The start of a new week and the US Treasury 10-year yield is up 10 basis points, always a noteworthy change. And with it, the 30-year mortgage rate should climb.

Since Biden/Pelosi/Schumer are in a lame duck session with Republicans taking the House in January, let’s see if Republicans can halt the insanity in Washington DC.

Be that as it may, Fed Funds Futures are pointing at a 50 basis point rate hike at the December 14th FOMC meeting.

Seriously, how is The Federal Reserve going to cope with $204 TRILLION … and growing Federal debt AND unfunded liabilities?

We are truly living in Strange Days under Joe Biden. And with Elon Musk’s release of Twitter’s suppression of the Hunter Biden laptop scandal, they call Joe Biden the Sleaze.

As The Federal Reserve tries to crush Bidenflation, we are seeing Fed Remittances to the US Treasury soaring (white line). At the same time, we see the Biden Administration draining the Strategic Petroleum Reserve (orange dashed line). And as The Fed tightens, M2 Money growth crashes (green line).

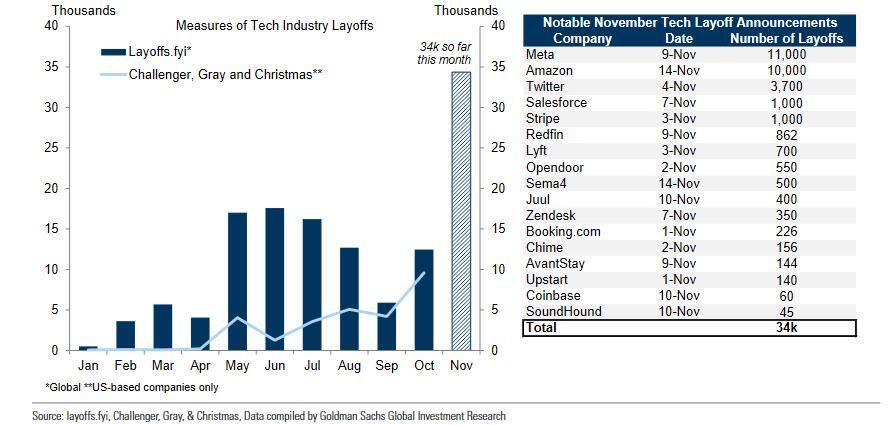

And with tech layoffs, I predict that 2023 job growth will be pretty bad.

As I have discussed before, I am a fan of ADP’s job reports and not a fan of the BLS NFP reports. As M2 Money growth slows, we can see declining ADP jobs added (yellow line), but BLS’s NFP report shows huge spikes.

Lastly, we have Sam Bankman-Fried and FTX. SBF should be in custody for being involved in one of the biggest fraud cases in history, but like Hunter Biden, is roaming free and trying to raise MORE funds. Why are these lapses in justice occuring with “10% for The Big Guy” Biden?

Warning! Evidence of a US recession is appearing. And with a recession, prices will likely fall due to lack of demand.

Why might inflation be falling? Take a gander at ISM Prices Paid. They just fell to the lowest level since the infamous Covid economic shutdowns of 2020.

M2 Money growth YoY is the lowest in years, but The Fed’s balance sheet remains elevated. But apparently the Covid-related sugar rush has ended.

Yes, The US Treasury 10Y-2Y yield curve remains inverted, for the 104th straight day. And Bankrate’s 30-year mortgage rate has dropped -57 basis points since November 3, 2022.

This comes after a gruesome Pending Home Sales and mortgage applications reports today.

The hawkish drumbeat from central bankers is raising fears of a downturn, with global bonds joining US peers in signaling a recession, as a gauge measuring the worldwide yield curve inverted for the first time in at least two decades.

The US Treasury 10Y-2Y yield curve, on the other hand, has been inverted for 107 straight months.

And in Europe, 10-year sovereign yields are dropping like a paralyzed falcon.

The world and US yield curves are pointing to trouble. And drums along the Potomac (DC) and East River (NYC).

The US has an inflation problem. Both headline and core inflation YoY remain high compared to the previous 40 years. And The Federal Reserve is resolute in trying to curb inflation to 2%.

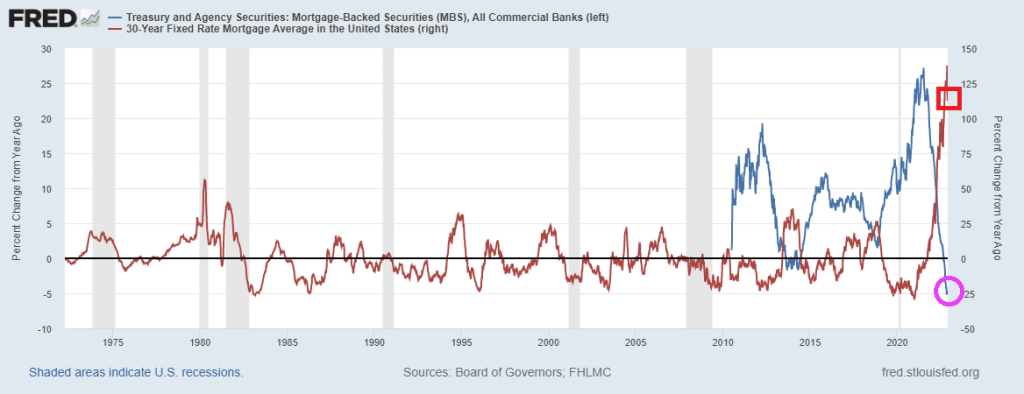

But as The Fed counterattacks inflation by raising their target rate, we are seeing a problem forming at the nation’s commercial banks. The growth in deposits YoY is now -0.6%. Commercial bank holdings of Treasuries and Agency MBS are declining as well. Agency MBS holdings are down -4.6% YoY and Treasuries and Agency holdings are down 0.0%.

How about M2 Money growth and M2 velocity? M2 Money growth has fallen to 1.3% YoY while M2 velocity has not been the same since the Covid sugar splash by The Fed and Federal government.

While inflation is creating havor for commercial bank deposit growth, it is interesting to follow the adventures of a spoiled child from MIT and his multi-billion dollar lemonade stand with all the controls of a child.

Once again, how did regulators get this SOOOOO wrong? And why didn’t investment advisors look at the balance sheet of FTX and Alameda Research. Yes, the media loves to report on FTX orgies, but the FTX fiasco points to something far more sinister. Were Sam Bankman-Fried and his paramore Caroline Ellison fronting this operation on behalf of some other parties?

I recall one of Woody Allen’s best lines. When asked what an investment manager does, the response was “they manage your money until nothing is left.” Sounds like SBF has a great future on Wall Street! And Caroline Ellison should have known better than to post things like “Here are what I think about some things: controlling most major world governments.”

Due to high inflation, reduced consumer spending, higher rents and other economic pressures, U.S.-based small business owners’ rent problems just escalated to new heights nationally this month, based on Alignable’s November Rent Poll of 6,326 small business owners taken from 11/19/22 to 11/22/22.

Unfortunately, 41% of U.S.-based small business owners report that they could not pay their rent in full and on time in November, a new record for 2022. Making matters worse, this occurred during a quarter when more money should be coming in and rent delinquency rates should be decreasing. But so far this quarter, the opposite has been true.

Last month, rent delinquency rates increased seven percentage points from 30% in September to 37% in October. And now, in November, that rate is another four percentage points higher, reaching a new high across a variety of industries.

All told in Q4 so far, the rent delinquency rate continues to increase at a significant pace, up 11 percentage points from where it was just two months ago.

Well, this is not good.

And on the mortgage front, not all is quiet.

Commercial bank holding of Agency mortgage-backed securities (MBS) has collapsed with Fed tightening and mortgage rate increases.

You must be logged in to post a comment.