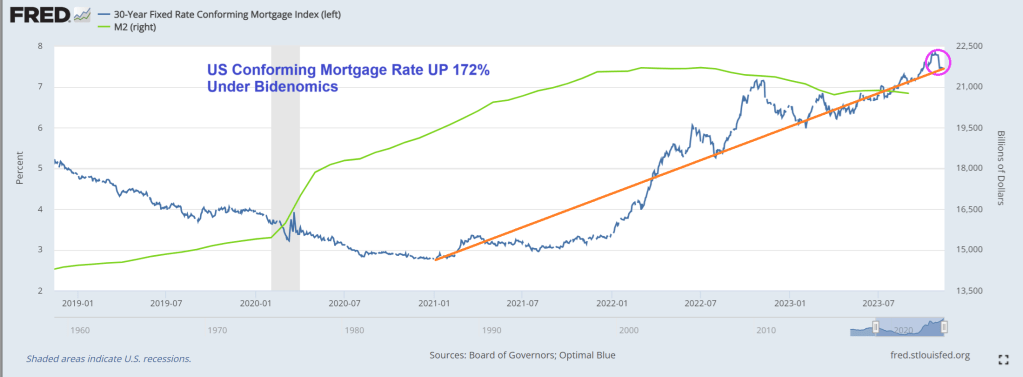

Under Biden’s Reign of Error (or green economic transformation), the US has seen over 8 million illegal immigrants enter the US which is a far greater number than births in the US. In other words, Americans apparently are NOT being born under a bad sign. Hence, the US is seeing the demand for housing increase. But …. housing start were DOWN -4.2% YoY in October.

Housing Starts:

Privately‐owned housing starts in October were at a seasonally adjusted annual rate of 1,372, the October 2022 rate of 1,432,000. Single‐family housing starts in October were at a rate of 970,000; this is 0.2 percent above the revised September figure of 968,000. The October rate for units in buildings with five units or more was 382,000.

Building Permits:

Privately‐owned housing units authorized by building permits in October were at a seasonally adjusted annual rate of 1,487,000. This is 1.1 percent above the revised September rate of 1,471,000, but is 4.4 percent below the October 2022 rate of 1,555,000. Single‐family authorizations in October were at a rate of 968,000; this is 0.5 percent above the revised September figure of 963,000. Authorizations of units in buildings with five units or more were at a rate of 469,000 in October.

Total starts were down 4.2% in October compared to October 2022. And starts year-to-date are down 11.3% compared to last year.

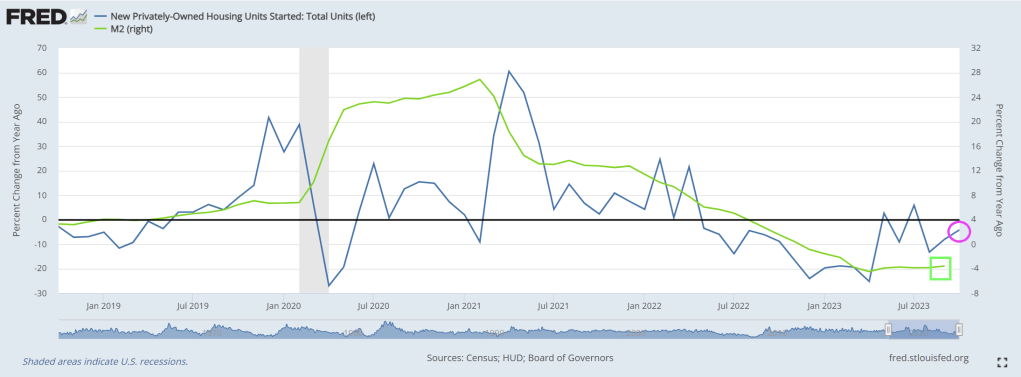

In YoY terms (change since one year ago), shows housing starts declining with dying M2 Money growth.

Starts have been down year-over-year for 16 of the last 18 months (May and July 2023 were the exceptions), and total starts will be down this year – although the year-over-year comparisons are somewhat easier in Q4.

{kind=link}

{kind=link}

You must be logged in to post a comment.