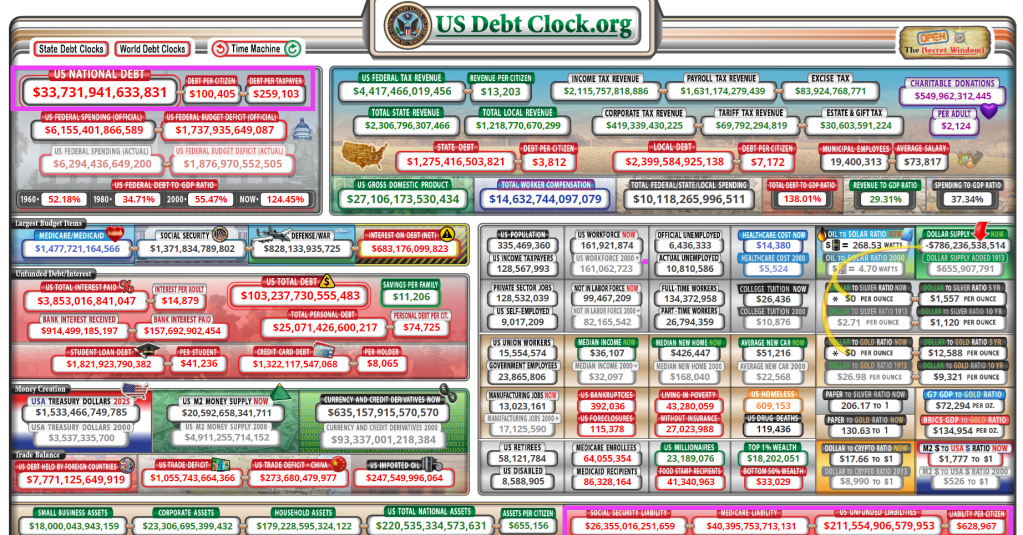

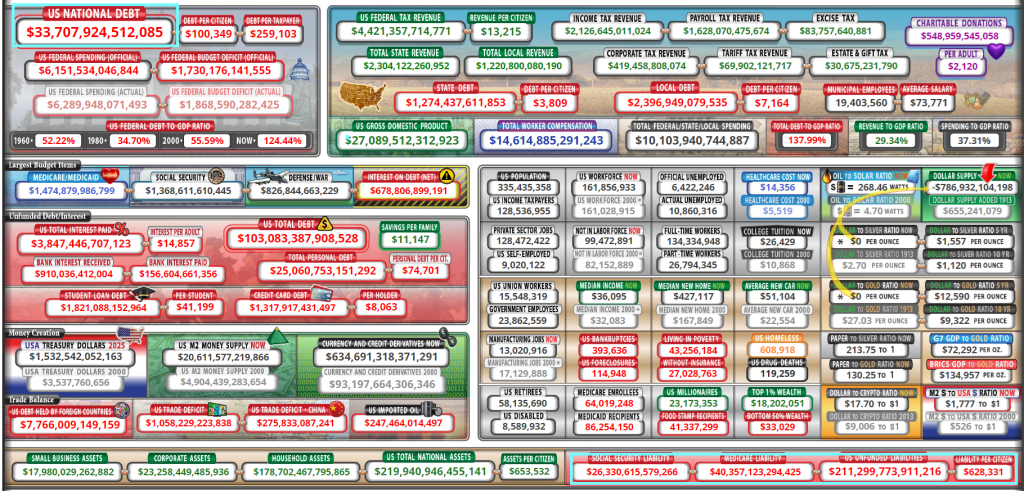

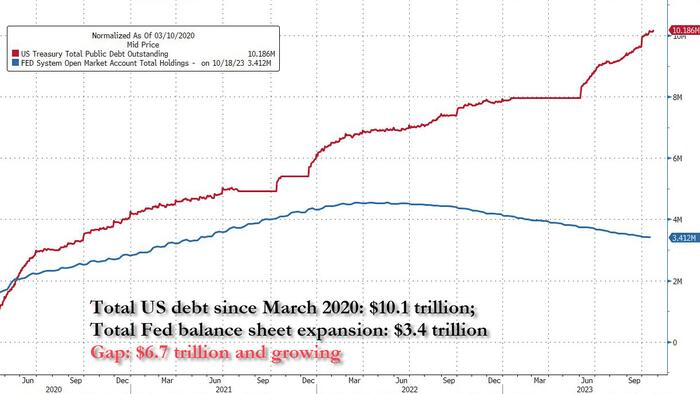

In fact, Congress and the Biden (mis) Administration are spending like the proverbial drunk sailors in port. US national debt is up to $33.7 TRILLION. That transates to $259,103 per taxpayer. With US debt to GDP of 138%!

Now, HERE IS THE REAL BAD NEWS! Unfunded promises that politicians made to Americans (Social Security, Medicare, Medicaid, etc.) now stands at $211.6 TRILLION. That equates to $629,000 per citizen. Maybe that should be the deal at the southern border: all immigrants must pay $629,000 for admission!

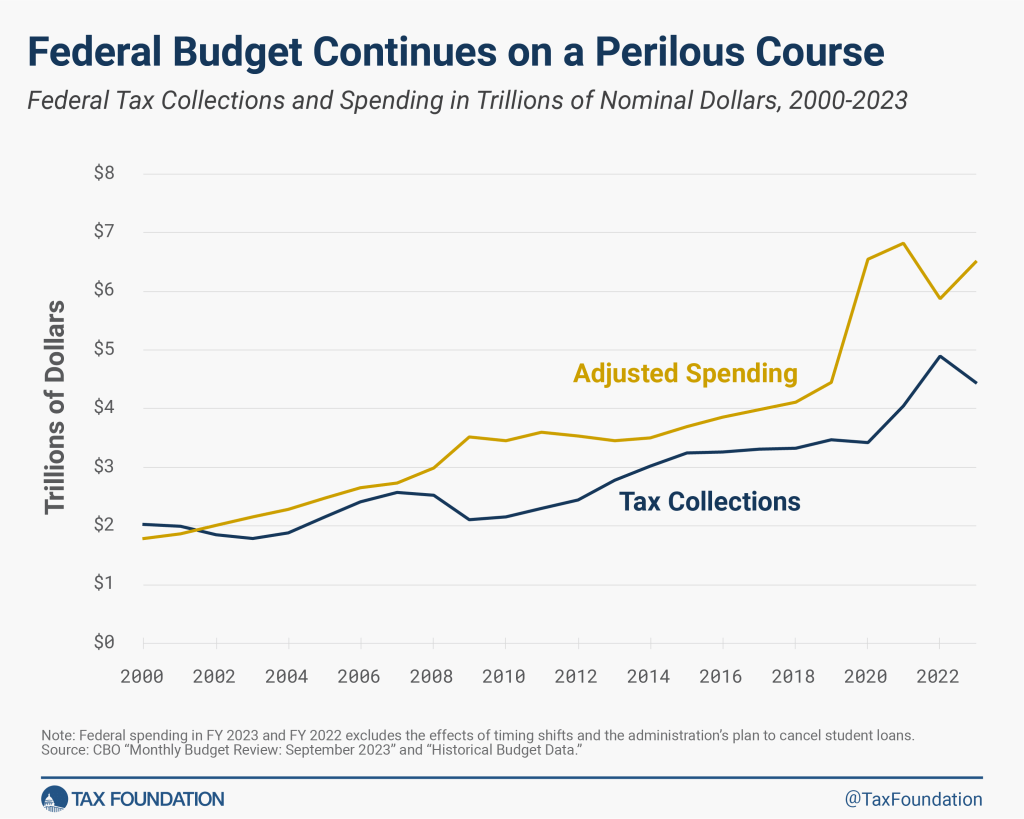

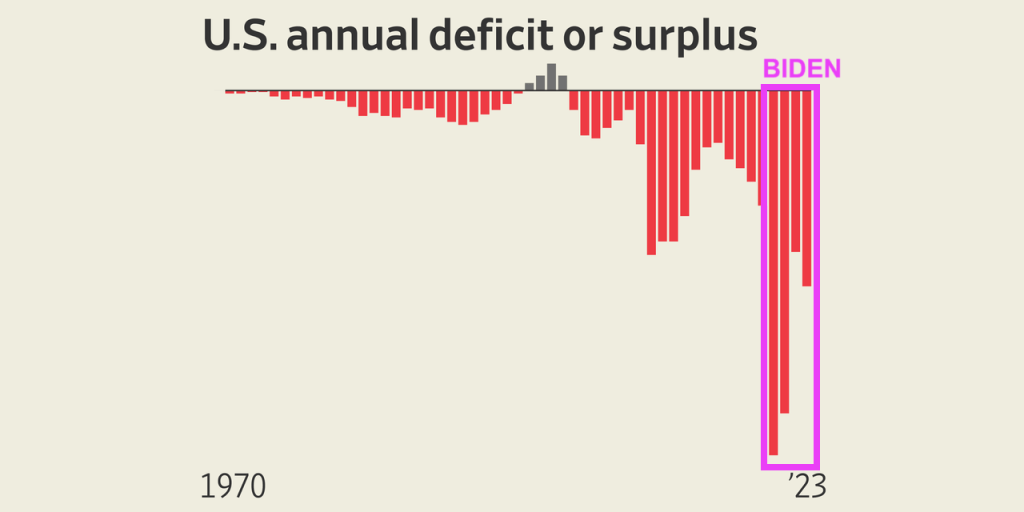

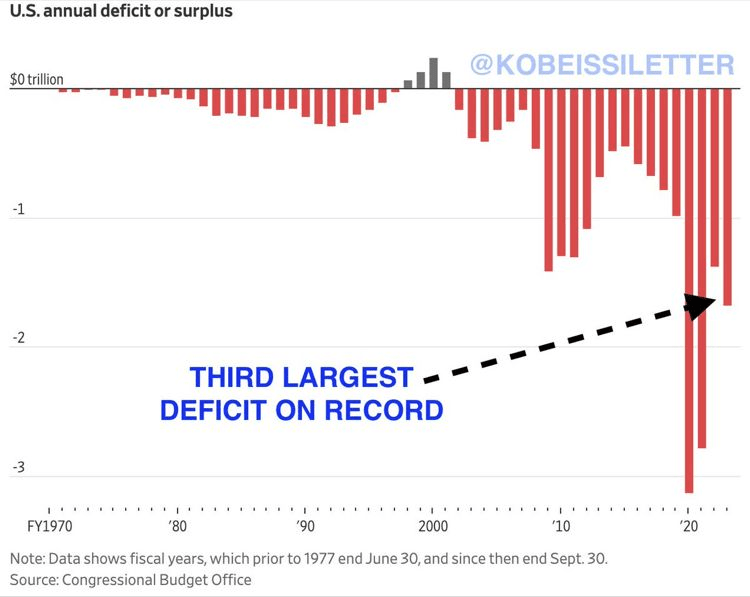

And the Federal budget deficit keeps on getting worse.

The budget deficits under Biden/Yellen have been the worst in history. So much for Biden whispering “Bidenomics is working!”

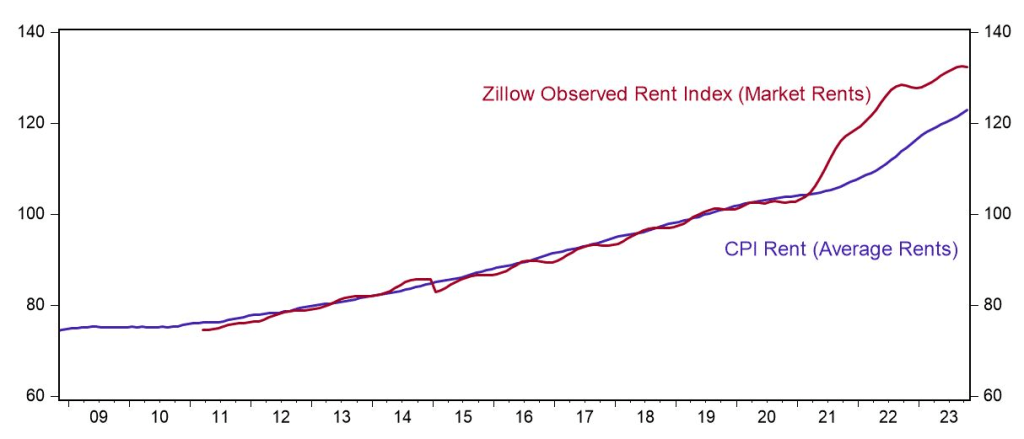

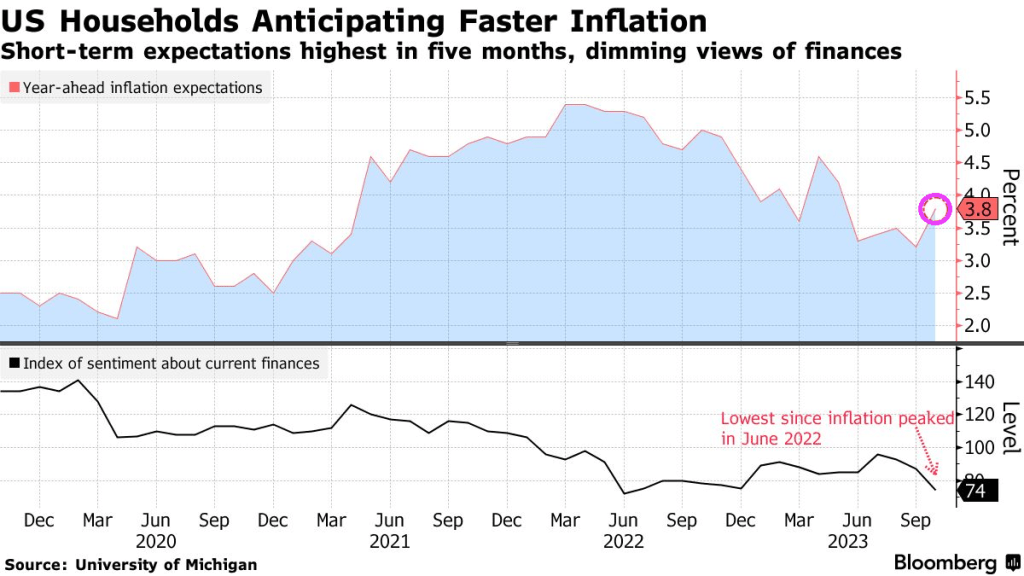

Rents in the US remain unaffordable to many.

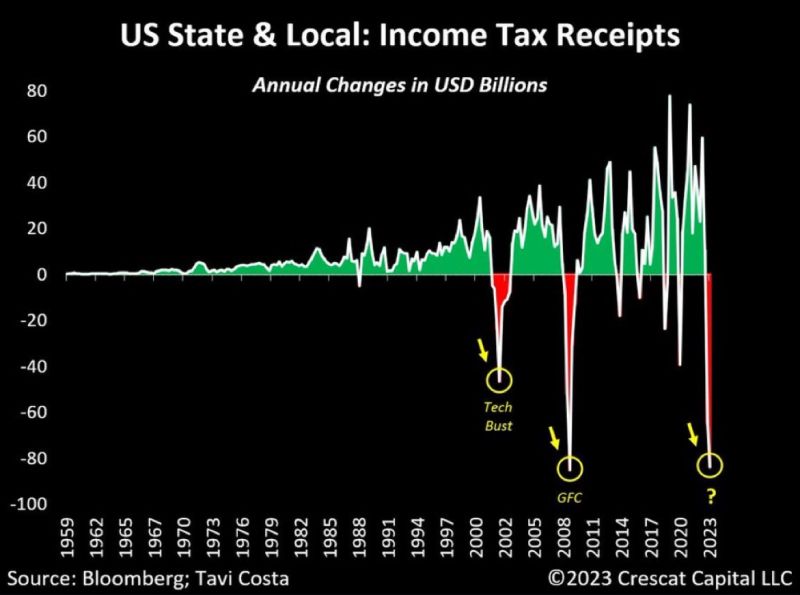

And Yellen, our nation’s financial consigliari, hasn’t said much about the dire decline in income tax receipts.

But Biden’s favorite country China, a classic top-down command economy like Biden and Yellen love,

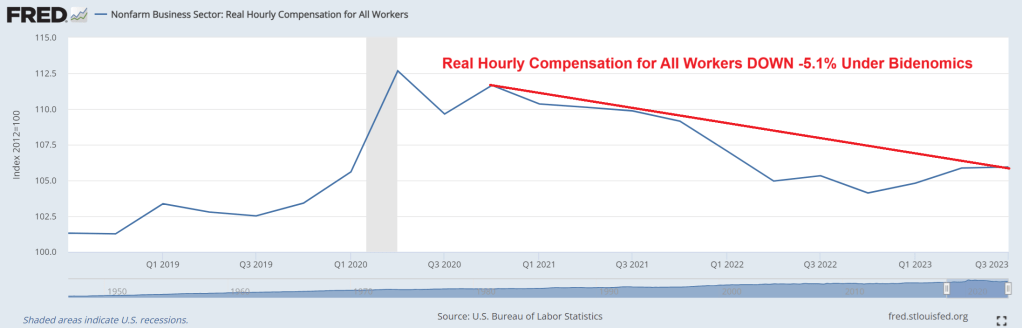

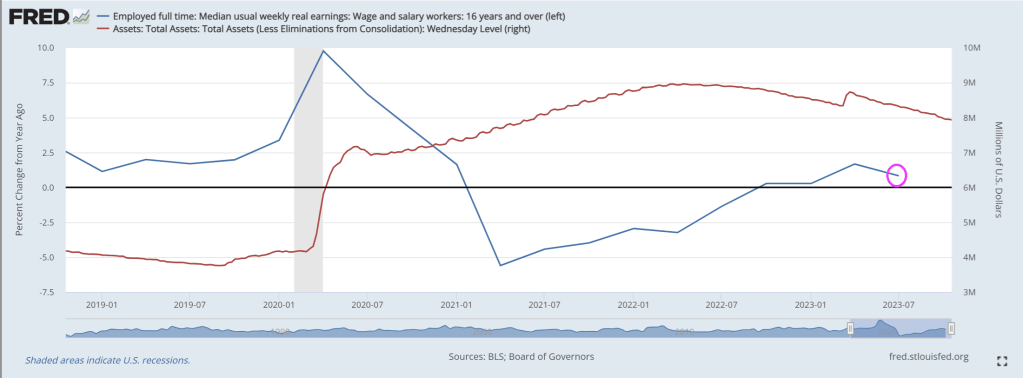

On Sunday, President Joe Biden tweeted, “Right now, real wages for the average American worker is higher than it was before the pandemic, with lower wage workers seeing the largest gains. That’s Bidenomics.” That’s right, Joe! Except real hourly compensation has DECLINED by -5.1% under Biden.

After listening in horror to Joe Biden’s press conference after his summit with China’s Xi, I had to ask the following question: what does Joe Biden has in common with Georgia Tech? Answer? They are both rambling wrecks. Biden made a horrendous foreign policy blunder by calling Xi a “dictator” and almost blew it by nearly spillling the beans on our foreign policy negotiations with Israel. SecState Blinken had to intervene. We are represented by Winken (Harris), Blinken and Nod (Biden, who usually looks asleep or confused).

But back to the horrors of a slowing economy.

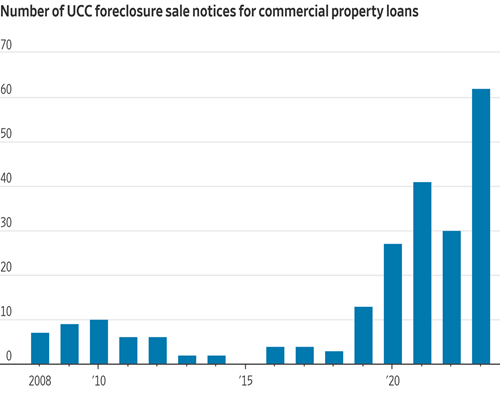

As the US economy slows down (like Biden himself), we are seeing further cracks in the real estate market. Foreclosure sale notices for commercial property loans are exploding.

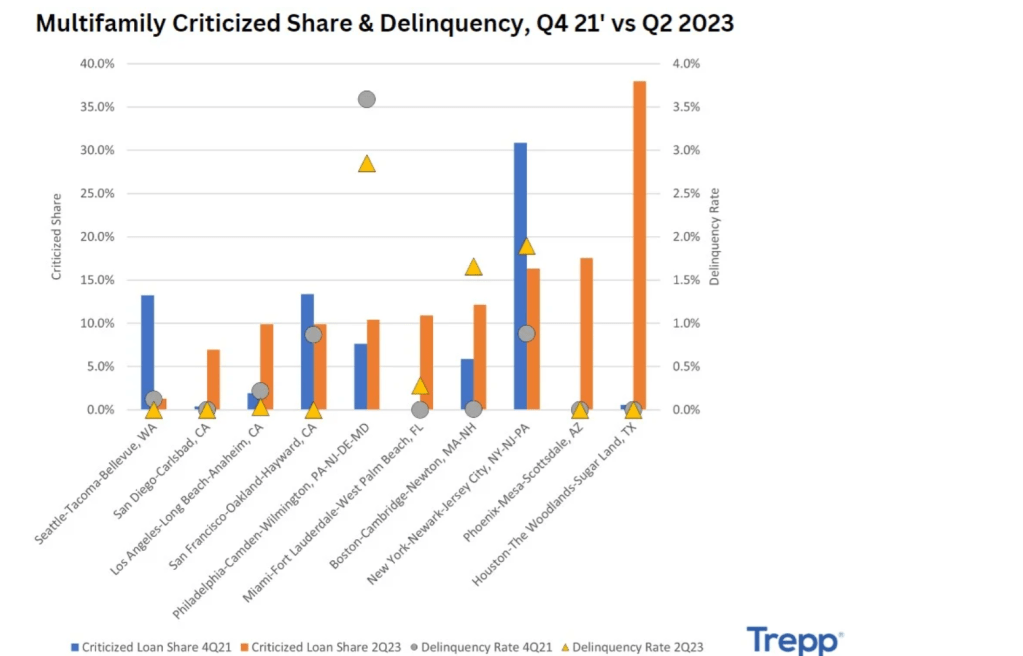

And depending on the MSA, multifamily delinquencies are booming, like in Houston, Texas, New York City and Phoenix AZ.

Then we have this headline: “Not Just Office Towers – Commercial Real Estate Sales Crater Throughout Los Angeles.” It’s difficult to find big commercial real estate deals of any kind in Los Angeles. A new report from NAI Capital reveals how severe and universal the decline in activity is throughout the region this year amid collapsing values, higher interest rates, and a new tax on property sales above $5 million.

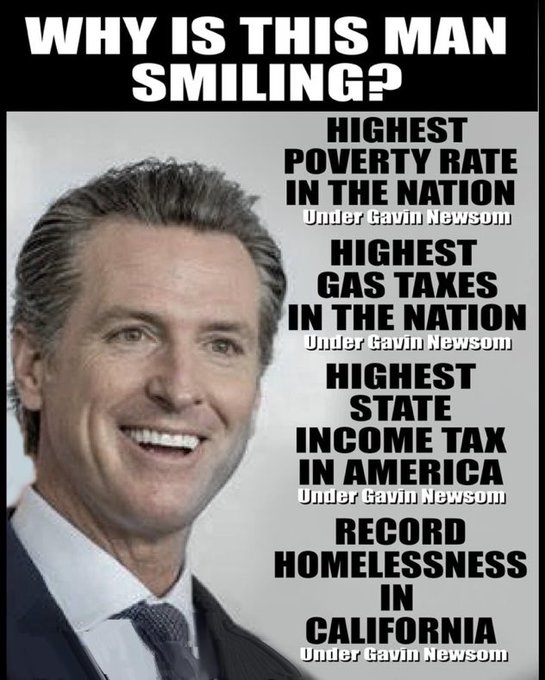

Yes, I know, California’s real estate woes are mostly the fault of their politicians like Governor Gavin (Gruesome) Newsom. The same guy who ordered San Francisco’s homeless population to be moved creating a new Potemkin Village. But rising interest rates are the fault of excessive spending by Congress and the Biden Administration.

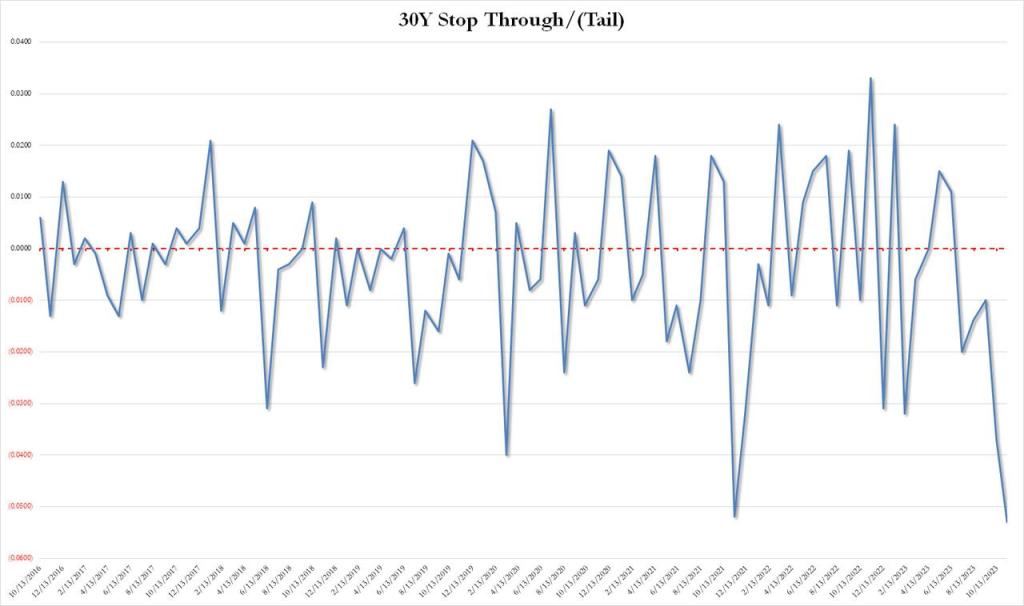

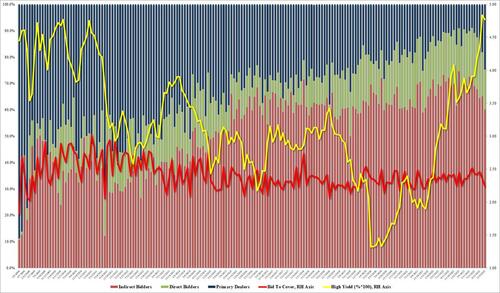

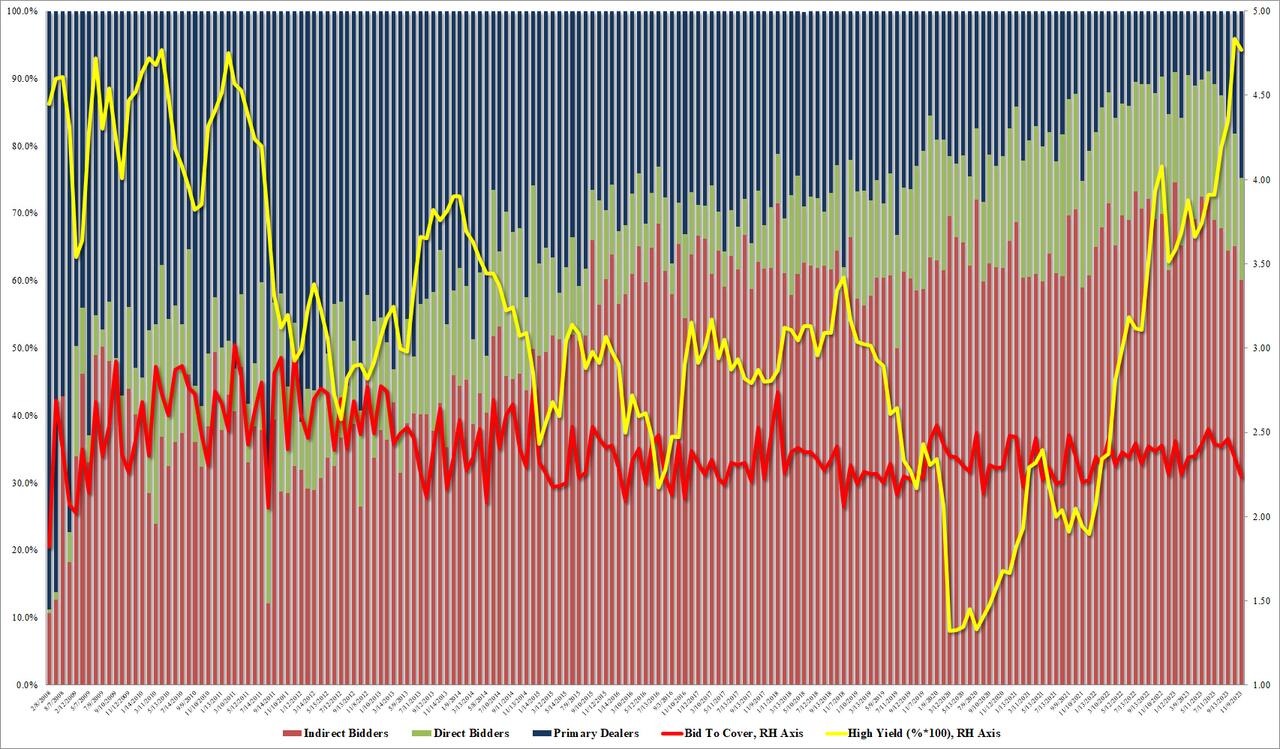

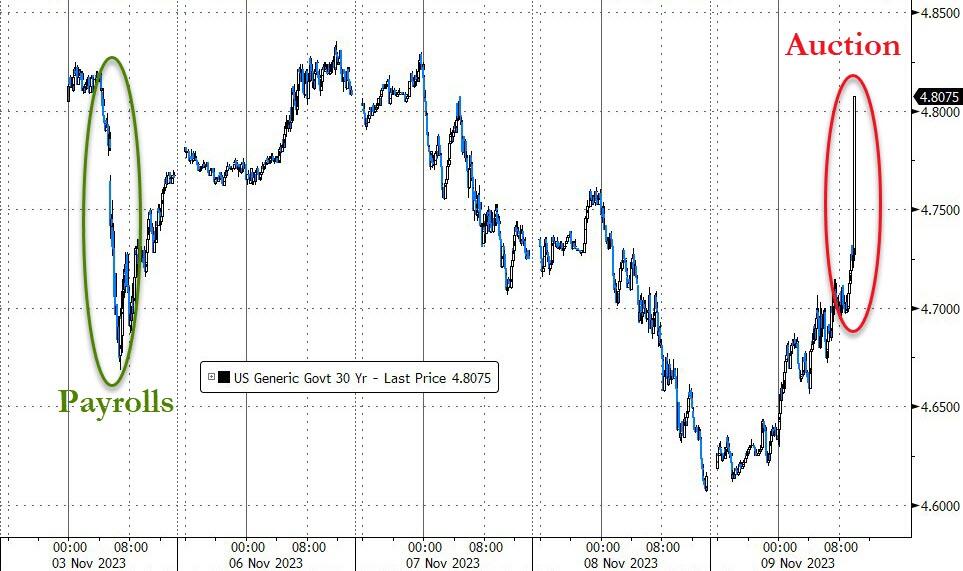

The bond priced at a high yield of 4.769%, which was below last month’s 4.837%, and just shy of the April 2010 high. But more importantly, it tailed the When Issued by a whopping 5.3bps, which was… well… terrible, because as shown in the chart below, this was the biggest tail on record (going back to 2016).

The bid to cover was just as bad: at 2.236 it was the lowest since Dec 2021.

The internals were even worse as foreign bidders (Indirects) tumbled from 65.1% to 60.1%, the lowest since Nov 2021, and with Directs taking down only 15.2%, banks (Dealers) were forced to step up and take the balance, or a whopping 24.7%, double the recent average of 12.7%, and the highest since Nov 2021.

This is a big warning flag because every time we have seen a surge in Dealer takedowns, some sort of Fed intervention – QE or otherwise – has usually followed and we doubt this time will be different.

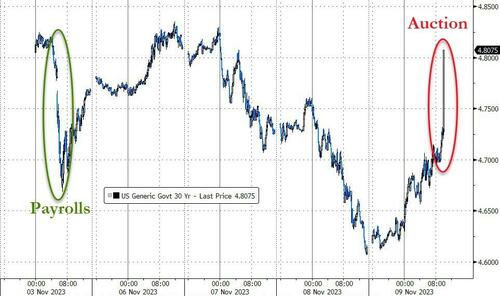

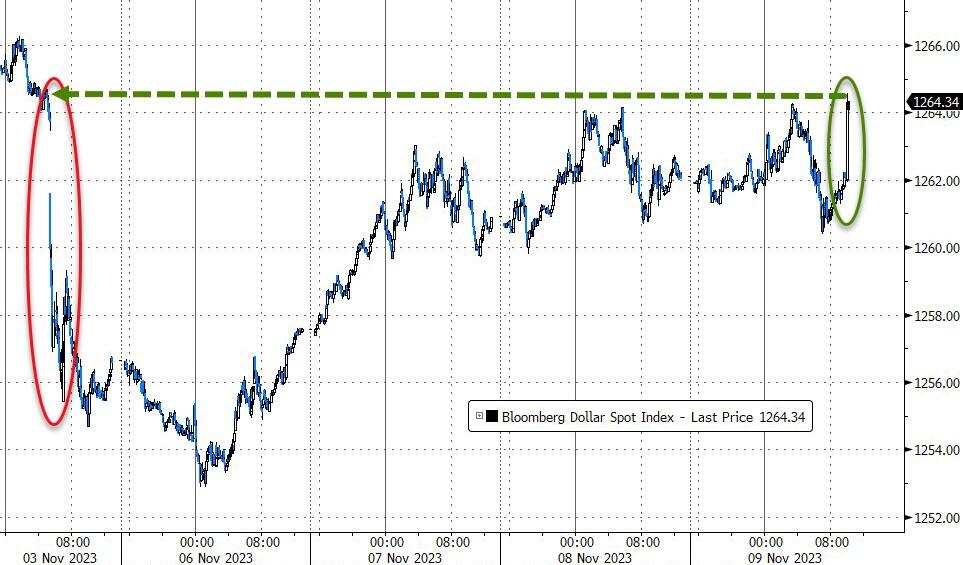

The market reaction to the catastrophic 30Y auction was immediately, sparking a swift and painful response across markets with bonds and stocks hammered lower and the dollar spiking.

Treasury yields – as you would expect – exploded higher, with 30Y Yields back up to pre-payrolls levels…

That is the biggest spike in 30Y yields since March 2020…

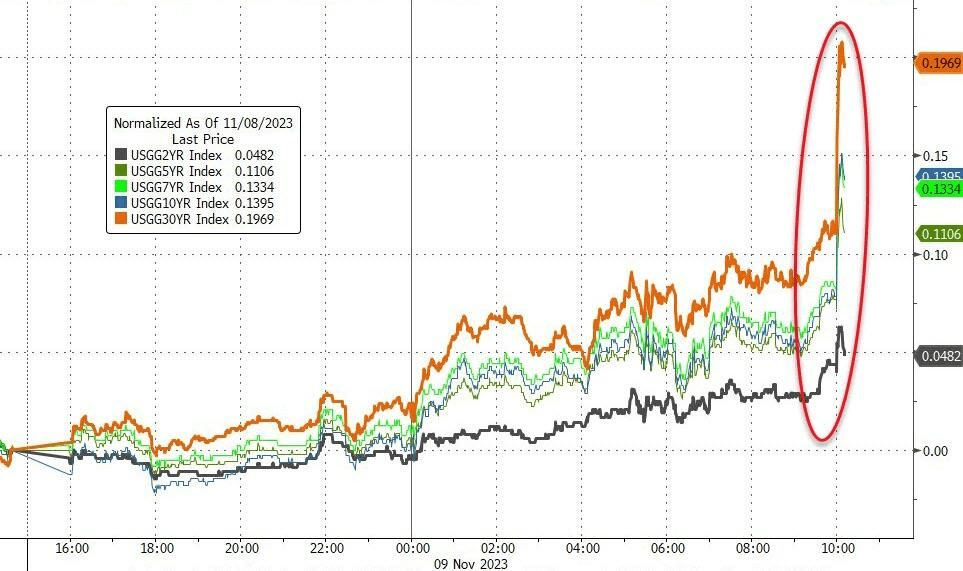

But the entire curve is higher in yields…

Stocks tanked…

Regional bank stocks tumbled…

The dollar ripped back up to pre-payrolls levels…

Finally, we note that this ugly auction comes as Treasury Liquidity is evaporating dramatically…

The Fed (and The Treasury) have a problem!! Particularly since the 30Y yield reversed course and is on the rise again.

And at the 10 year tenor, the rate rose to 4.638%.

All together now!!

The Edmund Fitzgerald, symbolic of the US under Biden and Janet Yellen.

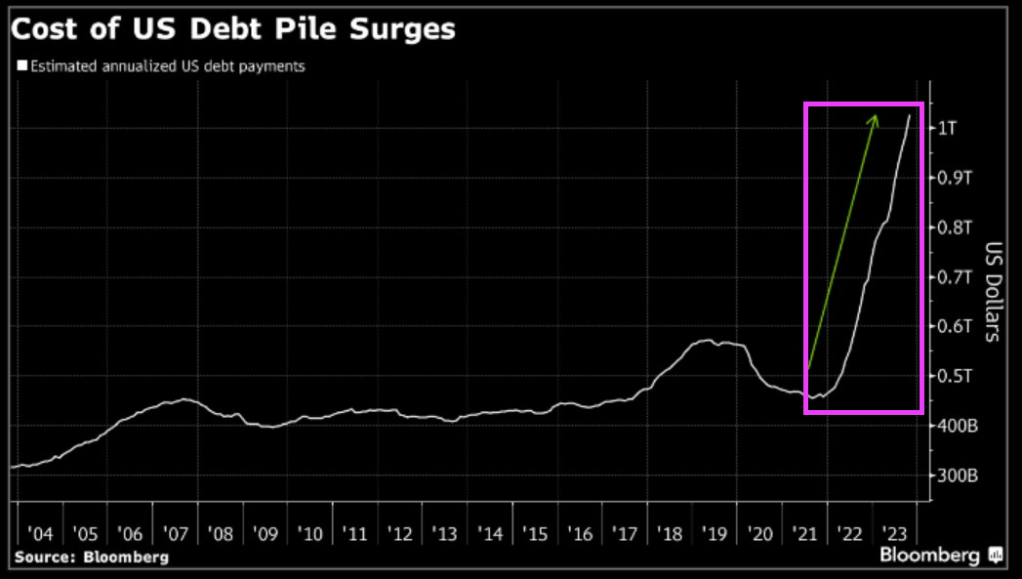

US Federal debt just hit $33.71 TRILLION. And unfunded liabilities (promises from Uncle Spam) are now $211 TRILLION. That is 526% of the the current debt load. Which means either lots of additional debt, higher tax rates or cuts in entitlements.

The cost of US debt continues to soars as The Fed combats Bidenflation.

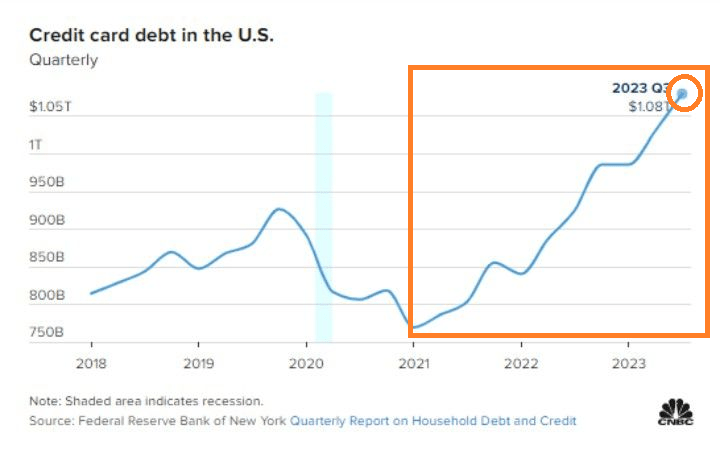

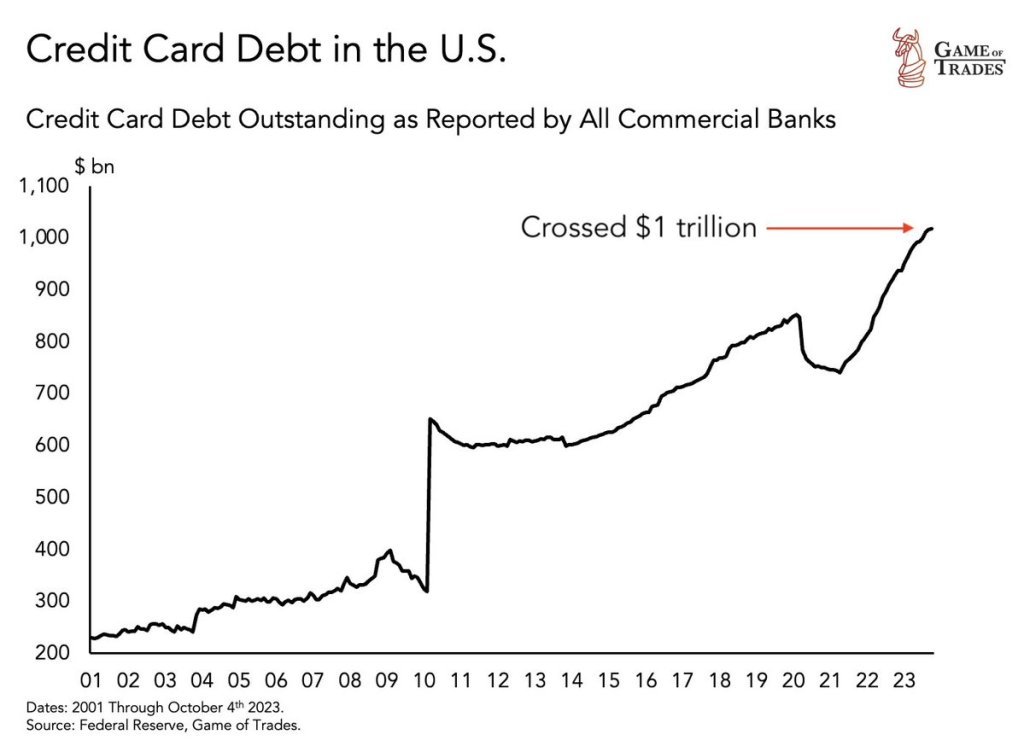

But it isn’t just Federal government debt that is exploding under Bidenomics. Consumer credit card debt has exploded under Bidenomics as consumer struggle with inflation.

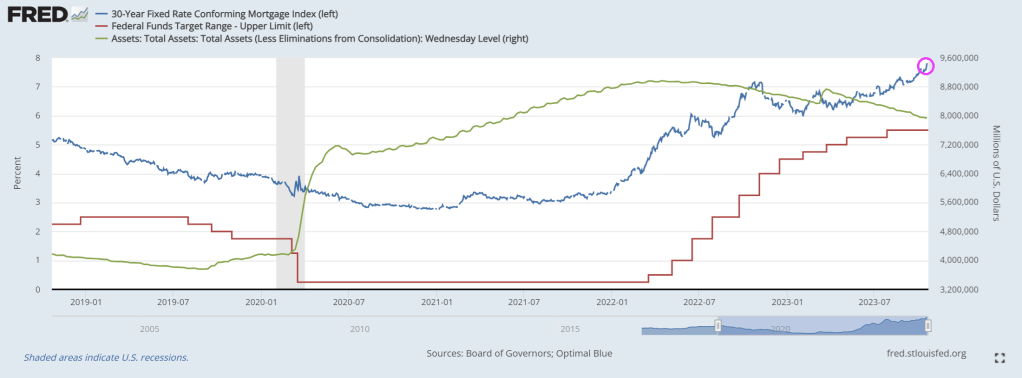

No, this isn’t the tilt effect in the mortgage market where inflation is front-loaded in mortgage rates making mortgage payments quite unaffordable. Although inflation is causing mortgage rates to be up 174% under Biden (while Biden continues to brag about how Bidenomics is helping). Meanwhile, the 10Y Treasury yield is up 402% under Biden (making refinancing the US staggering debt load more difficult to refinance. Higher mortgage rates tilt the present value of mortgage payments to the front, making housing even more unaffordable. Thanks Joe!

But the Tilt effect I am talking about is the TLT effect. TLT (iShares US Treasuries 20y+ ETF) calls. Friday was the largest TLT call volume ever.

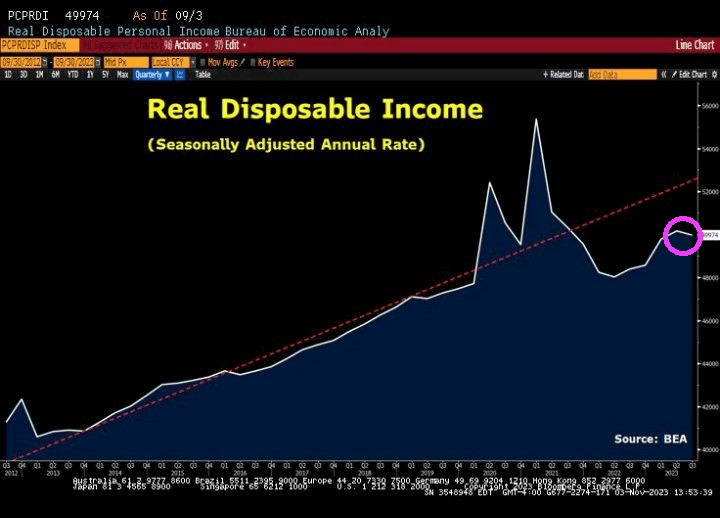

Meanwhile, US real disposable income is declining.

Bidenomics new theme song is “Addicted To Gov.” Bidenomics needs lots of Federal spending and borrowing to survive. But all this spending and borrowing is causing rapid price increases and other distortions.

Bidenomics has been a massive windfall for the top 1% of households in terms of wealth due to the emphasis on green energy transformation. But for the 99%, Bidenomics has been a disaster (unless you consider low-paying job creation a victory).

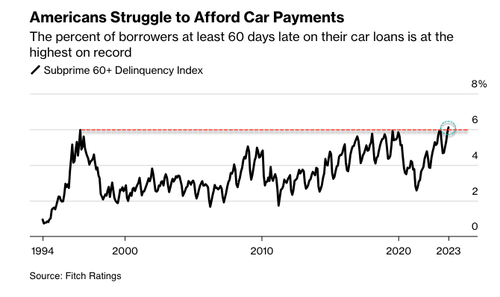

The auto sector, considered a leading economic indicator, pinpoints the arrival of the crushing auto loan crisis and even the possibility of the onset of the next recession. In late January, we Fitch revealed tat consumers are falling behind on auto payments – the most since the peak of the Great Financial Crisis. Fast forward nine months later, to September, that rate just hit the highest level in nearly three decades.

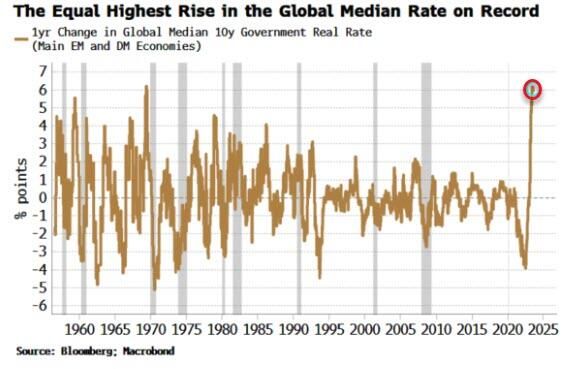

And with interest rates rising the fastest in history,

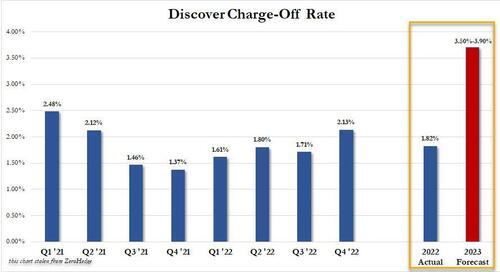

And Discover projected charge off rate for 2023 would more than double from its current 1.82% to as much as 3.90%!

In what could be the early innings of the auto loan crisis, something we called a “perfect storm” earlier this year, Bloomberg cites new Fitch data:

The percent of subprime auto borrowers at least 60 days past due on their loans rose to 6.11% in September, the highest in data going back to 1994, according to Fitch Ratings.

Source: Bloomberg

“The subprime borrower is getting squeezed,” said Margaret Rowe, senior director with Fitch.

Rowe said, “They can often be a first line of where we start to see the negative effects of macroeconomic headwinds.”

What has been widely known is the consumer has been funding car purchases with even more debt to afford record-high prices, with many monthly payments exceeding $1,000. Factor in the Federal Reserve’s most aggressive interest rate hiking cycle in a generation, elevated inflation, and the restarting of the federal student loan payments, tens of millions of consumers are under immense pressure this fall.

An endless stream of retailers, such as Walmart, Nordstrom, Macy’s, and Kohl’s – all of whom have recently warned about a consumer slowdown. Banks have also raised concerns, such as Morgan Stanley’s Mike Wilson, who believes the consumer is ‘falling off a cliff.’ And the latest high-frequency data from Barclays shows card spending has taken another leg down.

As delinquencies rise, Cox Automotive forecasts that 1.5 million vehicles will be seized this year, up from 1.2 million in 2022. That’s still below pre-pandemic levels, but the numbers could soar if a recession materializes in 2024.

Bloomberg cited Bankrate data that shows consumers with excellent credit can lock in an average interest rate of around 5.07% for a new car and 7.09% for a used vehicle. Those with bad credit should expect a new car rate of 14.18% and 21.38% for a used car.

The perfect storm we described earlier this year is unfolding.

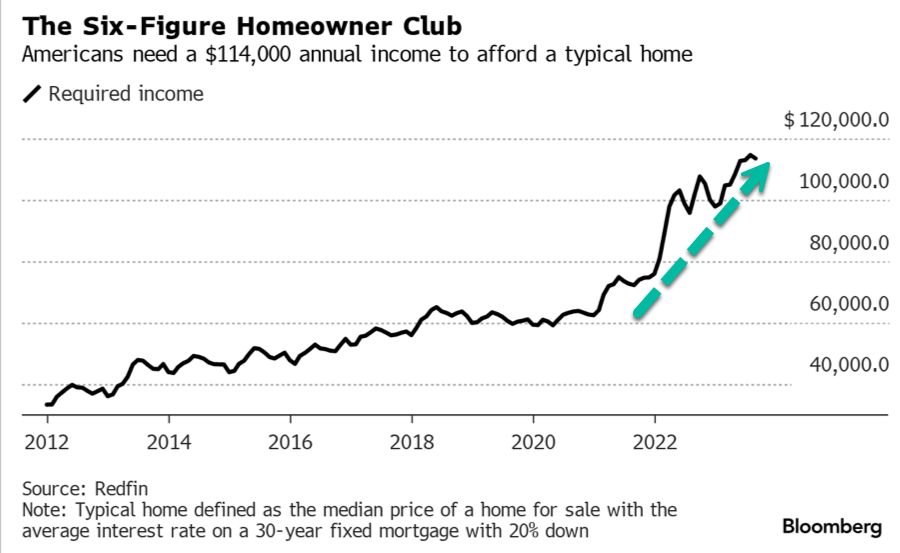

At least residential mortgage delinquency rates remain low. With elevated home prices, the incentive to default on a loan is limited.

So The Perfect Storm hasn’t hit residential real estate … yet. But with households needing $114,000 in annual income to afford a typical home …

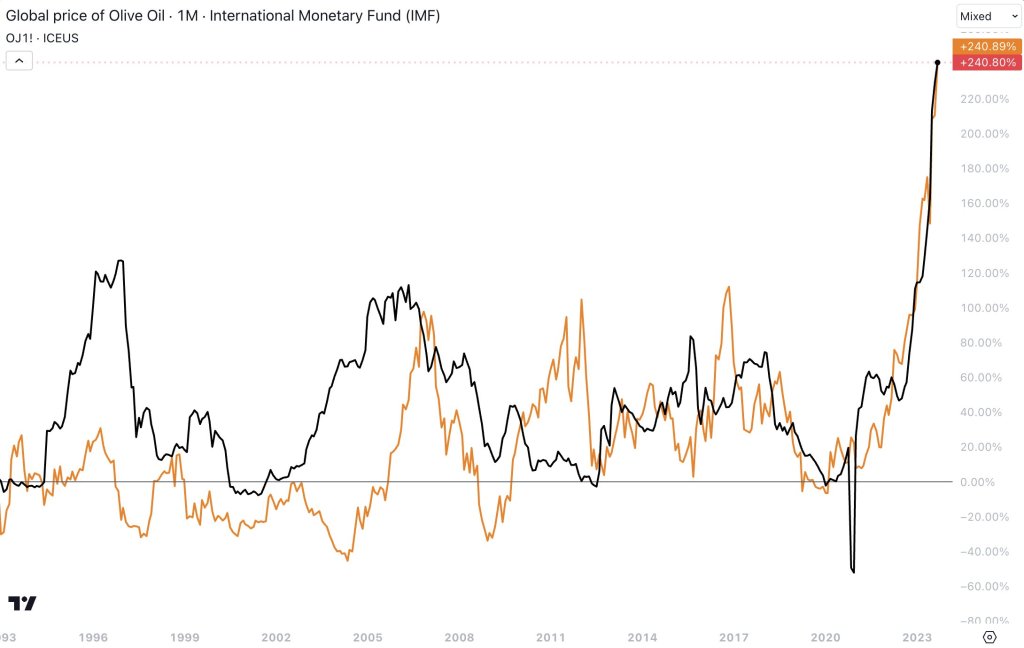

But at least home prices aren’t rising as fast as olive oil and orange juice!! Wow, that excesssive stimulypto by The Fed and Federal government is really screwing things up in the economy.

Biden is like George Clooney in “The Perfect Storm” sending the US out into stormy, violent seas while obessing about Ukraine and protecting Iran/Hamas.

Bidenomics strikes … again. No, not his inane ramblings about Hamas being “the other team” or that Hamas has to learn to shoot straight. But his policies freezing effects on the economy. Like housing.

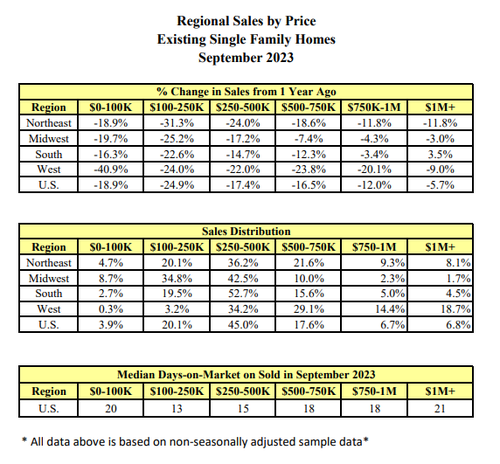

Existing-home sales faded in September, according to the National Association of REALTORS®. Among the four major U.S. regions, sales rose in the Northeast but receded in the Midwest, South and West. All four regions registered year-over-year sales declines.

Total existing-home sales – completed transactions that include single-family homes, townhomes, condominiums and co-ops – waned 2.0% from August to a seasonally adjusted annual rate of 3.96 million in September. Year-over-year, sales dropped 15.4% (down from 4.68 million in September 2022). … Total housing inventory registered at the end of September was 1.13 million units, up 2.7% from August but down 8.1% from one year ago (1.23 million). Unsold inventory sits at a 3.4-month supply at the current sales pace, up from 3.3 months in August and 3.2 months in September 2022.

The total existing home sales SAAR dropped back below 4mm for the first time since October 2010 (during the foreclosure crisis)…

Source: Bloomberg

Sales fell in all regions except the Northeast in September… and in every price range…

Single-family home sales fell to an annualized 3.53 million pace, the lowest since 2010. Condominium and co-op sales also declined.

“As has been the case throughout this year, limited inventory and low housing affordability continue to hamper home sales,” said Lawrence Yun, NAR’s chief economist.

“The Federal Reserve simply cannot keep raising interest rates in light of softening inflation and weakening job gains.”

First-time buyers made up a historically low 27% of purchases, down from the prior month.

Cash sales represented 29% of total sales, matching the highest level in over a decade. Investors, who often purchase with cash and are therefore less sensitive to mortgage rates, made up 18% of the market.

“It would be very unusual to have higher cash compared to first time buyers,” Yun said on a call with reporters.

And, if mortgage rates (and thus affordability) are anything to go by, things are about to get real…

Source: Bloomberg

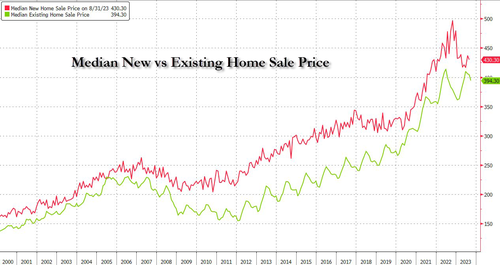

The median selling price rose 2.8% from a year earlier to $394,300, the highest September reading on record, pushing affordability even lower. But existing home prices are falling relative to new home prices (with the ratio near record lows)…

It looks like The House may elect a RINO as Speaker (Patrick McHenry, RINO-NC) to replace McCarthy. One RINO replacing another RINO … all so The House can continue its insane, inflation inducing spending.

We are Livin’ la vida Biden as Biden continues to push illegal immigration and working with Communist dictators like Venezuela’s Nicolas Maduro and NOT expand US energy production.

The Consumer Financial Protection Bureau (CFPB) and the Department of Justice (DOJ) released a joint statement telling financial institutions that while it is not illegal to consider a person’s immigration status in the decision on whether to lend money, an overreliance on it could run afoul of the law, according to the statement. The statement implicates the Equal Credit Opportunity Act (ECOA), which makes it illegal to discriminate on the basis of race, color, religion, national origin, sex and more in considering a person’s credit application as the mechanism, even though the law does not list citizenship status as a protected attribute.

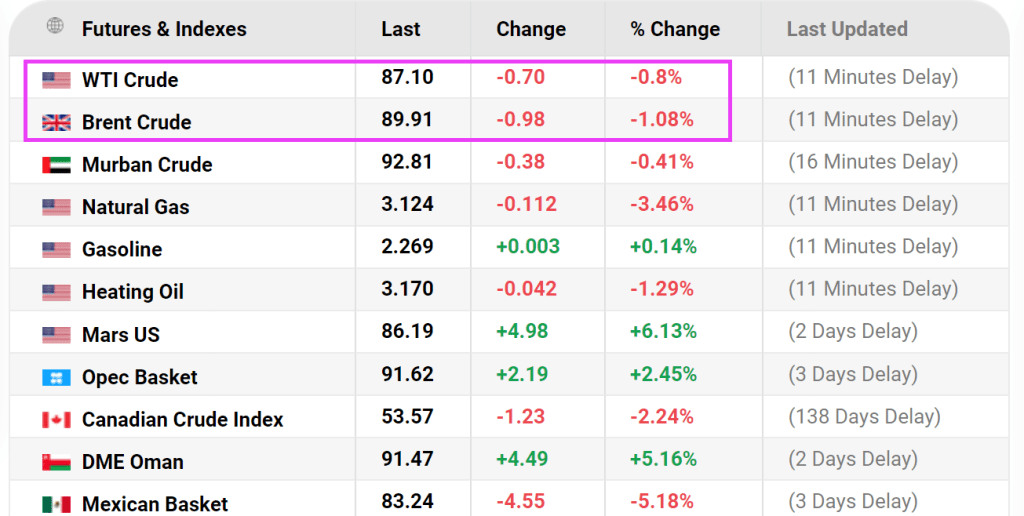

The result? WTI Crude is down almost -1% today and Brent Crude is down over -1%.

The sad part of Biden’s deal with brutal Marxist dictator Nicolas Maduro requires Venezuela to allow another candidate to run against Maduro in the next Presidential election. What? Biden and Democrats are working hard to eliminate Donald Trump from running for President in 2024, but want Venezuela to have competition??

So, Biden is sticking to his anti-US energy production stance while supporting a brutal Marxist dictator AND forcing banks to lend to illegal immigrants.

Joe Biden and brutal Marxist dictator Nicolas Maduro.

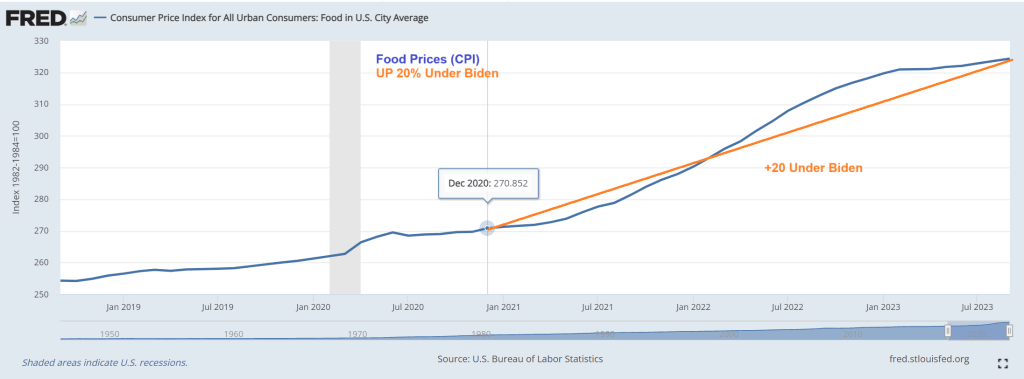

First, food prices are up 20% since December 2020. Talk about destruction of middle class wealth!

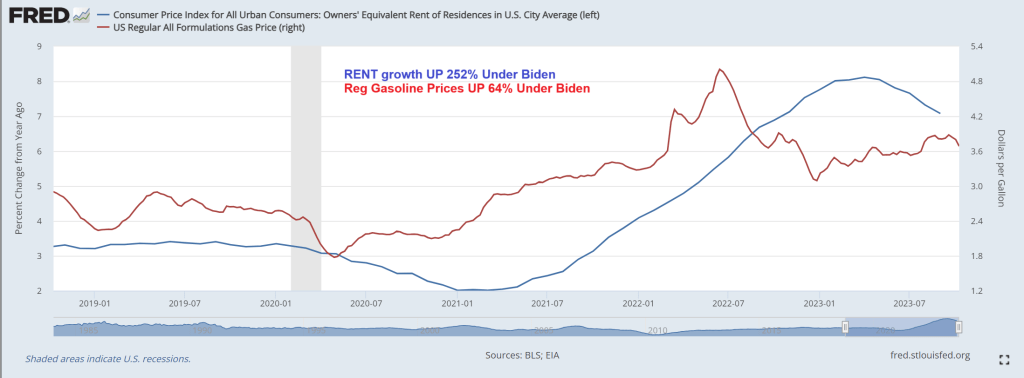

That is in addition to gasoline prices are up 64% under Biden while rent growth is up 252%. Well, Biden waived through millions of illegal immigrants and rent had to rise. Biden and Washington DC’s broken borders is Livin’ La Vida Loco.

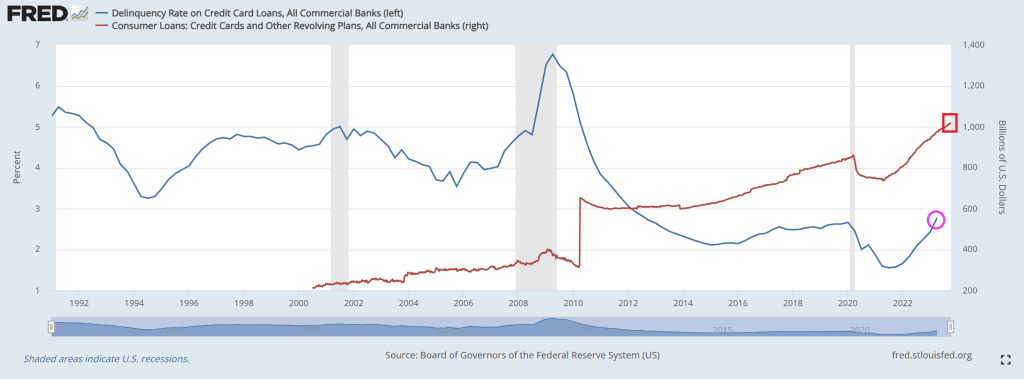

To cope with inflation (that Paul Krugman claims is over but the last inflation report showed that the tinders of inflation are hard to extinguish), consumers have turned to credit cards to survive. In fact, credit cards have expanded 38% since April 2021 despite rapidly rising interest rates. And credit card delinquency rates are rising and are now above Covid-era economic shutdown levels.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.