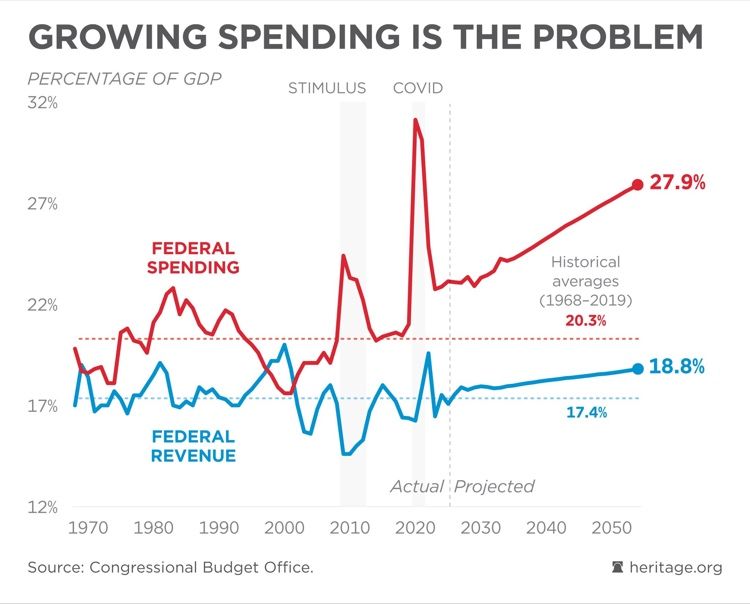

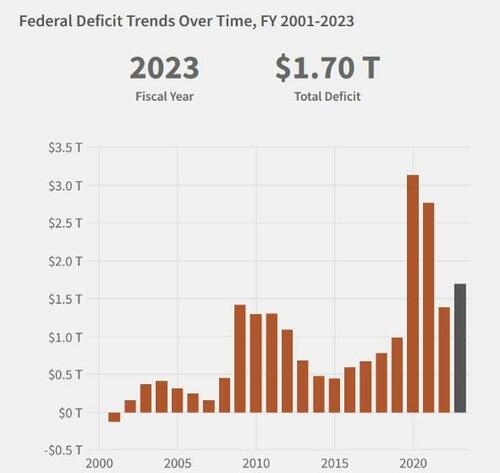

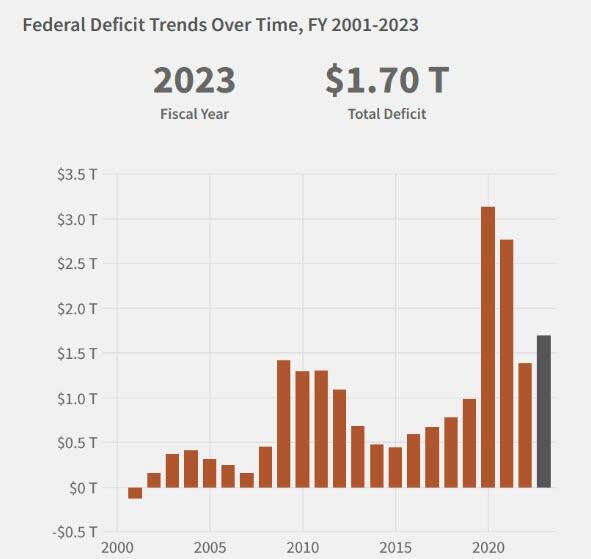

Following yesterday’s release of Biden’s $7.3 trillion budget, the Biden administration bragged about lowering the deficit by $3 trillion over the next decade – an average of 0.8% of GDP over that period.

This would consist of roughly $2.6 trillion over 10 years in additional spending programs, offset by around $4.8 trillion in tax increases over the same period. Most of the tax and spending proposals have been included in prior budget proposals from the White House, according to Goldman’s Alec Phillips, however there are several new items.

The budget would increase the corporate alternative minimum tax on book income from 15% to 21%, raising $137 billion over the next decade. It also limits a corporation’s ability to deduct employee pay exceeding $1mm/year, raising $272 billion over 10 years. The largest proposed tax increases include; raising the corporate minimum tax from 21% to 28%, as well as a series of tax increases on high-income earners, including new Medicare taxes, and a new 25% minimum tax on incomes over $100 million, raising $500 billion over the next decade.

Of course, it has zero chance of passing under the current Congress – but that’s not the point.

As one DC strategist wrote in a morning email noted by CNBC‘s Brian Sullivan, the budget deficit will still grow by another $16 trillion over the next decade – and that’s with aforementioned tax hikes.

Without them, the deficit grows to $19 trillion.

In short, talk of ‘$3 trillion saved’ is total bullshit in the grand scheme of things, given how much the national debt will grow in the best case scenario.

“No family budget or business could exist with this kind of math,” says Sullivan.

Yes Brian, no family budget could exist with this kind of math AND SPENDING!

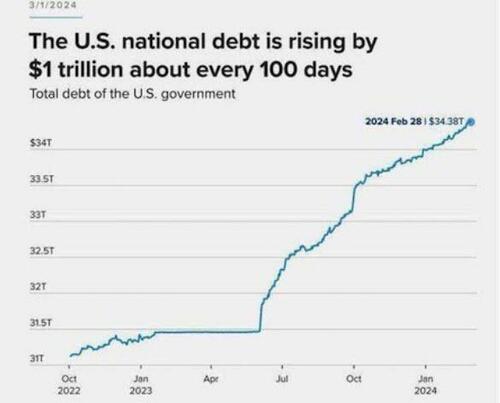

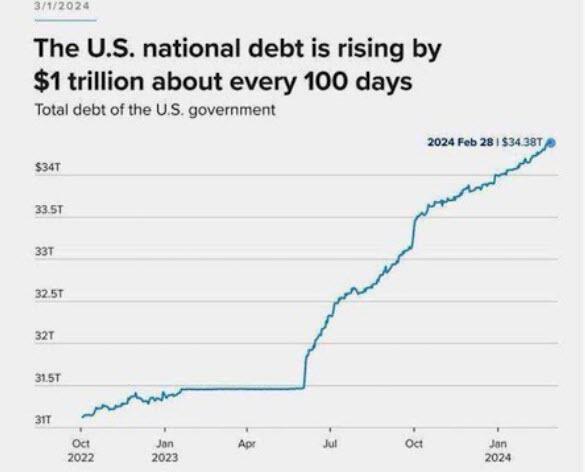

And the national debt is rising by $1 TRILLION every 100 days. Before Spending Joe’s budget!

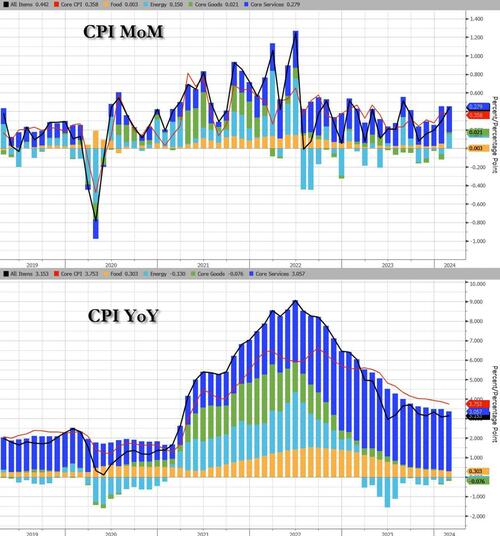

Unlike what Grand-dad Joey Biden screamed at the State of The Union (SOTU) address, inflation is NOT been defeated. In fact, inflation has defeated Biden and The Federal Reserve.

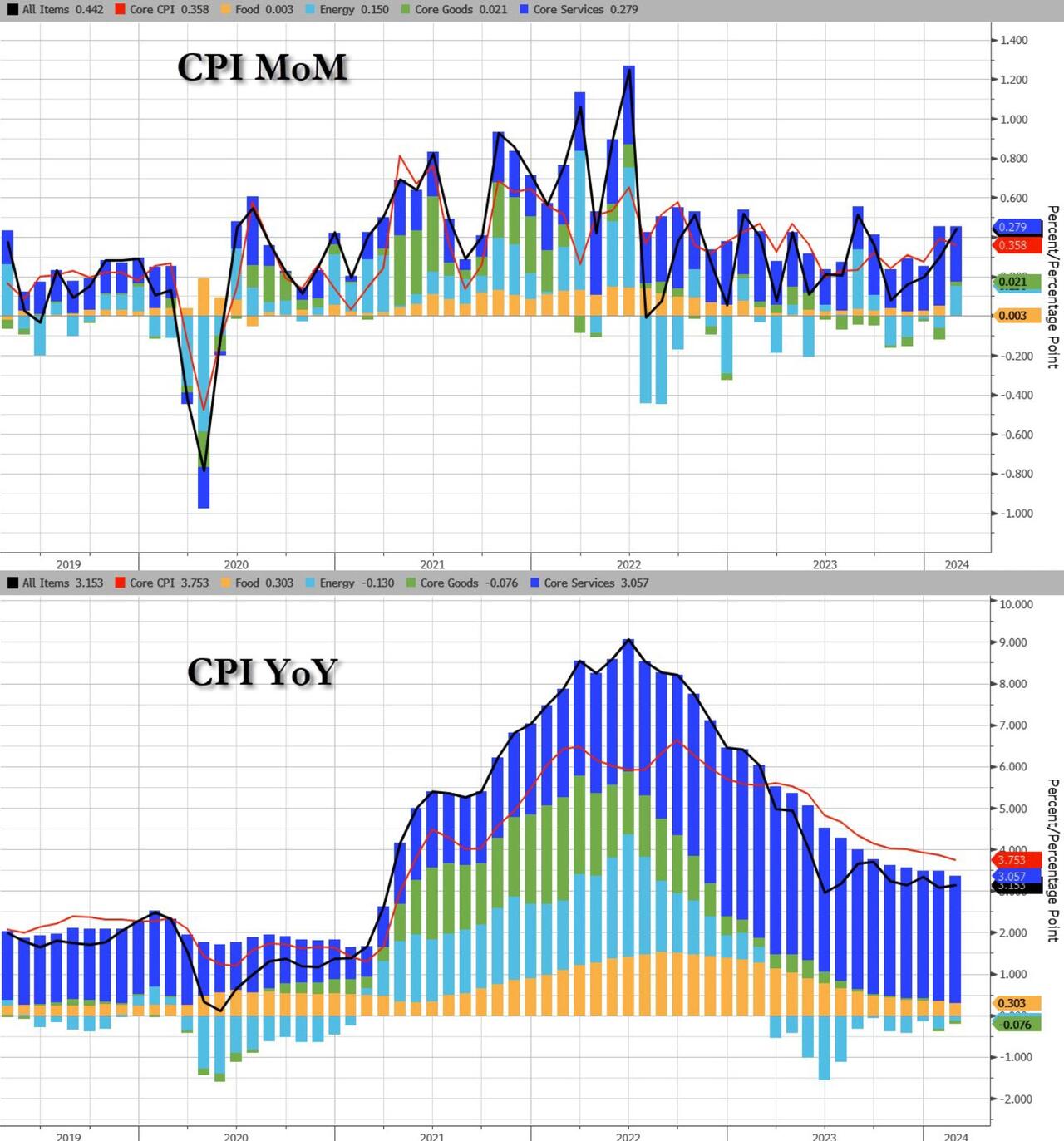

The 3-month annualized CPI rate was rose to 2.8% from 1.9%. The 6-month annualized core rate dropped to 3.2% from 3.3%.

Energy costs surged MoM as Core Services inflation slowed MoM…

Source: Bloomberg

Full CPI MoM breakdown:

The index for all items less food and energy rose 0.4 percent in February, as it did the previous month.

The shelter index increased 0.4 percent in February and was the largest factor in the monthly increase in the index for all items less food and energy.

The index for rent rose 0.5 percent over the month, while the index for owners’ equivalent rent increased 0.4 percent.

The lodging away from home index increased 0.1 percent in February, after rising 1.8 percent in January.

The airline fares index rose 3.6 percent in February, following a 1.4-percent increase in January.

The index for motor vehicle insurance increased 0.9 percent over the month.

The medical care index was unchanged in February after rising 0.5 percent in January.

The index for hospital services decreased 0.6 percent over the month and the index for physicians’ services decreased 0.2 percent.

The prescription drugs index fell 0.1 percent in February.

The index for dental services was among those that rose in February, increasing 0.4 percent.

The index for personal care fell 0.5 percent in February, following a 0.6-percent increase in January.

The household furnishings and operations index fell 0.1 percent over the month, as did the new vehicles index.

Among other indexes that rose in February were apparel, recreation, and used cars and trucks.

Full CPI YoY breakdown:

The index for all items less food and energy rose 3.8 percent over the past 12 months.

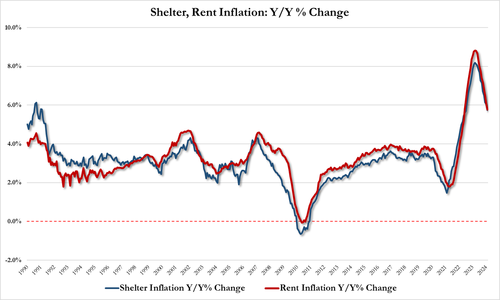

The shelter index increased 5.7 percent over the last year, accounting for roughly two thirds of the total 12-month increase in the core CPI index

Feb Shelter inflation: 5.74% down from 6.04% in Jan

Feb rent inflation: 5.77%, down from 6.09% in Jan

Other indexes with notable increases over the last year include motor vehicle insurance (+20.6 percent), medical care (+1.4 percent), recreation (+2.1 percent), and personal care (+4.2 percent).

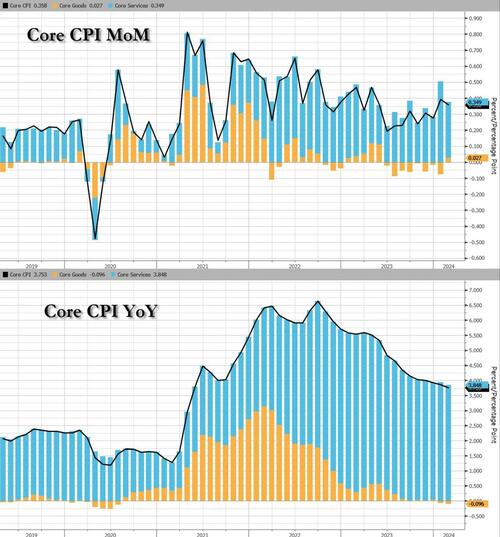

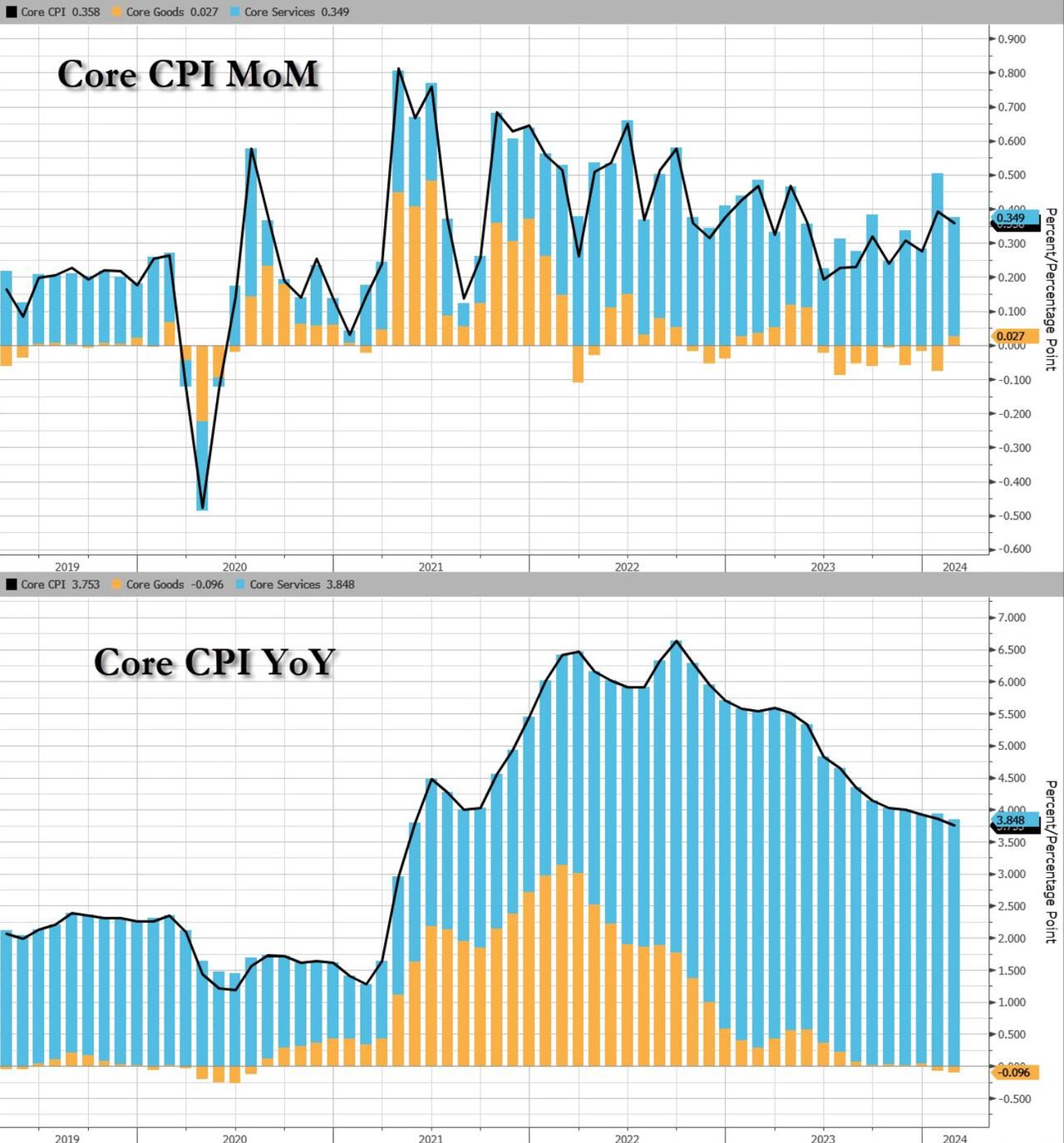

Core CPI rose 0.4% MoM (hotter than the +0.3% exp) and up 3.8% YoY (hotter than the +3.7% exp), but still the lowest since April 2021…

Source: Bloomberg

The 3-month annualized Core CPI rate was rose to 4.1% from 3.9%. The 6-month annualized core rate rose to 3.8% from 3.5%.

Core Goods actually rose MoM for the first time since June 2023…

Goods deflation continues (-0.3% YoY) but has flattened out, while services inflation remains stubbornly high at +5.2% YoY…

Source: Bloomberg

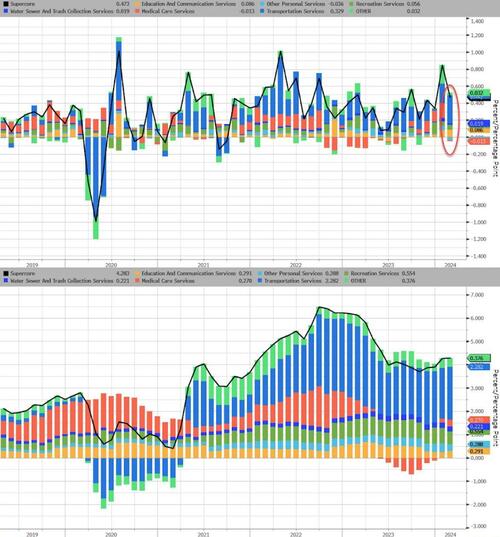

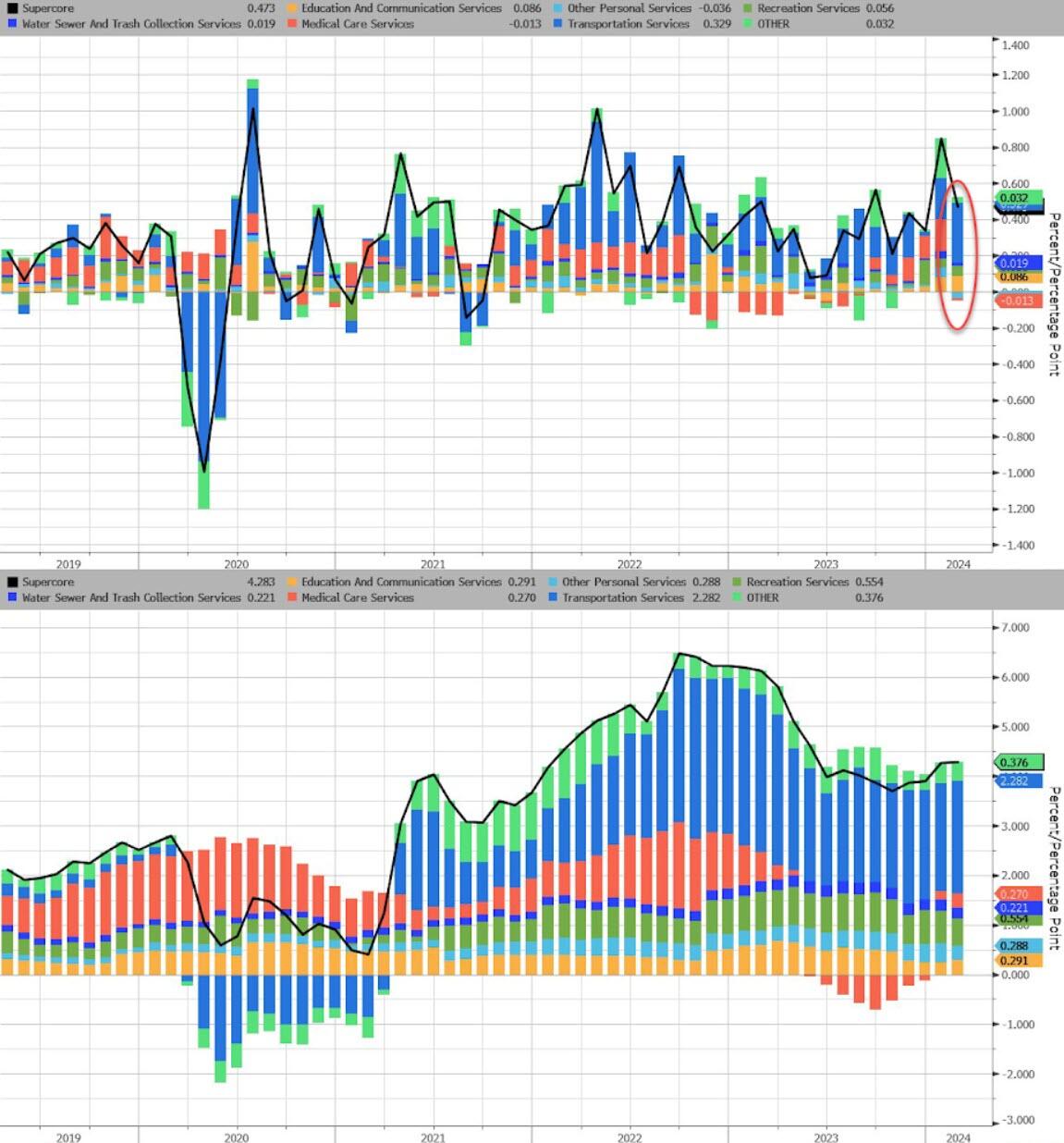

And one step deeper – the so-called SuperCore: Core CPI Services Ex-Shelter index – soared 0.5% MoM up to 4.5% YoY – the hottest since May 2023…

Source: Bloomberg

While SuperCore CPI slowed MoM, there was a large jump in Transportation Services MoM…

Source: Bloomberg

Finally, we note that consumer prices have not fallen in a single month since President Biden’s term began (July 2022 was the closest with ‘unchanged’), which leaves overall prices up 19% since Bidenomics was unleashed. And prices have never been more expensive…

Source: Bloomberg

That is an average of 5.6% per annum (more than triple the 1.9% average per annum rise in price during President Trump’s term).

So, about that shrinkflation – did companies only ‘get greedy’ when Biden took office?

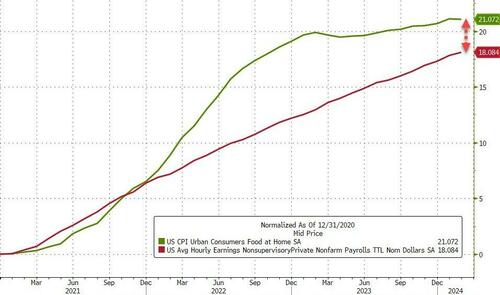

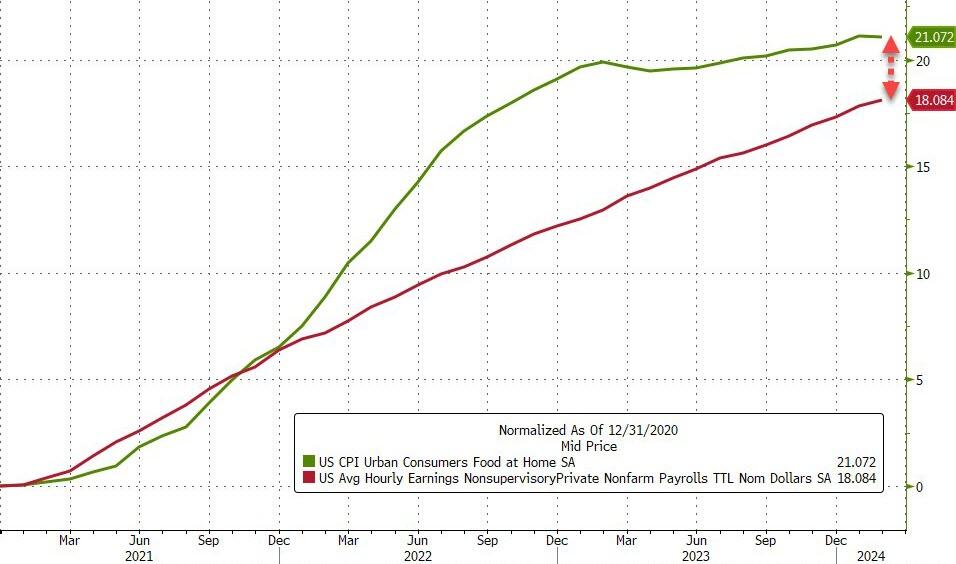

But it gets worse, real wage growth has lagged significantly for the average joe in America…

Source: Bloomberg

Despite a very modest decline in Feb, Food costs are up over 21% since Biden’s term began, but non-supervisory wages are up only 18%.

Bidenomics for the win!

Are we going to see a replay on the ’70s?

Source: Bloomberg

The market narrative of slow and steady disinflation just broke harder.

…or are we still set for a massive wave of depressionary deflation?

Inflation remains hot, hot, hot although Biden/Yellen will undoubtedly say that it is lower than last year. But remember, consumer prices are up a staggering 19% under Bidenomics. THAT is a major tax of those making under $200,000 per year, Joey.

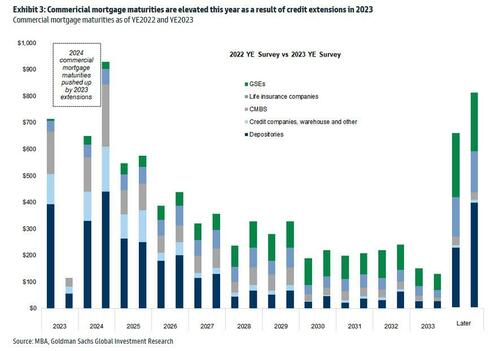

Holders of commercial real estate (CRE) debt are riding the tiger. Meaning that if interest rates don’t come down, there will be a lot of pain and suffering.

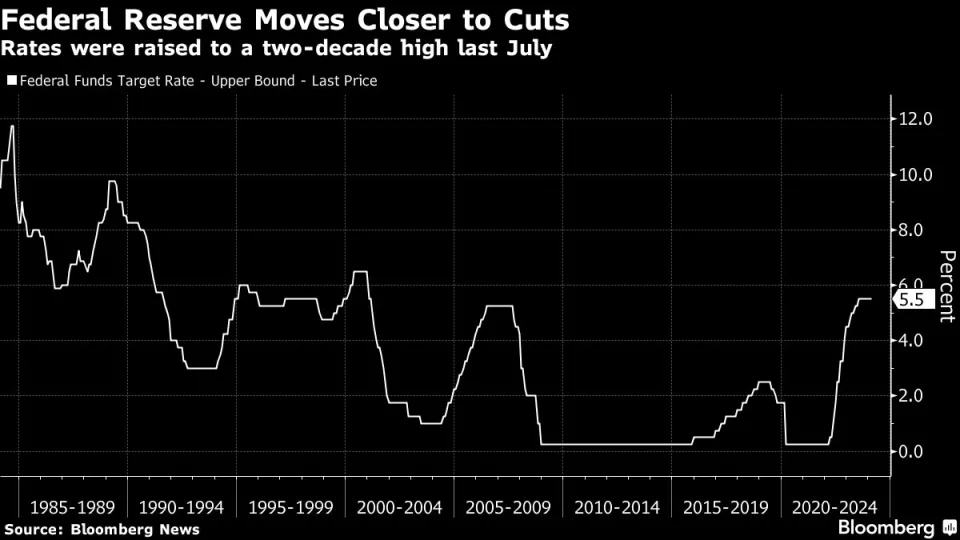

“We’re far from neutral now,” said America’s Fed Chairman, Jerome Powell, to the Senate Banking Committee. As The Fed moves closer to cutting rates.

All those rent-seekers stacked up with commercial real estate holdings nodded in violent agreement. That of course includes the nation’s regional banks, which continue to succumb to the power of their systemically important rivals, now so big that they cannot possibly be allowed to fail.

And this has turned America’s banking behemoths into for-profit wards of the state, recipients of an unspoken but ironclad insurance policy that underwrites catastrophic losses and adds them to the national debt.

“Interest rates right now are well into restrictive territory. They’re well above neutral,” added Chairman Powell without, well, sharing his definition of the word ‘well’. And truth be told, no one really knows the definition of ‘neutral’ when it comes to interest rates.

Economic PhDs will generally tell you that the neutral real interest rate is 0.50%. Their level of confidence is inversely proportional to the amount of capital they have at risk in markets — which would have been Newton’s Fourth Law had he bothered to study the art of economics.

Those of us less academically gifted, who must resort to taking risk for a living, lack the conviction of Nobel Laureates. We see that there are times in an economic cycle when 0.50% real rates stimulate growth, and times when they restrict economic activity.

Sometimes neutral rates have no effect at all. Which is to say that the economic impact of real rates simply depends. Like now when signals are far from uniform. Stock markets hit all-time highs despite collapsing commercial real estate, crypto and gold prices are soaring to records, massive government stimulus programs like the IRA are cranking up, student debt is being forgiven in successive waves, unemployment is near record lows, core inflation is starting to rise again, and the budget deficit is around 6% despite robust GDP growth.

All of which screams that a 0.50% real rate is preposterously low to everyone but economic PhDs.

In statistics we talk about “jump processes.” Like Federal government spending every time there is a financial crisis like the subprime crisis of 2008-2009 and the Covid lockdowns of 2020. Each crisis brought a jump in the level of spending and jump in Federal debt.

Federal debt under Biden started at $27.7 trillion and is currently at $34.5 trillion, that amounts to $6.75 TRILLION in additional debt under Old Grand-dad Joe Biden. Federal spending, of course, is out of control with Biden/Congress spending $569 BILLION since Joey took office.

Generally speaking, the Federal government needs to justify the elevated levels of Federal spending, like another COVID outbreak, escalate the war in Ukraine, get into a hot war with Iran and China, or … say … Washington DC pols never need much of an excuse to go on a spending spree.

If only Biden would retire gracefully. He could be the new face of “Old Grand-dad Bourbon Whiskey.” Except Biden’s version would be an angry 80+ year old man with dementia.

Somehow, Biden left this factoid out of his State of The Union (SOTU) address. In February, immigrants added 1,277 million jobs while native Americans lost -420,000 jobs according to the BLS. Or maybe Biden can change his campaign motto to “Make America Great Again … For Immigrants, NOT Natives.”

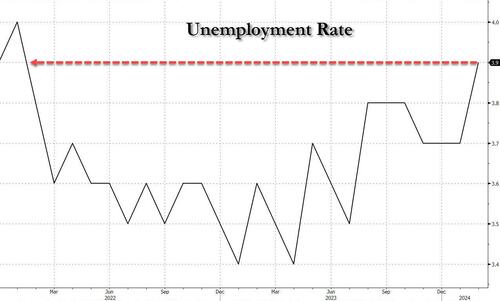

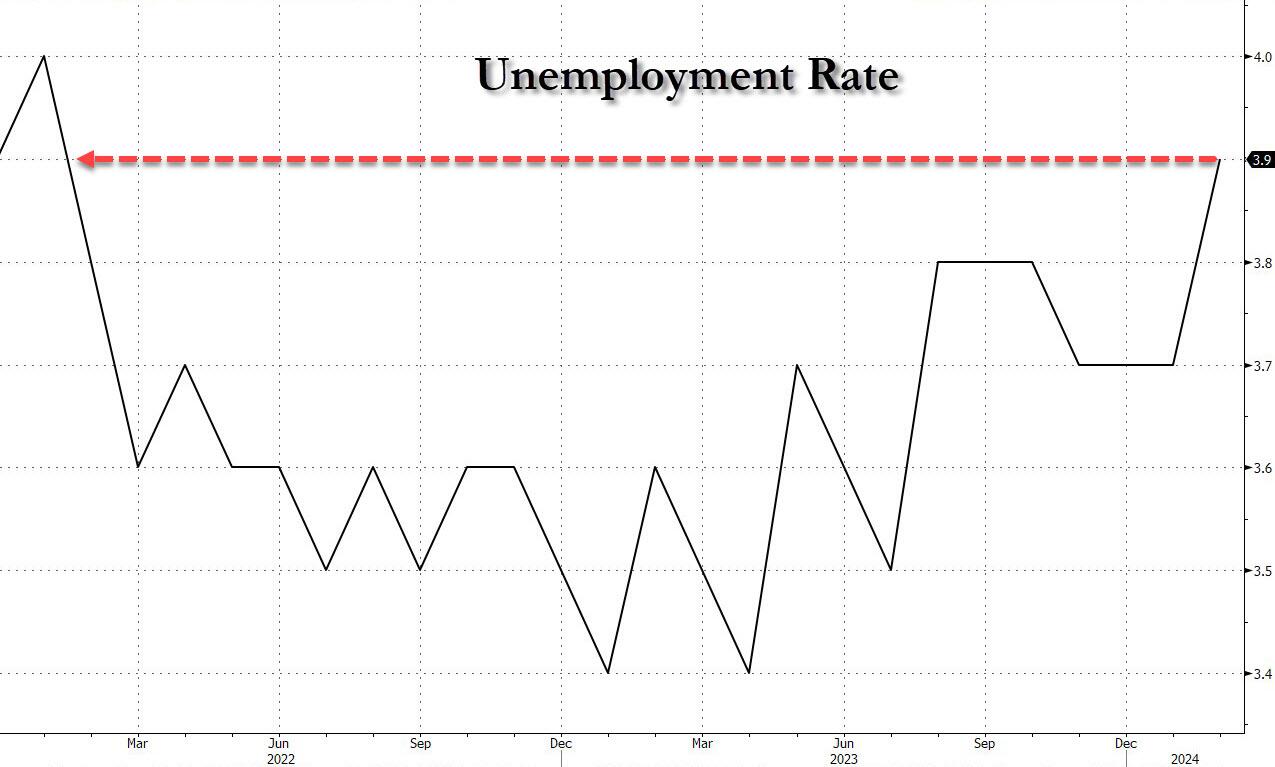

In February, the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%).

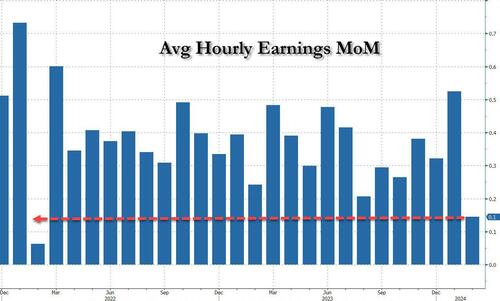

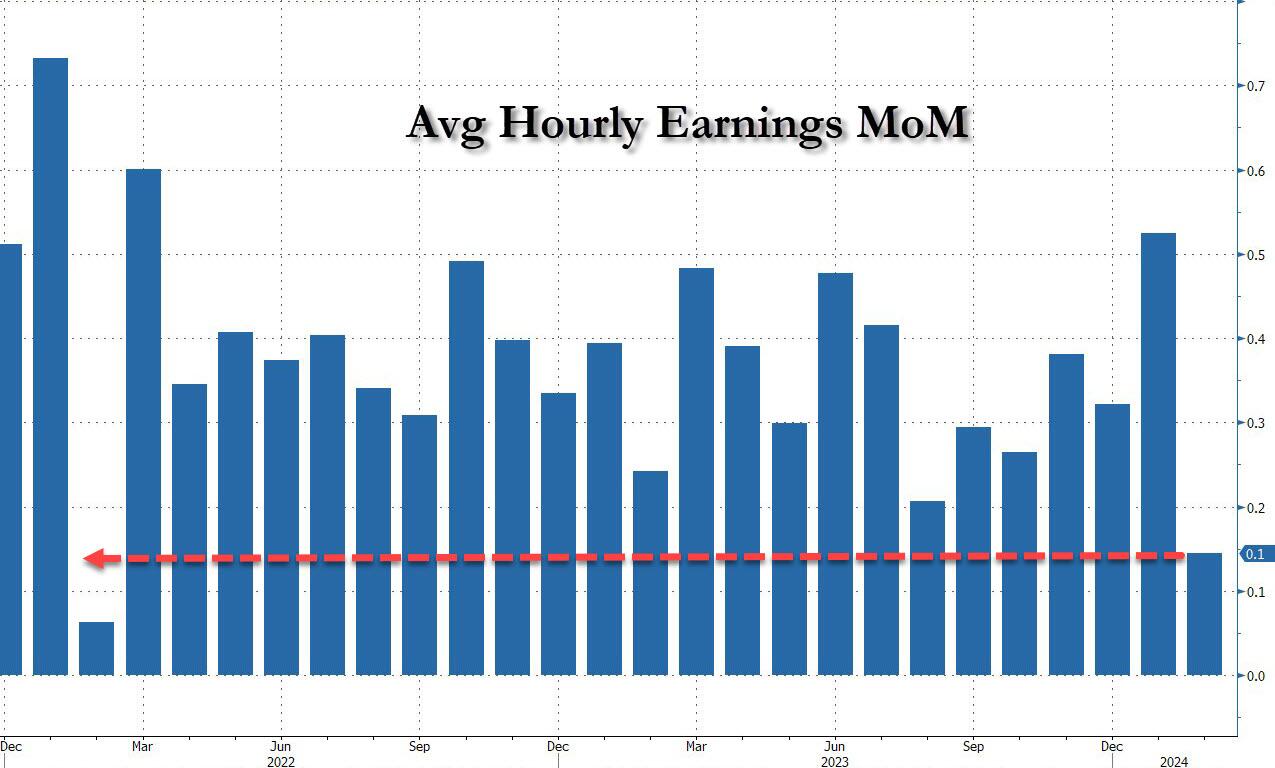

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years…

It is clear that the labor market is softening, but Biden/Mayorkas will continue to let millions of illegal immigrants pour across the border making the labor market even softer than before. But the top 1% are making out like bandits from the illegal immigration. Bandits benefitting bandits.

We are living in a banker’s paradise. Where a top administrative official pushes to change forecasts of the economy. Hey, it’s a Presidential election year and literally anything goes.

The disagreement was over forecasts for 10-year Treasury yields in the budget, a linchpin estimate that is intertwined with other measures, like debt service costs.

Forecasts in the president’s budget proposal — scheduled for release Monday — are typically set by Treasury Secretary Janet Yellen, Office of Management and Budget Director Shalanda Young and the chair of the Council of Economic Advisers, Jared Bernstein. The group is known in fiscal circles as the troika.

An October meeting, however, included a fourth invited principal: Brainard, who directs the National Economic Council. Brainard at one point disagreed with Yellen, Young and Bernstein on the 10-year interest rate projections and predicted a slightly lower rate, the people said, speaking on condition of anonymity to detail the discussions.

The difference between the forecasts was modest and both were well within range of private-sector estimates, the people said. The exact scope of Brainard’s changes aren’t clear.

Brainard’s forecast painted a modestly better picture for Biden. A lower interest-rate forecast would have the effect of an improved overall outlook by offering more support for growth and suggesting less concern about inflation. It also would lower borrowing cost projections at a time of rising worries about the US deficit and debt.

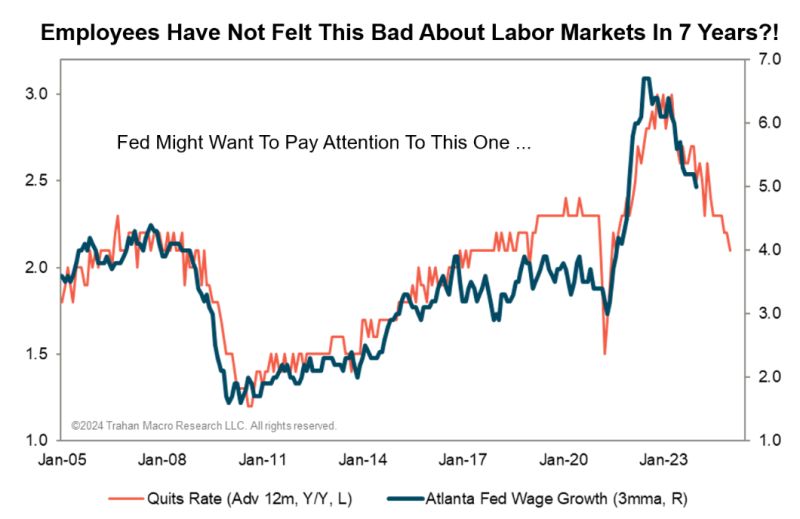

Let’s see what the Troika have to say about the quits rate.

Yes, it is the Ides of March. No, not Nikki Haley trying to sabotage Donald Trump’s campaign after Nikki got clobbered in all but two state primaries. So in a sour grapes move, Haley didn’t endorse Trump. But the Ides of March refers to the stabbing of Julius Caesar (led by Brutus).

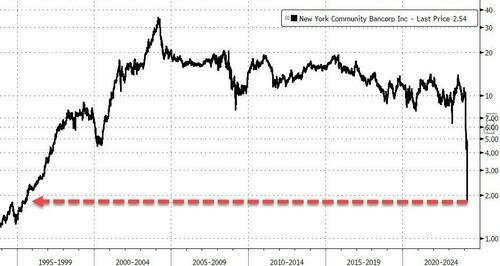

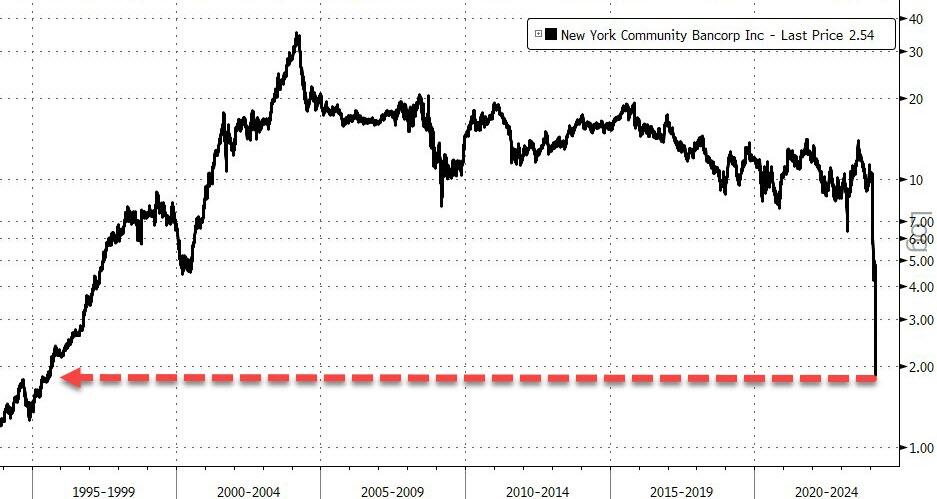

Once the darling of the small banking crisis comeback, New York Community Bancorp has crashed 45% to fresh 30 year lows after The Wall Street Journal reportsthe bank is seeking to raise equity capital in a bid to shore up confidence in the troubled regional lender.

According to people familiar with the matter, NYCB has dispatched bankers to gauge investors’ interest in buying stock in the company.

There’s no guarantee there will be a deal, or that one would succeed in addressing the bank’s challenges, which as of Wednesday morning had led to a roughly 80% decline in its stock price since January.

This is not a good picture for a bank… Would you hold your deposits there?

Last month, DiNello laid out a series of options the bank could explore to bolster its balance sheet, including selling assets from certain non-core businesses. The bank has also considered turning to newfangled financial instruments that would share the risks of those loans with outside investors, people familiar with the matter said.

As WSJ reports, finding takers for those assets, at least at prices that would make a deal worthwhile, has been challenging and U.S. officials have expressed reservations with banks pursuing credit-risk transfers that would shift the burden of potential losses to entities outside of the regulated banking system.

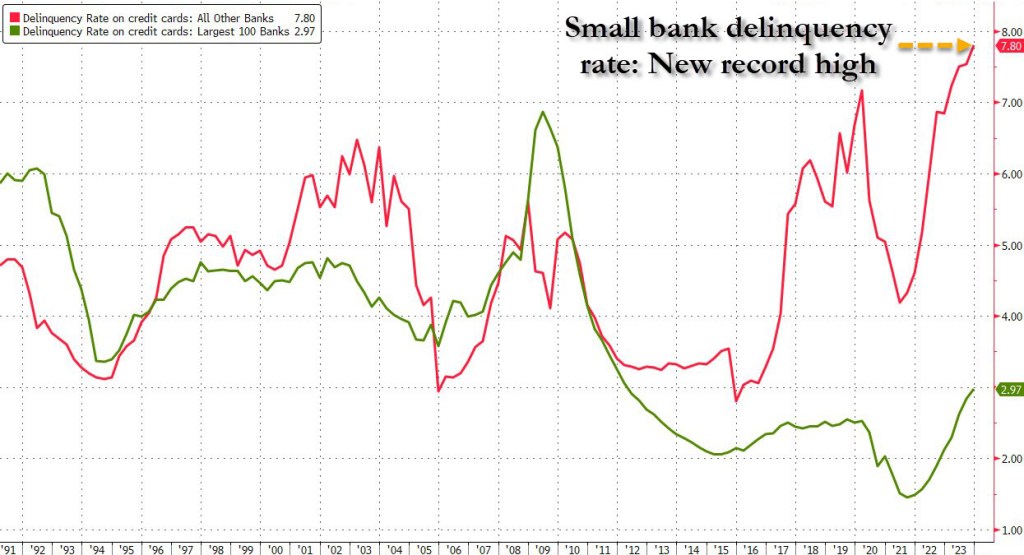

Finally, as a reminder, NYCB is not alone. The red line below shows ‘small banks’ are in trouble absent The Fed’s BTFP facility…

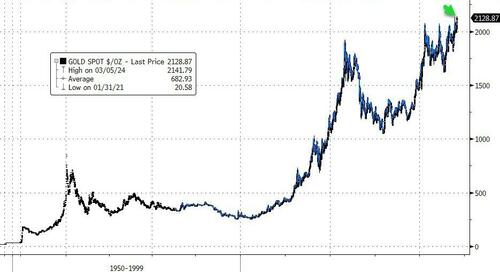

Let’s start with gold. Extending their run of the last few days, spot gold prices just exceeded their all-time highs, topping $2140 for the first time in history…

Source: Bloomberg

A longer view.

Source: Bloomberg

What is gold pricing in about future Fed action? Real rates dramatically negative? As Luke Gromen noted on X:

“When gold rises in your currency DESPITE positive real rates, the gold market is saying ‘Your government will have a debt spiral if real rates remain positive’.“

Source: Bloomberg

Bitcoin just hit $68,567.57, also an all-time high.

The Alt-Assets (gold, silver, Bitcoin) have counterattacked!!

Too much debt! US politicians are spending too much money and borrowing too much. Unfortunately, that is what Biden and Bidenomics is all about: Federal targeted spending and loads of debt.

Now it requires $1 trillion of new debt every 100 days to achieve nothing but remaining static economically. The regime media pundits and the cabal on Wall Street tell us the economy is doing great. No recession in sight. All is well. The dumbed down and distracted ignorant masses don’t realize all the reported “economic growth” is “created” by the government, enabled by The Fed, spending billions on their wars in Ukraine and the Middle East, funneling the money into the Military Industrial Complex corporations; paying for the transportation, feeding, and housing of the illegal invading hordes; hiring more government drones to harass the citizenry, and desperately trying to prop up a corrupt tottering empire in its final death throes.

Anyone with even the slightest mathematical acumen knows increasing the national debt at a rate of $1 trillion every 100 days is a death wish. Why would those pulling the strings behind the scenes of this acceleration towards the cliff of national suicide be doing so at this point in time? It’s almost as if the November elections are a deadline for them to complete their exit strategy plan.

I believe we are entering the Great Taking phase of this clown show.

They are purposely creating a global financial disaster in order to take everything you and I have. It sounds crazy, but so is adding $1 trillion of debt every 100 days.

Cash on the barrelhead. To pay for outrageous inflation and food prices under Joe “Nero” Biden.

President Biden: “Inflation is the lowest it has been in nearly three years. And wages, wealth, and jobs are higher than they were before the pandemic.”

Paul Krugman, Nobel Laureate in economics and propaganda expert (ala, Leni Riefenstahl) pointed to this chart to illustrate that inflation is declining or at least hasn’t doubled under Biden, (although it looks like food prices are up 21% under Biden). Most elites won’t notice since someone does the shopping for them. Can you imagine Joe and Jill Biden at the local Kroger grocery store? Or Barrack and Mike Obama at the local grocery store on Martha’s Vineyard??

A counter to Biden’s and Krugman’s claims of “everything is peachy!” is that the situation is actually dire.

1. Prices have never been higher and are starting to accelerate to the upside again

2. All the jobs created in the past year have been part time.

3. There has been zero job growth for native-born Americans since 2018; all jobs have gone to immigrants (mostly illegal immigrants)

4. Real wages have not only been negative for most of the Biden presidency, they just turned negative again

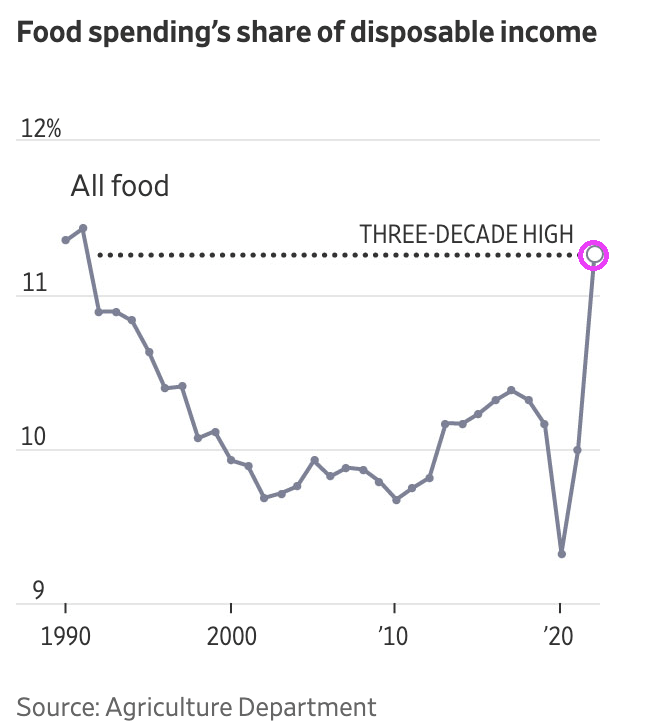

In addition, food spending’s share of disposable income is at its highest in three decades.

Nero supposedly fiddled while Rome was burning. Joe “Nero” Biden eats ice cream while the USA burns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.