Biden Press Secretary KARINE JEAN-PIERRE: “The American people are beginning to feel Bidenomics”

Prices are up 16.6% and real wages are down 3% since Biden took office.

Well, at least Jean-Pierre didn’t claim like her boss Joe Biden claimed that he “ended cancer as we know it.”

But getting back to Jean-Pierre’s claim that “The American people are beginning to feel Bidenomics.” She is right (for once). Americans are REALLY feeling Bidenomics. And it hurts SO BAD!!!

What hurts so bad? Food (CRB Foodstuffs) are up 56% under Bidenomics. Real weekly wage growth is down -90% since Biden assumed office. Regular gas prices are up 52%. And the 30Y mortgage rate is up a staggering 153%. Yes, Karine, this hurts so bad!

While real wages are down -3% under Biden and the real average weekly wage growth is down -90%. That REALLY hurts so good.

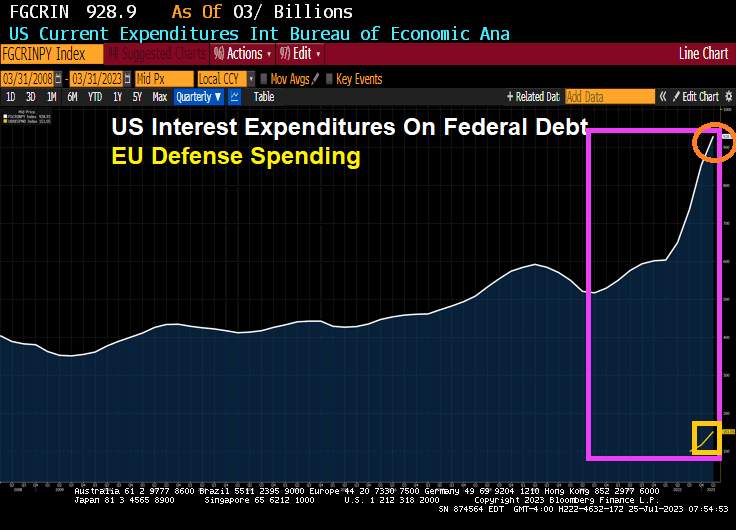

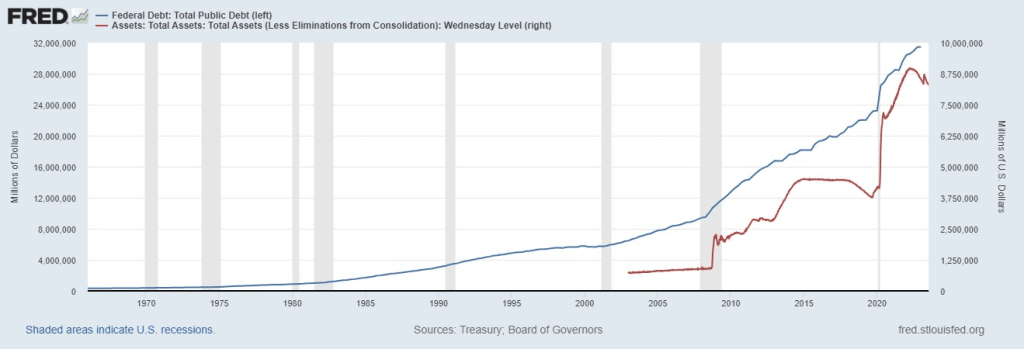

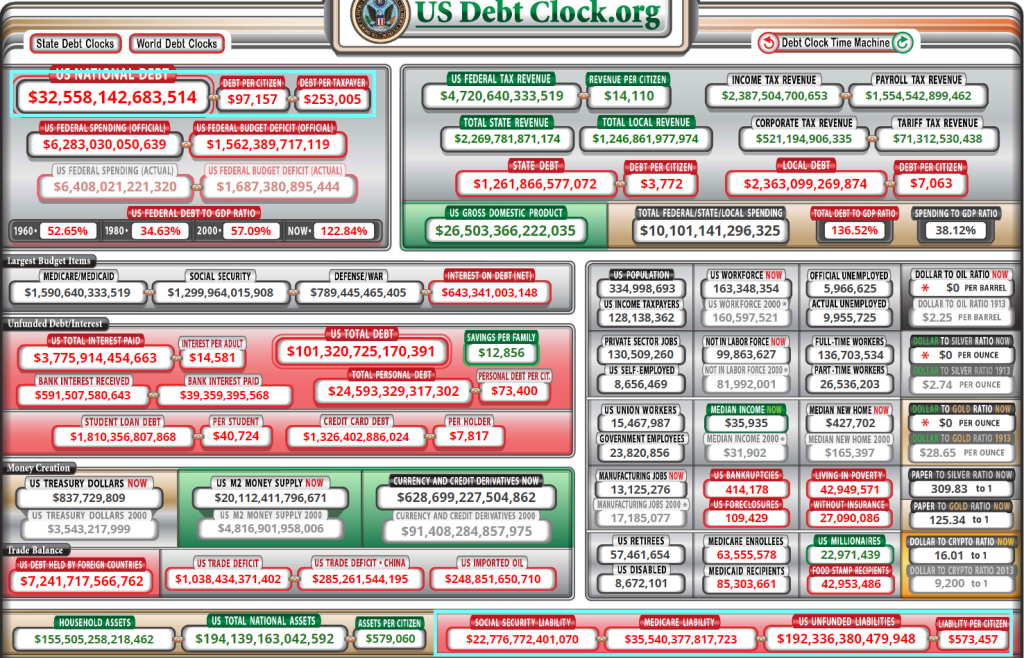

How badly has Bidenomics and generally Federal spending has crippled the US? An example. The interest on US Federal debt is approaching $1 TRILLION (and Biden/Democrats REFUSE to cut any spending, not that Republicans are much better). To show up how messed up this is, the EU’s defense budget (remember Ukraine?) is far smaller that the US interest payments on their debt. That is, US interest payments alone on the massive Federal debt of over $32 trillion is over 6 times larger than the entire defense budget for the European Union!

How this all works, considering the nation’s technically insolvent, is quite miraculous. But it works, nonetheless. Again and again, the Treasury borrows money. And Washington spends it.

Yellen likely knows that full faith and credit is too good to be true. The U.S. government’s gross fiscal mismanagement should call the veracity of its notes into question. But why focus on it when there’s an abundance to be acquired from weekly Treasury bill auctions?

On a recent trip to China, Yellen was spotted by a local food blogger consuming a plate of magic mushrooms. An aide to Yellen later confirmed that she did, indeed, order them. The restaurant’s “staff said she loved [the] mushrooms very much. It was an extremely magical day.”

We don’t know what their acute effects on Yellen were, while she was in Beijing. But the mushrooms appear to be contributing to her chronic hallucinations about the U.S. economy’s current health. This week, for example, while attending the G20 meeting in India, Yellen remarked:

“For the United States, growth has slowed, but our labor market continues to be quite strong. I don’t expect a recession. The most recent inflation data were quite encouraging.”

These, no doubt, are the fantasies of a person under the influence of mind-altering chemicals. Either that, or her mind has turned soft over decades of working as a professional economist for the Federal Reserve and the Treasury.

Tempered Perspective

The unemployment rate reported by the Bureau of Labor Statistics (BLS) is, in fact, just 3.6 percent. Yellen can celebrate the data point. But the quality of the jobs being created is not the type that will drive economic growth.

Higher-paying technology and finance jobs are being purged. While leisure, hospitality, and government are the sectors contributing to employment growth. These jobs may be important. Still, they will not create new wealth or help America compete with its global rivals.

Yellen, while under the influence, also remarked that she doesn’t expect a recession. Maybe this is why you should expect one.

Her predictive acumen has missed the target in the past. If you recall, in 2017 she said she did not believe another financial crisis would happen in our lifetime. Since then, we’ve had one financial crisis after another, including the most recent bank failures this spring.

Just this week, Bank of America reported its bond losses in the second quarter increased $7 billion to nearly $106 billion. And Starwood Capital Group just defaulted on a $215.5 million mortgage on an Atlanta office tower. Probably nothing to worry about, right?

In addition, this week Taiwan Semiconductor Manufacturing Company (TSMC), the mega chip maker, reported its first profit drop in 4 years. Revenue slipped 10 percent from a year ago. What’s more, net income fell 23.3 percent. Wasn’t AI supposed to drive silicon wafer production to commanding heights?

With respect to what Yellen called ‘encouraging inflation data’. While under the influence, she was likely referring to the recent CPI report from the BLS, which showed that in June, consumer prices increased at an annualized rate of 3 percent. This is still 50 percent higher than the Fed’s arbitrary inflation target.

Moreover, the energy commodities component showed a 16.7 percent price decline over the last year. This has coincided with President Biden draining the Strategic Petroleum Reserve to a 40-year low. Without these short-sighted actions, the current inflation data would be much less encouraging.

Structural Crisis

In short, the U.S. economy’s prospects do not quite align with Yellen’s positive outlook. And if you look out further than just the current data reports, you’ll be greeted with a structural crisis of significant consequence.

In fact, simple arithmetic quickly reveals the precarious predicament the 118th Congress is putting the American people in.

The Treasury Department, the agency Yellen oversees, recently reported that for the first 9 months of the 2023 fiscal year, the federal government ran a budget deficit of nearly $1.4 trillion. That’s a 170 percent increase from the same period last year.

The big surprise, however, was that interest on Treasury debt securities for the first 9 months of FY2023 topped $652 billion. A 25 percent increase for this period a year ago.

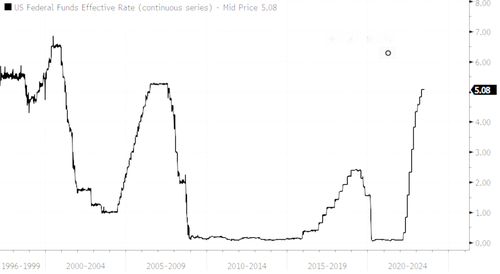

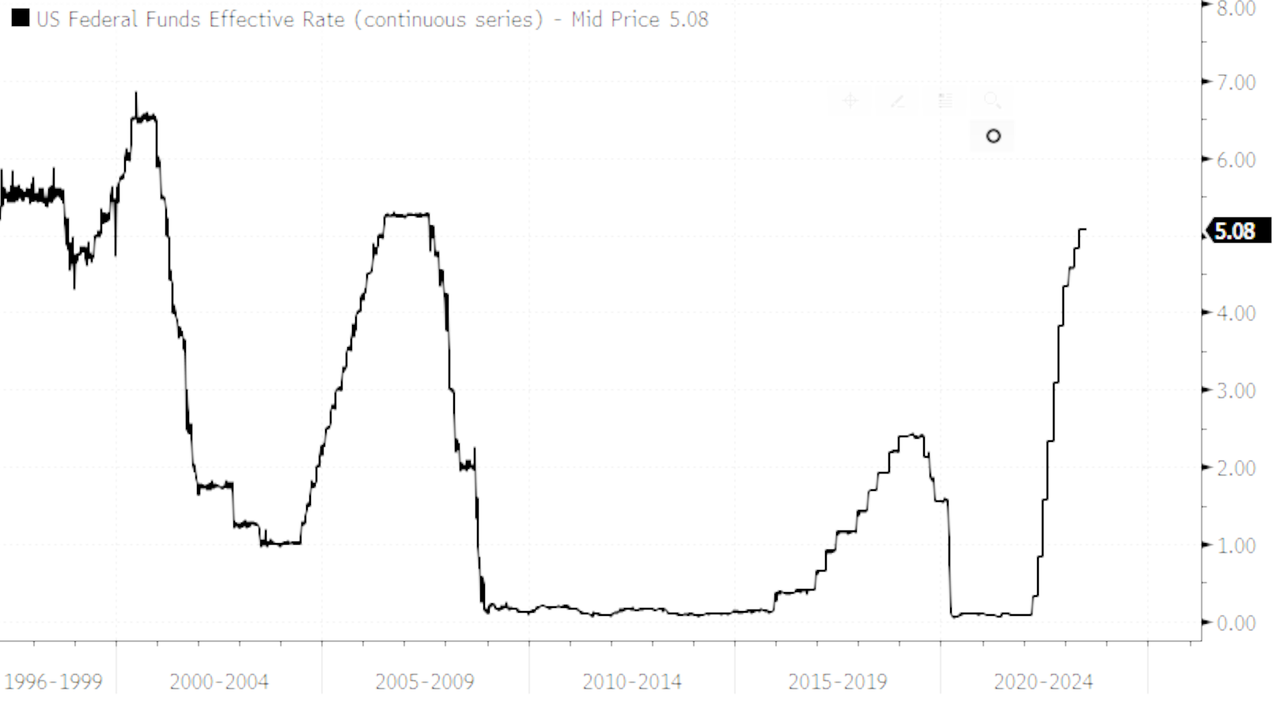

Rapid and repeated interest rate hikes by the Fed to contain the raging price inflation of its own making, has blown out the interest owed on Treasury debt. Anyone with half an inkling knew this was coming from miles away.

The growth of federal debt has been out of control for decades. But the rate of debt growth in the 21st century has rapidly accelerated.

The solution that’s commonly offered by the politicians for getting a handle on Washington’s debt problem is for the economy to somehow grow its way out. Countless policies over the years have generally involved borrowing money from the future and spending it today.

Yet economic growth never manages to outpace the debt increases. Instead, the debt piles up higher and higher with each passing year. The simple fact is you can’t grow your way out of debt when the debt’s increasing faster than gross domestic product (GDP).

For example, in 2000 the federal debt was about $5.6 trillion, and U.S. GDP was about $10 trillion. Today, the federal debt is over $32.5 trillion, and GDP is about $26.5 trillion. In just 23 years the federal debt has increased by over 480 percent while GDP has increased just 165 percent.

How Washington Ruined America’s Future

Recently, the Peter G. Peterson Foundation attempted to characterize the $32 trillion federal debt. The number is so large it is difficult to comprehend. Here is some of what the foundation came up with:

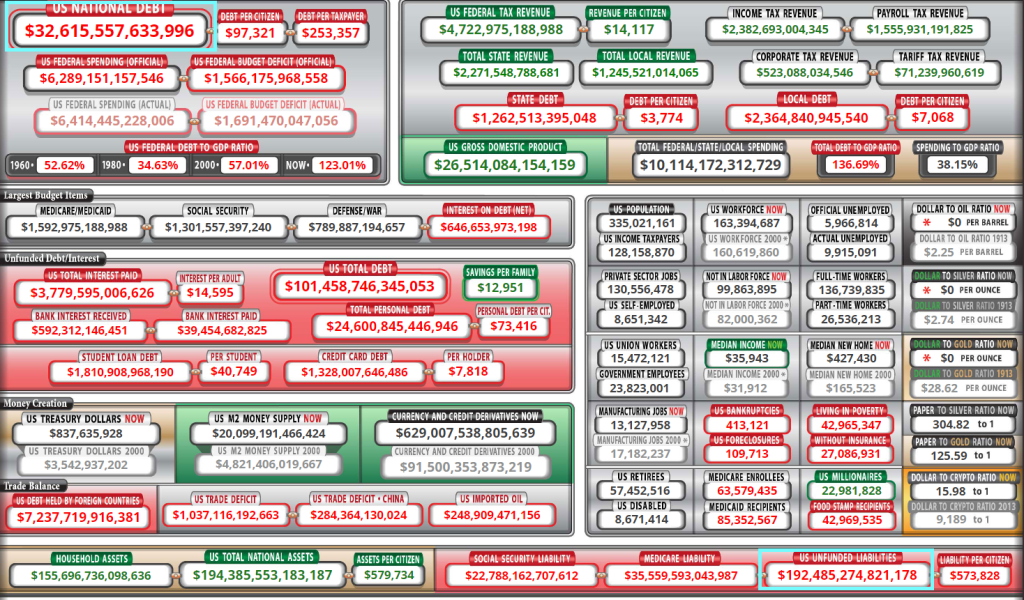

The $32 trillion debt is more than the combined values of the economies of China, Japan, Germany, and the United Kingdom. It represents $244,000 per household or $96,000 per person in America. And if every household contributed $1,000 per month towards paying down the national debt it would take over 20 years.

Without question, Washington has run up an impossible tab. Yet, what does it have to show for all this recklessness?

America’s cities are decaying from the inside out. The infrastructure is crumbling. The country has been involved in one overseas quagmire after another. And the populace is struggling with gender identification pronouns.

The political will to stop this massive debt pileup has been nonexistent. Democrats and Republicans have both spent like drunken sailors. There’s been no tradeoffs or compromises to cut spending. There’s been zero effort to balance the budget. And now it’s too late.

As mentioned above, interest on Treasury debt securities for the first 9 months of FY2023 topped $652 billion – a 25 percent increase from a year ago. But this is just the beginning.

As interest rates continue to rise, the annual interest on Treasury debt will soon pass $1 trillion. That would put this line item at par with outlays for Social Security, the U.S. government’s largest expenditure.

This would also put spending on interest payments above the combined spending of research and development, infrastructure, and education.

Consequently, by repeatedly borrowing and spending money, piling up massive debt, and then being forced to jack up interest rates, Washington has ruined America’s future.

Yippee! Look Ma, no hands! The face of America decline: Former Fed Chair Janet “Too Low For Too Long” Yellen who is now our woefully inept Treasury Secretary. You know, the Treasury Secretary who bowed three times to a Chinese Communist Party leader.

A reminder of the pickle that our politicians have put us in. US Federal debt is at $32.62 TRILLION … and UNFUNDED LIABILITIES (Social Security, Medicare, Medicaid, etc) are at $192.5 TRILLION!!! Yes, the US economy is broken beyond hope of repair, yet dunce voters keep reelecting imbeciles like Joe Biden, Chuck Schumer, John McConnell, etc.

Jared Bernstein was VP Joe Biden’s former Chief Economist and is now chair of the United States Council of Economic Advisers. Pretty impressive! Except that Bernstein is not really an economist. He has a PhD in social welfare from Columbia University. In other words, Bernstein is a Progressive Marxist cheerleader, not a real economist. Perfect for The Biden Adminstration where they installed a small town Mayor with no experience (Buttigieg) as Transportation Secretary.

BERNSTEIN: “Yes, it depends on what your benchmark is.”

Bernstein’s answer reminds me of the infamous reply of President Clinton about having sex in the Oval Office with Monica Lewinsky: “It depends on what the definition of sex is.”

Well, Jared, here is the data.

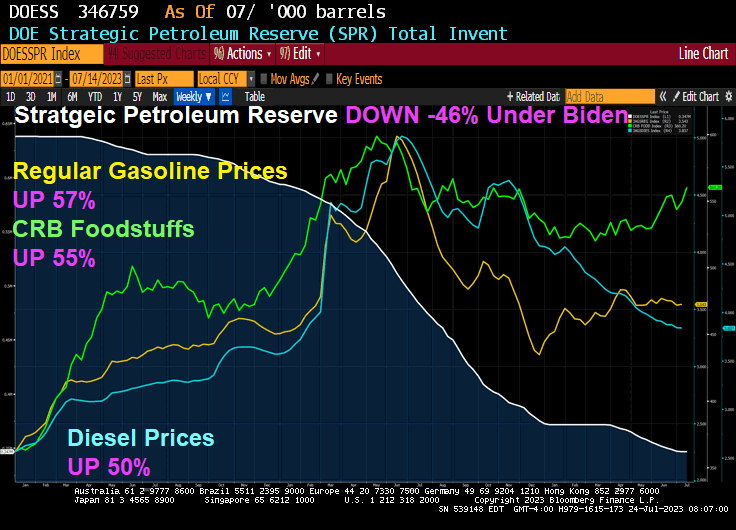

Since January 2021, regular gasoline prices are up 57% under Biden’s and Bernstein’s Reigns of Error. CRB Foodstuffs are up 55% under Clueless Joe and Diesel prices 50% under Bully Biden. Meanwhile, the Strategic Petroleum Reserves is DOWN -46% under Hidin’ Biden.

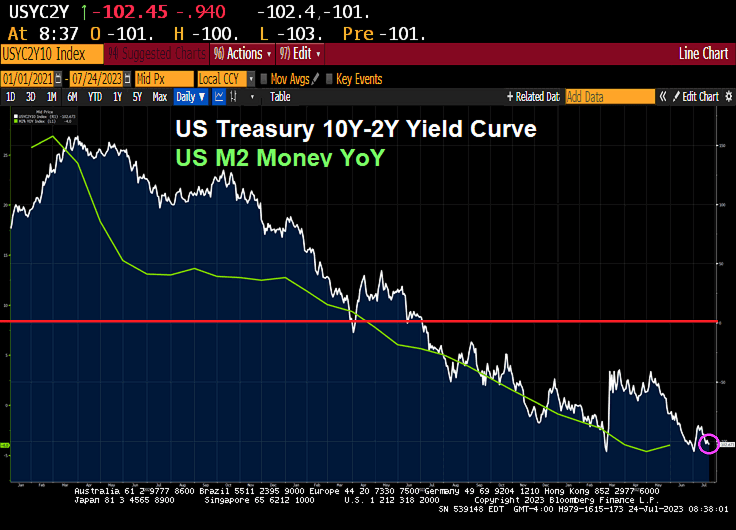

Meanwhile, the US Treasury 10Y-2Y yield curve has inverted to -102.45 as it does prior to a recession. I would love to hear “economist” Jared Bernstein explain that!

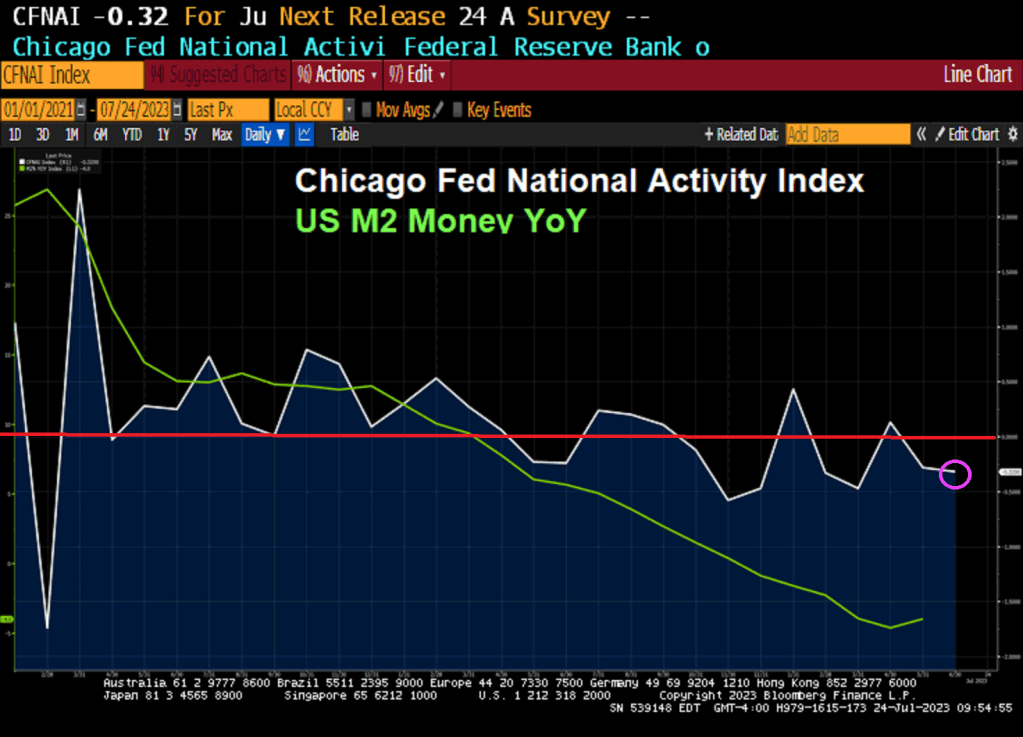

The Chicago Fed’s National Activity index fell to -0.32 in June. That is negative readings for 6 of the last 8 months.

The Fed still hasn’t removed its monetary stimulypto from the market.

No, this isn’t a John Kerry/Greta Thunberg hysterical warning about climate change. But a storm created by 1) Biden/Congress spending splurge and 2) excessive monetary stimulypto by The Federal (Feral) Reserve. Now that The Fed is withdrawing the excess stimulus, we are seeing a world of pain for commercial real estate. A financial climate change!

“We’re in a Category 5 hurricane,” Sternlicht said in an interview on June 28 taped for a July 25 release in an upcoming episode of Bloomberg Wealth with David Rubenstein.

Sternlicht warned, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

He explained the CRE downturn was sparked by the Federal Reserve’s sixteen months of aggressive interest rate hikes to tame inflation — and unlike past downturns — not due to reckless speculation.

Tighter credit conditions following the regional bank crisis in March have made refinancing existing buildings exceptionally hard for landlords and come as vacancies rise.

Sternlicht recalled that his firm tried to obtain a bank loan for a small property not too long ago. He said his staff reached out to 33 banks, and only two came back with offers.

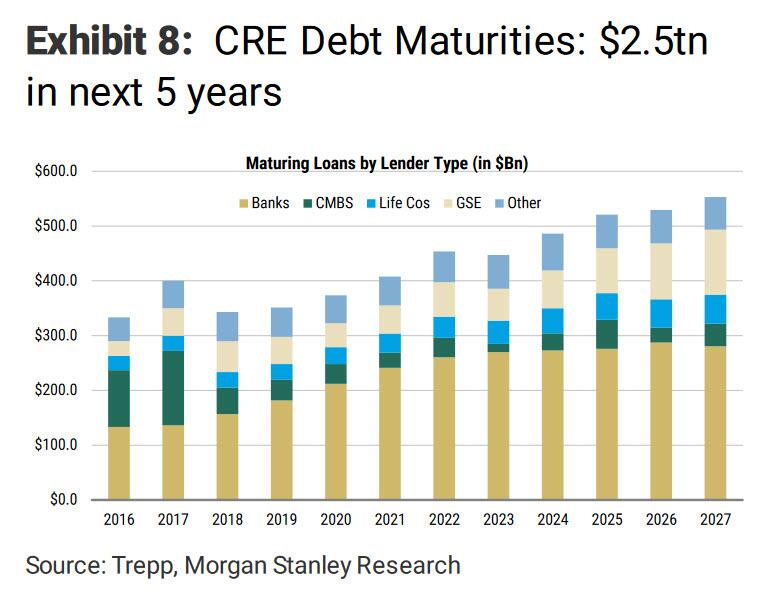

According to Morgan Stanley, the elephant in the room is a massive debt maturity wall of CRE loans that totals $500 billion in 2024 and $2.5 trillion over the next five years.

As we’ve seen in San Francisco, the inability to refinance as some properties sustain rising vacancies will pressure landlords to sell properties or walk away from them.

Sternlicht said there’s a very real possibility of a “second RTC” event playing out, referring to Resolution Trust Corp., the government entity that led the effort to liquidate assets of the savings and loan associations that failed three decades ago.

“You could see 400 or 500 banks that could fail,” he said. “And they will have to sell. It also will be a great opportunity.”

Sternlicht launched his real estate firm during the era of RTC, purchasing multi-family units and flipping them to billionaire Sam Zell 18 months later for triple the price.

Sternlicht said the Federal Deposit Insurance Corp would likely begin offloading CRE loans on Signature Bank’s books, which failed in March. He said, “The government’s going to prop up the value of that portfolio by providing very cheap financing to it.”

* * *

Transcript of the interview:

David Rubenstein:

Sometimes people are saying that the best investment opportunity now is distressed real estate debt — that you can buy the debt from banks at a discount. But do you think it’s too early for that?

Barry Sternlicht:

You know, we were gonna give back an office building. And they said, “Well, not so fast. If you want to, we’ll restructure the loan. And we’ll cut the loan in half. And you put the money in here. And we’ll take this as a junior note.” Because the banks don’t want the assets back. They’re not set up to carry these assets. It’s not their business.

So you’re beginning to see stuff. We’re going to see this big trade of the [Signature] Bank portfolio. That’s going to be a benchmark for market.

David Rubenstein:

A lot of fortunes were made in the real estate world in’ 07-’08 when people bought distressed real estate. The late ’80s too, when the RTC was here. Do you see funds being formed to buy these assets? But you think they won’t be available for a year or two?

Barry Sternlicht:

Right now you have an unusual situation in the real estate markets because everyone’s sort of looking at the yield curve. And it says rates will be lower later. Everyone says, “You know, survive till ’25. Hold onto your assets.” So transaction volumes have plummeted.

Unless you have to sell something today, nobody wants to sell anything today. They think tomorrow will be rosier. So for the most part, everybody’s pushing any sales back. But what you’re seeing is when a loan is maturing and a borrower can’t cover the current debt service. Something’s gotta give. Unfortunately, we’re also a lender.

David Rubenstein:

Are we going to change the way office buildings are really valued in the future because tenants aren’t going to need as much space? Or do you think eventually the tenants will come back and the employees will come back?

Barry Sternlicht:

The work-from-home phenomenon is a US phenomenon. If you go to England or Germany, rents are up, and vacancy rates in the top German property markets — Berlin, Frankfort, Munich, Hamburg — are less than 5%. People are back in the office. You and I go to the Middle East, they’re full. We have offices in Asia, they’re full. So this is a US situation.

In the US you have two markets. The nice buildings will stay rented and my guess is at pretty good rates. And the B and C stuff is going to be — maybe fields of grain or something. It’ll be very pretty. We’ll have all these little mid-block parks in New York City because there won’t be anything else to do with those buildings.

The other thing about office is AI. AI is going to hit a couple of these industries that have been big users of office space. So that’s sort of a big question mark in the investment equation.

David Rubenstein:

Let’s suppose I’m an average person. Where should I put my money as an investor in real estate?

Barry Sternlicht:

High interest rates are depressing the number of single-family home units that have been built so now you’re having an ever-increasing scarcity of residential. Given the cost of construction, the whole residential complex — including single-families for rent, multi-family, the housing market, even residential land — I think they make interesting investment opportunities today.

David Rubenstein:

Is it a good thing for people to now invest in a real REIT?

Barry Sternlicht:

I think real estate has a nice place in the balance sheet of any individual. In the pandemic, we raised a special-situations fund and bought 15 names in the REIT business, and we were up, like 70% at one point. We’re going to do that again. And if you take a long-term view, some of these are good companies with the wrong interest-rate environment. I wouldn’t even say they have the wrong balance sheet, but they are so out of favor. There are some really good buys out there. So if you’re clever, you could buy some public REITs.

David Rubenstein:

What kind of return should an average REIT investor expect?

Barry Sternlicht:

In the mortgage REIT, Starwood Property Trust, we’re paying a 10% dividend. So you get that and any appreciation in the stock, and the stock’s currently trading below book value. It usually trades above book value. It used to trade at 1.23 times and now it’s trading at .9. So if it reverts, you’ll get a 15% return. We’ve averaged 11.3% over 10 years.

David Rubenstein:

Why should somebody want a career in real estate? Why is that a good business to be in?

Barry Sternlicht:

You’ve got to find niches, and there are a lot of niches in real estate. And it’s very micro, block by block. If I didn’t have my firm today, could I buy — even in a city like New York — and redo apartments and housing. I could make money doing that. I have a friend of a friend who’s bought 300 homes. He turned living rooms into bedrooms, put them all on Airbnb. He’s earning a fortune and using Airbnb as his distribution set. It’s a giant industry. There’s always something to do.

David Rubenstein:

You were based in the northeast part of the US for much of your career. You grew up in Connecticut, you were born in Long Island. But you picked up and moved to Miami. Why did you do that a few years ago? And any regrets about moving to Miami?

Barry Sternlicht:

Well, my mom’s down there. And I got divorced. That was one reason. Change your life, start over. There was obviously a tax benefit to doing so. And I had sold an interest in my firm at the time. I was based in Connecticut. I was based in Greenwich, our headquarters was there. I looked at my travel calendar in a normal year and I was only home for about a third of it. So I didn’t think it’d be that hard to move and make that my base of operations. It turned I caught the wave perfectly.

I was an early settler into Miami. And, you know, the home prices probably tripled there. I should have bought everything with my house. I would have had the best-performing real estate fund in the world.

David Rubenstein:

If your mother came to you and said, “I have $100,000. I need to invest it somewhere. Where should I invest it?” You would say where, real estate?

Barry Sternlicht:

Today if you look at my portfolio, I have a significant amount of cash that I never had before because I’m getting 5% for the cash. Pretty soon I’m going to just start deploying that capital when I can see the sun coming through the clouds of the Fed’s movement. When the Fed basically tells you they’re done, I think real estate will catch a very firm bid.

Greta Kerry? John Thunberg?? They are the same repeater, and non thinker.

Here the real (financial) climate terrorists!! Yellen and Powell.

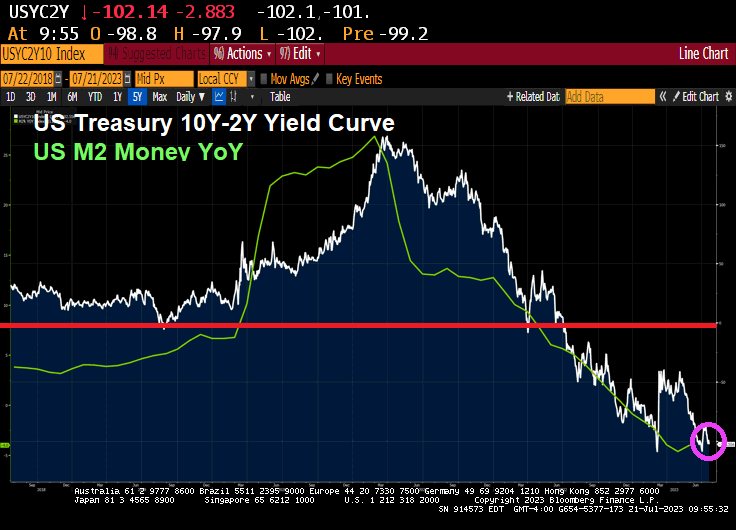

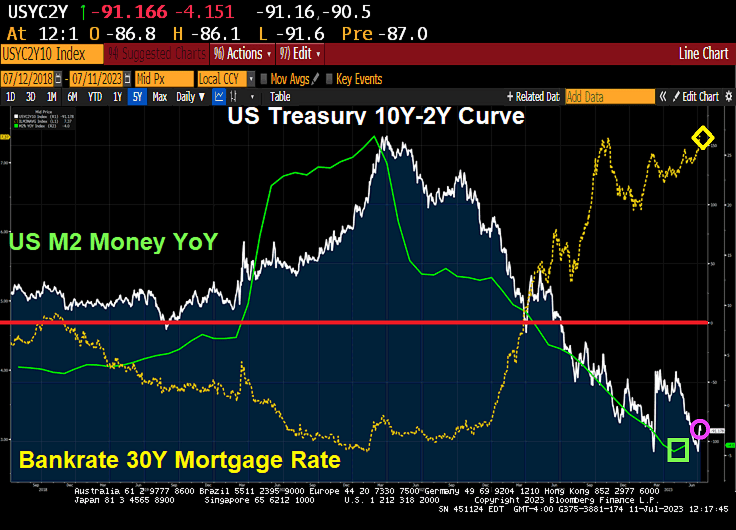

I have never seen anything like this. The US Treasury 10Y-2Y yield curve is deep in inversion and has had a negative slope for 265 straight days. Bidenomics is born under a bad sign!

On the commodities front, heating oil is up almost 2% this morning and nickel (an important element in Biden’s green energy mandates) is up 1.78%.

On the crypto front, Bitcoin is up 0.47% and Dogecoin is up 5.58%.

You can always buy Kamala’s Own Word Salad Dressing!

When I see the faces of Alan Greenspan, Ben Bernanke, Janet Yellen and Jerome Powell, all I think of is …. the Minsky Moment brigade!

From Zero debt in 1776 to $21 trillion in 1997 and just in the last 4 years, debt has gone up by that same $21 trillion. This graph shows the debt explosion, a 63x increase.

And then we have Congress promising >$192 trillion in entitlements (wealth transfers) that will likley be added to the already >$32 trillion in Federal debt.

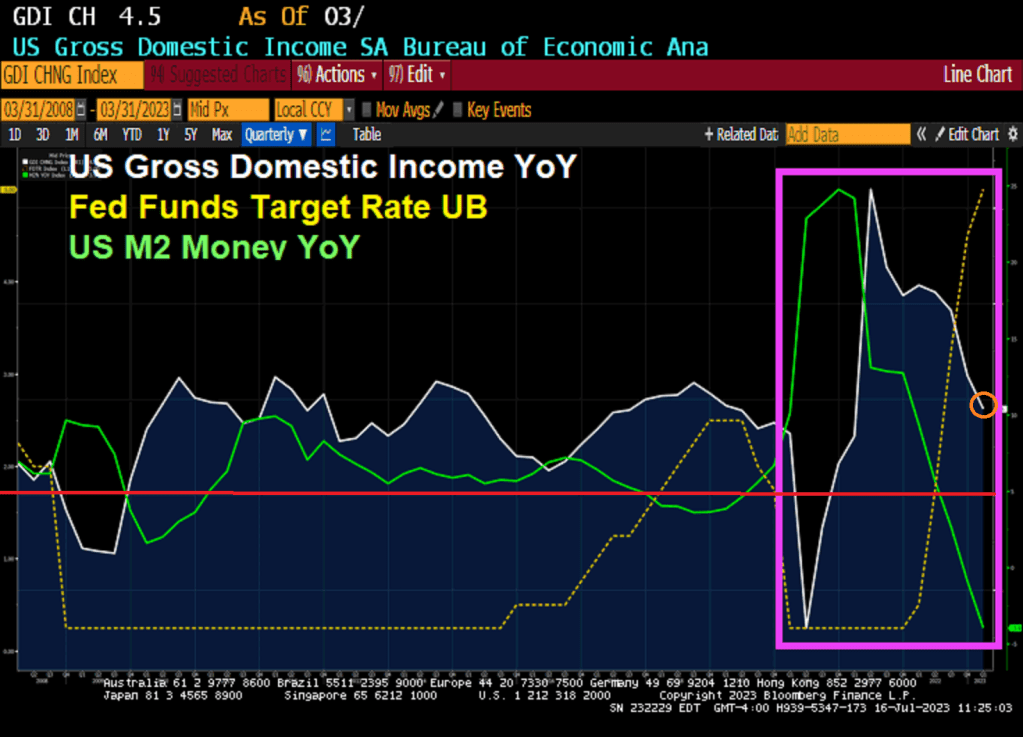

As The Federal Reserve is poised to continue it inflation-fighting crusade, the US economy is rapdily approaching DEFLATION. US Producer Price Index FINAL DEMAND fell to 0.1% YoY in June.

Bidenomics, the combination of insane monetary stimulus and insane directed Federal spending towards going green at all costs, is running out of steam. M2 Money growth was last measured to be -4% YoY and the US Dollar is down -8.2% since September 2022.

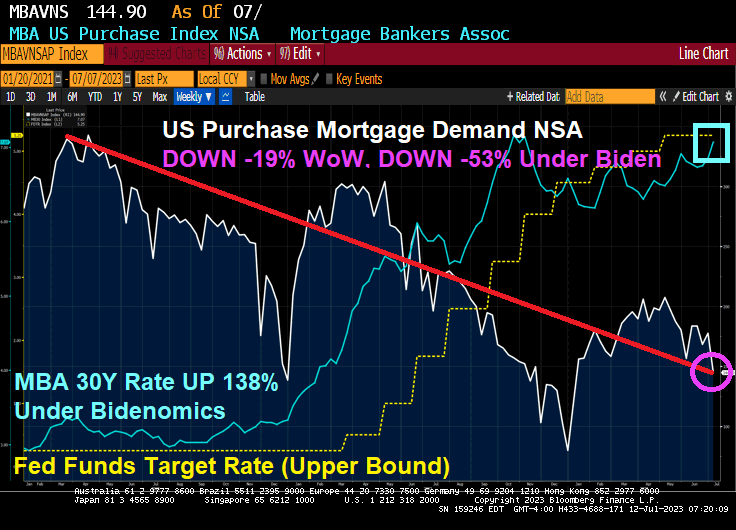

As Bidenomics (why Biden would brag about massive inflation in energy, food and shelter is beyond me), lurches forward, we have another shred of lousy economic news: US mortgage purchase demand fell -19% from the previous week and is how down -53% under Bidenomics).

Mortgage applications increased 0.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 7, 2023. This week’s results include an adjustment for the observance of Independence Day.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 19 percent compared with the previous week. The Refinance Index decreased 21 percent from the previous week and was 39 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index decreased 19 percent compared with the previous week and was 26 percent lower than the same week one year ago.

Yes, mortgag purchase demand is down a staggering -53% under Bidenomics (another word for the next best thing to Socialism which is Federal control of where the trillions are spent). Economic traffic led by The Keystone Kops.

Here is the rest of the data. Mark Zandi will look at the seasonally adjusted data, I look at the raw or non-seasonally adjusted data.

On a different note, I watch “Sound of Freedom” last night. A tremendous film highlighting the problem of pedophelia and child sex slavery in the US and Latin America. Very, very moving. Biden should be ashamed for cancelling Trump’s anti trafficking program.

I am anxiously waiting for the US inflation report tomorrow, so I am just looking at the US Treasury yield curve, mortgage rates and cryptos today.

The US Treasury 10Y-2Y yield curve stumbled (just like Biden and Bidenomics) to -91.166 basis points as the turnaround in M2 Money growth has stalled. Bankrate’s 30Y mortgage rate is up to 7.37%, that is UP 156% under Bidenomics.

Bitcoin is down today. At least Solana is up.

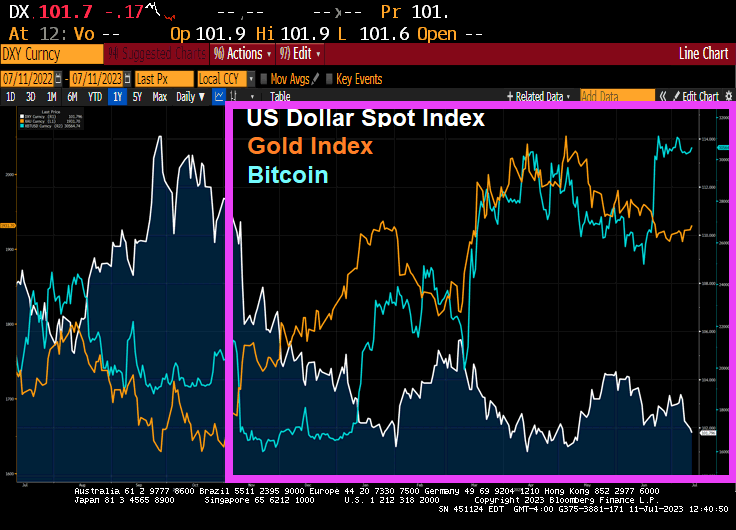

Since November 3, 2022, the US Dollar Index is DOWN -9.68%, Gold is UP 18.55% and Bitcoin (Elizabeth Warren’s latest obsession) is UP 51.11%.

{kind=link}

{kind=link}

You must be logged in to post a comment.