While ”Angry Joe” Biden screams about democracy (while having his attorney general prosecute his likely Presidential election opponent), and he and Congress continue to spend and borrow like there is no tomorrow (not a bad assumption since Biden is a sickly 81, Pelosi is 83 and assorted other aging policitians in the District of Corruption will never live beyond 10 more years), we are now seeing more attention to the boiling frog problem facing our children and grandchildren. I call this “Biden Stew.”

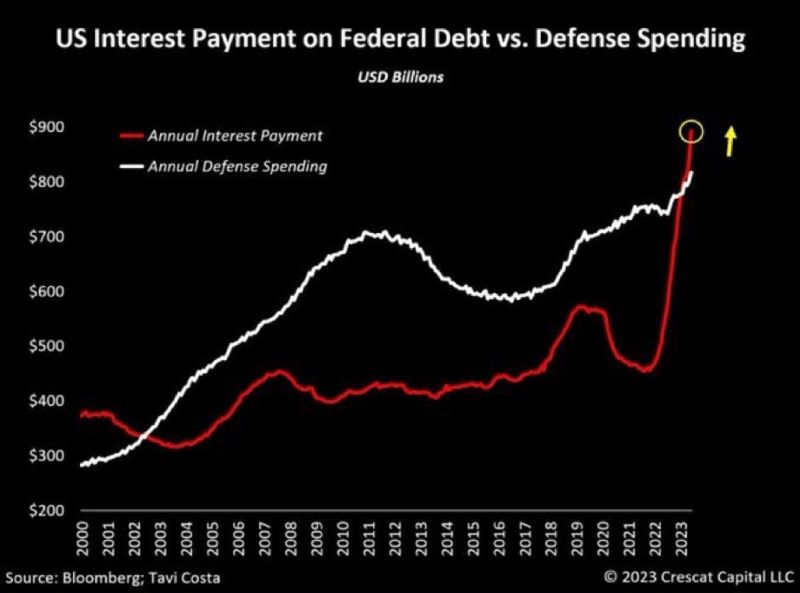

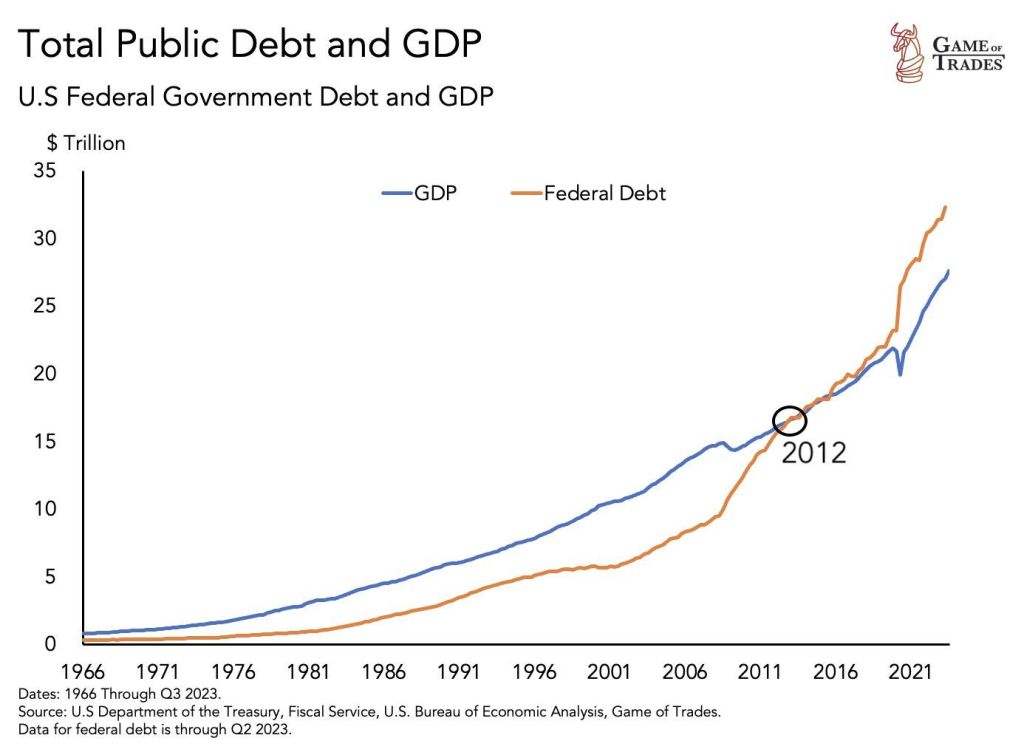

The country’s soaring national debt — which recently surpassed a record-high $34 trillion — is akin to a “boiling frog” for the economy and Wall Street investors, a senior analyst at JPMorgan Chase warned.

Michael Cembalest, who runs JPMorgan’s market and investment strategy unit in the bank’s asset management division, predicted dire consequences for the economy if the Biden administration doesn’t start tackling the debt.

Cembalest wrote in a newsletter published last week by JPMorgan that the country cannot sustain higher deficits and ballooning net interest payments, which are soon expected to exceed the federal government’s total revenue by early next decade.

“The problem for the US is the starting point; every round of fiscal stimulus brings the US one step closer to debt unsustainability,” Cembalest wrote in the newsletter titled “Pillow Talk.”

“However, we’re accustomed to deteriorating US government finances with limited consequences for investors, and one day that may change (the boiling frog analogy).”

The “boiling frog” concept comes from a metaphor used to describe a situation whereby an undesirable set of circumstances is tolerated for an extended period of time — such as a frog that is thrown into water that is gradually heated.

Once the circumstances become too dire — and the water is heated to a boil — it is too late for the frog to act and it is cooked alive.

Cembalest predicted that by early next decade, “all Federal government revenues will be consumed by entitlement payments and interest on the Federal debt.”

“Entitlement payments” refer to Medicaid, Medicare, Social Security, unemployment insurance and other aspects of the federal welfare safety net.

Cembalest wrote that before the next decade he anticipates that “a combination of market pressure and rating agency downgrades” will “force the US to make substantial changes to taxes and entitlements.”

In November, Moody’s lowered the US government’s credit ratings outlook from “stable” to “negative.”

Last summer, Fitch Rating downgraded the federal government’s long-term credit rating from AAA to AA+.

The national debt, which is the total amount of outstanding borrowing by the federal government, stood at $34.006 trillion as of Monday, according to the Treasury Department’s official debt tracker. And growing REALLY fast!!

While Biden pushes for MORE Ukraine war funding and cancelling student debt (like a demonic Daddy Warbucks from Little Orphan Annie), he ignores unfunded entitlements of $213 TRILLION.

To be sure, the Biden Stew has been a trainwreck for decades, but Biden has the golden opportunity to act like a leader instead of “Angry Joe” screaming about Democracy as he and his minions attempt to cancel their politicial opponents.

It doesn’t help that The Federal Reserve Board of Governors seems like the cast of the ice hockey flick “Slap Shot.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.