What a mess Biden and his Progressive backers have made. And we are forced to suffer the consequeinces of his policies. Or follies!

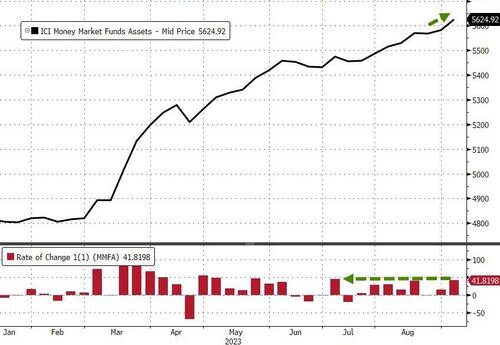

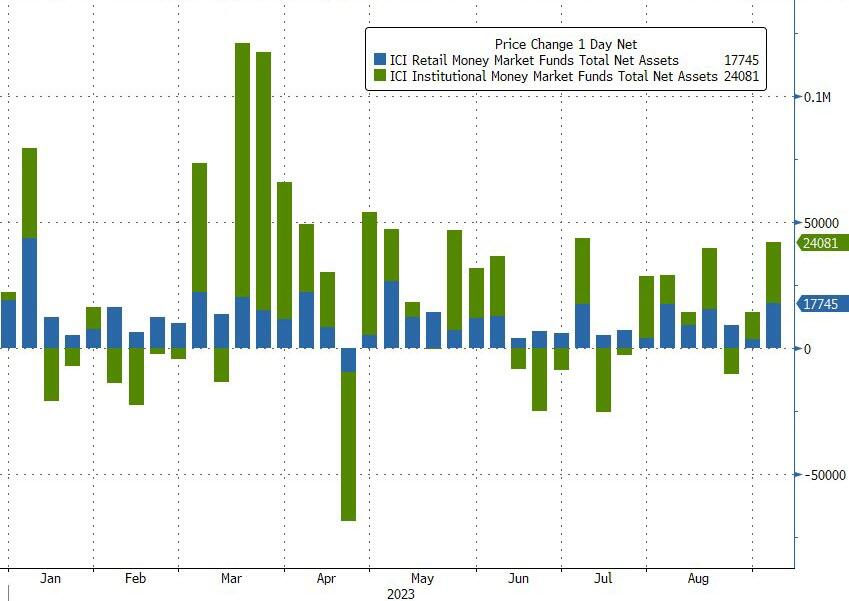

Money-market funds saw inflows for the 7th week of the last 8 with a $42BN jump (the most in 2 months) to a new record high of $5.625TN…

Source: Bloomberg

The inflow was dominated by a $24BN increase in Institutional fund assets while Retail also saw a sizable $17.7BN increase…

Source: Bloomberg

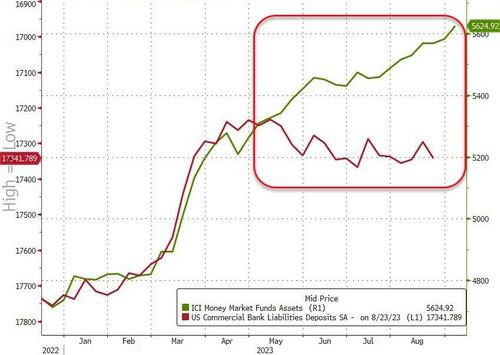

And the divergence between money-market fund assets and bank deposits continues to grow…

Source: Bloomberg

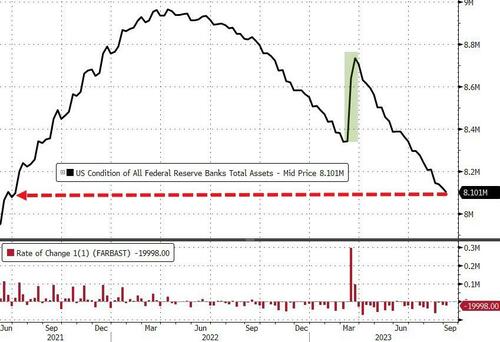

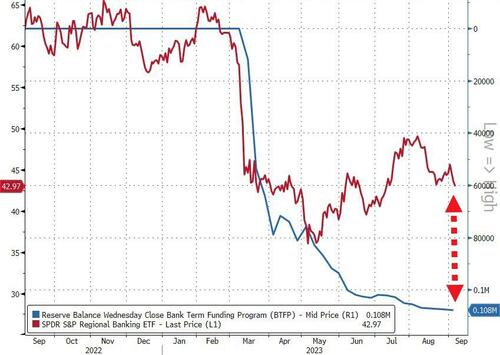

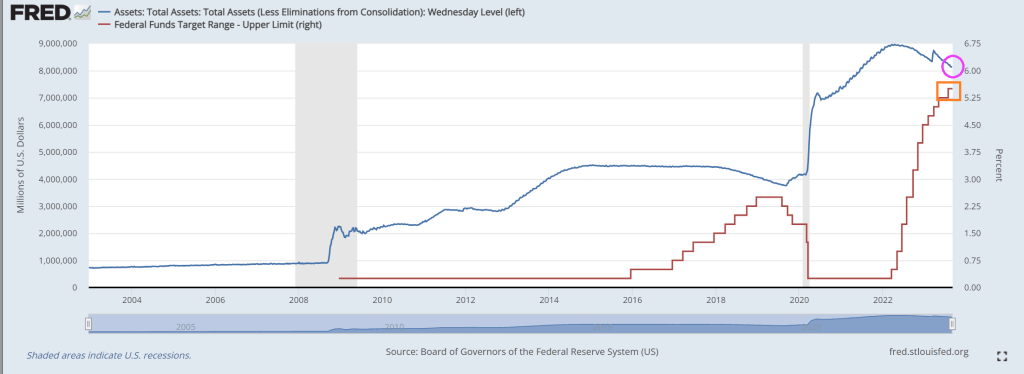

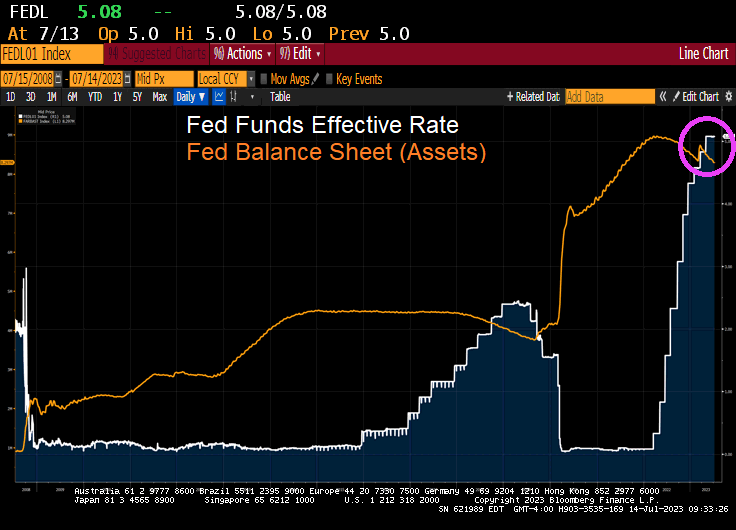

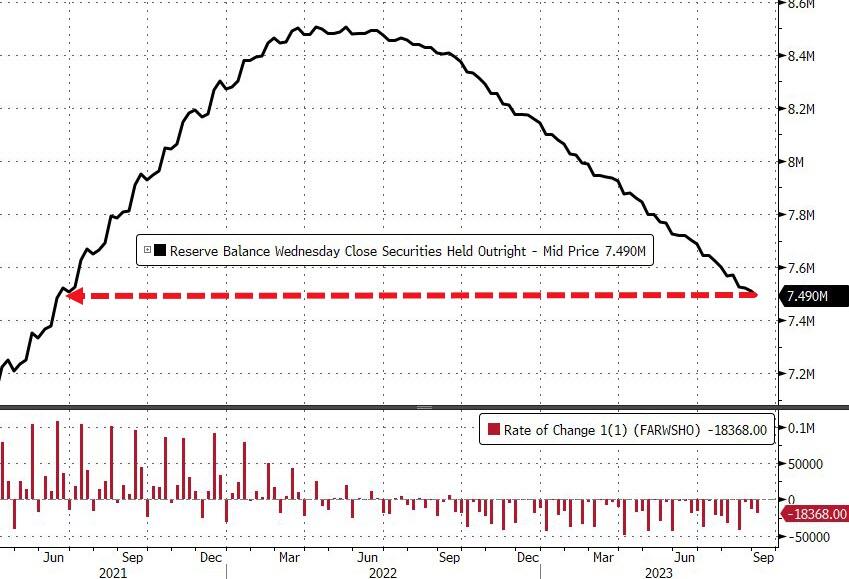

And while we actually saw huge deposit outflows (on a non-seasonally-adjusted basis) – despite The Fed’s seasonally-adjusted deposits increase – The Fed balance sheet shrank by another $20BN last week to its smallest since June 2021…

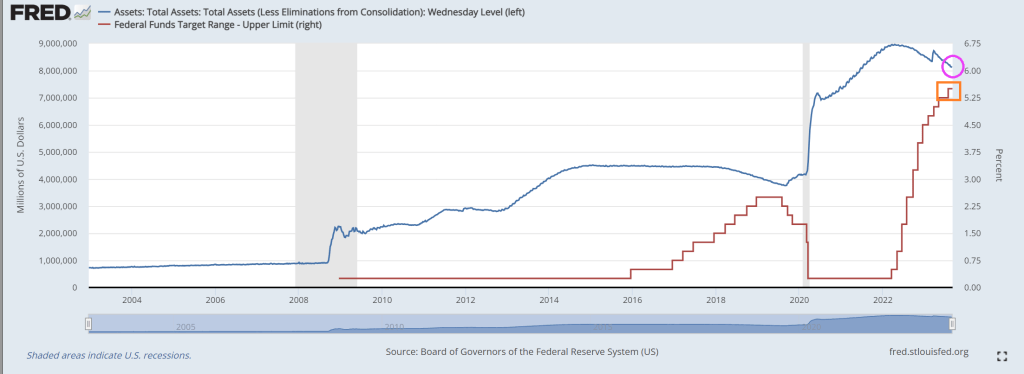

Source: Bloomberg

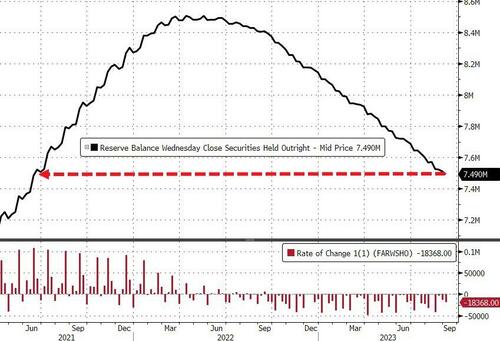

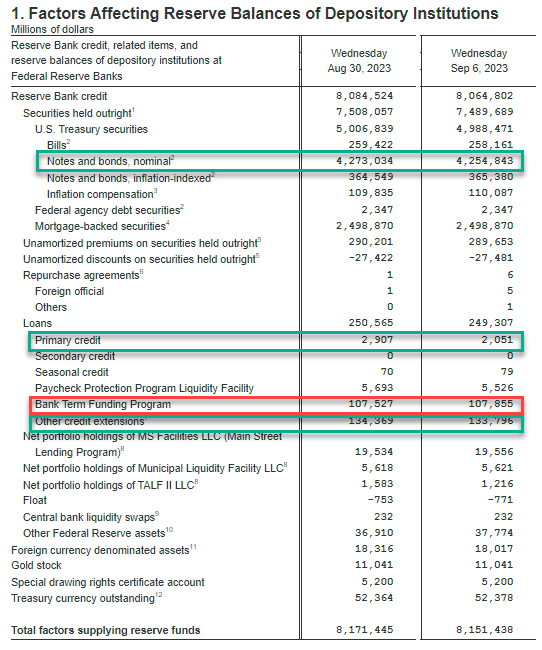

The Fed’s QT program continues apace with$18.4BN sold last week to its smallest since June 2021…

Source: Bloomberg

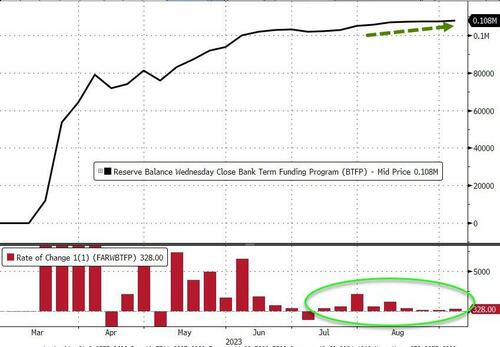

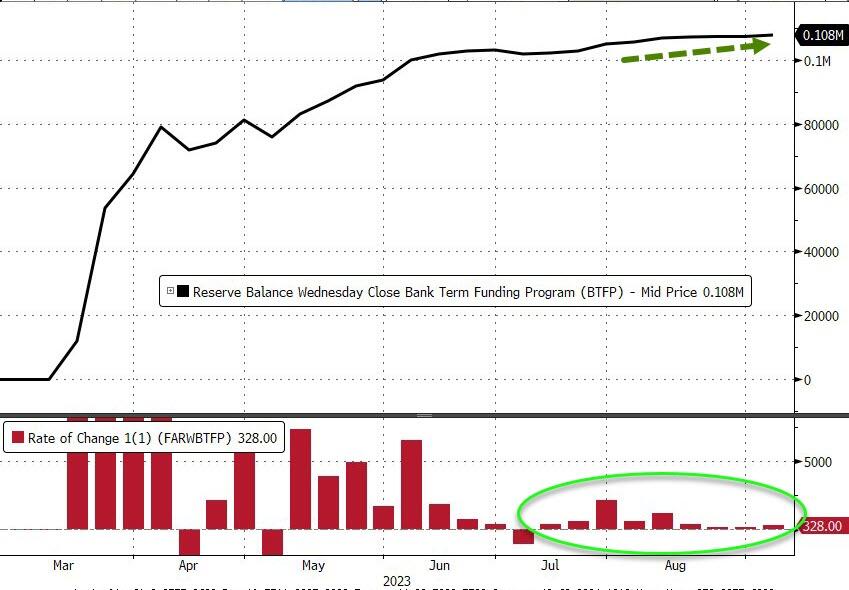

Usage of The Fed’s emergency bank funding facility jumped by $328 Million last week to a new high of $108BN…

Source: Bloomberg

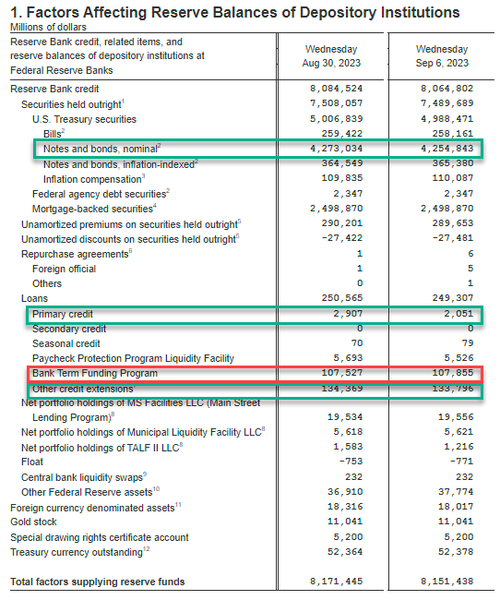

Fed BS weekly change:

- Fed balance sheet QT (Notes and bonds decline): $4.255 trillion, down $18,2BN

- Discount Window $2.1BN, down $800M from $.29BN

- BTFP new record $107.9BN, up $400MM

- Other Credit Extensions (FDIC Loans): $133.8BN, down $0.6BN from $134.4BN

Finally, US equity markets and bank reserves at The Fed have converged a little recently, but the gap remains wide (thanks to the plunge in reverse repo balances)…

Source: Bloomberg

Tick, tock, banks!

Source: Bloomberg

You have six months to figure out how to clean up the $108 Billion hole in your balance sheet that you’re currently paying The Fed’s exorbitant rates to fill.

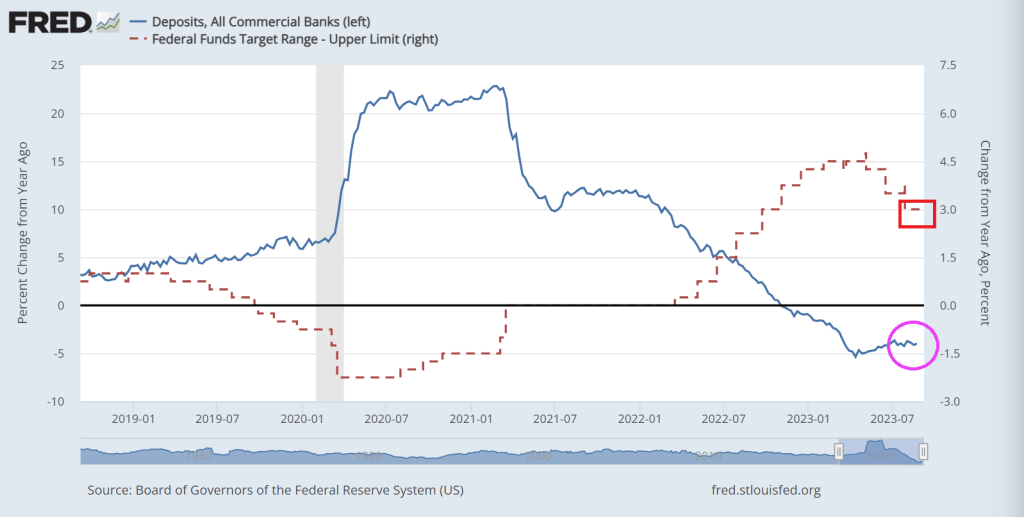

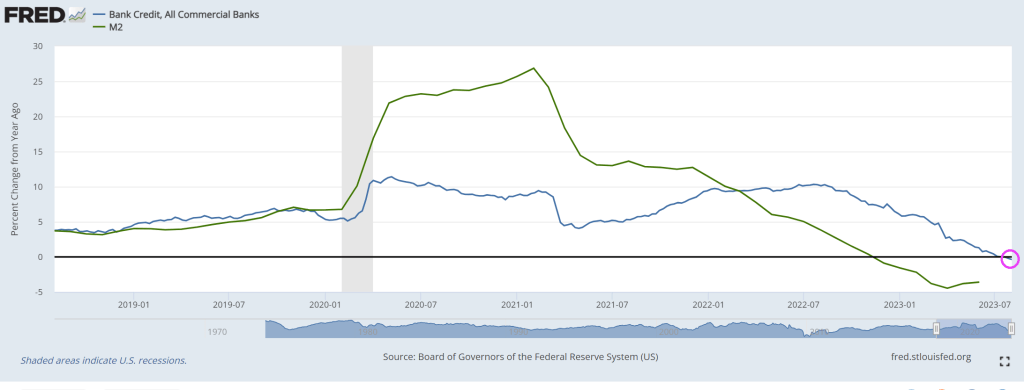

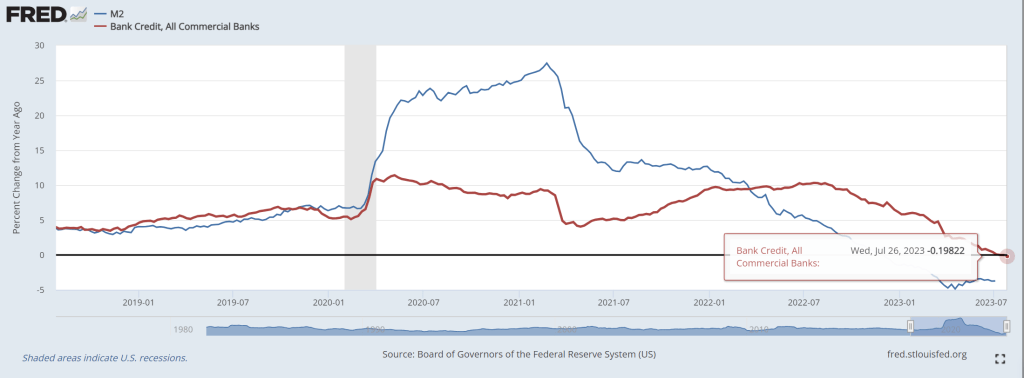

Bank deposit growth remains negative as The Fed tightens its overly accomodative monetary policy.

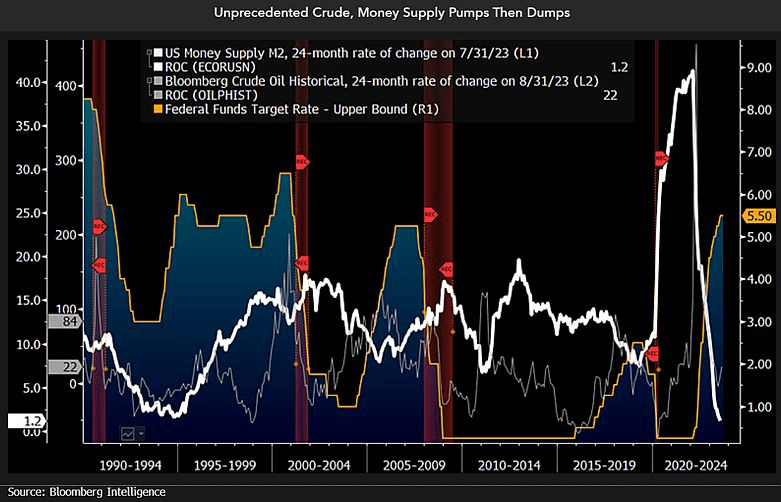

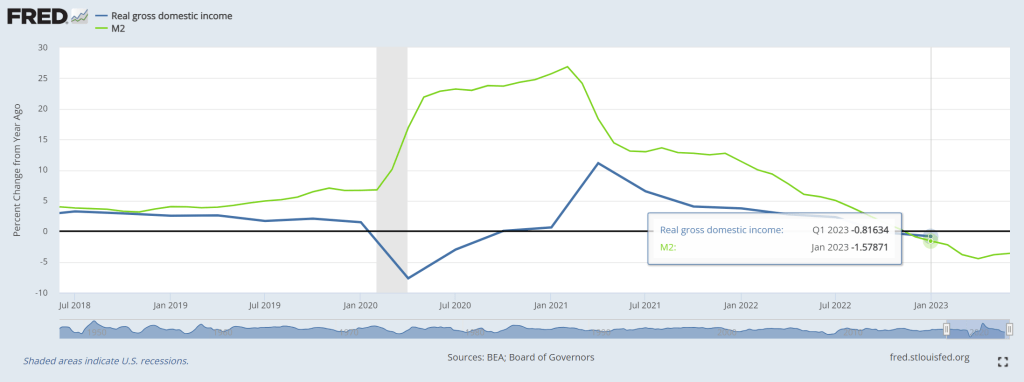

And then we have this chart showing plinging M2 Money (white line fever).

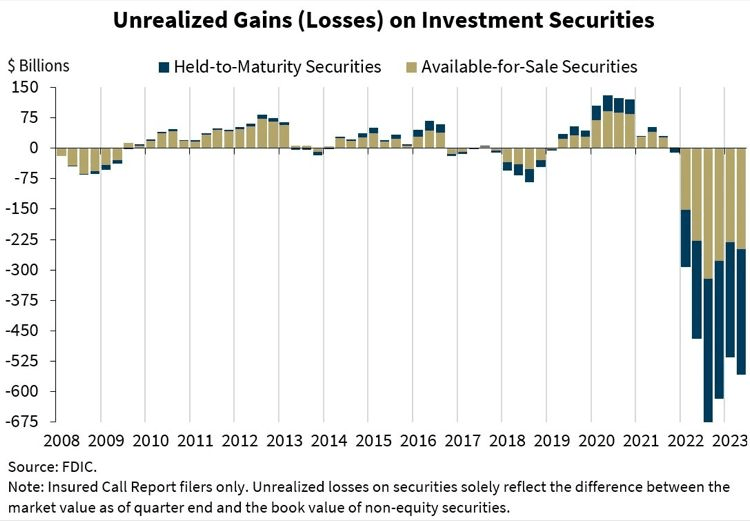

And the horrific unrealized losses on bank’s books.

Bidenomics is failing America. Primarily because Biden was one of the stupidest members of the US Senate. Not to mention nasty. Great President, America! /sarc

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.