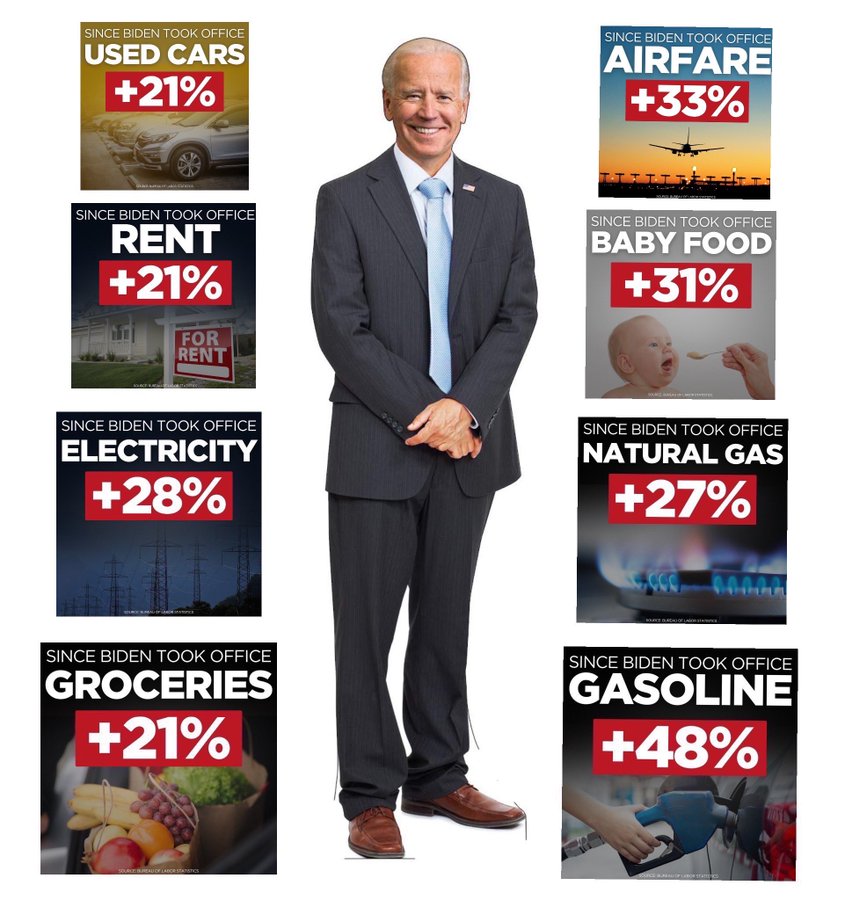

Bidenomics, a massive subsidy to the political donor class, but heartless towards the middle class.

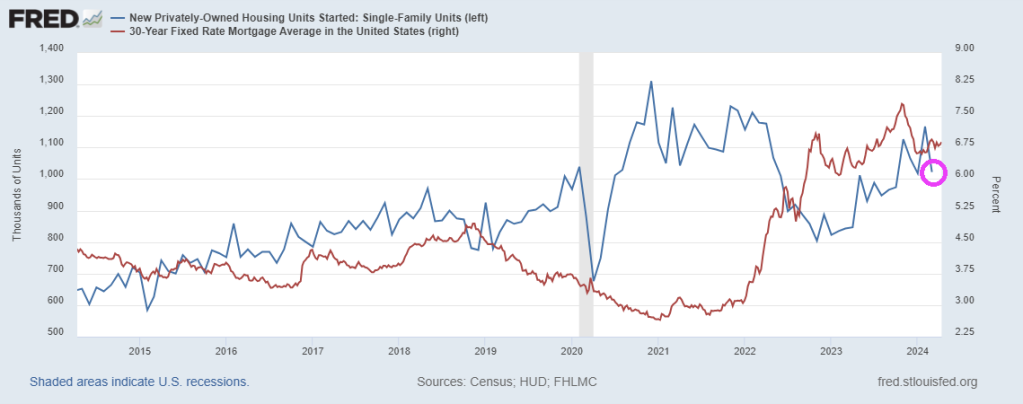

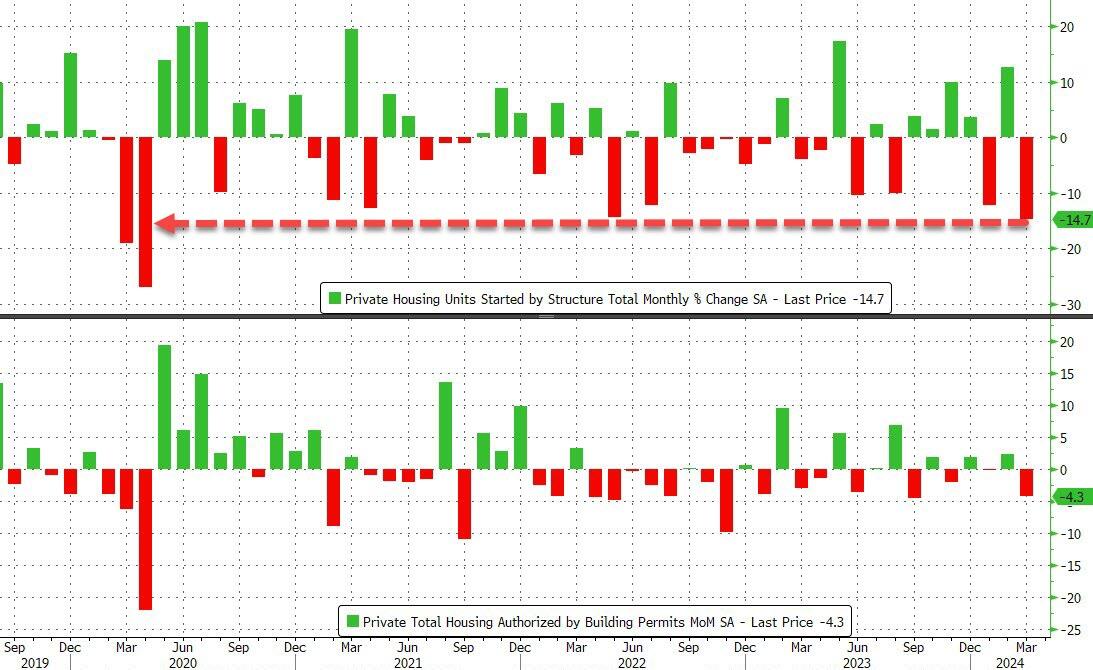

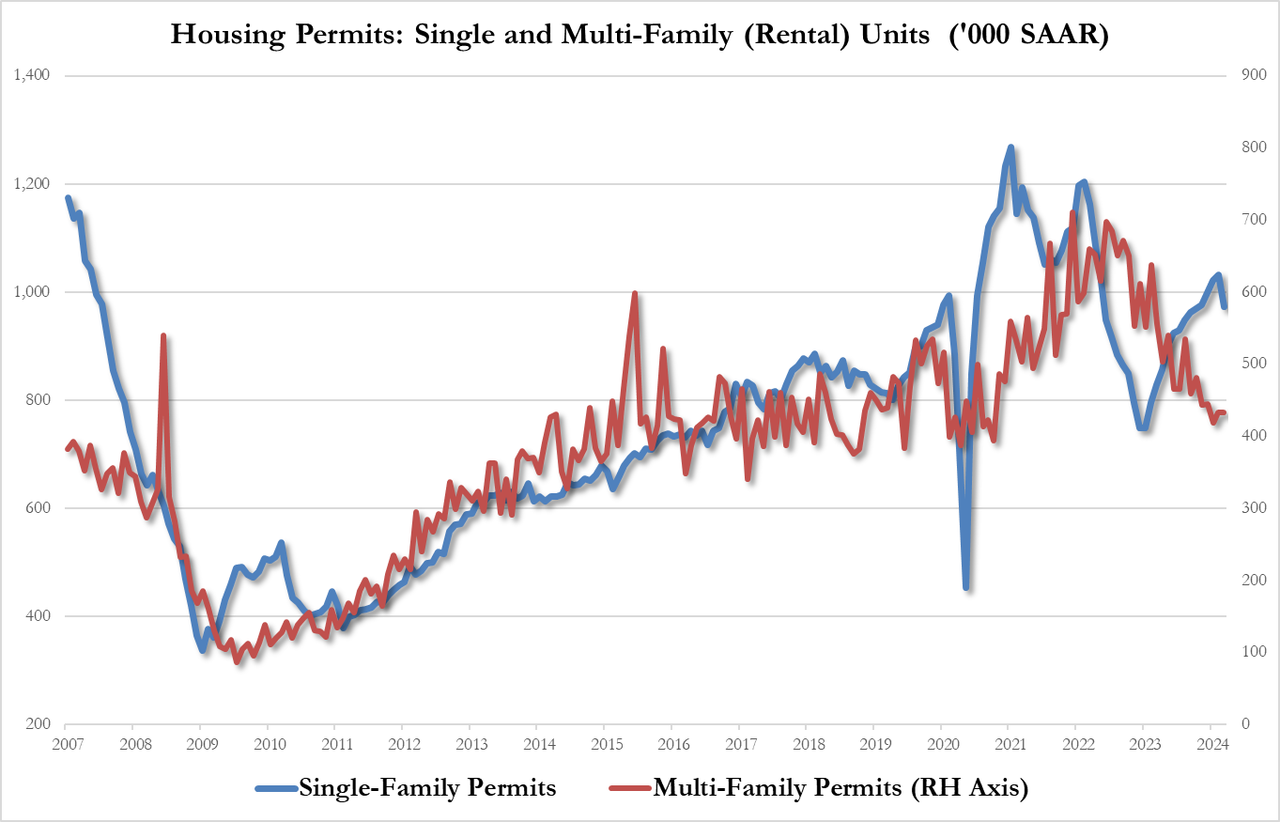

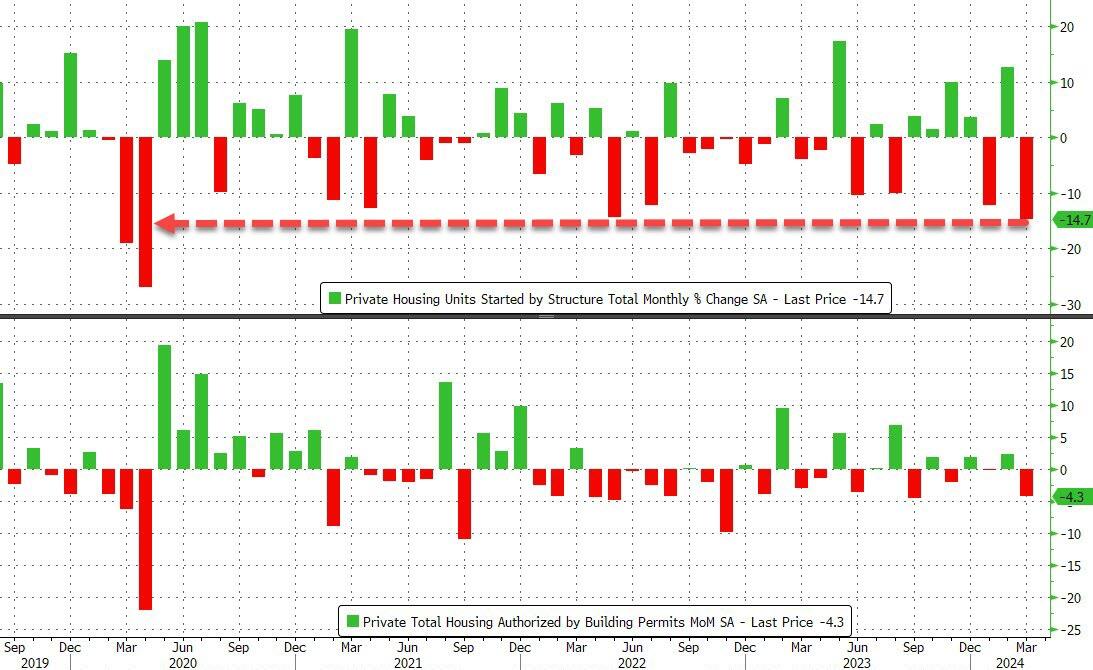

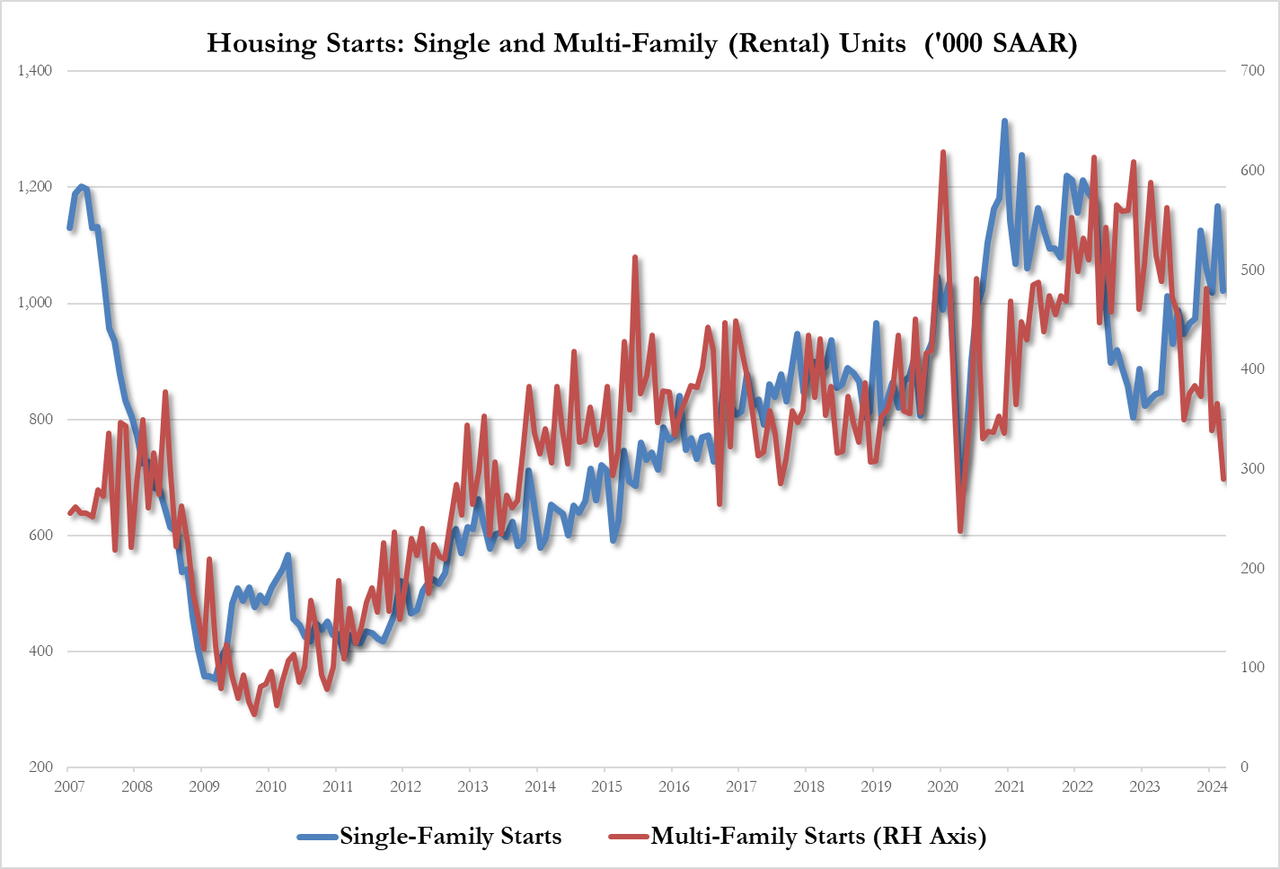

Come feel the noise! After steady growth in 1-unit housing starts under Trump, housing starts have been eratic under Biden despite the foreign invasion force of millions … of low wage workers.

For context, this is the largest MoM drop in housing starts since the COVID lockdowns…

Source: Bloomberg

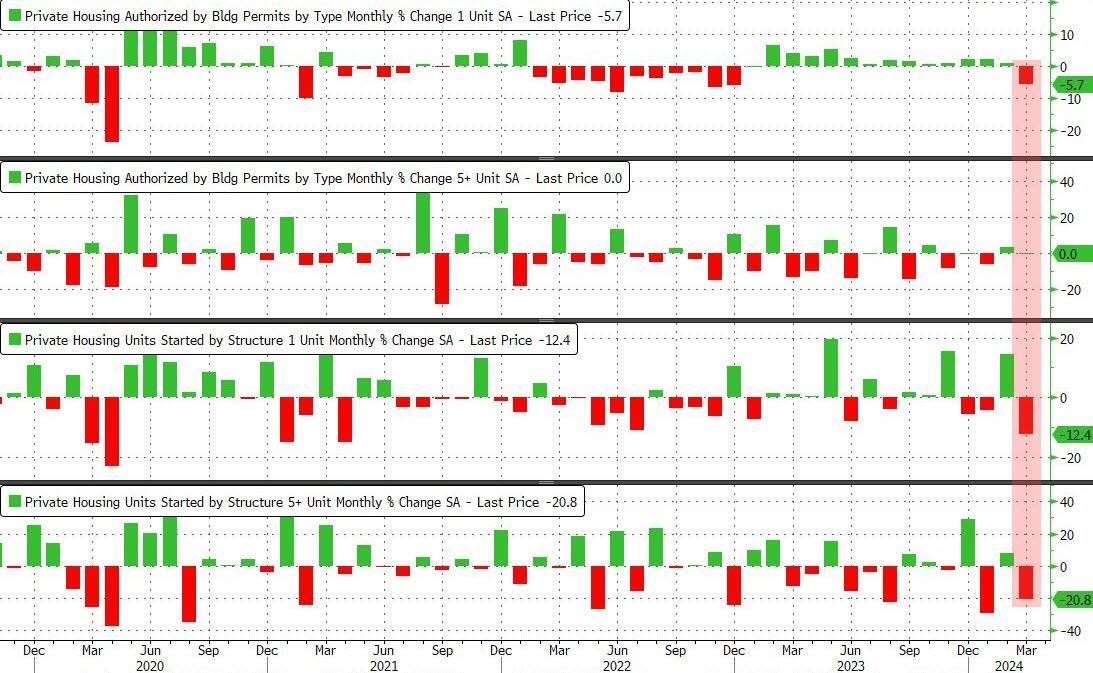

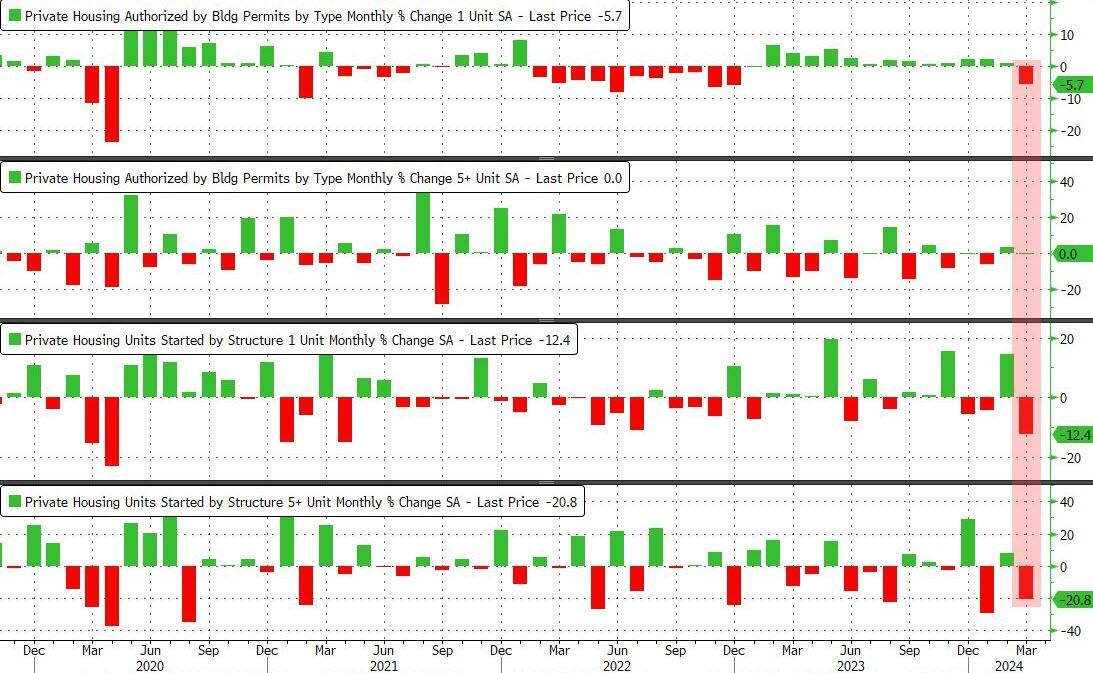

It was a bloodbath across the board with Rental Unit Starts plummeting 20.8% MoM…

Source: Bloomberg

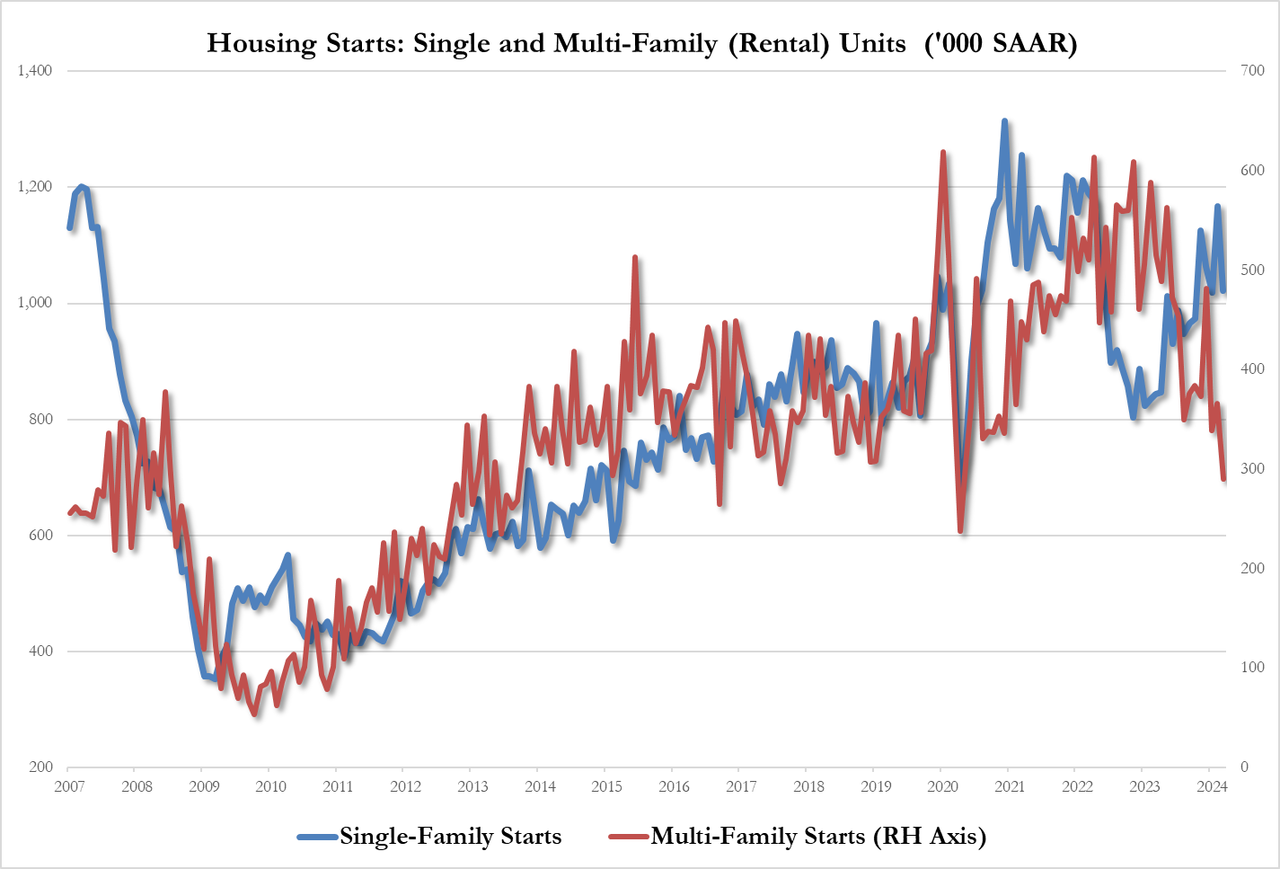

That pushed total multi-family starts SAAR down to its lowest since COVID lockdowns…

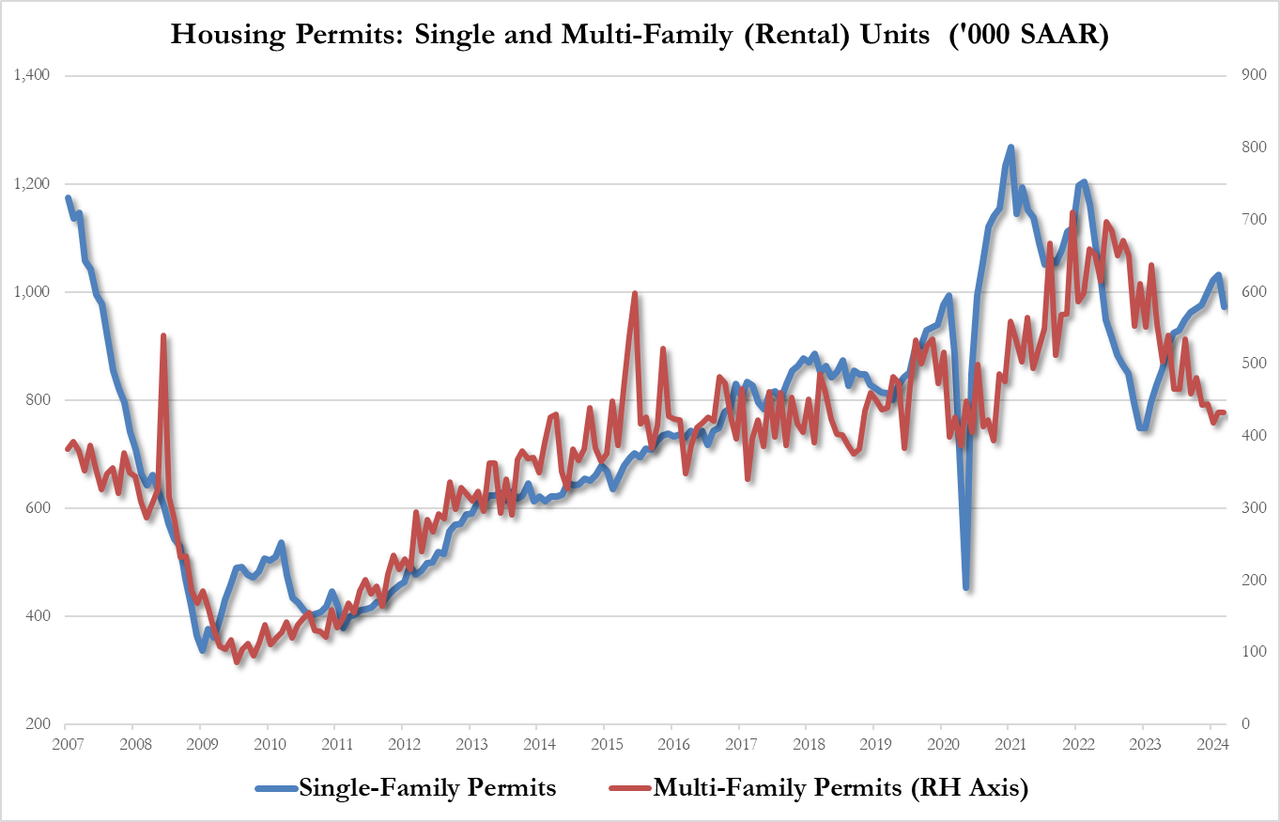

The plunge in permits was less dramatic and driven completely by single-family permits down 5.7% to 973K SAAR, from 1.032MM, this is the lowest since October. Multi-family permits flat at 433K

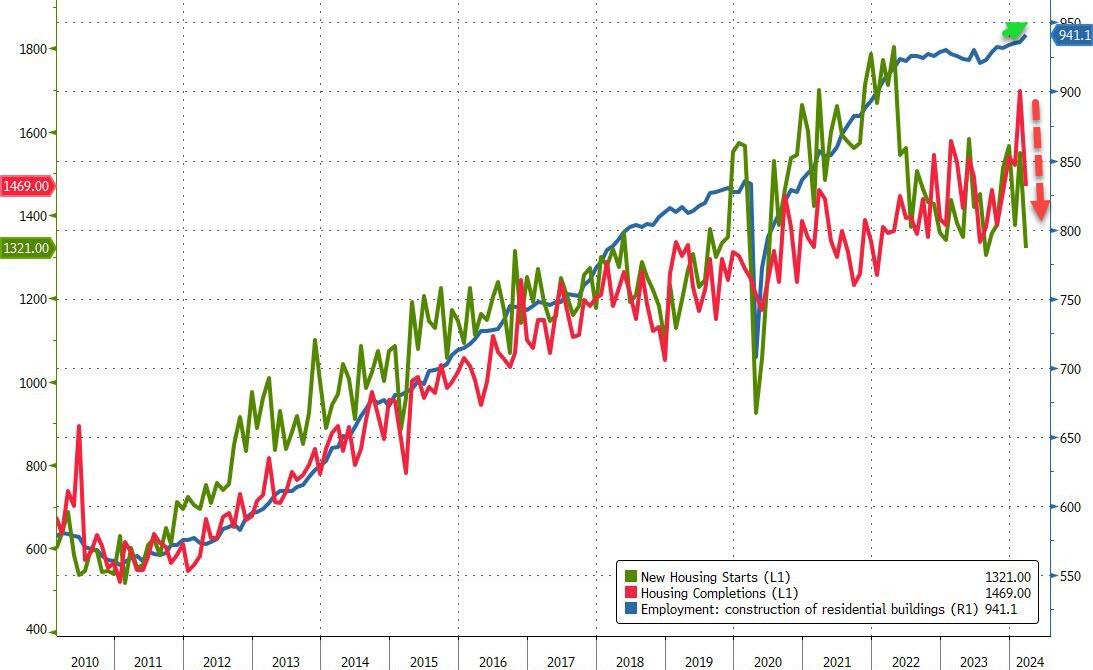

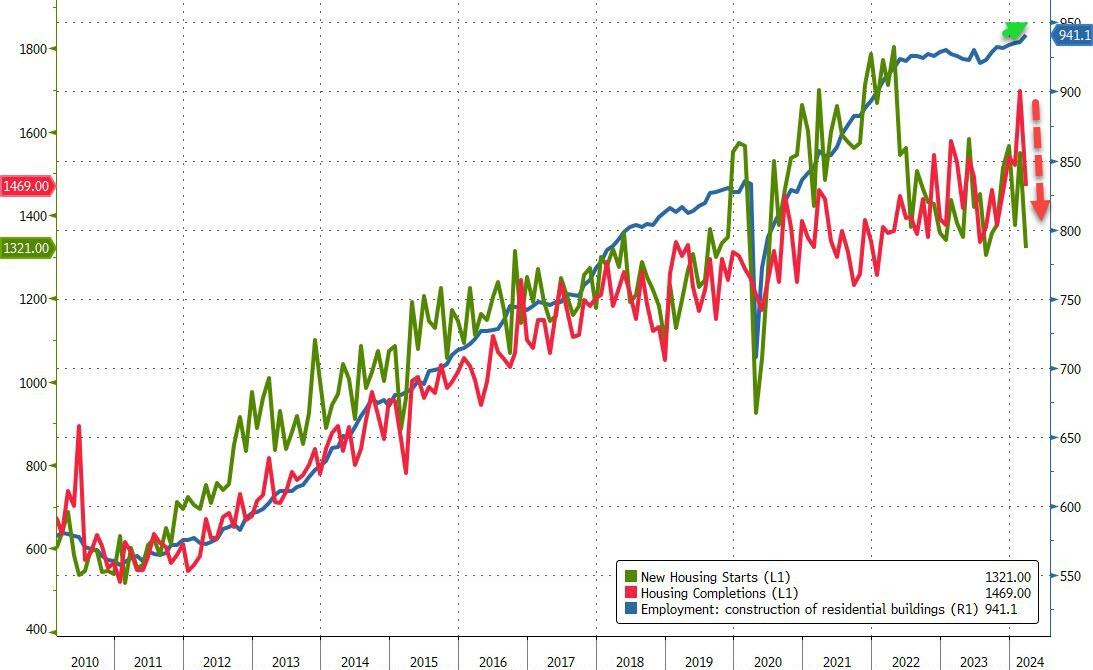

Intriguingly, while starts and completions plunged in March, the BLS believes that construction jobs surged to a new record high…

Source: Bloomberg

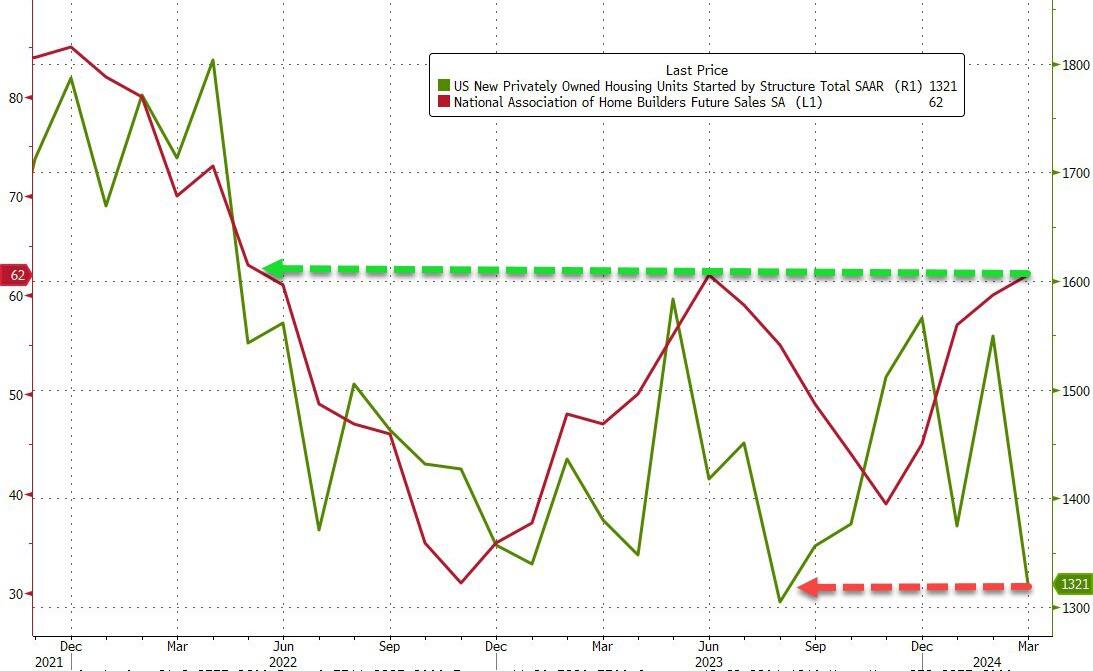

Finally, just what will homebuilders do now that expectations for 2024 rate-cuts have collapsed?

Source: Bloomberg

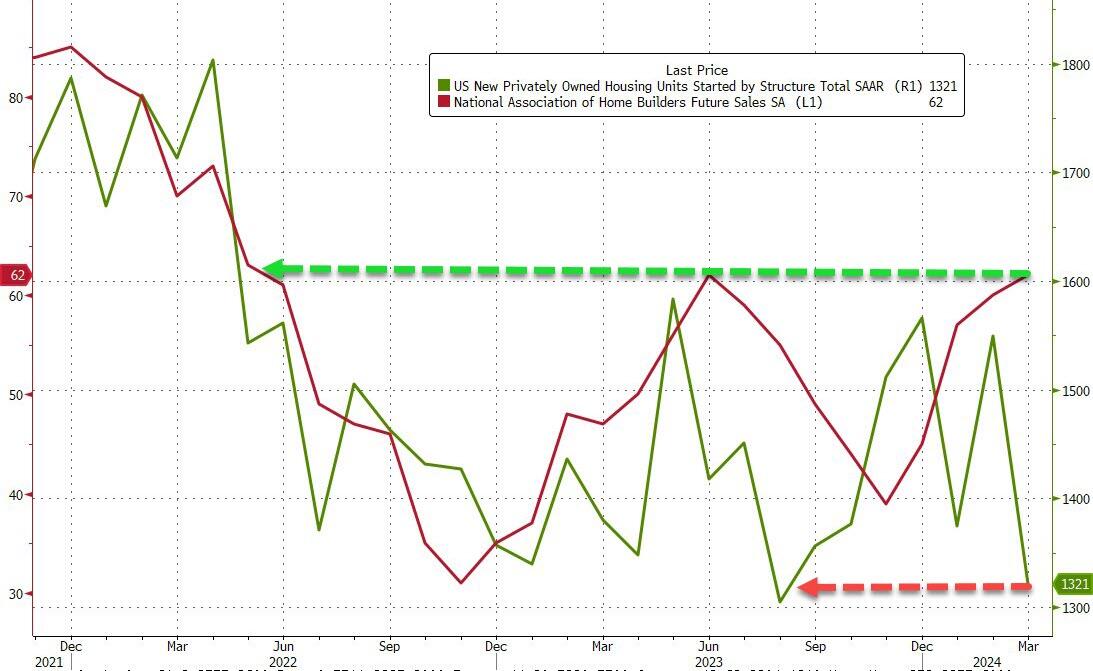

One thing is for sure – do not trust what homebuilders ‘say’ (as NAHB confidence jumped to its highest since May 2022 at the same time as housing starts crashed)…

US CPI on trend for 4-5% at US election in November.

Source: BofA

Above 5%…?

Strong CPI raises market probability of YE25 rates above 5%.

Source: Goldman

Cyclical inflation remains too elevated

“Our measure of cyclical inflation–which should capture the impact of excess demand on prices–appears to be stuck at around 5%, which is too elevated”

Source: Safra

US alone

The US is the only economy in the G10 where the latest inflation print surprised to the upside.

Source: Goldman

200% of GDP

Under current policies, government debt outstanding will grow from 100% to 200% of GDP.

Source: Apollo

Close to $9 trillion in maturities

That’s a significant amount of government debt maturing within the next year.

Source: Apollo

Every year a deficit

OMB forecasts 5% budget deficit every year for the next 10 years.

Source: Apollo

A billion per day….is long gone

US government interest payments per day have doubled from $1bn per day before the pandemic to almost $2bn per day in 2023.

Source: Apollo

Biggest Story of 2020s…Ugly End of 40-year Bond Bull

Chart shows long-term US government bond (15+ year) rolling 10-year annualized returns, %.

Source: Flow Show

Highest yields in 15 years

The intermediate part of the yield curve still offers the highest yields in over fifteen years.

Source: Piper Sandler

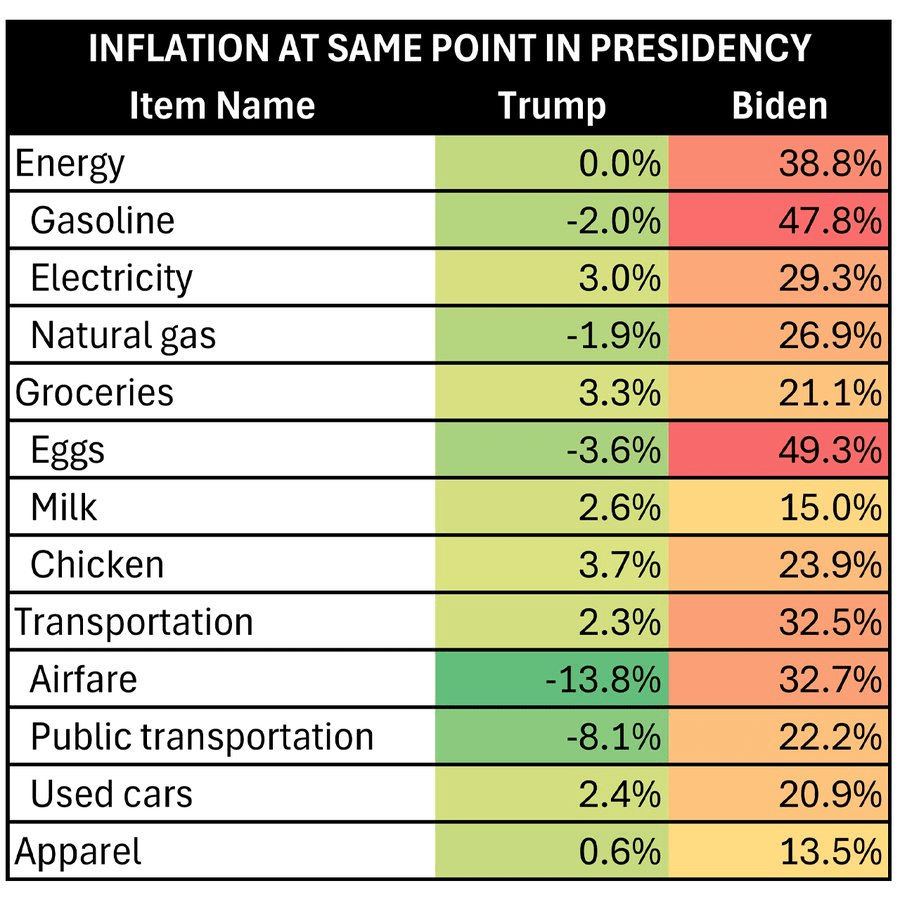

Finally, electricity costs keeps rising, ESPECIALLY with the misnamed Inflation Reduction Act (IRA). The real name of the IRA should have been the Large Green Donor Increase Act (LGDIA).

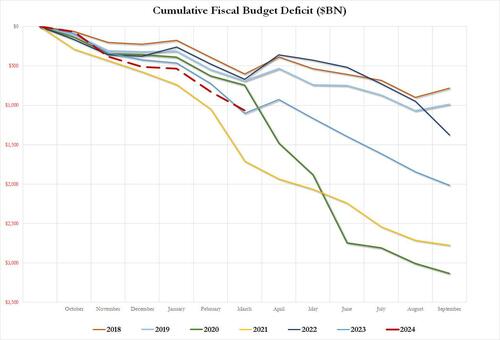

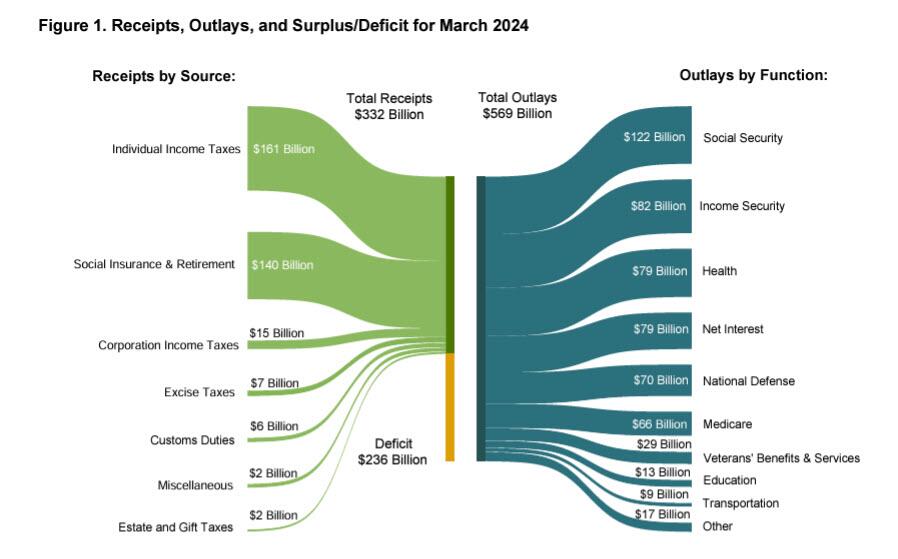

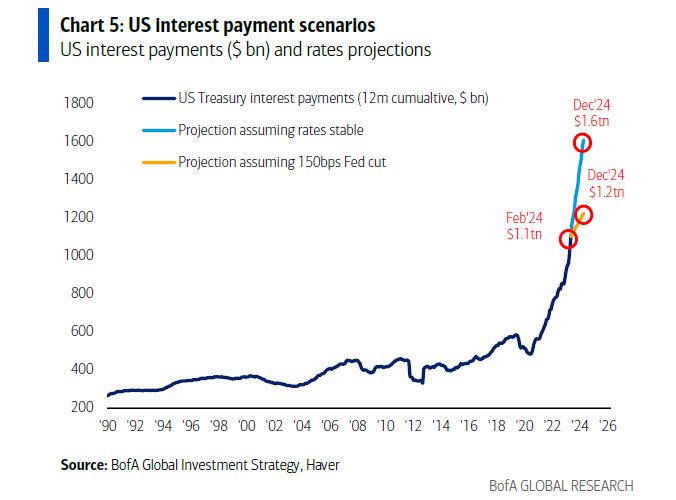

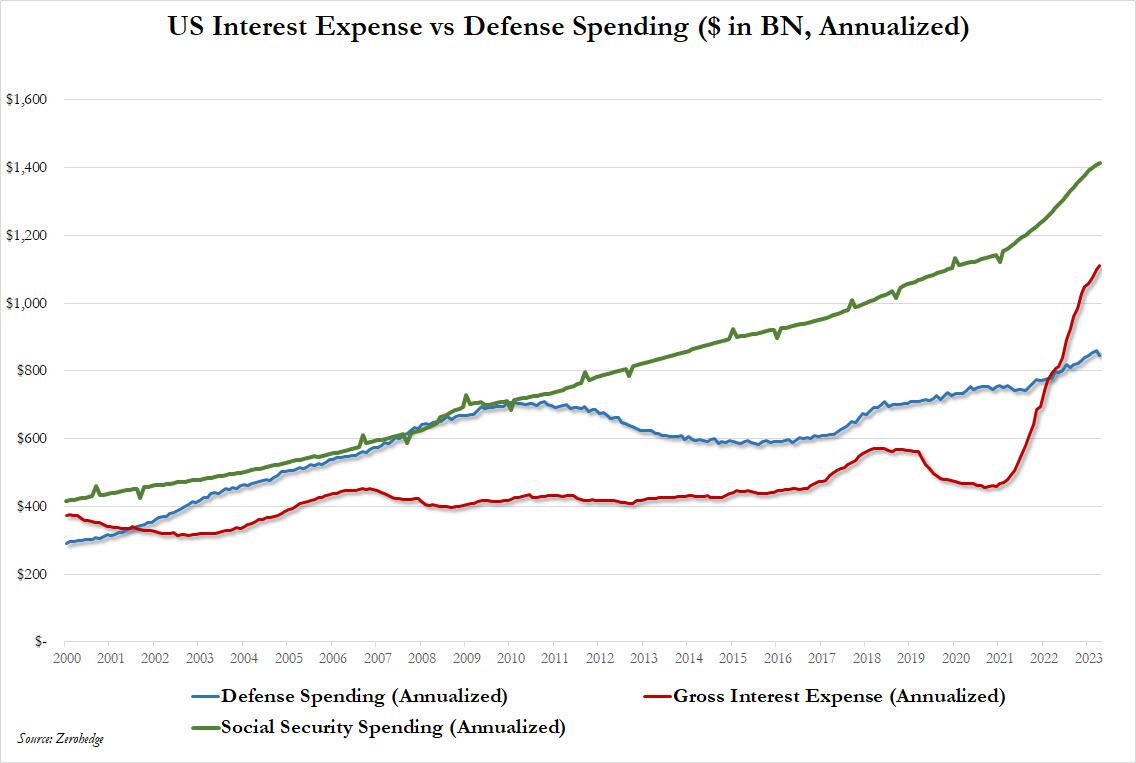

Under Biden’s “Reign of Error”, the interest on US debt just hit a record $1.1 trillion and the US deficit for just the first six months of fiscal 2024 is also $1.1 trillion.

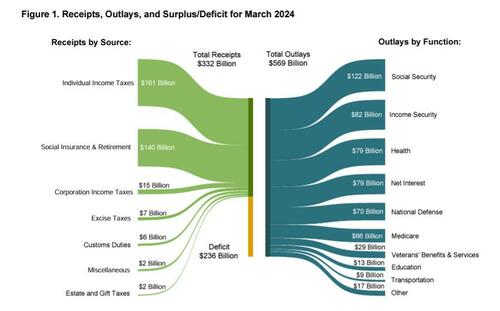

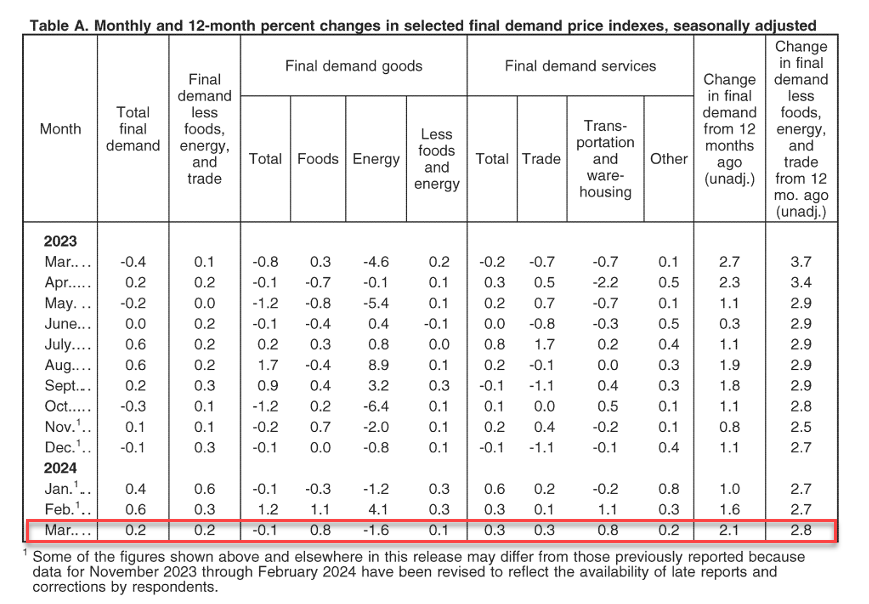

According to the latest Treasury Monthly Statement, in March the US deficit hit $236 billion, some $40 billion more than the $196 billion expected, if below February’s $296 billion…

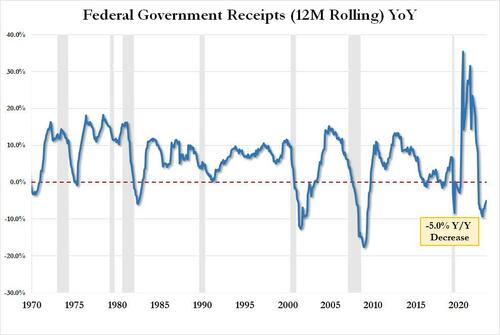

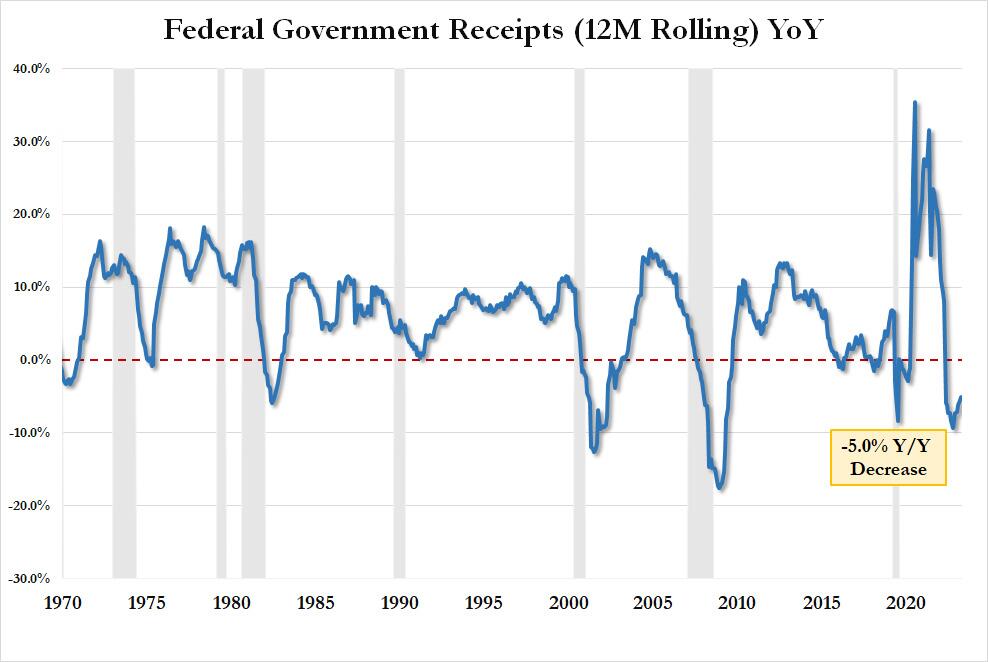

… which was the result of $332 billion in govt tax receipts – translating into $4.580 trillion in LTM tax receipts, and which was down 5% compared to a year ago…

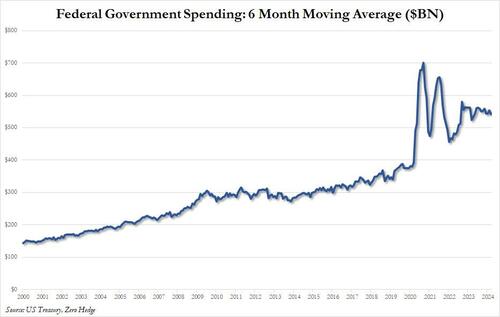

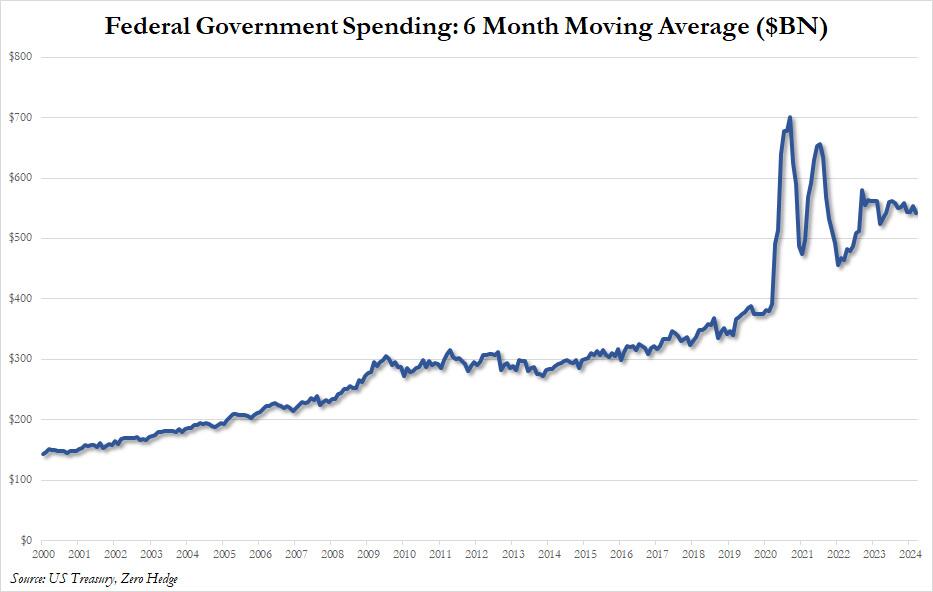

… offset by the now traditional ridiculous monthly outlays, which in March amounted to $568 billion, up from $567 billion in February and the highest monthly spending total in calendar 2024, which translated into a 6 month moving spending average (for smoothing purposes) of $542 billion. Take a wild guess what will happen to the chart below during and after the next recession.

This, incidentally, is a reminder that the US does not have a tax collection problem – it has a spending problem, and no amount of tax changes will fix it; in fact all higher taxes will do is force more billionaires to move to Dubai where they pay zero taxes.

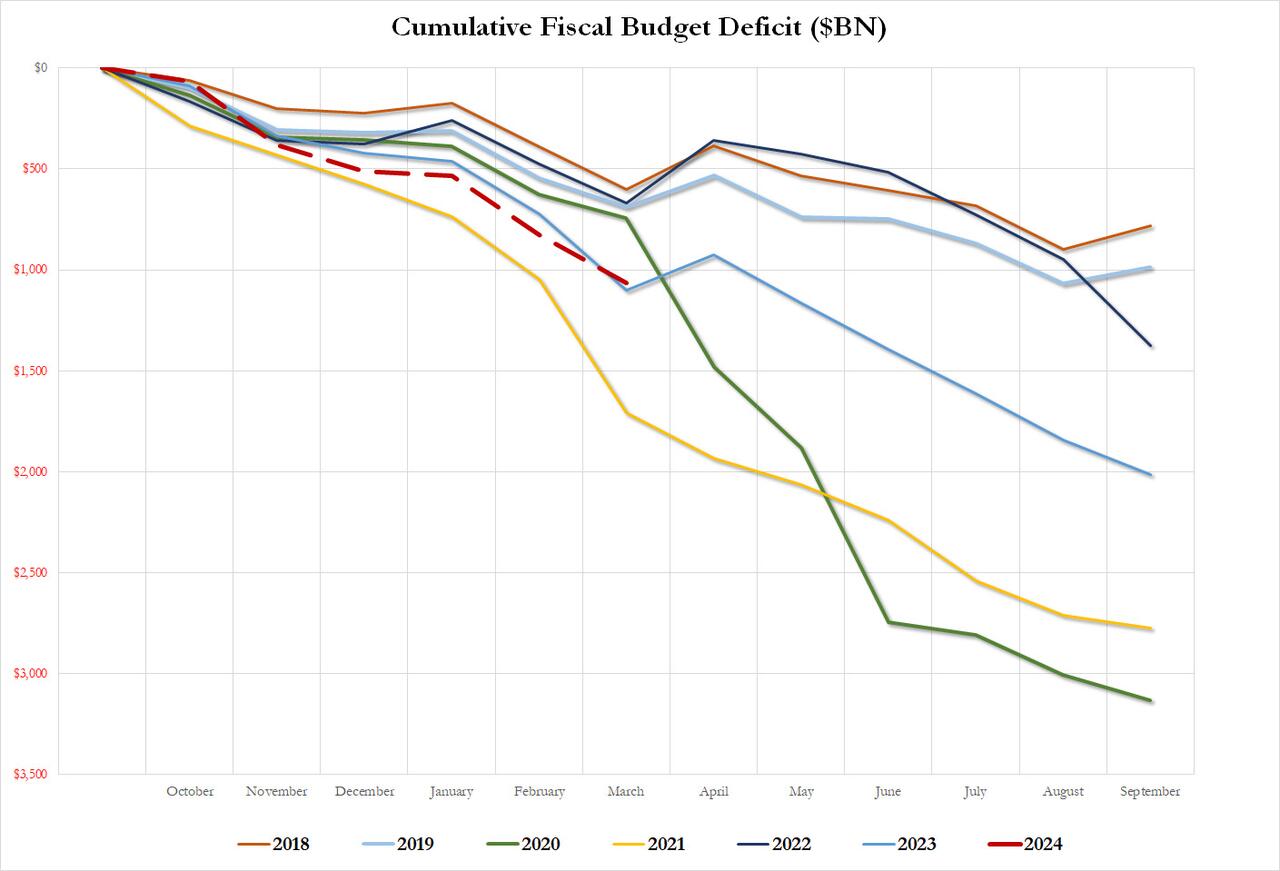

Putting the YTD deficit in context, in the first six months of fiscal 2024, the US deficit hit $1.065 trillion, just shy of the $1.1 trillion reached last year, which was the 2nd highest on record and only the post-covid 2021 was worse. Annualized, we expect total deficit to hit $2.2 trillion in fiscal 2024, a year when the US is supposedly “growing” at a nice, brisk ~2.5% pace. One can only imagine what the GDP growth would be if the US wasn’t set to have a wartime/crisis deficit…

… and we can’t even imagine what US deficit will be after the next recession/depression.

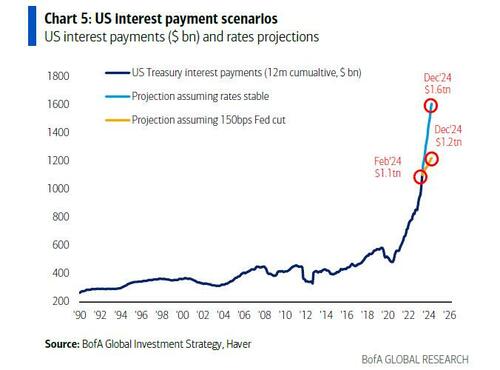

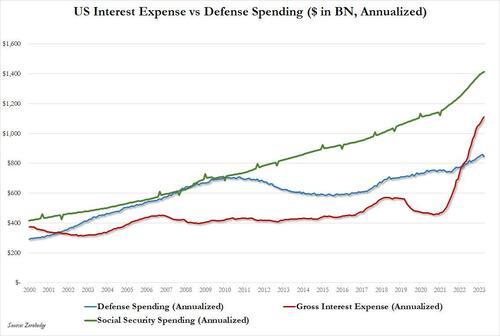

Meanwhile, as reported previously, total US interest continues to explode, and after surpassing total annual defense spending about a year ago, just the interest on US debt will soon become the single largest government outlay as it surpasses social security by the end of 2024, when according to BofA’s Michael Hartnett it hits $1.6 trillion…

.. and surpasses Social Security spending as the single largest spending category in the US government.

Biden has wanted to get rid of Social Security for a long-time and now wants to get rid of Medicare Advantage programs and put everyone on Medicare. Looks like Cloward-Piven!

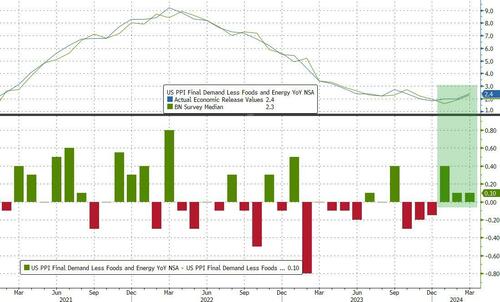

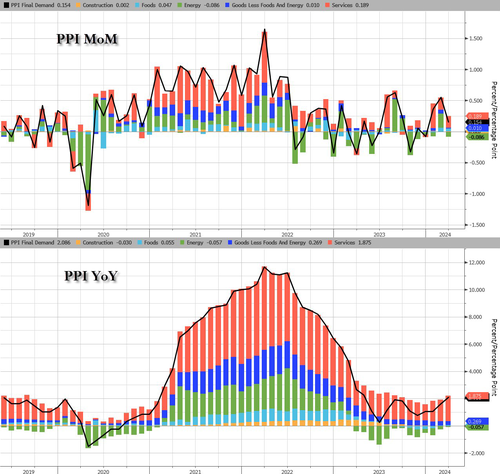

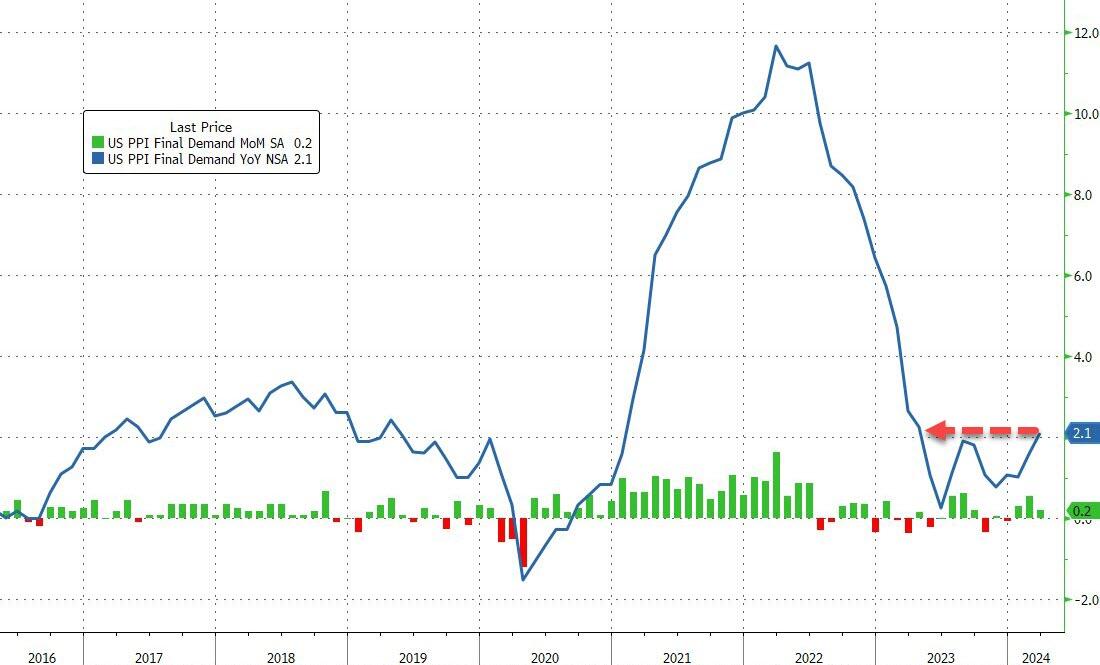

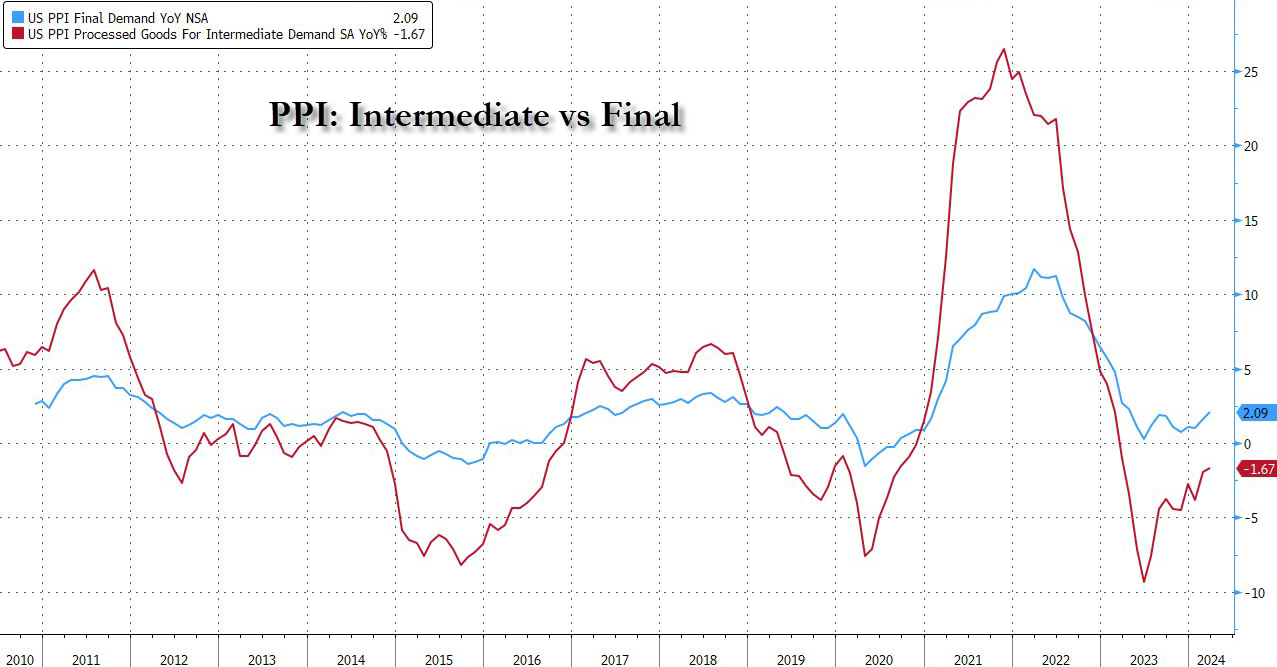

On top of skyroceting budget deficits, we have Producer Prices rising at fastest pace in a year in March.

After yesterday’s CPI-surge, PPI followed along, with headline producer prices rising 0.2% MoM (+0.3% MoM exp), pushing the YoY PPI to +2.1% (+2.2% exp) from +1.6% – the highest since April 2023…

Source: Bloomberg

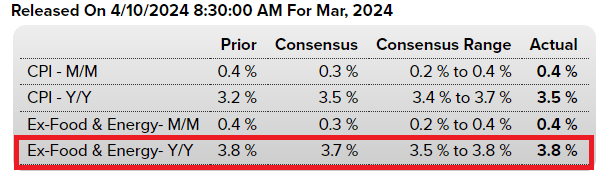

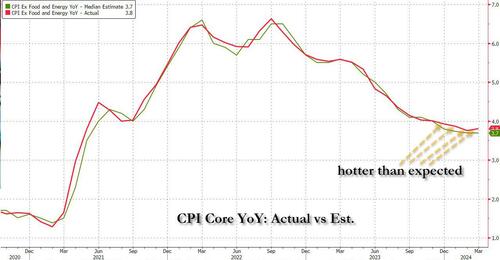

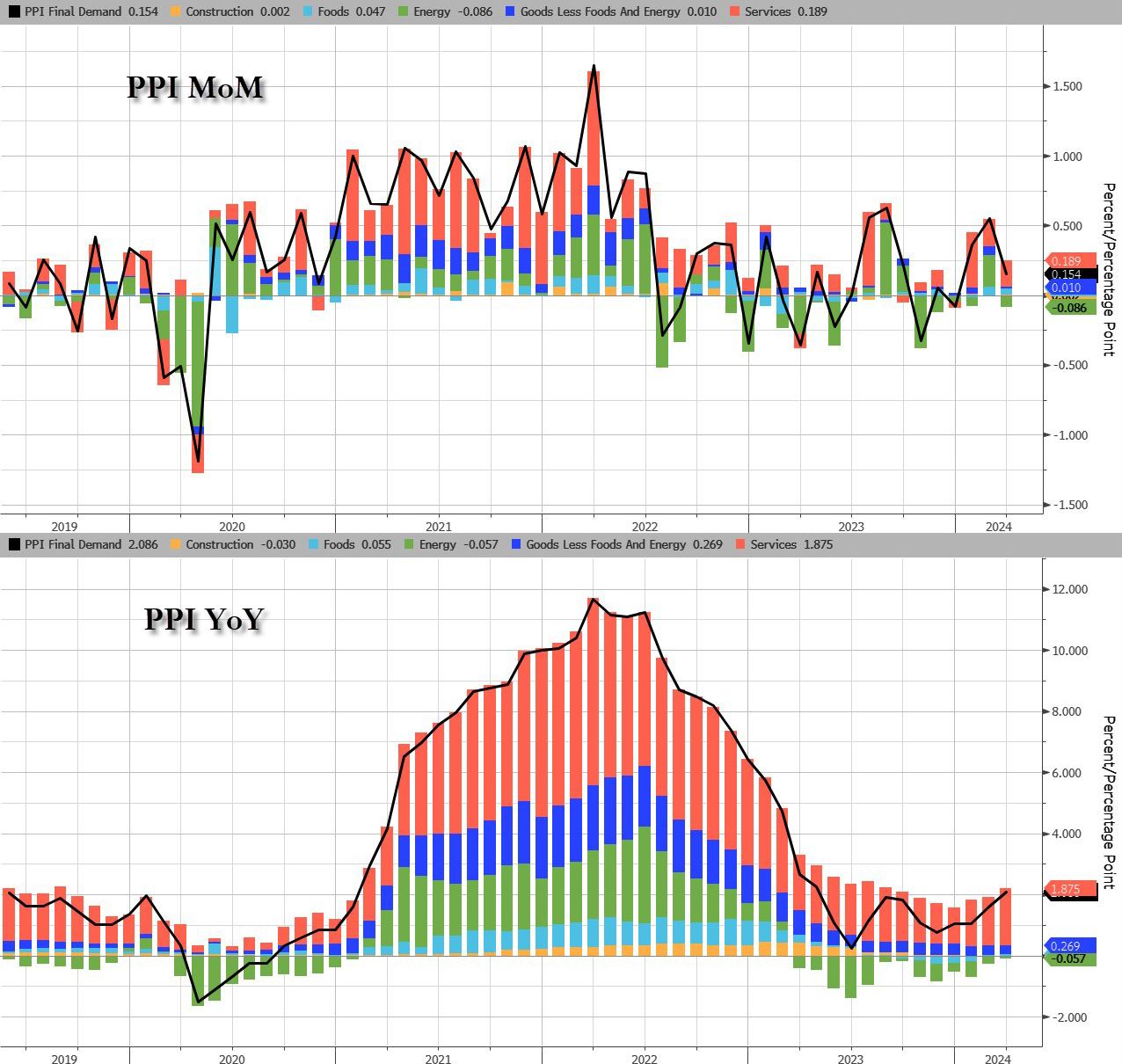

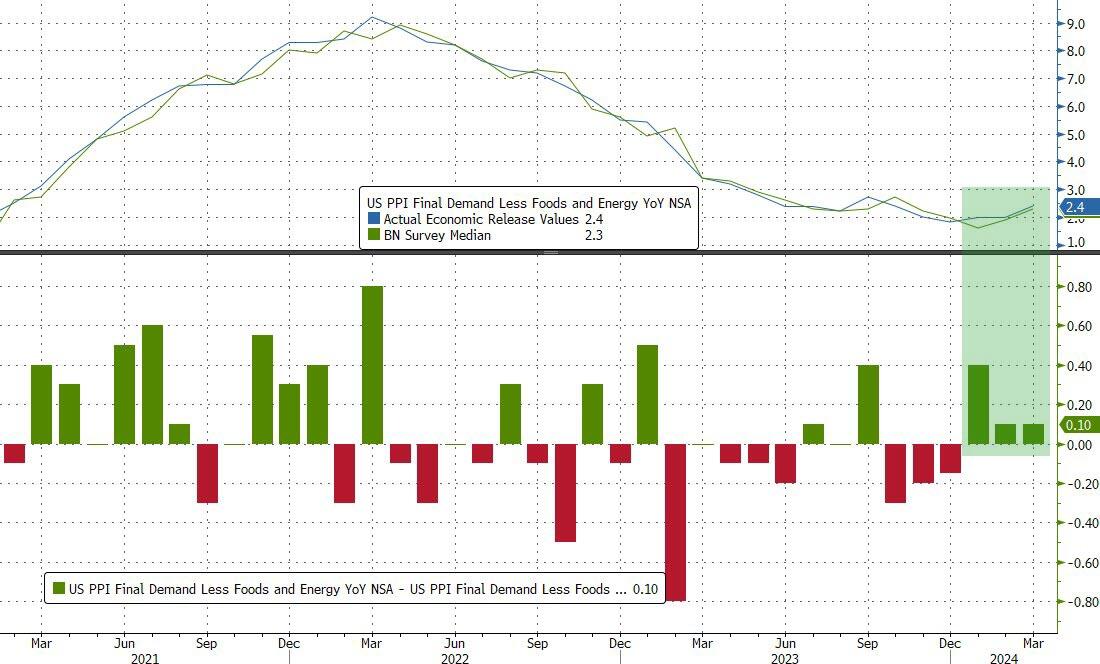

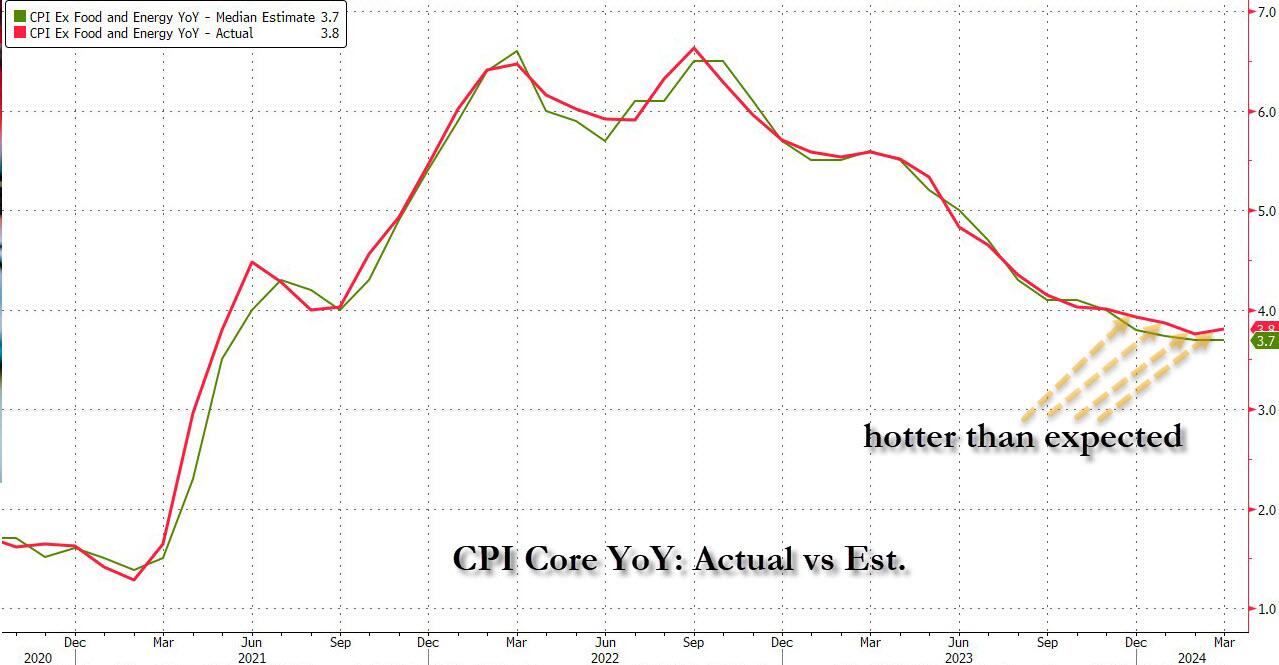

Core CPI rose 2.4% YoY (hotter than the expected 2.3%) – the third hotter-than-expected core PPI print in a row…

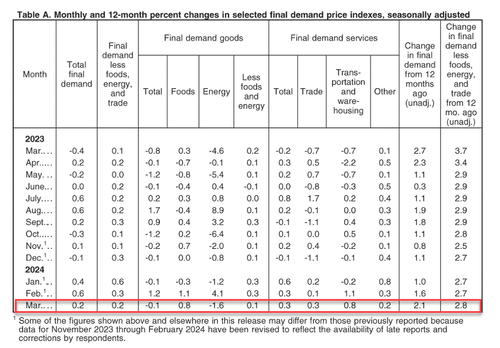

Under the hood, Services prices rose while goods prices declined MoM.

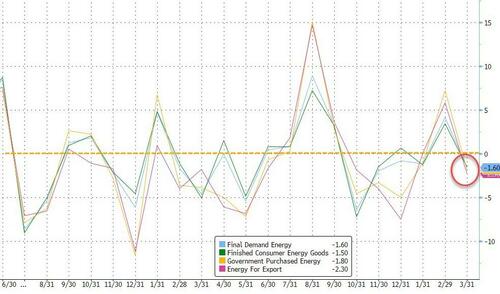

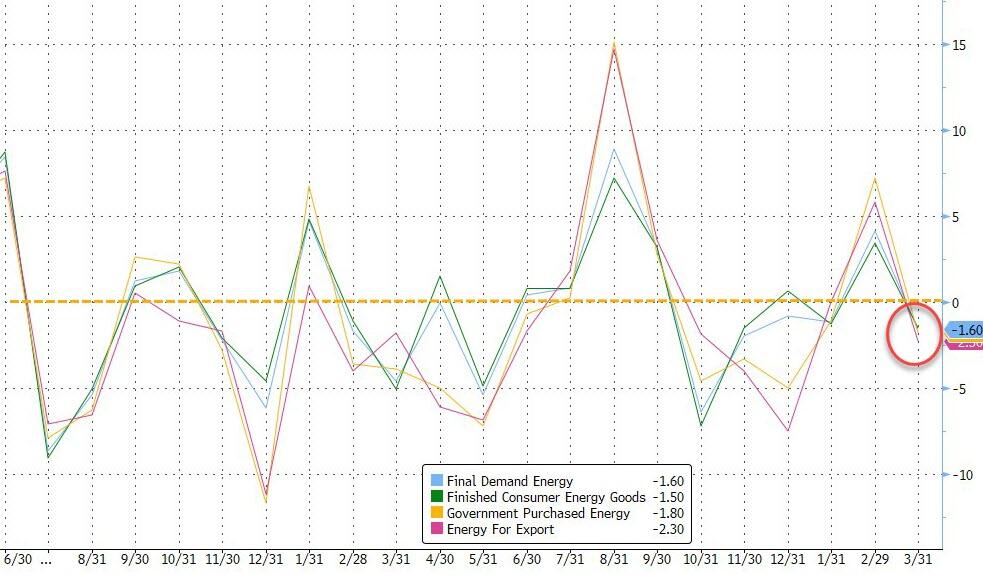

One thing that stands out as rather odd is the 1.6% MoM decline in Energy costs in the month… as prices soared for crude and gasoline?

Leading the March decline in the index for final demand goods, prices for gasoline decreased 3.6 percent…

And blame the markets for why the print was hot:

A major factor in the March increase in prices for final demand services was the index for securities brokerage, dealing, investment advice, and related services, which rose 3.1 percent.

And on a YoY basis, Services costs are accelerating…

Pressure continues to build in the inflation pipeline too…

While some may cling with grim hope to the ‘cooler than expected’ headline PPI print, core PPI is hot, damn hot, and headline PPI is rising. Not at all what The Fed, or Biden, wants to see – no matter how hard they spin it.

This is Victor Davis Hansen from Stanford’s Hoover Institute.

Funky cold Joe Biden is his reaction to inflation caused by his outragous spending. His legion of sycophants are now saying inflation is a good thing or don’t notice it. But Biden will never stop spending .

Coming into today’s CPI number, which followed three previous red-hot inflation prints, we said that it’s time for a “miss” (the first of 2024) not because the data demands it – on the contrary, prices continue to rise at a frightening pace – but because a dovish CPI print today would be the last opportunity for the Fed to set a timetable for a rate cut calendar ahead of November’s election.

Well, you can wave goodbye to all that, because we just got the 4th consecutive “inflation beat” in a row…

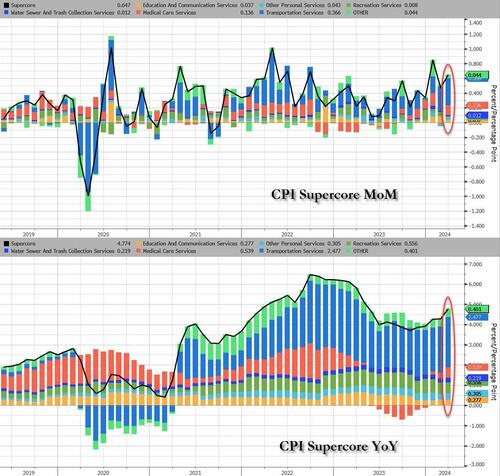

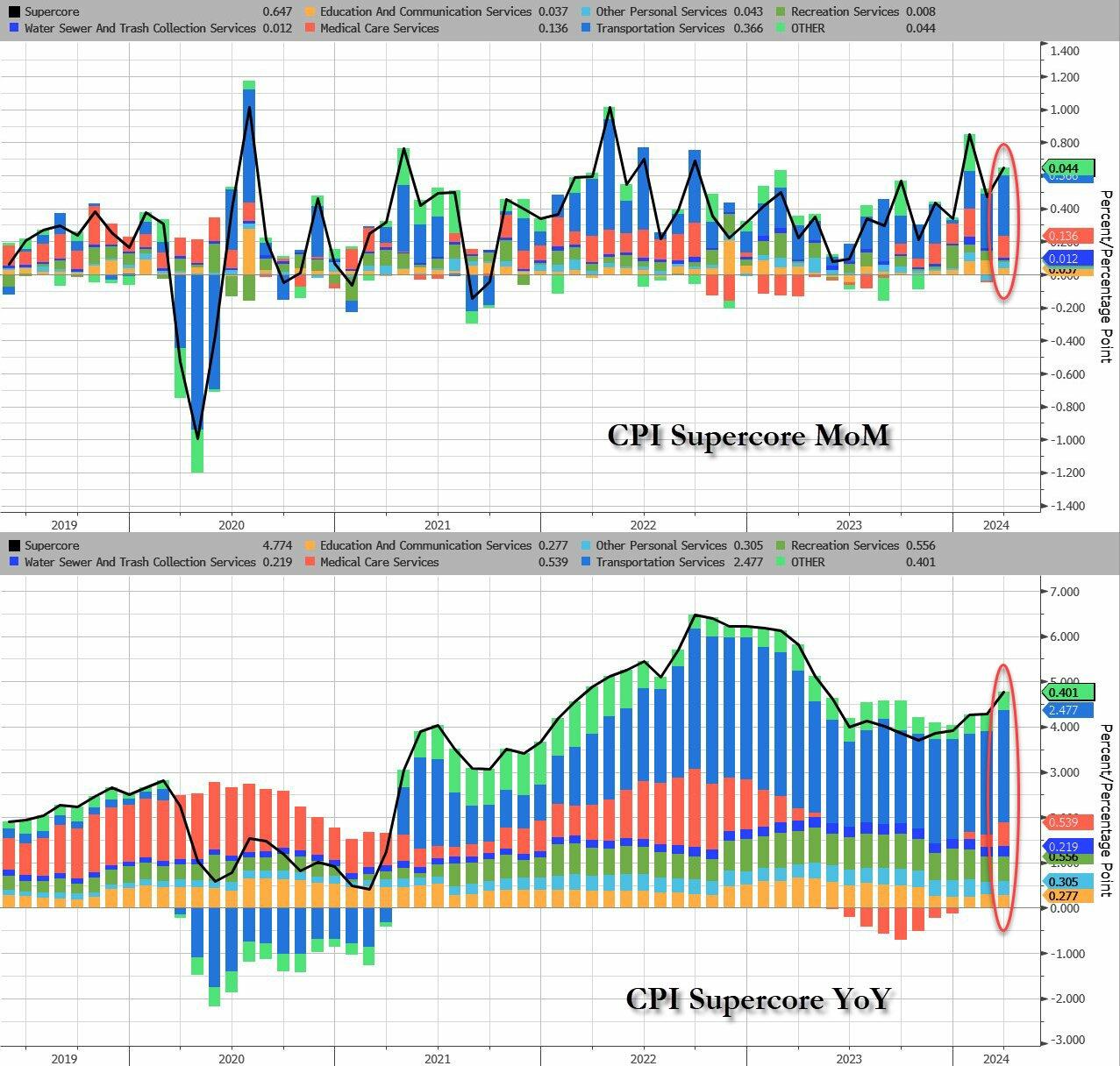

… with supercore inflation coming in blazing hot…

… thanks to a boiling inflation print which saw every single CPI metric coming in hotter than expected – was a shock, not because it reflected reality, but because it effectively sealed Biden’s fate because as Bloomberg’s Chris Antsey writes, “obviously, this is very bad news for Joe Biden… we’re approaching the point where high inflation is bound to still be in voters’ minds when they head to the polls, regardless of how the price figures come in over summer.”Easy financial conditions continue to provide a significant tailwind to growth and inflation. As a result, the Fed is not done fighting inflation and rates will stay higher for longer.”

It’s about to get even worse: recall today we have a $39 billion 10-year auction which is already being dubbed “sloppy” and a definitive break of 4.5% could easily extend if underwriting dealers are left holding the bag. As it stands, the 10yr has popped above the 4.5% parapet. Ian Lyngen at BMO Capital Markets says:“We expect the setup to the auction will break 4.50% in 10-year yields with ease.”

Obviously, this is very bad news for Joe Biden. It’s still only April, and we’ll have another half-a-year’s worth of inflation reports before the election. But we’re approaching the point where high inflation is bound to still be in voters’ minds when they head to the polls, regardless of how the price figures come in over summer.

Joe Biden continues to act like a gangsta giving away student loan forgiveness despite being told no by the US Supreme Court. As I said, Funky Cold Joe Biden. But Biden’s gangstaism favors the top 0.5% of net worth people, not the masses.

As Biden gropes for more voters, claiming he was raised in Puerto Rican, Greek, Black, and every other race on the planet, he probably sings “Ride The White Horse” to The Presidency. Reminiscint of Hillary Clinton claiming she kept a packet of hot sauce in her purse when talking to a black commentator.

We are living in the USA where corruption, favoritism, open borders and an out-of-control Federal budget and debt are destroying this once great nation.

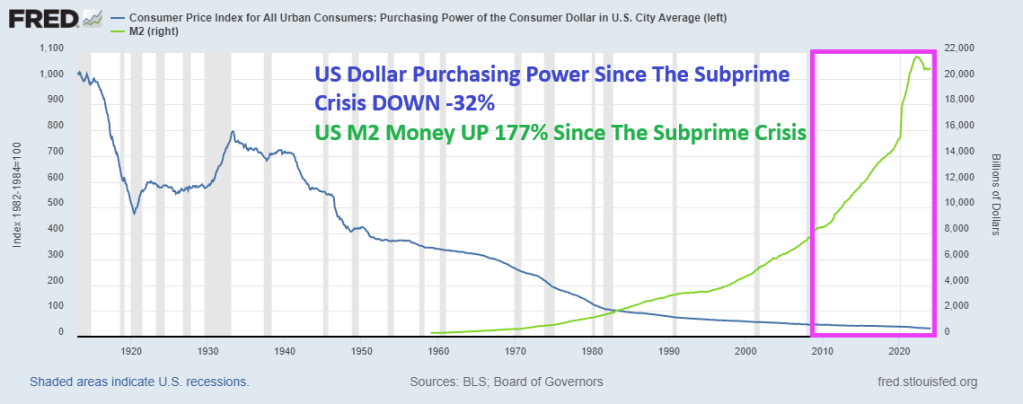

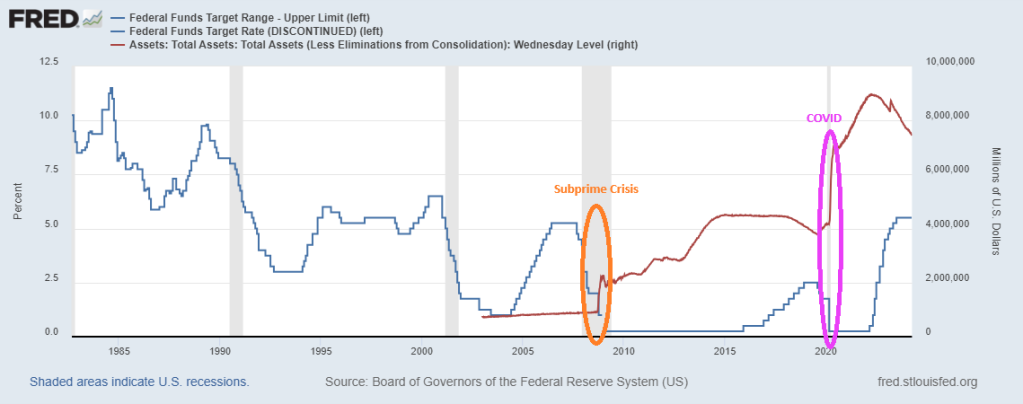

Former Kansas City Fed President Thomas M. Hoenig was absolutely right when he said recently that The Federal Reserve panders to Wall Street, Congress and special interest groups, prioritizing immediate relief over financial stability. Bernanke’s zero-interest rate policies (ZIRP) and Quantitative Easing (QE) were short-term fixes that never went away. Indeed, since the subprime mortgage crisis of 2008-2009, US Dollar purchasing power is DOWN -32% and M2 Money is up a staggering 177%. While Yellen stuck with zero-interest policies until Trump was elected, then raised The Fed Funds Target Rate 8 times. Yellen only raised the target rate once under Obama. Clearly playing political favoritism.

The Federal Reserve’s lack of transparency comes amidst reports that countries are removing their gold and other assets from the U.S. in the wake of the unprecedented Western sanctions imposed on Russia over its invasion of Ukraine. According to a 2023 Invesco survey, a “substantial percentage” of central banks expressed concern about how the U.S. and its allies froze nearly half of Russia’s $650 billion gold and forex reserves.Headline USA filed a FOIA request with the Fed for records reflecting how much gold the Federal Reserve Bank of New York currently holds in its vault, as well as records reflecting the ownership stake that each of FRBNY’s central bank/government clients have in that gold. The FOIA request also sought records about the Fed’s gold holdings prior to Russia’s February 2022 invasion of Ukraine. However, the Federal Reserve denied the FOIA request on Wednesday.

It influences the price of nearly everything, as well as the availability of jobs, the stability of our banking system, and the purchasing power of our money.

When the Fed Chair speaks, the entire world stops to listen.

But the average person has a poor understanding of how this colossally important entity operates. Or even why it exists.

And after a series of asset price bubbles — which some argue we’re in another one now — a chorus skeptical of the Fed’s actions has emerged.

So today we’re doing our best to shine as bright a light as possible on the Fed: how & why it operates, the good & as well as the shortcomings of its actions to date, what direction its policies are likely to take from here, and how all of this impacts the households of regular people like you and me.

Here are my top takeaways from from a speech by former KC Fed President Thomas Hoenig:

Dr Hoenig admits the Federal Reserve has experienced substantial “mission creep” since its creation as a lender of last resort. Its track record is very much “mixed” in terms of delivering on the intent of its policies. In Dr. Hoenig’s opinion, its efforts to add stability sometimes instead only create more instability.

While very critical of the Fed’s QE and ZIRP policies in the wake of the GFC, and more recently in the $trillions in monetary & fiscal stimulus unleashed post-COVID, Dr Hoenig thinks current Fed policy is “about right”. Though he expects the Fed to come under serious pressure soon as ebbing liquidity allows recessionary forces to build. He thinks the Fed will need to make an important decision within the coming year: return to QE and re-flame inflation, or allow a recession to occur.

Dr Hoenig criticizes the Federal Reserve for pandering to various interests, noting that short-term thinking and pressures from Wall Street, Congress, and interest groups often lead to decisions that prioritize immediate relief over long-term stability — a sort of “We’ll act now for optics sake and hopefully figure things out later”

In Dr Hoenig’s opinion, our fiscal policy is a runaway disaster. He criticizes both political parties of Congress for their roles in the cycle of ever-increasing deficits. Democrats advocate increased spending and tax hikes, while Republicans aim to keep taxes low but fail to curb spending. He warns of dire long-term consequences for future generations due to this impasse.

Dr Hoenig is very worried about the current stability of the banking system (and this from a former Direct of the FDIC!). He advocates for essential reforms to address government spending, prioritize essential areas without relying on future borrowed funds or inflationary measures, and communicate transparently with the public. He stresses the importance of reducing debt growth substantially below national income growth to avoid a full-blown crisis scenario in the future.

Dr Hoenig predicts the purchasing power of the US dollar (and other world fiat currencies) will continue to decline due to current policies and the lack of a “discipline” to money creation. Until such a discipline is restored (perhaps a return to some sort of hard backing of the currency), the dollar’s fall in purchasing power won’t abate.

Dr Hoenig suggests investing time in reading history and biographies as a valuable way to learn about leadership and gain insights into what strategies works and which don’t.

Here is the “Sound Money Parade” in 1896. By the aftermath of the subprime crisis, Janet Yellen (1993-2020) adopted the UNSOUND Money Fest, an orgy of printing and charging near zero interest rates. Powell in 2021 is ever-so-slowly unwinding The Fed’s balance sheet, but Powell has raised The Target Rate to its highest level since 1998 to fight inflation caused by Biden’s policies.

Combine The Fed not telling us how much gold they hold and their overprinting problems since 2008, and you can see why investors are turning to gold and silver and crypto currencies. The adoption of Central Bank Digital Currency (CBDC) is a step towards financial collapse.

Here is a parade you will NEVER see in Washington DC. A Sound Money Parade!

Powell is beginning to act like a sound money fan, but he still is taking his sweet time shriking the balance sheet.

I am thinking of fleeing to Lilliehammer Normay like Frank Tagliano.

Joe Biden (aka, BeelzeBiden) is really a piece of … work. His policies are helping drive prices through the roof, he seeks to protect deepstate employees against removal by Trump, had a disastrous withdrawal from Afghanistan and is getting the US engaged in possible hot wars in Ukraine (against Russia), open borders allowing US crime to spike, seems to be suppoporting Hamas over our long-time ally Israel, the list goes on. Biden’s big push for electric cars is a Socialist fantasty and simply unrealistick, drives up energy costs and is EXPENSIVE. It is like Biden is the demon Beelzebub from the TV show “Supernatural.” I once referred to Washington DC as “Mordor on The Potomac.”

Throw in the Federal Reserve operating outside their mandate (excessive interference in the financial crisis of 2008, the excessive interfernce after the Covid outbreak in 2020) and the two together are destroying the US.

Look at housing prices (up 32.5% under Biden) against the purcchasing power of the US dollar (down -16.1% under Biden).

The problem has gotten so bad that Sedona, Arizona, recently set aside a parking lot exclusively for these homeless workers. The city is even installing toilets and showers for the new occupants.

Apparently, the City Council thought installing temporary utilities was cheaper than solving the area’s cost-of-living crisis.

And what a crisis it is.

The average home in the city sells for $930,000, while most of the housing available for rent is not apartments, but luxury homes targeted at wealthy people on vacation.

With such a shortage of middle-class housing and with starter homes essentially nonexistent, low- and even middle-income blue-collar workers have nowhere to go at night but their back seat.

Much like America’s Great Depression in the 1930s, this marks a serious regression in our national standard of living. But shantytowns were not prevalent in the 1920s (a decade that began with a depression) or the 1910s. Nor were they ubiquitous following the Panic of 1907, which set off one of the worst recessions in American history.

Indeed, Americans in the Great Depression faced such a cost-of-living crisis that many were forced to accept a standard of living below what their parents and even their grandparents had.

Fast-forward about 90 years, and countless families are in the same boat. Many young people today don’t think they’ll ever be able to achieve the American dream of homeownership that their parents and grandparents achieved. The worst inflation in 40 years, rising interest rates, and a collapse of real (inflation-adjusted) earnings mean a huge step backward financially.

That inflation has pushed up rents so much that young Americans are moving back in with their parents at rates not seen since the Great Depression because they can’t make it on their own. Sometimes, they can’t even make it with multiple roommates.

But many people cannot move back in with family, so the car it is.

The housing problem is not limited to wealthy towns in Arizona, however. It is systemic. The monthly mortgage payment on a median-price home has doubled since January 2021, and rents are at record highs. Like the Great Depression, this disaster stems from impolitic public policy.

For the past several years, the government has spent, borrowed, and created trillions of dollars it didn’t have. The predictable result of this profligacy was runaway inflation, followed by equally foreseeable interest rate increases.

The deadly combination of high prices and high interest rates has frozen the housing market and reduced homeownership affordability metrics to near-record lows. In several major metropolitan areas, it takes more than 100 percent of the median household after-tax income to afford a median-price home.

Since rents and virtually all other prices have risen so much faster than incomes over the past three years, even renting is unaffordable today, so many people have to go into debt to keep a roof over their heads. And for some, that’s a car roof.

This is the kind of story you might expect from a Third World country or somewhere behind the Iron Curtain during the Cold War, not the largest economy in the world—at least not outside of a depression like the one in the 1930s.

Hoover certainly deserved some blame for the Great Depression, but so did the progressives in Congress, who came from both parties and repeatedly voted to meddle in the economy instead of allowing it to recover from the initial downturn.

Similarly, President Joe Biden deserves blame for constantly advocating runaway government spending. (Runaway Joe??)

But today’s multitrillion-dollar deficits are also made possible by the big spenders in Congress, who come from both parties.

If this bipartisan prodigality of Washington continues, Bidenvilles will only become more widespread as the housing affordability crisis worsens.

Biden’s official White House portrait.

Washington DC under Biden and Schumer, Pelosi, etc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.