We are seeing a slowing of the US economy. For example, the JOLTs (job openings) numbers are out for June and they are down -5.5% from May. And from April to May, JOLTs declined -3.2% MoM. That is a clear slowing trend.

And on the housing front, the CoreLogic HPI Forecast indicates that home prices will increase on a month-over-month basis by 0.6% from June 2022 to July 2022 and on a year-over-year basis by 4.3% from June 2022 to June 2023. But rose +18.3% YoY in June. Also a clear cooling trend.

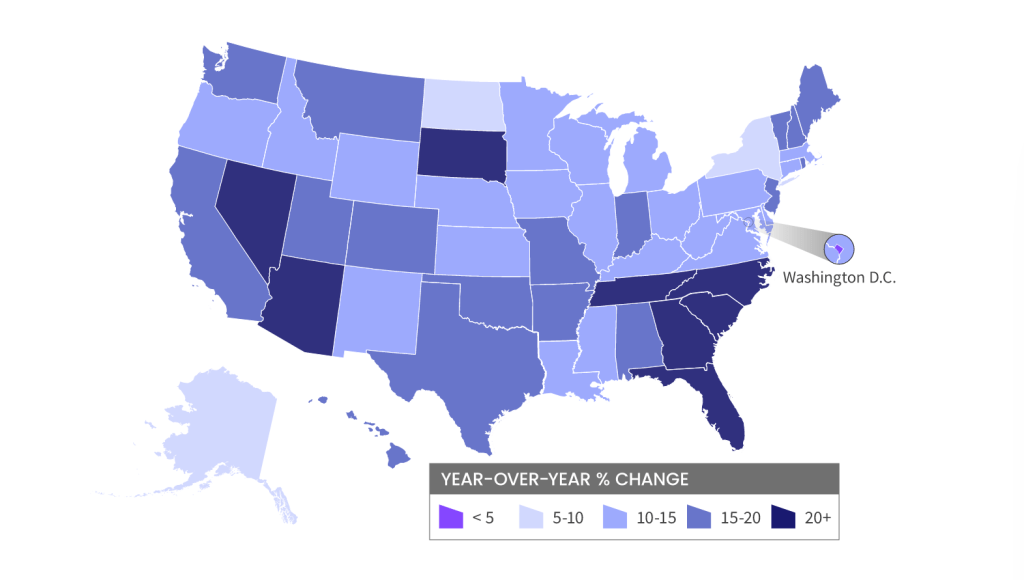

And its “Escape From Blue States” (perhaps a new Kurt Russell movie), with home prices rising fastest in red states (primarily The South). And contiguous migration from California to Nevada and Arizona.

The Fed Funds Futures market is pricing in rate hikes until the March 2023 FOMC meetings. After all, Prince Imhotep (aka, Minneapolis Fed’s Neel Kashkari) is screaming for more rate hikes to fight inflation … caused by 1) loose monetary policies since late 2008 and 2) insane Federal government spending.

Let’s see if “Mr. Freeze” (aka, Jerome Powell) relents on Fed rate increases before the March 2023 FOMC meeting.

The spendiholics in Washington DC (aka, Biden and Congress) have passed yet another inflationary legislation, this time the sadly misnamed “The Inflation Reduction Act” since it will likely lead to a furthering recession of the US economy. Well, that is one way to reduce inflation: cause a recession and job loss.

An analysis by the National Association of Manufacturers says the tax in 2023 alone will reduce real GDP by $68.5 billion and cut labor income by $17.1 billion. One well-known economic truth is that corporations don’t really pay taxes (they pass on taxes to consumers in the form of higher prices). They are essentially tax collectors, as the corporate tax rate ultimately falls on some combination of workers, shareholders and customers. Raise the corporate tax rate, and you’re cutting wages and salaries for workers.

“Americans are already experiencing the consequences of Democrats’ reckless economic policies. The mislabeled ‘Inflation Reduction Act’ will do nothing to bring the economy out of stagnation and recession, but it will raise billions of dollars in taxes on Americans making less than $400,000,” said Sen. Mike Crapo, an Idaho Republican who sits on the Senate Finance Committee as a ranking member, and who requested the analysis.

“The more this bill is analyzed by impartial experts, the more we can see Democrats are trying to sell the American people a bill of goods,” Crapo added.

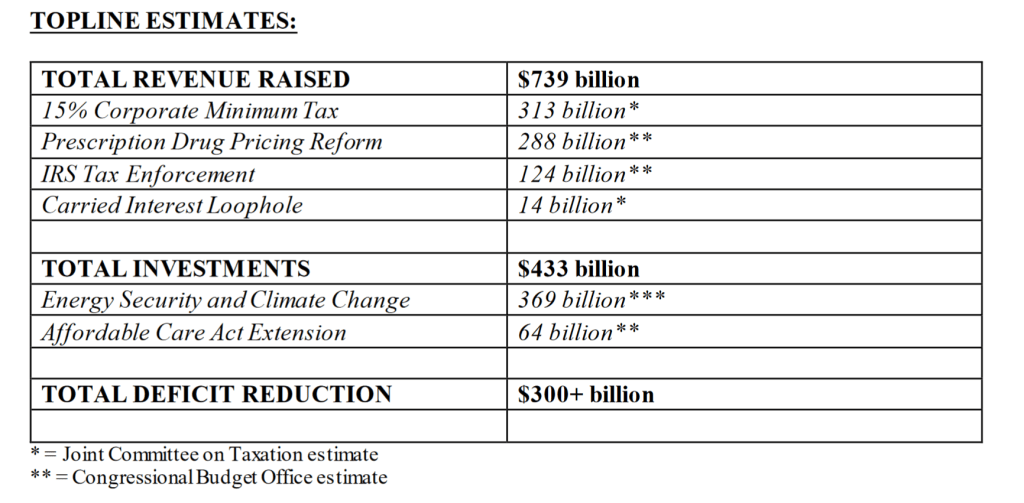

According to Schumer and Manchin, “The Inflation Reduction Act of 2022 will make a historic down payment on deficit reduction to fight inflation, invest in domestic (green) energy production and manufacturing, and reduce carbon emissions by roughly 40 percent by 2030. The bill will also finally allow Medicare to negotiate for prescription drug prices and extend the expanded Affordable Care Act program for three years, through 2025.”

No wonder House Speaker Nancy Pelosi took her extensive entourage on a paid vacation to Singapore, Malaysia and perhaps Taiwan. Its called “Getting out of Dodge.” If Pelosi believed in this legislation, she could have “saved the environment” by simply doing a Zoom call. Then again, Biden’s Climate Envoy, John Kerry, still travels the globe trying to sell green energy and carbon reductions in his private carbon-spewing jet. But I forget, Biden, Pelosi, Schumer and Kerry are our elites who deserve platinum treatment, not lowly serfs like 99% of the US population.

So, here we go loop-de-loop. Politicians want to spend money on their friends and donors and then raise taxes on the rest of us.

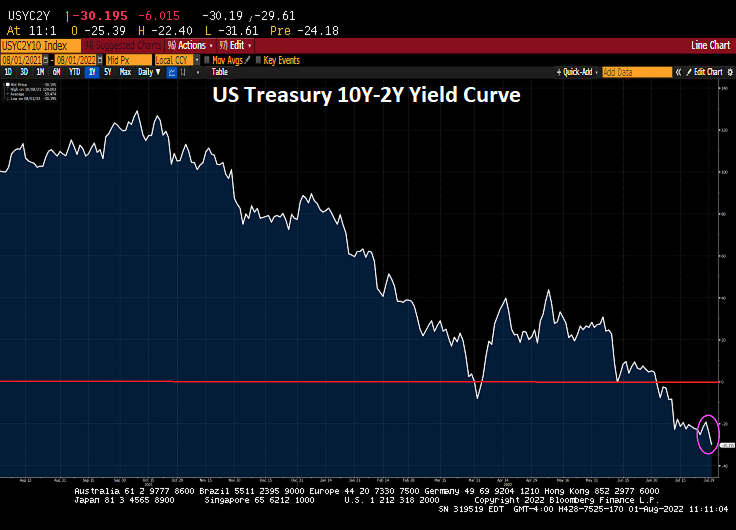

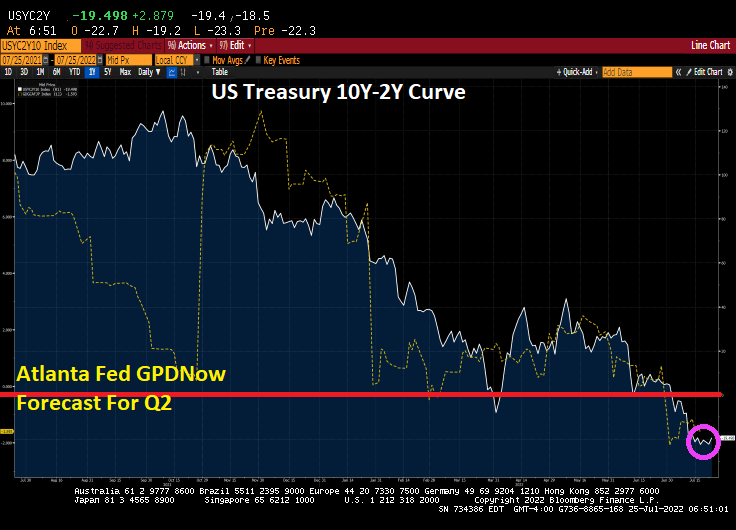

On the recession front, the 10Y-2Y US Treasury yield curve just flattened another -6.015 basis points to an inverted -30.195 basis points.

After breaking the 6% barrier back in June 2022, Bankrate’s 30-year mortgage rate has backed-off to 5.28% despite Federal Reserve rate hikes.

The reason for the decline in the US Treasury 10-year is, amongst other things, a global economic slowdown (partly due to the US and Europe “going green” and cutting the supply of fossil fuel-based energy). Instead of “The Great Reset,” I call it “The Great Economic Suicide.” The 10-year US Treasury yield and Bankrate’s 30-year mortgage rate are declining with declining global GDP.

US inflation, based on June’s Personal Consumption Expenditures (PCE) deflator, rose to its highest level since 1982. The PCE Deflator YoY rose to 6.8% while the core PCE deflator (less food and energy, the two things more households care about) rose to 4.8% YoY in June.

In order to fight inflation, The Federal Reserve is going to have to raise their target rate to … 17.78% based on 6.80% PCE deflator YoY. We are currently at 2.50%.

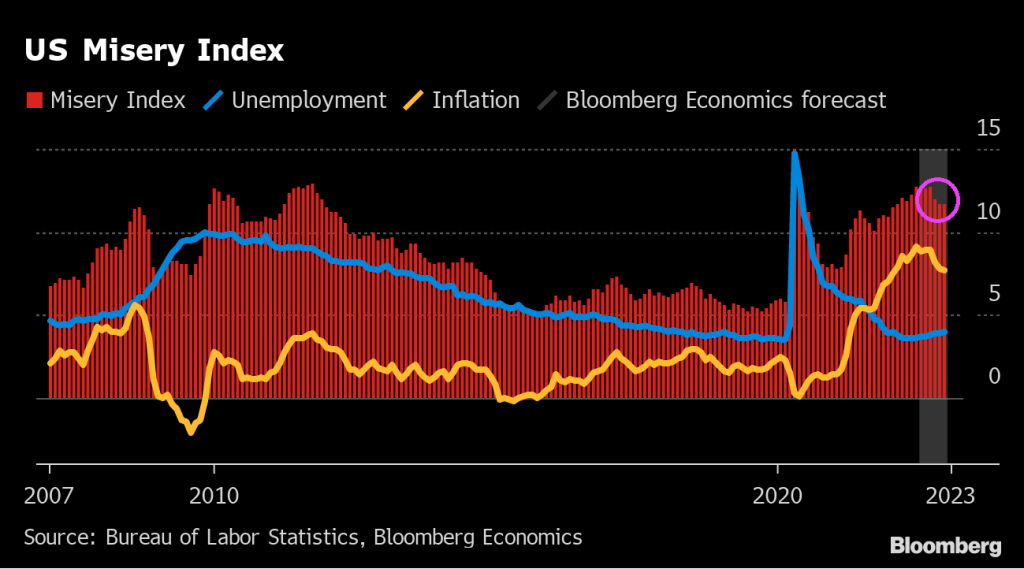

The US Misery Index remains elevated.

Based on the PCE Deflator YoY and U-3 unemployment, the misery index remains elevated compared to before Covid and The Fed’s/Federal government hyper-stimulypto to counter the Covid economic shutdowns. We never fully recovered.

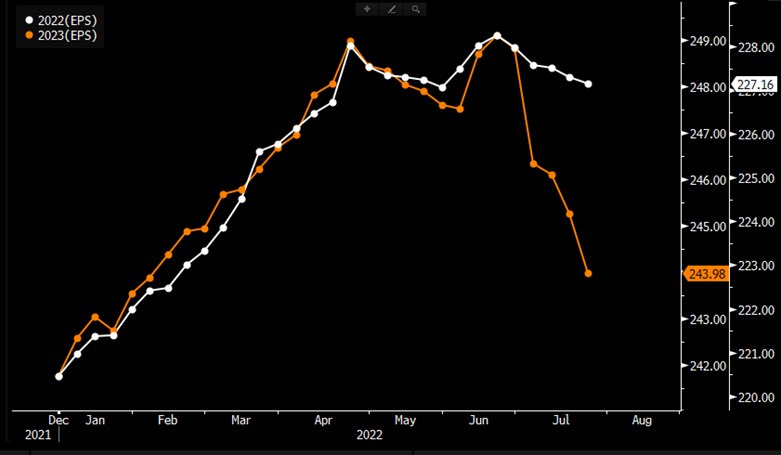

S&P 500 2023 EPS expectations falling off a cliff (orange line).

My former colleague at Deutsche Bank, Joe Carson, said recently that the US economy is not in a recession, but corporate profits are in a recession. While I cling to the traditional definition of recession (two consecutive quarters of negative real GDP growth), there is another component of the US economy that is in recession: consumer sentiment.

The University of Michigan Consumer Sentiment Index rose slightly in the latest release, but remains depressed at 51.5. University of Michigan Buying Conditions for House also rose to 47.0, also a depressed reading.

While unemployment remains low, the price of gasoline is crushing the wallets of American households helping to cause a recession in consumer sentiment.

Biden feebly attempts to explain why 2 consecutive quarters of negative real GDP growth (better known as contraction) is NOT a recession.

Hold on, The Fed is coming! To raise their target rate by 75 basis points at Wednesday’s FOMC meeting. Will this stem the tide of rising inflation?

Under Biden, we have seen regular gasoline prices rise 82% despite recent declines. Diesel fuel is up 121% and foodstuffs are up 46%. And house rents keep rising at a staggering 14.75% YoY. The recent declines is more due to the global economic slowdown and central bank rate increases than anything Washington DC is doing.

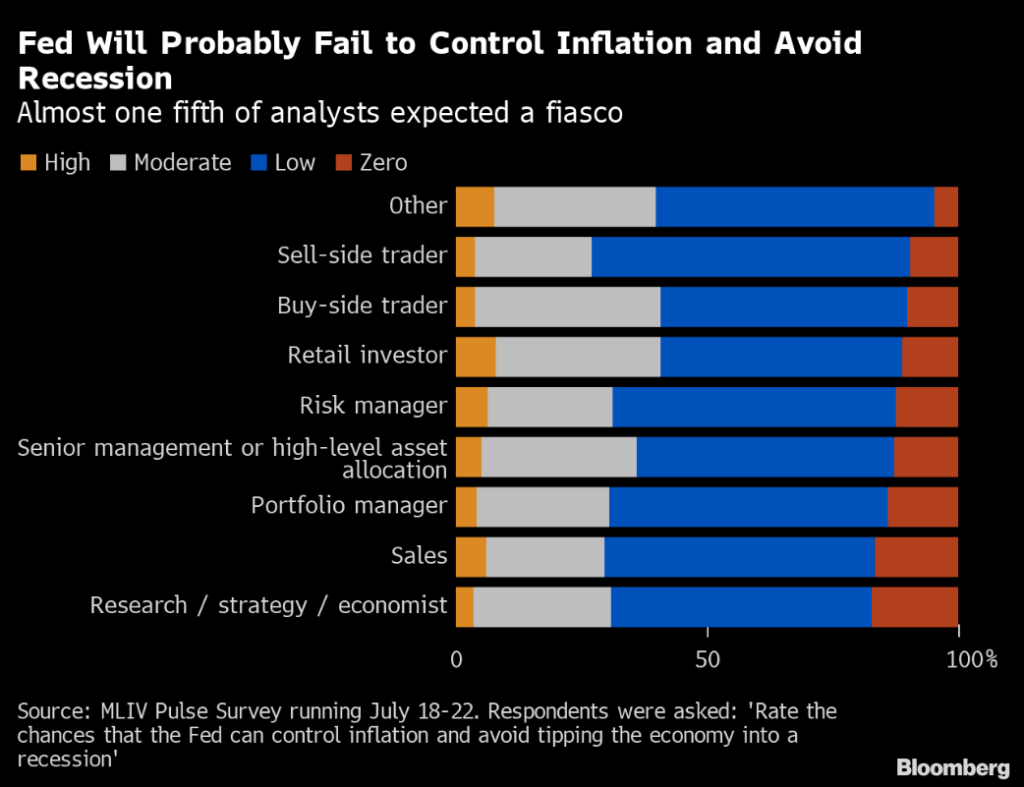

(Bloomberg) Investors are skeptical that the Federal Reserve can tame the worst inflation in four decades without driving the economy into a recession.

That’s bad news for Americans, who face the prospect of a downturn as their bills for food, rent and fuel swell. But to bond investors hit by deep losses this year, it may mean any further pain will be short-lived, as a recession will spark the US central bank to cut rates next year. That’s according to the results of the latest MLIV Pulse survey.

Over 60% of 1,343 respondents in the survey said there’s a low or zero probability that the US central bank can rein in consumer-price pressures without causing an economic contraction. The survey was conducted July 18-22 and included retail and professional investors.

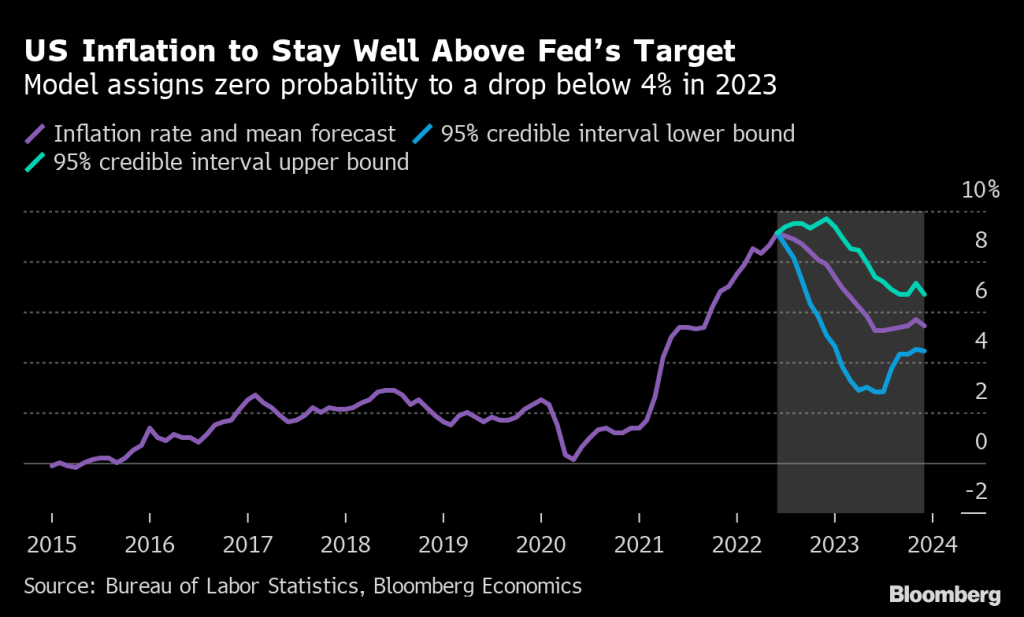

US inflation may be close to a peak, but it’s very likely to stay above 8% through year-end. Bloomberg Economics’ model assigns zero probability to a drop below 4% in 2023. Taken together with increasing recession risks, the Fed faces a tough balancing act as it attempts to bring stubborn price pressures under control without tipping the economy into contraction.

Of course, The Federal Reserve doesn’t really consider energy or food inflation, which are typically higher than core inflation. But going into Wednesday’s meeting, we see the US Treasury 10Y-2Y curve remains inverted (a signal of impending recession) and the Atlanta Fed GDPNow Q2 tracker at -1.6% after a negative Q1 reading.

Will raising the target rate (or ACTUALLY shrinking their balance sheet) reduce inflation? We shall see, but it has got to be better than Lawrence Summer’s suggestion to reduce inflation: raise taxes. Wait a minute, Larry. Inflation was caused by 1) overstimulus by The Fed combined with 2) massive Covid spending by Biden, Pelosi, Schumer and 3) Biden’s anti-fossil fuel policies. So instead of suggesting a decrease in Federal spending, Summer’s wants to give MORE of your money to Biden and Congress to spend. What an unbelievable nitwit.

Here is a picture of Larry Summers, Jay Powell and Janet Yellen attending the FOMC meeting in Washington DC.

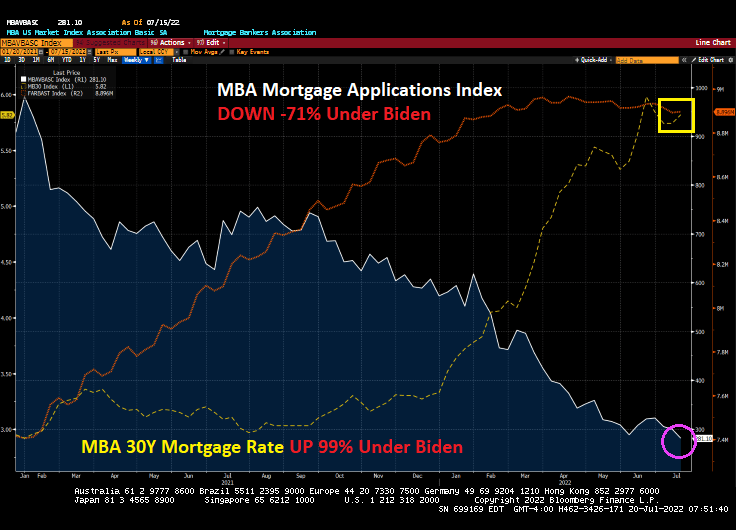

Mortgage applications declined for the third week in a row, reaching the lowest level since 2000.

Mortgage applications decreased 6.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 15, 2022.

The Refinance Index decreased 4 percent from the previous week and was 80 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index increased 16 percent compared with the previous week and was 19 percent lower than the same week one year ago.

Heartache #1: Mortgage rates have risen 99% under Biden.

Heartache #2: Mortgage application have fallen -71% under Biden.

As The Federal Reserve continues to fight inflation caused by 1) excessive stimulus by The Federal Reserve and Federal government surrounding Covid and 2) Biden’s energy policies, we are seeing the mortgage market as collateral damage.

The US is short on supply of housing for a myriad of reasons (high costs, Not-in-my-backyard (NIMBY) local zoning laws, etc), but The Fed’s cranking up interest rates isn’t helping.

US housing starts, a measure of supply, declined -6.3% YoY in June as The Fed cranked up rates.

1-unit (aka, single family detached) starts dropped -8.05% MoM in June while 5+ unit (aka, multifamily) starts rose 15% MoM.

1-unit permits dropped -8% MoM in June while 5+ unit starts were up 13% MoM.

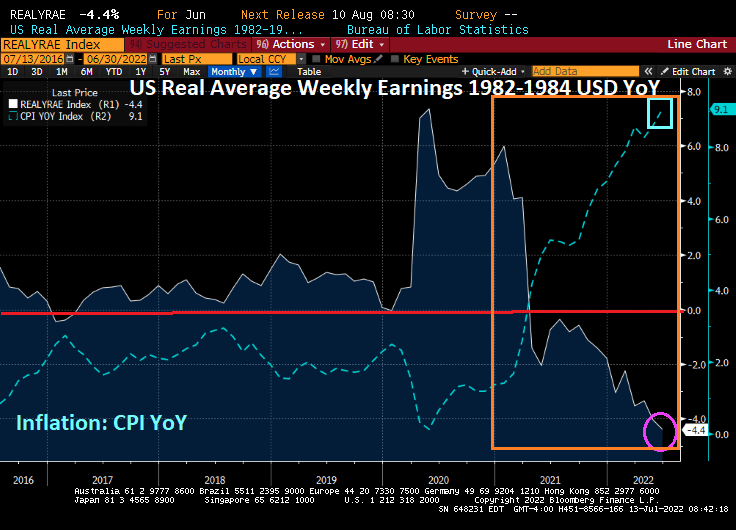

The reason? REAL weekly earnings growth declined -4.4% YoY in June thanks to Bidenflation.

You must be logged in to post a comment.