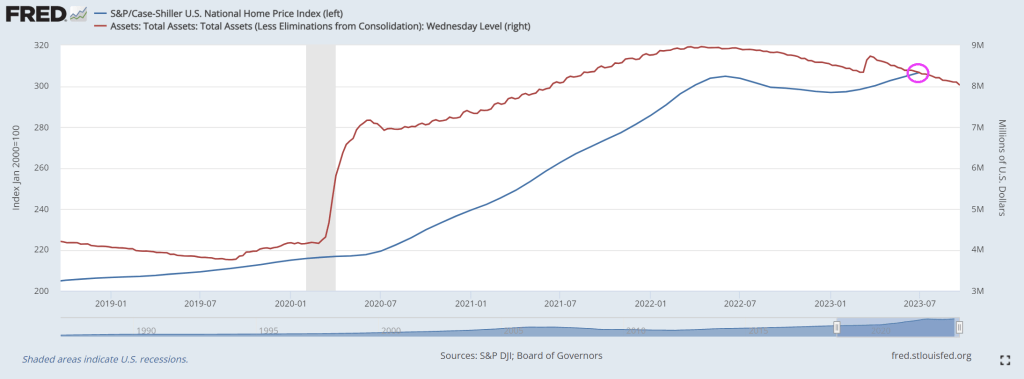

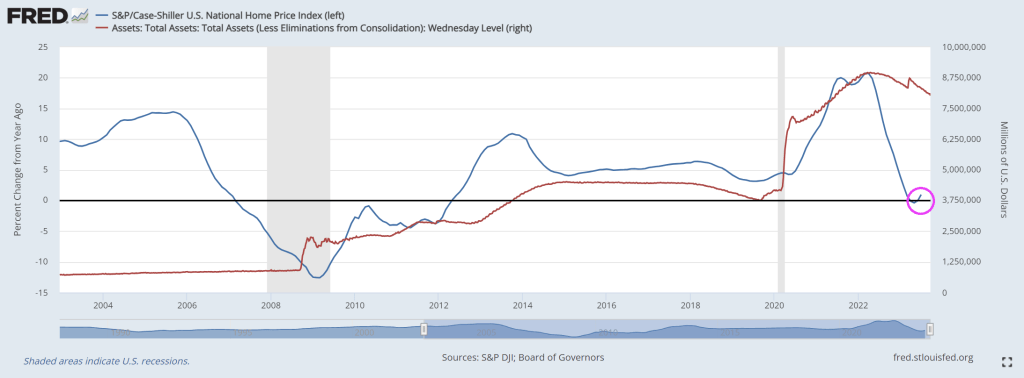

Thanks to rampant Federal spending and overstimulus by The Federal Reserve, US housing prices are simply unaffordable for many. Particularly since the Covid epidemic (Wuhan China Flu).

Yes, home prices grew in July despite rising mortgage rates. As CS Lewis wrote “That Hideous Strength” but this is about how The Fed doesn’t understand what they have done.

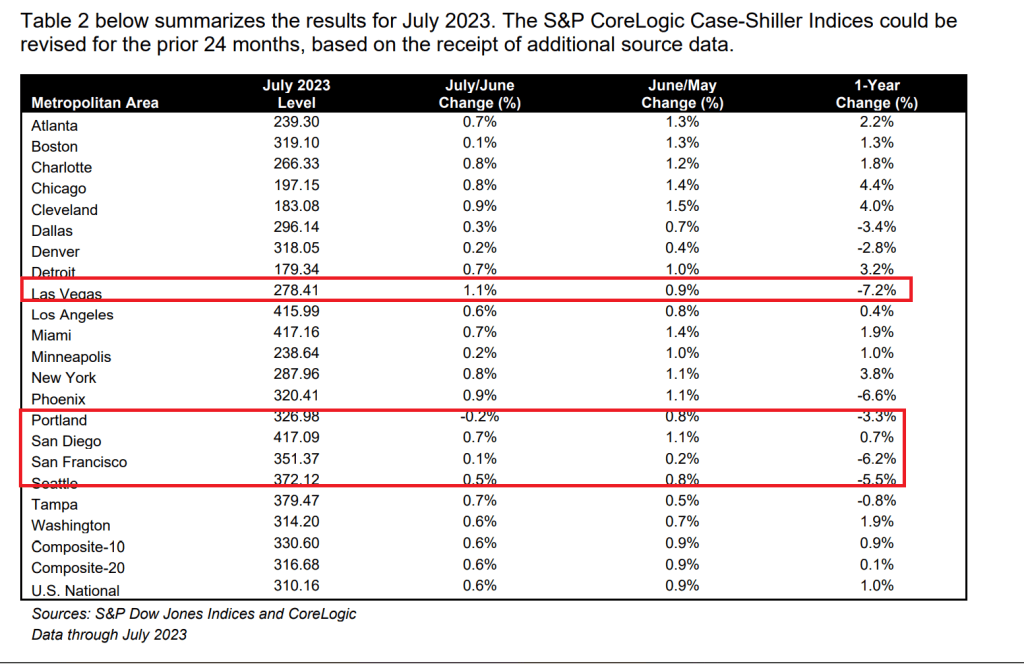

At the metro level, Las Vegas leads in YoY price declines at -7.2%. In a close second is San Francisco at -6.2%. Portland and Seattle also declined.

Here is Screamin’ Joe Biden. You know Biden is lying when he gets angry.

Donald Trump was famous for his “Make America Great Again!” campaign. Joe Biden seems to want to make America LAST again (MALA).

A newly aired “60 Minutes” segment entitled The unexpected way American tax dollars are being used in Ukraine has uncovered that the US government is paying the salaries of some 57,000 Ukrainian civic services personnel.

The report details the various ways non-military aid is being spent at a moment GOP Congressional leaders are intensely debating whether to move forward with a proposed defense budget that includes Biden’s push for $24 billion more in military assistance for Kiev.

“The U.S. has spent just over $43 billion on military aid to Ukraine since Russia invaded. That’s equivalent to about 5% of the American defense budget. European countries combined have contributed around $30 billion,” the 60 Minutes report narrates.

American taxpayers are financing more than just weapons. We discovered the U.S. government’s buying seeds and fertilizer for Ukrainian farmers… and covering the salaries of Ukraine’s first responders – all 57,000 of them.

That includes the team that trains this rescue dog – named Joy – to comb through the wreckage of Russian strikes looking for survivors.

Political commentator Collin Rugg has noted in relation to the potential government shutdown looming for Oct. 1st: “Yes, your tax dollars will be used to fund Ukrainian salaries while American citizens are forced to wait for their pay while the government remains closed,” he said on X.

Rugg is referencing the fact that the Biden administration and Pentagon have declared that Ukraine aid will remain exempt from any potential government shutdown. This means Ukrainian salaries will still be paid, even while federal employees aren’t, in the event of a shutdown.

Here’s more from the 60 Minutes video, featuring a Ukrainian woman “thanking” US taxpayers for footing the bill for Ukrainian employees, thanks to USAID funding:

Tatiana Abramova: Especially in the condition of war, we have to work. We have to pay taxes, we have to pay wage– salary to our employees. We have to work, don’t stop.

Holly Williams: Why does that help Ukraine win the war?

Tatiana Abramova: Because economy is the foundation of everything.

American officials from USAID – the agency in charge of international development – helped Abramova find new customers overseas. In the midst of war, her company is supporting over 70 families.

Meanwhile, a fresh Newsweek headline: US Will Pay Salaries to Thousands of Ukrainians During Government Shutdown…

“US taxpayers will pay the salaries of thousands of Ukrainians, even as the country faces a government shutdown at the end of September.”

But as noted above, this is more like tens of thousands of Ukrainian salaries.

“A federal government shut down will effectively begin on October 1 if Congress isn’t able to pass a funding plan that Biden signs into law,” Newsweek underscores. “If that happens, federal agencies have to stop all nonessential work and will not send paychecks for as long as the shutdown lasts.”

Appropriately, the 60 Minutes episode invoked memory of the late John McCain…

In total, America’s pumped nearly $25 billion of non-military aid into Ukraine’s economy since the invasion began – and you can see it working at the bustling farmers market on John McCain Street in central Kyiv.

The late senator is revered in Ukraine because he pushed the U.S. government to start sending arms to the country… back in 2014.

Here’s how 60 Minutes presents bipartisan support for Biden’s blank check for Ukraine:

While in Kyiv, we learned that three of McCain’s former colleagues were also in town: Democratic Sens. Elizabeth Warren and Richard Blumenthal and Republican Sen. Lindsey Graham. They don’t normally agree on much – together, though, they’re some of the staunchest supporters of U.S. funding for Ukraine’s resistance.

Indeed Zelensky himself while meeting with US Senators in Washington last week said something similar – that without continuing American funds, the war effort is doomed. He urged Congress to keep the billions in aid flowing, and sought to present that Moscow will one day expand aggression beyond just Ukraine.

* * *

Meanwhile, the “aid from the heart of every ordinary American person” will continue (whether those ordinary Americans like or not)…

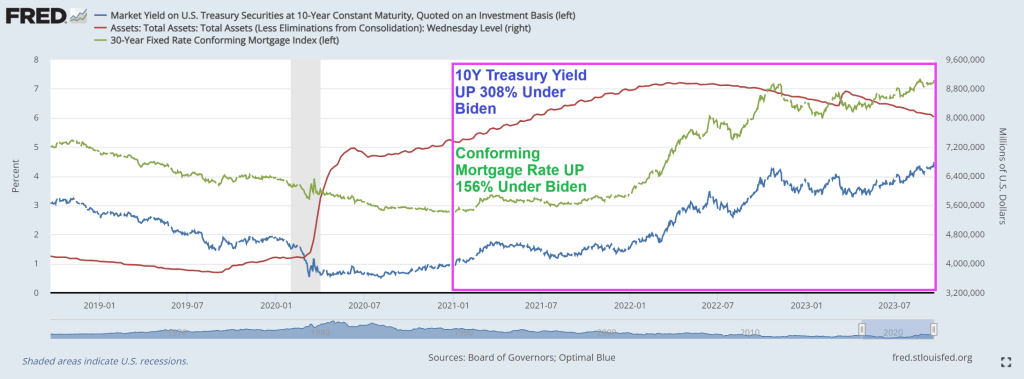

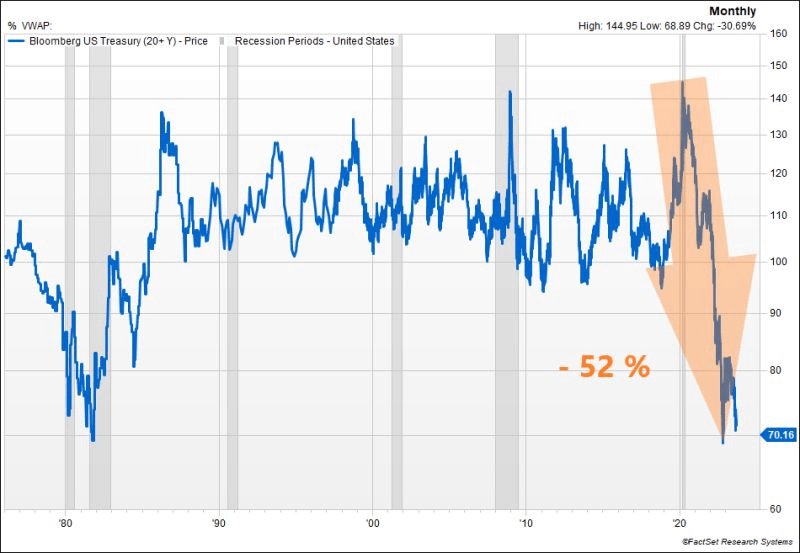

Alarm! US 10-year Treasury yields are soaring along with mortgage rates.

The US Treasury market is witnessing another significant selloff, pushing the 10y UST yield close to the 4.50% mark. The surge in real rates is remarkable, reaching 2.12% for the 10y, a level not seen since 08’. While this might appear attractive in real terms compared to historical benchmarks, could we be on the brink of a third consecutive year of negative performance for US Treasuries? To put this into perspective, such a scenario has never occurred in history.

The conforming mortgage rate is at 7.3%, up 156% under since Biden’s coronation as El Presidente of the United Banana Republics of America. Where political opponents are indicted prior to elections.

In Biden’s Banana Republic economy, the US Treasury 10y-2y yield curve remains inverted.

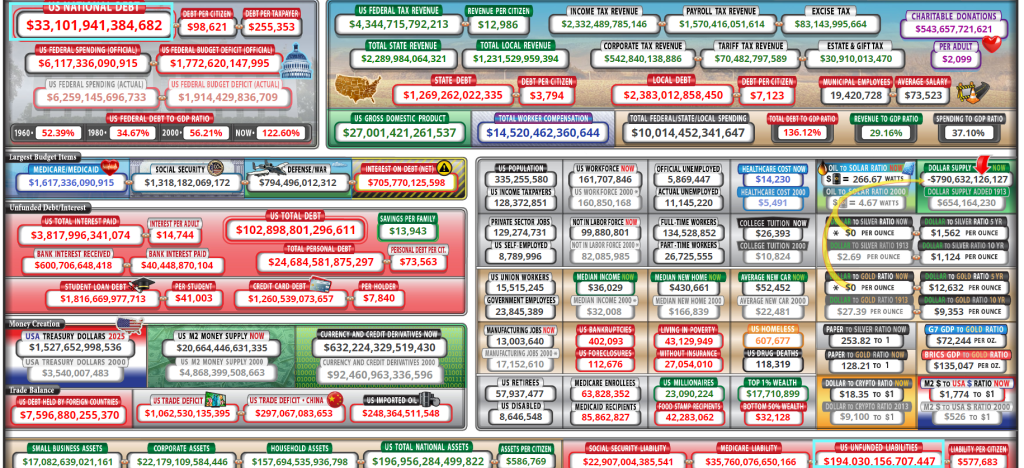

And then we have Mish’s chart on debt as a percentage of GDP from CBO. Remember, we used to worry about the US breaking the 80% debt to GDP level. It is now projected to be 181%. Wow.

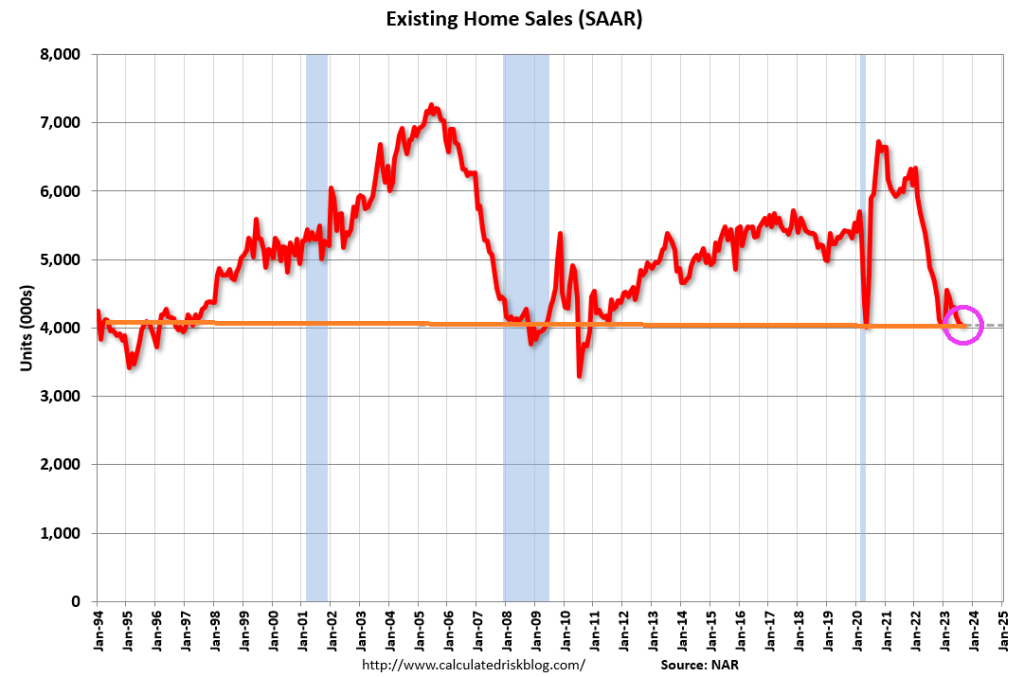

The most recent report on US exisiting home sales showed that sales decreased in 17 of the last 19 months as The Fed tightens monetary policy to combat inflation caused by … 1) The Fed and 2) Bidenomics spending on green energy.

The US housing market will be “back in black” once Biden and Congress stop their reckless spending and borrowing. Biden has added $5,352,202 to the national debt since being selected (not by me!). That is a 19% increase in The Federal debt in just 33 months!

Not to mention the ludicrous $194 TRILLION in unfunded liabilities that the geezers in the Biden Administration (Biden is 80 and slipping into dementia) and the Geriatric wing of Congress (the US Senate) is home to fossils like Mitch McConnell (not looking well) and Diane Feinstein (90 and looking poorly). I didn’t forget about Nancy Pelosi (Communist-California) who is 83 and running for re-election. Younger doesn’t necessarily mean better since Pelosi’s nephew California governor Gavin Newsom is 55 years old and helped destroy California’s economy. Of course, the DNC will probably selected Newsom to replace scandal-ridden Biden as the Democrat in order to finish the job Obama started.

Existing-home sales slipped again in August as rising mortgage rates make housing prices the least affordable ever. Despite denials in many corners, a crash is underway.

Existing-home sales retreated 0.7% in August to a seasonally adjusted annual rate of 4.04 million.

Sales dropped 15.3% from one year ago.

The median existing-home sales price climbed 3.9% from one year ago to $407,100, an increase of 3.9% from August 2022 ($391,700). It’s the third consecutive month the median sales price surpassed $400,000.

The inventory of unsold existing homes dipped 0.9% from the prior month to 1.1 million at the end of August, or the equivalent of 3.3 months’ supply at the current monthly sales pace.

First-time buyers were responsible for 29% of sales in August, down from 30% in July and identical to August 2022.

All-cash sales accounted for 27% of transactions in August, up from 26% in July and 24% in August 2022.

And mortgage rates are now up to 23 year highs!

If Biden bows out and Newsom runs for President … and loses, Newsom always has a career in Hollywood in vampire movies. “I will suck your (economic) blood!” – Count Newsom.

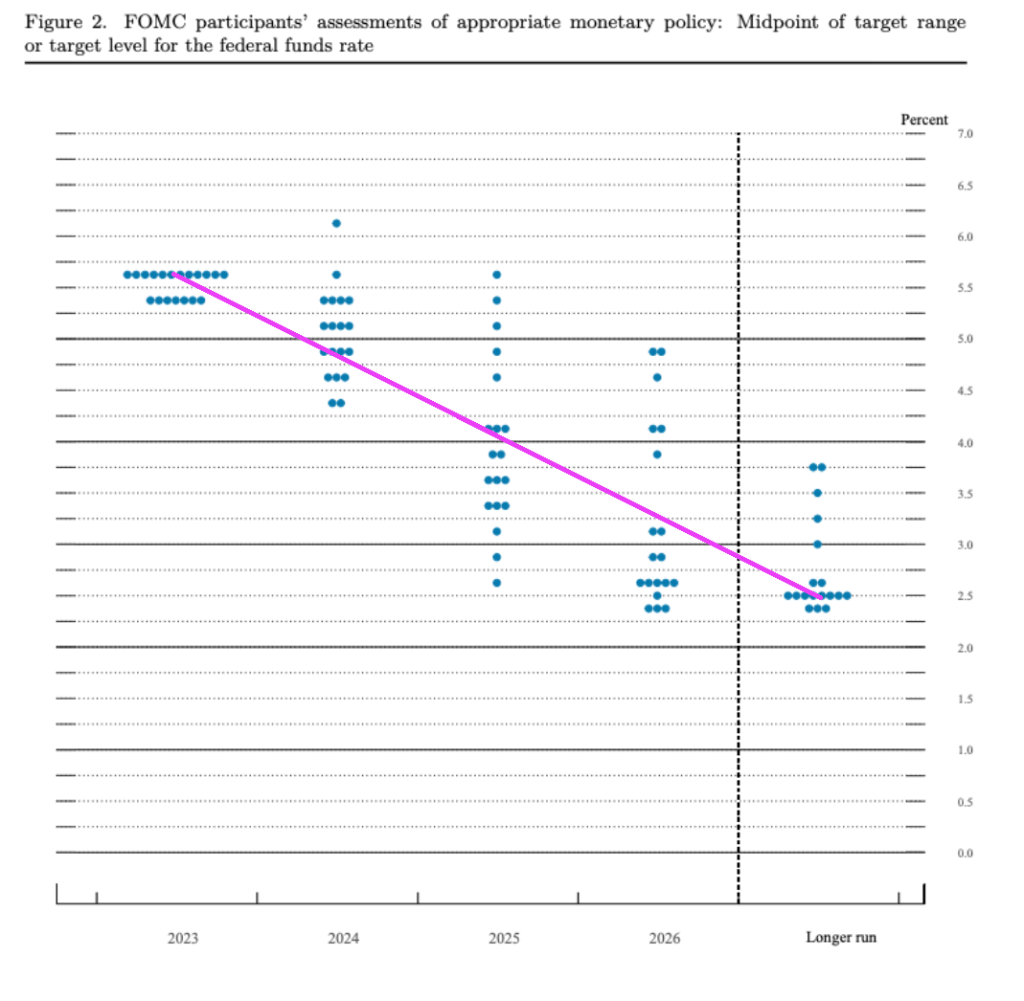

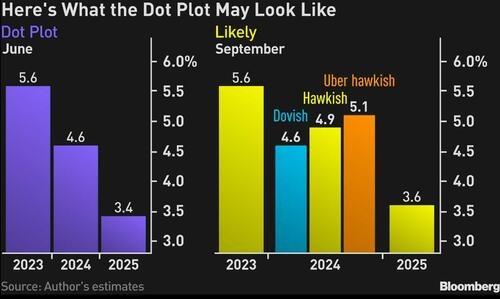

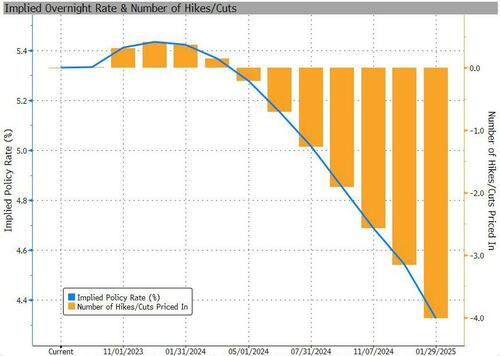

So much for The Federal Reserve raising rates until it gets inflation to 2%. Yesterday, the left their target rate unchanged. But yesterday, The Fed released their dot project showing their target rate is expected to decline in 2024 and beyond.

On the housing front, existing-home sales moved lower in August, according to the National Association of REALTORS®. Among the four major U.S. regions, sales improved in the Midwest, were unchanged in the Northeast, and slipped in the South and West. All four regions recorded year-over-year sales declines.

Total existing-home sales – completed transactions that include single-family homes, townhomes, condominiums and co-ops – slid 0.7% from July to a seasonally adjusted annual rate of 4.04 million in August. Year-over-year, sales fell 15.3% (down from 4.77 million in August 2022).

Of course now that I read that The Clinton’s see blood in Ukraine and are having the Biden Administration use the Clinton Global Initiative (CGI) be in charge of $25 BILLION on humanitarian relief. After The Clinton’s debacle with Haiti, nothing surprises me anymore.

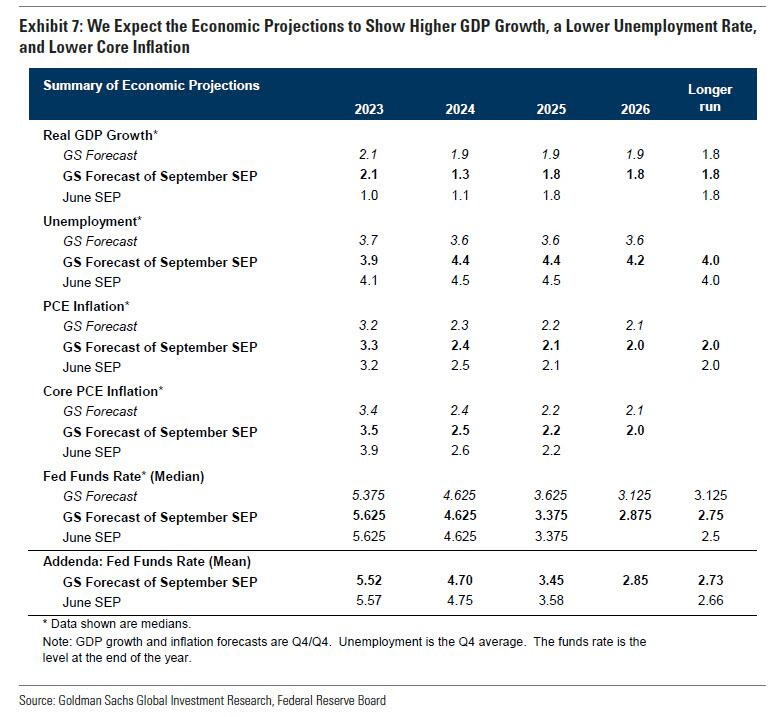

The median of indications will show that policymakers expect a decline in the benchmark rate of as little as 50 basis points or 75 basis points for 2024, compared with the 100 basis points their plot showed in June. I expect the Fed to leave its dot plot for 2023 intact, with the funds rate indicated at 5.6%.

Investors have, of late, swung between pricing rate cuts between the spring and the summer of 2024, which the Fed isn’t in a position to acknowledge based on the current strength of the US economy. The most definitive way of pushing back against that notion is to pencil in less by way of policy loosening than the central bank did in June.

Since that meeting, headline inflation has accelerated, while inflation stripped of housing and energy is still hovering above 4%. Meanwhile, the jobless rate has averaged 3.6% so far this year, around as low as we have ever seen historically — and way below what the Fed estimates will be required to bring the labor market into balance.

The resilience of the job market may, in fact, spur policymakers to pencil in a lower unemployment rate for 2024 than the 4.5% they indicated in June.

Consistent with that outlook, the Fed may be disinclined to revise its 1% growth projection for next year by more than a whisker.

Those revisions are likely to mean that the Fed has reduced scope to loosen policy at the first sign of material weakness in the economy.

Given that James Bullard quit the Fed in August, the new set of projections will be lacking a prescient hawk, whose dot plot has been a rewarding schemata to follow for investors in this cycle. That suggests the skew between the median of the Fed rate projections for next year and top range will be considerably narrower.

An interesting corner of the summary of economic projections to watch will be the Fed’s assumption on the neutral real policy rate, which neither stokes inflation nor crimps output. For several years now the Fed has penciled in a longer-run funds rate of 2.50% predicated on inflation of 2%, thereby projecting a neutral rate of 50 basis points.

However, researchers at the New York Fed reckon that the real neutral rate will reach a staggering 250 basis points by the end of the year, one reason why Treasury long-dated yields have been sticky this late in the policy cycle.

All told, the dot plot and summary of economic projections is what will guide the Treasury market reaction, and from the looks of it, the markets may not like what they see.

This isn’t Barbara Tuchman’s class novel about the horrors of World War I, but the ongoing horrors of Bidenomics with its guns pointed at the American middle class.

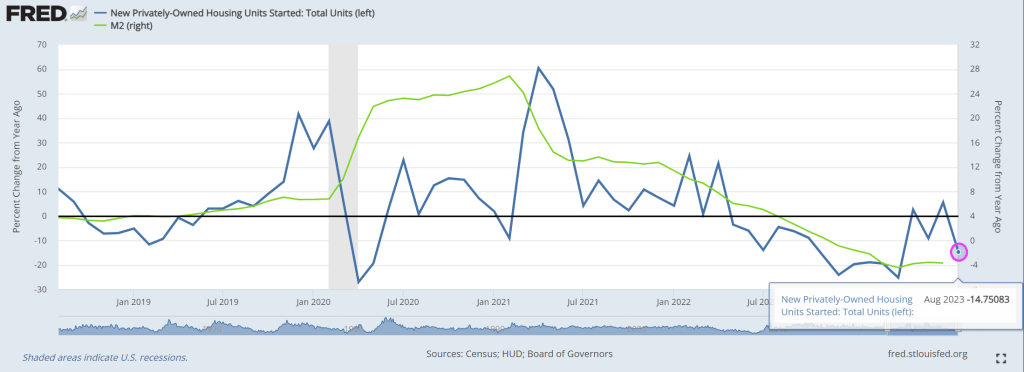

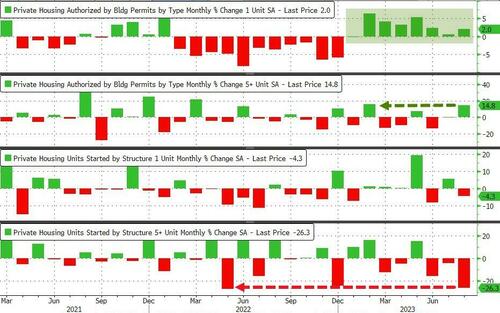

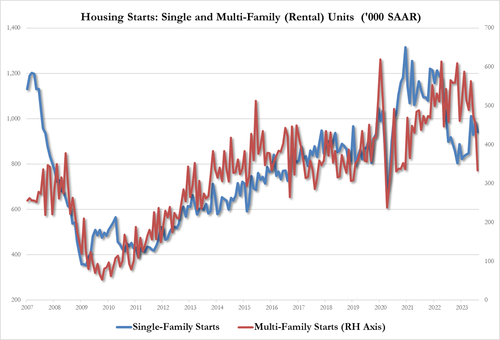

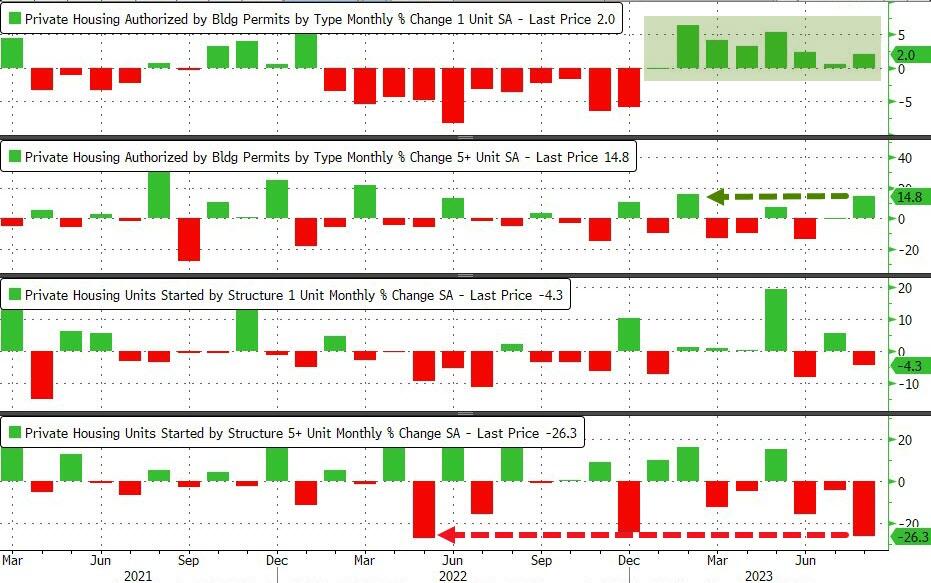

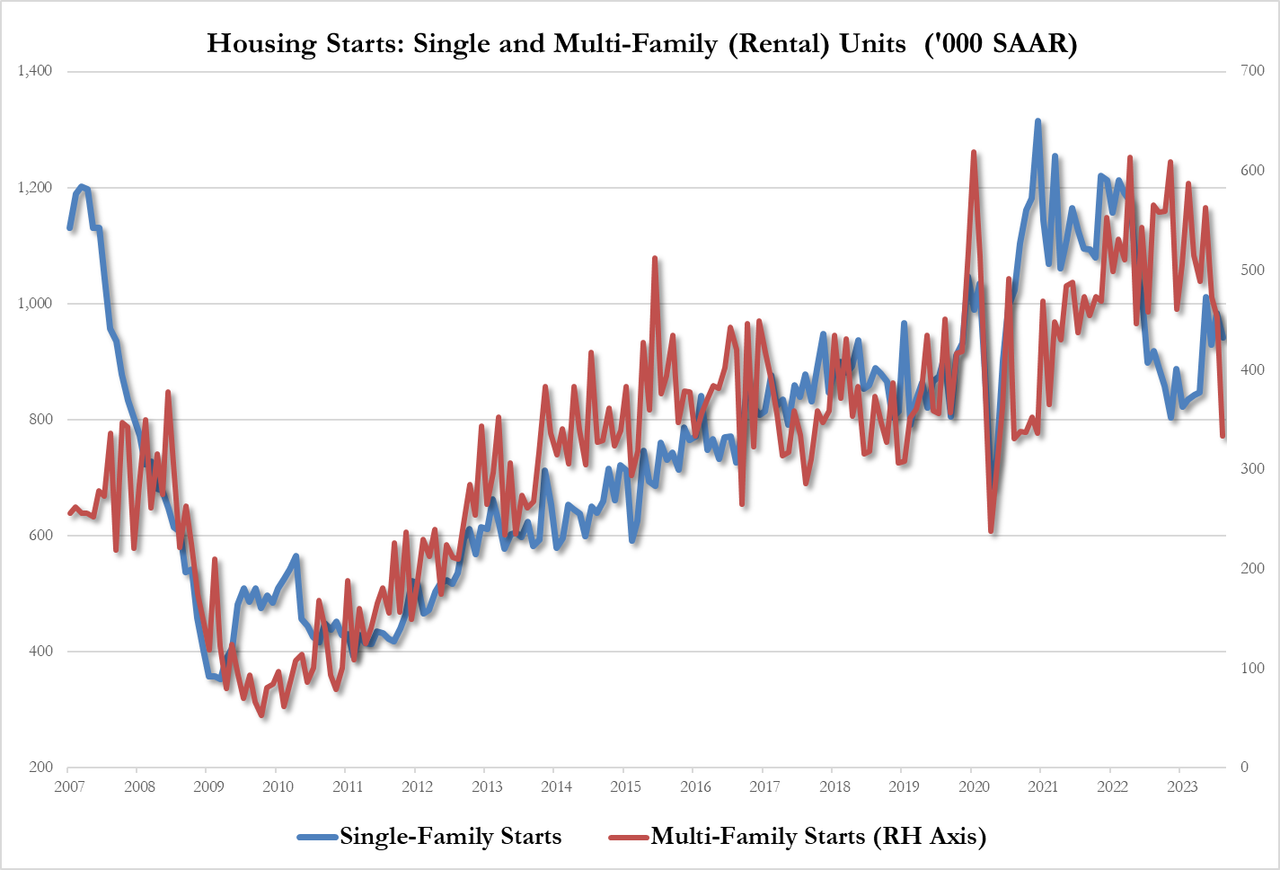

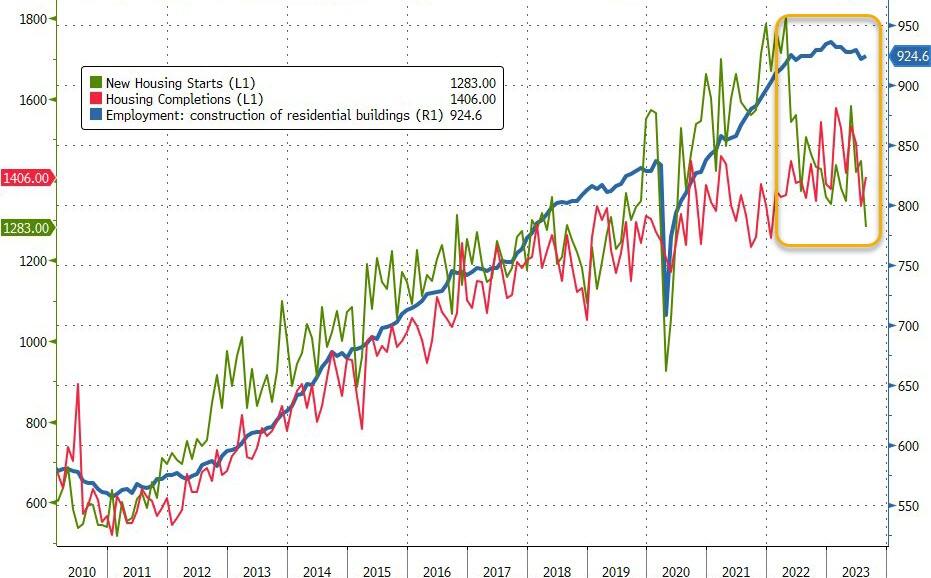

Privately‐owned housing starts in August were at a seasonally adjusted annual rate of 1,283,000. This is 11.3 percent below the revised July estimate of 1,447,000 and is 14.8 percent below the August 2022 rate of 1,505,000.

Single‐family housing starts in August were at a rate of 941,000; this is 4.3 percent below the revised July figure of 983,000. The August rate for units in buildings with five units or more was 334,000. This leaves Starts (SAAR) at their lowest since June 2020 and Permits (SAAR) at their highest since Oct 2022…

Source: Bloomberg

Under the hood, multi-family rental starts plunged by the most since June 2020 while single-family permits rose for the 8th straight month…

Source: Bloomberg

For context…

Finally, if sentiment among homebuilders is collapsing again, why are they loading up on permits?

Source: Bloomberg

Source: Bloomberg

And why is construction employment still holding near its highs…

Source: Bloomberg

Will The Fed see permits soaring as homebuilders betting on their dovishness and step in tomorrow to curb-stop that optimism?

The Guns of August … Bidenomics’ guns pointed at the American middle class.

Call Bidenomics a new name: The Biden Blitzkrieg Bop since the administration launched a blitzkrieg attack on America’s middle class and low wage workers through bad energy policies and soaring inflation.

Clearly, economists were wrong earlier this year when they forecast an economic contraction that has yet to manifest. Could they be wrong now?

To be sure, economic growth, the labor market and consumer spending have proven unexpectedly resilient in the face of rising interest rates and elevated inflation. But there are still plenty of signs a recession might still be on its way.

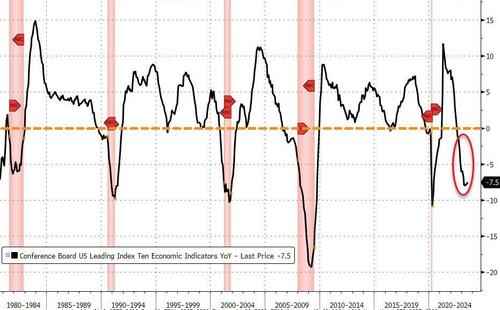

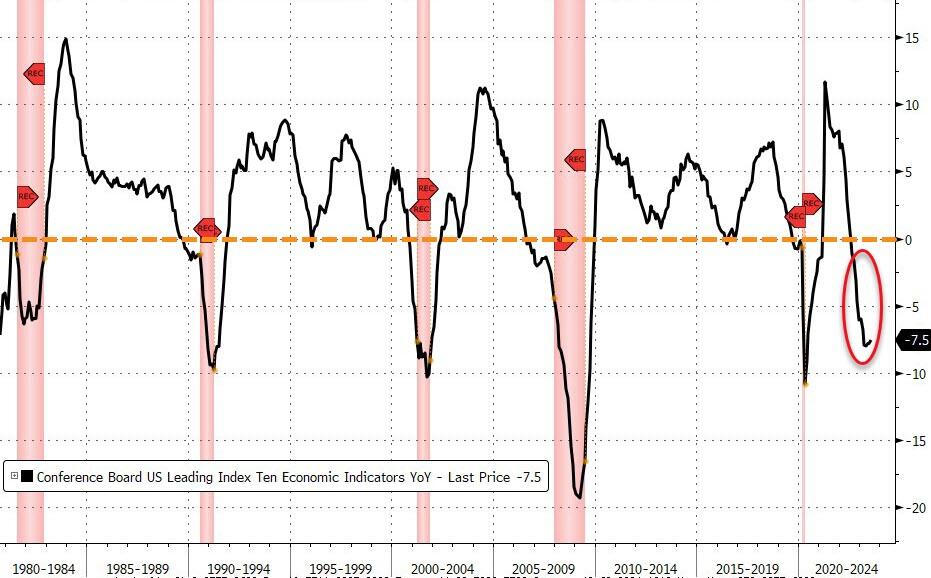

1. An “uncertain outlook” from leading indicators

Many mainstay economic indicators measure the past. So-called leading indicators reflect what likely lies ahead.

“The outlook remains highly uncertain,” said Justyna Zabinska-La Monica, senior manager of business cycle indicators, at The Conference Board.

“The leading index continues to suggest that economic activity is likely to decelerate and descend into mild contraction in the months ahead.”

The index is based on 10 components, ranging from stock prices and interest rates to unemployment claims and consumer expectations for business conditions.

2. Consumer confidence is just a hair above recessionary levels

The Conference Board’s consumer confidence index came in at 80.2 in August, hovering just above 80, the level that often signals the U.S. economy is headed for a recession in the coming year.

It is also a leading indicator used to predict consumer spending, which drives more than two-thirds of U.S. economic activity.

3. Consumers are foregoing big-ticket purchases

Retailers report that their customers have shifted their purchasing habits, spending less on furniture and other big ticket items in favor of necessities. They have also been trading down on grocery items, ditching pricier cuts of beef and buying chicken.

“We saw some switch even to some canned products, like canned chicken and canned tuna and things like that,” Costco’s Chief Financial Officer Richard Galanti told analysts on a May conference call.

Consumer spending has remained one of the bright spots in the economy, but most investors expect consumer spending to slow by as early as next year, Bloomberg’s latest Markets Live Pulse survey found.

4. Credit cards are getting maxed out

U.S. consumers ran up their credit card debt past the $1 trillion mark for the first time last month, according to a report on household debt from the Federal Reserve Bank of New York.

Total household debt, which includes home and auto loans, has eclipsed $17 trillion.

The Federal Reserve Bank of St. Louis reports that credit card delinquencies, which are still low compared to periods such as the Great Financial Crisis, are on the rise.

5. Banks are increasingly reluctant to lend

The latest Senior Loan Officer Opinion Survey by the Federal Reserve reports tightening credit conditions across the board, from business loans to home mortgages and consumer credit.

“Regarding banks’ outlook for the second half of 2023, banks reported expecting to further tighten standards on all loan categories,” the Fed survey concluded.

“Banks most frequently cited a less favorable or more uncertain economic outlook and expected deterioration in collateral values and the credit quality of loans as reasons for expecting to tighten lending standards further.”

When banks pull back on lending, businesses curb their investments and consumers cut spending, and this trend is expected to continue for at least the rest of the year.

6. Corporate bonds are maturing and refinancing them will be costly

Goldman Sachs estimates that $1.8 trillion in corporate debt is coming due over the next two years and it will have to be refinanced at higher interest rates.

The expense will eat up more corporate resources, possibly leading to slower growth and investment.

Recessions occur as debt levels peak and borrowers begin to default.

Moody’s has already reported a surge in corporate defaults this year. In the first half of the year, it counted 55, that’s 53% more than the 36 that defaulted in all of 2022.

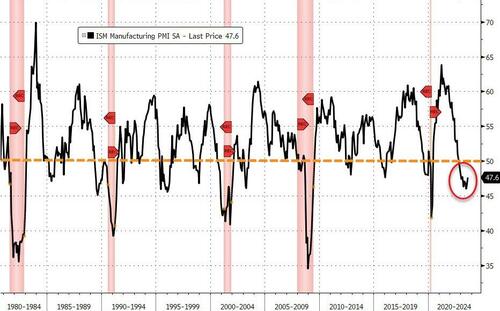

7. Manufacturing remains in a prolonged post-pandemic slump

Respondents to the ISM survey reported weaker customer demand because of higher prices and interest rates.

“Orders are in fact falling faster than factories are cutting output, suggesting firms will need to continue scaling back their production volumes into the near future,” writes Chris Williamson, chief business economist at S&P Global Market Intelligence.

“An increasing sense of gloom about the near-term outlook has meanwhile hit hiring and led to a further major pull-back in purchasing activity.”

8. ‘Cascading crises’ could tip the balance of a slowing global economy

China, a growth engine for the past 40 years, is still struggling to recover from the pandemic, global economic growth has fallen below long-term average, and the ailing world could pull the U.S. economy down with it.

Like a plane crash, every economic disaster stems from a confluence of mishaps. Along these lines, G20 nations on Saturday put out a dire warning:

“Cascading crises have posed challenges to long-term growth,” the group said.

“With notable tightening in global financial conditions, which could worsen debt vulnerabilities, persistent inflation and geoeconomic tensions, the balance of risks remains tilted to the downside.”

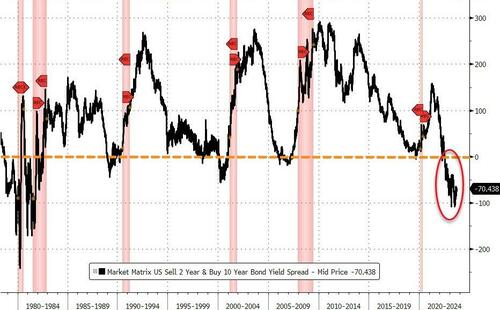

9. The yield curve, a classic recessionary signal, is still inverted

Investors should be paid more for taking a long-term risk than they should for a short-term risk. That’s why the yield on a 10-year Treasury is supposed to pay a higher yield than a 2-year Treasury.

When this is not the case, it’s called an inverted yield curve, and it has long been considered a sign that a recession is due within the next 18 months.

The yield curve for 10-year and the 2-year Treasury has been inverted since July 2022. It’s been inverted for so long that many observers have given up on its reliability — though it still hasn’t been 18 months since it first inverted.

As for history, the yield curve last inverted was in late 2019, just before the pandemic U.S. recession.

10. Inflation is sticky, and the Fed isn’t done

The soft landing scenario that is so widely embraced is based on observations that inflation has dropped precipitously as the economy continues to grow at a healthy pace and the labor market is still holding strong with the unemployment rate at 3.8%.

The Fed, which has raised interest rates 11 times since March 2022 to curb inflation, can now take a bow. The consumer price index, which measures inflation, has come down from a peak of over 9% in June 2022 to 3.2% on its last reading in July.

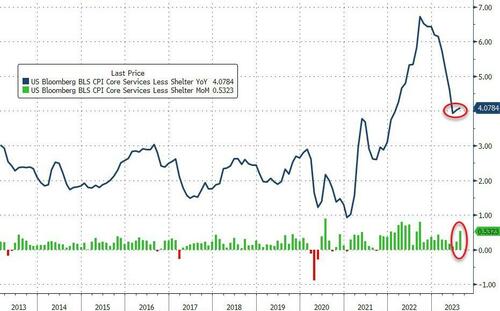

The latest reading on CPI, for August, came out Wednesday, and re-accelerated more than expected, with The Fed’s most-watched ‘Core Services CPI Ex-Shelter’ back above 4.00%…

Meanwhile, the Fed, which next meets on Sept. 19-20 to decide on interest rates, is holding fast to its 2% target for inflation and will keep rates higher for longer, or possibly even raise them further to meet that goal.

Wall Street traders are not expecting another increase this month, according to the CME FedWatch tool, which is based on Fed funds futures trading.

Policy makers are still waiting to see what happens next after raising rates to their highest level in 22 years. Perhaps those actions have already sent the economy on a path of contraction. Or perhaps they haven’t done enough to continue slowing inflation.

Sticky inflation presents on ongoing risk of a recession.

“I believe we must proceed gradually,” Dallas Fed President Lorie Logan said last week, “weighing the risk that inflation will be too high against the risk of dampening the economy too much.”

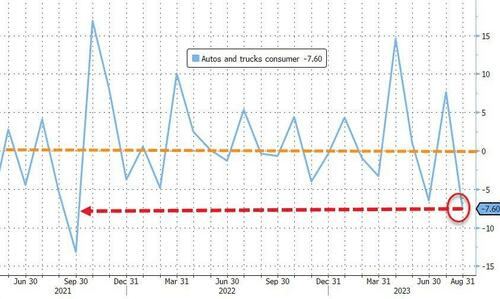

The Big Three auto companies and the UAW are suffering under Bidenomics (code for massive green energy payoffs to large donors). As I pointed out yesterday, the auto industry suffered a large decline of -7.60% in Q2 as a result of rising car prices (going electric is EXPENSIVE) and increasing consumer debt to cope with Bidenomics.

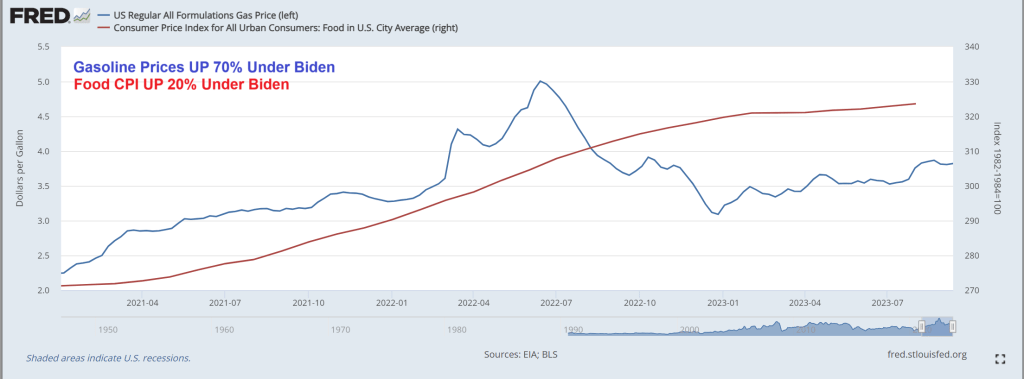

So when we consider the UAW’s demands of $20 an hour hike in pay, you have to consider that under “Union Joe” gasoline prices are up 70%, and food CPI is up 20%. So a 20% pay hike won’t even cover the cost of commuting and will just cover the increased food costs.

The shortened work week to 32 hours? How European of the the UAW.

But perhaps they will have the extra time to travel to Paris France to eat some beef au poivre at Le Bistrot Paul Bert.

Shape of things in the US economy. But a better tune to descible what is happening is over, under, sideways down.

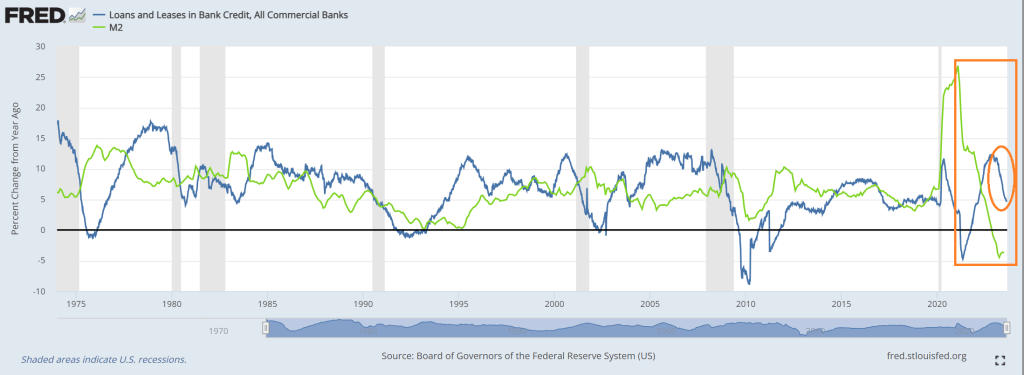

For example, look at this chart of loans and leases at commercial banks, since last year (YoY). The growth rate is plunging rapidly. Of course, M2 Money growth has already crashed.

Loan delinquenices? The trend in delinquencies is rising as consumers struggle with inflation.

When asked about future Fed policies, Powell angrily replied “I’m a man.” Just kidding, but that is almost as nonsensical as his other answers.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.