Like the Mel Gibson movie “Apocalypto!”, we are seeing the US middle class and low-wage workers being economically sacrificed by The Federal Reserve, the Biden Administration and Congress.

Despite the rhetoric that Fed stimulus (aka “Stimulypto!”) is being removed, the US remains plagued by NEGATIVE real 10-year Treasury yields, NEGATIVE real Fed Funds Target rate and NEGATIVE real average hourly earnings growth under Inflation Joe.

This chart demonstrates the Stimulytpo problem. Prior to Covid, US wage growth was consistently higher than headline inflation. But starting in March 2021, three months after Biden became President, headline inflation became higher than wage growth.

Even with all these negative REAL rates, the US economy is forecast to have almost no growth in 2023.

To quote Peggy Lee, Is That All There Is? Trillions in Federal spending and Fed monetary stimulus and all we get it 0.50% Real GDP??

The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

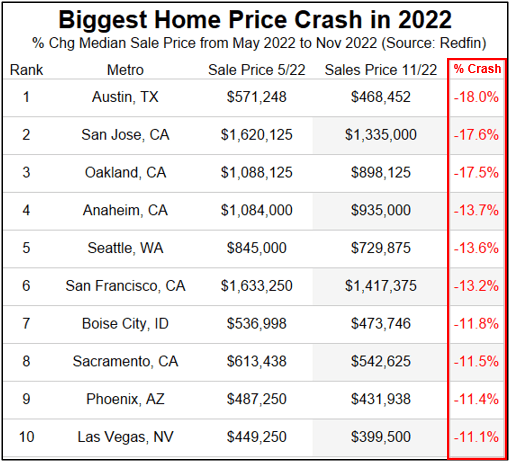

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

Here is a chart (courtesy of Zero Hedge) showing reported payrolls and REVISED payrolls. Somehow, I don’t think Jean Pierre (Biden’s spokesperson, not the French chef) will be touting “Unlike Trump, our administration barely added any jobs in March, April, May and June 2022.

How will this revelation influence the Fed’s open market committee (FOMC) going forward knowing that the Biden Administrations job creation claims are wildly overstated?

Perhaps it doesn’t matter since Bernanke, Yellen and Powell don’t follow any rules (like the Taylor Rule), but generally with job creation almost nonexistant in March through June of 2022, The Fed should be cutting rates like mad. But wait! Can they with significant inflation?

The good news is that inflation is coming off its peak, but will take a while to get to The Fed’s 2% target. Hence The Fed may raise their target rate since they cannot achieve it will energy price up substantially since Biden became President.

The numbers coming out today are not good. November numbers were 1) US Industrial Production was down -0.2% MoM, 2) manufacturing production is down -0.6%, 3) retail sales advanced down -0.6% (most in 11 months) and …

The Empire State Manufacturing outlook was down -11.2% and the Philadelphia Fed (or Phed) business outlook was down -13.8% in November.

And with all this bad news, global equity markets are dropping like a paralyzed falcon.

But at least Biden traded a dangerous international arms dealer for WBNA star Brittney Griner. Possilby the worst trade in history after the Chicago Cubs traded future Hall of Famer Lou Brock for sore-arm pitcher Ernie Broglio. Griner is Ernie Broglio.

Apparently, despite the denials from the Biden Administration, someone at Bureau of Labor Statistics or someone in Congress or the Federal Reserve or the Biden Admininstration itself likely tipped the wink on the soft CPI report on Tuesday.

Treasuries were well on the front-foot in the lead up to the below-estimate November CPO print, as a surge of buying took place seconds before the official 8:30 am New York release time. Over a 60 second period before the data, 13,518 March 10-year futures traded as the contract moved from 114-04+ up to 114-22. Gains were then extended up to 115-11 session highs once the data was released.

On the equity side, stock futures suddenly spiked more than 1%. Trading in Treasury futures surged, pushing benchmark yields lower by about 4 basis points. Those are major moves in such a short period of time — bigger than full-session swings on some days. And they should get scrutinized by regulators, long-time market observers say, even if a leak is only one of several possible explanations for why traders suddenly started buying right before the report was published.

Remember that current Treasury Secretary Janet Yellen was accused of leaking information to a NY hedge fund ahead of the Fed Open Market Committee meeting? And then we have the Wolf of Wall Street.

I wonder if the REAL Wolf of Wall Street did this?

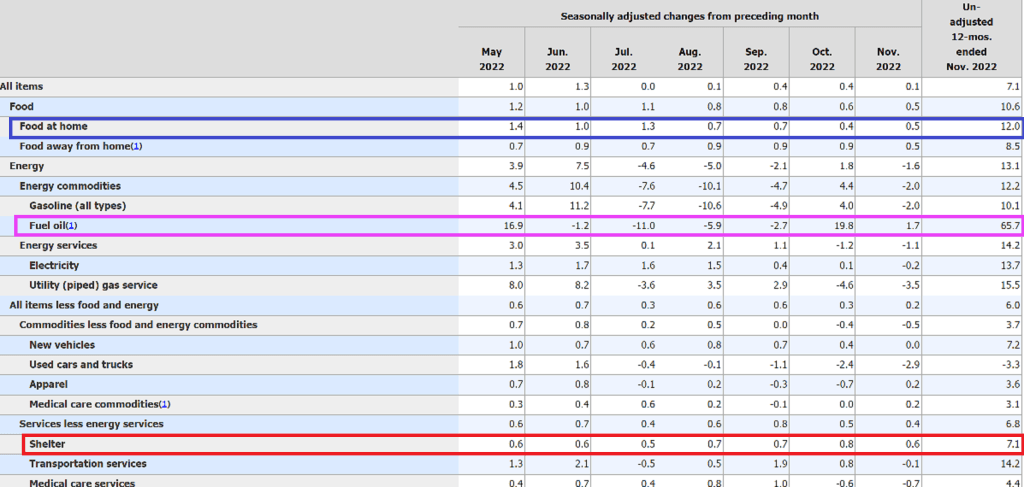

Is inflation “gone in November”? Nope. Slowing, yes, but at 7.1% YoY and core inflation at 6.0% YoY, it is still considerably higher than The Fed’s target of 2%.

And the American middle class and low wage workers are still suffering with REAL average hourly earnings growth at -1.9% YoY.

Fun week ahead. US inflation numbers are out on Tuesday (forecast? CPI YoY = 7.3%, Core CPI YoY = 6.1%) and The Federal Reserve’s Open Market Committee (FOMC) rate decision is on Wendesday.

So, where are we sitting on Monday?

First, the US Treasury 10Y-2Y yield curve has been inverted (a precursor to recession) for 116 straight days). Second, the likelihood of recession in 2023 is 100%. Third, with the forecast of core inflation at a still numbing 6.1%, The Fed seems dead set on raising their target rate by 50 basis points to 4.50% on Wednesday.

dddd

So, as The Fed debates recession versus fighting inflation (partly caused by The Fed), we have Kevin Malone from The Office debating Angela versus double-fudge brownies:

Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. They are deliberately causing recessions by overtightening policy to try to rein in inflation. That makes recession foretold. We see central banks eventually backing off from rate hikes as the economic damage becomes reality. We expect inflation to cool but stay persistently higher than central bank targets of 2%.

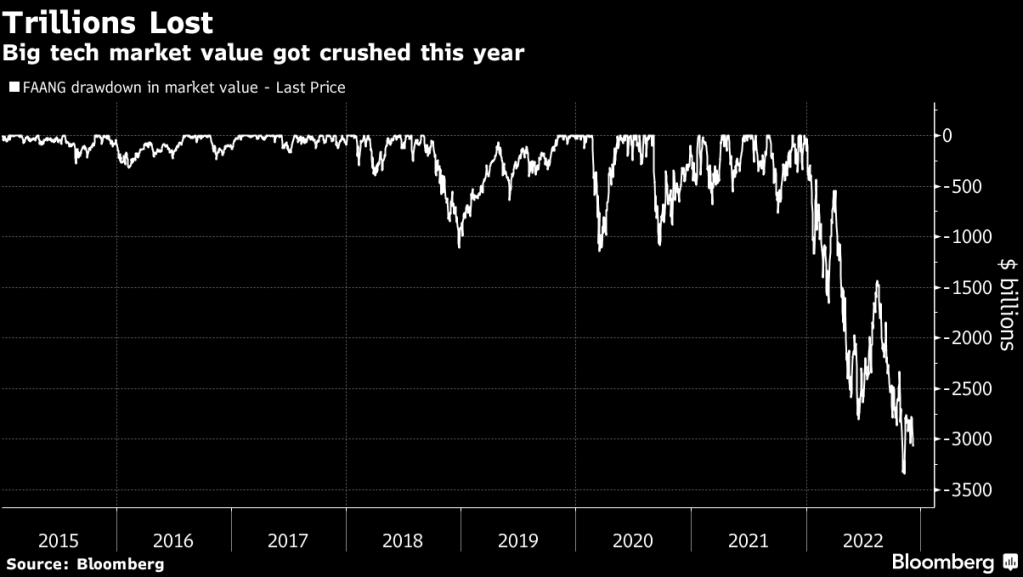

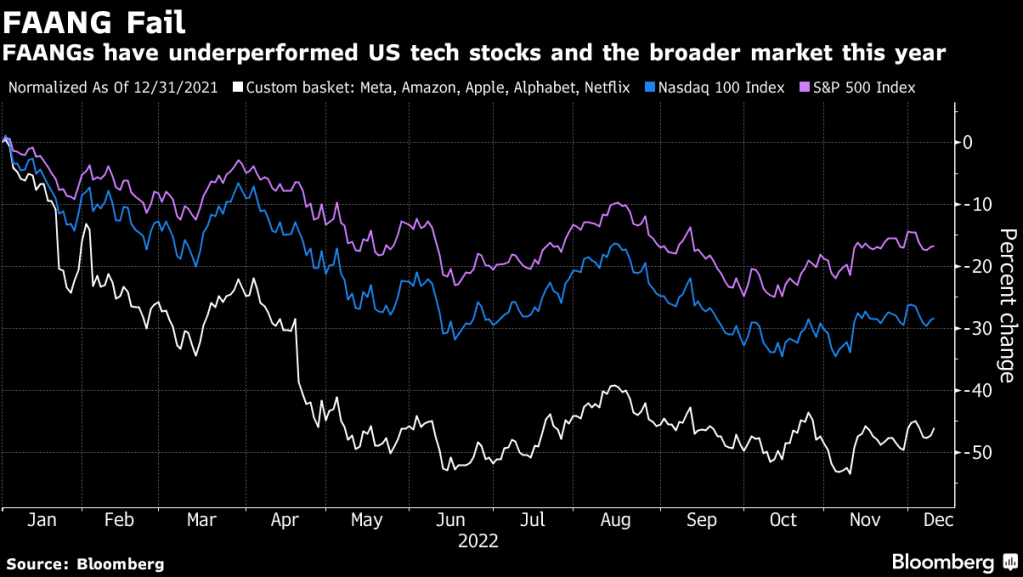

For some investors, this year’s rout in high-flying technology stocks is more than a bear market: It’s the end of an era for a handful of giant companies such as Facebook parent Meta Platforms Inc. and Amazon.com Inc.

Those companies — known along with Apple Inc., Netflix Inc. and Google parent Alphabet Inc. as the FAANGs — led the move to a digital world and helped power a 13-year bull run. And FAANG drawdown have reached over $3 trillion.

FAANGs (Meta, Amazon, Apple, Alphabet, Netflix) are getting clobbered in 2022.

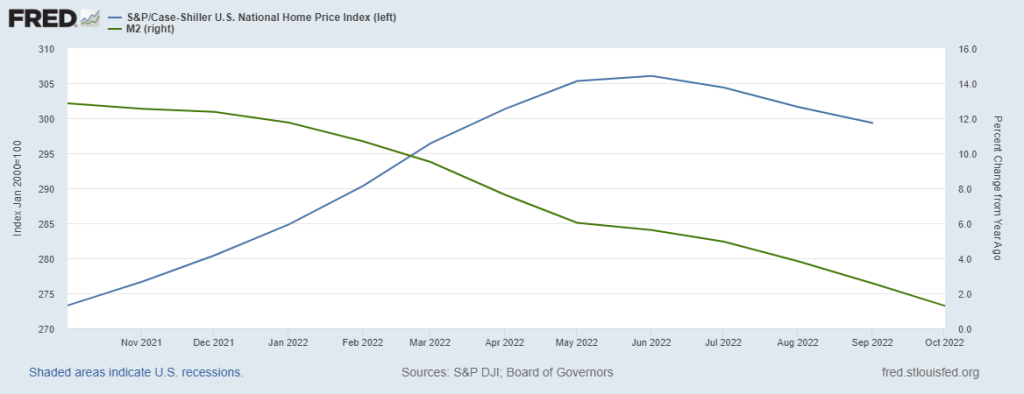

Typically, when The Fed prints too much money, such as 10% or higher (red line), inflation follows. Particularly when The Fed prints at 25% YoY in Q4 2020, it was followed by the highest inflation rate in 40 years. But if M2 Money continues to slow, inflation will likely slow, but not to The Fed’s target of 2%.

Despite what Minneapolis Fed’s Neal Kashkari said about The Fed having infinite printing resourses, The Fed is going to fight inflation THAT THEY HELPED CAUSE. Biden’s energy policies (did you see that Elon Musk has a car that uses plentiful hydrogen?), and excessive Federal spending by Biden/Pelosi/Schumer, are culprits in creating the supply chain problems facing America. BUT after the 25% surge in M2 Money in 2020 and 2021, we saw M2 Money VELOCITY crash and burn to its lowest level in history. Which means the “bang for the buck” for printing more money is negligible.

Of course, big tech firms got caught influencing the 2020 Presidential election (see Musk’s release of Twitter files) and engaged in restriction of the 1st Amendment (Freedom of Speech). How much will that impact FAANG stocks going foward?

And yes, the US Treasury yield curve is inverted pointing to a recession in 2023.

And yes, apparently Biden was complicit in the Twitter fiasco.

US producer prices rose in November by more than forecast, driven by services and underscoring the stickiness of inflationary pressures that supports Federal Reserve interest-rate increases into 2023.

The producer price index for final demand climbed 0.3% for a third month and was up 7.4% from a year earlier, Labor Department data showed Friday. The monthly gains for October and September were revised higher.

At the same time, the annual increase was the smallest in 18 months, extending a months-long easing and suggesting the central bank still has scope to pause its rate hikes next year as expected. Cooler demand at home and abroad has taken some stress off supply chains.

The data come just days before the release of the closely watched consumer price index, which is forecast to show inflation, while much too high, continues to decelerate.

While PPI is declining, it is still far above The Fed’s inflation rate of 2% (red line).

Watch out for energy prices when the sleeping giant (China) opens up again and demand for energy skyrockets. Meanwhile, Clueless Joe is merrily draining the US Strategic Petroleun Reserve.

Lastly, congratulations to former Cleveland Brown QB Baker Mayfield for winning with the LA Rams against the Las Vegas Raiders with a stunning 99 yard drive for a TD at the end of the game.

You must be logged in to post a comment.