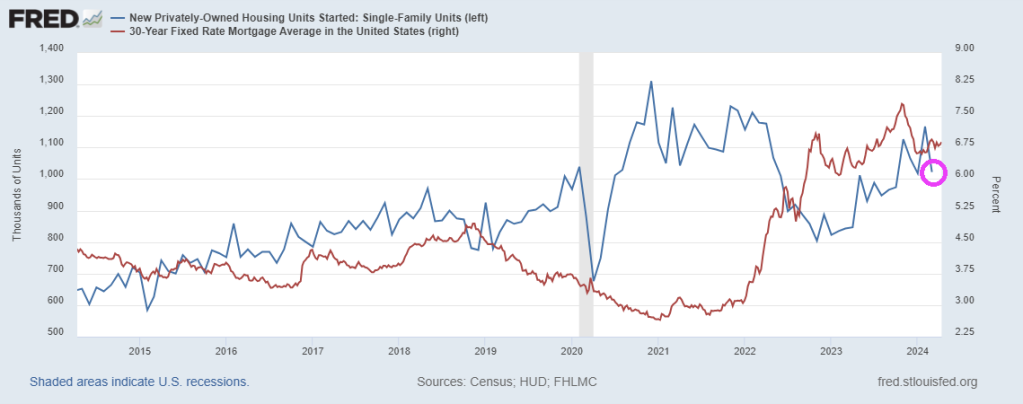

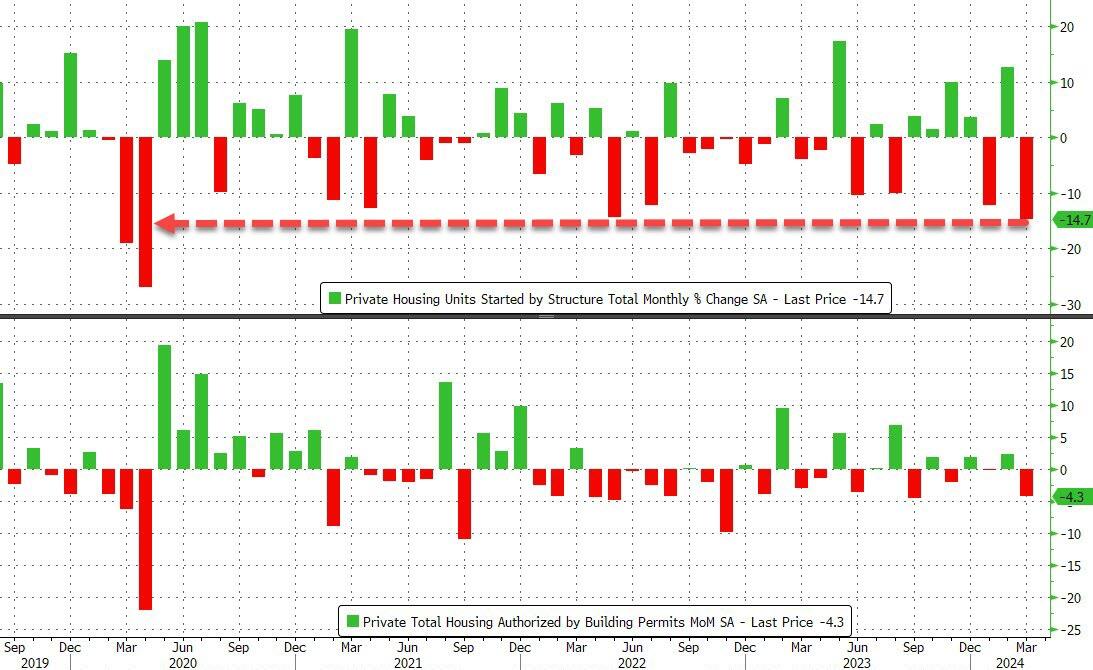

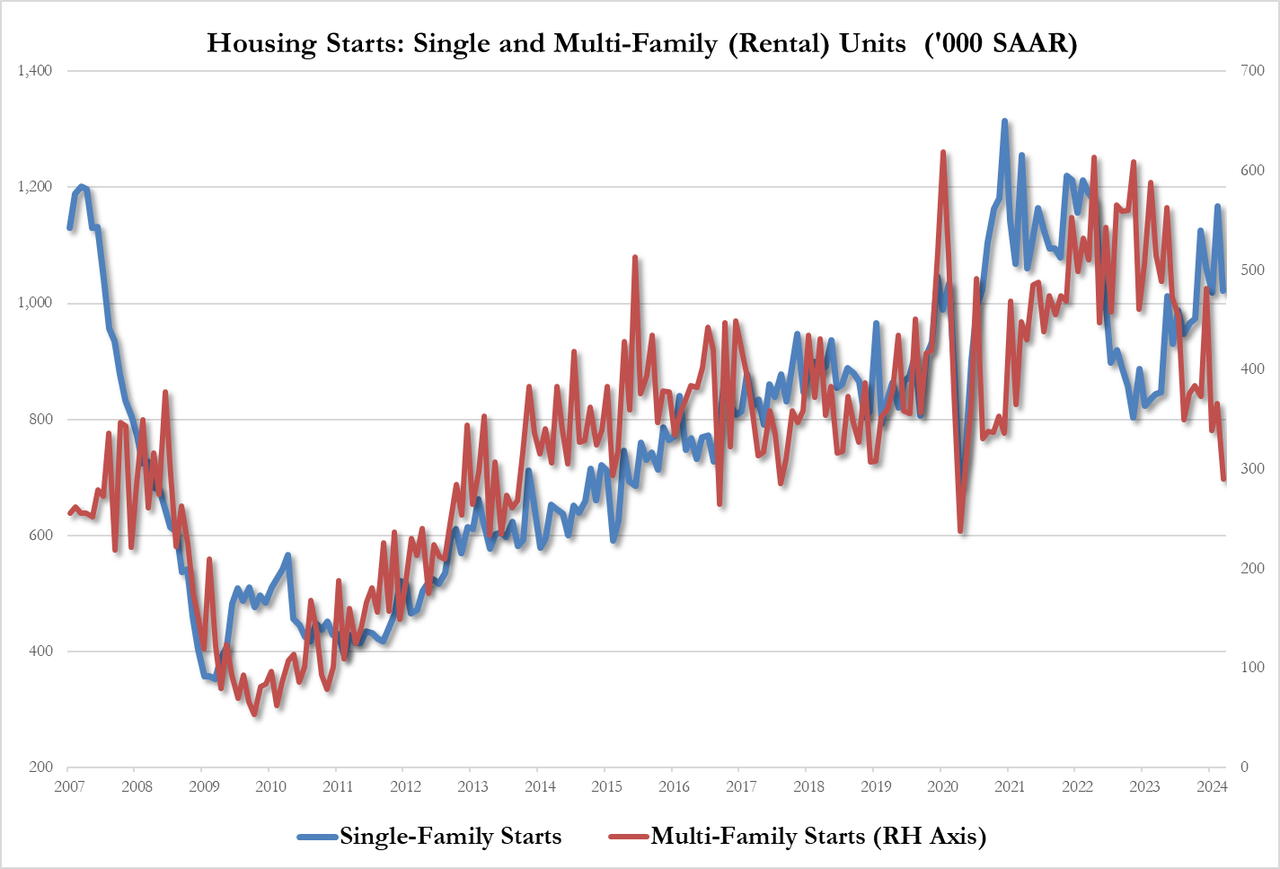

Come feel the noise! After steady growth in 1-unit housing starts under Trump, housing starts have been eratic under Biden despite the foreign invasion force of millions … of low wage workers.

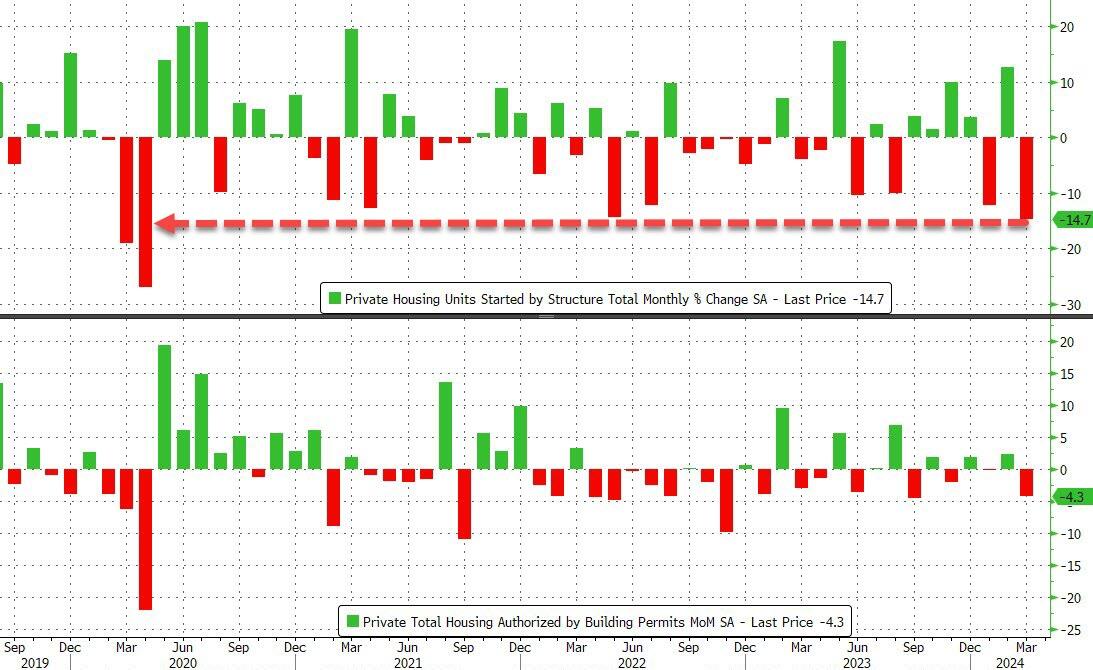

For context, this is the largest MoM drop in housing starts since the COVID lockdowns…

Source: Bloomberg

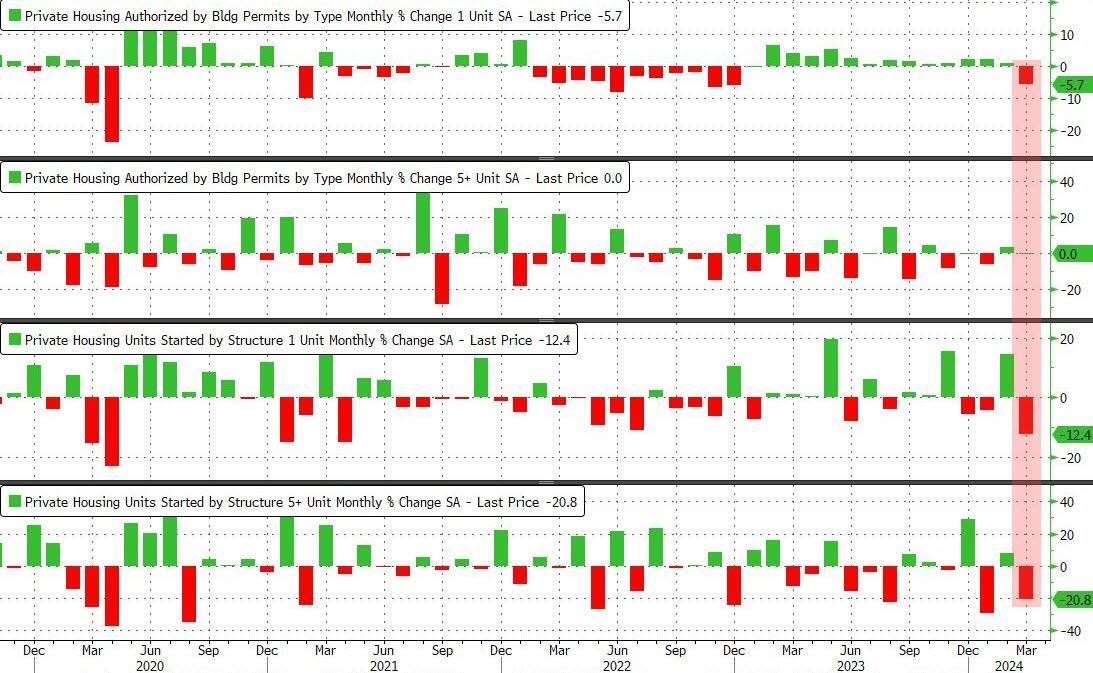

It was a bloodbath across the board with Rental Unit Starts plummeting 20.8% MoM…

Source: Bloomberg

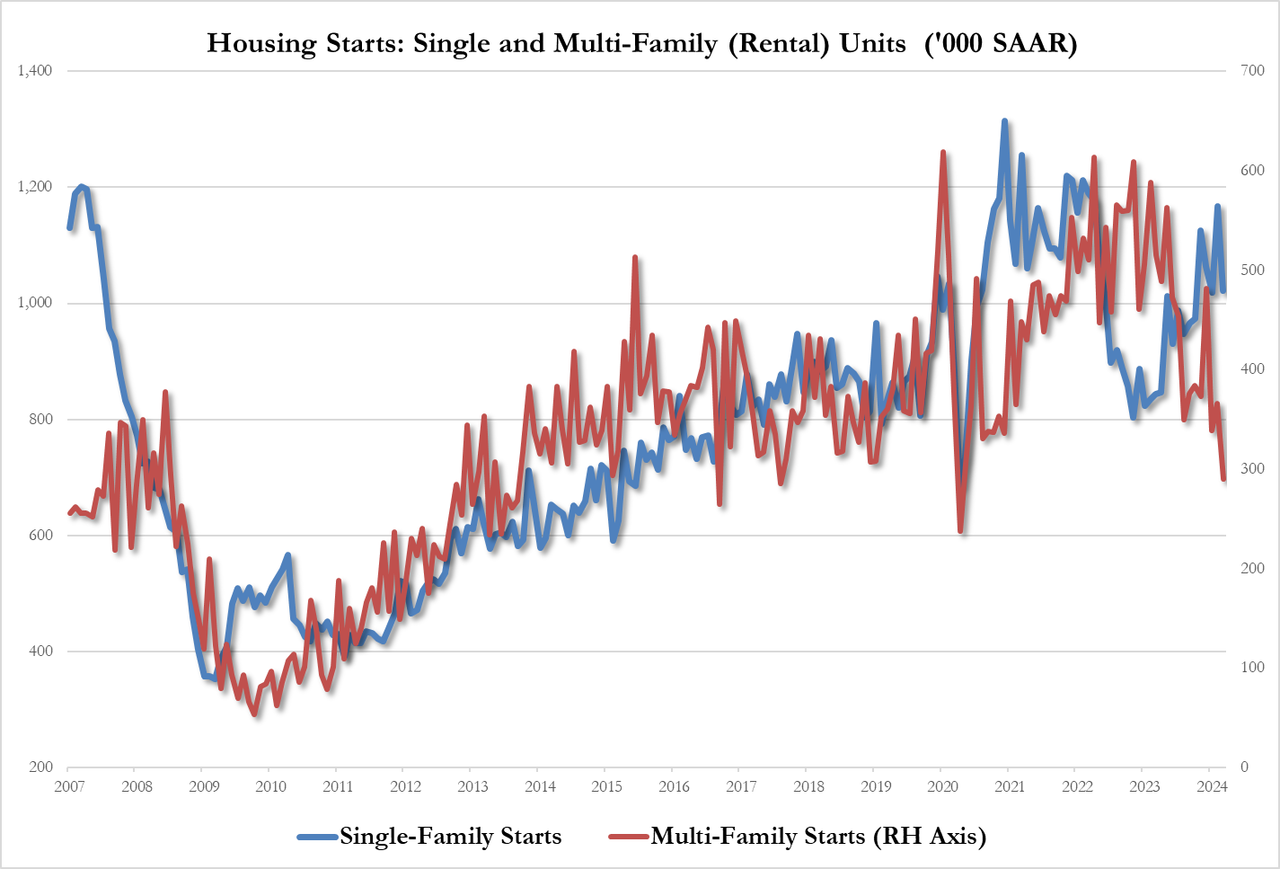

That pushed total multi-family starts SAAR down to its lowest since COVID lockdowns…

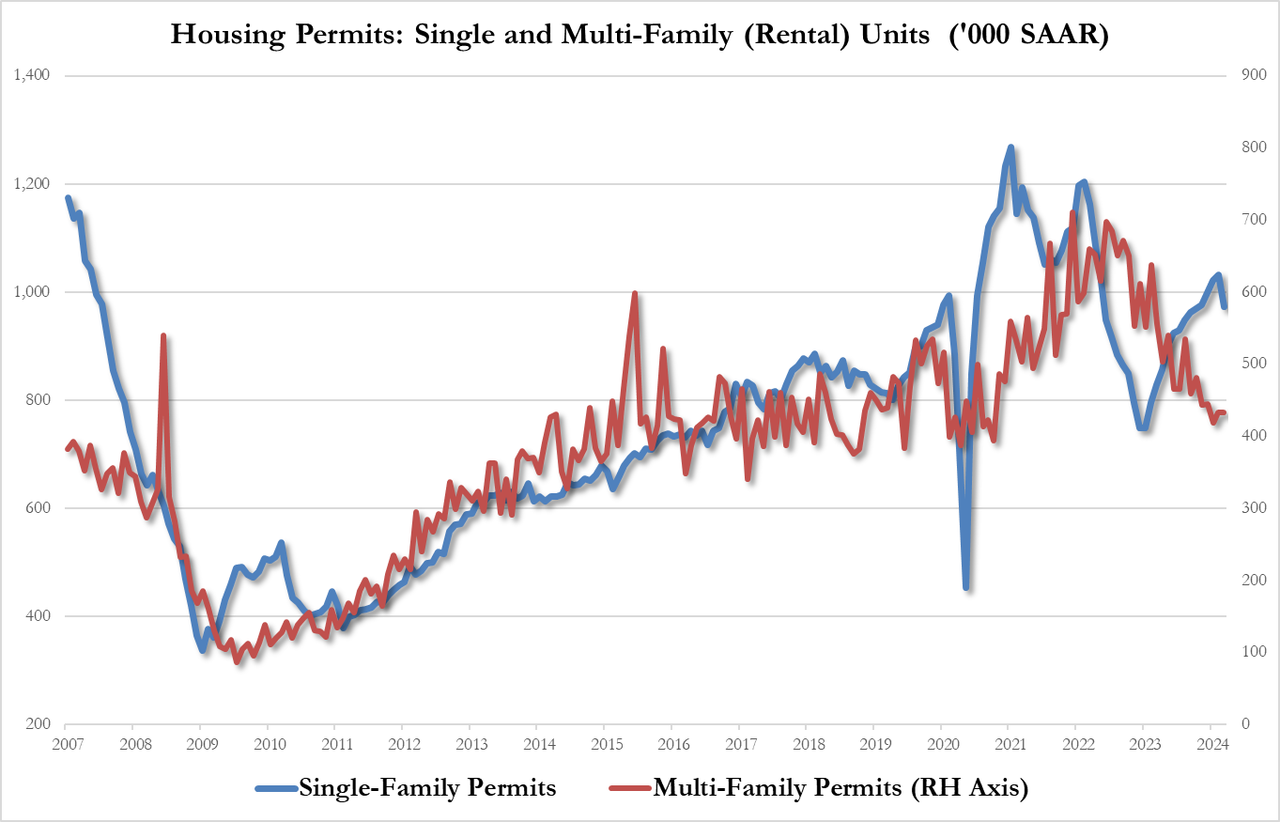

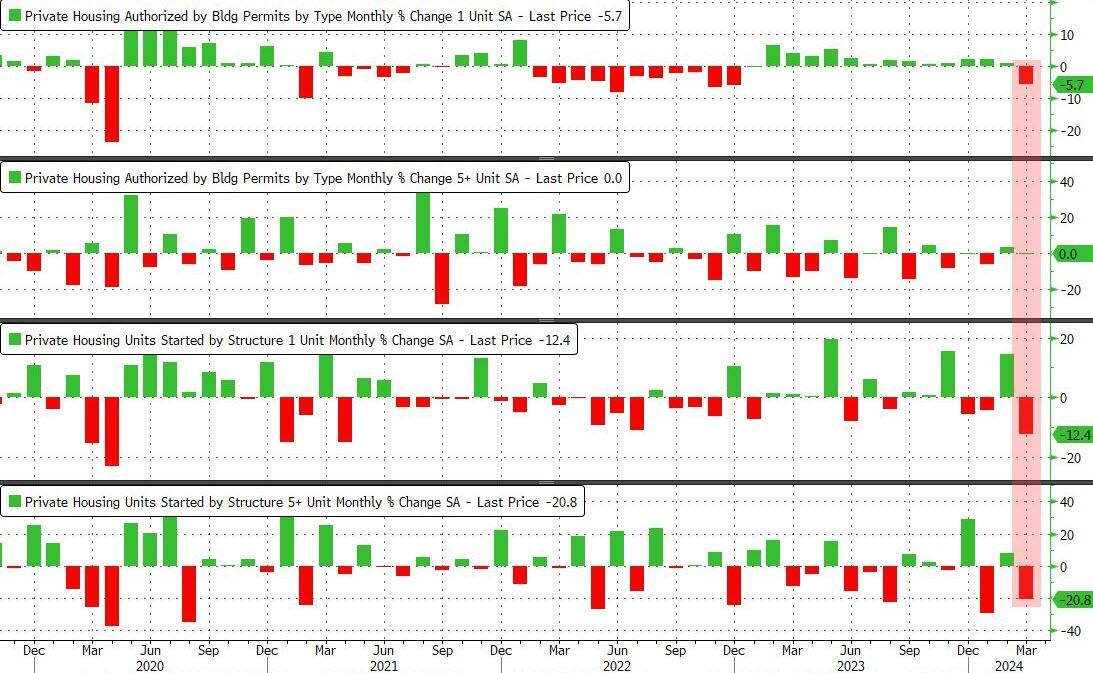

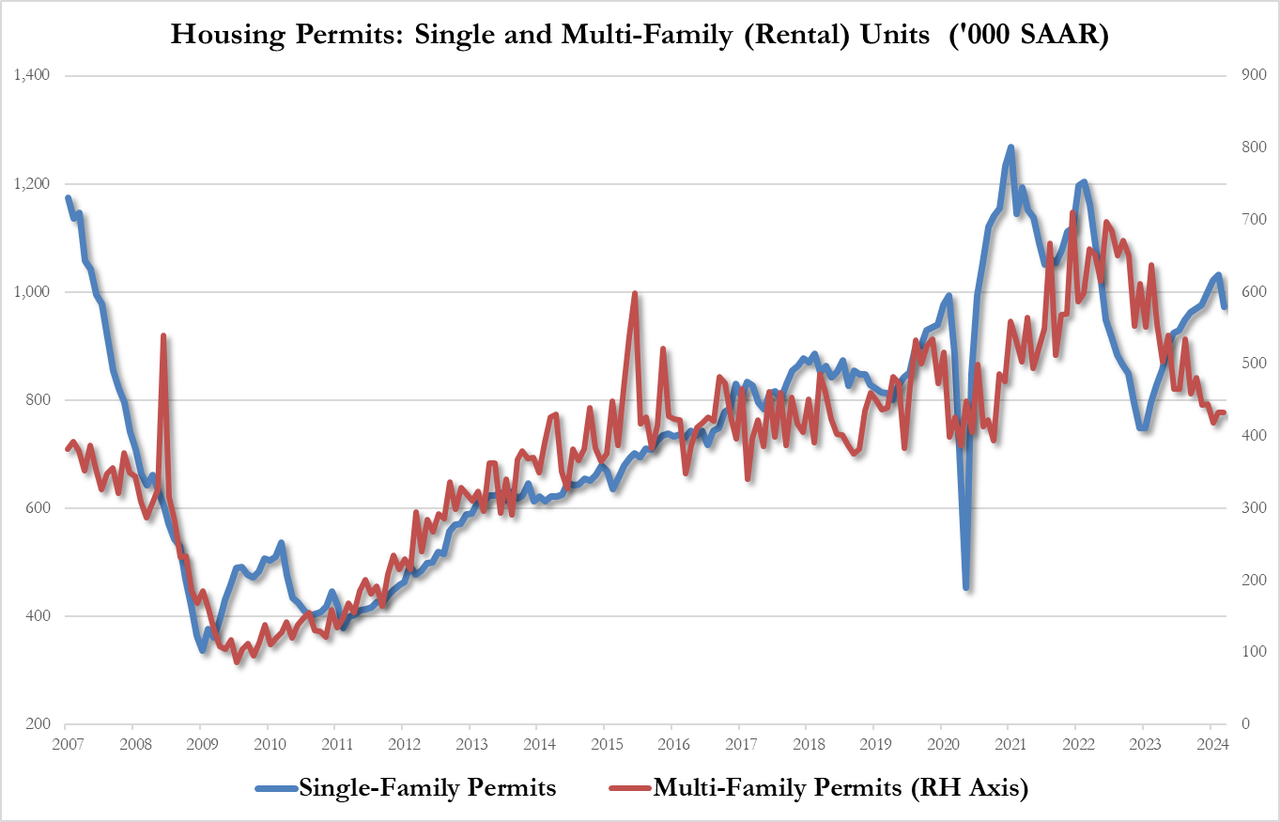

The plunge in permits was less dramatic and driven completely by single-family permits down 5.7% to 973K SAAR, from 1.032MM, this is the lowest since October. Multi-family permits flat at 433K

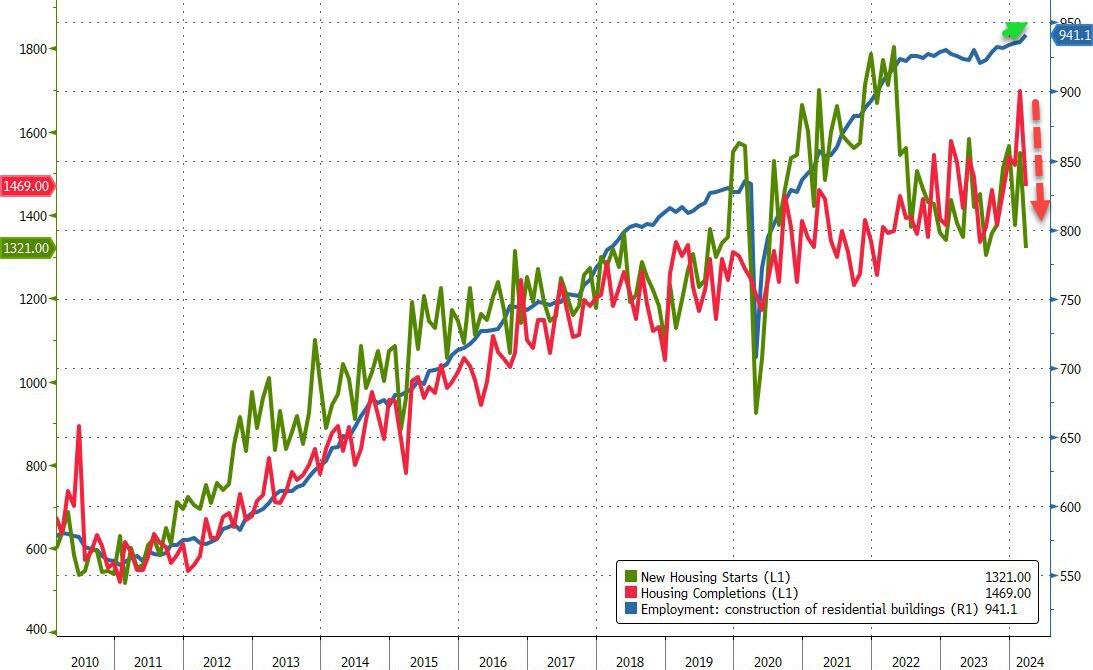

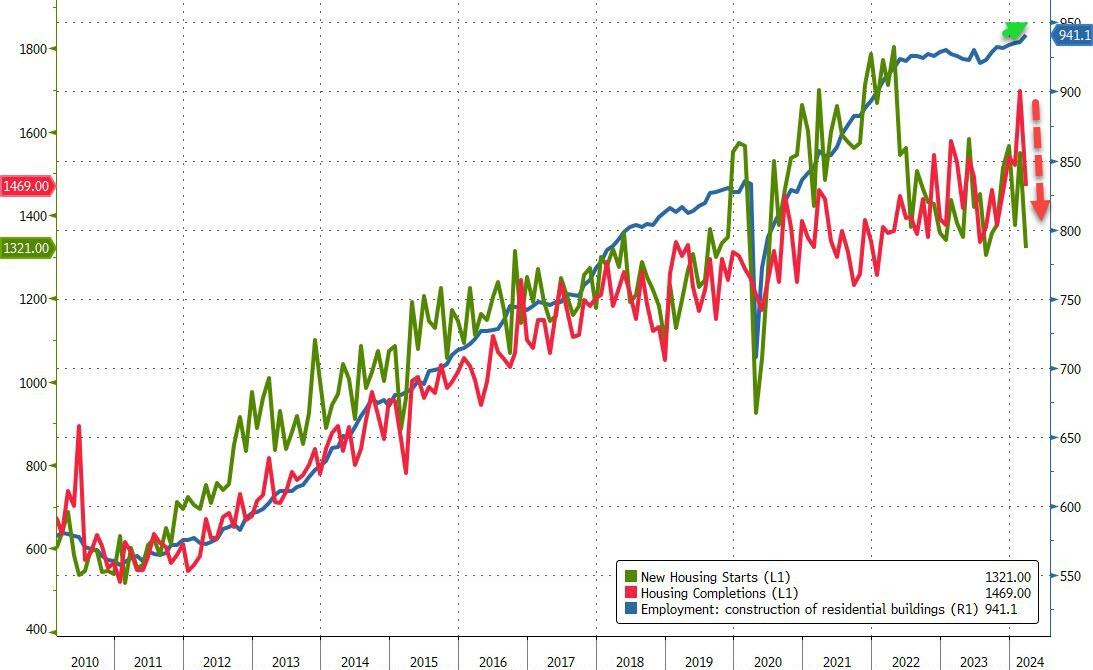

Intriguingly, while starts and completions plunged in March, the BLS believes that construction jobs surged to a new record high…

Source: Bloomberg

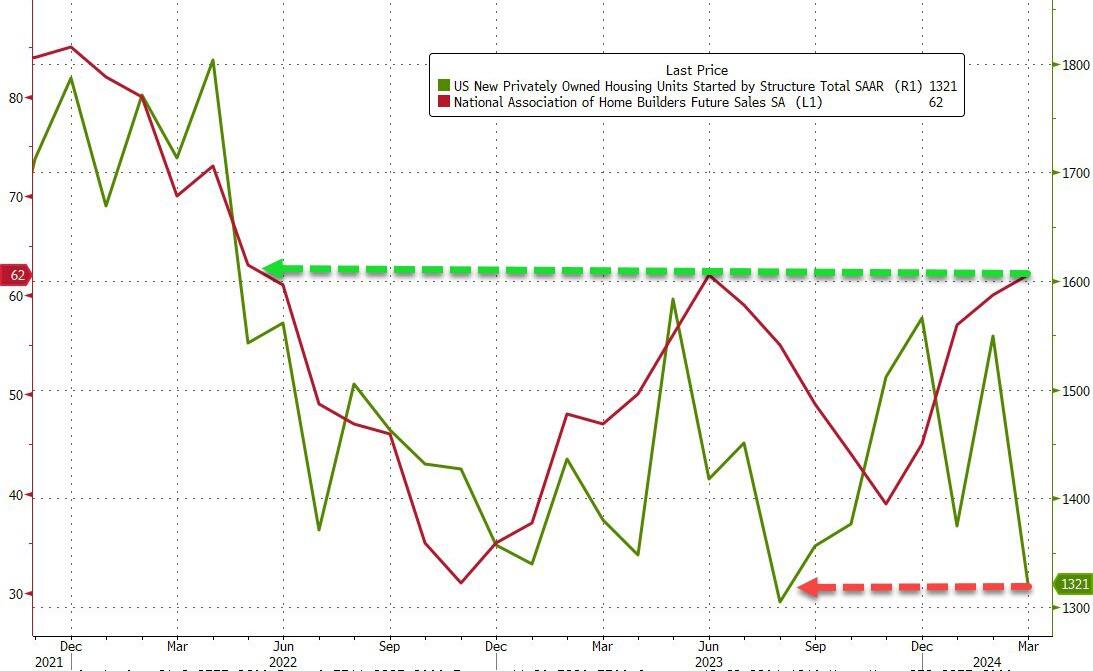

Finally, just what will homebuilders do now that expectations for 2024 rate-cuts have collapsed?

Source: Bloomberg

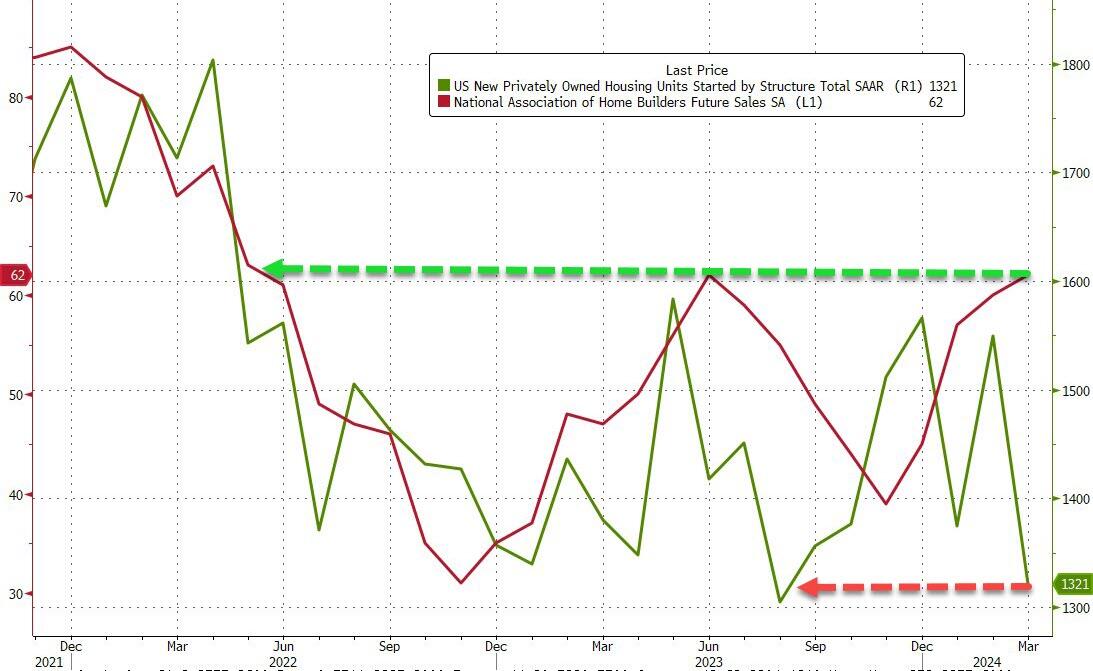

One thing is for sure – do not trust what homebuilders ‘say’ (as NAHB confidence jumped to its highest since May 2022 at the same time as housing starts crashed)…

Joe Biden likes to sell himself as “working class Joe” or “union Joe.” The truth is anything but. He is “Washington DC insider Joe” or “big corporate Joe.”

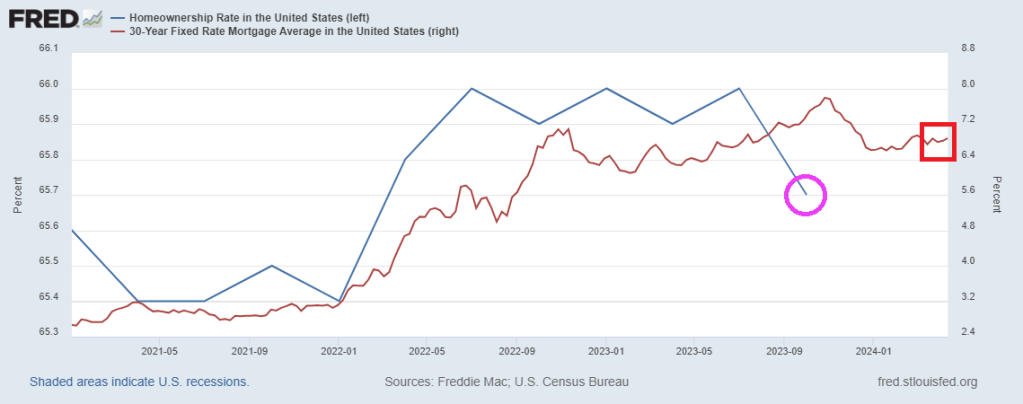

The US mortgage 30 year rate is down slightly today to 7.30%. That is a whopping 160% increase since Biden’s Presidency began.

Mortgage rates will continue to climb as the US Treasury 10-year yield climbs.

The US homeownership rate is falling as mortgage rates climb.

US CPI on trend for 4-5% at US election in November.

Source: BofA

Above 5%…?

Strong CPI raises market probability of YE25 rates above 5%.

Source: Goldman

Cyclical inflation remains too elevated

“Our measure of cyclical inflation–which should capture the impact of excess demand on prices–appears to be stuck at around 5%, which is too elevated”

Source: Safra

US alone

The US is the only economy in the G10 where the latest inflation print surprised to the upside.

Source: Goldman

200% of GDP

Under current policies, government debt outstanding will grow from 100% to 200% of GDP.

Source: Apollo

Close to $9 trillion in maturities

That’s a significant amount of government debt maturing within the next year.

Source: Apollo

Every year a deficit

OMB forecasts 5% budget deficit every year for the next 10 years.

Source: Apollo

A billion per day….is long gone

US government interest payments per day have doubled from $1bn per day before the pandemic to almost $2bn per day in 2023.

Source: Apollo

Biggest Story of 2020s…Ugly End of 40-year Bond Bull

Chart shows long-term US government bond (15+ year) rolling 10-year annualized returns, %.

Source: Flow Show

Highest yields in 15 years

The intermediate part of the yield curve still offers the highest yields in over fifteen years.

Source: Piper Sandler

Finally, electricity costs keeps rising, ESPECIALLY with the misnamed Inflation Reduction Act (IRA). The real name of the IRA should have been the Large Green Donor Increase Act (LGDIA).

Joe Biden, his Administration, and The Federal Reserve are really “The Alligator People.” Despite what they tell you, they have small brains (particularly Biden) and are hyperfocused on spending.

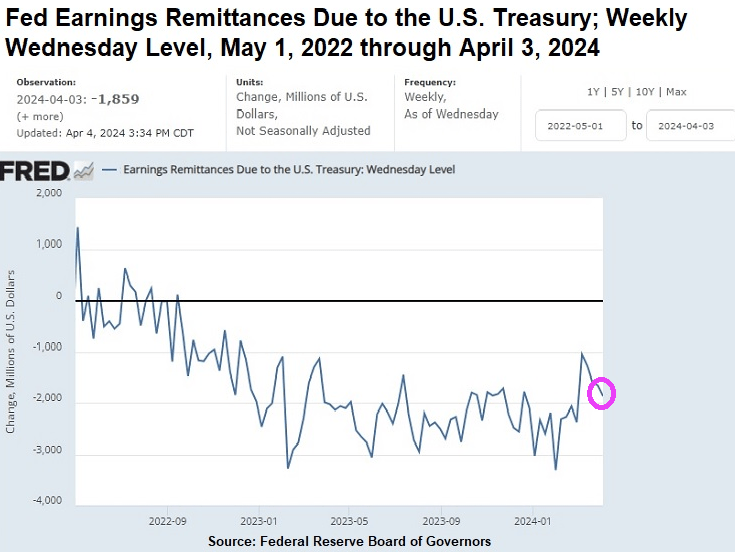

A good example comes from “Wall Street On Parade” where they show that The Federal Reserve is still paying BILLIONS to US Treasury in the form of remittances (losses). While at the same time, paying the mega banks on Wall Street high interest loans.

As of April 3 of this year, the Federal Reserve (Fed) has racked up $161 billion in accumulated losses. We’re not talking about unrealized losses on the underwater debt securities the Fed holds on its balance sheet, which it does not mark to market. We’re talking about real cash losses it is experiencing from earning approximately 2 percent interest on the $6.97 trillion of debt securities it holds on its balance sheet from its Quantitative Easing (QE) operations while it continues to pay out 5.4 percent interest to the mega banks on Wall Street (and other Fed member banks) for the reserves they hold with the Fed; 5.3 percent interest it pays on reverse repo operations with the Fed; and a whopping 6 percent dividend to member shareholder banks with assets of $10 billion or less and the lesser of 6 percent or the yield on the 10-year Treasury note at the most recent auction prior to the dividend payment to banks with assets larger than $10 billion. (This morning the 10-year Treasury is yielding 4.41 percent.)

Operating losses of this magnitude are unprecedented at the of Fed, which was created in 1913. In a press release dated March 26, the Fed stated this: “The Reserve Banks’ 2023 sum total of expenses exceeded earnings by $114.3 billion.”

As the chart above indicates, the Fed’s ongoing weekly losses have ranged from a high of $3.3 billion for the week ending Wednesday, January 31, 2024, to $1.86 billion for the most recent week ending Wednesday, April 3, 2024.

American taxpayers have good reason to sit up and pay attention to the Fed’s giant and ongoing losses. That’s because when the Fed is operating in the green, as it was on an annual basis for 106 years from 1916 through 2022, the Fed, by law, turns over excess earnings to the U.S. Treasury – thus reducing the amount the U.S. government has to borrow by issuing Treasury debt securities. According to Fed data, between 2011 and 2021, the Fed’s excess earnings paid to the U.S. Treasury totaled more than $920 billion.

WHO pays for the student loan forgiveness? It just doesn’t vanish, it is transferred to taxpayers. Alligators like Alexandria Ocasio Cortez going on talk shows to argue the benefits of being free from financial obligations that student voluntarily agreed to. Say, can AOC get my mortgage forgiven?? Just kidding. Now those same students can borrow additional money to get MBA degrees with the expectation that the student loan is “free money.”

Yes, Biden is acting recklessly (no surprise). Here is a picture of King Gator, Joe Biden.

The Biden Administration and The Federal Reserve ARE the alligator people. Except these gators are hungry for your money and votes constantly.

Despite Biden’s rambling that inflation is improving, bear in mind that the inflation rate is at it highest in 50 years. Yes, it has improved from 18% in 2022 to above 10% today.

A recent research paper by four noted economists, including Larry Summers, the former Treasury Secretary under Barack Obama and former Harvard President, discovered that the real inflation rate during the Biden years, using pre-1983 calculations reached 18% in 2022.

The number is the highest inflation rate the country has seen in over 50 years.

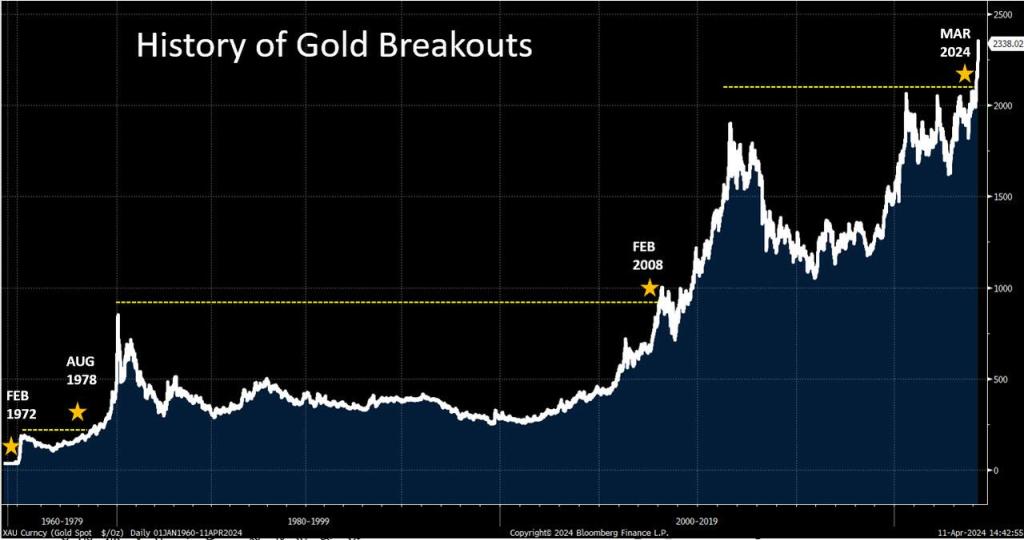

Gold futures prices are soaring and are at $2,422.00. Gold futures prices are up 19.61% over the past year.

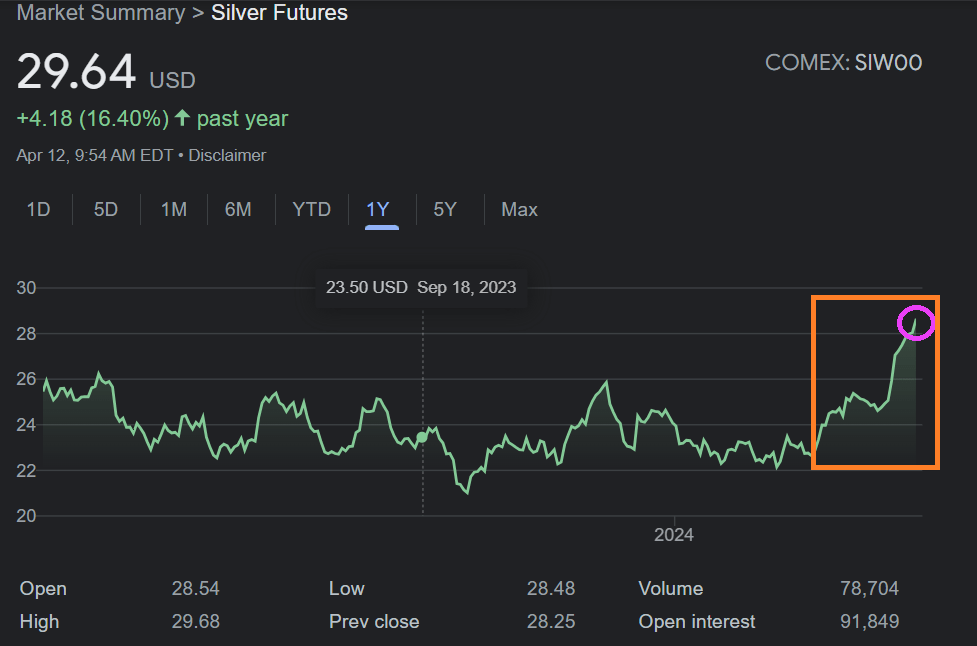

Silver futures prices are also soaring and are at $29.64. Silver futures prices are up 16.40% over the past year.

Bitcoin is almost at $70,000 and is up 133.44% over the past year.

Returning to gold, we are seeing another gold breakout, like the breakout in 2008.

Even central banks are loading up on gold, silver, and cryptos. Why? Primarily fear of US reckless budgets and exploding debts/deficits (don’t listen to Biden talk about how “he” reduced deficits and debt (both have risen to dangerous levels under he inattentive eyes).

However, calming the jangled nerves of pension funds is that the S&P 500 stock market index is up 26.04% over the past year.

Overall prices are up by 19.4% since Biden took office.

Of course, the S&P 500 is not sustainable given that it has been driven by excessive spending by the Biden Adminstration coupled with still massive monetary stimulus from The Federal Reserve.

In summary, gold, silver and cryptos are rising on FEAR! Of Biden, Congress and The Fed.

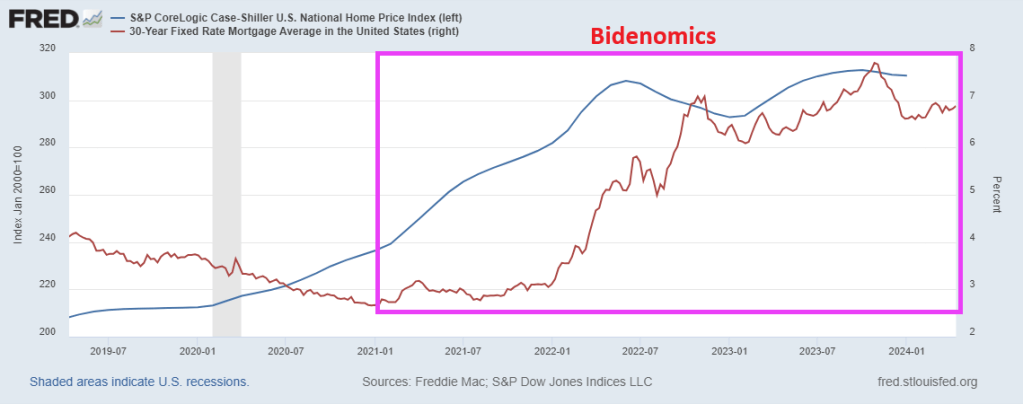

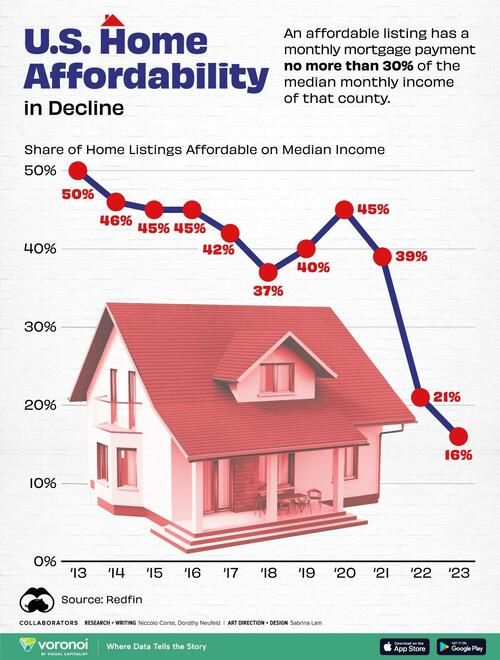

One reason that America’s youth is disgusted with Bidenomics is skyrocketing prices, particulalry housing. (simply unaffordable). Thanks to awful economic policies, home prices are up 32.5% under Biden and 30-year mortgage rates are up a whopping 160%! Good luck buying a home with a part-time job.

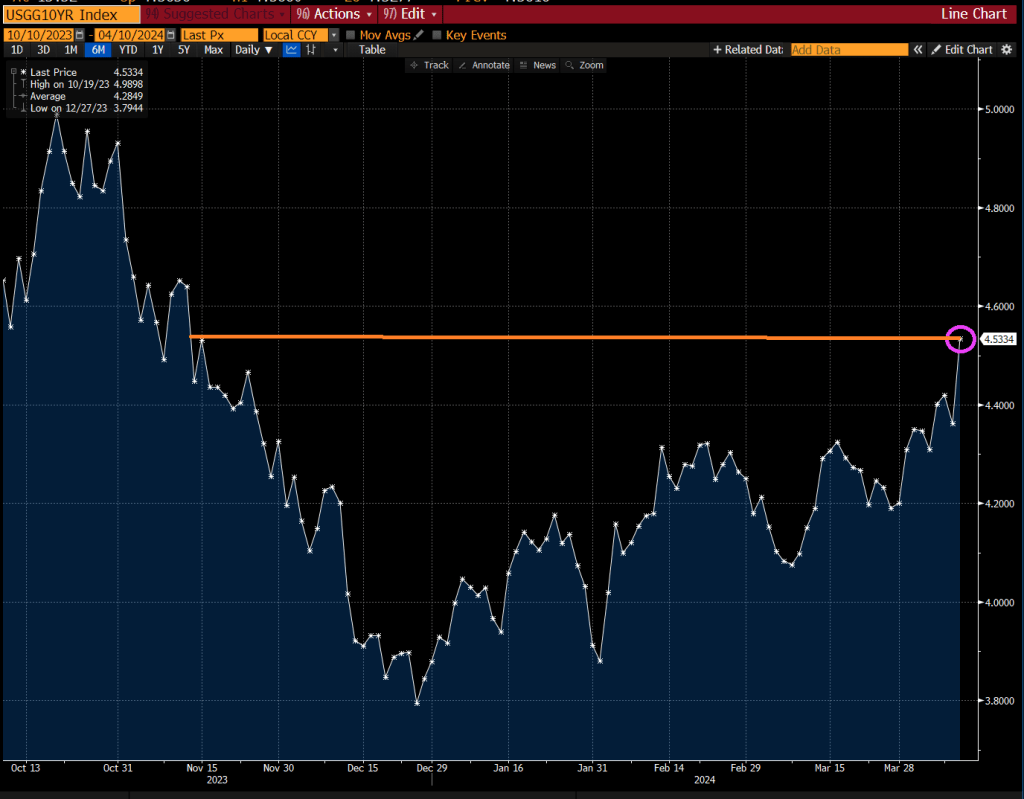

The bad news is that the 10-year Treasury yield rose to 4.53%, the highest since November 2023. This means that mortgage rates will rise even further.

Yes, rising rates AND home prices are daunting to part-time job holders.

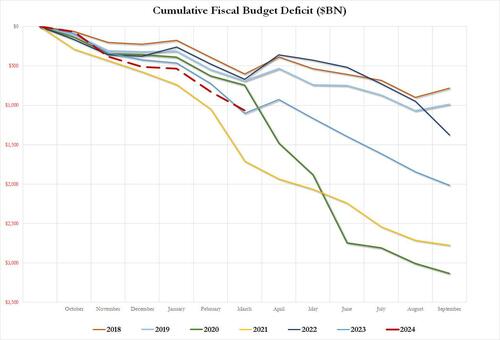

Under Biden’s “Reign of Error”, the interest on US debt just hit a record $1.1 trillion and the US deficit for just the first six months of fiscal 2024 is also $1.1 trillion.

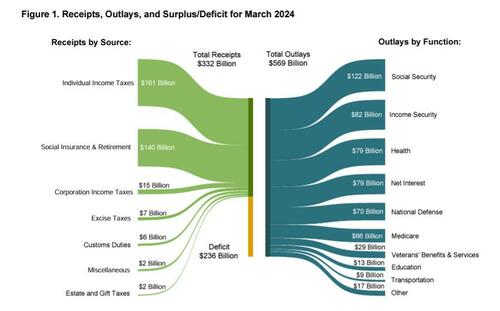

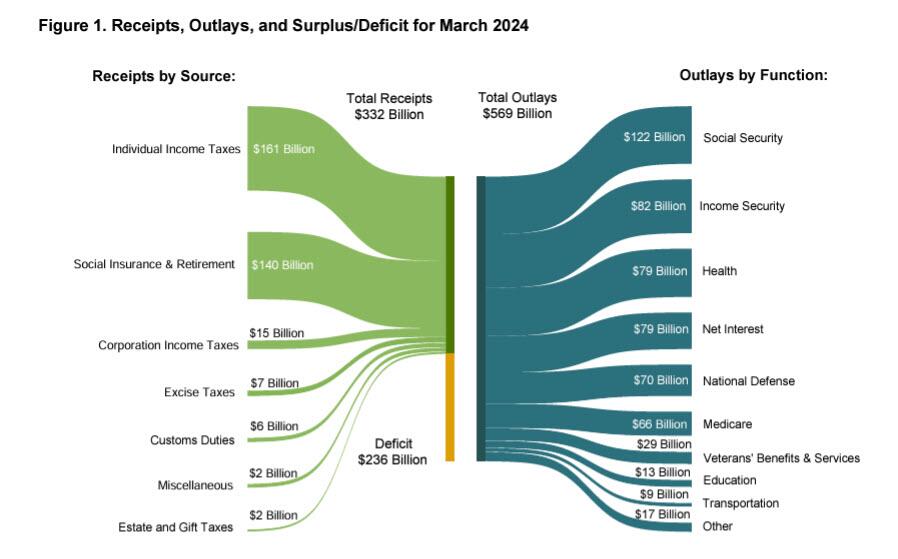

According to the latest Treasury Monthly Statement, in March the US deficit hit $236 billion, some $40 billion more than the $196 billion expected, if below February’s $296 billion…

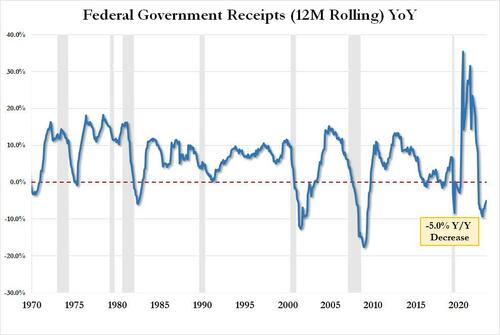

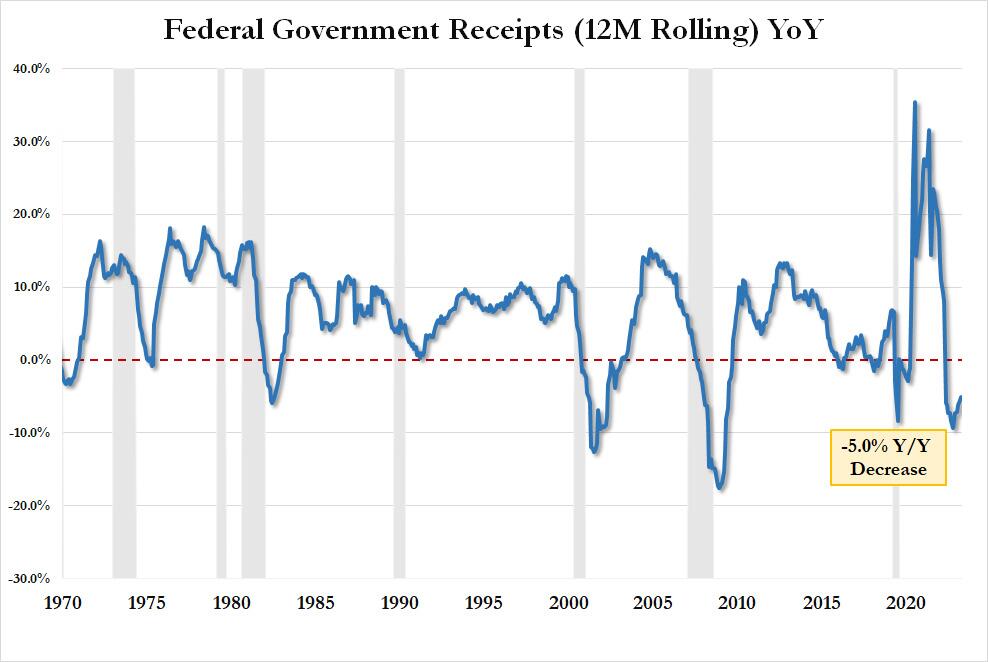

… which was the result of $332 billion in govt tax receipts – translating into $4.580 trillion in LTM tax receipts, and which was down 5% compared to a year ago…

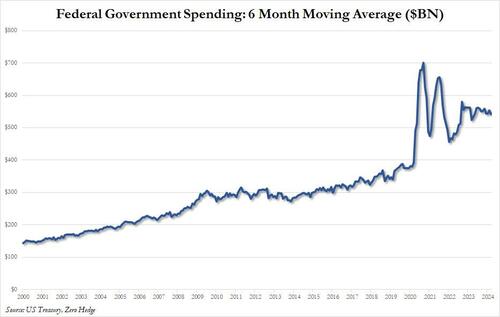

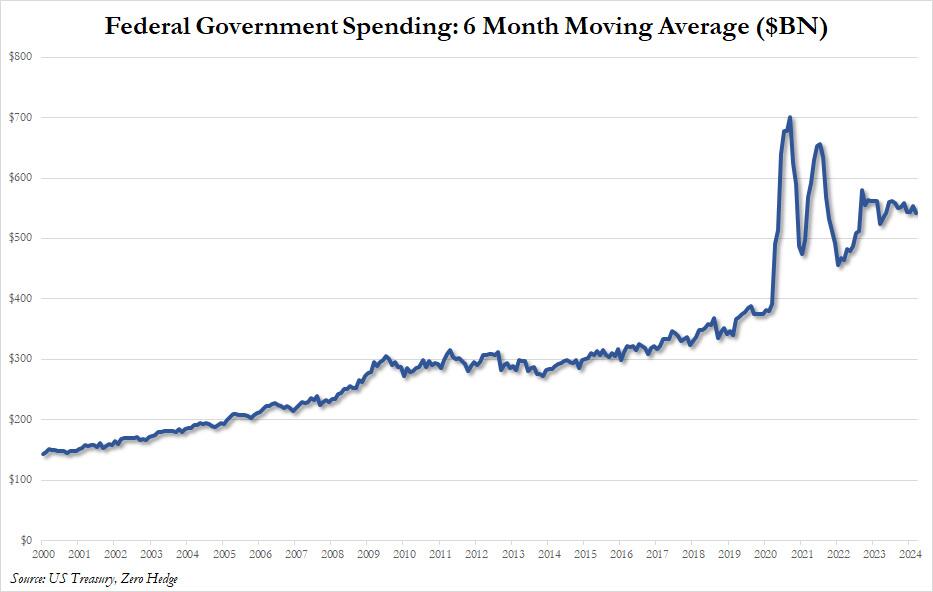

… offset by the now traditional ridiculous monthly outlays, which in March amounted to $568 billion, up from $567 billion in February and the highest monthly spending total in calendar 2024, which translated into a 6 month moving spending average (for smoothing purposes) of $542 billion. Take a wild guess what will happen to the chart below during and after the next recession.

This, incidentally, is a reminder that the US does not have a tax collection problem – it has a spending problem, and no amount of tax changes will fix it; in fact all higher taxes will do is force more billionaires to move to Dubai where they pay zero taxes.

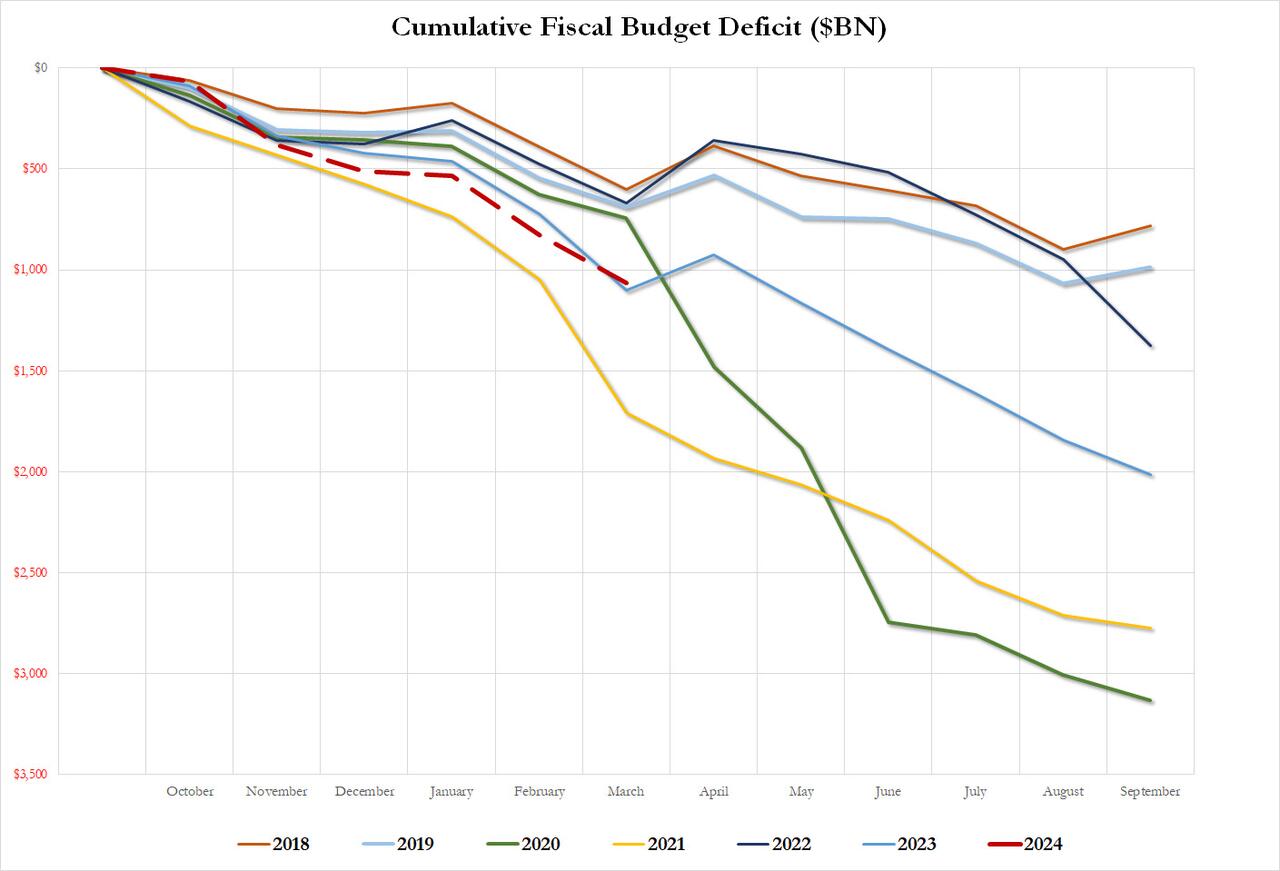

Putting the YTD deficit in context, in the first six months of fiscal 2024, the US deficit hit $1.065 trillion, just shy of the $1.1 trillion reached last year, which was the 2nd highest on record and only the post-covid 2021 was worse. Annualized, we expect total deficit to hit $2.2 trillion in fiscal 2024, a year when the US is supposedly “growing” at a nice, brisk ~2.5% pace. One can only imagine what the GDP growth would be if the US wasn’t set to have a wartime/crisis deficit…

… and we can’t even imagine what US deficit will be after the next recession/depression.

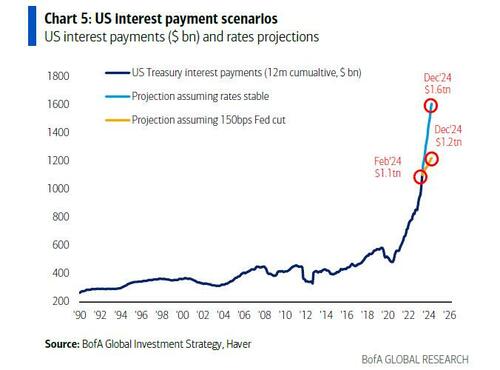

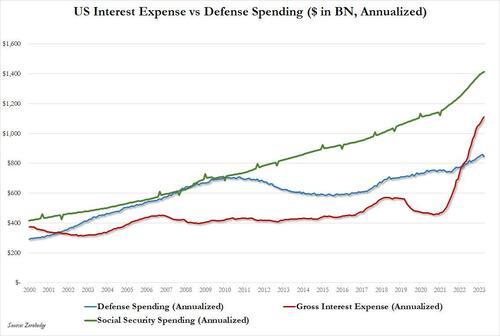

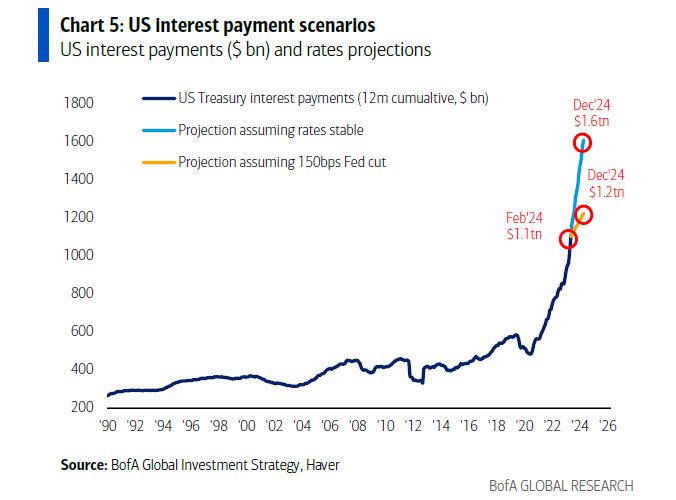

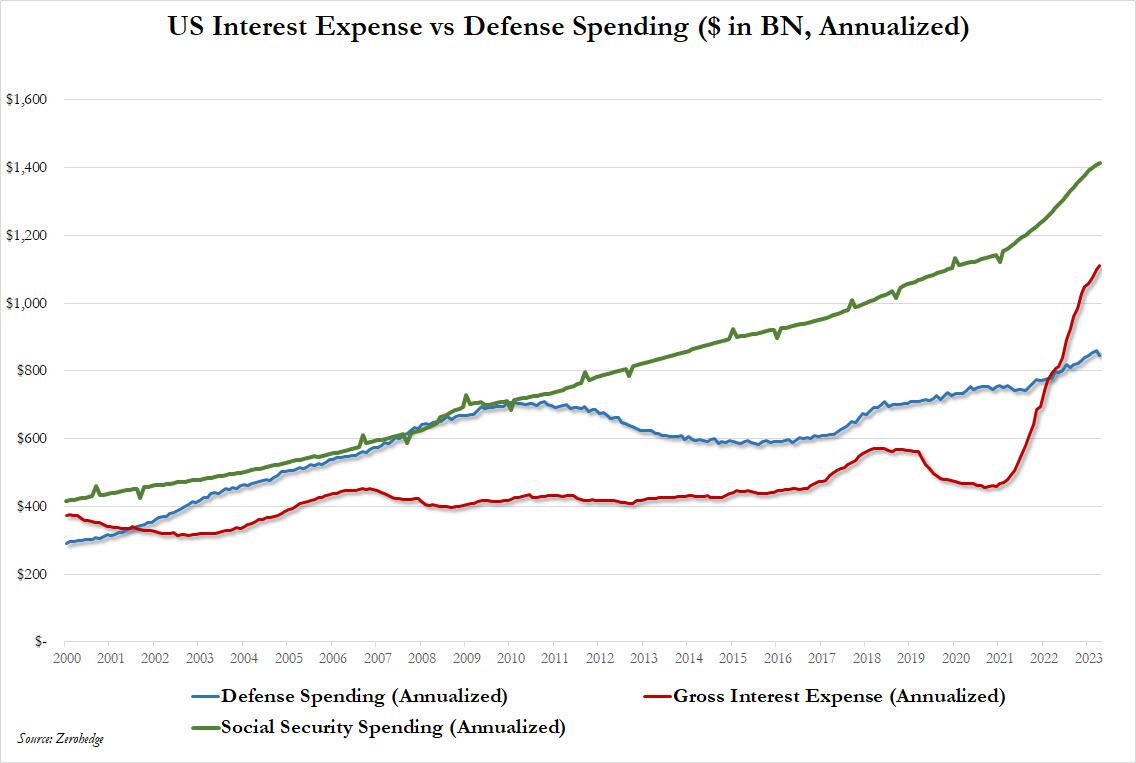

Meanwhile, as reported previously, total US interest continues to explode, and after surpassing total annual defense spending about a year ago, just the interest on US debt will soon become the single largest government outlay as it surpasses social security by the end of 2024, when according to BofA’s Michael Hartnett it hits $1.6 trillion…

.. and surpasses Social Security spending as the single largest spending category in the US government.

Biden has wanted to get rid of Social Security for a long-time and now wants to get rid of Medicare Advantage programs and put everyone on Medicare. Looks like Cloward-Piven!

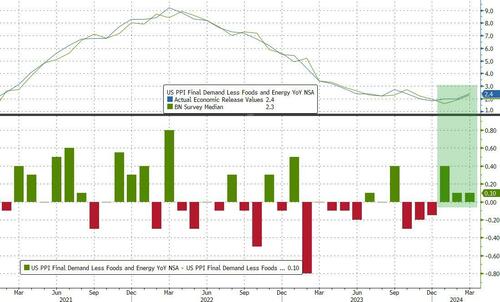

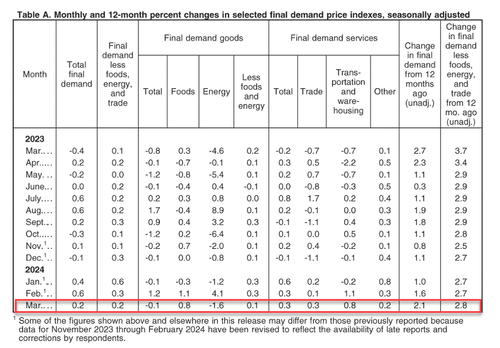

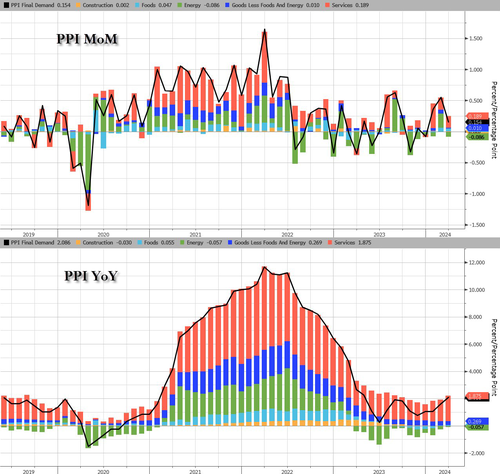

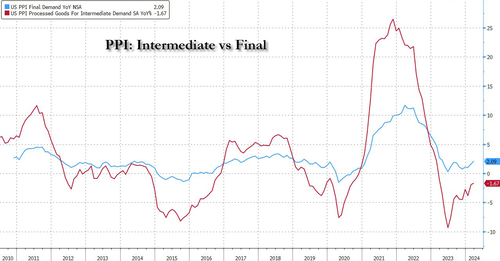

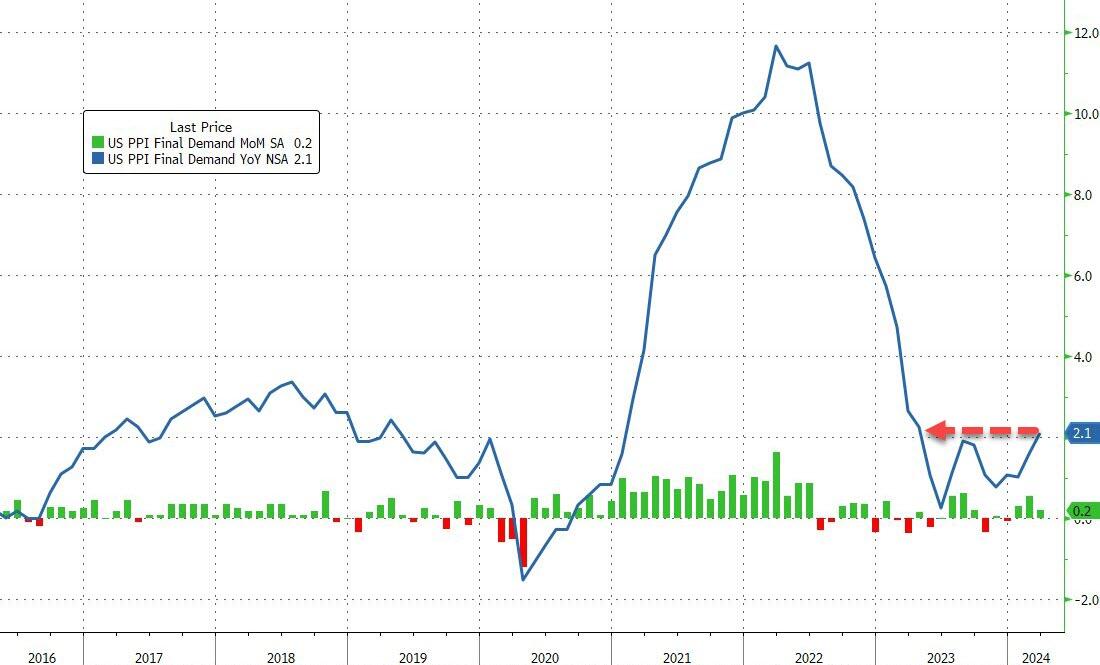

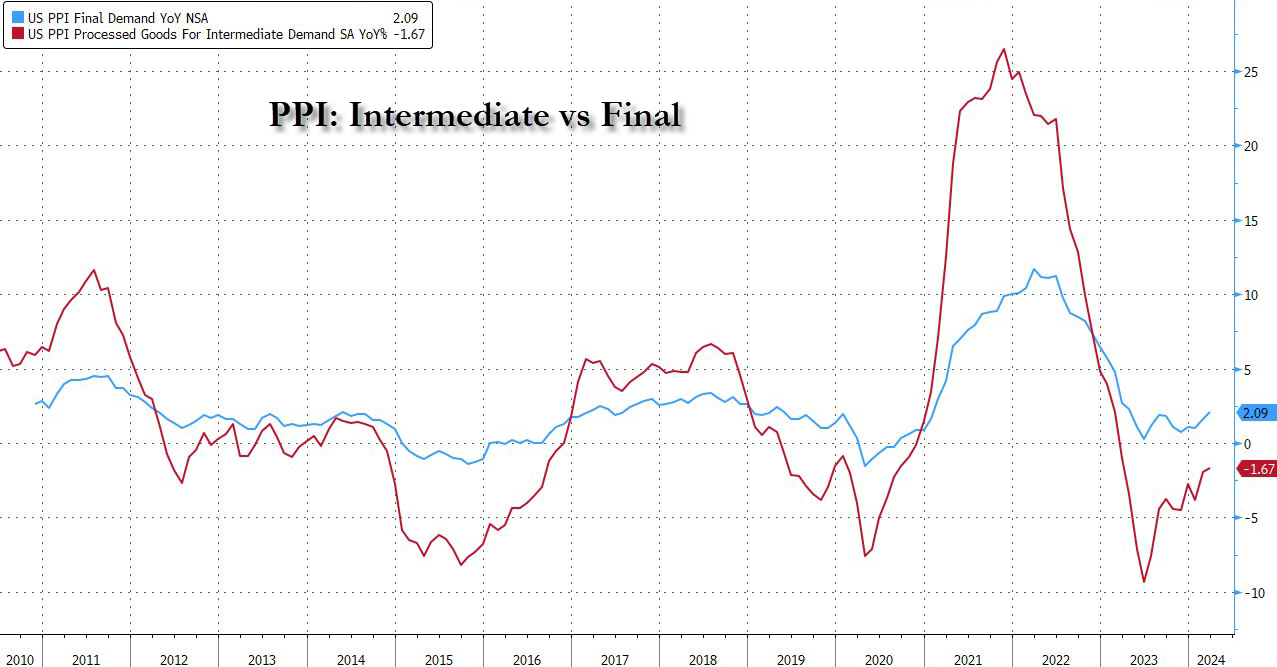

On top of skyroceting budget deficits, we have Producer Prices rising at fastest pace in a year in March.

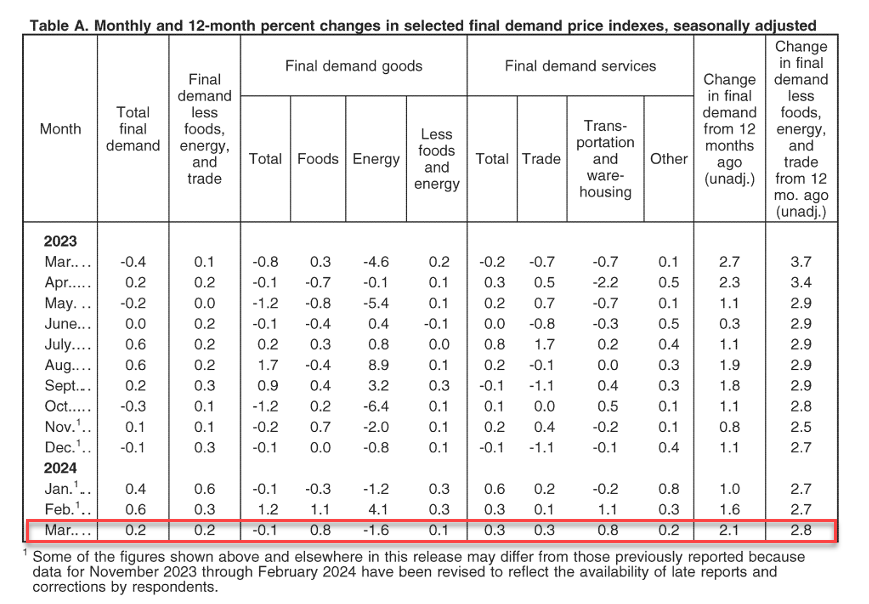

After yesterday’s CPI-surge, PPI followed along, with headline producer prices rising 0.2% MoM (+0.3% MoM exp), pushing the YoY PPI to +2.1% (+2.2% exp) from +1.6% – the highest since April 2023…

Source: Bloomberg

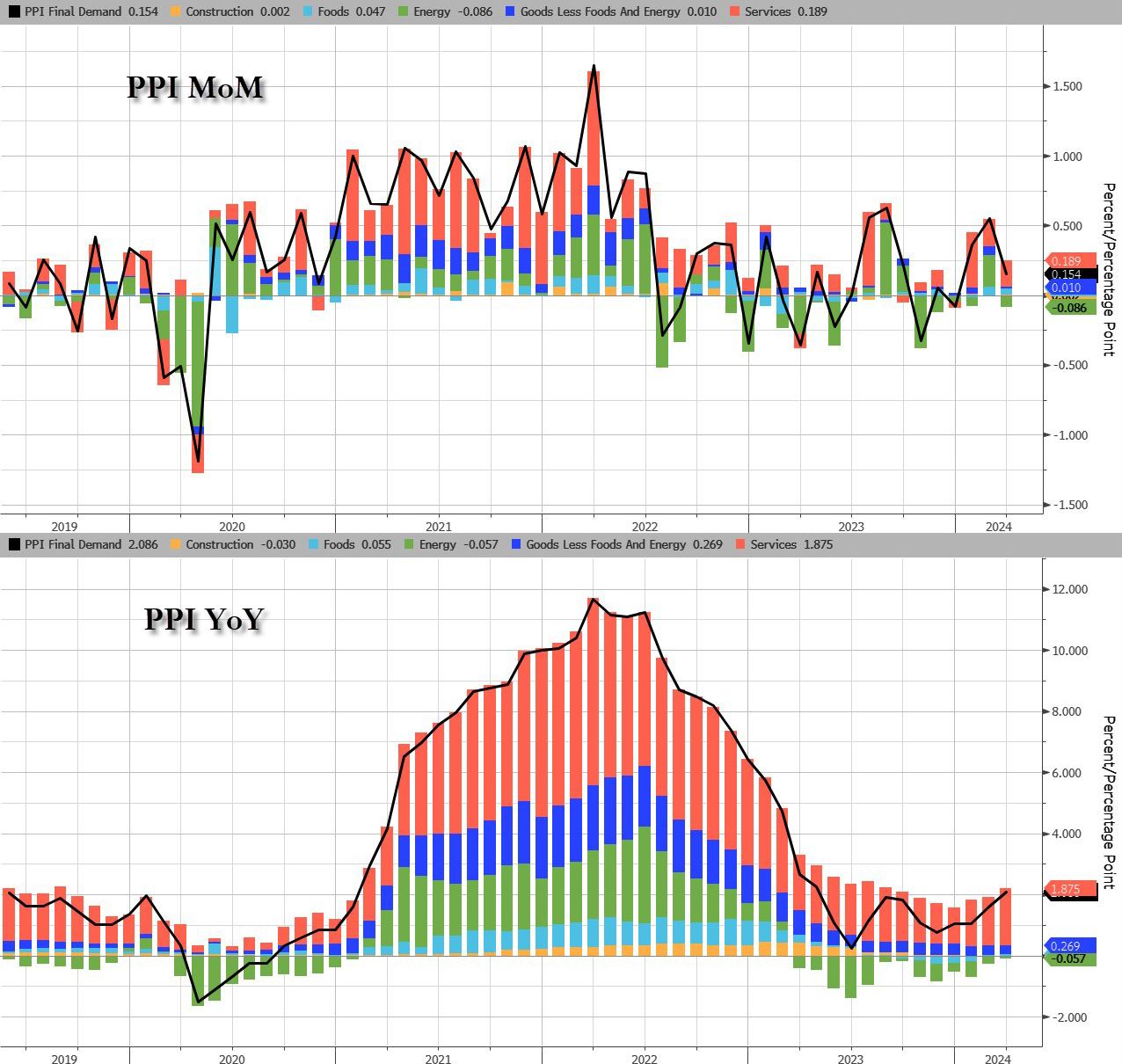

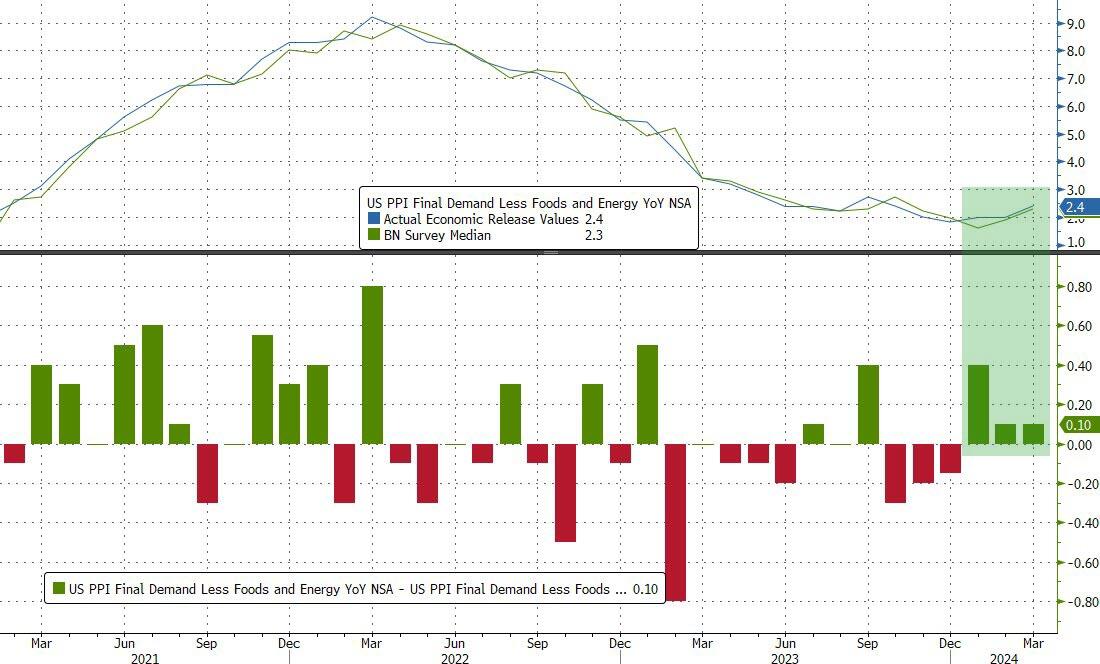

Core CPI rose 2.4% YoY (hotter than the expected 2.3%) – the third hotter-than-expected core PPI print in a row…

Under the hood, Services prices rose while goods prices declined MoM.

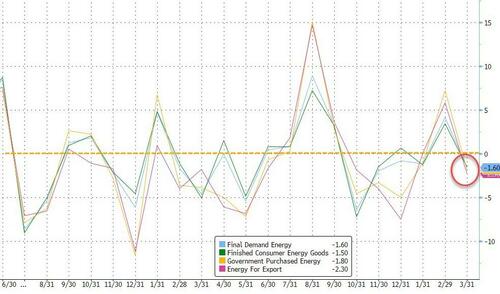

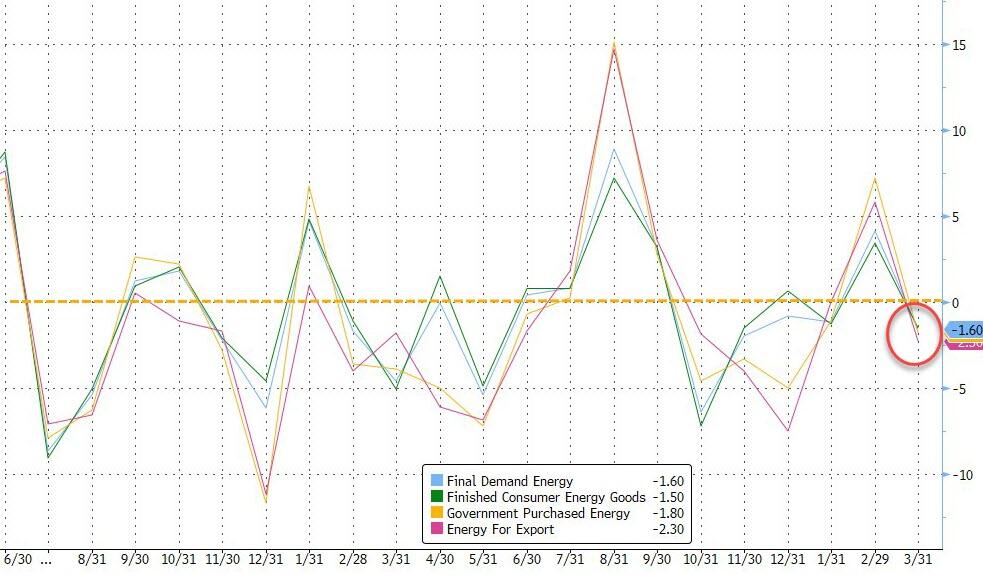

One thing that stands out as rather odd is the 1.6% MoM decline in Energy costs in the month… as prices soared for crude and gasoline?

Leading the March decline in the index for final demand goods, prices for gasoline decreased 3.6 percent…

And blame the markets for why the print was hot:

A major factor in the March increase in prices for final demand services was the index for securities brokerage, dealing, investment advice, and related services, which rose 3.1 percent.

And on a YoY basis, Services costs are accelerating…

Pressure continues to build in the inflation pipeline too…

While some may cling with grim hope to the ‘cooler than expected’ headline PPI print, core PPI is hot, damn hot, and headline PPI is rising. Not at all what The Fed, or Biden, wants to see – no matter how hard they spin it.

This is Victor Davis Hansen from Stanford’s Hoover Institute.

Mortgage applications increased 0.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 5, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 0.2 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 23 percent lower than the same week one year ago.

The Refinance Index increased 10 percent from the previous week and was 4 percent higher than the same week one year ago.

We are living in the USA where corruption, favoritism, open borders and an out-of-control Federal budget and debt are destroying this once great nation.

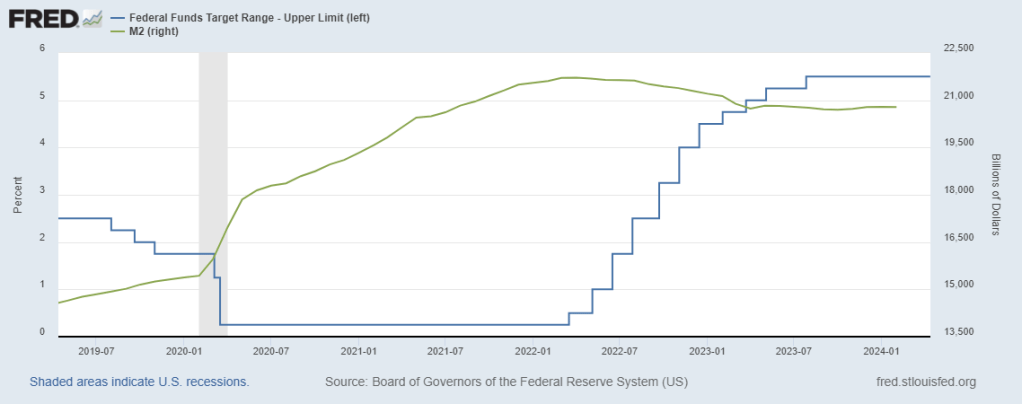

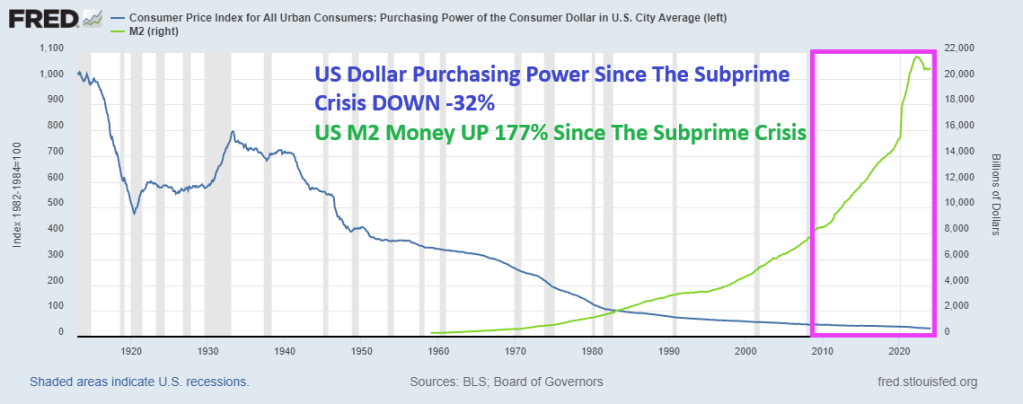

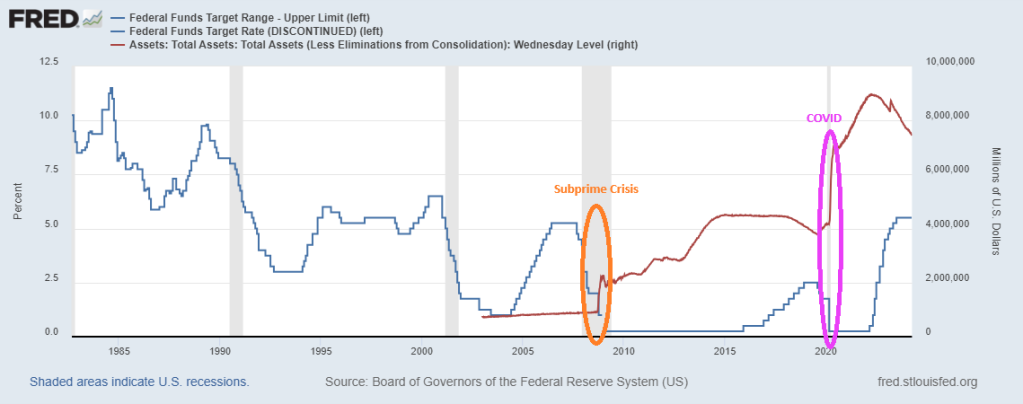

Former Kansas City Fed President Thomas M. Hoenig was absolutely right when he said recently that The Federal Reserve panders to Wall Street, Congress and special interest groups, prioritizing immediate relief over financial stability. Bernanke’s zero-interest rate policies (ZIRP) and Quantitative Easing (QE) were short-term fixes that never went away. Indeed, since the subprime mortgage crisis of 2008-2009, US Dollar purchasing power is DOWN -32% and M2 Money is up a staggering 177%. While Yellen stuck with zero-interest policies until Trump was elected, then raised The Fed Funds Target Rate 8 times. Yellen only raised the target rate once under Obama. Clearly playing political favoritism.

The Federal Reserve’s lack of transparency comes amidst reports that countries are removing their gold and other assets from the U.S. in the wake of the unprecedented Western sanctions imposed on Russia over its invasion of Ukraine. According to a 2023 Invesco survey, a “substantial percentage” of central banks expressed concern about how the U.S. and its allies froze nearly half of Russia’s $650 billion gold and forex reserves.Headline USA filed a FOIA request with the Fed for records reflecting how much gold the Federal Reserve Bank of New York currently holds in its vault, as well as records reflecting the ownership stake that each of FRBNY’s central bank/government clients have in that gold. The FOIA request also sought records about the Fed’s gold holdings prior to Russia’s February 2022 invasion of Ukraine. However, the Federal Reserve denied the FOIA request on Wednesday.

It influences the price of nearly everything, as well as the availability of jobs, the stability of our banking system, and the purchasing power of our money.

When the Fed Chair speaks, the entire world stops to listen.

But the average person has a poor understanding of how this colossally important entity operates. Or even why it exists.

And after a series of asset price bubbles — which some argue we’re in another one now — a chorus skeptical of the Fed’s actions has emerged.

So today we’re doing our best to shine as bright a light as possible on the Fed: how & why it operates, the good & as well as the shortcomings of its actions to date, what direction its policies are likely to take from here, and how all of this impacts the households of regular people like you and me.

Here are my top takeaways from from a speech by former KC Fed President Thomas Hoenig:

Dr Hoenig admits the Federal Reserve has experienced substantial “mission creep” since its creation as a lender of last resort. Its track record is very much “mixed” in terms of delivering on the intent of its policies. In Dr. Hoenig’s opinion, its efforts to add stability sometimes instead only create more instability.

While very critical of the Fed’s QE and ZIRP policies in the wake of the GFC, and more recently in the $trillions in monetary & fiscal stimulus unleashed post-COVID, Dr Hoenig thinks current Fed policy is “about right”. Though he expects the Fed to come under serious pressure soon as ebbing liquidity allows recessionary forces to build. He thinks the Fed will need to make an important decision within the coming year: return to QE and re-flame inflation, or allow a recession to occur.

Dr Hoenig criticizes the Federal Reserve for pandering to various interests, noting that short-term thinking and pressures from Wall Street, Congress, and interest groups often lead to decisions that prioritize immediate relief over long-term stability — a sort of “We’ll act now for optics sake and hopefully figure things out later”

In Dr Hoenig’s opinion, our fiscal policy is a runaway disaster. He criticizes both political parties of Congress for their roles in the cycle of ever-increasing deficits. Democrats advocate increased spending and tax hikes, while Republicans aim to keep taxes low but fail to curb spending. He warns of dire long-term consequences for future generations due to this impasse.

Dr Hoenig is very worried about the current stability of the banking system (and this from a former Direct of the FDIC!). He advocates for essential reforms to address government spending, prioritize essential areas without relying on future borrowed funds or inflationary measures, and communicate transparently with the public. He stresses the importance of reducing debt growth substantially below national income growth to avoid a full-blown crisis scenario in the future.

Dr Hoenig predicts the purchasing power of the US dollar (and other world fiat currencies) will continue to decline due to current policies and the lack of a “discipline” to money creation. Until such a discipline is restored (perhaps a return to some sort of hard backing of the currency), the dollar’s fall in purchasing power won’t abate.

Dr Hoenig suggests investing time in reading history and biographies as a valuable way to learn about leadership and gain insights into what strategies works and which don’t.

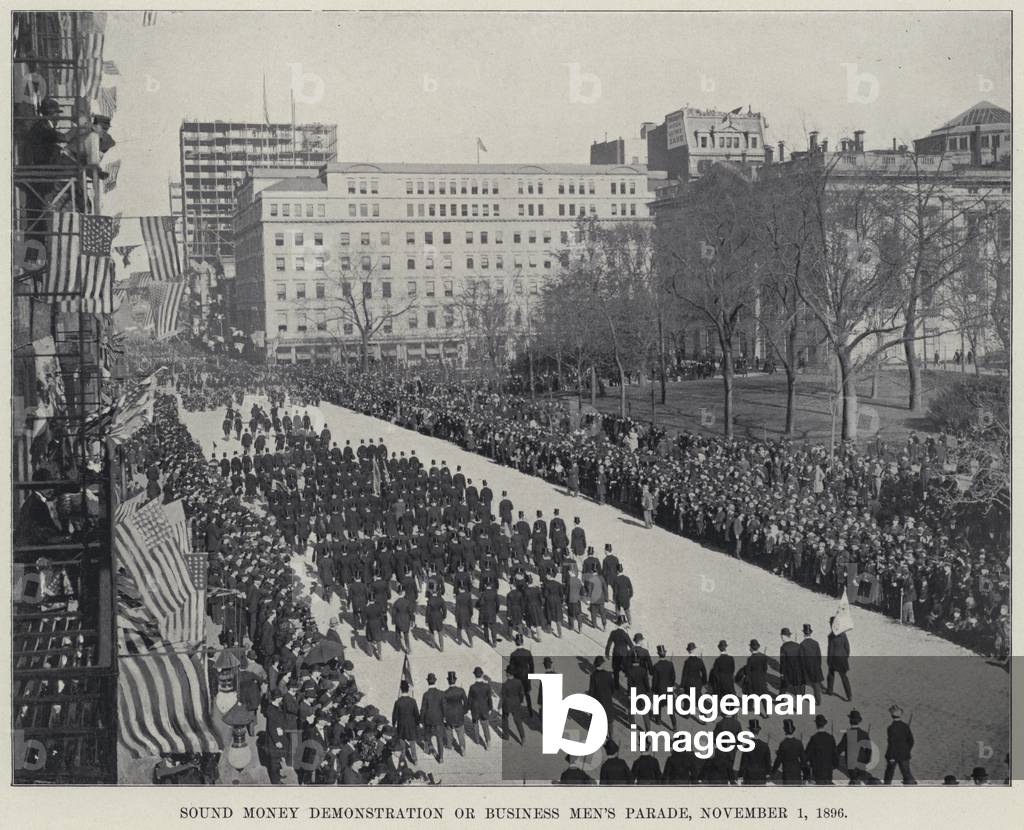

Here is the “Sound Money Parade” in 1896. By the aftermath of the subprime crisis, Janet Yellen (1993-2020) adopted the UNSOUND Money Fest, an orgy of printing and charging near zero interest rates. Powell in 2021 is ever-so-slowly unwinding The Fed’s balance sheet, but Powell has raised The Target Rate to its highest level since 1998 to fight inflation caused by Biden’s policies.

Combine The Fed not telling us how much gold they hold and their overprinting problems since 2008, and you can see why investors are turning to gold and silver and crypto currencies. The adoption of Central Bank Digital Currency (CBDC) is a step towards financial collapse.

Here is a parade you will NEVER see in Washington DC. A Sound Money Parade!

Powell is beginning to act like a sound money fan, but he still is taking his sweet time shriking the balance sheet.

I am thinking of fleeing to Lilliehammer Normay like Frank Tagliano.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.